UK Data Center Market Size, Share, Trends and Forecast by Component, Type, Enterprise Size, End User, and Region, 2026-2034

UK Data Center Market Size & Forecast 2026-2034

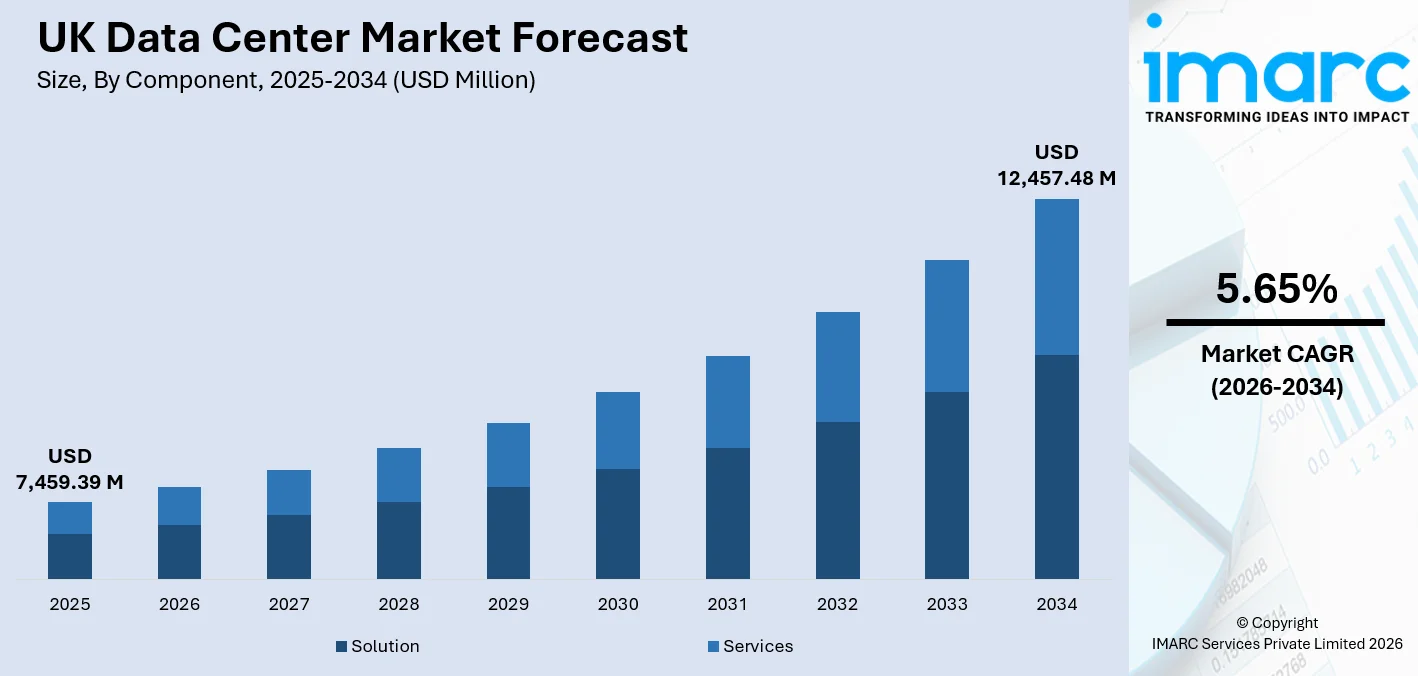

The UK data center market size was valued at USD 7,459.39 Million in 2025, is projected to reach USD 12,457.48 Million by 2034, growing at a CAGR of 5.65% from 2026-2034. The rising adoption of cloud computing services, the rapid adoption of AI workloads, and the strategic position of the United Kingdom as Europe's premier connectivity hub are among the factors driving the growth of the data center market in the UK. Furthermore, the government's 2023 recognition of data centers as Critical National Infrastructure is a clear indication of the growth prospects of the UK data center market.

To get more information on this market Request Sample

UK Data Center Industry Analysis - Key Insights

- Solution component commands a 56.3% share in 2025 - The solutions segment, encompassing power, cooling, and IT hardware infrastructure, dominates the UK data center market. This reflects the capital-intensive nature of building and equipping hyperscale and colocation facilities to meet the demanding uptime and performance requirements of enterprise, hyperscale, and government customers.

