UAE Food Service Market Size, Share, Trends and Forecast by Type, Outlet, Location, and Region, 2026-2034

UAE Food Service Market Summary:

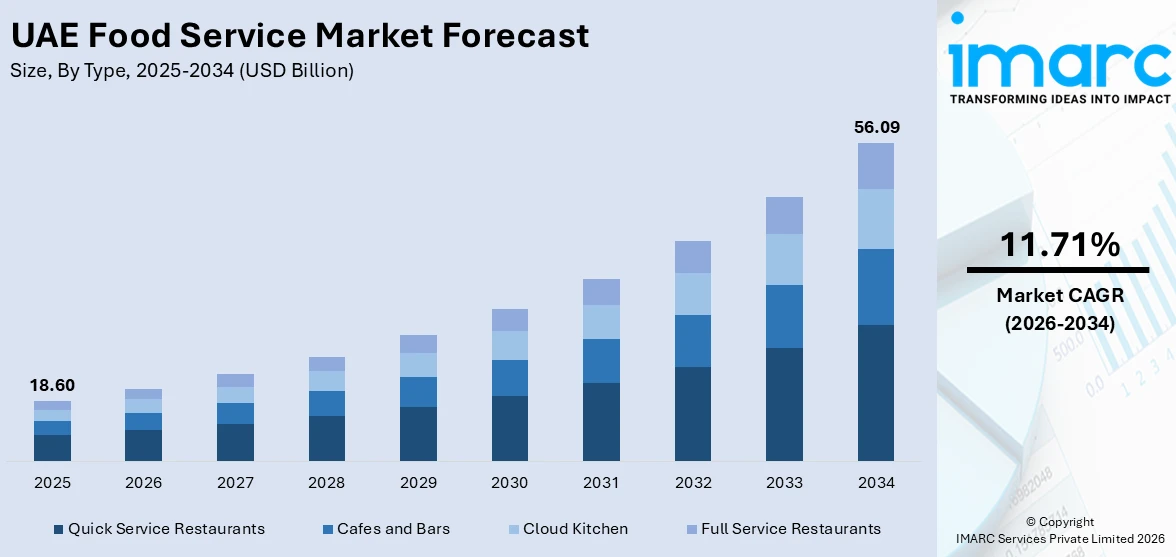

The UAE food service market size was valued at USD 18.60 Billion in 2025 and is projected to reach USD 56.09 Billion by 2034, growing at a compound annual growth rate of 11.71% from 2026-2034.

The UAE food service market is driven by a thriving tourism sector, a large expatriate population spanning over 200 nationalities, and consistently high consumer spending on dining and hospitality. Digital transformation across ordering, delivery, and payment channels has redefined how consumers engage with food service operators. Rapidly evolving health-consciousness, the proliferation of chained international brands, and government-backed tourism initiatives continue to accelerate the UAE food service market.

Key Takeaways and Insights:

- By Type: Quick service restaurants dominate the market with a share of 43.6% in 2025, owing to the fast-paced urban lifestyle, rising preference for affordable and convenient dining, and the strong footprint of global QSR brands across malls, airports, and business districts. Increasing digital food delivery adoption and menu diversification further reinforce this dominance.

