UAE Furniture Market Size, Share, Trends and Forecast by Product, Material, End Use, and Region, 2026-2034

UAE Furniture Market Size, Share, Trends & Forecast (2026-2034)

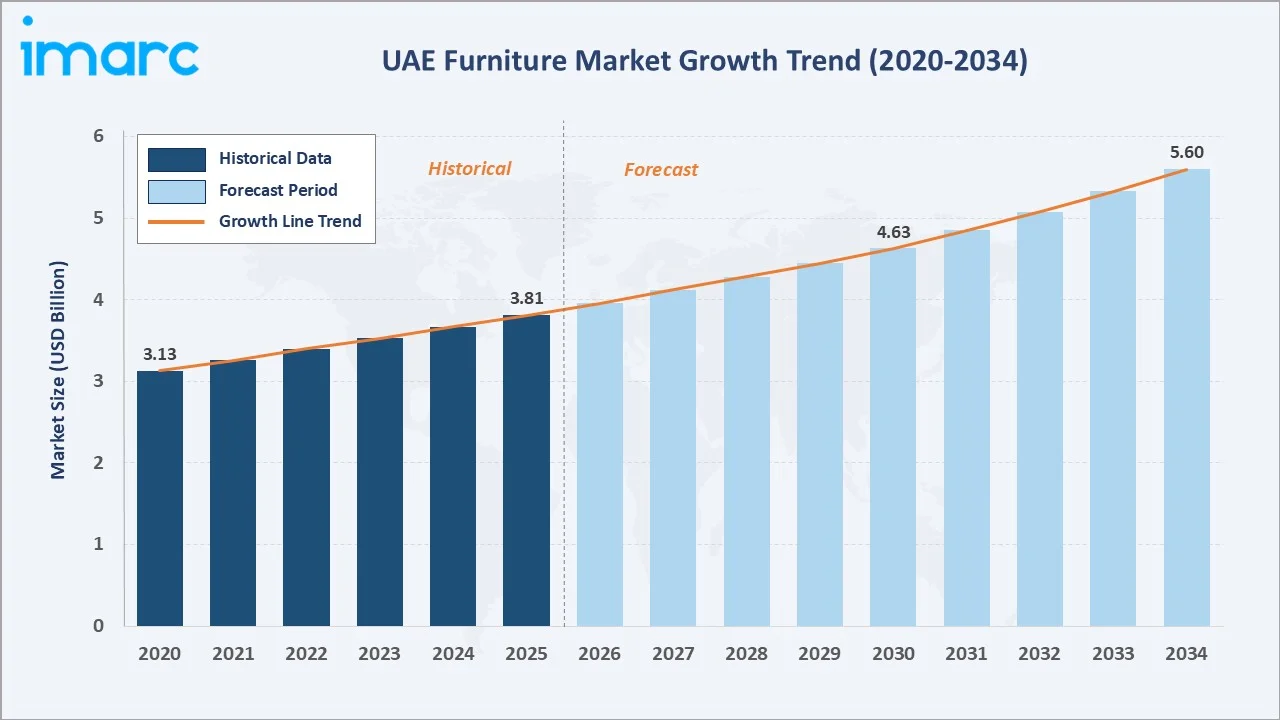

The UAE furniture market size reached USD 3.81 Billion in 2025 and is projected to reach USD 5.60 Billion by 2034, exhibiting a CAGR of 4.01% during 2026-2034. Rapid urbanization, booming real estate activity, a thriving tourism and hospitality pipeline, a large affluent expatriate base, and rising demand for sustainable and smart furniture are the primary forces driving growth.

