UAE Bottled Water Market Size, Share, Trends and Forecast by Product Type, Distribution Channel, and Region, 2026-2034

UAE Bottled Water Market Size, Share, Trends & Forecast (2026-2034)

The UAE bottled water market size was valued at USD 1.61 Billion in 2025 and is projected to reach USD 3.51 Billion by 2034, growing at a CAGR of 8.26% during 2026-2034. Rapid population growth, a highly urbanized lifestyle, and an arid climate with negligible freshwater resources collectively underpin strong demand.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.61 Billion |

|

Forecast Market Size (2034) |

USD 3.51 Billion |

|

CAGR (2026-2034) |

8.26% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

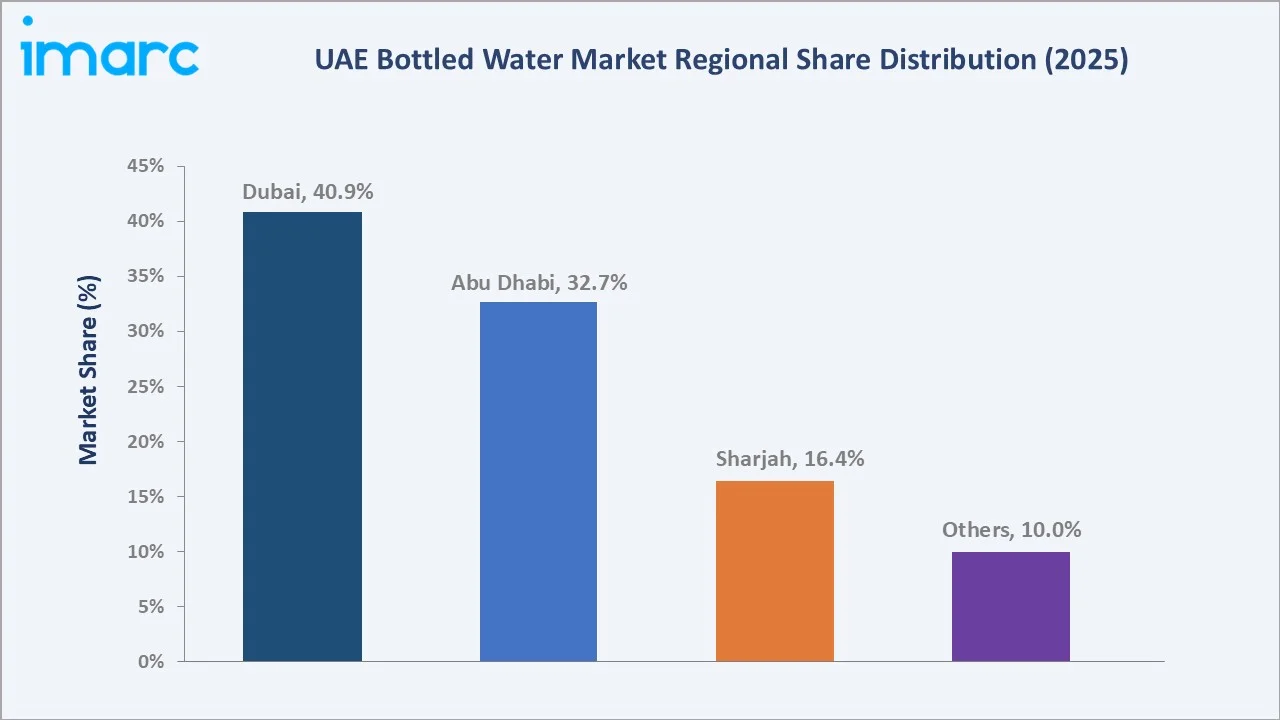

Dubai (40.9% share, 2025) |

|

Fastest Growing Region |

Abu Dhabi (~8.9% CAGR) |

|

Leading Product Type |

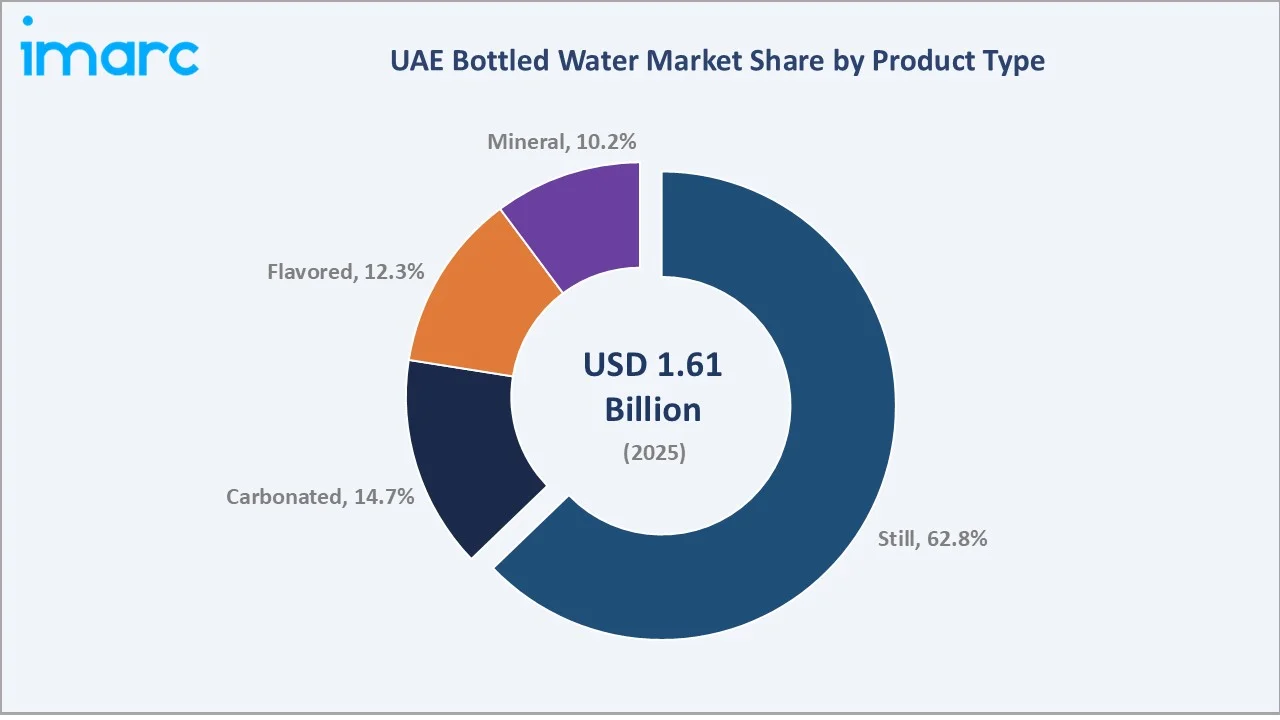

Still Water (62.8%, 2025) |

|

Leading Distribution Channel |

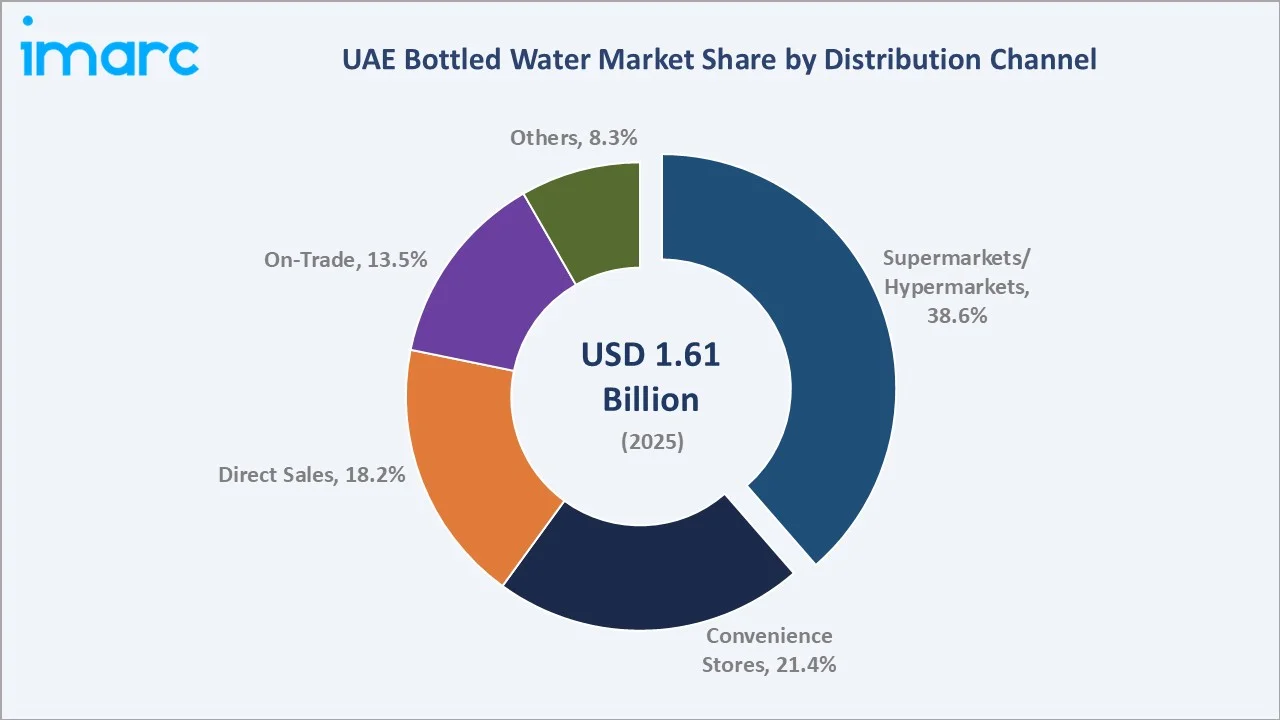

Supermarkets/Hypermarkets (38.6%, 2025) |

The chart below illustrates the UAE bottled water market growth trajectory from 2020 through 2034, contrasting historical expansion against a sustained forecast curve powered by tourism, health consciousness, and infrastructure investment.