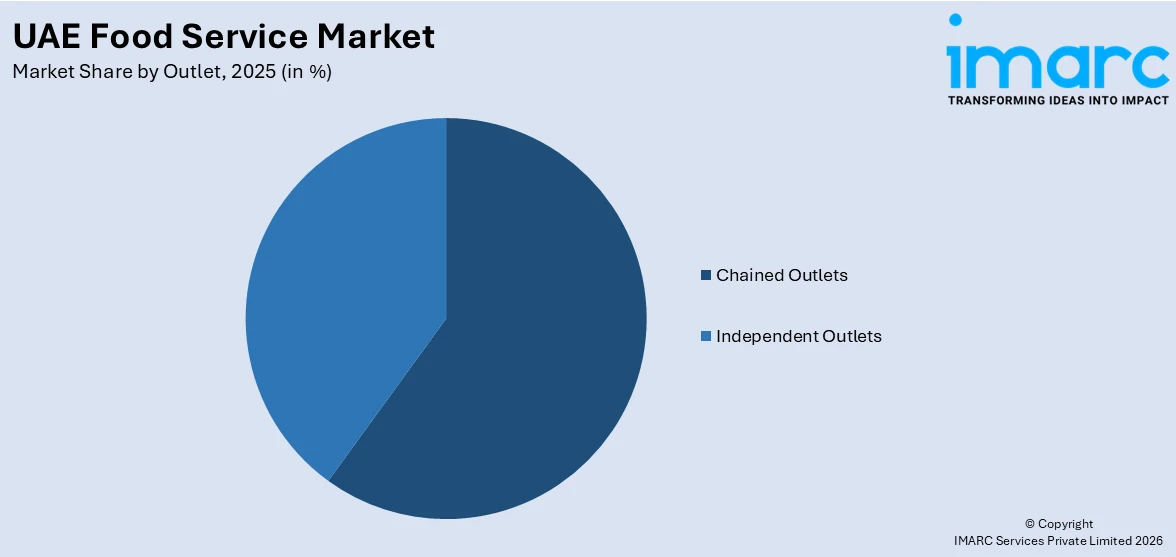

- By Outlet: Chained outlets lead the market with a share of 58.9% in 2025. This dominance is driven by the strong brand recognition of international and regional franchise operators, their standardized service quality, and their strategic placement in high-footfall retail and leisure environments across the UAE's key urban centres.

- By Location: Standalone represents the largest segment with a market share of 36.7% in 2025, reflecting the widespread preference for independent dining venues that offer greater flexibility in concept, cuisine, and customer experience, particularly in residential and suburban zones where prime rental costs are comparatively lower.

- By Region: Dubai represents the largest region with 39.5% share in 2025, driven by its unparalleled status as a global tourism and business hub, dense concentration of food outlets, diverse multicultural resident and visitor base, and sustained government investment in hospitality and lifestyle infrastructure.

- Key Players: Key players drive the UAE food service market by expanding brand portfolios, investing in digital ordering and delivery infrastructure, and diversifying menus to cater to the country's multicultural population. Their focus on franchise partnerships, loyalty programmes, and strategic location expansion enhances market penetration and accelerates adoption across urban and suburban consumer segments.

To get more information on this market Request Sample

The food service market in the UAE has emerged as an industry that is not only highly dynamic but is also rapidly growing as an aspect of the overall hospitality market of the country. The market has been driven by the young, urban, cosmopolitan, and affluent population of the UAE, with a high willingness to eat out as often as possible. The multicultural base of the population of the UAE, comprising expatriates from different countries of South Asia, East Asia, the Middle East, as well as the West, has created a market that is highly diverse in the types of cuisines that are in demand. The Dubai Tourism Strategy 2031, as well as the Abu Dhabi hospitality development programmes, have created an environment that is conducive to the growth of the market, with the proliferation of food delivery apps, cloud kitchens, as well as AI restaurant management tools, adding a new dimension of competition to the market.

UAE Food Service Market Trends:

Rising Adoption of Digital Ordering and Delivery Platforms

The rapid expansion of food delivery platforms has fundamentally reshaped consumer engagement with food service operators across the UAE. Driven by high smartphone penetration, convenience-oriented lifestyles, and a tech-savvy resident and tourist population, mobile-first ordering has become the default mode of food consumption for a growing share of consumers. Restaurants are investing in data analytics, contactless payment systems, and loyalty applications to enhance customer retention and operational efficiency. This digital transition is enabling smaller operators to compete more effectively with larger chains through aggregator platforms, broadening market participation across the sector.

Growth of Cloud Kitchens and Hybrid Foodservice Models

Cloud kitchens, delivery-only facilities that eliminate front-of-house costs, have gained significant traction in the UAE, emerging as a capital-efficient model that enables food service operators to test new culinary concepts, expand geographic reach, and optimise margins without the financial commitment of a traditional restaurant setup. The emergence of hybrid models that combine conventional dining with ghost kitchen operations reflects the sector's agility in responding to evolving consumer preferences for both dine-in and delivery occasions. This structural shift is attracting entrepreneurial operators and established brands alike, reshaping the competitive dynamics of the broader food service landscape.