- Hyperscale data centers lead type segment at 40.2% in 2025 - Hyperscale facilities operated by global cloud providers including AWS, Microsoft Azure, and Google Cloud command the largest type share. The UK's unparalleled connectivity, skilled workforce, and proximity to global financial markets make it a primary destination for hyperscale capacity expansion in Europe.

- Large enterprise size leads the enterprise segment at 58.4% in 2025 – Large enterprises dominate demand due to extensive requirements for secure storage, hybrid cloud integration, disaster recovery, and regulatory compliance. Banks, government bodies, healthcare providers, and multinational corporations increasingly depend on scalable colocation and hyperscale infrastructure to manage rising data volumes and digital transformation initiatives.

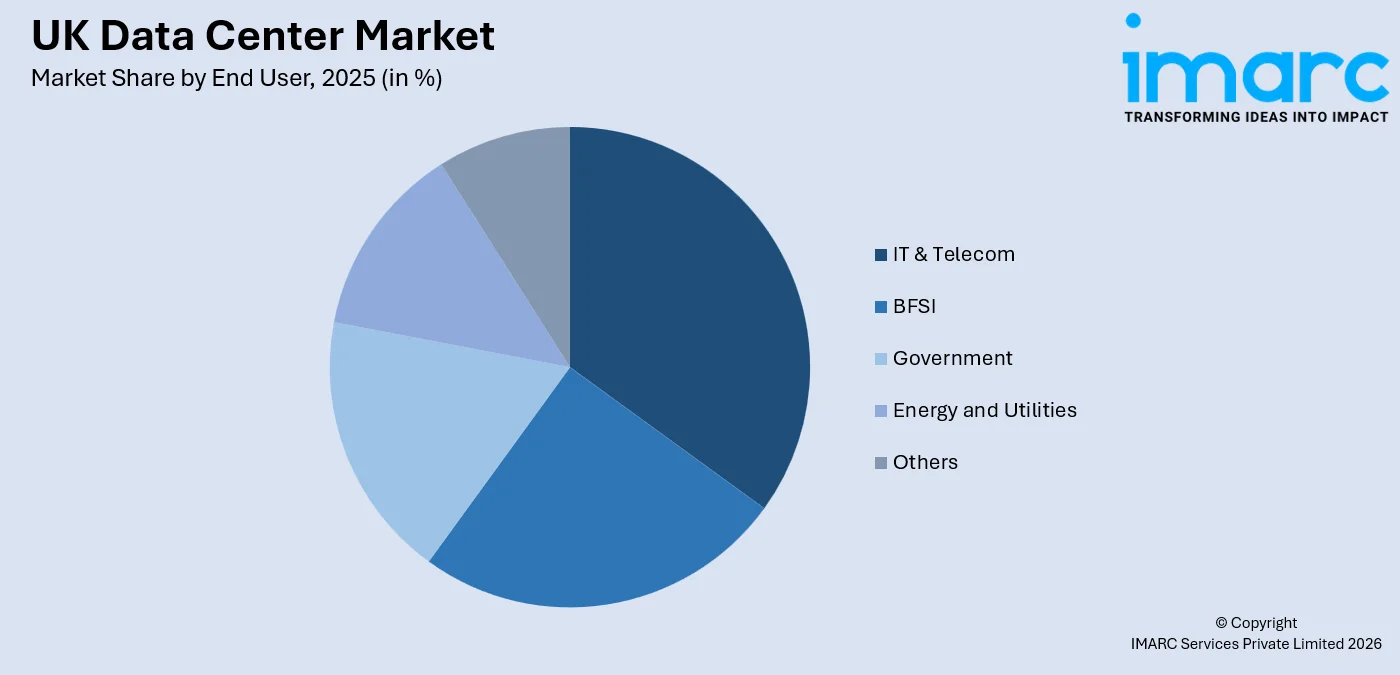

- IT and telecom dominates the end user at 28.7% segment in 2025 - The IT and telecom sector leads demand as cloud adoption, 5G rollout, and data traffic growth accelerate infrastructure needs. Telecom operators and cloud providers require highly connected, low-latency facilities to support network services, streaming platforms, and enterprise digital applications across the UK market.

