Turkey Residential Real Estate Market Size, Share, Trends and Forecast by Type and Region, 2026-2034

Turkey Residential Real Estate Market Overview:

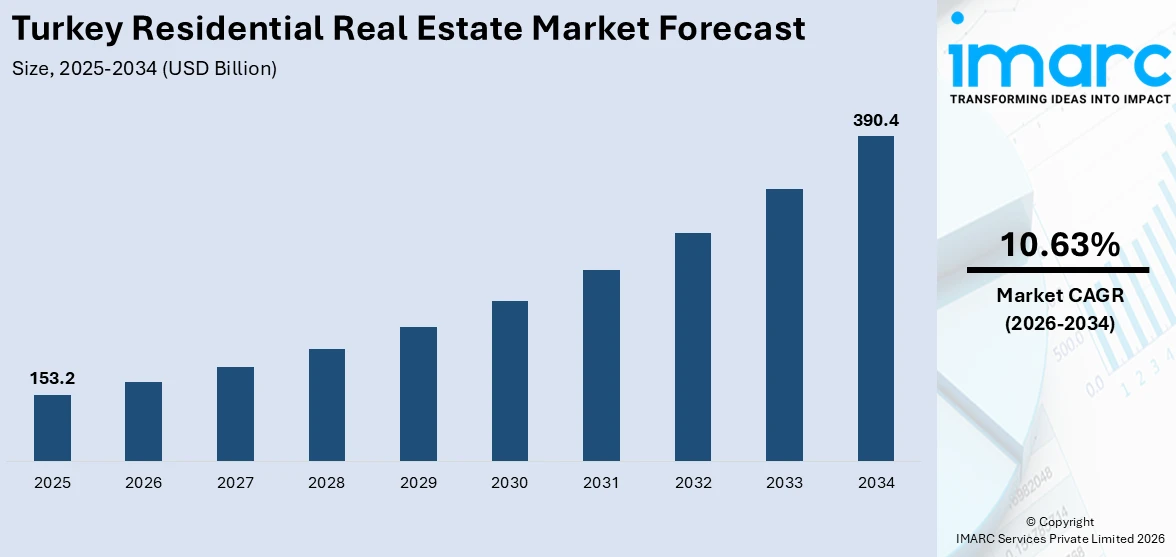

The Turkey residential real estate market size reached USD 153.2 Billion in 2025. The market is projected to reach USD 390.4 Billion by 2034, exhibiting a growth rate (CAGR) of 10.63% during 2026-2034. The demand is fueled by numerous large-scale urbanization processes, an increasing middle class, and high domestic housing demand. There are government stimulus packages like citizenship-for-property offers, cheap mortgages, and tax credits that drive investment. Infrastructure construction, particularly in Istanbul and coastal areas, adds to property attractiveness. Foreign investment, driven by strategic positioning and cheap prices, also contributes to Turkey residential real estate market share. Economic forces such as inflation and interest rates determine purchasing power, whereas cultural affinity for home ownership drives long-run growth in the residential sector.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 153.2 Billion |

| Market Forecast in 2034 | USD 390.4 Billion |

| Market Growth Rate 2026-2034 | 10.63% |

Turkey Residential Real Estate Market Trends:

Foreign Investment and Strategic Location

Turkey’s strategic geographic position, bridging Europe and Asia, makes its residential real estate market attractive to foreign investors. Affordable property prices compared to Western Europe, combined with high rental yields, attract buyers seeking both investment and residency opportunities. The government’s citizenship-for-property program has accelerated international demand, particularly in Istanbul, Antalya, and coastal regions. Foreign interest stimulates development of luxury apartments, resort-style residences, and mixed-use projects tailored to international tastes. Additionally, geopolitical stability in certain regions and the country’s cultural appeal enhance its marketability. Developers benefit from foreign capital inflows, which drive innovation, premium construction standards, and urban regeneration projects. As foreign demand remains robust, it continues to shape supply trends, pricing strategies, and overall market dynamics, reinforcing Turkey’s residential real estate sector as a competitive global investment destination.

To get more information on this market Request Sample

Urbanization and Demographic Growth

Rapid urbanization remains a key driver of Turkey’s residential real estate market trends, with 77.89% of the population living in urban areas in 2024, up from 77.46% in 2023. Cities like Istanbul, Ankara, and Izmir face increasing housing demand due to rural-to-urban migration and the expansion of young households entering the market. This demographic shift fuels the need for apartments, condominiums, and mixed-use developments, while urban growth drives modernization of older neighborhoods and large-scale housing projects. Developers respond with high-density complexes, vertical housing, and integrated amenities to optimize land use. Population growth and internal migration continually reshape city layouts, influencing property prices, availability, and investment potential. These trends sustain activity across both primary sales and rental markets, reinforcing long-term growth in Turkey’s residential real estate sector.