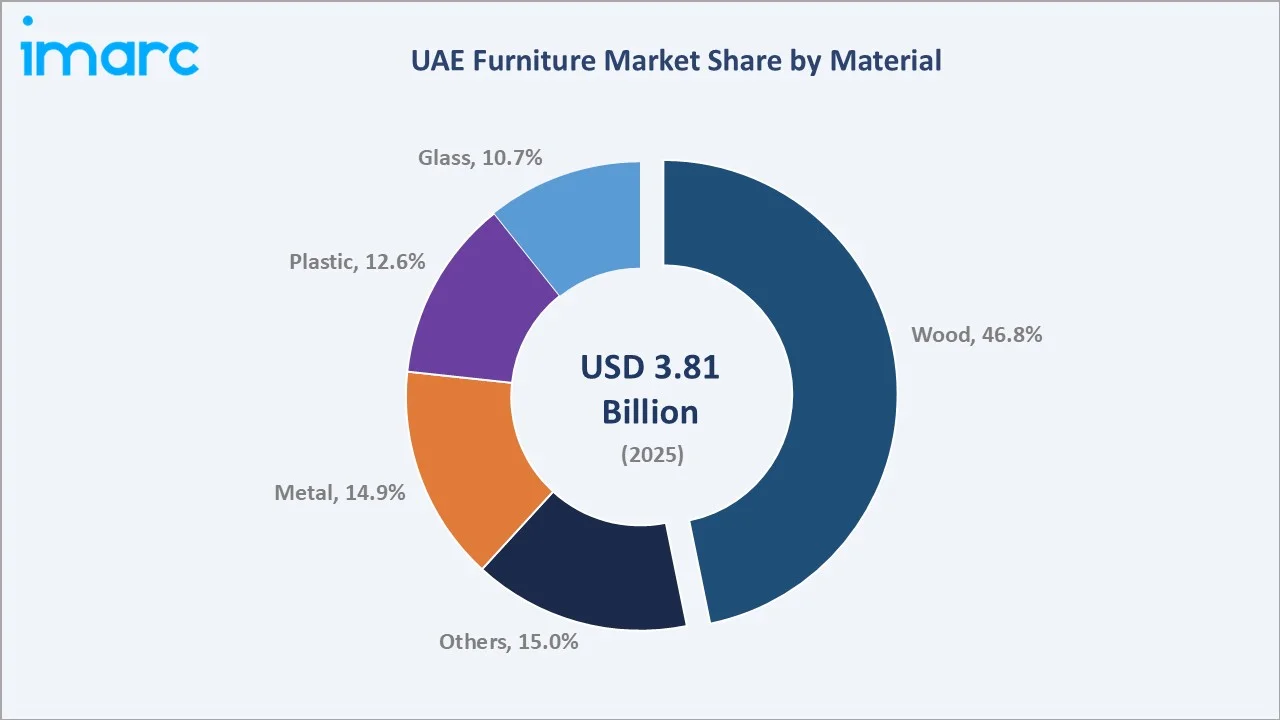

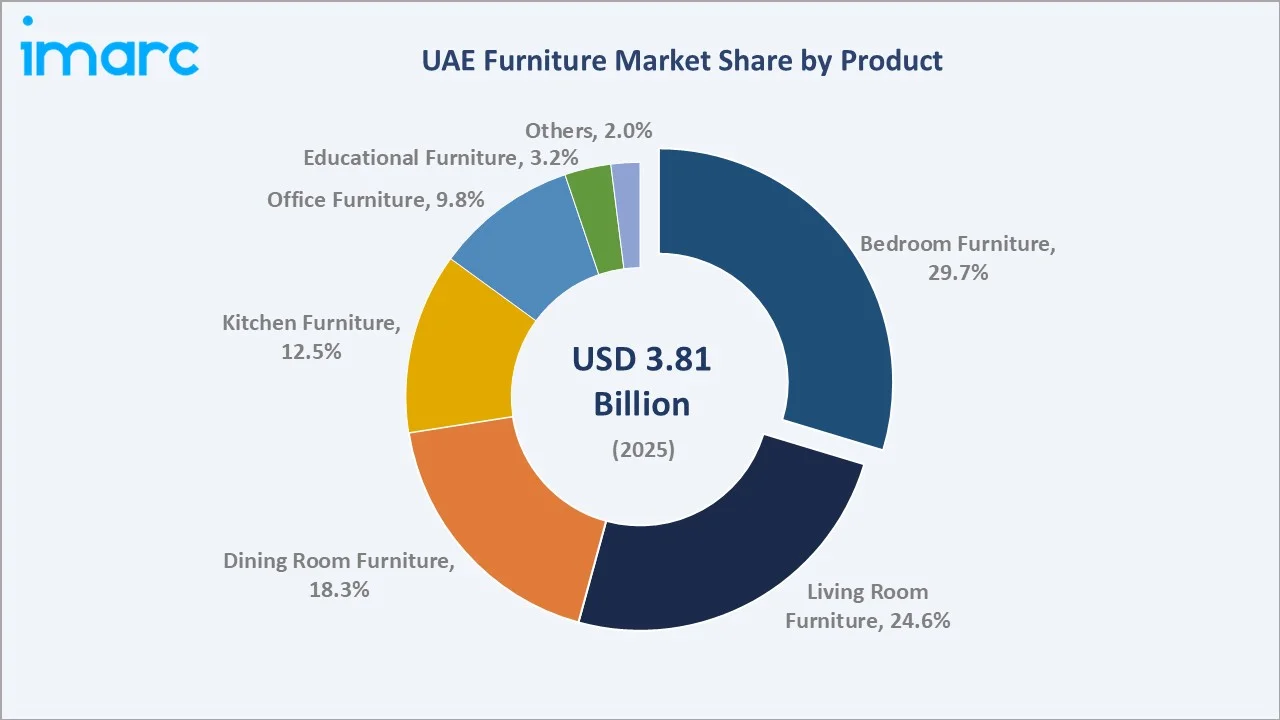

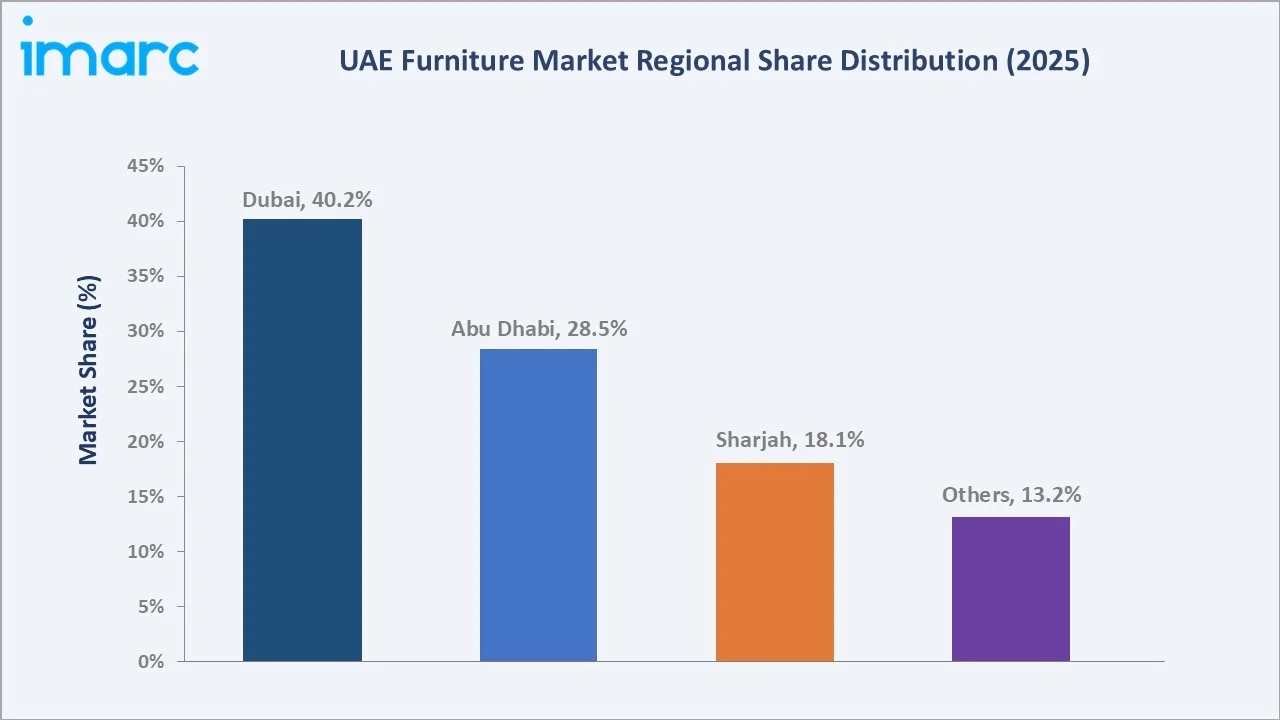

Wood leads materials with 46.8% share in 2025, while bedroom furniture dominates products at 29.7%. Dubai commands a 40.2% regional share, reflecting its status as the UAE's primary residential, commercial, and hospitality hub.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.81 Billion |

|

Forecast Market Size (2034) |

USD 5.60 Billion |

|

CAGR (2026-2034) |

4.01% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Dubai (40.2% share, 2025) |

|

Second Largest Region |

Abu Dhabi (28.5% share, 2025) |

|

Leading Material |

Wood (46.8%, 2025) |

|

Leading Product |

Bedroom Furniture (29.7%, 2025) |

The UAE furniture market growth trajectory from 2020 through 2034, with historical expansion to USD 3.81 Billion in 2025, reflects consistent residential and hospitality demand, while the forecast to USD 5.60 Billion captures accelerating urbanization, tourism expansion, and sustained expatriate-driven household formation across the emirates.

