Turkey Halal Food Market Size, Share, Trends and Forecast by Product, Distribution Channel, and Region, 2026-2034

Turkey Halal Food Market Size, Share, Trends & Forecast (2026-2034)

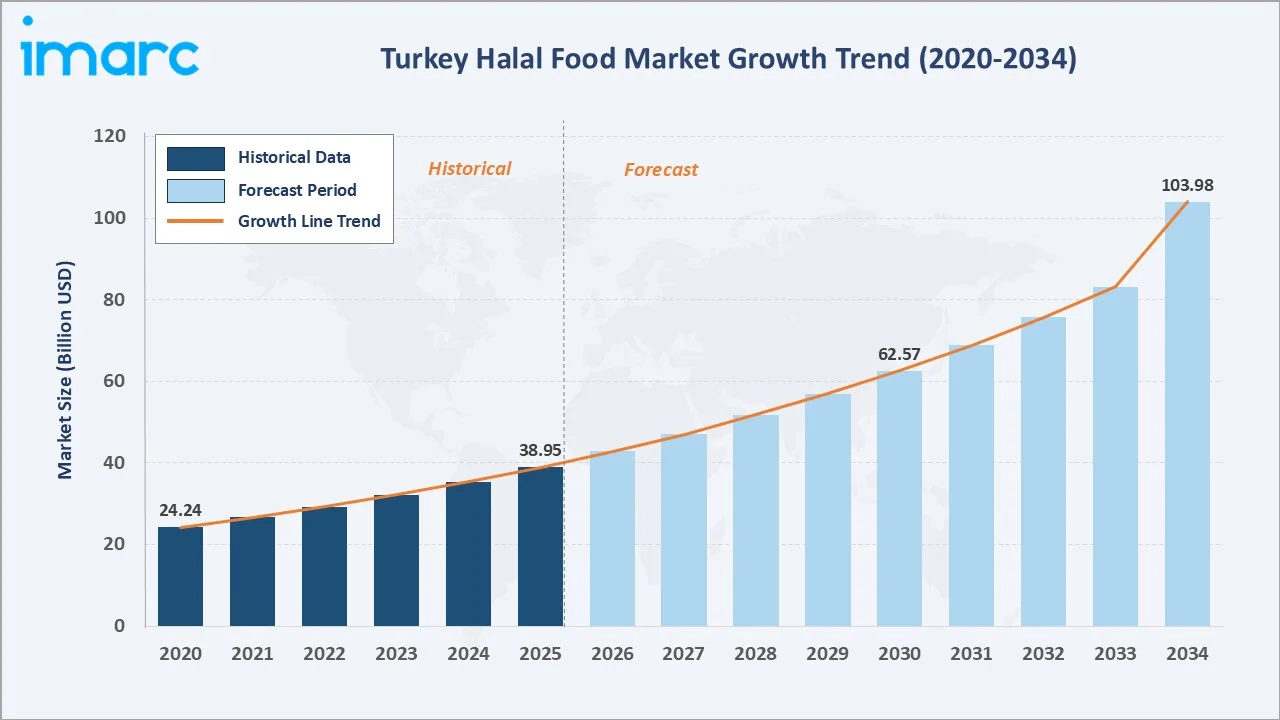

The Turkey halal food market was valued at USD 38.95 Billion in 2025 and is projected to reach USD 103.98 Billion by 2034, exhibiting a CAGR of 9.95% during 2026-2034. A predominantly Muslim population, strong domestic demand for halal-certified products, and Turkey's expanding role as a global halal food exporter are key factors driving market growth. Additionally, increasing consumer awareness of food quality, safety, and traceability is further supporting the adoption of halal food products across the country.