Government Incentives and Policy Support

Government policies significantly influence Turkey’s residential real estate market. Incentives like low-interest mortgages, tax reductions, and housing credit support increase affordability and encourage both domestic and foreign investment. The citizenship-for-property program attracts international buyers, particularly from the Middle East, Europe, and Asia, boosting high-end property sales. Infrastructure projects, including new roads, airports, and urban renewal initiatives, enhance property values and development opportunities. Regulatory frameworks supporting property ownership and construction stimulate developer confidence, while public-private partnerships accelerate large-scale housing projects. Housing projects are often designed to align with government urban transformation strategies, addressing earthquake resilience and modern living standards. Overall, supportive government measures create a favorable environment that drives continuous Turkey residential real estate market growth, liquidity, and investor participation in the residential real estate sector.

Turkey Residential Real Estate Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country and regional levels for 2026-2034. Our report has categorized the market based on type.

Type Insights:

Access the comprehensive market breakdown Request Sample

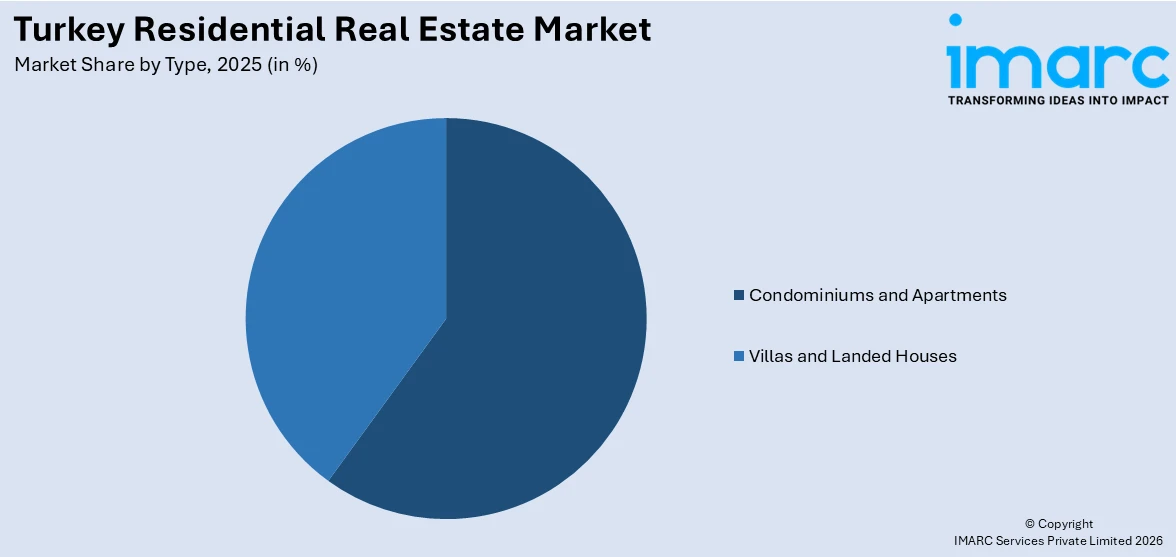

- Condominiums and Apartments

- Villas and Landed Houses

A detailed breakup and analysis of the market based on the type have also been provided in the report. This includes condominiums and apartments and villas and landed houses.

Regional Insights:

- Marmara

- Central Anatolia

- Mediterranean

- Aegean

- Southeastern Anatolia

- Black Sea

- Eastern Anatolia

The report has also provided a comprehensive analysis of all the major regional markets, which include Marmara, Central Anatolia, Mediterranean, Aegean, Southeastern Anatolia, Black Sea, and Eastern Anatolia.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Turkey Residential Real Estate Market News:

- In February 2025, Türkiye’s Emlak Konut launched a new housing campaign targeting middle-income buyers, offering zero down payment, decreasing installments, a 12-month grace period, or a leasing model across 25 projects in Istanbul, Izmir, Antalya, and Balıkesir. Amid rising rents, high property prices, and increased borrowing costs, the program aims to ease homeownership. With Türkiye’s population nearing 85.7 million and expected to exceed 88 million by 2030, the initiative addresses growing housing demand while providing flexible, low-interest repayment options of up to 60 months.

Turkey Residential Real Estate Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Condominiums and Apartments, Villas and Landed Houses |

| Regions Covered | Marmara, Central Anatolia, Mediterranean, Aegean, Southeastern Anatolia, Black Sea, Eastern Anatolia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the Turkey residential real estate market performed so far and how will it perform in the coming years?

- What is the breakup of the Turkey residential real estate market on the basis of type?

- What is the breakup of the Turkey residential real estate market on the basis of region?

- What are the various stages in the value chain of the Turkey residential real estate market?

- What are the key driving factors and challenges in the Turkey residential real estate market?

- What is the structure of the Turkey residential real estate market and who are the key players?

- What is the degree of competition in the Turkey residential real estate market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Turkey residential real estate market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Turkey residential real estate market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Turkey residential real estate industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)