To get more information on this market, Request Sample

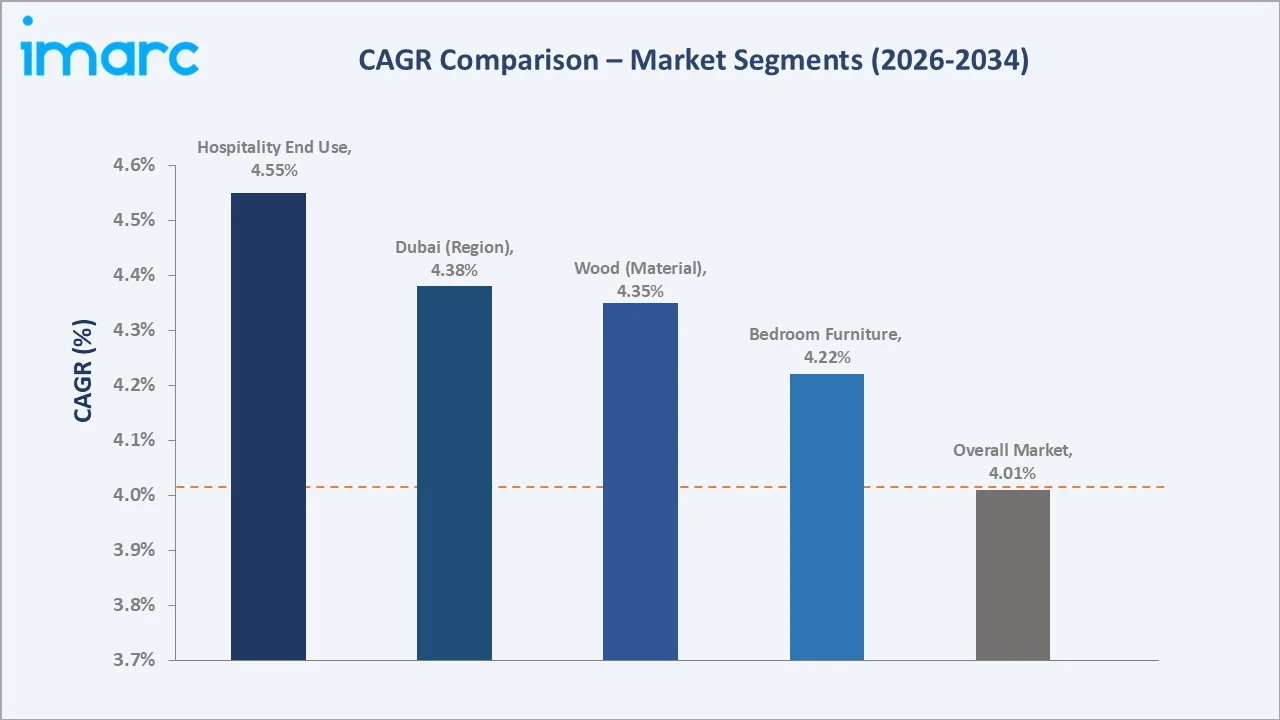

The CAGR trajectories across key material, product, and regional sub-segments, with hospitality end use at ~4.55% CAGR and Dubai at ~4.38% CAGR, are the fastest-growing categories within the UAE furniture industry analysis through 2034.

Executive Summary

The UAE furniture market is on a sustained growth trajectory from USD 3.81 Billion in 2025 to USD 5.60 Billion by 2034. Furniture, an essential consumer and commercial product deployed across residential units, hotels, offices, and healthcare facilities, benefits from steady household formation and hospitality expansion across the emirates.

Wood dominates the material mix at 46.8% in 2025, owing to its timeless aesthetic appeal, durability, and versatility across traditional and contemporary designs.

Bedroom furniture leads products at 29.7% in 2025, reflecting residential real estate turnover and consumer emphasis on premium private spaces.

Dubai dominates regionally at 40.2% in 2025, supported by record residential handovers, dense high-net-worth concentration, and an expansive hospitality pipeline. Abu Dhabi (28.5%) and Sharjah (18.1%) contribute meaningfully through government housing initiatives, industrial diversification, and comparatively affordable residential supply across the northern emirates.

Key Market Insights

|

Insight |

Data |

|

Largest Material |

Wood – 46.8% share (2025) |

|

Leading Product |

Bedroom Furniture – 29.7% share (2025) |

|

Leading Region |

Dubai – 40.2% revenue share (2025) |

|

Second Largest Region |

Abu Dhabi – 28.5% revenue share (2025) |

|

Top Companies |

Al-Futtaim, Landmark Group, Pan Home, 2XL Home, THE One UAE, Danube Group, Western Furniture |

Key analytical observations expanding on the above data:

- Wood, with 46.8% in 2025, dominates because it aligns with multicultural consumer preferences, from classic Arabic-inspired interiors to Scandinavian minimalism, while FSC-certified and engineered wood panels satisfy tightening green building norms.

- Bedroom furniture, at 29.7% in 2025, leads because residential handovers across Dubai, Abu Dhabi, and Sharjah continuously drive demand for beds, wardrobes, and storage systems, reinforced by growing cultural emphasis on sleep wellness and bespoke interiors.

- Dubai's 40.2% dominance reflects record housing turnover, the densest high-net-worth population in the UAE, and a continuously expanding hospitality pipeline in Dubai Marina, Downtown Dubai, and Palm Jumeirah requiring large-scale commercial procurement.