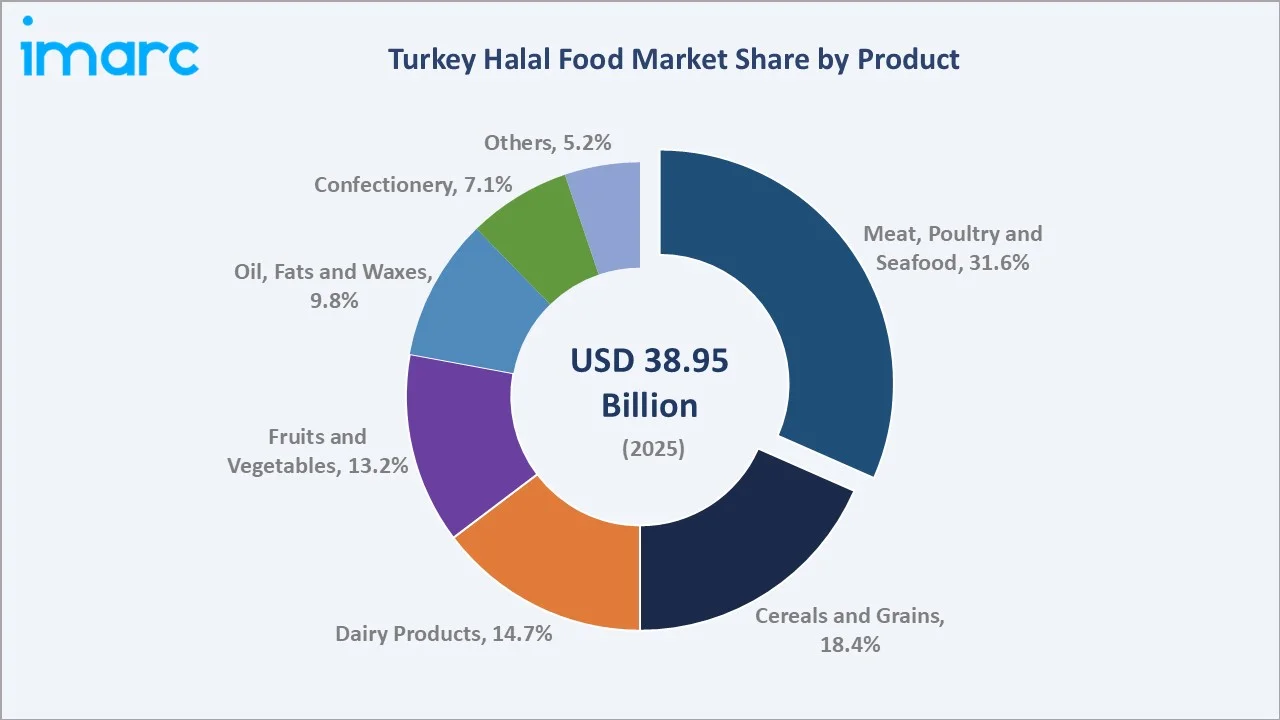

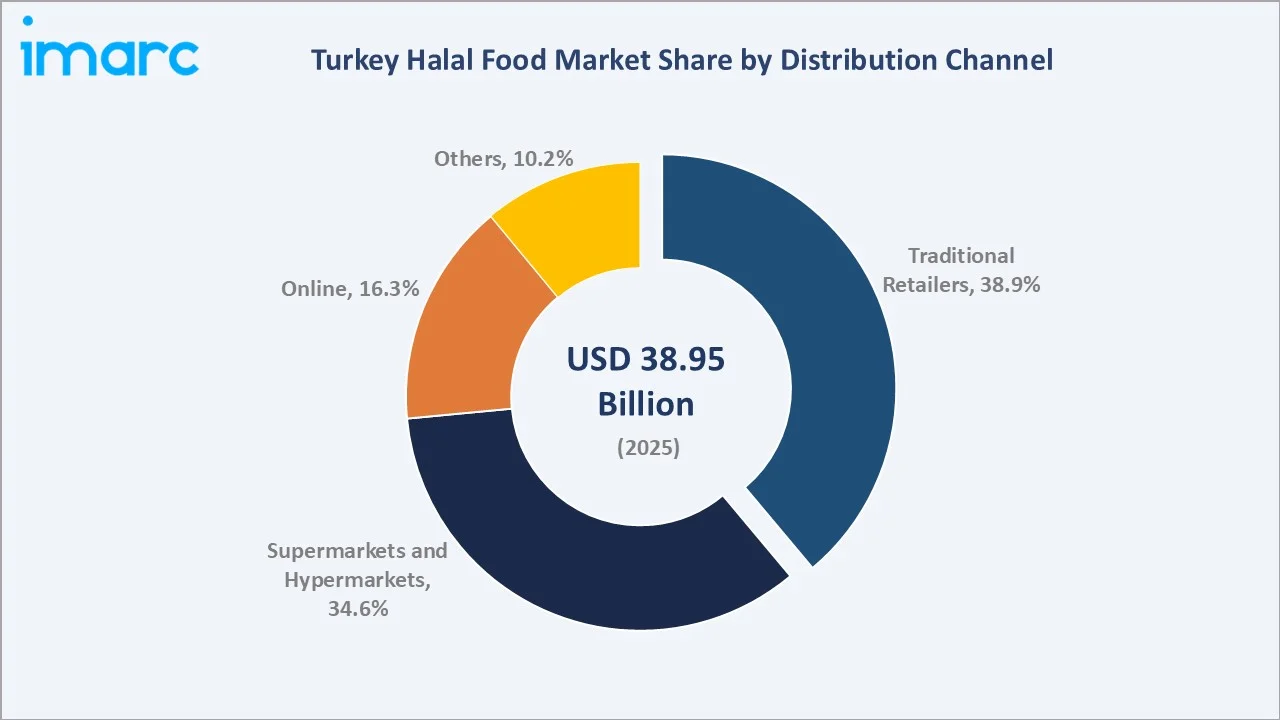

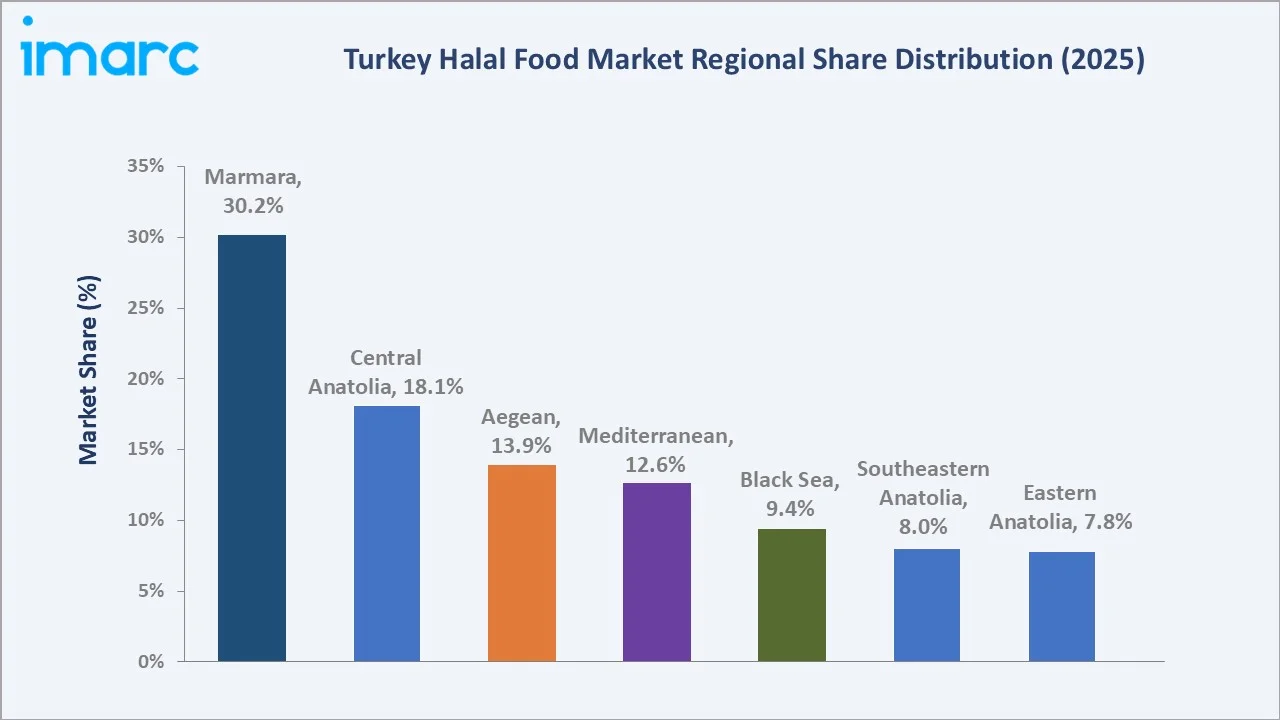

Meat, poultry and seafood lead the product segment at 31.6%, traditional retailers dominate the distribution channel segment at 38.9%, and Marmara commands 30.2% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 38.95 Billion |

|

Forecast Market Size (2034) |

USD 103.98 Billion |

|

CAGR (2026-2034) |

9.95% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Marmara (30.2%, 2025) |

|

Second Largest Region |

Central Anatolia (18.1%, 2025) |

|

Leading Product |

Meat, Poultry and Seafood (31.6%, 2025) |

|

Leading Distribution Channel |

Traditional Retailers (38.9%, 2025) |

The Turkey halal food market expanded from USD 24.24 Billion in 2020 to USD 38.95 Billion in 2025, driven by growing domestic halal consumption, government-backed export programs, and rising institutional interest from Gulf Cooperation Council trading partners. Anchored at USD 62.57 Billion in 2030, the forecast to USD 103.98 Billion by 2034 reflects accelerating export diversification, product innovation in value-added categories, and deepening penetration of modern and digital retail channels.

To get more information on this market, Request Sample

CAGR trajectories across product and distribution sub-segments show online and dairy products expanding faster than the overall 9.95% market CAGR, underpinned by growing e-commerce adoption, cold-chain investment, and rising demand for convenient halal food formats.

Executive Summary

The Turkey halal food market is on a robust growth trajectory from USD 24.24 Billion in 2020 to USD 103.98 Billion by 2034, representing a CAGR of 9.95% over the forecast period. The market has evolved from a domestically oriented, informally certified sector to a formally regulated, export-oriented ecosystem spanning meat and poultry processing, grain milling, dairy, fresh produce, edible oils, confectionery, and packaged food categories.

Meat, poultry and seafood lead product segmentation at 31.6% in 2025, supported by large-scale processing infrastructure and strong export demand. Traditional retailers command 38.9% of distribution channel share, benefiting from widespread consumer trust in established butcher shops, supermarkets, and specialty halal food outlets that offer certified products and personalized purchasing experiences. Marmara prevails over the market with a 30.2% share, fueled by Istanbul's large population base, strong retail and food processing infrastructure, and high purchasing power. As per World Population Review, the estimated population of Istanbul in 2026 is 15,791,519.

Key Market Insights

|

Insight |

Data |

|

Leading Product |

Meat, Poultry and Seafood - 31.6% share (2025) |

|

Second Largest Product |

Cereals and Grains - 18.4% share (2025) |

|

Leading Distribution Channel |