Increasing Demand for Health-Conscious and Plant-Based Dining

Consumer health awareness is reshaping menu strategies across the UAE food service sector. A growing cohort of residents and tourists is seeking organic, plant-based, allergen-friendly, and nutritionally transparent food options, driven by rising wellness consciousness and greater dietary awareness across the country's diverse population. This trend is compelling established operators to reformulate menus and introduce dedicated wellness-focused categories that balance nutritional integrity with culinary appeal. The integration of health-forward dining concepts into both premium and casual formats signals a structural shift in consumer expectations that is expected to sustain demand for sustainable and plant-based offerings throughout the forecast period.

Market Outlook 2026-2034:

The UAE’s food service industry is on the cusp of a sustained period of growth, driven by an increasing trend in tourism inflows, urbanisation, and digitalisation in the modes of service delivery. In addition, changing consumer profiles are shifting towards experiences that provide quality, speed, and convenience. This is expected to result in an increasing average transaction value as consumers opt for healthy and premium experiences. Moreover, the support provided by the UAE’s government to the hospitality industry and the infrastructure created in Dubai, Abu Dhabi, and Sharjah are expected to provide additional growth opportunities. In addition, the sustained growth of international franchise brands and the emergence of innovative local concepts are expected to continue providing competitive vigor and ensure sustained growth in the industry over the forecast period. The market generated a revenue of USD 18.60 Billion in 2025 and is projected to reach a revenue of USD 56.09 Billion by 2034, growing at a compound annual growth rate of 11.71% from 2026-2034.

UAE Food Service Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Type |

Quick Service Restaurants |

43.6% |

|

Outlet |

Chained Outlets |

58.9% |

|

Location |

Standalone |

36.7% |

|

Region |

Dubai |

39.5% |

Type Insights:

- Cafes and Bars

- By Cuisine

- Bars and Pubs

- Cafes

- Juice/Smoothie/Desserts Bars

- Specialist Coffee and Tea Shops

- By Cuisine

- Cloud Kitchen

- Full Service Restaurants

- By Cuisine

- Asia

- European

- Latin American

- Middle Eastern

- North American

- Others

- By Cuisine

- Quick Service Restaurants

- Bakeries

- Burger

- Ice Cream

- Meat-based Cuisines

- Pizza

- Others

Quick service restaurants dominate with a market share of 43.6% of the total UAE food service market in 2025.

Quick service restaurants hold the leading position within the UAE food service market, driven primarily by the country's fast-paced urban lifestyle, high concentration of working professionals, and the persistent demand for time-efficient yet satisfying meal options. The widespread presence of internationally recognised QSR brands across shopping malls, transportation hubs, office districts, and leisure destinations ensures consistent footfall and repeat custom. Digital ordering via mobile applications has further amplified QSR accessibility, enabling operators to capture both dine-in and delivery revenue streams with minimal friction. The model's inherent scalability and relatively lower operational complexity compared to full-service dining continue to attract franchise investment.

The appeal of quick service restaurants is further reinforced by the UAE's diverse expatriate demographic, which generates demand for a broad spectrum of cuisines within a quick-service format — from American-style burgers and pizza to Middle Eastern wraps and South Asian snacks. The country's openness to international culinary concepts continues to attract global QSR brands seeking market entry, reflecting the robust commercial opportunity presented by the UAE's affluent, food-savvy consumer base. The combination of brand diversity, digital delivery integration, and consumer preference for convenience and value positions quick service restaurants as the enduring anchor of the UAE food service landscape, with ongoing franchise expansion and menu innovation expected to sustain the segment's leadership throughout the forecast period.

Outlet Insights:

Access the comprehensive market breakdown Request Sample

- Chained Outlets

- Independent Outlets

Chained outlets lead with a share of 58.9% of the total UAE food service market in 2025.