- Abu Dhabi, with 28.5% in 2025, benefits from large government housing benefit programs, Saadiyat and Yas Island tourism developments, and rising demand from institutional and healthcare procurement aligned with Vision 2030 diversification.

UAE Furniture Market Overview

Furniture, in the UAE, spans residential, commercial, hospitality, and institutional categories, encompassing bedroom, living room, dining, kitchen, office, and educational product lines manufactured from wood, metal, plastic, and glass. Products range from mass-market configurations to bespoke luxury collections tailored to the UAE's highly diverse expatriate population.

The ecosystem integrates raw material suppliers, domestic and international manufacturers, design houses, importers and distributors, omnichannel retailers, logistics and warehousing providers, fit-out contractors, and end-use segments spanning residential, commercial, hospitality, and healthcare, underpinned by regulators, sustainability councils, and design hubs.

Market Dynamics

To evaluate market opportunities, Request Sample

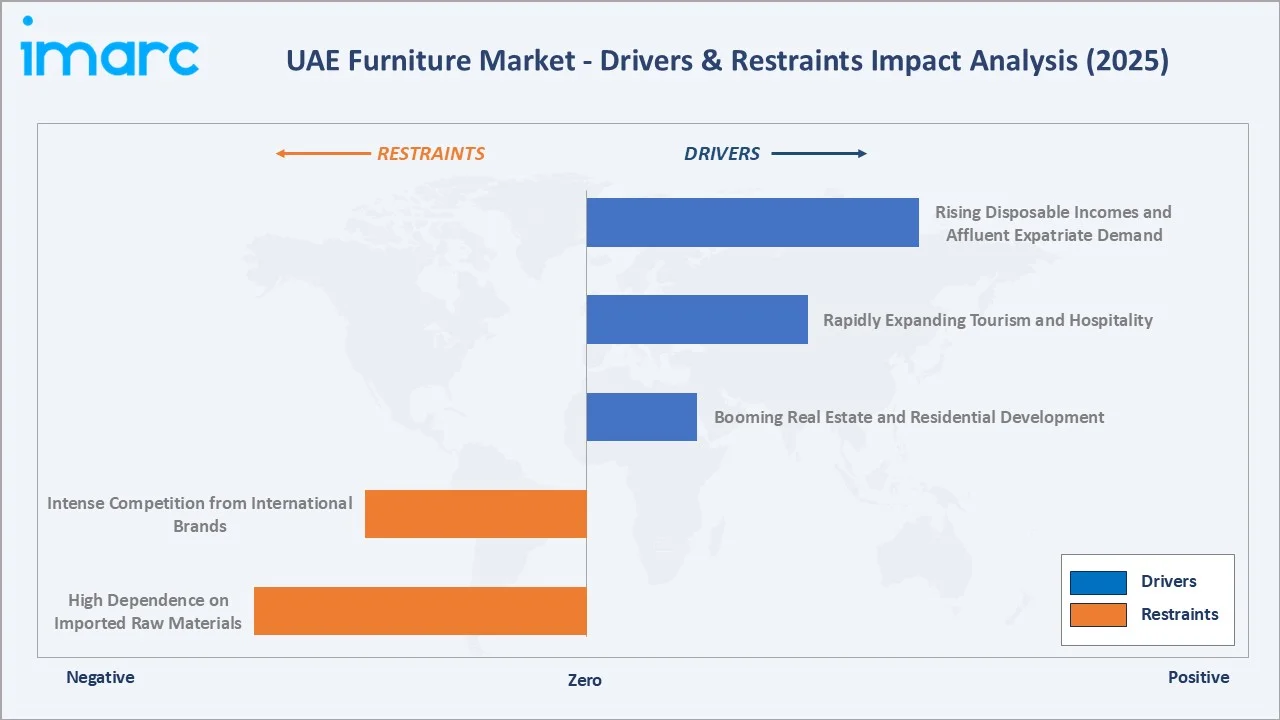

Market Drivers

- Booming Real Estate and Residential Development: Dubai's record real estate transactions, the golden visa program, and large-scale Emirati housing initiatives are triggering simultaneous furnishing requirements across primary, secondary, and rental residences UAE-wide. In 2024, the total value of real estate transactions reached an all-time high of AED 760.99 billion, reflecting a 20.4% year-on-year increase.

- Rapidly Expanding Tourism and Hospitality: Ongoing luxury and upper-upscale hotel openings in Dubai, Abu Dhabi, and Ras Al Khaimah, combined with Dubai's MICE leadership, are generating sustained commercial furniture procurement across guest rooms, lobbies, and event venues. The UAE's 51-hotel pipeline by 2026 arrives during a global period of supply-demand imbalance, positioning the market for 8-12% rate compression by 2027-2028.

- Rising Disposable Incomes and Affluent Expatriate Demand: A multicultural expatriate community from over 200 nationalities, rising per-capita incomes, and cultural emphasis on well-appointed interiors are elevating per-household furniture spending across premium and mid-market segments.

Market Restraints

- High Dependence on Imported Raw Materials: Structural reliance on imported timber and engineered wood panels exposes manufacturers to freight cost escalation, currency fluctuations, and global supply disruptions that erode gross margins on wood-intensive product lines.

- Intense Competition from International Brands: Established global retailers benefit from supply chain scale, design leadership, and brand equity that enable aggressive pricing, compressing margins for domestic manufacturers and smaller regional players competing on similar assortments.

Market Opportunities

- Hospitality Pipeline Expansion: The UAE's pipeline of luxury and lifestyle hotel openings, particularly across Dubai and Ras Al Khaimah, is creating large-scale opportunities for bespoke contract furniture providers to supply branded, design-forward solutions with premium pricing.

- 'Make it in the Emirates' Localization: Government-backed industrial localization initiatives are encouraging domestic manufacturing scale-up, unlocking opportunities for investors building wood-processing, metal-fabrication, and upholstery capabilities within UAE free zones and industrial cities.

Market Challenges

- Economic Sensitivity to Expatriate Flows: The market's heavy reliance on transient expatriate households creates inherent volatility, as geopolitical tensions, oil price swings, or employment disruptions can rapidly reduce household formation rates and furniture spending.

