Turkey Electric Vehicle Charging Station Market Size, Share, Trends and Forecast by Charging Station Type, Vehicle Type, Installation Type, Charging Level, Connector Type, Application, and Region, 2026-2034

Turkey Electric Vehicle Charging Station Market Size, Share, Trends & Forecast (2026-2034)

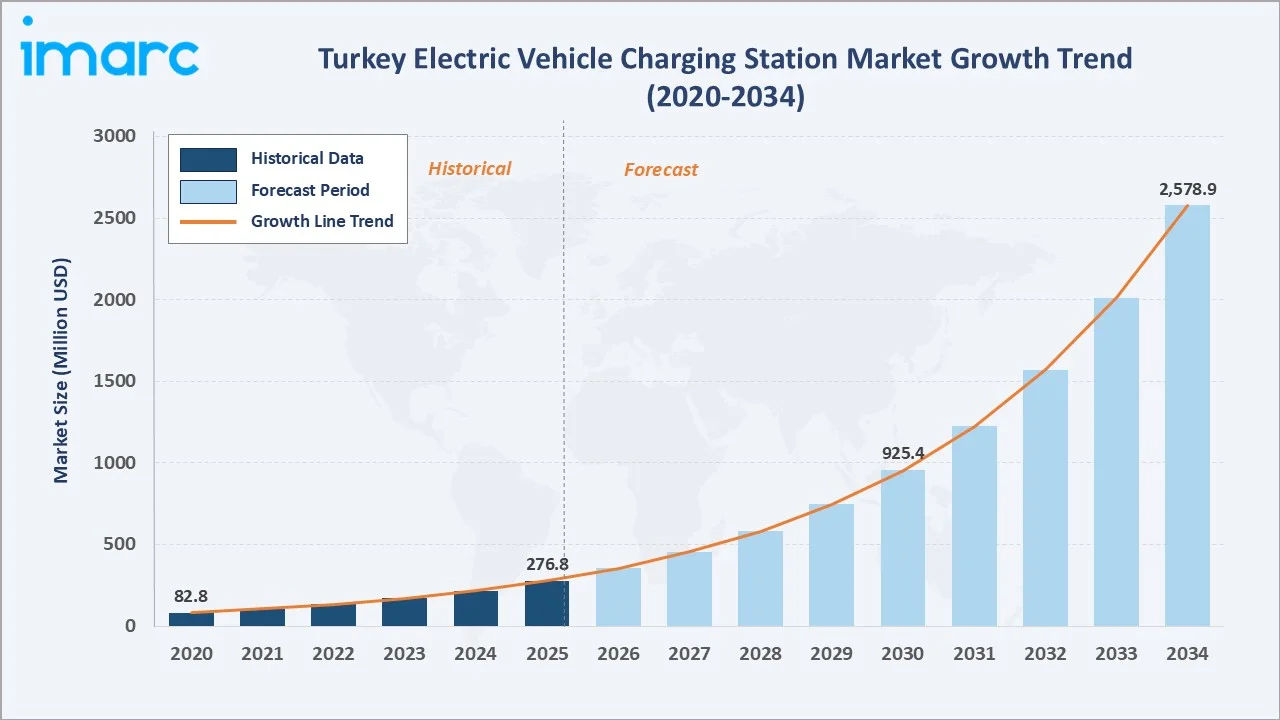

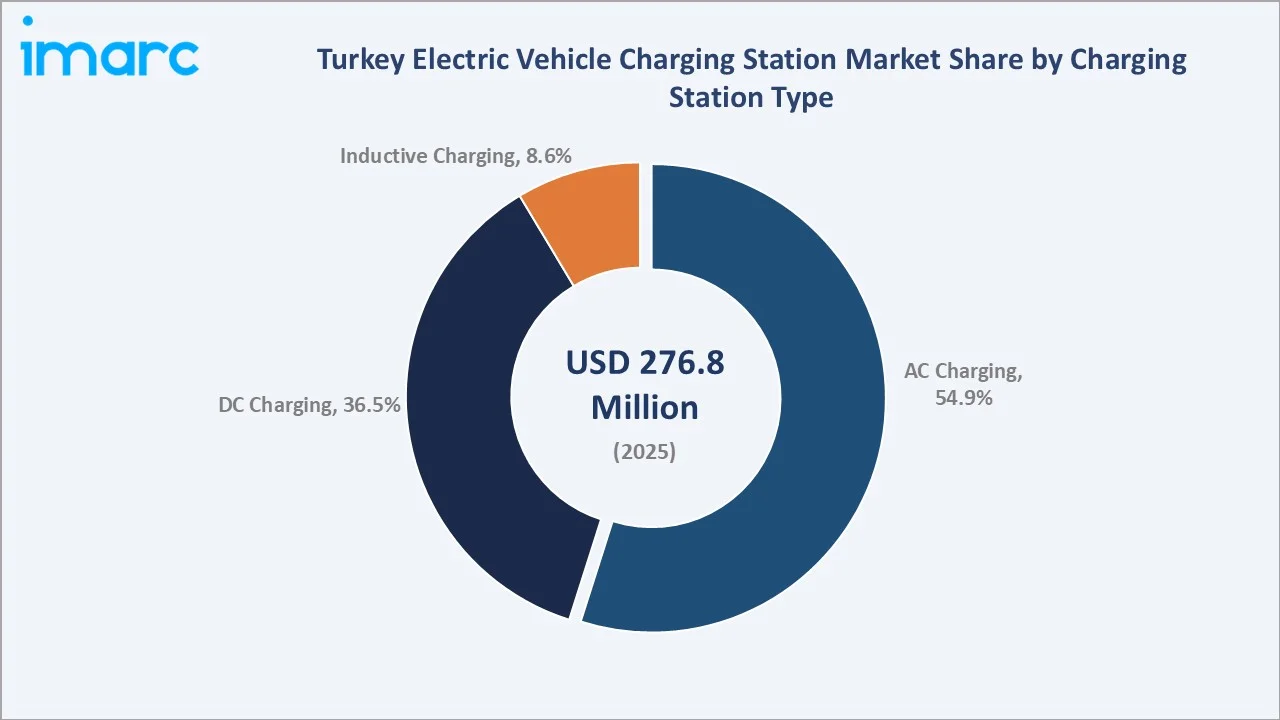

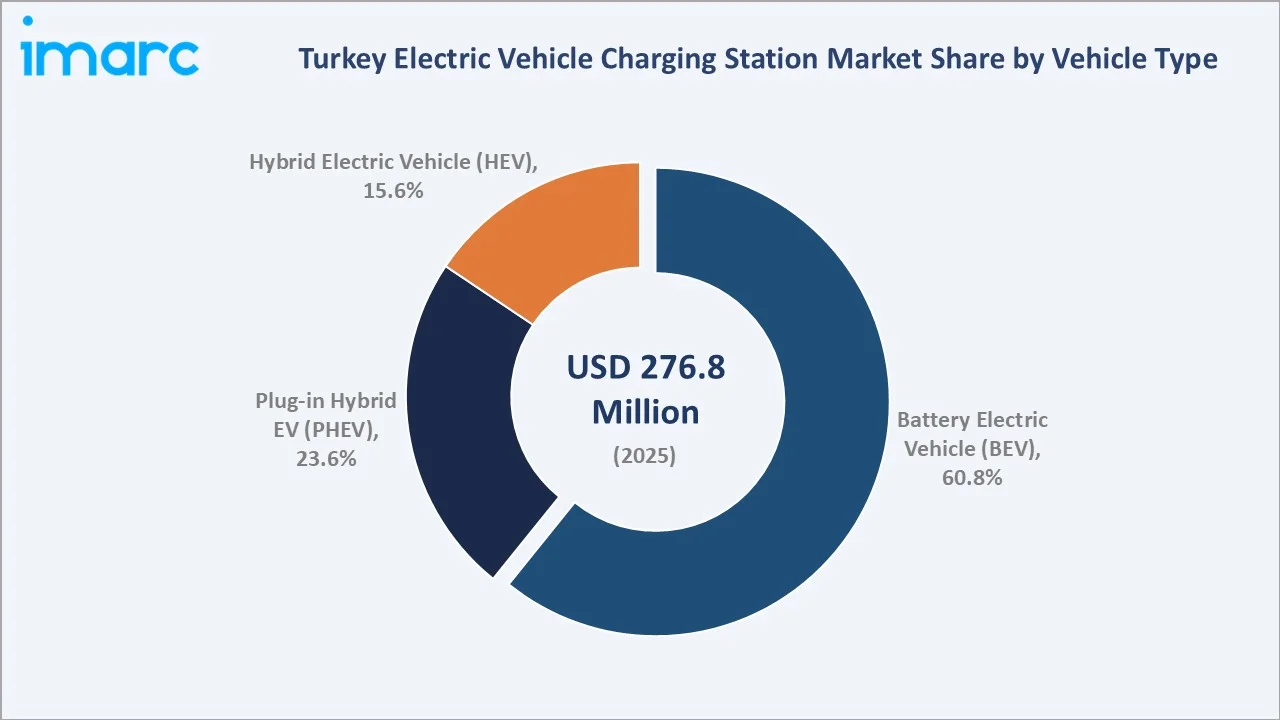

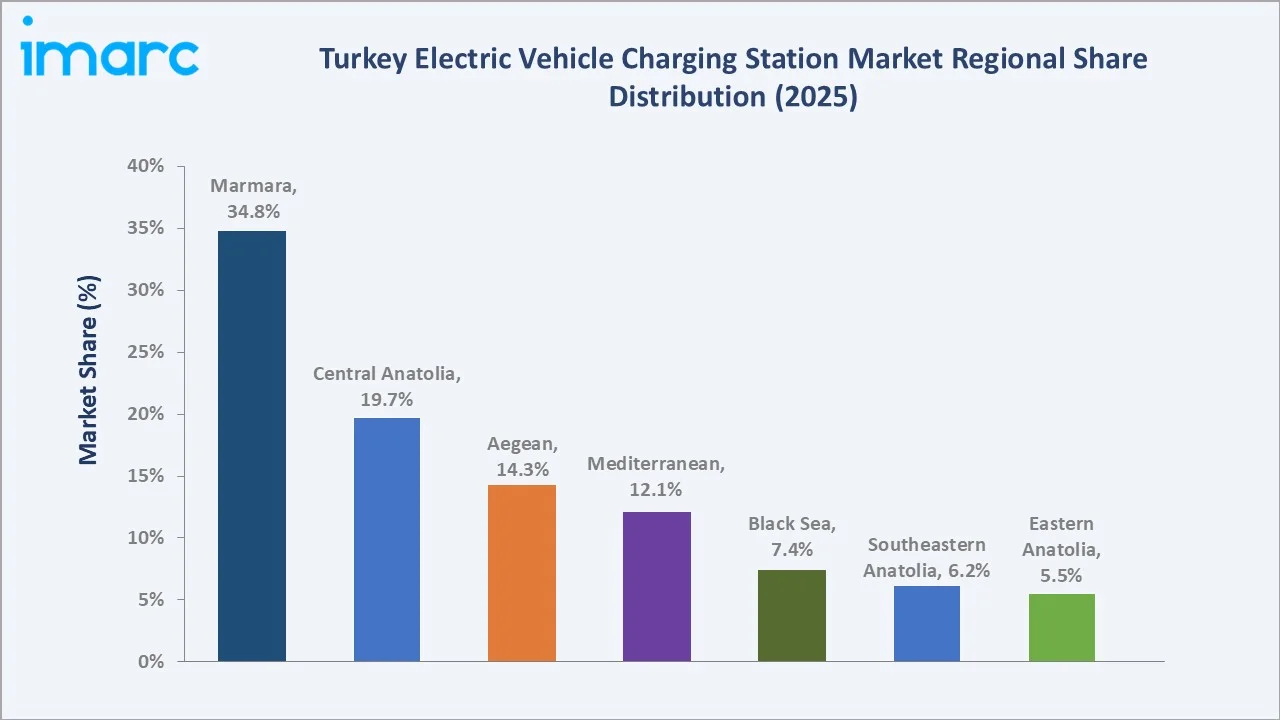

The Turkey electric vehicle charging station market reached USD 276.8 Million in 2025 and is projected to reach USD 2,578.9 Million by 2034, growing at a CAGR of 27.30% during 2026-2034. The market is driven by rising EV adoption, led by domestic EV production, supportive government policies, and expanding public charging infrastructure. Turkey projects around 1.3 million EVs and 142,000 charging points by 2030, rising further to 3.3 million EVs and 273,000 chargers by 2035. This strong long-term outlook is supporting the market by encouraging infrastructure investment, fast-charger deployment, and wider participation from utilities, automakers, and private charging operators. AC charging leads at 54.9%. Battery electric vehicle (BEV) leads vehicle type at 60.8%. Marmara leads regionally at 34.8%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 276.8 Million |

|

Forecast Market Size (2034) |

USD 2,578.9 Million |

|

CAGR (2026-2034) |

27.30% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Charging Station Type |

AC Charging (54.9%, 2025) |

|

Dominant Vehicle Type |

Battery Electric Vehicle - BEV (60.8%, 2025) |

|

Leading Region |

Marmara (34.8%, 2025) |

Turkey's EV charging station market expanded from USD 82.8 Million in 2020 to USD 276.8 Million in 2025, anchored at USD 925.4 Million in 2030, and forecast to reach USD 2,578.9 Million by 2034, reflecting rapid infrastructure deployment. This growth is supported by increasing EV adoption, government incentives, fast-charging network expansion, and investments by utilities and private charging operators.