To get more information on this market, Request Sample

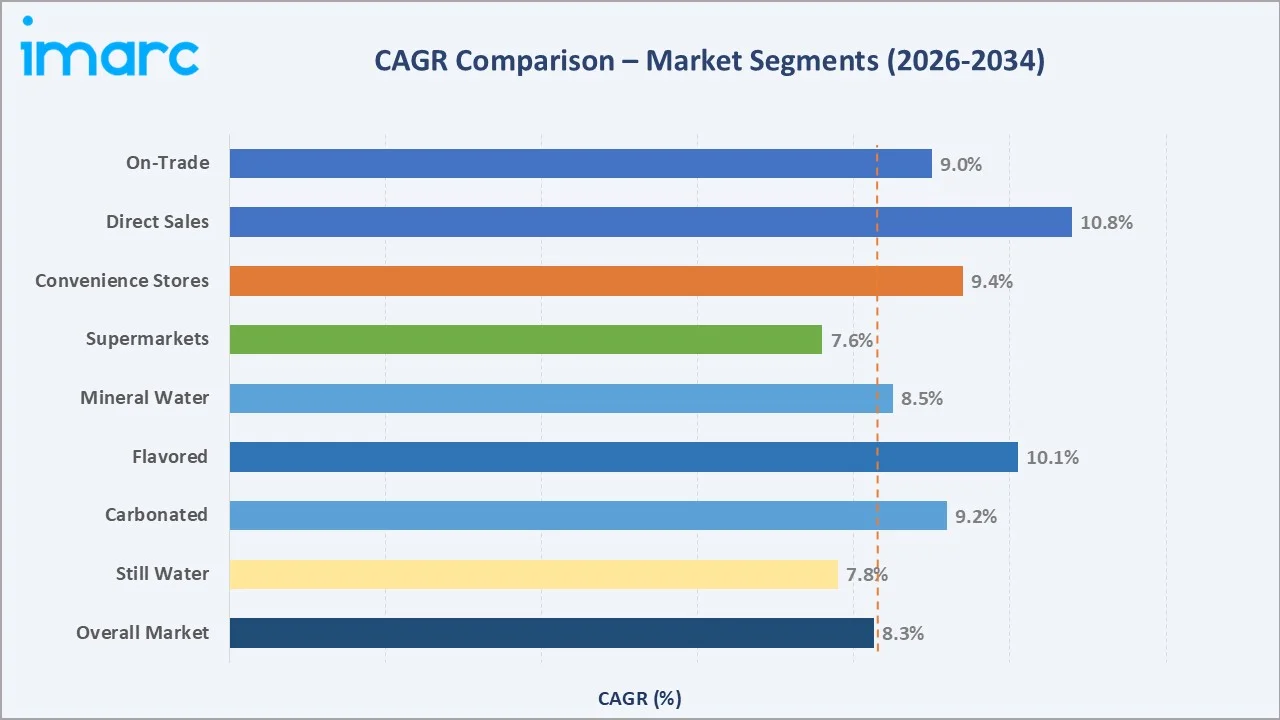

Segment-level CAGR comparisons highlight flavored and direct sales sub-categories as the fastest-growing channels within the UAE bottled water market forecast through 2034.

Executive Summary

The UAE bottled water market is experiencing robust expansion, underpinned by a unique convergence of environmental, demographic, and lifestyle factors. Valued at USD 1.61 Billion in 2025, the market has grown from USD 1.08 Billion in 2020, reflecting sustained historical demand. It is forecast to reach USD 2.39 Billion by 2030 and USD 3.51 Billion by 2034 at a CAGR of 8.26%.

Still water commands a dominant 62.8% share in 2025, driven by everyday hydration needs among the UAE's large expatriate population and a health-conscious consumer base. Flavored water is the fastest-growing product sub-segment, posting an estimated CAGR of 10.1% as consumers diversify from plain water.

Dubai accounts for 40.9% of national revenue in 2025, driven by its tourism, hospitality, and high-density residential base. Abu Dhabi follows with 32.7%, supported by government institutional procurement. The outlook through 2034 remains strongly positive as premiumization, eco-packaging mandates, and smart dispensing adoption redefine category dynamics across the UAE.

Key Market Insights

|

Insight |

Data |

|

Largest Product Type |

Still Water – 62.8% share (2025) |

|

Fastest Growing Product |

Flavored Water – ~10.1% CAGR (2026-2034) |

|

Leading Distribution Channel |

Supermarkets/Hypermarkets – 38.6% (2025) |

|

Fastest Growing Channel |

Direct Sales – ~10.8% CAGR (2026-2034) |

|

Leading Region |

Dubai – 40.9% revenue share (2025) |

|

Fastest Growing Region |

Abu Dhabi – ~8.9% CAGR (2026-2034) |

|

Top Companies |

Agthia Group PJSC, Masafi, Nestlé, Danone, PepsiCo, Inc., The Coca‑Cola Company, Our Oasis |

|

Market Opportunity |

Premiumization + Eco-packaging segments |

Key Analytical Observations Supporting The Data Above:

- Still water's 62.8% dominance in 2025 is rooted in the UAE's near-total dependence on desalinated tap water, which many consumers avoid due to taste and safety concerns, making bottled still water the daily hydration default.

- Flavored water, growing at 10.1% CAGR through 2034, reflects younger UAE consumers' growing appetite for functional and flavored beverages positioned between plain water and carbonated soft drinks.

- Supermarkets and hypermarkets lead with a 38.6% channel share in 2025 because of the UAE's highly developed modern trade network, frequent promotional pricing, and convenience of bulk purchasing for households.

- Direct sales channel is rising rapidly at an estimated 10.8% CAGR through 2034 as businesses, hospitals, and residential complexes increasingly subscribe to bottled water home and office delivery services.

- Dubai's regional dominance at 40.9% market share in 2025 is fuelled by over 19.6 million tourists annually, the highest hotel room density in the UAE, and a large, high-income residential base demanding premium water variants.

- Premiumization and sustainability, driven by eco-friendly packaging and smart vending and dispensing technologies, represent a significant incremental opportunity by 2030, attracting strategic investment from global FMCG players.

UAE Bottled Water Market Overview

Bottled water encompasses packaged water products including still, carbonated, flavored, and mineral variants sold in PET, glass, or biodegradable containers. The UAE market sits at the intersection of one of the world's driest climates and one of its highest per-capita consumer spending environments. With no natural surface freshwater, the country relies on desalination and groundwater, making bottled water a near-essential consumer product.

The industry spans raw material procurement (PET resins, caps), water sourcing and purification, bottling and packaging, multi-channel distribution, and end-user consumption across households, hotels, offices, retail, and food service. Regulatory oversight from the Emirates Authority for Standardization and Metrology (ESMA) and increasing sustainability mandates are shaping product specifications and packaging materials, especially towards recyclable and reduced-plastic formats.