- Sustainability Compliance and Certification Costs: Tightening Dubai Municipality green procurement norms and Estidama standards impose FSC, LEED, and low-VOC certification costs on manufacturers, challenging smaller players lacking capital for compliance-ready product lines.

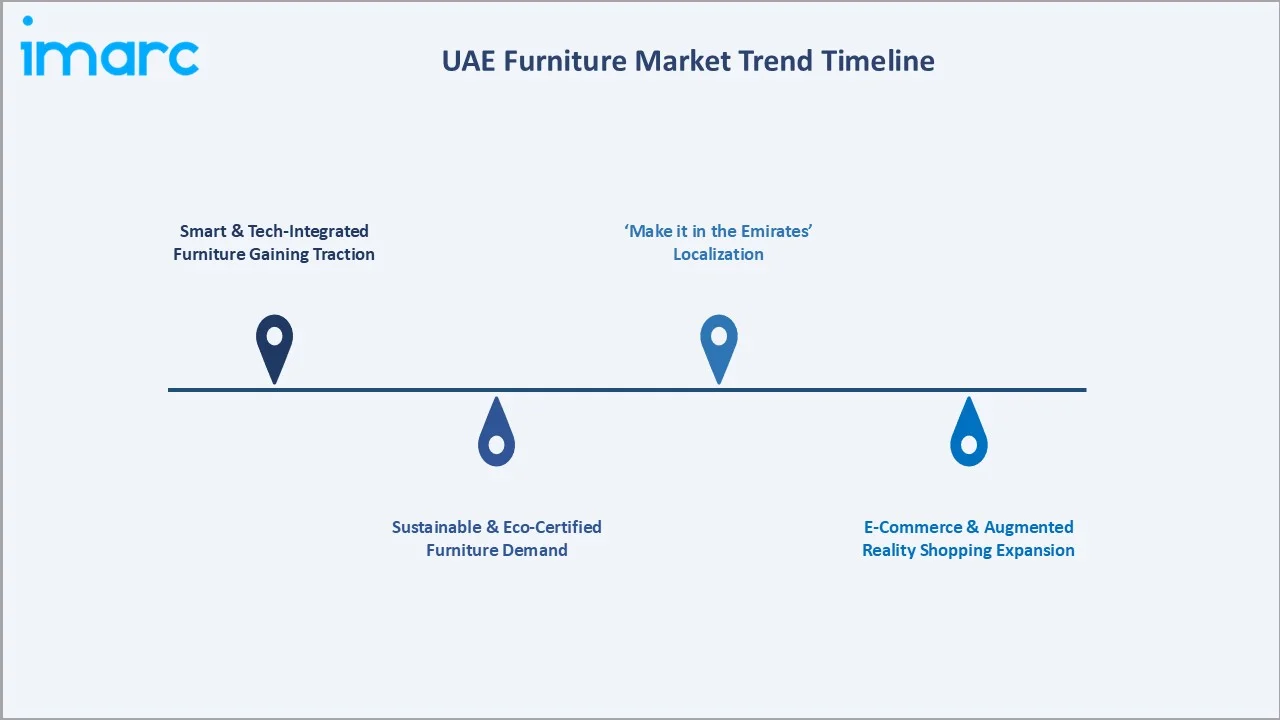

Emerging Market Trends

1. Smart and Tech-Integrated Furniture Gaining Traction

Smart home integration is reshaping UAE furniture preferences as consumers demand pieces that complement connected living ecosystems. Wireless charging pads, IoT lighting controls, motorized mechanisms, and voice-activation compatibility are gaining ground, particularly in premium residential developments across Dubai and Abu Dhabi.

2. Sustainable and Eco-Certified Furniture Demand

Sustainability is a defining trend, driven by consumer awareness and mandatory green building standards. FSC-certified wood, low-VOC coatings, and recycled materials are specified across residential and commercial segments, supported by Dubai Municipality mandates and the UAE Net Zero 2050 Strategy.

3. E-Commerce and Augmented Reality Shopping Expansion

Digital retail is transforming furniture discovery and purchase. Online platforms with augmented reality visualization enable consumers to preview furniture within living spaces before buying, accelerating purchase cycles, broadening retailer reach, and democratizing access to premium collections across the UAE.

4. 'Make it in the Emirates' Localization

Domestic manufacturing is scaling under the 'Make it in the Emirates' initiative, reducing import dependence, shortening lead times, and enabling faster customization for residential and hospitality customers. Free zone manufacturing clusters and Dubai Design District are anchoring this localization wave.