Traditional Retailers - 38.9% share (2025) |

|

Second Largest Distribution Channel |

Supermarkets and Hypermarkets – 34.6% share (2025) |

|

Leading Region |

Marmara - 30.2% share (2025) |

|

Second Largest Region |

Central Anatolia - 18.1% share (2025) |

|

Top Companies |

Nestle, Yaşar Holding, Cargill, Incorporated |

Key Analytical Observations Expanding On The Data Above:

- Meat, poultry and seafood dominance at 31.6% reflects Turkey's significant slaughterhouse infrastructure, integrated poultry value chains, and high domestic halal protein consumption, with export demand from Gulf and African markets providing additional structural support.

- Cereals and grains at 18.4% are supported by Turkey's position as a leading wheat and flour producer. Turkey is set to produce 20.5 Million Tons of wheat, including durum, in the 2026-27 (June-May) season, an increase from 16.5 Million Tons in 2025-2026. Halal-certified bakery inputs, pasta, and ready-meal components drive both domestic demand and export volume to halal-importing markets.

- Traditional retailers at 38.9% remain dominant, sustained by deep community trust, proximity, and established relationships with local halal butchers and specialized food stores.

- Supermarkets and hypermarkets at 34.6% are gaining traction due to their extensive product assortments, dedicated halal-certified sections, competitive pricing strategies, and growing presence across urban centers. Their ability to offer quality assurance, convenience, and one-stop shopping experiences continues to attract a broad consumer base.

- Marmara at 30.2% leads regional share anchored by Istanbul, Turkey's largest metropolis and food processing hub, along with Bursa and Kocaeli, which together house a significant share of Turkey's food manufacturing capacity.

Turkey Halal Food Market Overview

Halal food refers to food and beverages that comply with Islamic dietary law as defined in the Quran and interpreted by Islamic jurisprudence. In Turkey, this encompasses the entire spectrum of food production from certified animal slaughter and ingredient sourcing through processing, packaging, and retail delivery. The market integrates agricultural producers, slaughterhouses, food processing companies, halal certification bodies, logistics providers, retail distributors, and end consumers within a formally regulated ecosystem.

Turkey sits at a unique intersection of significant domestic halal consumption demand and growing international export ambition. The country's food processing infrastructure, cold-chain capabilities, and established trade relationships with halal-importing regions position it as a materially important player in the global halal food economy. Macroeconomic factors, including inflation-driven price sensitivity, currency dynamics, and evolving trade policy, shape both domestic consumption patterns and export competitiveness.