Market Dynamics

To evaluate market opportunities, Request Sample

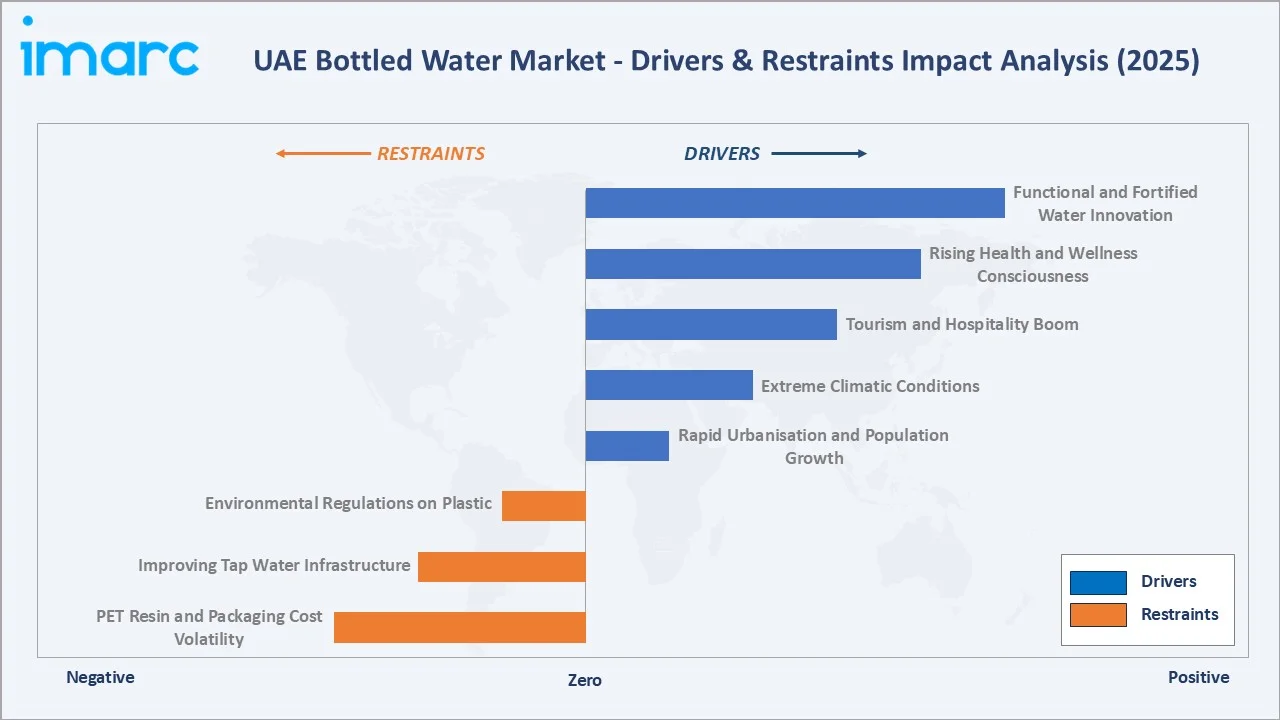

Market Drivers

- Rapid Urbanisation and Population Growth: The UAE's resident population exceeded 11.3 million in 2024, with over 88% residing in urban centres. Large-scale real estate and hospitality projects generate structural demand for bottled water across residential, hotel, and commercial segments.

- Extreme Climatic Conditions: With consistently high temperatures, outdoor and construction workers require substantial volumes of bottled water year-round. A large construction workforce drives significant institutional procurement demand, supporting steady consumption across infrastructure and development activities.

- Tourism and Hospitality Boom: An estimated 19.59 million tourists visited the UAE in 2025. Hotels, restaurants, and airlines are major institutional buyers. Dubai's hospitality sector is a key consumer of bottled water, serving as a major growth driver for premium and sparkling variants.

- Rising Health and Wellness Consciousness: Growing awareness of hydration and wellness is driving per-capita bottled water consumption higher. UAE Wellness Economy Surges to $34.1 Billion, the Largest in the Middle East in 2025, with bottled water benefiting from its positioning as a clean, safe hydration choice.

Market Restraints

- PET Resin and Packaging Cost Volatility: Prices of PET resin, the primary packaging material, have fluctuated significantly due to petrochemical market dynamics and supply chain disruptions, compressing manufacturer margins and limiting pricing flexibility at the retail level.

- Improving Tap Water Infrastructure: Government investment in advanced desalination technologies is improving tap water quality, particularly in Abu Dhabi where treated water meets international standards. Rising consumer confidence in tap water could moderate growth in lower end bottled water segments.

- Environmental Regulations on Plastic: The UAE government's single-use plastic reduction initiatives and ESMA regulations mandate greater recyclability, increasing compliance costs for manufacturers, particularly SME bottlers, and putting pressure on overall operational expenditure.

Market Opportunities

- Functional and Fortified Water Innovation: Functional waters infused with minerals, electrolytes, and vitamins represent a nascent but rapidly growing sub-category, with limited SKU availability currently dominating the segment and leaving substantial white space for new entrants and brand extensions.

- Smart Dispensing and Vending Infrastructure: Smart vending machines and IoT-enabled water dispensers in malls, offices, and residential buildings are gaining traction, creating an incremental channel opportunity for water brands and supporting the expansion of automated, on-demand distribution networks.

- Sustainable Packaging Premium: Gulf sustainability commitments, including UAE Net Zero 2050, are creating demand for refillable and biodegradable water packaging. Brands investing in rPET and glass alternatives are positioned to win premium-tier institutional contracts with government entities and luxury hotels.

Market Challenges

- Intense Competitive Fragmentation: The UAE market hosts numerous licensed bottled water brands, including international and regional players. Intense price competition in the still water segment has compressed average retail price realization, challenging brand differentiation strategies.

- Logistics and Cold-Chain Constraints: Cold-chain integrity and last-mile delivery efficiency remain critical, especially for small-format retail distribution in Sharjah and the Northern Emirates. High logistics costs in direct sales channels continue to limit margin expansion.

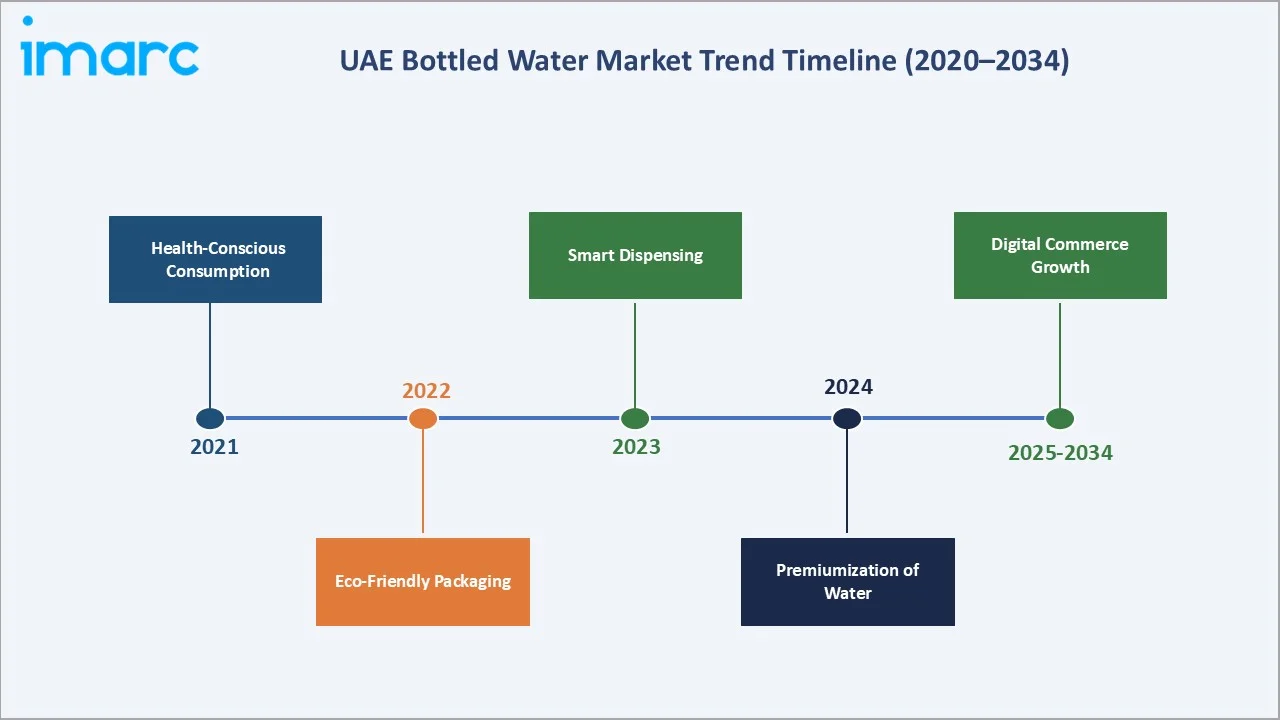

Emerging Market Trends

1. Health-Driven Premiumization

UAE consumers are increasingly trading up from commodity still water to premium mineral and functional variants. Products with added electrolytes, alkaline pH, and trace minerals are gaining traction and commanding significant price premiums over standard offerings.

2. Eco-Friendly and Sustainable Packaging

UAE Vision 2031 sustainability commitments and ESMA packaging directives are pushing manufacturers toward rPET, biodegradable plastics, and glass alternatives. Eco-labelling is becoming increasingly prominent among premium water products, reflecting a growing shift toward sustainable packaging solutions.

3. E-Commerce and Subscription-Based Direct Delivery

Online grocery and e-commerce platforms such as Noon, Amazon.ae, and Talabat are driving strong growth in bottled water sales. Subscription-based home and office delivery models are gaining traction, providing stable recurring revenue streams for leading brands.

4. Smart Dispensing and Touchless Technology

Post-pandemic hygiene awareness has accelerated the adoption of touchless and smart water dispensers across corporate offices, schools, and healthcare facilities. This shift is reducing reliance on single-use bottles in institutional settings and supporting more sustainable consumption practices.

5. Flavored and Functional Water Diversification

Flavored water variants are the fastest-growing product segment, driven by new launches featuring natural fruit infusions, zero-calorie formulations, and vitamin-enhanced options targeting health-conscious millennial and Gen Z consumers.

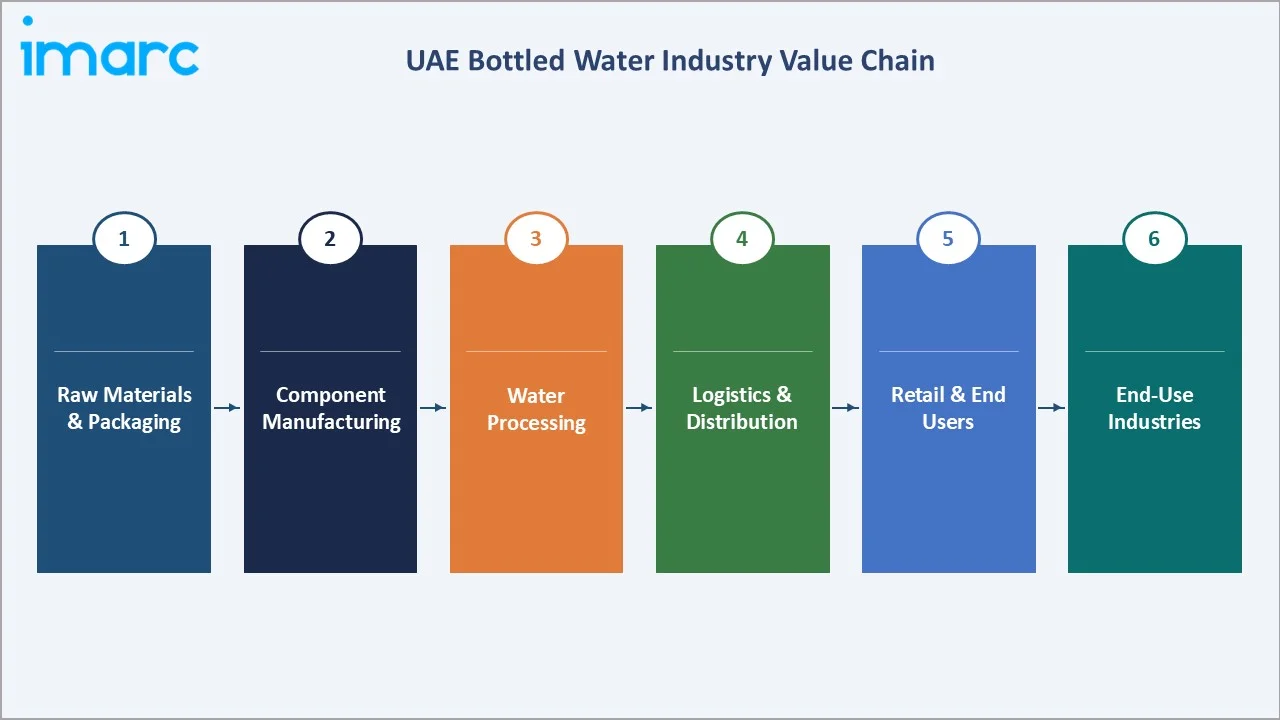

Industry Value Chain Analysis

The UAE bottled water value chain comprises five key stages, beginning with raw materials and packaging, followed by component manufacturing and water processing. Each of these upstream and midstream stages involves specialized players responsible for sourcing inputs, producing packaging components, and ensuring water purification and quality standards.

|

Stage |

Key Activities |

Key Players / Participants |

|

Raw Materials & Packaging |

PET resin procurement, cap and label sourcing, glass manufacturing |

SABIC, Alpla, Greiner Packaging |

|

Component Manufacturing |

Automated filling, capping, labelling, quality testing, batch coding |

Masafi, Al Ain Water, Nestlé UAE, Agthia |

|

Water Processing |

Groundwater extraction, desalinated water intake, reverse osmosis, UV treatment |

UAE desalination plants, regional spring sources |

|

Logistics & Distribution |

Refrigerated transport, warehouse management, last-mile delivery, fleet management |

Aramex, Al Futtaim Logistics, brand-owned fleets |

|

Retail & End Users |

Shelf placement, e-commerce fulfilment, vending, institutional delivery |

Carrefour, LuLu, Spinneys, Noon, Hotels, Offices |

Downstream, the value chain includes logistics and distribution and finally retail and end users. These stages focus on efficient product movement, storage, and final delivery to consumers, collectively adding value and ensuring product availability across multiple sales channels.

Technology Landscape in the UAE Bottled Water Industry

Advanced Water Purification Technologies

Reverse osmosis (RO) technology underpins the majority of bottled water production in the UAE, driven by reliance on desalinated and groundwater sources. Leading producers are investing in energy-efficient RO systems and UV sterilisation units to reduce production costs. Nano-filtration is emerging as a premium-tier purification technology for mineral water variants.

Smart Packaging and Traceability

QR-code enabled packaging and RFID-based traceability systems are being adopted by premium brands to communicate water source, purification standards, and sustainability credentials. Smart labelling is gaining traction in modern trade and is expected to become increasingly prevalent in the coming years.

Automation and Industry 4.0 in Bottling

Leading manufacturers are deploying robotic bottling lines to enhance production efficiency and reduce labour costs. AI-powered vision systems are being integrated for real-time quality control, minimizing defects and improving consistency. Companies such as Agthia Group are investing in automated bottling infrastructure to strengthen operational capabilities.

IoT-Enabled Smart Dispensers and Vending

IoT-connected dispensing units provide real-time consumption data, predictive maintenance alerts, and remote refill scheduling. This technology is transforming traditional direct-sales models by enabling dynamic pricing and subscription-based analytics for more efficient operations.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Still |

62.8% |

2025 |

|

Distribution Channel |

Supermarkets/Hypermarkets |

38.6% |

2025 |

|

Region |

Dubai |

40.9% |

2025 |

By Product Type

To access detailed market analysis, Request Sample

Still water is the dominant product type, holding a 62.8% share of the UAE market in 2025. This dominance is structural driven by everyday hydration needs of the resident population and institutional procurement by offices, schools, and healthcare facilities.

By Distribution Channel

Supermarkets/hypermarkets represent the most significant distribution channel at 38.6% of 2025 revenue. Retailers such as Carrefour, LuLu Hypermarket, Spinneys, and Union Co-op provide nationwide reach and high shelf visibility. Promotional pricing and bulk-pack formats drive high-volume offtake through this channel.

Regional Market Insights

|

Region |

Market Share (2025) |

Est. CAGR (2026-34) |

Key Growth Drivers |

|

Dubai |

40.9% |

8.5% |

Tourism, hospitality, high-density residential, premium demand |

|

Abu Dhabi |

32.7% |

8.9% |

Government procurement, large population, industrial zones |

|

Sharjah |

16.4% |

7.8% |

Industrial workforce, growing residential, budget-conscious buyers |

|

Others |

10.0% |

7.2% |

Northern Emirates expansion, tourism in Ras Al Khaimah |

The UAE bottled water market is primarily concentrated across three emirates - Dubai, Abu Dhabi, and Sharjah - which collectively accounted for approximately 90% of national revenue in 2025. Each emirate presents a distinct demand profile shaped by population density, economic activity, and tourism intensity.

Dubai – 40.9% Market Share (2025)

Dubai is the UAE's largest bottled water market, generating approximately USD 659 Million in 2025. The emirate's over 19.6 million annual tourists drive outsized per-capita bottled water consumption, particularly in the premium still, sparkling, and mineral sub-categories. Over 800 hotel with140,000+ hotel rooms create substantial on-trade demand. Dubai's free zone industrial clusters and large expatriate workforce continue to sustain strong institutional demand, supporting steady market expansion over the forecast period.

Competitive Landscape

The UAE bottled water market is moderately fragmented, with the top five companies accounting for approximately 60-65% of combined revenue in 2025. International FMCG players compete alongside strong regional and UAE-origin brands. Competition is driven by pricing, distribution reach, brand equity, packaging innovation, and sustainability credentials.

|

Company Name |

Brand Name |

Market Position |

Competitive Strength |

|

Agthia Group PJSC |

Al Ain Water |

Market Leader |

Largest UAE-origin brand, extensive distribution, government contracts |

|

Masafi |

Masafi |

Market Leader |

Oldest UAE brand (1976), strong loyalty, nationwide penetration |

|

Nestlé |

Nestlé Pure Life |

Challenger |

Global brand equity, strong modern trade presence, premium packaging |

|

Danone |

Evian / Volvic |

Challenger |

Premium import brand, loyal hospitality and lifestyle consumer base |

|

PepsiCo, Inc. |

Aquafina |

Volume Player |

High-volume still water, competitive pricing, vending channel strength |

|

The Coca‑Cola Company |

Dasani |

Challenger |

Carbonated water leader, premium lifestyle positioning |

|

Our Oasis |

Oasis |

Niche Player |

Direct sales and office delivery specialist, 5-gallon dispenser leader |

Key Company Profiles

Agthia Group PJSC

Agthia Group PJSC is a leading food and beverage conglomerate headquartered in Abu Dhabi, UAE, and listed on the Abu Dhabi Securities Exchange. The company is a dominant player in the regional packaged food and water segment, with a strong presence across the UAE and broader GCC markets.

- Product & Platform Portfolio: Agthia’s water portfolio is led by Al Ain Water, offering a wide range of bottled water products catering to retail, institutional, and bulk consumption segments, with growing emphasis on premium and sustainable packaging formats.

- Recent Developments: In 2025, Agthia Group PJSC showcased its sustainability and product innovations at Gulfood 2025, highlighting its supply of Al Ain rPET water bottles and earning DNATA’s ‘Most Sustainable Supplier’ award.

- Strategic Focus: Agthia’s strategy focuses on capacity expansion, regional market growth, and sustainability innovation. The company is actively developing biodegradable bottle formats in line with UAE environmental regulations, while enhancing its position in the premium and export-oriented bottled water segments.

Masafi

Masafi is a leading UAE-based bottled water and beverages company, headquartered in Masafi, Ras Al Khaimah. Established in 1976, the company is renowned for its Masafi water brands and operates across retail, institutional, and export markets throughout the GCC.

- Product & Brand Portfolio: Masafi’s portfolio includes natural bottled water, mineral water, flavoured water, and ready-to-drink beverages, catering to both everyday consumption and premium segments. The company also produces private-label beverages for regional retail chains.

- Recent Developments: In 2025, Masafi Company LLC is celebrating Ramadan with special-edition packaging designed in collaboration with Emirati artist Mariam Abbas. The packaging, featured on Masafi water and tissue products, highlights UAE cultural heritage, incorporating iconic symbols such as Sheikh Zayed Mosque, the Together sculpture, and traditional water pitchers.

- Strategic Focus: Masafi’s strategy emphasizes sustainability through recyclable packaging, premiumization via new water variants, and market expansion across the GCC. The company focuses on maintaining strong brand recognition, enhancing product quality, and capturing growth in both retail and institutional channels.

Nestlé

Nestlé is a global leader in food and beverages, headquartered in Vevey, Switzerland. Founded in 1866, it operates across multiple segments including bottled water, dairy, nutrition, and coffee, with a presence in over 185 countries worldwide. In the UAE, Nestlé is a key player in the bottled water market through its Nestlé Pure Life brand.

- Product & Brand Portfolio: Nestlé’s UAE water portfolio is led by Nestlé Pure Life, offering purified and mineral water products across retail, institutional, and on-the-go channels. The brand includes standard bottled water, sparkling variants, and premium offerings designed to meet diverse consumer needs.

- Recent Developments: In 2021, Nestlé launched Egypt’s first 1.5 L water bottles made from 100% recycled plastics (rPET), reinforcing its global commitment to sustainable packaging. The bottles meet EU safety standards and undergo rigorous quality testing, as part of Nestlé’s $2 billion investment to expand food-grade recycled plastic usage worldwide.

- Strategic Focus: Nestlé’s strategy in the UAE emphasizes sustainability, premiumization, and market expansion. The company focuses on strengthening its brand presence, driving adoption of eco-friendly packaging, and leveraging retail and e-commerce channels to capture growth in both household and institutional segments.

Market Concentration Analysis

The UAE bottled water market exhibits moderate concentration, with the top 5 brands, collectively holding an estimated 60-65% of combined market revenue in 2025.