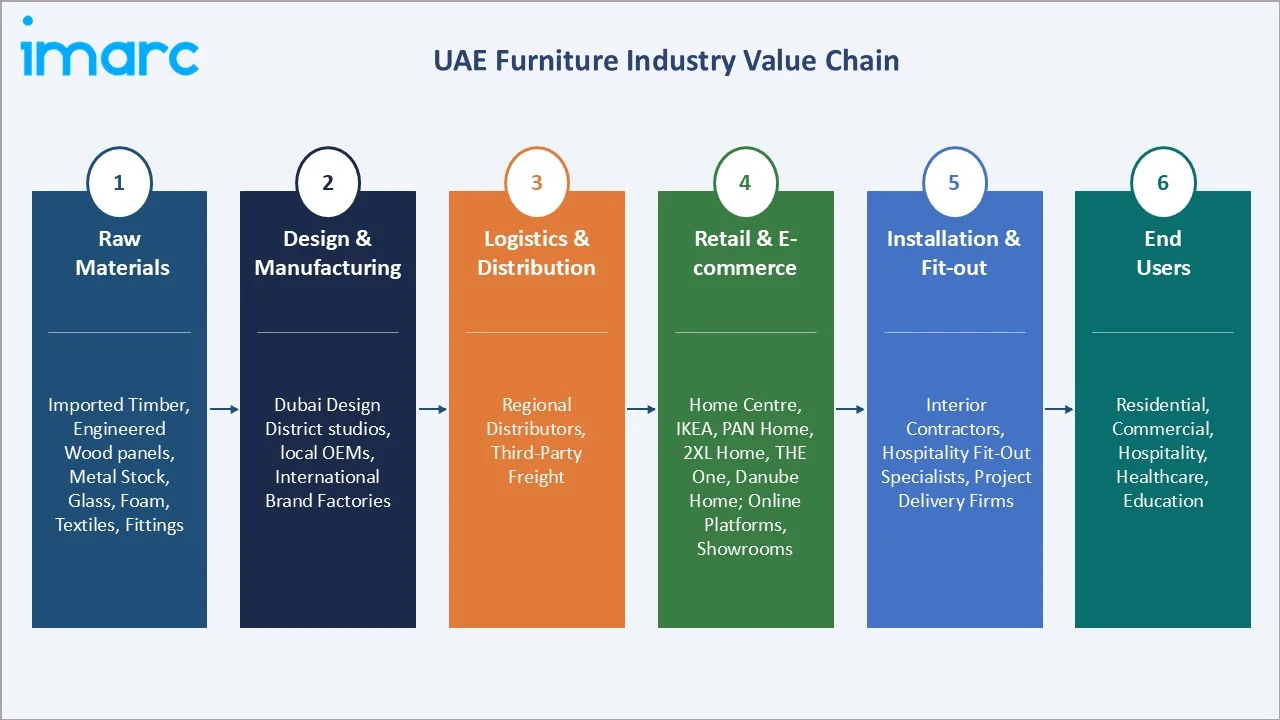

Industry Value Chain Analysis

The UAE furniture value chain spans six stages from raw material input through end-use installation. Design, fit-out, and premium retail capture the highest value-add margins, while import logistics and project-specific customization generate working capital requirements that favor well-capitalized omnichannel retailers and contract specialists.

|

Stage |

Key Players / Examples |

|

Raw Materials |

Imported timber, engineered wood panels, metal stock, glass, foam, textiles, fittings |

|

Design & Manufacturing |

Dubai Design District studios, local OEMs, international brand factories |

|

Logistics & Distribution |

Regional distributors, third-party freight |

|

Retail & E-commerce |

Home Centre, IKEA, PAN Home, 2XL Hone, THE One, Danube Home; online platforms, showrooms |

|

Installation & Fit-out |

Interior contractors, hospitality fit-out specialists, project delivery firms |

|

End Users |

Residential, Commercial, Hospitality, Healthcare, Education |

Integrated retailers with captive manufacturing, design capabilities, and regional logistics, such as Al-Futtaim IKEA and Landmark's Home Centre, achieve cost and speed advantages over pure importers, creating meaningful competitive moats in the mid-market and mass-premium segments.

Technology Landscape in the UAE Furniture Industry

Smart Furniture and IoT Integration

Furniture embedded with IoT-enabled lighting, motorized recliners, wireless charging surfaces, and voice-assistant compatibility is transitioning from novelty into mainstream premium demand. Integration with Apple HomeKit, Google Home, and Alexa ecosystems is a key specification criterion for high-end residential buyers.

Sustainable Materials and Circular Design

Furniture manufacturers are investing in FSC-certified timber, low-VOC adhesives, recycled PET upholstery, and modular designs enabling disassembly and refurbishment. These advances align with Dubai Municipality procurement rules and LEED/Estidama-compliant project specification requirements across commercial builds.

Digital Retail, 3D Configurators, and AR Visualization

Retailers are deploying 3D room planners, AR-based preview tools, and AI-driven recommendation engines to reduce purchase friction. These tools shorten decision cycles, lower return rates, and extend retailer reach beyond showrooms into Northern Emirates and cross-border GCC demand pools.

Automation in Manufacturing and Fit-out

CNC cutting, robotic finishing, and automated upholstery lines are gradually being adopted by UAE manufacturers within Jebel Ali and Khalifa Industrial Zone. These technologies reduce labor intensity, tighten tolerances, and enable cost-competitive domestic production against imports from China and Turkey.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product | Bedroom Furniture | 29.7% | 2025 |

| Material | Wood | 46.8% | 2025 |

| End Use | Residential | 55.4% | 2025 |

| Region | Dubai | 40.2% | 2025 |

By Material

Wood commands a 46.8% majority share in 2025 owing to its timeless aesthetic appeal, durability, and versatility across traditional Arabic-inspired interiors and contemporary Scandinavian minimalism. Engineered wood and hybrid wood-composite constructions combine natural warmth with enhanced structural performance across residential segments.

To access detailed market analysis, Request Sample

Others (15.0%) and metal (14.9%) serve commercial, outdoor, and modern décor applications where durability and industrial aesthetics are valued. Plastic (12.6%) supports outdoor and utility furniture, while glass (10.7%) is specified in premium décor, dining, and office configurations for its transparency and modern visual appeal.

By Product

Bedroom furniture dominates the product segment at 29.7% in 2025, reflecting sustained residential handovers, cultural emphasis on premium private spaces, and growing consumer focus on sleep wellness. Customizable wardrobes, ergonomic bedframes, and coordinated bedroom collections drive recurring replacement and new-purchase cycles.

Living room furniture, with 24.6% in 2025, ranks second, reflecting the cultural importance of hospitality-oriented reception spaces. Dining room furniture (18.3%) follows, supported by the UAE's family-centric dining culture. Kitchen (12.5%), office (9.8%), educational (3.2%), and others (2.0%) round out the portfolio across commercial and institutional end uses.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Dubai |

40.2% |

Record real estate turnover; luxury hospitality pipeline; HNW residents; Dubai Design District |

|

Abu Dhabi |

28.5% |

Government housing benefits; Saadiyat/Yas tourism; Vision 2030 diversification; institutional demand |

|

Sharjah |

18.1% |

Affordable residential supply; family-oriented expatriate base; manufacturing clusters; cultural tourism |

|

Others |

13.2% |

Ajman, RAK, Fujairah, UAQ: tourism development, affordable housing, emerging industrial corridors |

Dubai's 40.2% dominance in 2025 is driven by record real estate turnover, the densest concentration of high-net-worth residents in the UAE, and a continuously expanding hospitality pipeline. Luxury villa communities in Palm Jumeirah, Emirates Hills, and Dubai Hills Estate anchor premium furniture demand.

Abu Dhabi, with 28.5% in 2025, is supported by large government housing benefit announcements, Saadiyat Island cultural tourism, and institutional procurement linked to healthcare and education investments under Vision 2030 economic diversification.