Market Dynamics

To evaluate market opportunities, Request Sample

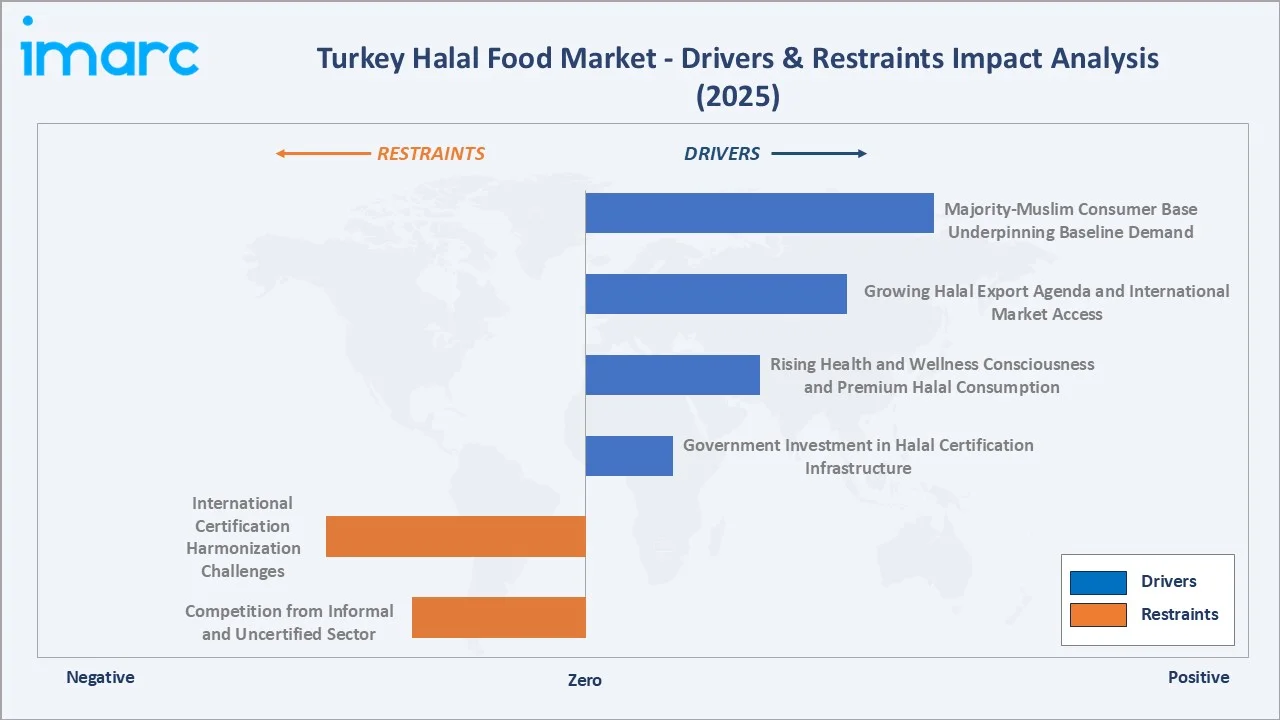

Market Drivers

- Majority-Muslim Consumer Base Underpinning Baseline Demand: Predominantly Muslim population in Turkey is creating an exceptionally large, structurally embedded domestic halal food demand that underpins market scale across all product categories and distribution formats.

- Growing Halal Export Agenda and International Market Access: The Turkish government's strategic priority to grow food exports to halal-importing markets in the Gulf, Southeast Asia, and Sub-Saharan Africa is driving investment in certified production capacity, traceability systems, and international accreditation.

- Rising Health and Wellness Consciousness and Premium Halal Consumption: Urban Turkish consumers are increasingly associating halal certification with product quality, hygiene, and ethical production standards beyond religious compliance. As per IMARC Group, the Turkey health and wellness market size reached USD 51.7 Billion in 2025. This broadening value proposition is expanding demand for premium halal ready meals, organic halal produce, and clean-label packaged foods.

- Government Investment in Halal Certification Infrastructure: Institutional support through the Halal Accreditation Agency is standardizing certification processes, reducing compliance costs for producers, and strengthening the credibility of Turkish halal marks in international markets, facilitating export growth.

Market Restraints

- International Halal Certification Harmonization Challenges: Turkey's halal certification standards are not universally recognized in all target export markets. Gulf Cooperation Council states, Malaysia, and Indonesia maintain distinct certification requirements, requiring Turkish exporters to pursue multiple certifications at additional cost and administrative burden.

- Competition from Informal and Uncertified Sector: A meaningful portion of domestic food consumption, particularly in rural and lower-income segments, is served by informal traders and small retailers offering products without formal halal certification, limiting the addressable market for certified producers.

Market Opportunities

- Expansion into Value-Added and Ready-to-Eat Halal Categories: Rising dual-income households, urbanization, and time-poor consumer lifestyles are creating growing demand for convenience halal food formats including ready meals, halal frozen foods, and snack categories.

- Digital Commerce and Direct-to-Consumer Halal Channels: The rapid growth of grocery e-commerce and food delivery platforms, combined with improving cold-chain infrastructure, is enabling halal food producers to reach urban consumers directly.

Market Challenges

- Supply Chain Traceability and Certification Integrity: Ensuring end-to-end halal integrity across complex global supply chains, particularly for imported ingredients used in processed foods, requires investment in traceability technology and third-party audit capabilities.

- Currency Volatility Impacting Export Competitiveness: Turkish lira fluctuations create pricing uncertainty for international buyers and complicate long-term contract negotiations, periodically affecting Turkey's export competitiveness relative to other halal-producing countries.

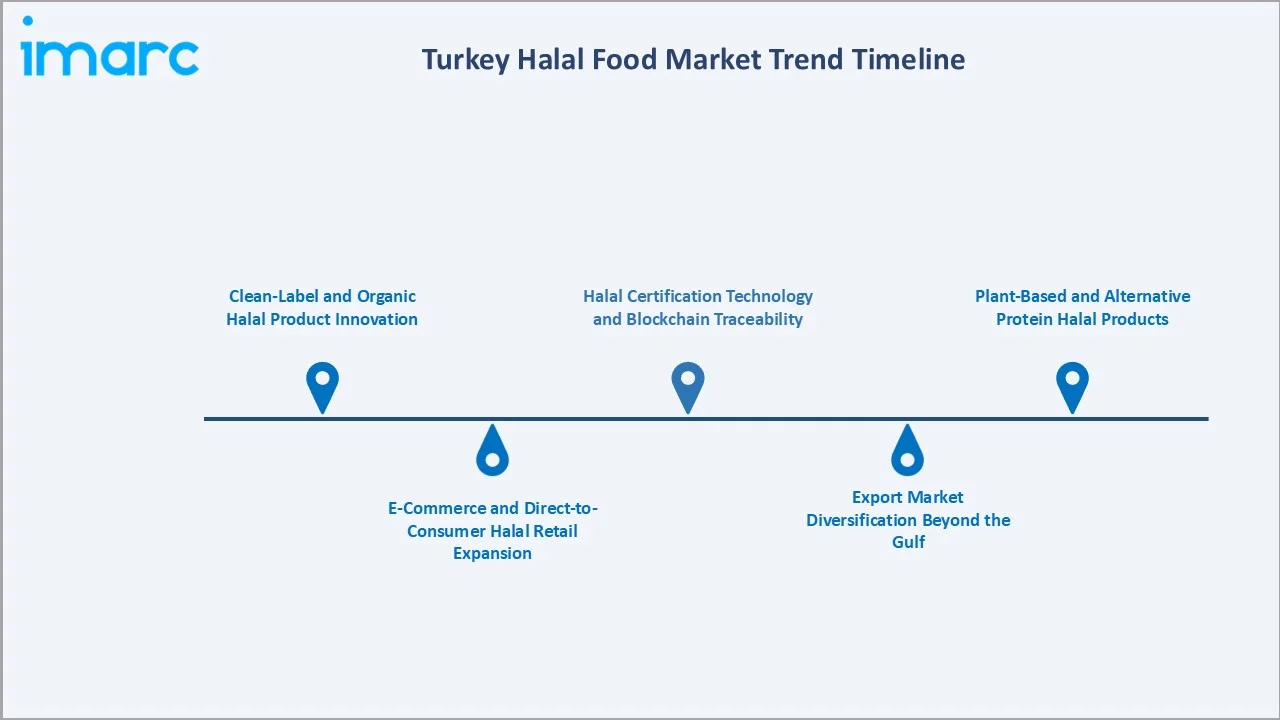

Emerging Market Trends

1. Clean-Label and Organic Halal Product Innovation

Turkish food manufacturers are increasingly launching clean-label halal products that combine religious certification with natural ingredient claims, non-GMO declarations, and reduced additive profiles. This dual positioning is addressing evolving urban consumer preferences for transparency and is enabling premium pricing in domestic retail and export markets.

2. E-Commerce and Direct-to-Consumer Halal Retail Expansion

Online grocery platforms and direct-to-consumer subscription models for fresh, frozen, and packaged halal food are expanding rapidly in major Turkish cities. The growing adoption of mobile commerce, digital payment solutions, and app-based food delivery services is making halal-certified products more accessible to urban consumers seeking convenience and wider product variety.

3. Halal Certification Technology and Blockchain Traceability

Technology-enabled halal assurance is gaining traction among premium food producers and export-focused companies. Blockchain-based traceability platforms, digital audit trails, and IoT-enabled cold-chain monitoring are being adopted to provide verifiable halal chain of custody from farm to shelf, particularly relevant for Turkey's meat export sector.

4. Export Market Diversification Beyond the Gulf

Turkish halal food exporters are actively diversifying their target markets beyond traditional Gulf destinations to include Southeast Asia, Central Asia, East Africa, and European Muslim-minority populations, reducing concentration risk associated with Gulf market dependence.

5. Plant-Based and Alternative Protein Halal Products

A nascent but growing segment of halal-certified plant-based protein products is emerging in Turkey, targeting both health-conscious domestic consumers and halal export markets in Southeast Asia where plant-based food innovation is accelerating.