The market is gradually consolidating at the premium tier as leading players invest in brand differentiation, technology, and sustainability. Smaller local bottlers, particularly in the commodity still water segment, face margin compression from PET cost pressures and are likely acquisition targets for regional FMCG groups seeking distribution scale.

The flavored and functional water sub-segments remain highly fragmented, with no single brand commanding more than 15% category share in 2025, presenting both competitive intensity and opportunity for new entrants.

Investment & Growth Opportunities

Functional and Premium Water – High-Growth Sub-Segment

The functional water segment in the UAE is still in its early stages, with limited product offerings. Growth opportunities exist for brands introducing electrolyte-enhanced, alkaline, or vitamin-infused formulations, as competition remains relatively low, though early entry is critical before international players establish a strong presence.

Sustainable Packaging Technology

UAE government sustainability mandates and luxury hotel procurement standards are driving preference for rPET, glass, and biodegradable packaging. Investments in recyclable and carbon-neutral packaging offer a strategic opportunity for differentiation among ESG-conscious institutional buyers in the UAE.

Smart Vending and Office Water-as-a-Service

Dubai is on track to significantly expand its office space inventory. By the end of 2026, the total stock is expected to reach 9.7 million square metres, a sharp rise from the current 6.26 million square metres. This growth will be largely driven by the addition of 415,000 square metres of new office space over the next two years. The rise in office stock will drive increased demand for convenient, on-site water services.

Future Market Outlook (2026-2034)

The UAE bottled water market is positioned for sustained and structurally sound growth through 2034. The overall market is projected to expand from USD 1.61 Billion in 2025 to USD 3.51 Billion by 2034, at a CAGR of 8.26%. This trajectory is underpinned by a combination of macroeconomic resilience, tourism growth, population expansion, and category premiumization.

Premium and functional water segments are set to grow faster than the overall market, increasing their share of total market value over the coming decade. Direct-to-consumer and digital subscription channels will gain further traction as urban consumers increasingly prioritize convenience over traditional retail.

Technological integration will redefine production efficiency and consumer interaction: smart water dispensers, AI-driven inventory management, and blockchain-based quality traceability are expected to be mainstream by 2030. Regulatory pressure on single-use plastics will likely intensify post-2027, accelerating transition toward circular economy packaging models.

Research Methodology

Primary Research

Primary research involved structured interviews and surveys with key industry participants including bottled water manufacturers (10+ interviews), distribution channel managers, retail category heads, and institutional procurement officers. Interviews were conducted across Dubai, Abu Dhabi, and Sharjah between Q3 2024 and Q1 2025. Expert opinion was gathered from 5 UAE-based food and beverage industry consultants to validate market sizing assumptions.

Secondary Research

Secondary research encompassed analysis of published data from the UAE Ministry of Economy, Emirates Authority for Standardization and Metrology (ESMA), Dubai Statistics Centre, and Abu Dhabi Department of Economic Development. Trade databases including UN Comtrade (import-export volumes), company annual reports, investor presentations, and sector-specific industry publications were systematically reviewed.

Market Estimation and Forecasting Models

Market sizing employed a bottom-up approach, aggregating production volumes from licensed UAE bottled water manufacturers, reconciled against retail sales data and import statistics. The forecast model integrates regression analysis, CAGR extrapolation, and scenario-adjusted projections calibrated against GDP growth, population forecasts, and tourism arrival data from the UAE Ministry of Tourism. All estimates were validated through triangulation with three independent data sources.

UAE Bottled Water Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Still, Carbonated, Flavored, Mineral |

| Distribution Channels Covered | Supermarkets/Hypermarkets, Convenience Stores, Direct Sales, On-Trade, Others |

| Regions Covered | Dubai, Abu Dhabi, Sharjah, Others |

| Companies Covered | Agthia Group PJSC, Masafi, Nestlé, Danone, PepsiCo, Inc., The Coca‑Cola Company, Our Oasis, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the UAE Bottled Water Market Report

The UAE bottled water market was valued at USD 1.61 Billion in 2025 and is projected to reach USD 3.51 Billion by 2034, growing at a CAGR of 8.26%.

The market is projected to grow at a CAGR of 8.26% during the forecast period 2026-2034, driven by population growth, tourism, and premiumization trends.

Still water leads with a 62.8% market share in 2025, driven by daily hydration needs, institutional demand, and consumer distrust of tap water quality.

Dubai dominates with 40.9% market share in 2025, supported by its tourism base, hospitality sector density, and high-income residential population.

Supermarkets and hypermarkets lead with a 38.6% share in 2025, enabled by UAE's highly developed modern trade network and bulk purchasing convenience.

Flavored water is the fastest growing product type at an estimated 10.1% CAGR through 2034, driven by health-conscious youth demographics and functional beverage trends.

Leading companies include Agthia Group PJSC, Masafi, Nestlé, Danone, PepsiCo, Inc., The Coca-Cola Company, and Our Oasis.

Key drivers include extreme climate, rapid urbanisation, a high-volume tourism sector, growing health awareness, and the lack of natural freshwater sources.

Primary challenges include PET resin cost volatility, environmental regulations on single-use plastics, intense brand competition, and improving tap water infrastructure in some emirates.

E-commerce bottled water sales grew 28% year-on-year in 2024. Direct delivery subscriptions now represent 18.2% of total sales and are the fastest growing distribution channel at 10.8% CAGR.

High-growth opportunities exist in functional water innovation, sustainable packaging, smart vending infrastructure, and expansion into underpenetrated Northern Emirates and GCC export markets.

The UAE bottled water market is projected to reach USD 2.39 Billion by 2030, reflecting sustained double-digit sector expansion supported by tourism, population, and premiumization drivers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)