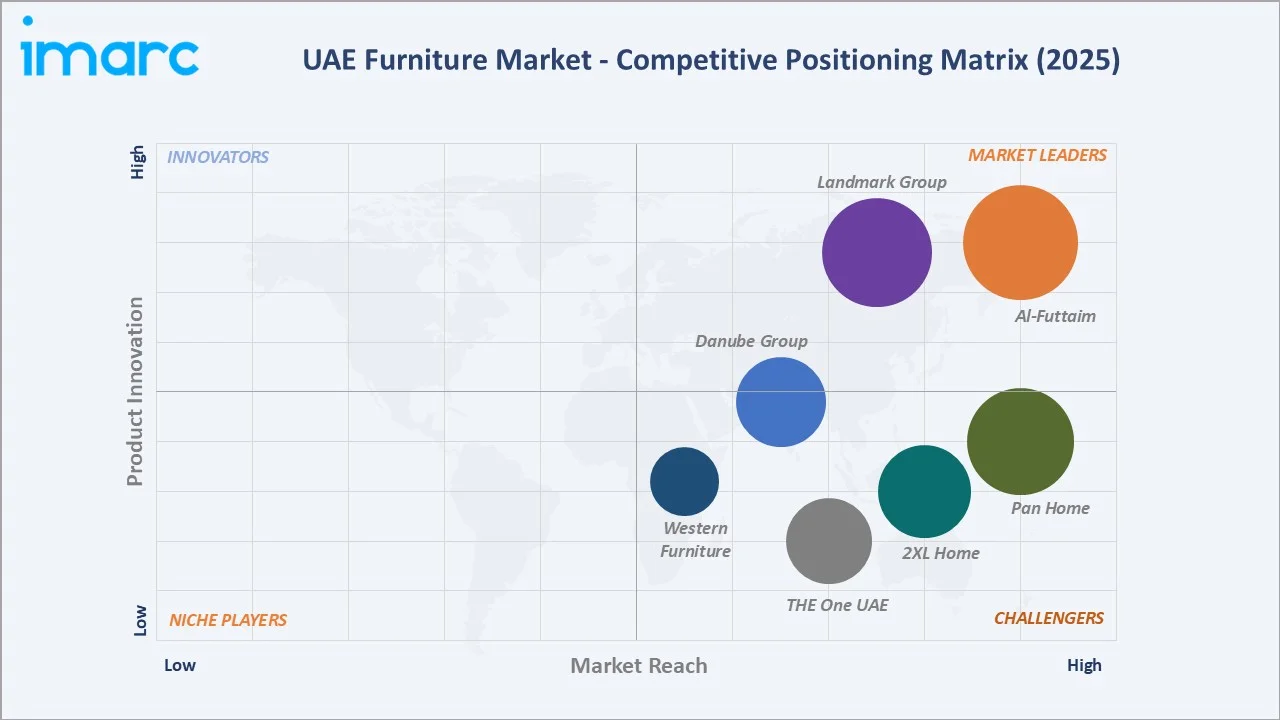

Competitive Landscape

The UAE furniture market is moderately fragmented, with multi-category retailers, luxury boutique brands, and local manufacturers competing across residential, commercial, and hospitality segments. Omnichannel strategy, sustainability certifications, exclusive distributorships, and Dubai Design District presence are key competitive levers.

|

Company Name |

Key Products |

Market Position |

UAE Strategic Focus |

|

Al-Futtaim |

Flat-pack, modular furniture, kitchens, home accessories |

Leader |

Operating IKEA in UAE-wide; mass-mid market; sustainability; small-format expansion |

|

Landmark Group |

Living, bedroom, dining, home décor |

Leader |

Operating Home Centre/Home Box, Regional leader; omnichannel; value-premium; private labels |

|

Pan Home |

Full-range home furniture, décor, mattresses |

Challenger |

Mid-market strength; multiple showrooms; value pricing |

|

2XL Home |

Classic and contemporary furniture, accessories |

Challenger |

Mid-to-premium; expanding omnichannel |

|

THE One UAE |

Lifestyle furniture, home accessories, café experience |

Challenger |

Experiential retail; design-led; premium positioning |

|

Danube Group |

Home furnishing, flooring, building materials |

Challenger |

Operating Danube Home, Value-to-mid; diversified retail; regional expansion |

|

Western Furniture |

Premium Italian/European residential and office furniture retail |

Challenger |

Premium Italian furniture retail; design-led; showroom-based |

Key players include Al-Futtaim, Landmark Group, Pan Home, 2XL Home, THE One UAE, Danube Group, Western Furniture, and others.

Key Company Profiles

Al-Futtaim

Al-Futtaim is the UAE's leading mass-to-mid-market furniture retailer, operating IKEA stores across Dubai, Abu Dhabi, Al Ain, and Fujairah under a long-standing franchise with Inter IKEA Systems, supplemented by small-format city stores and omnichannel platforms.

- Product Portfolio: Flat-pack and modular furniture, kitchens, storage systems, mattresses, lighting, and home accessories.

- Recent Developments: In November 2025, IKEA, operated by Al-Futtaim, opened a new store at JIMI Mall in Al Ain, marking a key milestone in the brand's ongoing expansion across the UAE.

- Strategic Focus: Al-Futtaim IKEA's UAE strategy centers on expanding geographic accessibility through small-format stores, deepening omnichannel and AR-based shopping capabilities, and accelerating sustainability credentials via renewable material sourcing and LEED-certified operations.

Landmark Group

Landmark Group is a leading home-furnishing omnichannel retailer across the UAE and GCC, operating a strong network of large-format stores, flagship showrooms, and an integrated e-commerce platform. The group offers a diversified portfolio of private-label brands that cater to a wide spectrum, ranging from value-driven to mass-premium segments. Among its key brands is Home Centre, which specializes in furniture and home décor, providing a comprehensive range of stylish and functional solutions for modern living spaces.

- Product Portfolio: Living, bedroom, dining, outdoor, home décor, kids' furniture, and textiles across private labels.

- Recent Developments: In January 2022, Home Centre, a brand of Landmark Group, introduced a refreshed brand identity, accompanied by the launch of a redesigned flagship store at City Centre Mirdif. The rebranding is centered around a customer-first approach, highlighted through the campaign “Inspired By You,” which reflects the brand’s connection with millions of homes it has served over the years.