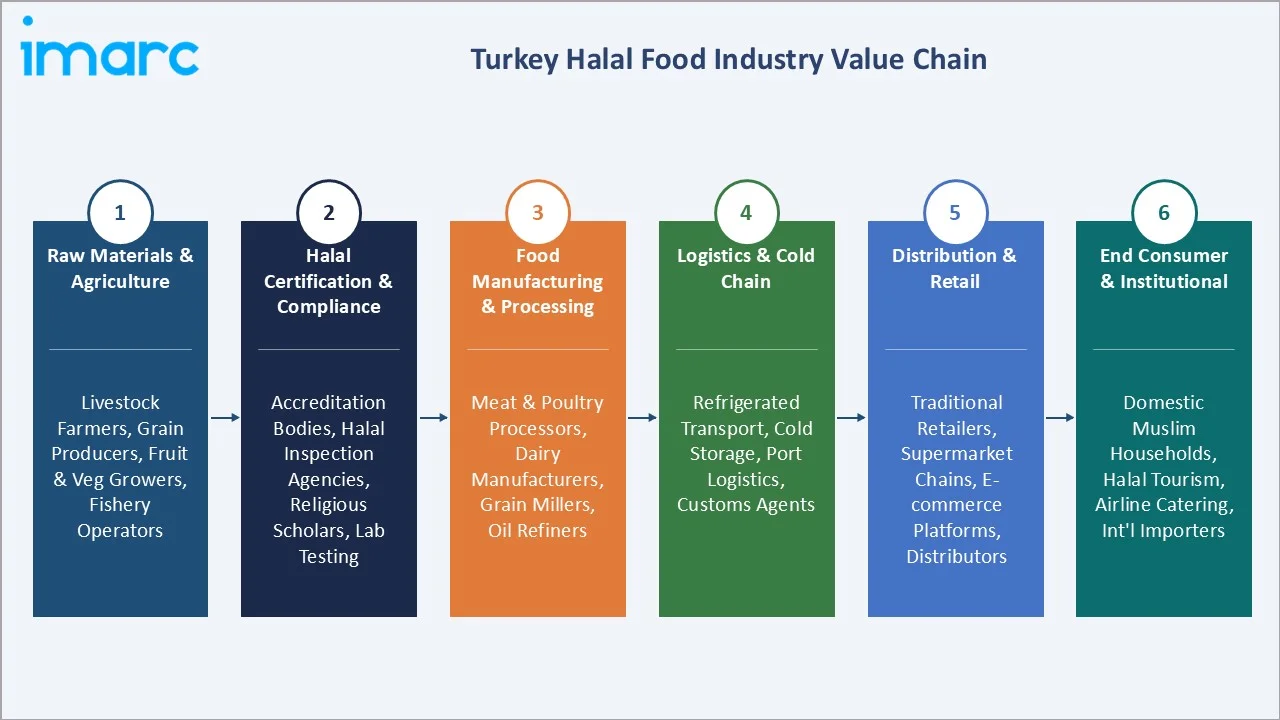

Industry Value Chain Analysis

The Turkey halal food value chain spans six stages, from agricultural raw material supply through consumer delivery and lifecycle management. Halal certification and compliance oversight runs as a cross-cutting function across all stages, distinguishing the halal supply chain from conventional food production.

|

Stage |

Key Players / Examples |

|

Raw Materials & Agriculture |

Livestock farmers, grain producers, fruit and vegetable growers, fishery operators, and ingredient importers supplying halal-compliant inputs to the food manufacturing sector |

|

Halal Certification & Compliance |

Accreditation bodies, halal inspection agencies, religious scholars serving as halal supervisors, laboratory testing providers, and third-party audit firms ensuring product compliance |

|

Food Manufacturing & Processing |

Meat and poultry processors, dairy manufacturers, grain millers, edible oil refiners, confectionery producers, and packaged food companies operating certified halal facilities |

|

Logistics & Cold Chain |

Refrigerated transport operators, cold storage warehouse providers, port logistics firms, and customs clearance agents managing domestic distribution and export shipments |

|

Distribution & Retail |

Traditional neighborhood retailers, supermarket and hypermarket chains, e-commerce grocery platforms, wholesale distributors, and export trading companies |

|

End Consumer & Institutional |

Domestic Muslim households, halal tourism and hospitality operators, airline and institutional catering services, and international halal food importers across Gulf, Asian, and African markets |

Technology Landscape in the Turkey Halal Food Industry

Halal Authentication and Testing Technologies

Advanced analytical techniques, including DNA-based species identification, polymerase chain reaction testing, isotope ratio analysis, and near-infrared spectroscopy, are being deployed across the Turkey halal food sector to authenticate ingredient composition and detect adulteration. These technologies support both domestic regulatory compliance and export certification integrity.

Food Processing Automation and Halal Compliance Integration

Modern automated slaughterhouse and food processing facilities in Turkey are integrating halal compliance protocols directly into production line management systems, reducing human error, enabling real-time compliance monitoring, and generating digital audit records required by international certification standards.

Cold Chain and Traceability Technology

IoT-enabled temperature monitoring, RFID tracking, and blockchain-based supply chain platforms are being adopted by leading Turkish halal food exporters to provide end-to-end visibility from farm to retailer, addressing increasing requirements of Gulf and Southeast Asian certification bodies.

E-Commerce and Digital Retail Platforms

Mobile-first e-commerce platforms, subscription meal kit services, and integrated halal food marketplaces are leveraging AI-powered personalization, digital payment infrastructure, and same-day delivery capabilities to serve urban Turkish halal consumers.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Meat, Poultry and Seafood |

31.6% |

2025 |

|

Distribution Channel |

Traditional Retailers |

38.9% |

2025 |

|

Region |

Marmara |

30.2% |

2025 |

By Product

Meat, poultry and seafood command a 31.6% majority share in 2025, supported by Turkey's extensive halal-certified slaughterhouse network, large-scale integrated poultry processing capacity operated by key players, and strong export demand from the Gulf.

To evaluate market opportunities, Request Sample

Cereals and grains at 18.4% reflect Turkey's position as a leading wheat, flour, and pasta producer. Strong domestic consumption and growing demand for halal-certified staple food products further support the segment's market presence.

By Distribution Channel

Traditional retailers command 38.9% of distribution share in 2025, reflecting the deeply embedded role of neighborhood stores, specialized halal butchers, and local food markets in Turkish food purchasing behavior.

Supermarkets and hypermarkets at 34.6% are expanding their halal-certified product assortments, leveraging extensive retail networks, modern merchandising formats, and growing consumer demand for convenient access to trusted halal food brands.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Marmara |

30.2% |

Dense urban population, major food processing hubs, strong export logistics infrastructure, and highest concentration of food manufacturing capacity |

|

Central Anatolia |

18.1% |

Large agricultural output, growing agri-food processing investment, rising urban food consumption in Ankara, and expanding modern retail penetration |

|

Aegean |

13.9% |

Strong fresh produce and olive oil production, growing food tourism, established export infrastructure, and rising premium food consumption in Izmir |

|

Mediterranean |

12.6% |

Expanding citrus and vegetable production, growing food processing investment, tourism-driven institutional food demand, and developing cold-chain infrastructure |

|

Black Sea |

9.4% |

Hazelnut production leadership, expanding fishery and seafood processing, growing domestic food demand, and improving logistics connectivity |

|

Southeastern Anatolia |

8.0% |

Cross-border trade activity with neighboring Gulf-adjacent markets, livestock production strength, expanding food processing investment, and growing regional food demand |

|

Eastern Anatolia |

7.8% |

Livestock and dairy production base, growing agri-food processing investment, improving transport infrastructure, and expanding domestic market access |

Marmara at 30.2% in 2025 leads the regional landscape, anchored by Istanbul, Turkey's largest city and primary food processing and logistics hub, alongside Bursa and Kocaeli. Istanbul's role as a gateway for halal food exports to Gulf, African, and Asian markets, combined with high urban consumer food spending in Turkey, sustains regional leadership across all product categories and distribution channels.

Central Anatolia at 18.1% represents a significant and growing regional market, anchored by Ankara and supported by expanding agricultural processing capacity. The region benefits from proximity to domestic grain and livestock production, improving logistics infrastructure, and rising modern retail penetration.

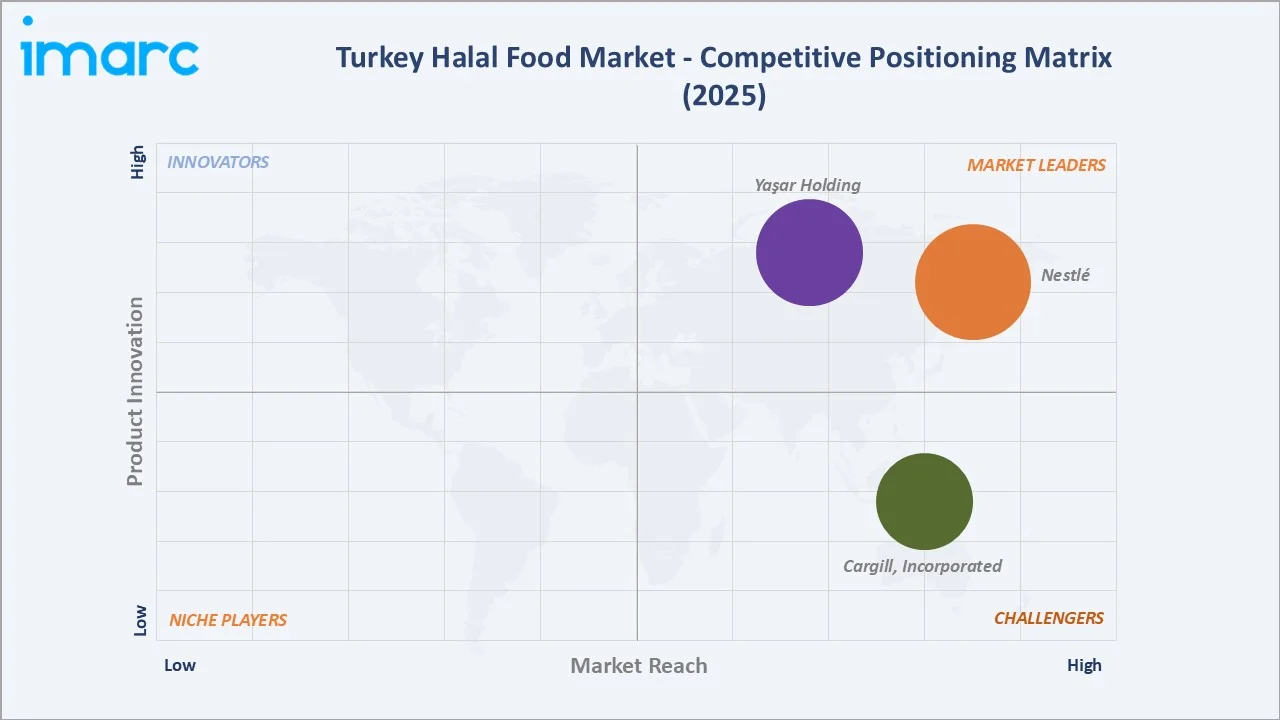

Competitive Landscape

The Turkey halal food market is moderately fragmented, with multinational food conglomerates, regional halal specialists, and vertically integrated domestic processors competing across product categories and distribution channels. Brand trust, halal certification credibility, distribution scale, and export market relationships form the primary competitive moats in this market.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Nestlé |

Nestlé |

Leader |

Expanding halal-certified packaged food and dairy portfolio across emerging markets |

|

Yaşar Holding |

Pınar Et |

Leader |

Vertically integrated halal meat and dairy production targeting domestic retail and regional export markets |

|

Cargill, Incorporated |

Cargill Türkiye |

Challenger |

Halal ingredient supply and food processing solutions enabling manufacturers to scale certified production |

Key players include Nestle, Yaşar Holding, and Cargill, Incorporated, among others.

Key Company Profiles

Nestlé

Nestlé is a multinational food and beverage company headquartered in Vevey, Switzerland, and one of the largest food companies in the world by revenue. The company operates across several markets with a portfolio spanning dairy, nutrition, coffee, culinary, confectionery, and packaged food categories. Nestlé has developed a broad halal-certified product range catering to Muslim-majority and Muslim-minority markets globally, including Turkey.

- Product Portfolio: Nestlé's Turkey-facing halal-certified product range includes dairy-based products, breakfast cereals, culinary aids, infant nutrition, confectionery, and bottled water, produced and certified under internationally recognized halal standards.

- Recent Developments: Nestlé has continued expanding its halal-certified product range, with the company leading the launch of halal-certified iron-fortified cereals and milk formulas in several countries, strengthening its position as a global halal food supplier.

- Strategic Focus: Expanding halal-certified packaged food and dairy portfolio across emerging markets through product innovation, local manufacturing investment, and strengthening halal certification infrastructure.

Yaşar Holding

Yaşar Holding is a diversified Turkish food and beverage conglomerate. The group operates across multiple segments, including dairy products, meat processing, animal nutrition, and food distribution. It supplies a broad portfolio of halal-certified products to domestic and international markets, supported by an extensive distribution network.

- Product Portfolio: The group's meat subsidiary produces and distributes halal-certified fresh and processed red meat products under the Pınar Et brand, alongside a comprehensive halal-certified dairy range.

- Recent Developments: The group continues to invest in production capacity and export market development across Gulf and European markets, with ongoing operations through its international distribution subsidiaries in Germany and the Gulf region.

- Strategic Focus: Vertically integrated halal meat and dairy production targeting domestic retail and regional export markets.

