Turkey EV Battery Market Size, Share, Trends and Forecast by Battery Type, Propulsion Type, Vehicle Type, and Region, 2026-2034

Turkey EV Battery Market Summary:

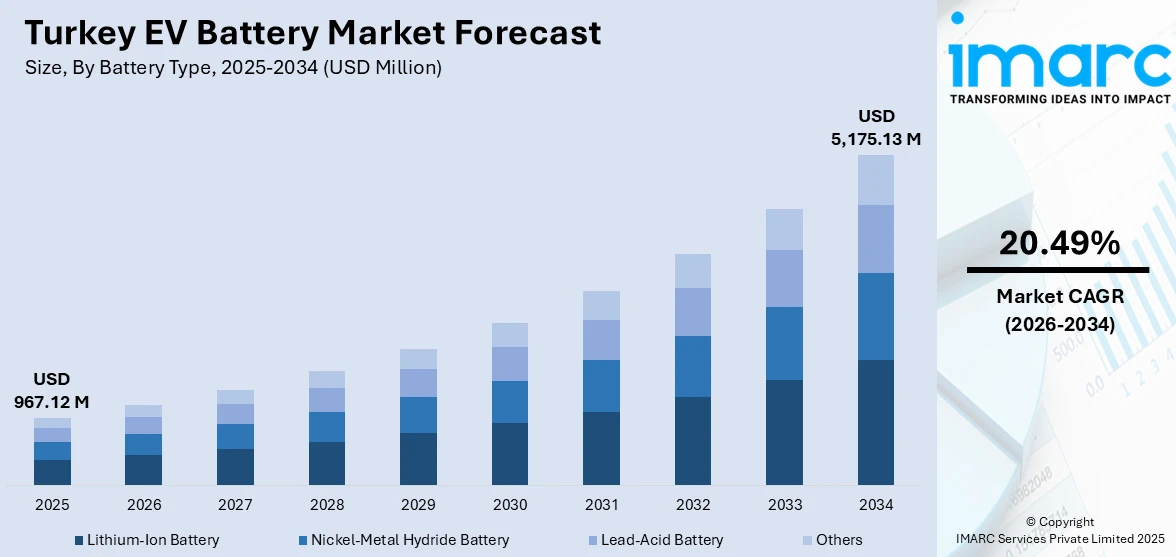

The Turkey EV battery market size was valued at USD 967.12 Million in 2025 and is projected to reach USD 5,175.13 Million by 2034, growing at a compound annual growth rate of 20.49% from 2026-2034.

The Turkey EV battery market demonstrates robust expansion, fueled by strategic government policies, domestic manufacturing initiatives, and growing EV adoption. The country is positioning itself as a regional production hub through joint ventures and foreign direct investments (FDIs) in battery technology. Favorable tax incentives, expanding charging infrastructure, and increasing consumer preferences for sustainable mobility solutions are accelerating market penetration across passenger and commercial vehicle segments.

Key Takeaways and Insights:

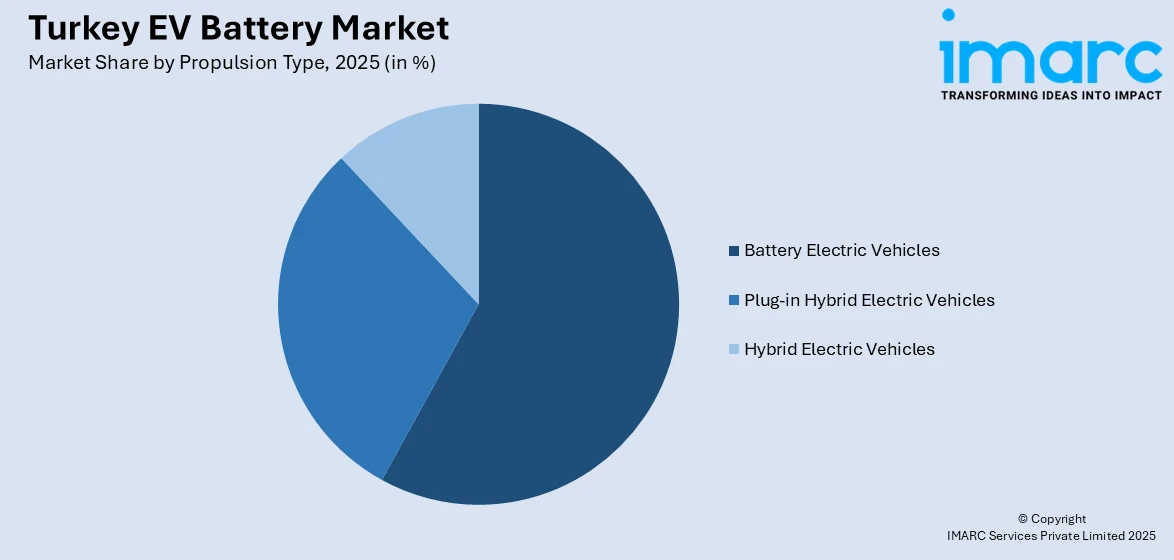

- By Propulsion Type: Battery electric vehicles dominate the market with a share of 57.7% in 2025, owing to favorable special consumption tax rates, expanding charging infrastructure, and growing consumer preferences for zero-emission mobility. Government incentives targeting lower-powered battery electric vehicles are fueling market expansion.

- By Vehicle Type: Passenger car leads the market with a share of 63.2% in 2025. This dominance is driven by domestic EV manufacturing initiatives, increasing model availability across price segments, and rising environmental consciousness among urban consumers seeking sustainable personal transportation solutions.

- By Region: Marmara represents the largest region with 42.1% share in 2025, driven by the concentration of automotive manufacturing facilities in Bursa and Kocaeli, superior charging infrastructure, and presence of major EV battery production facilities.

- Key Players: Key players drive the Turkey EV battery market by expanding local production capacities, establishing joint ventures with global technology partners, and investing in research and development (R&D) activities. Their focus on vertical integration, cost optimization, and strategic partnerships strengthens nationwide supply chains while ensuring consistent product availability across diverse vehicle segments.

To get more information on this market Request Sample

The Turkey EV battery market is witnessing transformative growth, driven by strategic industrial policies and substantial foreign investments. The government's High-Technology Investment Program (HIT-30) announced in July 2024 allocated USD 4.5 billion to accelerate battery and EV expansion, targeting one million EVs annually. The market benefits from Turkey's strategic geographic position, providing access to European markets while serving as a gateway to Middle Eastern and Central Asian markets. Robust domestic demand for EVs, supported by government incentives and subsidies, is fueling rapid adoption of EV batteries across passenger and commercial vehicle segments. Local manufacturers are collaborating with global battery technology leaders to enhance production capacity and technological capabilities. Expansion of lithium-ion battery gigafactories and associated supply chains is strengthening Turkey’s position as a regional EV hub. Additionally, growing focus on renewable energy integration is driving the development of stationary energy storage solutions, further diversifying EV battery applications.

Turkey EV Battery Market Trends:

Localization of Battery Manufacturing Capabilities

Turkey is rapidly establishing domestic battery production capabilities through strategic joint ventures and foreign investments. The establishment of Siro’s battery cell facility in Gemlik in 2023 represents a milestone in local manufacturing, employing advanced lithium-ion technology for battery modules and packs. Multiple battery manufacturing plants are being developed across Marmara, positioning Turkey as a regional production hub. This localization trend reduces dependency on imports, strengthens supply chain resilience, and enables competitive pricing for domestic EV manufacturers while creating export opportunities to European markets.

Expansion of Fast-Charging Infrastructure Networks

Turkey's EV charging infrastructure is experiencing exponential growth, addressing range anxiety concerns that previously hindered EV adoption. The Energy Market Regulatory Authority (EPDK) reported that Turkey had 11,949 EV charging stations, as of June 2025. Cutting-edge fast-charging systems are being implemented on highways and in urban areas, as operators launch high-capacity chargers that enable quick vehicle charging. This infrastructure buildout supports growing EV fleets and enhances consumer confidence in transitioning to electric mobility solutions.

Integration of Advanced Battery Technologies

Turkish battery manufacturers and their international partners are increasingly adopting advanced lithium-ion technologies, including lithium iron phosphate and nickel manganese cobalt chemistries. R&D centers are being established to support continuous innovation in battery performance, energy density, and longevity. The focus on developing energy storage solutions extends beyond automotive applications to include renewable energy integration and grid storage systems. This technological advancement trend strengthens Turkey's competitive position in the global battery supply chain ecosystem.

Market Outlook 2026-2034:

The outlook for the Turkey EV battery market is positive, driven by ambitious government plans, increasing manufacturing capacity, and a rapidly growing adoption rate for EVs. Strategic investments by leading global players are making Turkey a battery production giant in the region, with the potential for export to European and Middle Eastern markets. The market generated a revenue of USD 967.12 Million in 2025 and is projected to reach a revenue of USD 5,175.13 Million by 2034, growing at a compound annual growth rate of 20.49% from 2026-2034. A complete value chain ecosystem is being created by the combination of domestic automakers with international battery technology suppliers. Over the course of the projection period, strong market expansion is expected to be sustained by ongoing infrastructure development, supportive legislative frameworks, and growing consumer acceptance of electric mobility.

Turkey EV Battery Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Propulsion Type |

Battery Electric Vehicles |

57.7% |

|

Vehicle Type |

Passenger Car |

63.2% |

|

Region |

Marmara |

42.1% |

Battery Type Insights:

- Lithium-Ion Battery

- Nickel-Metal Hydride Battery

- Lead-Acid Battery

- Others

Lithium-ion battery is a notable battery type in the Turkey EV battery market, because of its high energy density, long cycle life, and lightweight properties that are much suitable for EVs. Heavy investments in domestic lithium-ion battery production and joint ventures with foreign technology partners are fueling the adoption. Increasing demand for passenger EVs, commercial EVs, and energy storage solutions is further propelling the swift growth and development of the segment.

Nickel-metal hydride battery holds a niche position in the Turkey EV battery market, mainly used in hybrid electric vehicles (HEVs). Its stability, safety, and moderate pricing make it a suitable choice for certain applications, where long-term durability is given more importance over high energy density. R&D activities in HEVs and their gradual acceptance in public transportation and fleet vehicles are sustaining the growth of this segment.

Lead-acid battery remains a cost-effective solution in the Turkey EV battery market, mainly used in two-wheelers, low-speed EVs, and backup power systems. Although it has lower energy density, the technology is appreciated for its strength, recyclability, and cost-effectiveness. The segment has the benefit of well-established production facilities and a stable demand base, ensuring reliable growth opportunities alongside other innovative battery technologies.

Propulsion Type Insights:

Access the comprehensive market breakdown Request Sample

- Battery Electric Vehicles

- Plug-in Hybrid Electric Vehicles

- Hybrid Electric Vehicles

Battery electric vehicles dominate with a market share of 57.7% of the total Turkey EV battery market in 2025.

Battery electric vehicles represent the primary propulsion type in the market in Turkey, benefiting from favorable special consumption taxes, which ensure significant price benefits compared to traditional cars. The local battery electric vehicle brand Togg recorded sales of 30,093 units in 2024, achieving considerable market share with its T10X model. The expansion of model ranges offered by local and global brands is further fueling the growth of the segment. Increasing consumer knowledge about long-term cost savings on fuel and maintenance is also bolstering the growth of the segment.

The battery electric vehicles segment in Turkey is benefiting from the overall development of charging infrastructure. Consumer demand for zero-emission vehicles is increasing, especially in urban areas where environmental issues are influencing consumer purchasing decisions. Several global brands are expanding their battery electric vehicle model ranges in Turkey, increasing competition and further fueling consumer choice across various price segments and vehicle types. Improved charging accessibility is reducing range anxiety and supporting wider adoption.

Vehicle Type Insights:

- Passenger Car

- Commercial Vehicles

- Two-Wheeler

Passenger car leads with a share of 63.2% of the total Turkey EV battery market in 2025.

Passenger car dominates the Turkey EV battery market, driven by growing consumer acceptance of electric mobility and expanding model availability across price segments. The passenger car segment benefits from favorable taxation policies that significantly reduce the total cost of ownership compared to conventional vehicles. Battery capacity requirements for passenger cars continue to increase, as manufacturers introduce longer-range models to address consumer expectations. The segment is expected to maintain leadership throughout the forecast period, as charging infrastructure expands and EV prices become increasingly competitive.

The growth of passenger car segment in the Turkey EV battery market is further supported by increasing investments in R&D activities, enabling manufacturers to offer more efficient and durable battery systems. Consumer interest in smart features, connectivity, and energy-efficient designs is driving differentiation among models. Collaborations between automakers, battery suppliers, and government agencies are accelerating infrastructure deployment and incentivizing adoption. As awareness about environmental benefits rises, passenger cars are emerging as the preferred choice for urban and suburban mobility, solidifying their dominance in the Turkish EV battery ecosystem.

Regional Insights:

- Marmara

- Central Anatolia

- Mediterranean

- Aegean

- Southeastern Anatolia

- Black Sea

- Eastern Anatolia

Marmara exhibits a clear dominance with a 42.1% share of the total Turkey EV battery market in 2025.

Marmara leads the Turkey EV battery market, benefiting from its concentration of automotive manufacturing facilities, major population centers, and superior charging infrastructure. Istanbul alone accounted for 7,641 EV charging points in 2024, representing the highest density nationwide. Major EV manufacturers operate production facilities in this region, creating an integrated ecosystem for battery supply and vehicle assembly. Government incentives and regional policies supporting EV adoption further strengthen Marmara’s position as the primary hub for electric mobility.

The region's strategic advantages extend to its proximity to European export markets and access to major port facilities in Gemlik and Kocaeli that facilitate international trade. The concentration of high-income consumers in Istanbul and surrounding metropolitan areas drives significant passenger EV adoption. Continued infrastructure investments and manufacturing expansion are expected to maintain the region's dominant market position throughout the forecast period. Additionally, partnerships between local universities and automotive companies are fostering innovation in battery technology and production efficiency.

Market Dynamics:

Growth Drivers:

Why is the Turkey EV Battery Market Growing?

Strategic Government Policies and Investment Incentives

The Turkish government has formulated holistic policies to promote the adoption of EVs and the local production of batteries. There are project-based investment incentives that offer tax relief, customs exemption, and land support for large-scale battery production investments. Such supportive policy environments have encouraged substantial FDI from international manufacturers interested in setting up production facilities in Turkey. The supportive policies are promoting local innovations in battery technology and the development of a strong local value chain. Public-private partnerships are improving technology transfer, human capacity building, and productivity. Thus, Turkey is emerging as a hotspot for advanced EV battery production and energy storage solutions. The local production capacity is expected to cater to the rising demand in the passenger and commercial EV markets.

Rapid Expansion of EV Charging Infrastructure

Turkey's charging infrastructure has experienced remarkable expansion, addressing a critical barrier to EV adoption and driving corresponding growth in battery demand. As per IMARC Group, the Turkey EV charging station market size reached USD 216.97 Million in 2024 and is projected to reach USD 2,480.65 Million by 2033. The increasing availability of fast-charging and ultra-fast charging stations across major cities and highways is supporting longer-range battery adoption and higher consumer confidence in EVs. Investments in smart-grid integration, renewable energy-powered charging, and interoperability standards are further enhancing efficiency and reliability. This rapid infrastructure development directly drives demand for larger capacity and high-performance EV batteries. Consumer awareness campaigns and partnerships between energy companies and automakers are also playing a critical role in accelerating market expansion.

Technological Advancements in Battery Performance

One of the key growth drivers for the Turkey EV battery market is ongoing technological advancement in battery design and performance. Manufacturers are increasingly focusing on improving energy density, charging speed, and lifespan of lithium-ion and next-generation batteries to meet consumer expectations for longer-range EVs. Breakthroughs in thermal management and battery management systems are making EVs safer and more reliable, which in turn increases consumer confidence. Enhanced battery performance also enables heavier vehicles like commercial EVs and buses to enter the market, broadening applications. The adoption of modular and scalable battery packs allows manufacturers to cater to diverse vehicle segments efficiently. Overall, these technological improvements are reducing operational costs, expanding EV use cases, and fueling sustained growth of the market.

Market Restraints:

What Challenges the Turkey EV Battery Market is Facing?

Dependency on Imported Raw Materials and Components

Turkey faces significant challenges related to raw material procurement for battery production. The country lacks substantial domestic reserves of critical battery minerals, including lithium, cobalt, and nickel, necessitating reliance on international supply chains. Global supply concentration among few producing nations creates vulnerability to price volatility and potential disruptions. Currency fluctuations affecting import costs compound these challenges, impacting overall battery production economics and potentially limiting competitive positioning in regional markets.

Uneven Geographic Distribution of Charging Infrastructure

Despite rapid infrastructure expansion, charging network coverage remains concentrated in western metropolitan areas and coastal tourism regions. Eastern Anatolia, Black Sea, and Southeastern Anatolia regions have significantly lower charging station density, limiting EV adoption in these areas. Rural communities across the country face substantial gaps in charging accessibility, creating barriers to nationwide market penetration. This geographic imbalance affects overall market development and constrains battery demand growth potential in underserved regions.

High Import Tariffs Limiting Model Availability and Competition

Turkey's protectionist trade policies limit consumer access to competitively priced models. While intended to encourage domestic manufacturing investment, these barriers constrain market competition and potentially slow adoption rates. Minimum tariff requirements and dealer network mandates create additional hurdles for international manufacturers seeking market entry. These trade restrictions may delay broader consumer adoption by limiting affordable EV options in the near term.

Competitive Landscape:

The Turkey EV battery market features a competitive landscape, shaped by strategic partnerships between domestic manufacturers and international technology leaders. Joint ventures are driving local production capabilities, with manufacturers focusing on expanding capacity, improving technology, and optimizing costs to serve both domestic demand and export markets. Companies are investing in R&D facilities to advance battery performance and develop next-generation energy storage solutions. The market structure emphasizes vertical integration strategies, with participants seeking control across the value chain from cell production to module and pack assembly. Distribution partnerships with automotive manufacturers are strengthening market positioning, while investments in after-sales service networks support customer retention and brand loyalty across the rapidly evolving electric mobility ecosystem.

Turkey EV Battery Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Battery Types Covered |

Lithium-Ion Battery, Nickel-Metal Hydride Battery, Lead-Acid Battery, Others |

|

Propulsion Types Covered |

Battery Electric Vehicles, Plug-in Hybrid Electric Vehicles, Hybrid Electric Vehicles |

|

Vehicle Types Covered |

Passenger Car, Commercial Vehicles, Two-Wheeler |

|

Regions Covered |

Marmara, Central Anatolia, Mediterranean, Aegean, Southeastern Anatolia, Black Sea, Eastern Anatolia |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Turkey EV Battery Market Report

The Turkey EV battery market size was valued at USD 967.12 Million in 2025.

The Turkey EV battery market is expected to grow at a compound annual growth rate of 20.49% from 2026-2034 to reach USD 5,175.13 Million by 2034.

Battery electric vehicles dominated the market with a share of 57.7%, driven by favorable tax incentives, expanding EV charging infrastructure, and the growing consumer preference for zero-emission mobility solutions.

Key factors driving the Turkey EV battery market include strategic government investment incentives, rapid charging infrastructure expansion, establishment of domestic battery manufacturing capabilities, and increasing EV adoption rates across the country.

Major challenges include dependency on imported raw materials, uneven geographic distribution of charging infrastructure, high import tariffs limiting model availability, currency volatility affecting production costs, and need for expanded battery recycling capabilities.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)