Chained outlets command the dominant share of the UAE food service market owing to the country's strong affinity for internationally recognised food brands, the operational advantages of standardised supply chains, and the brand assurance that resonates particularly with younger and expatriate consumer segments. The strategic clustering of chained operators within high-footfall environments, including major shopping malls, hotel complexes, and transport terminals, maximises visibility and accessibility. Franchise expansion continues at pace, with operators leveraging established marketing budgets, loyalty programmes, and centralised menu innovation to maintain competitive advantage. The UAE's business-friendly regulatory framework and its status as a Middle East franchise hub amplify the attractiveness of chained formats.

The resilience of chained outlets is further demonstrated by their capacity to integrate digital ordering and delivery systems at scale, enabling operators to serve both dine-in and off-premise demand through unified technology platforms. International chains, alongside established regional operators, maintain extensive multi-emirate footprints anchored by strong brand recognition and standardised service quality that resonate with the UAE's diverse consumer base. Franchise groups continue to invest in multi-site expansion strategies, leveraging economies of scale and centralised operational infrastructure to sustain competitive advantage across high-footfall retail, leisure, and hospitality environments. The consistent delivery of brand promise across multiple touchpoints deepens consumer loyalty and reinforces chained outlets' structural dominance throughout the forecast period.

Location Insights:

- Leisure

- Lodging

- Retail

- Standalone

- Travel

Standalone exhibits a clear dominance with a 36.7% share of the total UAE food service market in 2025.

Standalone food service locations account for the largest share of the UAE market, benefitting from lower occupancy costs compared to premium mall or hotel-integrated sites, as well as greater flexibility in outlet design, kitchen capacity, and brand identity. This format is particularly prevalent in residential neighbourhoods, suburban commercial zones, and community hubs where operators can tailor their offerings to local demographics without the constraints of landlord-imposed operating hours or F&B category restrictions. Standalone venues are also better positioned to accommodate cloud kitchen integration, offering dedicated space for delivery order preparation without disrupting dine-in operations.

Independent operators who favour standalone locations are able to cultivate a distinctive identity and build loyal community-level customer bases, a competitive advantage that differentiates them from the standardised experience offered by chained formats in retail environments. The format also accommodates a wider range of cuisine types and service styles, from casual neighbourhood cafes to destination fine-dining restaurants. As urban development spreads across previously underserved areas of Dubai and Abu Dhabi, guided by planning frameworks such as the Dubai 2040 Urban Master Plan, standalone operators are well-positioned to capitalise on emerging residential clusters and growing suburban consumer demand.

Regional Insights:

- Dubai

- Abu Dhabi

- Sharjah

- Others

Dubai represents the leading segment with a 39.5% share of the total UAE food service market in 2025.

Dubai's commanding position in the UAE food service market stems from its unrivalled global standing as a tourism, business, and lifestyle destination. The emirate's status as one of the world's most visited cities generates exceptional and diversified demand for all food service formats, from fast-casual and quick-service outlets to premium experiential and fine-dining concepts. This sustained tourism momentum, combined with a large and affluent resident expatriate community, ensures consistent footfall across a broad spectrum of dining environments. Dubai's expansive retail and leisure infrastructure, encompassing world-class shopping malls, entertainment complexes, and hospitality venues, provides a continuously growing base of high-footfall locations that attract both international franchise operators and independent culinary entrepreneurs seeking premium market positioning.

The emirate's progressive regulatory environment, the Dubai Department of Economy and Tourism's active promotion of the hospitality sector, and the city's strategic position as a global transit hub further amplify food service market activity. Government-led initiatives including the Dubai 2040 Urban Master Plan and the Dubai Tourism Strategy 2031 are generating sustained long-term infrastructure investment that creates favourable conditions for food service operators across all segments and formats. The rapid penetration of digital food delivery platforms has established Dubai as the primary hub of online food ordering activity in the UAE, driven by the city's high smartphone adoption, convenience-oriented consumer culture, and density of restaurant options. The combination of institutional support, elevated consumer spending power, and extraordinary cultural diversity ensures Dubai remains the dominant engine of the UAE food service market across the forecast period.