- London region commands 35.1% of the UK data center market in 2025 - Greater London remains the single largest data center hub in the UK and one of the top five globally, driven by concentration of financial services, tech sector headquarters, and dense carrier-neutral connectivity. Despite power constraints, London continues to attract hyperscaler pre-commitments and colocation investment across the M25 corridor.

UK Data Center Market Trends and Dynamics 2026

Market Trends

AI and High-Density Compute Reshaping UK Data Center Design Architecture

The rapid adoption of artificial intelligence, machine learning, and high-performance computing is becoming the primary growth engine of the UK data center market. For instance, Nscale, a UK based AI infrastructure company has raised USD 2 Billion in Series C funding to accelerate the global expansion of its AI data center and compute platform.

Sustainability and Net-Zero Commitments Driving Operational Transformation Across the Sector

UK data center operators are accelerating their transition toward carbon-neutral operations in response to the government's net-zero 2050 targets and growing customer ESG requirements. Equinix (UK) Limited, global data center and colocation provider currently has 100% renewable energy coverage across its European data centers, including major UK sites in London and Manchester.

Edge Computing Expansion Connecting UK Regional Markets to Distributed Infrastructure

The nationwide rollout of 5G networks is catalysing a new wave of edge data center deployments across the UK, positioned closer to end users in secondary cities and suburban areas to meet the ultra-low-latency requirements of autonomous systems, industrial IoT, and real-time analytics applications. This is creating demand for a new class of modular, prefabricated edge facilities in various markets.

- Modular and Prefabricated Construction Accelerating Time-to-Market: Operators are moving fast with prefabricated modular data center parts. They want to cut down build times and keep capital risk in check. This approach lets them add capacity as needed and fits perfectly with hyperscale build-to-suit projects, where being first to market really matters.

- Liquid Cooling Adoption Accelerating Across Colocation and Hyperscale Campuses: As AI workloads increase, cooling technologies such as rear-door heat exchangers, direct liquid cooling, and immersion cooling are becoming mainstream. In the UK, colocation providers now include liquid cooling as a standard option to attract customers who need more GPU power.

- Critical National Infrastructure Status Elevating Government and Institutional Engagement: Since the UK government designated data centers as critical national infrastructure in September 2023, operators have received increased government support during cyberattacks and major disruptions. They are also engaging more directly with regulators on planning, energy, and workforce development.

Growth Drivers

Cloud Adoption and Digital Transformation Across Enterprise and Public Sectors Creating Sustained Demand

The UK’s enterprise and public sector cloud migration is driving sustained demand for data center capacity. Government cloud-first policies, NHS digital transformation, and enterprise adoption of hybrid and multi-cloud architectures are increasing colocation and hyperscale usage, while frameworks like G-Cloud and Crown Hosting support structured procurement and long-term capacity planning.

AI and Machine Learning Workload Surge Driving High-Density Infrastructure Investment

Generative AI adoption in the UK's financial services, healthcare, media, and professional services sectors is driving significant demand for computing resources. In September 2025, Alphabet, the parent company of Google, announced plans to invest 5 billion pounds (USD 6.82 Billion) over two years in UK AI research, the expansion of DeepMind, and green data centers. This investment supports Britain’s ambition to become a global leader in AI.

Critical National Infrastructure Designation Strengthening Investor Confidence and Government Support

The UK government's recognition of data centers as Critical National Infrastructure has materially strengthened the investment case for the sector. The designation provides enhanced government support during cyber incidents and outages, improves resilience, and reduces operational risks. This policy reassurance is encouraging large-scale investments, including multibillion-pound projects supporting jobs and long-term digital infrastructure growth.

- Data Sovereignty and UK GDPR Requirements Sustaining Onshore Hosting Demand: Post-Brexit data sovereignty requirements and UK GDPR compliance obligations continue to drive enterprise preference for UK-domiciled data storage and processing, supporting structural demand for domestic colocation capacity rather than cross-border cloud alternatives.