- Strategic Focus: Home Centre's strategy leverages Landmark Group's regional scale, private-label supply chain, and omnichannel capabilities to defend its value-to-mid-premium position, while investing in experiential stores, sustainability-labelled ranges, and tech-enabled customer experiences.

PAN Home

PAN Home is a leading UAE full-range home furniture retailer, headquartered in Sharjah, operating large-format showrooms across Dubai, Abu Dhabi, Sharjah, and Al Ain, serving mid-market residential consumers with broad assortment breadth and value pricing.

- Product Portfolio: Living, bedroom, dining, office, mattresses, home décor, and outdoor furniture.

- Recent Developments: In July 2024, Pan Home announced the grand opening of a new store at Marina Mall, further strengthening its retail presence in Abu Dhabi. The store represents a major expansion for the brand and offers an extensive selection of over 25,000 furniture and home décor items. The new location is designed as a comprehensive destination for customers seeking stylish, functional, and affordable home furnishing solutions.

- Strategic Focus: PAN Home focuses on assortment breadth, store accessibility, and competitive pricing to defend its mid-market share, supplemented by growing online capabilities and periodic promotional calendars that sustain footfall across its multi-emirate showroom network.

Market Concentration Analysis

The UAE furniture market is moderately fragmented at the national level, with no single company controlling a dominant share. The top five retailers collectively account for an estimated 40-45% of organized retail value, while the remainder is served by specialist boutiques, independent showrooms, luxury brand franchises, and online-only entrants.

Consolidation is more advanced in modern, organized retail segments, where Al-Futtaim IKEA and Landmark's Home Centre maintain leading positions, while the premium and bespoke segments remain fragmented. Ongoing 'Make it in the Emirates' initiatives and e-commerce expansion are reshaping competitive dynamics.

Investment & Growth Opportunities

Fastest-Growing Segments

Hospitality end-use furniture is the highest-growth segment at ~4.55% CAGR through 2034, driven by the UAE's continually expanding luxury and lifestyle hotel pipeline. Bedroom furniture growth is supported by residential handovers, while smart and sustainable product lines are capturing disproportionate premium pricing.

Emerging Sub-Markets

The Northern Emirates — Ras Al Khaimah, Fujairah, Ajman, and Umm Al Quwain — represent the fastest-growing sub-regions, driven by tourism development, affordable housing expansion, and small-format retail rollouts that are unlocking furniture demand previously concentrated in Dubai and Abu Dhabi.

Venture & Investment Trends

Private capital is targeting omnichannel retail platforms, bespoke design studios, and sustainable furniture startups aligned with 'Make it in the Emirates'. Strategic investors view UAE furniture as a stable, infrastructure-linked demand base with structural tailwinds from tourism and expatriate population growth.

Future Market Outlook (2026-2034)

The UAE furniture market is forecast to expand from USD 3.81 Billion in 2025 to USD 5.60 Billion by 2034 at a CAGR of 4.01%, adding USD 1.79 Billion in incremental annual value. This growth reflects the market's structural links to real estate, tourism, and sustained expatriate-driven household formation.

Three forces will most significantly shape the landscape through 2034: deeper smart-furniture adoption aligned with connected living, accelerating sustainability mandates favoring FSC and low-VOC ranges, and omnichannel retail transformation led by AR visualization and localized manufacturing under 'Make it in the Emirates'.

Research Methodology

Primary Research

Primary research included structured interviews in 2024-2025 with furniture retailers, manufacturers, interior designers, real estate developers, hospitality procurement heads, logistics providers, and Dubai Design District stakeholders. Primary data validated market sizing, segment shares, regional demand, and technology adoption timelines.

Secondary Research

Key secondary sources include Dubai Statistics Centre, Statistics Centre Abu Dhabi, UAE Ministry of Economy reports, Dubai Land Department transaction data, Dubai Tourism annual statistics, DCAS publications, Dubai Municipality green building guidance, Emaar and Aldar annual reports, and industry trade publications.

Forecasting Models

Market size estimations and growth projections were derived via a combination of top-down and bottom-up forecasting models, incorporating GDP growth, real estate handover pipelines, population and expatriate dynamics, and historical evolution patterns. Scenario analysis (base, optimistic, conservative) was performed.

UAE Furniture Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Living Room Furniture, Dining Room Furniture, Bedroom Furniture, Kitchen Furniture, Office Furniture, Educational Furniture, Others |

| Materials Covered | Metal, Wood, Plastic, Glass, Others |

| End Uses Covered | Residential, Commercial, Hospitality, Healthcare, Others |

| Regions Covered | Dubai, Abu Dhabi, Sharjah, Others |

| Companies Covered | Al-Futtaim, Landmark Group, Pan Home, 2XL Home, THE One UAE, Danube Group, Western Furniture, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the UAE Furniture Market Report

The UAE furniture market reached USD 3.81 Billion in 2025, driven by robust real estate activity, expanding hospitality infrastructure, and sustained demand from the UAE's large, affluent, and diverse expatriate population.

The market is projected to reach USD 5.60 Billion by 2034, growing at a CAGR of 4.01% during 2026-2034, supported by urbanization, tourism expansion, smart and sustainable furniture adoption, and continued residential handovers across the emirates.

Wood leads with a 46.8% share in 2025, valued for its timeless aesthetic appeal, durability, and alignment with multicultural consumer preferences, reinforced by rising adoption of FSC-certified and engineered wood products across segments.

Bedroom furniture leads at 29.7% in 2025, reflecting sustained residential handovers, cultural emphasis on premium private spaces, and growing demand for customizable wardrobes, ergonomic bedframes, and coordinated bedroom collections across UAE households.

Dubai commands a 40.2% share in 2025, driven by record real estate transactions, a dense concentration of high-net-worth residents, an expanding luxury hospitality pipeline, and the Dubai Design District's role as a regional design epicentre.

Hospitality is the fastest-growing end-use segment at ~4.55% CAGR through 2034, driven by luxury and lifestyle hotel openings, MICE expansion, and branded residence pipelines requiring bespoke, design-forward commercial furniture packages across the UAE.

Leading companies include Al-Futtaim, Landmark Group, Pan Home, 2XL Home, THE One UAE, Danube Group, Western Furniture, and others.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)