Market Dynamics:

Growth Drivers:

Why is the UAE Food Service Market Growing?

Expanding Tourism and Hospitality Sector

The UAE's sustained investment in tourism infrastructure continues to be a foundational growth driver for the food service sector. As a global destination attracting tens of millions of international visitors annually, the country's seven emirates, led by Dubai and Abu Dhabi, offer an unparalleled mix of luxury resorts, cultural attractions, retail destinations, and entertainment venues that collectively generate immense demand for diverse dining experiences. Visitors from Europe, Asia, and North America seek both familiar global brands and authentic regional cuisine, creating a structurally broad market for food service operators across every price point and format. Government-backed programmes such as the Dubai Tourism Strategy 2031 and the National Tourism Charter under the UAE Tourism Strategy are systematically enhancing the country's hospitality infrastructure, reinforcing long-term demand for premium and casual dining alike. This tourism-driven consumption pattern ensures that food service operators enjoy a consistently replenishing customer base that is not reliant solely on the resident population, underpinning market resilience and growth throughout the forecast period.

High Disposable Incomes and Affluent Expatriate Population

The UAE's high per-capita income levels and the presence of a large, professionally employed expatriate community create a consumer base with both the financial capacity and the cultural inclination to dine out frequently. Expatriates from South Asia, East Asia, the Arab world, and Western markets bring diverse culinary preferences that drive demand for a wide range of cuisine types and food service formats, encouraging operators to constantly innovate and broaden their offerings. As urban professionals navigate busy work schedules, demand for convenient, high-quality dining options, across both quick-service and full-service categories, remains structurally elevated. Rising dual-income households further amplify per-occasion spending on dining experiences. The country's exceptionally high workforce participation rate, driven by a predominantly working-age adult population, underpins consistent and durable consumer engagement with food service operators across both functional and leisure dining occasions, providing a growing and stable customer base that supports sustained market expansion throughout the forecast period.

Digital Transformation and Food Delivery Platform Proliferation

The rapid digitisation of the UAE food service sector has unlocked new revenue streams, expanded geographic reach, and fundamentally altered consumer purchasing behaviour. The country's exceptionally high smartphone penetration and advanced digital infrastructure have made mobile-first food ordering the default mode for a growing share of consumers. Food delivery platforms have emerged as powerful distribution channels, enabling operators to reach customers across all seven emirates without proportionally increasing physical outlet counts. Restaurants are investing in AI-driven demand forecasting, digital loyalty programmes, contactless payment systems, and personalised menu recommendation engines to deepen customer engagement and improve operational efficiency. In April 2024, Careem launched Careem Food and Careem Pay in Abu Dhabi, expanding convenient meal ordering access to a broader consumer base. The emergence of cloud kitchens as delivery-optimised production facilities further enhances the economics of digital food service, allowing operators to test new cuisine concepts and capture delivery demand with minimal capital expenditure, driving structural expansion of the market's addressable customer base.

Market Restraints:

What Challenges the UAE Food Service Market is Facing?

High Operational Costs and Margin Compression

Operating within the UAE food service sector, particularly in prime locations across Dubai and Abu Dhabi, involves significant financial exposure to elevated rental costs, high labour expenses attributable to expatriate workforce dependency, and substantial licensing and compliance fees. Dubai's rental market recorded a 10% increase in commercial rents during the first half of 2024 alone, directly compressing profit margins for operators in malls, tourist zones, and retail districts. These structural cost pressures are particularly acute for independent and smaller-scale operators who lack the economies of scale available to large franchise groups. Food import dependency, given the UAE's limited domestic agricultural capacity, further compounds raw material cost volatility, especially during periods of global supply chain disruption or currency fluctuation. Sustaining profitability in this high-cost environment requires constant operational optimisation, menu engineering, and strategic sourcing, representing a persistent structural challenge for market participants.