- Financial Services and BFSI Sector Driving Latency-Sensitive Colocation Demand: The concentration of global banking, insurance, and fintech operations in London and its environs sustains premium colocation demand for carrier-neutral, low-latency proximity to financial market infrastructure, clearing systems, and trading venues.

- FCA and PRA Operational Resilience Rules Requiring Distributed Infrastructure: Financial regulators' operational resilience requirements mandating geographic distribution of critical systems and minimum recovery time objectives are driving investment in secondary UK data center sites, benefiting operators with multi-site regional footprints.

Market Restraints

Power Availability Constraints Limiting Capacity Expansion in Greater London: Power availability limitations are increasingly reducing data center expansion across Greater London, as grid capacity shortages delay new electricity connections and extend project timelines. Additionally, rising power demands from AI workloads are strengthening competition for energy infrastructure, prompting operators to shift their investments toward regional UK locations with better grid access and scalable power availability.

Planning and Permitting Delays Creating Uncertainty for Greenfield Development: Data center developers are facing material planning risk in the region, specifically in the Green Belt areas surrounding London, where significant land banks exist, but obtaining planning consent is difficult. Local community resistance to large-scale facilities often centerd on concerns about visual impact, water consumption, and traffic, has further delayed several major projects.

Rising Energy Costs and Sustainability Pressures Impacting Operational Margins: In Europe, electricity is most expensive in the UK, creating structural cost pressures for data centers. Key risk factors include volatile wholesale power prices, which are especially affecting smaller colocation providers, who face margin compression. Large operators can hedge energy costs through long-term PPAs and demand flexibility contracts, while rising expenses for meeting stricter sustainability commitments add further challenges to the sector's operational costs.

UK Data Center Market Segmentation Analysis

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Component | Solution | 56.3% | 2025 |

| Type | Hyperscale | 40.2% | 2025 |

| Enterprise Size | Large Enterprises | 58.4% | 2025 |

| End User | IT and Telecom | 28.7% | 2025 |

| Region | London | 35.1% | 2025 |

Component Insights

Solution - 56.3% Market Share (2025) | Leading Component

The solutions segment dominates the market, reflecting the capital-intensive nature of building and equipping facilities with power distribution, cooling, physical security, and IT hardware infrastructure. Strong enterprise and hyperscale investment in new capacity and the upgrade of existing facilities to support AI workload densities is sustaining robust demand for solutions through the forecast period.

|

Segment Breakdown Solution (56.3%) · Services |

Type Insights

Hyperscale - 40.2% Market Share (2025) | Leading Type

Hyperscale data centers lead the UK market type segment, emphasized by sustained capacity investment from AWS, Microsoft Azure, and Google Cloud, which continue to expand their UK regional footprints to serve enterprise cloud demand. The hyperscale segment benefits from economies of scale in power procurement, construction, and operations, and is driving the development of large campus-style facilities in the M4 corridor, Northampton, and Scotland.

|

Segment Breakdown Hyperscale (40.2%) · Colocation · Edge · Others |

Enterprise Size Insights

Large Enterprises - 58.4% Market Share (2025) | Leading Enterprise Size

Large enterprises are the dominant enterprise size of UK data center services. These organisations, primarily operating in financial services, retail, healthcare, and the public sector, require substantial, highly resilient colocation or cloud hosting capacity to support critical workloads, including ERP, CRM, transaction processing, and increasingly AI-driven analytics platforms.

Key Characteristics of Large Enterprise Segment:

|

Metric

|

Details

|

|---|---|

|

Market Share in 2025

|

58.4%

|

|

Key Industries

|

Financial Services & Banking, Government & Defence, Healthcare & Life Sciences, Retail & E-Commerce, Media & Entertainment |

|

Major Growth Drivers

|

Cloud migration programmes, AI workload expansion, operational resilience regulatory requirements, multi-site disaster recovery mandates |

|

Outlook

|

Sustained structural dominance through 2034, with SME segment growing fastest by percentage rate as cloud-native adoption broadens market addressability |

|

Segment Breakdown Large Enterprises (58.4%) · Small & Medium Enterprises |

End User Insights

Access the comprehensive market breakdown Request Sample

IT and Telecom - 28.7% Market Share (2025) | Leading End User

IT and Telecommunications dominate the UK data center market. Telecom operators need substantial colocation and edge data center capacity to enable network function virtualisation, software-defined networking, and the infrastructure for 4G and 5G networks. Cloud service providers, managed service providers, and systems integrators form the rest of the IT segment.

|

Segment Breakdown IT & Telecom (28.7%) · BFSI · Government · Energy and Utilities · Others |

Regional Insights

London - 35.1% Market Share (2025) | Leading Region

London dominates the UK data center market, strengthening its status as one of the world's top five global data center markets alongside Northern Virginia, Singapore, Frankfurt, and Amsterdam. The capital's advantages include unparalleled carrier-neutral connectivity anchored by the London Internet Exchange (LINX), one of the world's largest internet exchanges; proximity to global financial markets; a deep pool of digital infrastructure talent; and established long-term relationships with all major hyperscale’s.

|

Metric

|

Details

|

|---|---|

|

Market Share in 2025

|

35.1%

|

|

Key Clusters

|

Docklands / East London, Slough / Heathrow M4 Corridor, Park Royal, City of London financial district proximity |

|

Major Growth Drivers

|

Concentration of FTSE 100 and global financial services, highest density carrier-neutral connectivity, LINX interconnection ecosystem, hyperscaler anchor tenancy |

| Key Constraints | Grid power availability, Green Belt planning restrictions, land cost premium redirecting new large-scale development to M25 periphery and secondary markets |

|

Outlook

|

Sustained structural dominance driven by interconnection value and financial services demand; new hyperscale capacity increasingly deployed in outer London and surrounding counties |

|

Segment Breakdown London (35.1%) · South East · North West · East of England · South West · Scotland · West Midlands · Yorkshire and The Humber · East Midlands · Others |

Market Outlook 2026-2034

What is the future outlook of the UK data center market?

The UK data center market is expected to sustain steady revenue growth through 2034.

The UK data center industry is in line for steady growth until 2034, thanks to robust and long-term demand from the traditional pillars of the tech industry, namely cloud, AI, edge computing, and digital transformation. As these technologies continue to find traction in the industry, hyperscale cloud spend is expected to remain robust, and AI inference workloads will continue to scale. At the same time, edge computing is also expected to gain traction with 5G network densification and a surge in industrial IoT applications. Additionally, the status of data centers as Critical National Infrastructure is also a boon for the industry, with government initiatives to accelerate grid connections and ease the planning process for large infrastructure projects. As a result, supply constraints are also likely to ease over time. In parallel, secondary UK data centers, particularly in Manchester, the Midlands, and Scotland, are also in line for a larger share of new capacity, a trend that is likely to build over time as London becomes increasingly constrained by power and land costs.

UK Data Center Market - Leading Key Players

The UK data center landscape is anchored by global hyperscalers—Amazon Web Services, Microsoft Azure, and Google Cloud. These firms account for an estimated majority of new capacity investment. Major international colocation operators include Equinix, Digital Realty, and CyrusOne. Domestic specialists include VIRTUS Data Centers, Ark Data Centers, and Kao Data. Operators are differentiating through sustainability credentials and AI-ready high-density infrastructure. Other strategies include geographic diversification into secondary markets and developing long-term hyperscaler pre-commitment relationships to support capital investment decisions.

| Company | Leading Brands | Highlights |

|---|---|---|

| VIRTUS Data Centers | LONDON1-6 Campus, TOR1 (Toronto) | UK-focused operator with one of the largest campus footprints in Greater London. Specialises in hyperscale and wholesale colocation, with ongoing campus expansion in the Stockley Park area. Actively investing in AI-ready, high-density infrastructure with liquid cooling capability. |

| Ark Data Centers | Corsham Campus, Farnborough, Cody Park | Specialist in highly secure, government-grade data center provision with OFFICIAL-SENSITIVE and SECRET-accredited facilities. Primary provider of Crown Hosting services to UK central government departments, defence agencies, and national security bodies. |

| Kao Data | KLOUD Campus (Harlow), Slough | Purpose-built carrier-neutral campus operator positioned in the London-Stansted M11 corridor. Known for high-spec sustainable design, renewable energy commitment, and proximity to London connectivity nodes. Active in targeting AI compute and research institution customers. |

Some of the major players in the UK data center market include Equinix Inc., Digital Realty Trust Inc., Amazon Web Services (AWS), Microsoft Azure, Google Cloud, CyrusOne LLC, and Vantage Data Centers.

Latest Development & News

- In September 2025, Vantage Data Centers opened its second London campus, LHR2, in Park Royal, adding 20MW of IT capacity. The facility features one of Europe’s largest public art installations during the London Design Festival, integrates sustainable BREEAM Excellent-certified systems, and supports the UK’s expanding digital and hyperscale infrastructure needs.

- In November 2023, Microsoft announced its commitment to investing 2.5 billion pound in data center and AI-based cloud infrastructure in the UK over three years. This is one of the largest individual technology infrastructure investments announced by a company in the UK.

- In September 2024, The UK government recognizes data centers as Critical National Infrastructure (CNI). As a result, data centers are eligible for government support during cyber-attacks or major outages. The government has also increased efforts to address structural barriers, including grid connections and workforce training, in collaboration with data centers.

UK Data Center Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Solution, Services |

| Types Covered | Colocation, Hyperscale, Edge, Others |

| Enterprise Sizes Covered | Large Enterprises, Small and Medium Enterprises |

| End Users Covered | BFSI, IT and Telecom, Government, Energy and Utilities, Others |

| Regions Covered | London, South East, North West, East of England, South West, Scotland, West Midlands, Yorkshire and The Humber, East Midlands, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the UK Data Center Market Report

The UK data center market was valued at USD 7,459.39 Million in 2025.

The UK data center market is anticipated to reach a value of USD 12,457.48 Million by 2034.

The Solution component dominates the market with a share of 56.3% in 2025, driven by intensive capital investment in power infrastructure, cooling systems, and IT hardware required to equip hyperscale and colocation facilities to the technical standards demanded by enterprise and cloud customers, and increasingly to support the high-density compute requirements of AI workloads.

Hyperscale data centers lead the market with a share of 40.2% in 2025, underpinned by sustained capacity investment from AWS, Microsoft Azure, and Google Cloud, the UK's status as the primary European hyperscale destination, and the rapid growth of AI and cloud workloads driving demand for large-scale, power-dense compute infrastructure.

London currently leads the UK data center market, accounting for a share of 35.1% in 2025. Its dominance is driven by concentration of global financial services headquarters, the LINX internet exchange providing unmatched carrier-neutral connectivity, the presence of all major hyperscalers' UK regions, and the highest density of enterprise colocation demand in the country.

Some of the major players in the UK data center market include Equinix Inc., Digital Realty Trust Inc., Amazon Web Services (AWS), Microsoft Azure, Google Cloud, CyrusOne LLC, VIRTUS Data Centers, Ark Data Centers, Kao Data, Vantage Data Centers, and others.

Key trends include the accelerating demand for AI and high-density compute infrastructure driving adoption of liquid and immersion cooling technologies, the rapid expansion of edge data centers driven by 5G network densification, growing operator commitment to net-zero and renewable energy sourcing, the emergence of Manchester, the Midlands, and Scotland as significant secondary market destinations as London power constraints intensify, and the deepening involvement of institutional infrastructure capital in UK data center assets.

Key growth drivers include the accelerating enterprise and public sector cloud migration, the surge in AI and machine learning workload demands, the UK government's Critical National Infrastructure designation providing regulatory support, 5G-driven edge computing infrastructure requirements, data sovereignty and UK GDPR requirements sustaining onshore hosting demand, FCA and PRA operational resilience rules driving multi-site distribution, and sustained hyperscaler capital investment commitments including Microsoft's GBP 2.5 billion UK investment announced in 2024.

Key challenges include structurally constrained grid power availability in Greater London and the M4/M25 corridor creating multi-year delays for new connections, planning permission complexity particularly in Green Belt areas surrounding the capital, rising UK electricity costs among the highest in Europe impacting operational margins, planning and community opposition to large-scale greenfield facilities, a structural talent shortage in data center operations and engineering disciplines, and the increasing capital cost of meeting tightening sustainability and PUE requirements across new and legacy facilities.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)