To get more information on this market, Request Sample

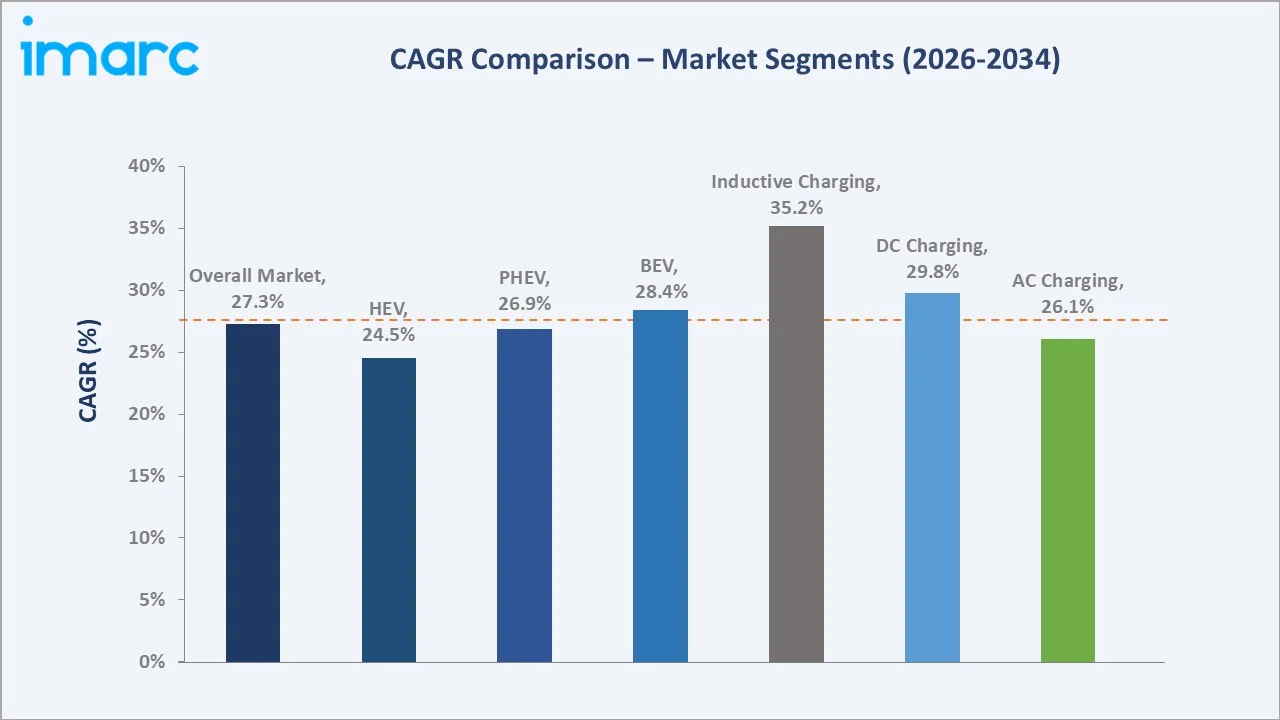

Inductive charging grows fastest at ~35.2% CAGR mainly linked to pilot deployments in fleet, bus, and depot applications. DC charging grows at ~29.8% CAGR through Turkey's highway and DC fast charger corridor development.

Executive Summary

Turkey EV charging station market reached USD 276.8 Million in 2025, supported by rising EV adoption, domestic EV production, and government-backed clean mobility initiatives. Increasing deployment of public, commercial, and highway fast-charging networks is strengthening market growth. Growing participation from utilities, automakers, and private charging operators is further improving charging accessibility across the country. The market is projected to reach USD 2,578.9 Million by 2034. AC charging at 54.9% leads through the national commercial and residential network. BEV at 60.8% leads through import BEV dominance. Marmara leads regionally at 34.8%.

Key Market Insights

|

Insight |

Data |

|

Dominant Charging Station Type |

AC Charging - 54.9% share (2025) |

|

Dominant Vehicle Type |

Battery Electric Vehicle (BEV) - 60.8% share (2025) |

|

Leading Region |

Marmara - 34.8% share (2025) |

|

Market Opportunity |

Highway DC fast charging corridor; Charging ecosystem expansion; Tourism route EVSE; Corporate fleet charging hub; Solar EV charging |

Key Analytical Observations Supporting The Above Data:

- AC Charging at 54.9%: The AC charging segment dominates due to its lower installation cost, easy deployment in homes, offices, malls, and parking areas, and suitability for routine overnight or destination charging.

- Battery Electric Vehicle (BEV) at 60.8%: The BEV segment dominates because fully electric vehicles require regular external charging, creating higher demand for public, residential, and workplace chargers.

- Marmara at 34.8%: Marmara dominates regionally due to its high urban population, strong vehicle ownership, and concentration of economic activity in cities. The region’s dense commercial centers, highways, and industrial corridors support faster charger deployment and higher utilization.

Turkey Electric Vehicle Charging Station Market Overview

Turkey EV charging station market operates within Turkey's broader automotive ecosystem as the fastest-growing market segment through EV adoption. The market's commercial uniqueness lies in the strong role of domestic EV adoption, led by Turkey’s homegrown EV manufacturer, Togg, which is accelerating demand for charging infrastructure. Additionally, the market is characterized by rapid private-sector investment in nationwide fast-charging networks and strategic deployment along major highways connecting urban and industrial centers.

Turkey's EV charging ecosystem integrates EVSE hardware importers, network operators, grid utilities, regulatory framework, and EV drivers and fleet end-users. Macroeconomic factors include rising urbanization, growing EV affordability, fuel price volatility, and government focus on reducing oil import dependence.

Market Dynamics

To evaluate market opportunities, Request Sample

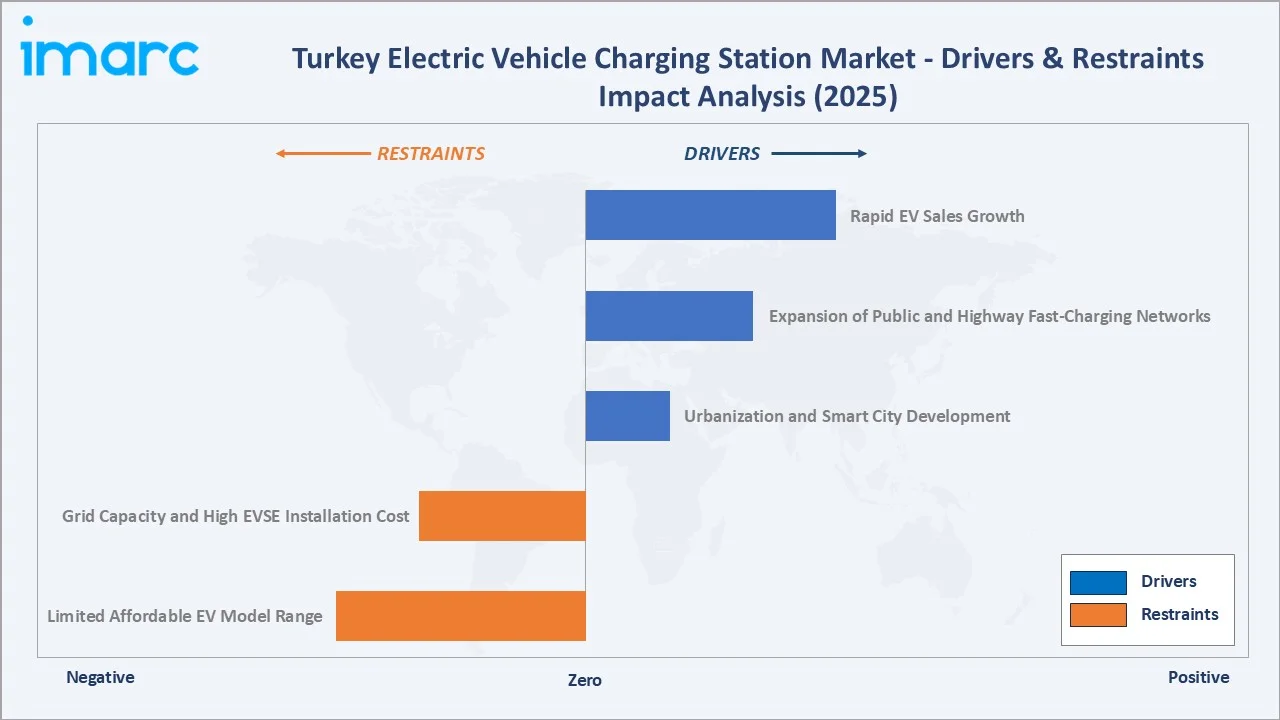

Market Drivers

- Rapid EV Sales Growth: In 2025, fully electric vehicles accounted for nearly 17% of new car sales in Turkey, bringing the country in line with the European Union’s overall EV sales share for the first time. With electric car sales reaching around 190,000 units, Turkey emerged as the fourth-largest electric vehicle market in Europe. These rapid EV sales increase the need for reliable public, residential, and workplace charging infrastructure. As more consumers shift toward BEVs and PHEVs, charging operators are expanding networks across cities, highways, malls, and commercial hubs. Rising EV ownership also improves charger utilization, making new projects more attractive for investors. This supports faster deployment of AC chargers and DC fast-charging stations across the country.

- Expansion of Public and Highway Fast-Charging Networks: The expansion of public and highway fast-charging networks improves charging accessibility for both urban and long-distance travel. Fast chargers along major transport corridors reduce charging times and alleviate range anxiety among EV users. Growing investments by charging operators, energy companies, and automakers are increasing network coverage across key cities and highways. This enhanced infrastructure is encouraging EV purchases and supporting the overall growth of the charging station market.

- Urbanization and Smart City Development: Urbanization and smart city development are increasing the demand for cleaner, connected, and efficient transport solutions in major cities. As cities expand, EV chargers are being integrated into malls, residential complexes, offices, parking areas, and public transport hubs. Smart city initiatives also support digital charging platforms, energy management, and grid-connected infrastructure. This improves charging accessibility and encourages wider EV adoption among urban users.

Market Restraints

- Grid Capacity and High EVSE Installation Cost: Grid capacity limitations are hampering the market because high-power EVSE, especially DC fast chargers, require stable and upgraded distribution infrastructure. In areas with weak grid availability, operators may need costly transformers, cabling, substations, and load management systems before installing chargers. High equipment and installation costs increase project CAPEX and extend payback periods. This makes deployment slower, particularly in smaller cities, rural areas, and highway corridors where charger utilization is still developing.

- Limited Affordable EV Model Range: Limited availability of affordable EV models is slowing mass-market EV adoption. When EV options remain expensive or concentrated in premium segments, the potential user base for charging stations grows more slowly. Lower EV penetration reduces charger utilization, making investments less attractive for operators. This can delay charging infrastructure expansion, especially in price-sensitive cities and emerging regional markets.

Market Opportunities

- Expansion of Superfast EV Charging Hubs: Expansion of superfast EV charging hubs, reducing charging time and improving convenience for EV users. These hubs can serve highways, city centers, shopping malls, airports, and fleet depots with high-power charging capacity. Faster charging supports long-distance travel and improves charger turnover, making stations more commercially viable. As EV adoption rises, superfast hubs can attract investments from energy companies, automakers, and charging operators.

- Integration of Charging Stations with Renewable Energy and Solar Power: Integration of charging stations with renewable energy and solar power reduces dependence on grid electricity and lowers operating costs. Solar-backed chargers can support sites in highways, commercial areas, and remote locations where grid capacity may be limited. This model also aligns with Turkey’s clean energy transition and emissions reduction goals. Combining EV charging with renewable power and battery storage can improve energy reliability and attract green infrastructure investments.

Market Challenges

- High Dependence on Imported Charging Equipment and Components: High dependence on imported charging equipment and components exposes operators to currency fluctuations, import duties, and global supply chain delays. Since chargers, power electronics, connectors, and software systems may rely on foreign suppliers, project costs can rise unexpectedly. This increases capital expenditure and makes investment planning less predictable. It can also delay installation timelines and slow the expansion of charging networks across the country.

- Long Payback Periods for Charging Infrastructure Investments: Long payback periods are challenging because charging infrastructure requires high upfront investment in equipment, grid connection, installation, and maintenance. In areas with low or developing EV adoption, charger utilization may remain limited, delaying revenue generation. This makes investors cautious, especially for highway and secondary-city locations. As a result, operators may prioritize high-traffic urban areas, slowing nationwide network expansion.

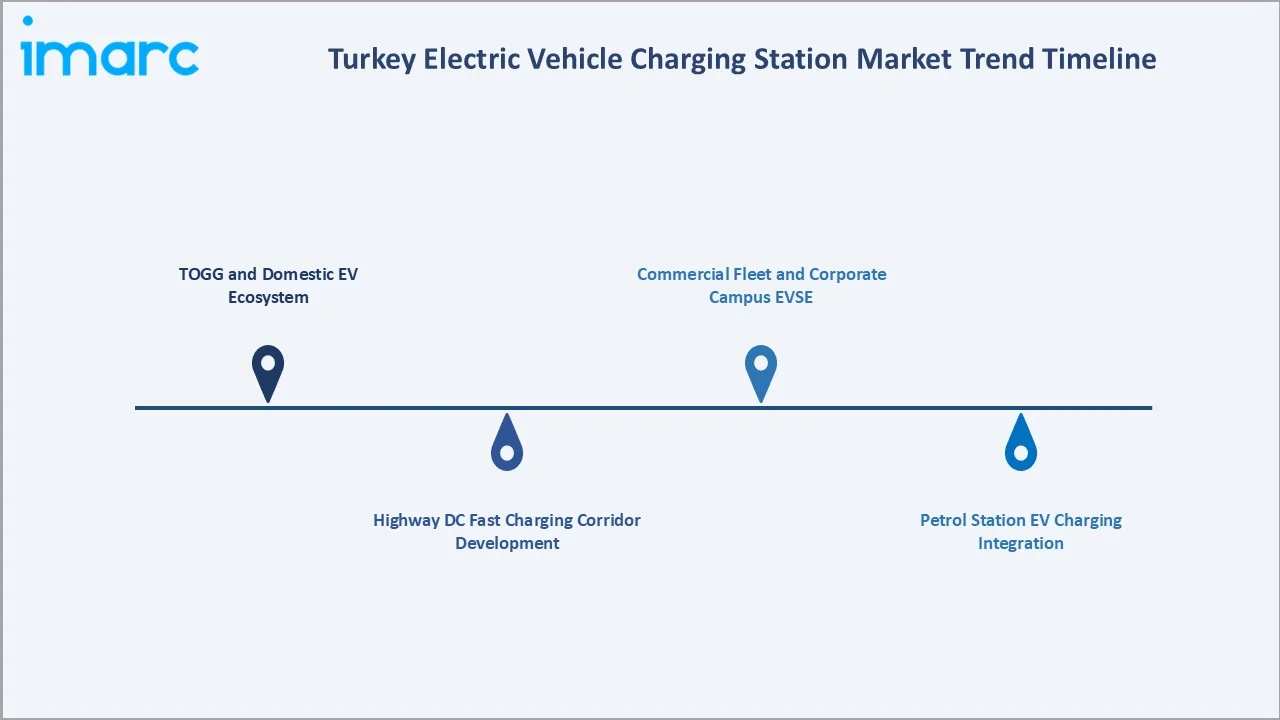

Emerging Market Trends

1. TOGG and Domestic EV Ecosystem

Togg produced around 40,000 vehicles in 2025. The company is targeting production of 60,000 units or more in 2026 and aims to manufacture 1 million vehicles across five segments by 2030. As TOGG expands vehicle production and sales, charging operators are increasing investments in public, residential, and highway charging networks. The growth of a domestic EV ecosystem is also encouraging collaboration among automakers, energy companies, technology providers, and charging operators. This integrated approach is strengthening Turkey’s EV value chain and supporting nationwide charging infrastructure development.

2. Highway DC Fast Charging Corridor Development

Highway DC fast-charging corridor development is emerging as operators expand charging infrastructure along major intercity routes and transport corridors. These networks enable long-distance EV travel by providing convenient access to high-power charging stations. The trend is helping reduce range anxiety and improving the practicality of EV ownership for both private users and commercial fleets. Growing investments from energy companies, charging operators, and government-backed initiatives are accelerating corridor development across the country.

3. Petrol Station EV Charging Integration

Petrol station EV charging integration is emerging as fuel retailers add chargers to existing forecourt networks. These sites already have strong highway access, parking spaces, retail facilities, and high vehicle footfall, making them suitable for fast-charging deployment. This model helps operators diversify beyond fuel sales while improving charging convenience for EV users. It also supports wider coverage across intercity routes and urban mobility corridors.

4. Commercial Fleet and Corporate Campus EVSE

Commercial fleet and corporate campus EVSE are emerging as companies electrify employee, logistics, and service vehicle fleets. Corporate offices, industrial parks, warehouses, and business campuses are installing dedicated chargers to support daily fleet operations. This reduces charging downtime, improves route reliability, and supports corporate sustainability targets. Rising fleet electrification is therefore creating steady demand for workplace, depot, and semi-public charging infrastructure.

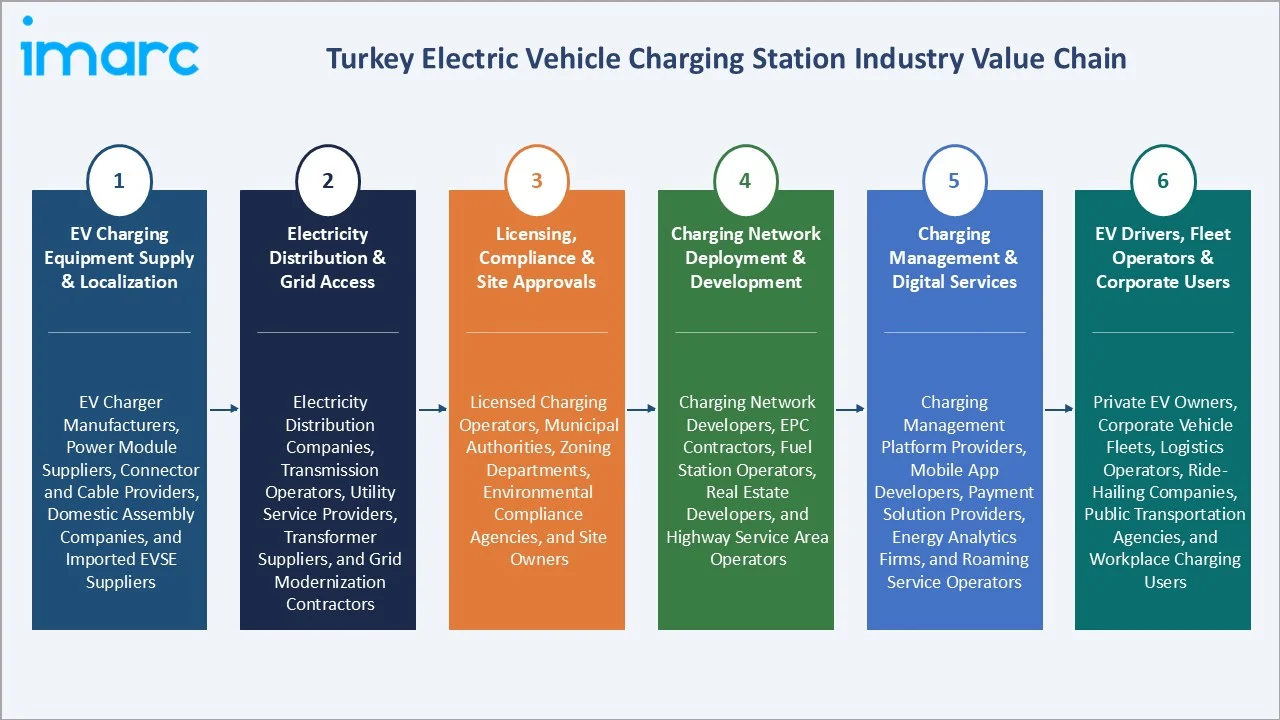

Industry Value Chain Analysis

Turkey EV charging station value chain integrates EV charging equipment supply & localization, electricity distribution & grid access, licensing, compliance & site approvals, charging network deployment & infrastructure development, charging management & digital services, and EV drivers, fleet operators & corporate users.

|

Stage |

Key Participants |

|

EV Charging Equipment Supply & Localization |

EV charger manufacturers, power module suppliers, connector and cable providers, domestic assembly companies, and imported EVSE suppliers |

|

Electricity Distribution & Grid Access |

Electricity distribution companies, transmission operators, utility service providers, transformer suppliers, and grid modernization contractors |

|

Licensing, Compliance & Site Approvals |

Licensed charging operators, municipal authorities, zoning departments, environmental compliance agencies, and site owners |

|

Charging Network Deployment & Infrastructure Development |

Charging network developers, EPC contractors, fuel station operators, real estate developers, and highway service area operators |

|

Charging Management & Digital Services |

Charging management platform providers, mobile app developers, payment solution providers, energy analytics firms, and roaming service operators |

|

EV Drivers, Fleet Operators & Corporate Users |

Private EV owners, corporate vehicle fleets, logistics operators, ride-hailing companies, public transportation agencies, and workplace charging users |

Charging network deployment & infrastructure development is the most critical stage in Turkey's EV charging station value chain because it directly determines the availability, accessibility, and coverage of charging infrastructure. Investments in highway corridors, fuel stations, commercial properties, and urban charging locations are essential for supporting the country's rapidly growing EV fleet.

Technology Landscape in the Turkey Electric Vehicle Charging Station Industry

Mobile App-Based Charging and Payment Platforms

Mobile app-based charging and payment platforms enable users to locate nearby chargers, check availability, start charging sessions, and make digital payments through a single interface. These platforms improve user convenience through features such as real-time monitoring, route planning, charger reservations, and charging history tracking. For operators, they provide valuable data on charger utilization, customer behavior, and network performance. As Turkey’s charging network expands, mobile applications are becoming essential for delivering a seamless and connected charging experience.

Plug-and-Charge Technology

Plug-and-charge technology allows EVs to automatically authenticate and initiate charging when connected, eliminating the need for RFID cards, mobile apps, or manual payment steps. This enhances user convenience and reduces charging session time. The technology relies on secure communication between the vehicle and charging station, improving interoperability and customer experience. As Turkey’s EV ecosystem matures, plug-and-charge solutions are expected to support faster adoption of public and highway charging networks.

Off-Grid Electric Vehicle Charging Infrastructure Technology

Off-grid electric vehicle charging infrastructure technology enabling EV charging in locations where grid connectivity is limited or costly. These systems often combine solar power, battery energy storage, and smart energy management to provide reliable charging services. In May 2026, Savvy Charging Technologies and EV Bee entered a strategic partnership to accelerate the rollout of off-grid EV charging infrastructure across Turkey, the Middle East, and other international markets. EV Bee’s expertise in vehicle-to-vehicle charging, combined with Savvy’s charging solutions, supports the development of flexible and grid-independent charging models. This supports Turkey’s technology landscape by promoting off-grid charging systems that can serve highways, remote areas, and locations with limited grid access.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Charging Station Type |

AC Charging |

54.9% |

2025 |

|

Vehicle Type |

Battery Electric Vehicle (BEV) |

60.8% |

2025 |

|

Installation Type |

🔒 |

🔒 |

2025 |

|

Charging Level |

🔒 |

🔒 |

2025 |

|

Connector Type |

🔒 |

🔒 |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

Region |

Marmara |

34.8% |

2025 |

By Charging Station Type

AC charging leads at 54.9% (2025). Turkey's AC charging encompasses residential 7.4kW-11kW for home garages, commercial 22kW three-phase at shopping malls, hotels, and corporate campuses, and public Level 2 above 10kW at urban parking, creating an urban residential and commercial Level 2 dominant charging type.

To access detailed market analysis, Request Sample

DC charging at 36.5% grows at ~29.8% CAGR through the highway corridor and fleet depot. Inductive charging at 8.6% grows fastest at ~35.2% CAGR through TOGG wireless pilot, electric bus terminus, and fleet depot wireless adoption.

By Vehicle Type

Battery electric vehicles (BEVs) lead at 60.8% (2025), as they rely entirely on external charging infrastructure for operation, unlike hybrid vehicles that can use conventional fuels. Rising BEV adoption, supported by longer driving ranges, lower operating costs, and government incentives, is driving greater demand for public, residential, and fast-charging networks.

Plug-in hybrid electric vehicle (PHEV) at 23.6% serves corporate fleet and private import PHEV, creating corporate PHEV charging demand. Hybrid electric vehicle (HEV) at 15.6% supports market growth by increasing consumer familiarity with electrified mobility and creating a transition path toward full EV adoption.

Regional Market Insights

|

Region |

Share (2025) |

Key Turkey EV Charging Station Market Drivers & Characteristics |

|

Marmara |

34.8% |

Supported by its high population density, strong vehicle ownership, concentration of economic activity, and extensive deployment of public and commercial charging infrastructure across major urban centers. |

|

Central Anatolia |

19.7% |

Driven by increasing EV adoption, growing workplace charging installations, and expanding intercity charging networks. |

|

Aegean |

14.3% |

Driven by rising EV ownership, strong tourism activity, increasing investments in destination charging, and the expansion of charging infrastructure in urban and coastal areas. |

|

Mediterranean |

12.1% |

Supported by growing demand for EV charging in tourism centers, logistics corridors, and commercial districts, and supported by expanding public and private charging networks. |

|

Black Sea |

7.4% |

Supported by gradual EV adoption, improving charging accessibility along regional transport routes, and increasing investment in public charging infrastructure. |

|

Southeastern Anatolia |

6.2% |

Anchored by urban development, improving transportation infrastructure, and the gradual expansion of charging stations in key metropolitan and commercial areas. |

|

Eastern Anatolia |

5.5% |

Supported by growing awareness of electric mobility, expanding highway charging coverage, and government efforts to improve regional connectivity. |

Marmara's 34.8% supported by high population density, strong vehicle ownership, and extensive public and commercial charging deployment. Central Anatolia's 19.7% driven by Ankara’s role as an administrative and business hub and expanding intercity charging networks.

Aegean’s 14.3% and Mediterranean's 12.1% benefit from tourism activity, coastal mobility, and rising destination charging demand. Black Sea's 7.4%, Southeastern Anatolia's 6.2%, and Eastern Anatolia's 5.5% supported by gradual EV adoption, improving road connectivity, and growing public charging investments.

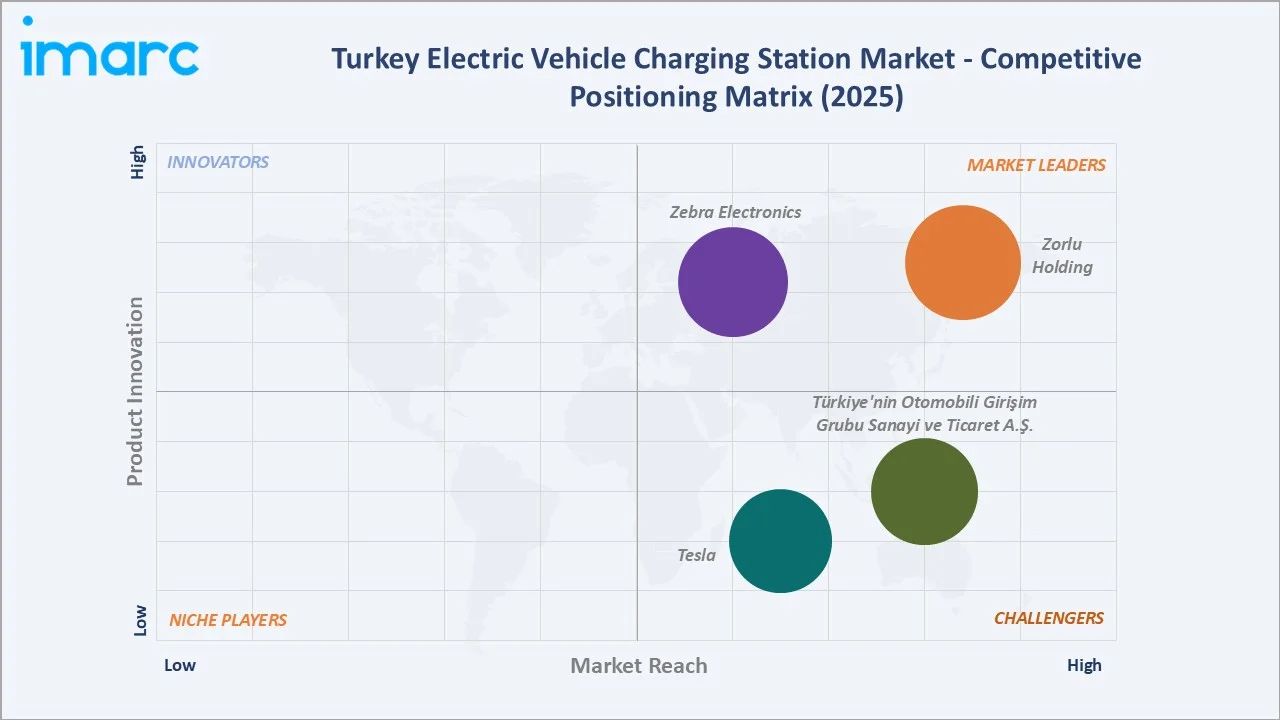

Competitive Landscape

Turkey EV charging station competitive landscape is commercially stratified between energy-company-integrated national CPO, domestic pure-play startup, domestic OEM charging, multinational fuel station CPO, premium international CPO, and international EVSE hardware supplier.

|

Company |

Key Products |

Market Position |

Core Strength |

|

|

AC 22 kW, 60 kW Dual Socket, 60 kW Single Socket, HPC 180kW, HPC 240 kW, HPC 400kW, HPC 720 kW |

Market Leader |

Zorlu Holding plays a pivotal, dual role in Turkey’s electric vehicle (EV) charging sector, acting as both a major charging network operator and a manufacturer of charging infrastructure. |

|

|

Individual User, Residential Complex / Residence, Parking Lot, Car Dealership |

Market Leader |

Zebra Electronics, through its Voltrun Enerji A.Ş, plays a significant role in electric vehicle (EV) charging in Turkey. |

|

|

Trugo |

Strong Challenger |

Türkiye'nin Otomobili Girişim Grubu Sanayi ve Ticaret A.Ş. (Togg), through its Trugo, plays a strategic, foundational role in the widespread adoption of electric vehicles (EVs) in Turkey by building a high-speed, nationwide charging network. |

|

|

Charging, Home Charging, Supercharging, Wall Connector for Business, Supercharger for Business |

Strong Challenger |

Tesla plays a pivotal role in Turkey’s EV charging landscape by deploying high-speed Supercharger stations along major highways, accelerating infrastructure growth, and opening its network to non-Tesla vehicles. |

Turkey EV charging station competitive landscape is evolving through TOGG ecosystem integration, petrol station network integration, and domestic currency-EVSE business model innovation.

Key Company Profiles

Zorlu Holding

Zorlu Holding is one of Turkey’s largest diversified conglomerates, with a significant presence in the energy sector through its subsidiary, Zorlu Enerji. The company provides nationwide charging services through an extensive network of AC, DC, and high-power charging stations deployed across urban centers, highways, commercial properties, and public locations.

- Key Products: AC 22 kW, 60 kW Dual Socket, 60 kW Single Socket, HPC 180kW, HPC 240 kW, HPC 400kW, HPC 720 kW.

- Strategic Focus: Expanding Turkey’s nationwide EV charging infrastructure by increasing the deployment of AC, DC, and ultra-fast charging stations across urban centers, highways, commercial properties, and tourism destinations.

Türkiye'nin Otomobili Girişim Grubu Sanayi ve Ticaret A.Ş.

Türkiye'nin Otomobili Girişim Grubu Sanayi ve Ticaret A.Ş. is Turkey’s leading domestic electric vehicle manufacturer and mobility technology company, established to develop a comprehensive EV ecosystem alongside its electric vehicle portfolio. Beyond vehicle production, TOGG plays a significant role in the EV charging station market through its wholly owned charging network product, Trugo, which provides high-speed charging services across Turkey.

- Key Products: Trugo.

- Strategic Focus: Expanding high-speed DC charging infrastructure across highways, urban centers, and key commercial locations.

Market Concentration Analysis

The Turkey EV charging station market exhibits a moderately concentrated competitive structure, led by a few major domestic and energy-backed operators. These companies benefit from extensive charging networks, strong financial backing, and nationwide expansion strategies. Competition is increasingly focused on ultra-fast charging deployment, highway corridor coverage, digital charging platforms, and service reliability. Energy companies and fuel retailers are also entering the market, intensifying competition and accelerating infrastructure rollout. Despite the presence of leading players, the market still offers opportunities for regional operators and technology providers due to the rapidly growing EV fleet. Strategic partnerships, network expansion, and investments in high-power charging infrastructure are expected to further shape market concentration over the coming years.

Investment & Growth Opportunities

Highest Growth Segments

Inductive charging (~35.2% CAGR), DC charging (~29.8% CAGR), BEV (~28.4% CAGR through TOGG scale-up), solar-EV integrated hub (~30-35% CAGR), corporate fleet campus EVSE (~25-28% CAGR), and tourism EVSE (~22-25% CAGR through resort hotel investment) represent Turkey's highest-growth EV charging investment vectors through 2034.

Investment Themes

TEM and O-1 highway DC fast-charging corridor investment: TEM and O-1 highway DC fast-charging corridor investment, improving charging access on key intercity and urban transport routes. These corridors connect major economic hubs, helping reduce range anxiety for long-distance EV users. Deployment of DC fast chargers along these highways enables faster charging stops and higher vehicle turnover. This investment also supports fleet mobility, tourism travel, and nationwide EV adoption.

Future Market Outlook (2026-2034)

Turkey EV charging station market is projected to grow from USD 276.8 Million in 2025 to USD 2,578.9 Million by 2034, delivering a 27.30% CAGR over the forecast period, driven by TOGG's domestic EV production scale-up, import BEV proliferation, and highway DC fast charger corridor completion. The market's anchor value of USD 925.4 Million in 2030 represents Turkey's EV charging at a commercial inflection.

Three structural forces define Turkey's EV charging growth through 2034: first, the rapid expansion of the domestic EV ecosystem, led by TOGG and increasing EV adoption, will drive sustained demand for charging infrastructure. Second, large-scale investments in public, highway, and ultra-fast charging networks will improve nationwide accessibility and support long-distance travel. Third, government decarbonization goals, renewable energy integration, and smart mobility initiatives will encourage continued investment in advanced charging technologies and network expansion.

Research Methodology

Primary Research

Primary research comprised interviews and discussions with EV charging operators, utilities, EV manufacturers, fleet operators, industry experts, and technology providers across Turkey. These interactions helped validate market trends, infrastructure deployment plans, investment priorities, and future growth opportunities in the EV charging ecosystem.

Secondary Research

Secondary research encompassed company websites, annual reports, press releases, government publications, regulatory sources, EV policy documents, and industry association databases. It also included reviews of charging network updates, market reports, news articles, and technology publications to assess market trends, competitive landscape, infrastructure growth, and outlook.

Forecasting Models

Market revenue forecasts developed using EV fleet EVSE penetration model: Turkey new EV registrations by vehicle type multiplied by EVSE-to-EV ratio multiplied by average EVSE installed cost and lifecycle by type and replacement rate.

Turkey Electric Vehicle Charging Station Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Charging Station Types Covered | AC charging, DC charging, Inductive charging |

| Vehicle Type Covered | Battery electric vehicle (BEV), Plug-in hybrid electric vehicle (PHEV), Hybrid electric vehicle (HEV) |

| Installations Covered | Portable charger, Fixed charger |

| Levels Covered | Level 1, Level 2, Level 3 |

| Connector Types Covered | Combined charging station (CCS), CHAdeMO, Normal charging, Tesla Supercharger, Type-2 (IEC 621196), Others |

| Applications Covered | Residential, Commercial |

| Regions Covered | Marmara, Central Anatolia, Mediterranean, Aegean, Southeastern Anatolia, Black Sea, Eastern Anatolia |

| Companies Covered | Zorlu Holding, Zebra Electronics, Türkiye'nin Otomobili Girişim Grubu Sanayi ve Ticaret A.Ş., Tesla, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Turkey electric vehicle charging station market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Turkey electric vehicle charging station market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Turkey electric vehicle charging station industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Turkey Electric Vehicle Charging Station Market Report

The Turkey EV charging station market reached USD 276.8 Million in 2025, driven by rapid EV adoption, domestic EV production led by TOGG, and government support for clean mobility. Expanding public and highway fast-charging networks are improving accessibility and reducing range anxiety. Rising investments by energy companies, charging operators, and fuel retailers are further accelerating infrastructure deployment across urban centers and intercity corridors.

The Turkey EV charging station market grows at 27.30% CAGR during 2026-2034, reaching USD 2,578.9 Million by 2034. The overall CAGR reflects TOGG's domestic EV production scale-up, government incentives, and BEV fleet multiplication.

AC charging leads at 54.9%, driven by its lower installation cost, ease of deployment, and suitability for homes, workplaces, malls, hotels, and parking areas. Its compatibility with routine overnight and destination charging makes it the most widely adopted charging option in Turkey.

BEV leads at 60.8%, driven by rising adoption of fully electric vehicles, which depend entirely on external charging infrastructure. Growing availability of BEV models, improved driving range, and lower operating costs are increasing demand for public, residential, and fast-charging stations.

Marmara region leads at 34.8%, driven by high EV ownership, dense urban population, and strong commercial activity. Its advanced road network, industrial base, and high traffic corridors support faster deployment and utilization of EV charging stations.

Leading companies include Zorlu Holding, Zebra Electronics, Türkiye'nin Otomobili Girişim Grubu Sanayi ve Ticaret A.Ş., and Tesla, among others.

The Turkey EV charging station market is projected to reach approximately USD 925.4 Million by 2030, with TOGG production and corporate fleet EV adoption.

Three priority investment opportunities: TEM and O-1 highway DC fast charging corridor, TOGG ecosystem smart charging hub, and tourism route EVSE.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)