Cargill, Incorporated

Cargill, Incorporated is an American multinational food corporation and one of the world's largest privately held companies by revenue. The company operates across the food, agriculture, financial, and industrial sectors in several countries.

- Product Portfolio: Cargill Türkiye supplies a wide range of halal-certified food ingredients to Turkish food manufacturers, including edible oils and plant proteins, all available with relevant halal, kosher, and other internationally recognized certifications.

- Recent Developments: Cargill has been strengthening its halal ingredient certification capabilities and supply chain partnerships with food manufacturers in Turkey, while investing in sustainable sourcing programs aligned with evolving halal and ethical consumption standards.

- Strategic Focus: Halal ingredient supply and food processing solutions enabling manufacturers to scale certified production efficiently and access international halal export markets.

Market Concentration Analysis

The Turkey halal food market exhibits moderate fragmentation, with multinational food companies, regional halal specialists, and a large number of domestic processors competing across product categories. The top tier of market participants, anchored by global players, such as Nestlé, alongside domestic leaders, commands a meaningful aggregate share of certified production volume and export activity.

Barriers to entry in the formally certified halal food segment include the cost of obtaining and maintaining internationally recognized halal certification, investment in compliant processing infrastructure, cold-chain logistics capability, and the brand equity required to command shelf space in modern retail. These factors favor established players with diversified product portfolios, multi-certification capability, and existing export market relationships.

Consolidation activity is gradual, with larger processors acquiring smaller certified facilities to expand capacity, while international players establish Turkish procurement and processing partnerships. The market is expected to progressively consolidate in export-oriented segments while remaining fragmented in domestically focused traditional retail channels.

Investment & Growth Opportunities

Fastest-Growing Segments

Online is expanding the fastest among distribution channels, driven by grocery e-commerce growth, cold-chain investment, and increasing digital adoption among younger halal food consumers. Dairy products and confectionery represent the fastest-growing product categories within the certified halal portfolio.

Emerging Markets

Central Anatolia at 18.1% represents a high-potential regional opportunity, supported by growing agri-food processing investment, rising urban food spending in Ankara, and improving logistics connectivity. Southeastern Anatolia at 8.0% offers strategic value given its proximity to cross-border trade routes with halal-importing markets in the Gulf region.

Venture & Investment Trends

Investment is flowing into cold-chain logistics infrastructure, halal certification technology platforms, e-commerce and direct-to-consumer food delivery models, and value-added processing facilities targeting export markets. Government-backed export support programs are also creating co-investment opportunities in halal food processing capacity and traceability infrastructure.

Future Market Outlook (2026-2034)

The Turkey halal food market is forecast to expand from USD 38.95 Billion in 2025 to USD 103.98 Billion by 2034 at a CAGR of 9.95%, adding approximately USD 65 Billion in incremental annual market value over the forecast period.

This expansion will be driven by four primary forces: deepening domestic halal consumption supported by population growth and premiumization; accelerating halal export diversification across Gulf, Asian, and African markets; structural shift toward modern retail and online distribution channels; and increasing product innovation in convenience, clean-label, and alternative protein halal categories.

By 2034, the Turkey halal food market is expected to be characterized by a more export-diversified, technology-enabled, and premium-oriented ecosystem, with consolidation among certified processors, deeper integration with international halal supply chains, and growing recognition of Turkish halal standards across major global import markets.

Research Methodology

Primary Research

Primary research included structured consultations with Turkish food industry executives, halal certification body officials, export promotion agency representatives, retail chain category managers, and supply chain logistics providers. These engagements validated market sizing estimates, segment growth trajectories, regional demand dynamics, and competitive positioning assessments.

Secondary Research

Secondary sources included Turkish Statistical Institute food production and export data, Ministry of Agriculture and Forestry trade statistics, TÜRKAK and Halal Accreditation Agency certification data, Turkish Exporters Assembly reports, Central Bank of the Republic of Turkey economic data, and publicly available annual reports and investor presentations from key market participants.

Forecasting Models

Market forecasts employed both top-down and bottom-up methodologies, combining domestic food consumption projections, export market demand modeling, product category growth rate analysis, distribution channel evolution scenarios, and macroeconomic variable integration.

Turkey Halal Food Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Meat, Poultry and Seafood, Fruits and Vegetables, Dairy Products, Cereals and Grains, Oil, Fats and Waxes, Confectionery, Others |

| Distribution Channels Covered | Traditional Retailers, Supermarkets and Hypermarkets, Online, Others |

| Regions Covered | Marmara, Central Anatolia, Mediterranean, Aegean, Southeastern Anatolia, Black Sea, Eastern Anatolia |

| Companies Covered | Nestlé, Yaşar Holding, Cargill, Incorporated, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Turkey halal food market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Turkey halal food market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Turkey halal food industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Turkey Halal Food Market Report

The Turkey halal food market was valued at USD 38.95 Billion in 2025, driven by strong domestic halal consumption demand, growing export activity, and expanding modern retail penetration.

The market is projected to reach USD 103.98 Billion by 2034, growing at a CAGR of 9.95% from 2026-2034, supported by export diversification and rising domestic premiumization.

Meat, poultry and seafood lead at 31.6% in 2025, supported by Turkey's large certified slaughterhouse infrastructure and strong export demand from Gulf and African markets.

Traditional retailers at 38.9% in 2025 prevails over the market, fueled by strong consumer trust in neighborhood stores, specialized halal butchers, and local food markets, as well as their widespread presence across both urban and rural areas of Turkey.

Marmara commands 30.2% in 2025, anchored by Istanbul's food processing hubs, export logistics infrastructure, and high urban consumer food spending in Turkey.

Key players include Nestle, Yaşar Holding, and Cargill, Incorporated, among others.

Grocery e-commerce expansion, cold-chain logistics investment, smartphone penetration, and demand for convenient halal food delivery among urban consumers are the primary drivers of online channel growth.

Turkey's halal food exports are growing driven by government export programs, bilateral trade agreements with Gulf and Asian markets, and surging global demand for authenticated halal products.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)