Labor Shortages and Workforce Retention Challenges

The UAE food service sector is confronted by sustained difficulties in attracting and retaining qualified culinary and service staff. The sector's heavy reliance on expatriate labour makes it vulnerable to immigration policy changes, visa processing delays, and competitive pressure from higher-paying industries such as technology and finance, which have driven up wage expectations for customer-facing roles. Emiratisation mandates require operators to balance local hiring requirements with available skill sets, extending onboarding timelines and increasing training costs. High employee turnover, driven by living cost pressures, salary stagnation concerns, and sector-wide mobility, disrupts service consistency and elevates recruitment expenditure, creating recurring operational inefficiencies that constrain profitability and service quality across food service establishments of all scales.

Intense Market Competition and Consumer Preference Complexity

The UAE food service market is characterised by intense competitive density, with food establishments competing for consumer attention across a highly fragmented landscape where no single player holds a dominant value share. International franchise giants, regional chains, and agile independent operators all compete simultaneously for the same consumer base, creating price pressure and accelerating the requirement for continuous menu innovation, branding investment, and service differentiation. The extraordinary diversity of the UAE's consumer base — spanning more than 200 nationalities — demands that operators cater to a wide and shifting range of dietary preferences, cultural sensitivities, and price expectations, adding complexity to menu planning and supply chain management that smaller operators may find particularly challenging to navigate profitably.

Competitive Landscape:

The UAE food service industry has witnessed a highly fragmented and competitive environment, with no single company holding a dominant value share in the industry. The industry has witnessed the interplay of traditional global franchise brands such as Americana Restaurants International, M.H. Alshaya, Apparel Group, and various regional brands and independent foodservice concepts. The players in the industry are focusing on the development of digital technologies, localising menus, and delivering premium foodservice concepts to capture the resident and tourist populations in the region. Differentiation in the competitive environment is being pursued through loyalty schemes, artificial intelligence-powered personalisation, franchise relationships, and the development of suburban markets, as the industry continues to evolve in the UAE.

Recent Developments:

- In September 2025, the Dubai Corporation for Consumer Protection and Fair Trade (DCCPFT), a body under the Dubai Department of Economy and Tourism, established a dedicated working group bringing together public and private sector stakeholders to strengthen oversight and standards within the city's online food delivery sector, signalling increasing institutional focus on the digital food service channel.

- In July 2025, Little Caesars opened its inaugural restaurant in the UAE in Dubai, offering its classic pizza menu including pepperoni, veggie, and cheese varieties, marking a significant milestone in the global chain's international expansion strategy and reflecting continued international brand interest in the UAE food service market.

- In February 2025, Chipotle Mexican Grill launched its first UAE restaurant at The Beach, Jumeirah Beach Residence in Dubai, in partnership with Alshaya Group as part of a broader Middle East expansion plan, with an additional location at Dubai Hills Mall announced soon after, underscoring the enduring attractiveness of the UAE market for international QSR entrants.

UAE Food Service Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered |

|

| Outlets Covered | Chained Outlets, Independent Outlets |

| Locations Covered | Leisure, Lodging, Retail, Standalone, Travel |

| Regions Covered | Dubai, Abu Dhabi, Sharjah, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the UAE Food Service Market Report

The UAE food service market size was valued at USD 18.60 Billion in 2025.

The UAE food service market is expected to grow at a compound annual growth rate of 11.71% from 2026-2034 to reach USD 56.09 Billion by 2034.

Quick service restaurants dominated the market with a share of 43.6%, driven by strong demand for fast, affordable, and convenient dining across the UAE's urban, tourist, and transit-oriented consumer base.

Key factors driving the UAE food service market include a booming tourism sector, high disposable incomes among a large expatriate population, rapid expansion of digital food delivery platforms, and strong government support for hospitality infrastructure and innovation.

Major challenges include high operational and rental costs in prime locations, labour shortages and elevated staff turnover driven by competition for expatriate workers, heavy dependence on food imports creating supply chain vulnerability, and intense competitive density across a highly fragmented market with over 15,500 registered food establishments.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade