UK Caustic Soda Market Size, Share, Trends and Forecast by Product Type, Manufacturing Process, Grade, Application, and Region, 2026-2034

UK Caustic Soda Market Overview:

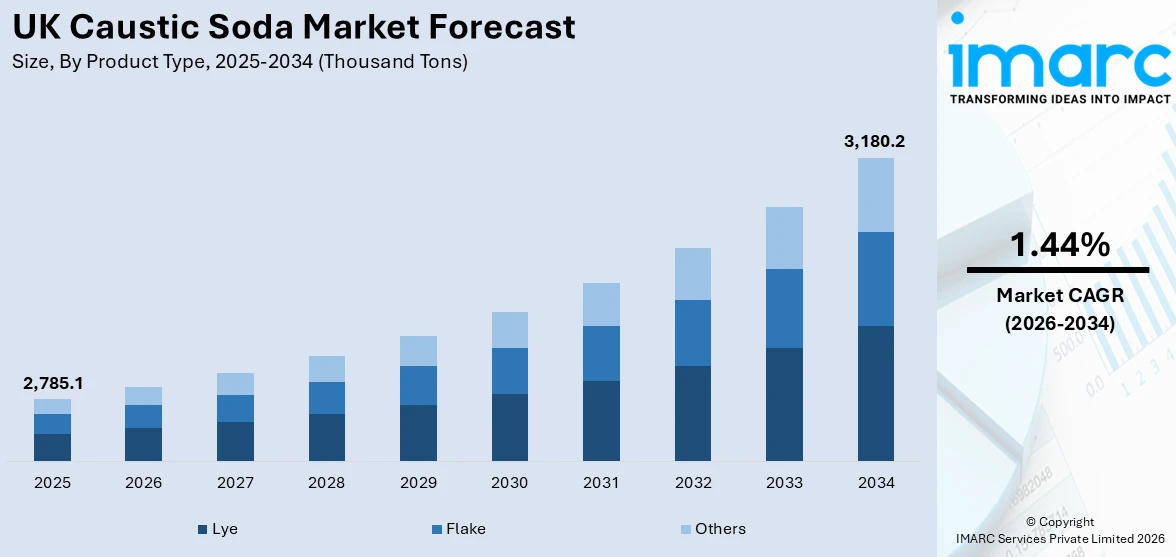

The UK caustic soda market size reached 2,785.1 Thousand Tons in 2025. The market is projected to reach 3,180.2 Thousand Tons by 2034, exhibiting a growth rate (CAGR) of 1.44% during 2026-2034. The market is fueled by the continued expansion of the country's manufacturing and chemical industries, which depend significantly on caustic soda as a major raw material. Moreover, growing investment in local chemical production plants and the upgrade of old facilities is enhancing supply reliability. In addition, growing emphasis on sustainability and recycling programs is increasing caustic soda demand for wastewater treatment and environmental purposes, which is further augmenting the UK caustic soda market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | 2,785.1 Thousand Tons |

| Market Forecast in 2034 | 3,180.2 Thousand Tons |

| Market Growth Rate 2026-2034 | 1.44% |

UK Caustic Soda Market Trends:

Shifting Demand Patterns Across End-Use Industries

The demand for caustic soda in the UK is gradually rebalancing. The pulp and paper industry historically accounted for a substantial share, but its demand is plateauing due to reduced paper consumption and increasing digitization. Simultaneously, the chemical sector’s requirements—for soda ash production, cleaning agents, and specialty chemicals—are rising, especially as manufacturers seek more alkaline inputs for higher-purity intermediates. Moreover, the alumina refining industry, though smaller in the UK, still contributes a steady baseline demand for caustic soda in its separation processes. Meanwhile, water treatment and soap and detergent manufacturing continue to depend on a consistent caustic soda supply, though innovations in detergent chemistry are marginally reducing per-unit usage. Overall, these shifts reflect divergent trajectories: declining demand from paper and pulp, stable consumption in alumina and water treatment, and moderate growth in specialty chemicals. Each sector’s policies and investment cycles influence procurement volumes and contract structures, affecting market pricing rigidity and supplier negotiation leverage.

To get more information on this market Request Sample

Emphasis on Supply Chain Resilience and Sourcing Flexibility

Supply chain robustness has gained prominence in the market. Historical dependencies on single-source suppliers or limited shipping routes have exposed operators to vulnerabilities, whether from shipping delays, strikes at ports, or production interruptions abroad. In response, buyers now diversify their supply base, contracting both domestic producers and importers from varied European and global suppliers to mitigate disruption risk. Besides this, inventory management practices are evolving as companies maintain buffer stocks and negotiate flexible delivery terms to weather potential shortages. Simultaneously, transport logistics have shifted, with higher reliance on rail and road transport inland to reduce port bottlenecks. Also, some firms explore on-site caustic soda generation through membrane or diaphragm electrolysis to supplement purchased volumes; this trend is particularly noticeable among large chemical integrators seeking autonomy. In line with this, cost structures are adapting, as holding buffer inventory increases carrying costs, yet the trade-off with continuity and supply security is considered worthwhile.

Regulatory Pressures Aligning Caustic Soda Production with Environmental Standards

Environmental regulation is a significant factor influencing the UK caustic soda market growth. The chemical manufacturing sector must comply with stringent emissions and effluent norms under UK environmental law and EU-derived standards retained post-Brexit. Furthermore, caustic soda producers face tightening limits on energy consumption and CO₂ output, spurring investments in energy-efficient electrolysis units and heat recovery systems. Also, water usage and wastewater discharge are increasingly monitored, motivating the installation of zero-liquid discharge systems or closed-loop cooling circuits. In addition, corporate responsibility expectations compel manufacturers to source electricity from low-carbon grids or invest in on-site renewables to offset their caustic soda’s carbon footprint. Documentation standards such as E-PRTR (European Pollutant Release and Transfer Register) remain relevant, requiring public reporting of pollutant emissions from high-volume chemicals. These regulatory and reputational pressures drive capital expenditure in cleaner production technologies. Moreover, purchasers increasingly favor suppliers who can demonstrate lower environmental impact per tonne of caustic soda, influencing contractual terms and potentially enabling premium pricing linked to sustainability credentials.

UK Caustic Soda Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country and regional levels for 2026-2034. Our report has categorized the market based on product type, manufacturing process, grade, and application.

Product Type Insights:

- Lye

- Flake

- Others

The report has provided a detailed breakup and analysis of the market based on the product type. This includes lye, flake, and others.

Manufacturing Process Insights:

- Membrane Cell

- Diaphragm Cell

- Others

A detailed breakup and analysis of the market based on the manufacturing process have also been provided in the report. This includes membrane cell, diaphragm cell, and others.

Grade Insights:

- Reagent Grade

- Industrial Grade

- Pharmaceutical Grade

- Others

The report has provided a detailed breakup and analysis of the market based on the grade. This includes reagent grade, industrial grade, pharmaceutical grade, and others.

Application Insights:

Access the comprehensive market breakdown Request Sample

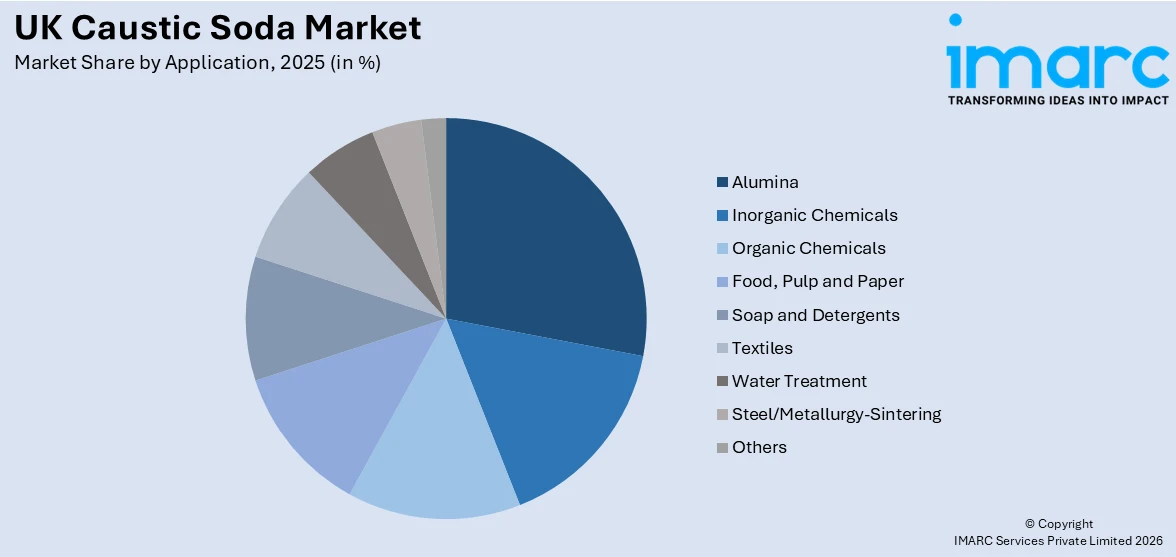

- Alumina

- Inorganic Chemicals

- Organic Chemicals

- Food, Pulp and Paper

- Soap and Detergents

- Textiles

- Water Treatment

- Steel/Metallurgy-Sintering

- Others

A detailed breakup and analysis of the market based on the application have also been provided in the report. This includes alumina, inorganic chemicals, organic chemicals, food, pulp and paper, soap and detergents, textiles, water treatment, steel/metallurgy-sintering, and others.

Regional Insights:

- London

- South East

- North West

- East of England

- South West

- Scotland

- West Midlands

- Yorkshire and The Humber

- East Midlands

- Others

The report has also provided a comprehensive analysis of all the major regional markets, which include London, South East, North West, East of England, South West, Scotland, West Midlands, Yorkshire and The Humber, East Midlands, and others.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

UK Caustic Soda Market News:

- In February 2024, INEOS Inovyn introduced an Ultra Low Carbon (ULC) range of chlor-alkali products, including caustic soda, caustic potash, and chlorine, achieving up to a 70% reduction in CO₂ emissions compared to industry averages. This advancement is facilitated by utilizing renewable energy sources such as hydroelectric power in Rafnes, Norway, and North Sea wind turbines in Antwerp, Belgium. Certified under the ISCC PLUS scheme, the ULC range enables customers to significantly lower their Scope 3 emissions and supports the transition to a Net Zero economy.

UK Caustic Soda Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Thousand Tons |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Lye, Flake, Others |

| Manufacturing Processes Covered | Membrane Cell, Diaphragm Cell, Others |

| Grades Covered | Reagent Grade, Industrial Grade, Pharmaceutical Grade, Others |

| Applications Covered | Alumina, Inorganic Chemicals, Organic Chemicals, Food, Pulp and Paper, Soap and Detergents, Textiles, Water Treatment, Steel/Metallurgy-Sintering, Others |

| Regions Covered | London, South East, North West, East of England, South West, Scotland, West Midlands, Yorkshire and The Humber, East Midlands, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the UK caustic soda market performed so far and how will it perform in the coming years?

- What is the breakup of the UK caustic soda market on the basis of product type?

- What is the breakup of the UK caustic soda market on the basis of manufacturing process?

- What is the breakup of the UK caustic soda market on the basis of grade?

- What is the breakup of the UK caustic soda market on the basis of application?

- What is the breakup of the UK caustic soda market on the basis of region?

- What are the various stages in the value chain of the UK caustic soda market?

- What are the key driving factors and challenges in the UK caustic soda market?

- What is the structure of the UK caustic soda market and who are the key players?

- What is the degree of competition in the UK caustic soda market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the UK caustic soda market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the UK caustic soda market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the UK caustic soda industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)