UK EdTech Market Size, Share, Trends and Forecast by Sector, Type, Deployment Mode, End User, and Region, 2026-2034

UK EdTech Market Summary:

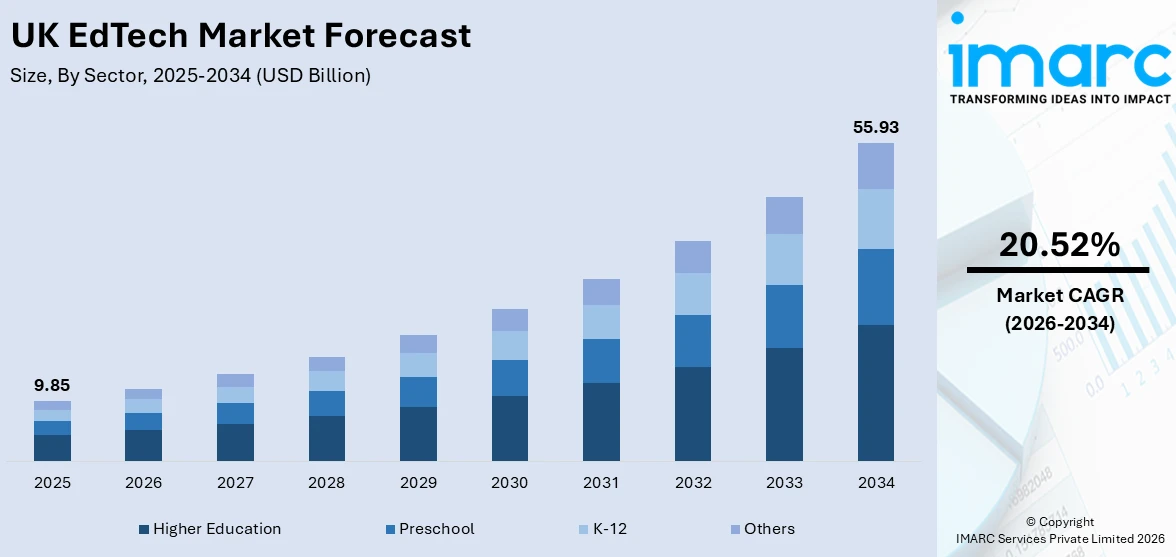

The UK EdTech market size was valued at USD 9.85 Billion in 2025 and is projected to reach USD 55.93 Billion by 2034, growing at a compound annual growth rate of 20.52% from 2026-2034.

The market is gaining significant momentum as educational institutions, government bodies, and enterprises increasingly embrace digital transformation in learning and skills development. Rising demand for personalized and adaptive learning experiences, coupled with growing emphasis on workforce upskilling and reskilling, is accelerating adoption across all education levels. Integration of artificial intelligence, immersive technologies, and data analytics into teaching and assessment frameworks is reshaping how education is delivered and consumed, positioning the United Kingdom as a leading hub for next-generation educational innovation and sharing the UK EdTech market share.

Key Takeaways and Insights:

- By Sector: Higher education dominates the market with a share of 37.2% in 2025, driven by the widespread integration of digital learning platforms, virtual classrooms, and AI-powered tools across universities and colleges.

- By Type: Software leads the market with a share of 52.4% in 2025, reflecting strong adoption of learning management systems, educational applications, and cloud-based collaboration platforms across institutional and enterprise settings.

- By Deployment Mode: Cloud-based solutions hold the largest share at 68.3% in 2025, supported by their scalability, cost-efficiency, and ability to facilitate remote and hybrid learning environments for diverse user groups.

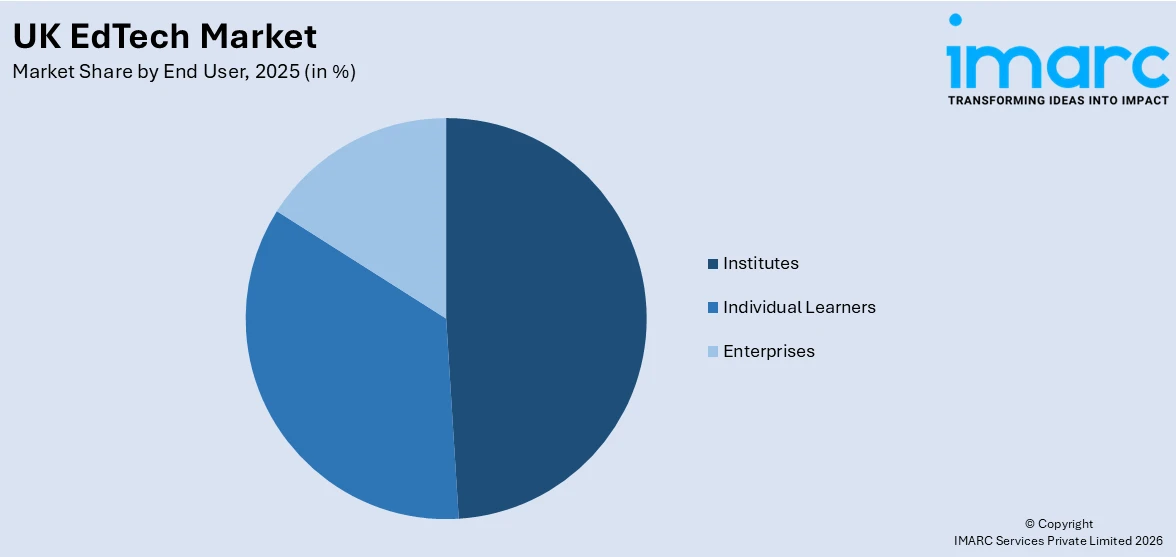

- By End User: Institutes account for the largest share at 48.5% in 2025, owing to growing institutional investments in digital infrastructure, smart classrooms, and technology-enabled assessment systems.

- By Region: London represents the largest regional segment with a 24.6% share in 2025, underpinned by the concentration of EdTech startups, world-class universities, and a thriving technology investment ecosystem.

- Key Players: The UK EdTech market exhibits a dynamic and competitive landscape, with established education companies, innovative startups, and global technology firms competing through product diversification, strategic partnerships, and investments in AI-driven learning solutions.

To get more information on this market Request Sample

The EdTech market in the UK is witnessing revolutionary growth as digital technologies assume a key role in the delivery of education and workforce development in the country. The growing role of AI, ML, and immersive technologies such as virtual and augmented reality is redefining the way students interact with educational content. The digital education strategies and funding programs launched by the government are accelerating the digitalization of the country's education infrastructure, reducing the digital divide, and ensuring the development of future skills. In June 2025, the UK Department of Education launched detailed AI guidelines for schools and announced an investment of GBP 45 million to improve digital connectivity across schools in the country, focusing on wireless network upgrades and fiber connections. Furthermore, the growing need to develop micro-credentials, continuous professional development, and upskilling programs driven by enterprises is expanding the UK EdTech market beyond the traditional academic space, providing fresh revenue streams across the lifelong learning journey.

UK EdTech Market Trends:

Accelerating AI Integration Across Educational Institutions

The implementation of artificial intelligence in the education sector of the UK is progressing at an incredibly fast rate, completely transforming the ways in which education, assessment, and administration are carried out. AI-based tools are being utilized in the education sector of the UK to automate the assessment of students, provide personalized feedback, and develop individualized learning paths that are tailored according to the needs of the students. In 2025, the UK government announced an investment of GBP 1 million specifically to develop AI tools that could be utilized in the classroom for tasks like assessment and feedback, boosting the UK EdTech market growth.

Expansion of Immersive and Extended Reality Learning Experiences

Virtual reality, augmented reality, and extended reality-based immersive technologies are being increasingly adopted by UK-based educational institutions as well as corporate training programs. Apart from this, these tools provide opportunities for experiential learning that increases engagement as well as retention capabilities in complex domains such as medicine, engineering, and vocational studies. Pearson has established its innovation hub in London in July 2025, specifically dedicated to developing scalable solutions with generative AI as well as immersive learning.

Rising Adoption of Digital Credentials and Micro-Learning Pathways

The increased focus on skill-based hiring and professional development is fueling the adoption of digital badges, micro-credentials, and modular learning. These flexible qualification models are helping learners prove their skills to employers. In 2025, the UK government announced a new initiative called TechFirst, with GBP 187 million in funding, to support more training in AI and digital skills through scholarships and community-based projects. Students across the UK will be given the skills and tools to access AI-driven jobs of the future through a new initiative announced by the Prime Minister.

Market Outlook 2026-2034:

The UK EdTech market is poised for sustained expansion over the forecast period, driven by deepening institutional digital transformation, escalating demand for AI-powered learning tools, and growing investments in workforce upskilling infrastructure. Government-led initiatives targeting digital literacy, school connectivity upgrades, and responsible AI deployment in education are expected to strengthen the enabling environment for EdTech adoption. The market generated a revenue of USD 9.85 Billion in 2025 and is projected to reach a revenue of USD 55.93 Billion by 2034, growing at a compound annual growth rate of 20.52% from 2026-2034. The growing convergence of education and enterprise training markets, coupled with rising international student enrolment in digitally-enabled UK universities, will further accelerate demand for scalable, cloud-based educational solutions.

.webp)

UK EdTech Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Sector |

Higher Education |

37.2% |

|

Type |

Software |

52.4% |

|

Deployment Mode |

Cloud-based |

68.3% |

|

End User |

Institutes |

48.5% |

|

Region |

London |

24.6% |

Sector Insights:

- Preschool

- K-12

- Higher Education

- Others

Higher education dominates the UK EdTech market with a 37.2% share of total market revenue in 2025.

The higher education sector dominates the UK EdTech space, owing to the widespread adoption of digital learning platforms, learning management systems, and virtual classroom solutions. The higher education sector of the UK is increasingly embracing AI-powered assessment solutions, data analytics tools, and online certification solutions. The trend of hybrid and blended learning has resulted in sustained demand for sophisticated educational solutions, driven by student demand and evolving learning patterns. The UK’s higher education sector has witnessed increased adoption of digital learning solutions, and this trend is expected to continue.

The increased focus on international student recruitment and flexible learning options is further boosting the segment's market position. Universities are using adaptive learning technology and cloud-based collaborative technology to provide scalable and differentiated education to the geographically dispersed student population. The increased institutional focus on employability-based training programs, micro-credentialing, and digital-based training programs is expanding the scope of EdTech adoption within the higher education sector, which is likely to boost the revenue contribution to the UK EdTech market.

Type Insights:

- Hardware

- Software

- Content

Software leads the UK EdTech market, holding the largest share at 52.4% in 2025.

The software segment has the maximum share in terms of revenue in the UK EdTech industry, owing to the extensive use of learning management systems, assessment tools, student management systems, and collaborative learning tools in academic as well as corporate environments. The increased adoption of AI-based software tools in the field of education is further boosting this segment’s position. The increased demand for subscription-based business models is facilitating access to advanced learning tools across various academic as well as business environments.

In particular, educational software platforms that are cloud-native have seen robust adoption as educational institutions seek integration, analytics, and access across devices. The trend towards digital assessment, virtual proctoring, and analytics continues to fuel software solutions for educational institutions. The trend towards training software for enterprises, including professional and skill development software, is also fueling the software segment’s growth as workforce development becomes an imperative for UK businesses.

Deployment Mode Insights:

- Cloud-based

- On-premises

Cloud-based is the largest segment, accounting for 68.3% of the UK EdTech market in 2025.

Cloud-based deployment holds the commanding share of the UK EdTech market, reflecting the strong preference among educational institutions and enterprises for scalable, flexible, and cost-efficient technology infrastructure. Cloud solutions enable seamless remote and hybrid learning by providing anytime, anywhere access to educational resources, collaboration tools, and assessment platforms. The reduced need for on-site hardware maintenance and upfront capital expenditure makes cloud deployment particularly attractive for resource-constrained schools and smaller educational organizations seeking to modernize their technology environments.

The accelerating migration of institutional IT infrastructure to cloud environments is further reinforcing this segment's dominance. Cloud platforms facilitate rapid deployment of updates, integration with emerging AI and analytics capabilities, and centralized management of multi-campus educational ecosystems. Growing concerns around data security have prompted cloud providers to enhance compliance frameworks, privacy controls, and encryption standards tailored to the education sector. These improvements, combined with government encouragement of cloud-first digital strategies, are sustaining strong adoption momentum across all educational tiers.

End User Insights:

Access the comprehensive market breakdown Request Sample

- Individual Learners

- Institutes

- Enterprises

Institutes hold the largest share at 48.5% of the UK EdTech market in 2025.

The institutes segment represents the largest end-user category in the UK EdTech market, encompassing schools, colleges, universities, and training academies. These institutions are investing heavily in digital infrastructure, smart classroom technologies, and integrated learning management systems to enhance educational delivery and student outcomes. The growing emphasis on evidence-based EdTech procurement, supported by government-backed testbed programs, is enabling institutions to make informed technology adoption decisions that align with pedagogical goals and operational efficiency requirements.

Multi-academy trusts and university networks are increasingly adopting centralized digital platforms that streamline administration, standardize content delivery, and enable data-driven insights across multiple campuses. The rising demand for accessibility-compliant technologies, assistive learning tools, and inclusive digital experiences is further expanding institutional spending on EdTech solutions. Institutions are also prioritizing cybersecurity investments and data governance frameworks as digital adoption deepens, recognizing the critical importance of protecting student data and ensuring compliance with evolving regulatory standards.

Regional Insights:

- London

- South East

- North West

- East of England

- South West

- Scotland

- West Midlands

- Yorkshire and the Humber

- East Midlands

- Others

London accounts for the highest revenue share at 24.6% of the UK EdTech market in 2025.

London holds the dominant position in the UK EdTech market, driven by its status as a major European technology and innovation hub. The region benefits from a dense concentration of EdTech startups, world-renowned universities, and strong venture capital activity that fuels continuous innovation in educational technology. London hosts major global EdTech events and serves as a gateway for international EdTech firms entering the UK market. The availability of specialized talent, proximity to government policymakers, and a robust digital infrastructure ecosystem further reinforce London's leadership position in the market.

The region's diverse student population, extensive network of higher education institutions, and thriving corporate training sector create sustained demand for advanced educational technologies. University-led research programs and EdTech accelerators in London are driving innovation in AI-powered learning, assessment technologies, and immersive educational content. Strong public and private sector collaboration, combined with favorable policies supporting digital education and skills development, positions London as the primary engine of growth for the UK EdTech market.

Market Dynamics:

Growth Drivers:

Why is the UK EdTech Market Growing?

Strong Government Support and Strategic Investment in Digital Education

The UK government is playing a pivotal role in driving EdTech market growth through comprehensive digital education strategies, dedicated funding programs, and policy frameworks that encourage technology adoption across all educational tiers. National initiatives focused on enhancing digital connectivity in schools, expanding AI literacy programs, and modernizing educational infrastructure are creating a robust foundation for widespread EdTech deployment. Government-sponsored testbed programs and innovation hubs are enabling educational institutions to evaluate and adopt evidence-based technology solutions with confidence. The establishment of clear guidance on responsible AI use in education and the development of standardized frameworks for EdTech procurement are reducing adoption barriers and fostering a more supportive regulatory environment for educational technology providers. In 2026, UK's Department for Education announced the summit along with £45 million in additional funding to enhance digital connectivity in English schools, £1 million to expedite AI-driven marking and feedback tools, and £3 million to create AI training datasets for educational use. The actions are part of a wider initiative by Education Secretary Bridget Phillipson to utilize AI as a means of lowering teacher workload and enhancing student results.

Escalating Demand for Personalized and Adaptive Learning Experiences

The growing recognition that learners have diverse needs, learning paces, and knowledge gaps is fueling demand for personalized and adaptive educational technologies across the UK. Educational institutions and corporate training providers are increasingly adopting AI-driven platforms that dynamically adjust content, assessments, and learning pathways based on individual learner performance and engagement patterns. The shift away from one-size-fits-all pedagogical approaches is creating strong market demand for intelligent tutoring systems, recommendation engines, and data analytics tools that enable educators to deliver targeted interventions and improve learning outcomes. This trend is reinforced by rising expectations from both students and employers for flexible, outcome-oriented educational experiences that align with evolving career and skills requirements.

Growing Enterprise Focus on Workforce Upskilling and Digital Transformation

The rapid pace of technological change, particularly the proliferation of artificial intelligence across industries, is compelling UK enterprises to invest significantly in workforce development and digital skills training. Organizations are recognizing that continuous upskilling and reskilling of employees is essential to maintaining competitiveness and addressing widening skills gaps. This has created a substantial and growing market for enterprise-grade EdTech solutions that deliver scalable professional training, digital certification, and competency assessment capabilities. The convergence of education and corporate training markets is broadening the addressable audience for EdTech platforms, with solutions increasingly designed to serve both academic institutions and business clients seeking integrated learning and credentialing ecosystems.

Market Restraints:

What Challenges the UK EdTech Market is Facing?

Persistent Digital Divide and Uneven Technology Access

Despite growing investments in digital infrastructure, significant disparities in technology access persist across different regions, socioeconomic groups, and educational institutions within the UK. Rural and economically disadvantaged areas often face limited broadband connectivity, outdated hardware, and insufficient technical support, creating barriers to equitable EdTech adoption. This uneven digital landscape restricts the reach and impact of educational technology solutions, particularly for learners who stand to benefit the most from digitally-enabled educational opportunities.

Data Privacy and Cybersecurity Concerns in Education

The expanding use of digital platforms and AI-powered tools in educational settings raises growing concerns about data privacy, student safety, and cybersecurity vulnerabilities. Educational institutions handle large volumes of sensitive personal information, making them attractive targets for cyberattacks. Stringent regulatory requirements, evolving data protection legislation, and the need for robust compliance frameworks increase operational complexity and costs for EdTech providers, potentially slowing adoption among institutions with limited resources to manage data governance effectively.

Limited Digital Literacy and Teacher Preparedness

While technology adoption in education is accelerating, many educators still lack the confidence and training needed to effectively integrate digital tools into their teaching practice. Insufficient professional development opportunities, time constraints, and institutional resistance to change hinder the meaningful adoption of EdTech solutions. Without adequate training and ongoing support, the potential benefits of educational technology remain underutilized, creating a gap between the availability of advanced tools and their effective deployment in classroom and training environments.

Competitive Landscape:

The UK EdTech market features a highly dynamic and competitive landscape characterized by the presence of established global education technology providers, innovative domestic startups, and major technology corporations expanding their education-focused offerings. Competition is primarily driven by the ability to deliver scalable, AI-enhanced learning solutions, build trusted partnerships with educational institutions, and demonstrate measurable improvements in learning outcomes. Market participants are actively pursuing strategies including product diversification, strategic acquisitions, and partnerships with technology leaders to strengthen their market positions. Investment in research and development, particularly in AI, immersive learning technologies, and adaptive platforms, remains a key differentiator. The market also benefits from a vibrant startup ecosystem supported by dedicated venture capital funds, government-backed accelerators, and innovation programs that foster continuous entrepreneurial activity in the educational technology space.

UK EdTech Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Sectors Covered | Preschool, K-12, Higher Education, Others |

| Types Covered | Hardware, Software, Content |

| Deployment Modes Covered | Cloud-based, On-premises |

| End Users Covered | Individual Learners, Institutes, Enterprises |

| Regions Covered | London, South East, North West, East of England, South West, Scotland, West Midlands, Yorkshire and The Humber, East Midlands, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the UK EdTech Market Report

The UK EdTech market size was valued at USD 9.85 Billion in 2025.

The market is expected to grow at a compound annual growth rate of 20.52% from 2026-2034 to reach USD 55.93 Billion by 2034.

Higher education, holding the largest revenue share of 37.2%, leads the UK EdTech market driven by widespread digital platform adoption, virtual classroom integration, and growing demand for AI-enhanced teaching and assessment tools across universities and colleges.

Key factors driving the UK EdTech market include strong government support for digital education, rising demand for personalized and adaptive learning, growing enterprise focus on workforce upskilling, integration of AI and immersive technologies, and expanding cloud-based educational infrastructure.

Major challenges include the persistent digital divide and uneven technology access across regions, growing data privacy and cybersecurity concerns, limited digital literacy among educators, fragmented procurement processes, and the need for sustained investment in teacher training and support.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade