Turkey Green Cement Market Size, Share, Trends and Forecast by Product Type, End Use Industry, and Region, 2026-2034

Turkey Green Cement Market Overview:

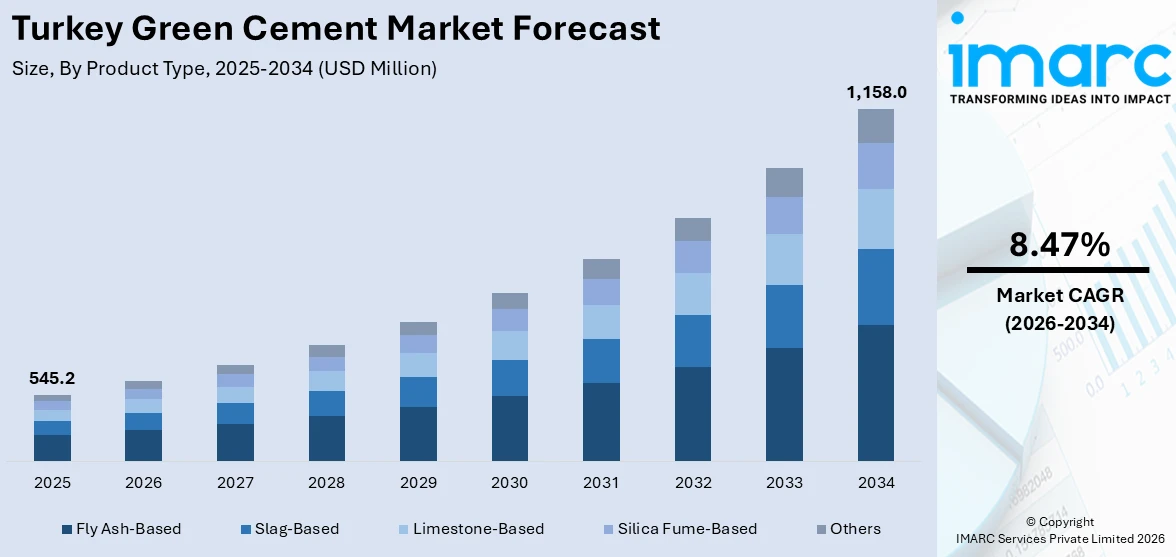

The Turkey green cement market size reached USD 545.2 Million in 2025. Looking forward, the market is projected to reach USD 1,158.0 Million by 2034, exhibiting a growth rate (CAGR) of 8.47% during 2026-2034. Demand for sustainable construction, stringent environmental regulations, and rising awareness of carbon footprints drive adoption. Advances in low‑carbon binders, waste‑based fuels, and industry collaboration reinforce progress. Investment incentives and green building certification programs support increasing Turkey green cement market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 545.2 Million |

| Market Forecast in 2034 | USD 1,158.0 Million |

| Market Growth Rate 2026-2034 | 8.47% |

Turkey Green Cement Market Trends:

Regulatory Pressure and Decarbonization Targets

Turkey’s commitment to EU‑aligned carbon reduction targets and national emissions reporting bolsters Turkey green cement market growth. Heightened scrutiny over CO₂ emissions compels cement producers to adopt clinker substitution technologies, including fly ash, slag, and natural pozzolans. Turkey's cement sector aims to cut 11 million tons of CO₂ in 10 years, avoiding 1.3 million tons of coal and petroleum coke imports, equal to the benefit of 500 million trees. Waste heat recovery now generates 154.5 MW in 17 plants, covering the daily electricity needs of 618,000 households. The sector is embracing a triple transformation: green, digital, and social, targeting net-zero emissions by 2053. Emission trading schemes and carbon taxes incentivize low‑carbon alternatives. Municipal procurement mandates for blended cements in public infrastructure projects stimulate adoption. Research partnerships between industry associations and universities facilitate pilot plants for geopolymer and CO₂‑cured cements. Certification schemes like LEED and BREEAM favor greener materials, enhancing developer demand. These compliance and policy stimuli collectively elevate acceptance and output of green cement, reinforcing Turkey green cement market growth.

To get more information on this market Request Sample

Industrial Innovation and Resource Circularity

Emerging practices in utilizing industrial by‑products, such as rice husk ash and marble waste, underpin Turkey green cement market growth. Kiln heat recovery systems and co‑processing of industrial residues reduce fossil fuel reliance. Vertical roller mills and precision blending optimize raw material usage and lower energy consumption. Digital process controls and kiln monitoring reduce emissions during production. The development of calcined clay and calcium sulfoaluminate cements further diminishes clinker dependency. Partnerships between cement producers and waste management firms supply sustainable inputs. These innovations in circularity and energy efficiency enhance cost competitiveness while reducing environmental impact, driving Turkey green cement market growth. For instance, Limak Cement, Turkey’s second-largest producer, operates 11 plants with an 18 Mt capacity and is piloting hydrogen fuel use. In 2024 trials with Air Liquide, Limak achieved 100% thermal substitution in the calciner using 3% hydrogen and AF, cutting CO₂ by up to 180,000 t/year per plant. Its AF use is 30–50%, targeting 60% average by 2030. Plans include a 400 MW renewable energy buildout and on-site electrolysers. Turkey targets 70 GW hydrogen capacity by 2053, aiming to be a hydrogen export hub.

Turkey Green Cement Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country and regional levels for 2026-2034. Our report has categorized the market based on product type and end use industry.

Product Type Insights:

- Fly Ash-Based

- Slag-Based

- Limestone-Based

- Silica Fume-Based

- Others

The report has provided a detailed breakup and analysis of the market based on the product type. This includes fly ash-based, slag-based, limestone-based, silica fume-based, and others.

End Use Industry Insights:

Access the comprehensive market breakdown Request Sample

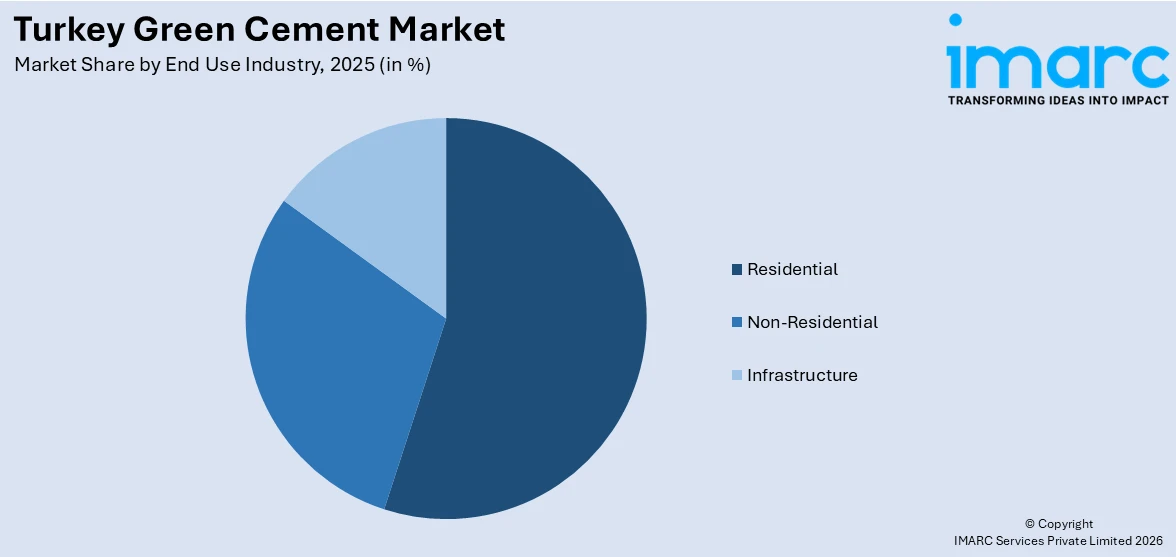

- Residential

- Non-Residential

- Infrastructure

The report has provided a detailed breakup and analysis of the market based on the end use industry. This includes residential, non-residential, and infrastructure.

Regional Insights:

- Marmara

- Central Anatolia

- Mediterranean

- Aegean

- Southeastern Anatolia

- Black Sea

- Eastern Anatolia

The report has also provided a comprehensive analysis of all the major regional markets, which include Marmara, Central Anatolia, Mediterranean, Aegean, Southeastern Anatolia, Black Sea, and Eastern Anatolia.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Turkey Green Cement Market News:

- In May 2025, Turkey's Medcem invested GBP35 Million in a new UK cement import facility in Liverpool, expanding its European and US footprint. The site will support low-carbon products and offer strategic supply chain advantages. With long-term UK agreements and a strong US presence, Medcem aims to become a mid-sized global cement player. Future projects include US terminals, a Florida unit revival, and sustainability-focused upgrades in Turkey.

Turkey Green Cement Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Fly Ash-Based, Slag-Based, Limestone-Based, Silica Fume-Based, Others |

| End Use Industries Covered | Residential, Non-Residential, Infrastructure |

| Regions Covered | Marmara, Central Anatolia, Mediterranean, Aegean, Southeastern Anatolia, Black Sea, Eastern Anatolia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the Turkey green cement market performed so far and how will it perform in the coming years?

- What is the breakup of the Turkey green cement market on the basis of product type?

- What is the breakup of the Turkey green cement market on the basis of end use industry?

- What is the breakup of the Turkey green cement market on the basis of region?

- What are the various stages in the value chain of the Turkey green cement market?

- What are the key driving factors and challenges in the Turkey green cement market?

- What is the structure of the Turkey green cement market and who are the key players?

- What is the degree of competition in the Turkey green cement market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Turkey green cement market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Turkey green cement market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Turkey green cement industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)