UK Alcoholic Beverages Market Size, Share, Trends and Forecast by Category, Distribution Channel, and Region, 2026-2034

UK Alcoholic Beverages Market Size & Forecast 2026-2034

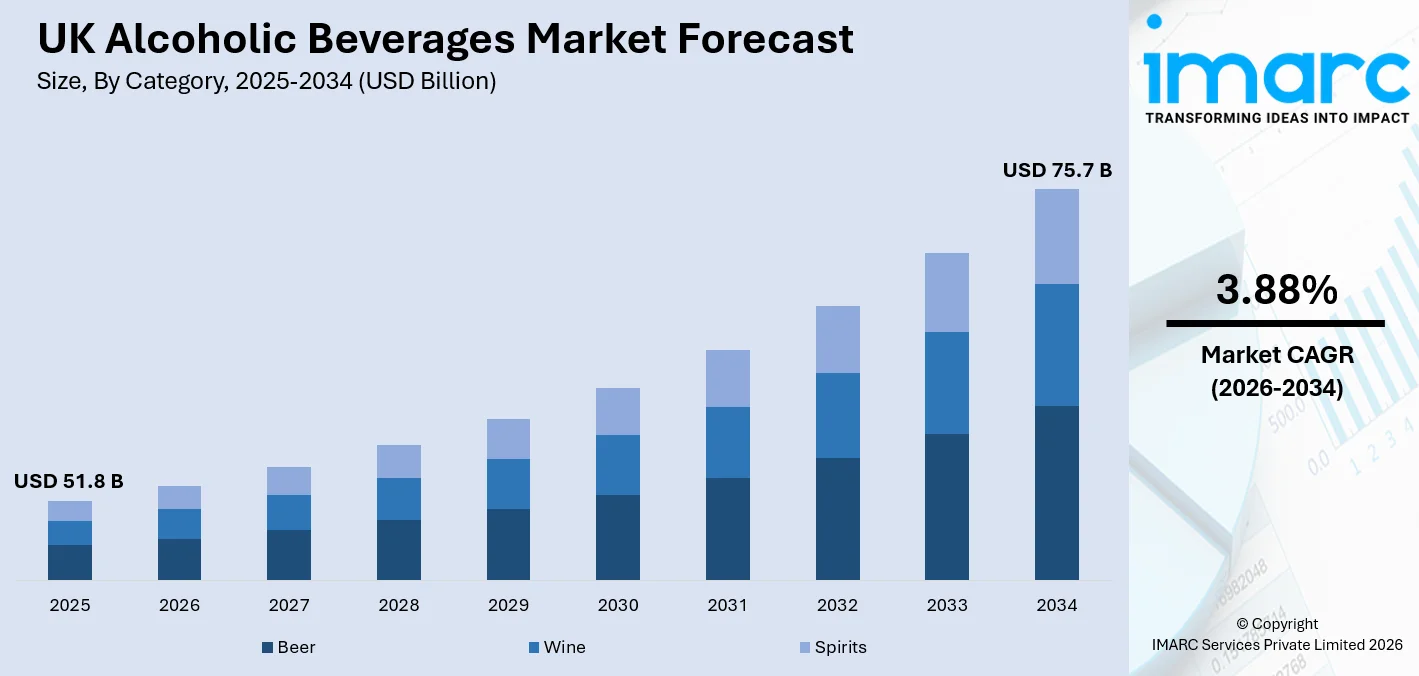

The UK alcoholic beverages market was valued at USD 51.8 Billion in 2025 and is projected to reach USD 75.7 Billion by 2034, exhibiting a CAGR of 3.88% during 2026-2034. The market relies on strong customer demand for high-quality beverages and craft drinks, the permanent social function of pubs, the increasing demand for drinks with no alcohol content, and the steady growth of off-site sales, which supermarkets support through their pricing, and people buying more products for home use. It has been reported that adults consume 10.7 litres of pure alcohol per person per year on average in the UK.

To get more information on this market Request Sample

UK Alcoholic Beverages Industry Analysis - Key Insights

- Beer leads 41.2% of category share in 2025 - beer has established itself as the top beverage choice due to its extensive cultural roots and its availability through both retail outlets and drinking establishments.

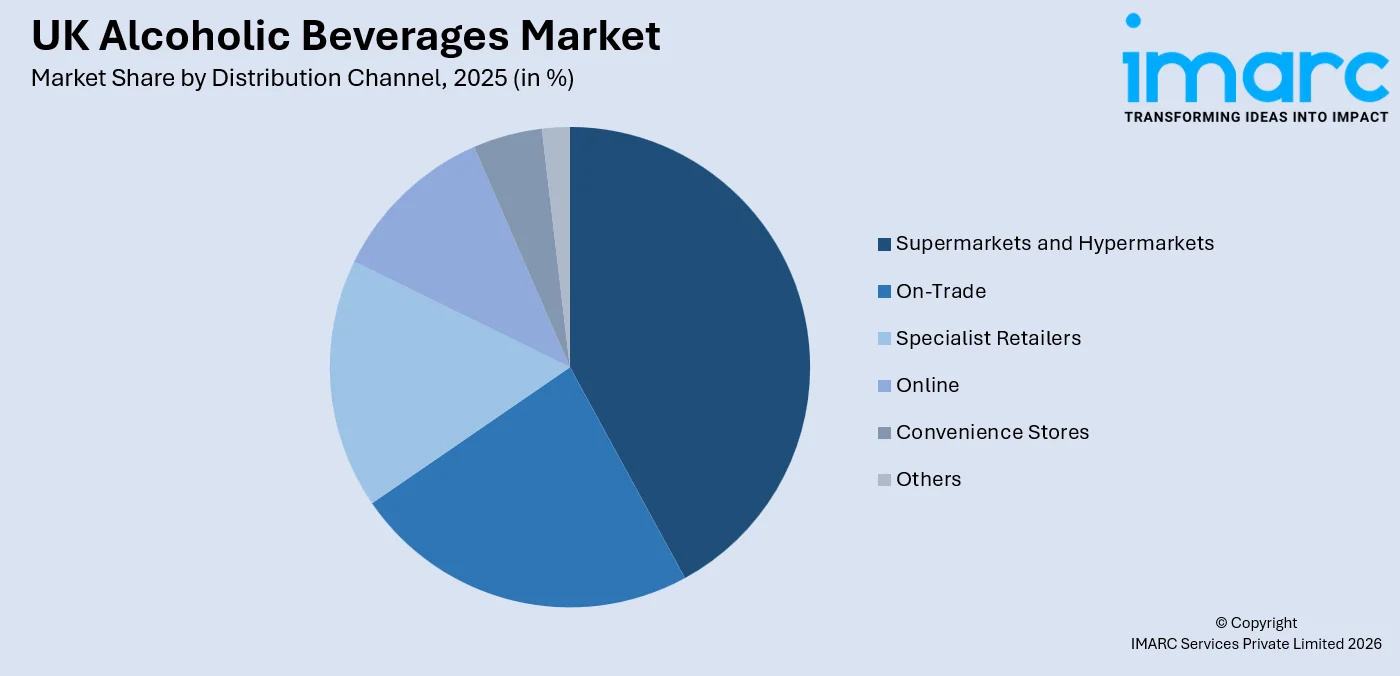

- Supermarkets and hypermarkets leads 44.5% of the distribution channel share in 2025 - UK alcohol shoppers choose to shop at their store since they offer numerous products at affordable prices, while private-label alcohol products become more popular.

- London holds the largest share at 16.2% in 2025 - high consumer affluence, a vibrant on-trade scene, tourism inflows, and strong demand for premium spirits and craft beverages anchor London's market leadership.

UK Alcoholic Beverages Market Trends and Dynamics 2026

Market Trends

Premiumisation and the 'drink less, drink better' consumer mindset

The UK alcoholic beverages market shows a premiumisation trend since consumers choose to drink higher-priced products when they drink less often. The on-trade channel price increases, together with health awareness growth and consumers' social status association with premium drinks, drive customers to select premium products in the beer, wine, and spirits markets. The number of cocktail bars in the United Kingdom experienced a 17.4% increase during 2024 when compared to the previous year. The increase in nightlife venues led to higher alcohol consumption in bars while creating additional opportunities for social drinking, which resulted in the continuous expansion of the UK alcoholic beverages market. The United Kingdom alcoholic beverages market trend provides main advantages to craft breweries, premium gin distillers, and aged whisky producers.

Ready-to-Drink (RTD) formats capitalising on convenience and flavour innovation

The RTD category is changing how alcoholic beverages compete in the UK market since it combines high-end spirit-based cocktails with portable canned and bottled drink options that people can easily access. Flavour innovation is the key element that distinguishes products from each other because tropical, citrus, and botanical flavour profiles attract younger UK consumers. Bacardi brought back its classic Breezer RTD product line in the UK market in June 2025 with three new flavours: Zesty Orange, Zing Lime, and Crisp Watermelon, which appeal to Gen Z tastes and Millennial nostalgia, thus supporting the prediction that RTD products will continue to grow in the UK alcoholic beverage market.

Growth Drivers

Deep-rooted pub culture and the resilience of on-trade consumption

The United Kingdom's on-trade channel, which includes pubs and bars, restaurants, and hospitality venues, serves as a vital distribution channel that has established itself as a major cultural force, which continues to operate successfully despite economic challenges. The pub functions as a main social gathering place, which maintains steady market demand for draught beer, premium spirits, and cocktails throughout both urban and suburban areas. Marston's and Reconomy Connect established their glass reuse program in October 2025, which has already processed more than 102,000 bottles while operating at nearly 600 pubs. The initiative creates operational efficiency through waste reduction and collection cost savings, which supports the ongoing development of the UK alcoholic beverages industry.

Supermarket dominance is driving accessible and competitive off-trade growth.

The UK alcohol distribution system operates under supermarket and hypermarket control, which they maintain through their multi-buy deals and increasing private-label alcohol offerings and capacity to provide economical home drinking options. The UK alcoholic beverages market grows because retailers such as Tesco, Sainsbury's, and Asda expand their online and in-store premium and specialist alcohol selections, which enables more customers to access mid-market and premium products.

Rising consumer affluence and premiumisation are driving value per unit.

Most UK consumers continue to spend extra money for high-quality products that show their origins and provide special drinking experiences despite economic challenges that affect household budgets. The drinking pattern shows that people now consume less alcohol, yet spend more money during each drinking event, which leads to substantial revenue expansion within premium beer, aged whisky, craft gin, and high-end wine markets. The retail market for Johnnie Walker, The Macallan, and Tanqueray shows strong performance because these premium spirits have established brand equity, which drives gift purchasing at both supermarket and specialist retail locations.

Market Restraints

Rising duties and taxation impose cost pressures on producers and consumers: The UK government executed alcohol duty reforms in August 2023, which they modified through their subsequent budgetary updates. The new system now uses alcohol by volume (ABV) measurements to determine tax rates, which result in higher expenses for various standard beer and spirits products. The ongoing increase in duties reduces producer profit margins, leading to higher retail prices that limit sales growth, especially in the value and mid-market segments, where consumers are most affected by price changes.

Intensifying health consciousness and alcohol moderation trends: Public health campaigns and NHS awareness programs, and continuing media coverage of alcohol consumption health risks have led to reduced drinking rates among UK adults. The increasing popularity of alcohol-free months and mindful drinking practices, and the consumption of non-alcoholic beverages that provide health advantages or contain minimal alcohol, create difficulties for market growth in all customer groups, particularly those aged under 35.

Cost-of-living pressures diverting household spend away from discretionary alcohol: The increasing costs of basic household necessities, which include energy, food, and rent payments, have decreased the financial resources which people use to purchase alcoholic beverages. The prices of premium lager and wine in on-trade establishments create higher expenses for customers than they would face in off-trade purchases. Pub closures continue to be a major problem because operators face increasing energy, wage, and business rate expenses, which prevent them from managing input cost increases without transferring those costs to customers.

UK Alcoholic Beverages Market Segmentation Analysis

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Category | Beer | 41.2% | 2025 |

| Distribution Channel | Supermarkets and Hypermarkets | 44.5% | 2025 |

| Region | London | 16.2% | 2025 |

Category Insights

Beer - 41.2% market share (2025) | Leading Category

The UK alcohol market shows its greatest category share through beer, which has become a national tradition, while businesses continue to develop. The craft beer segment keeps attracting loyal customers who buy products from both specialty stores and high-end drinking establishments because independent breweries use their local heritage, limited production methods, and unique taste combinations to stand out from mainstream brands. The UK craft beer market reached a value of approximately USD 5.1 billion in 2025, according to IMARC data, since customers increasingly preferred premium local beverages.

|

Segment Breakdown Beer (41.2%) · Wine · Spirits |

Distribution Channel Insights

Access the comprehensive market breakdown Request Sample

Supermarkets and Hypermarkets - 44.5% market share (2025) | Leading Distribution Channel

Supermarkets and hypermarkets control all alcohol sales throughout the United Kingdom, which makes them the primary off-trade distribution system for all beverage categories. The organization achieves its structural advantage through multiple interconnected factors, which include its ability to draw in large numbers of customers and its continuous marketing efforts that drive alcohol sales through special multipack and meal-deal alcohol deals and its capability to deliver high-value private label products that customers find valuable across beer wine and spirits and its shopping system which enables customers to buy alcohol during their regular grocery shopping trips.

|

Segment Breakdown Supermarkets and Hypermarkets (44.5%) · On-Trade · Specialist Retailers · Online · Convenience Stores · Others |

Regional Insights

London - 16.2% market share (2025) | Leading Region

London holds its position as the biggest regional market in the UK alcoholic beverages industry because the city contains many bars, its residents possess greater wealth, its citizens practice multiple drinking traditions from various cultures, and the city functions as an international tourist hub that sustains alcohol sales through its incoming visitors. The West End, Chelsea, and Canary Wharf districts of London display strong demand for premium Scotch whisky, imported champagne, and luxury spirits because wealthy residents and international business travelers spend more on alcohol than the national average.

South East- The South East region shows established development of its drinking market because residents have high disposable incomes and the area has numerous drinking establishments and active tourist traffic. The region also records high alcohol consumption rates and significant spending on both on-trade and off-trade alcoholic beverages.

North West- The North West alcoholic beverages market benefits from a strong pub culture and vibrant nightlife in cities such as Manchester and Liverpool. The urban population and social drinking habits of residents plus the presence of multiple drinking establishments create conditions which drive household alcohol expenditures to stay above normal levels.

East of England- The East of England market experiences growth because of increasing population numbers and rising disposable income and suburban consumers who exhibit particular drinking habits. People in this area continue to drink alcohol at high rates while they purchase retail alcohol and visit hospitality venues to drink socially.

South West- The South West region ranks among England's top alcohol-consuming areas because of its tourist attractions and coastal recreational sites and its strong pub culture. The region's households spend more money on alcoholic drinks than any other area in the United Kingdom.

West Midlands- The West Midlands alcoholic beverages market shows moderate drinking patterns because more people in this region choose not to drink compared to other areas of England. The demand for alcoholic beverages exists because both the Birmingham urban center and the increasing retail distribution of these products.

Yorkshire and the Humber - Yorkshire and the Humber exhibits strong alcohol consumption patterns because more adults in the region drink alcohol at dangerous levels. The established pub culture together with the region's large urban population creates ongoing demand for alcoholic drinks in the area.

East Midlands- The East Midlands alcoholic beverages market shows constant drinking patterns because households spend moderate amounts on alcoholic drinks. The urban areas of Nottingham and Leicester create demand for retail and on-trade activities which social drinking practices maintain throughout the local hospitality industry.

Scotland- Scotland functions as a major market for alcoholic beverages because its people possess deep cultural ties to spirits especially whisky. Health awareness programs and government alcohol regulations have not succeeded in reducing alcohol consumption which keeps driving customer demand throughout pubs and retail stores and tourist venues.

|

Segment Breakdown · London (16.2%) · South East · North West · East of England · South West · Scotland · West Midlands · Yorkshire and the Humber · East Midlands · Others |

Market Outlook 2026-2034

What is the future outlook of the UK Alcoholic Beverages Market?

The UK alcoholic beverages market is positioned for sustained and broad-based value growth through 2034.

The UK alcoholic beverages market is expected to reach USD 75.7 Billion by 2034, driven by the convergence of premiumisation, product innovation in low/no-alcohol and RTD categories, and the enduring structural importance of both on-trade and supermarket distribution channels. A compound annual growth rate of 3.88% over the forecast period reflects the market's robust underlying consumer base and its capacity for value growth even against a moderating volume backdrop.

UK Alcoholic Beverages Market - Leading Key Players

The UK alcoholic beverages market is characterised by a highly competitive landscape featuring globally dominant producers, strong national operators, and a vibrant ecosystem of independent craft breweries and artisanal distilleries. Leading multinationals, including Diageo, AB InBev, Heineken, Carlsberg, and Pernod Ricard, maintain extensive brand portfolios across all major categories and leverage significant distribution scale across both on-trade and off-trade channels.

| Company | Leading Brands | Highlights |

|---|---|---|

| Diageo plc | Guinness, Johnnie Walker, Tanqueray, Smirnoff, Baileys | UK-headquartered global spirits company, leveraging AI for personalised marketing and product innovation |

| Anheuser-Busch InBev (AB InBev) | Stella Artois, Budweiser, Corona, Becks | Brewer; expanding low- and no-alcohol portfolio to capture UK mindful drinking demand |

| Heineken N.V. | Heineken, Strongbow, Foster's, Amstel, Birra Moretti | Major UK beer and cider player; investing in premium and flavour-led innovation for Gen Z consumers |

Some of the existing key players in the UK Alcoholic Beverages Market are Carlsberg Group, Pernod Ricard, etc.

Latest Development & News

- In June 2025, Bacardi introduced its UK Breezer RTD product line following its previous discontinuation, which brought three new flavors to the market: Zesty Orange, Zingy Lime, and Crisp Watermelon. The relaunch aims to attract Gen Z customers through the brand's connection to current fruity flavor trends and home party activities, while it also seeks to restore connections with Millennial and Gen X customers who remember the brand from its 1990s and early 2000s peak.

- In January 2025, Carlsberg Group acquired Britvic plc through its subsidiary Carlsberg UK Holdings Limited, forming a unified UK beverage company named Carlsberg Britvic. The companies have merged various distribution and supply chain functions, while their experienced executives will help drive business expansion through their combined portfolios of beer, soft drinks, and alcoholic beverages.

- In May 2024, SPAR UK launched its new value-based alcoholic drink collection through its proprietary wine range which became available in all licensed retail establishments. The portfolio consists of three wine types which include fruity red wines and crisp white wines and fresh rosé wines to show SPAR's dedication to delivering consumers high-quality products that provide excellent value.

UK Alcoholic Beverages Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Categories Covered | Beer, Wine, Spirits |

| Distribution Channels Covered | Supermarkets and Hypermarkets, On-Trade, Specialist Retailers, Online, Convenience Stores, Others |

| Regions Covered | London, South East, North West, East of England, South West, Scotland, West Midlands, Yorkshire and The Humber, East Midlands, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the UK Alcoholic Beverages Market Report

The UK alcoholic beverages market was valued at USD 51.8 Billion in 2025.

The UK alcoholic beverages market is anticipated to reach a value of USD 75.7 Billion by 2034.

Beer leads the market with a share of 41.2%, driven by its deep cultural heritage, widespread distribution across both on-trade and off-trade channels, and dynamic product innovation spanning craft, premium, and alcohol-free sub-segments.

Supermarkets and Hypermarkets dominate the distribution landscape with a 44.5% share, supported by competitive pricing, multipack promotions, extensive own-label ranges, and increasing shelf space for premium and trending beverage categories.

London currently dominates the UK alcoholic beverages market, accounting for a share of 16.2%. The capital's combination of a vibrant on-trade scene, high consumer affluence, strong tourism demand, and its role as a launch hub for premium beverage brands sustains its market leadership.

Some of the major players in the UK alcoholic beverages market include Diageo plc, Anheuser-Busch InBev, Heineken N.V., Carlsberg Group, Pernod Ricard, among others.

Key trends include the accelerating premiumisation of beer, wine, and spirits, strong growth in low- and no-alcohol alternatives driven by health-conscious consumer behaviour, the rapid expansion of the RTD cocktail segment, increasing craft beverage adoption, and the rise of e-commerce and direct-to-consumer alcohol channels.

Growth is driven by the UK's deeply embedded pub and on-trade culture sustaining experiential drinking occasions, supermarket dominance enabling broad off-trade access to premium products, rising consumer willingness to pay for quality over quantity, and robust innovation across RTD, craft, and no-alcohol categories.

Challenges include rising alcohol duty and taxation compressing producer margins, the structural moderation trend reducing per-capita consumption frequency, particularly among under-35s, cost-of-living pressures diverting discretionary spending away from on-trade occasions, and the ongoing competitive pressure from non-alcoholic and functional beverage alternatives.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)