UK Food Delivery Market Size, Share, Trends and Forecast by Business Model, Order Type, Payment Method, Platform Type, and Region, 2026-2034

UK Food Delivery Market Summary:

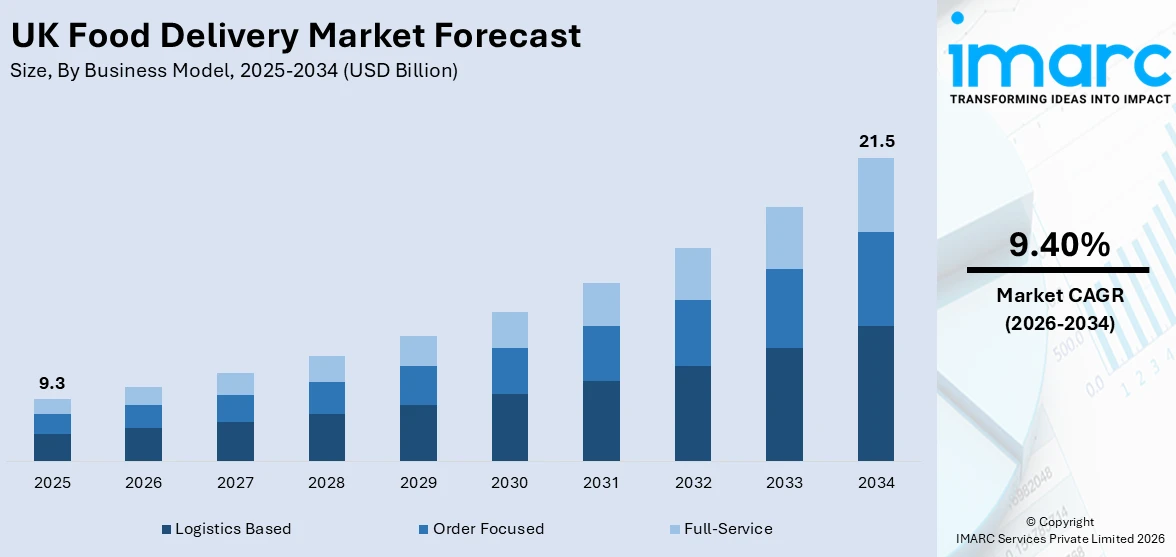

The UK food delivery market size was valued at USD 9.3 Billion in 2025 and is projected to reach USD 21.5 Billion by 2034, growing at a compound annual growth rate of 9.40% from 2026-2034.

The UK food delivery market is experiencing growth, propelled by a digitally connected user base, rising demand for convenience, and the proliferation of smartphone-enabled ordering platforms. The evolving dietary preferences and the mainstreaming of on-demand services are collectively transforming how consumers access restaurant meals, grocery essentials, and specialty food products. Continuous innovations across logistics technology, last-mile delivery infrastructure, and cloud kitchen models are reshaping the competitive landscape, creating substantial opportunities for platform operators, restaurant partners, and technology providers seeking to capture growing UK food delivery market share.

Key Takeaways and Insights:

- By Business Model: Logistics based dominates the market with a share of 48.3% in 2025, owing to its comprehensive end-to-end delivery management capabilities, enabling seamless fulfilment for restaurants and retail partners across urban and suburban areas.

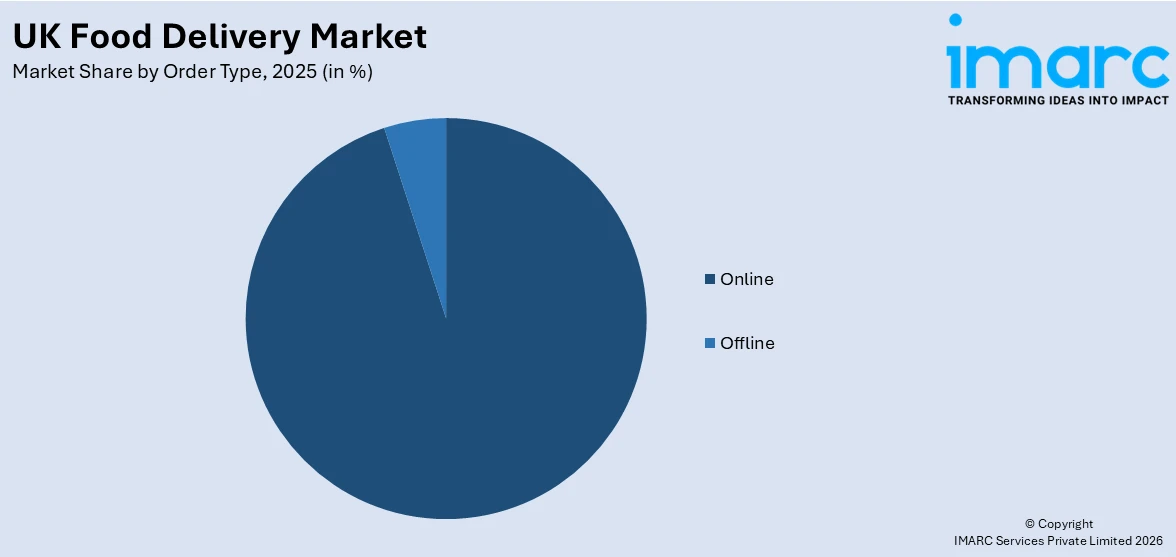

- By Order Type: Online London represents the largest segment with a market share of 94.2% in 2025, reflecting the widespread consumer preference for digital platforms that offer convenience, real-time tracking, and personalized meal recommendations.

- By Payment Method: Online payment leads the market with a share of 85.6% in 2025, underpinned by the rapid adoption of digital wallets, contactless card transactions, and integrated payment gateways that streamline the checkout experience for users.

- By Platform Type: Mobile applications dominate the market with a share of 72.4% in 2025, influenced by the convenience of app-based ordering, real-time delivery tracking, loyalty program integration, and AI-powered personalized recommendations on smartphones.

- By Region: London represents the largest segment with a market share of 24.8% in 2025, driven by high population density, strong demand for convenience, and widespread platform penetration.

- Key Players: The UK food delivery market exhibits highly competitive intensity, with major aggregator platforms competing alongside direct restaurant delivery services, focusing on technology investment, expanded restaurant networks, subscription models, and logistics optimization to strengthen market positioning.

To get more information on this market Request Sample

The UK food delivery market is driven by changing consumer lifestyles, rising preference for convenience, and increasing digital adoption. Busy urban populations continue to rely on quick-service solutions, supported by widespread smartphone usage and seamless app-based ordering. The expansion of restaurant partnerships and cloud kitchens has further broadened cuisine options, attracting a larger customer base. The growing disposable incomes and demand for premium and international food choices are also influencing the market. In addition, advancements in logistics and last-mile delivery are improving speed and reliability. Companies are actively investing in technology to enhance efficiency and reduce operational costs. In 2025, Uber announced the rollout of autonomous delivery robots in UK cities such as Leeds and Sheffield, starting in December, enabling food and grocery deliveries within 30 minutes over short distances using AI-based navigation. This move reflects the increasing focus on automation to optimize delivery operations and improve customer experience across the market.

UK Food Delivery Market Trends:

Rise of Rapid Meal Kit Delivery Models

The UK food delivery market is witnessing a growing shift toward rapid delivery of meal kits that combine convenience with home cooking. Consumers are increasingly seeking solutions that reduce preparation time while maintaining freshness and customization. In 2024, HelloFresh partnered with Just Eat to trial 30-minute delivery of recipe kits in Newcastle and Hackney, offering pre-portioned ingredients and guided recipes starting at £13.99 for two. This model bridges the gap between takeaway and home-cooked meals. The trend supports demand for healthier, flexible dining options while enabling platforms to diversify beyond traditional restaurant delivery and tap into evolving consumer preferences.

Integration of Delivery and Order Management Systems

A key trend shaping the UK food delivery market is the integration of delivery logistics with centralized order management platforms. Restaurants are increasingly adopting unified systems that allow seamless coordination of orders, inventory, and last-mile delivery. In 2024, Stuart partnered with Deliverect to integrate delivery services directly with order management systems, enabling businesses to manage operations through a single interface. This approach reduced errors, improved efficiency, and enhanced customer experience. It also supported scalability for restaurants transitioning to digital-first models, allowing them to handle higher order volumes while maintaining service quality and operational control across multiple sales channels.

Emergence of Drone-Based Food Delivery Solutions

The adoption of drone technology is emerging as a future-oriented trend aimed at improving delivery speed and operational efficiency. Companies are exploring aerial delivery systems to overcome urban traffic challenges and reduce delivery times. In 2025, Manna Aero announced plans to introduce the UK’s first food drone delivery pilot by 2026, leveraging quadcopters capable of transporting meals at low altitudes. With over 200,000 successful deliveries in other markets, the model demonstrates strong potential for scalability. This trend reflects growing investment in innovative logistics solutions, although regulatory approvals and concerns around noise and urban deployment remain key considerations.

Market Outlook 2026-2034:

The UK food delivery market is poised for sustained revenue growth throughout the forecast period, underpinned by strong structural demand, continuous technological advancement, and deepening platform-retailer partnerships. The market generated a revenue of USD 9.3 Billion in 2025 and is projected to reach a revenue of USD 21.5 Billion by 2034, growing at a compound annual growth rate of 9.40% from 2026-2034. Growth will be driven by the maturation of cloud kitchen ecosystems, greater penetration of mobile-first ordering in secondary cities, expanding quick commerce offerings, and AI-powered personalization technologies. Strategic consolidation across the competitive landscape will further accelerate innovation and service diversification, reinforcing the market's robust long-term trajectory.

UK Food Delivery Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Business Model |

Logistics Based |

48.3% |

|

Order Type |

Online |

94.2% |

|

Payment Method |

Online Payment |

85.6% |

|

Platform Type |

Mobile Applications |

72.4% |

|

Regional Insights |

London |

24.8% |

Business Model Insights:

- Order Focused

- Logistics Based

- Full-Service

The logistics-based dominates with a market share of 48.3% of the total UK food delivery market in 2025.

Logistics based leads the market due to its ability to offer extensive restaurant selection and efficient delivery services through centralized platforms. This model connects multiple restaurants with a wide customer base, providing convenience and variety in one place. By managing delivery operations independently, platforms ensure faster service, optimized routing, and better control over delivery quality. This approach allows restaurants without in house delivery capabilities to expand their reach. Additionally, advanced tracking systems and real time updates enhance customer experience, making logistics based platform highly preferred across urban areas.

The dominance of logistics based is further driven by its scalability and strong operational infrastructure. This platform leverages data analytics and automated systems to manage high order volumes and optimize delivery efficiency. The flexibility to onboard diverse restaurant partners increases platform attractiveness for consumers seeking variety. Furthermore, consistent service standards, promotional offers, and subscription models encourage repeat usage. Investments in delivery fleets, technology integration, and last mile logistics strengthen service reliability. As demand for quick and convenient food delivery continues to rise, logistics based model maintains a leading position in the market.

Order Type Insights:

Access the comprehensive market breakdown Request Sample

- Online

- Offline

Online leads with a market share of 94.2% of the total UK food delivery market in 2025.

Online represents the largest segment because of the increasing reliance on digital platforms for convenient and seamless food ordering. Consumers prefer online channels as they offer easy access to a wide range of restaurants, menu options, and pricing comparisons. Mobile applications and websites enable quick ordering, secure payments, and real time tracking, enhancing the overall user experience. The growing penetration of smartphones and internet connectivity further supports this shift toward digital ordering. Additionally, personalized recommendations, discounts, and loyalty programs available on online platforms encourage higher engagement and repeat purchases among users.

The dominance of online orders is influenced by the integration of advanced technologies that enhance efficiency and customer experience. Features, such as automated order processing, digital payment systems, and AI-based recommendations simplify and personalize the ordering journey. In 2025, IKEA Birmingham launched a pilot food delivery and click-and-collect service, enabling customers to order up to 80% of its Swedish Food Market range within a 10-mile radius, highlighting the shift toward convenience-led digital access. Additionally, quick commerce expansion, contactless delivery, and strong platform-restaurant partnerships continue to reinforce the preference for online channels.

Payment Method Insights:

- Online Payment

- Cash on Delivery

Online payment exhibits a clear dominance with 85.6% share of the total UK food delivery market in 2025.

Online payment dominates the market owing to its convenience, speed, and secure transaction process. Consumers increasingly prefer digital payment options such as cards, mobile wallets, and app-based payments that allow seamless checkout without handling cash. The integration of secure payment gateways and encryption technologies enhances trust among users. Additionally, online payments enable quick order confirmation and reduce delays during delivery. The widespread use of smartphones and digital banking services further supports this shift. Incentives such as cashback offers, discounts, and loyalty rewards also encourage consumers to adopt online payment methods.

The dominance of online payment is further supported by the growing emphasis on contactless transactions and improved user experience. Digital payment methods simplify the ordering process by storing user preferences and payment details for faster repeat purchases. Food delivery platforms actively promote online payments through exclusive deals and in app benefits. Moreover, businesses benefit from reduced cash handling risks and improved transaction tracking. Integration with financial technologies and real time processing ensures efficiency and reliability. As digital adoption continues to rise, online payment remains the preferred choice, reinforcing its leading position in the market.

Platform Type Insights:

- Mobile Applications

- Websites

- Others

Mobile applications dominate with a market share of 72.4% of the total UK food delivery market in 2025.

Mobile applications hold the biggest market share attributed to their ease of use, accessibility, and seamless user experience. Consumers prefer mobile apps for ordering food as they offer quick navigation, personalized recommendations, and secure payment options. The widespread adoption of smartphones and improved mobile internet connectivity has significantly increased app-based ordering. Features, such as real time order tracking, push notifications, and saved preferences enhance convenience and encourage repeat usage. Additionally, mobile apps allow users to explore multiple restaurants, compare options, and place orders efficiently, making them the preferred platform across various consumer groups.

The dominance of mobile applications is reinforced by continuous technological advancements and strong user engagement strategies. Companies focus on app optimization, intuitive interfaces, and data-driven personalization to enhance user experience and satisfaction. In 2025, Totalee Halal, the UK’s first halal-only food delivery app, was launched in London, offering certified halal food, groceries, and fresh meat, catering to niche consumer demand through a dedicated mobile platform. Additionally, in-app discounts, loyalty programs, seamless payment integration, and real-time communication features further drive frequent usage and strengthen customer retention.

Regional Insights:

- London

- South East

- North West

- East of England

- South West

- Scotland

- West Midlands

- Yorkshire and The Humber

- East Midlands

- Others

London leads with a market share of 24.8% of the total UK food delivery market in 2025.

London leads the UK food delivery market in terms of region due to its high population density, diverse consumer base, and fast paced urban lifestyle. The city has a large working population, students, and young professionals who rely heavily on convenient meal options due to busy schedules. High smartphone penetration and strong digital adoption further support frequent use of food delivery platforms. Additionally, London offers a wide variety of cuisines and restaurants, increasing demand for delivery services. The presence of numerous delivery partners and efficient logistics infrastructure ensures quick service, reinforcing the city’s leading position in the market.

The region’s dominance also benefits from higher disposable incomes and strong consumer willingness to spend on convenience and premium food options. London’s dynamic food culture also drives frequent ordering across diverse cuisines, supported by expanding cloud kitchens and quick commerce networks. In 2026, Amazon launched “Amazon Now” in London, offering grocery delivery within 30 minutes across thousands of products, reflecting rising demand for ultra-fast delivery services. Additionally, intense competition among platforms, along with continuous technological innovation and promotional strategies, enhances service quality and sustains high consumer engagement.

Market Dynamics:

Growth Drivers:

Why is the UK Food Delivery Market Growing?

Adoption of Artificial intelligence (AI)-Driven Personalization in Ordering

Artificial intelligence (AI) is increasingly being integrated into food delivery platforms to enhance personalization and simplify user interactions. AI-powered tools analyze user preferences and behavior to recommend tailored meal options, improving engagement and conversion rates. For example, in 2026, Just Eat introduced an AI-powered voice assistant within its UK app, acting as a food concierge that suggests meals based on individual preferences and supports multiple languages. This innovation enhanced accessibility while streamlining the ordering process. The trend highlights the role of intelligent automation in improving user experience and driving customer retention in a competitive digital marketplace.

Growth of Hyperlocal Hourly Delivery Services

The UK market is experiencing a rise in hyperlocal delivery models that focus on ultra-fast fulfilment of everyday essentials. Consumers increasingly expect near-instant access to food, beverages, and household items through mobile platforms. In line with this, in 2025, AliExpress launched an hourly delivery service in Greater London, enabling same-day delivery of products, including snacks and drinks, through partnerships with local providers like Hungry Panda. This approach strengthened local fulfilment networks and supports faster service. This reflects the growing importance of speed and convenience, encouraging platforms to build localized supply chains and expand their presence in urban areas.

Expansion of Quick Commerce Through Retail Partnerships

Partnerships between food delivery platforms and major retailers are contributing to the growth of quick commerce in the UK. These collaborations enable rapid delivery of groceries and essential items, meeting increasing demand for convenience-driven shopping. In 2025, Just Eat Go partnered with Tesco to expand the Tesco Whoosh service, supporting on-demand delivery across multiple store formats. This initiative enhanced access to convenience retail, particularly during high-demand periods, such as festive seasons. This highlights the convergence of food delivery and grocery retail, allowing platforms to diversify offerings and strengthen their position in the evolving on-demand economy.

Market Restraints:

What Challenges the UK Food Delivery Market is Facing?

Rising Operational and Labor Costs

Escalating labor costs, fuel expenses, and insurance premiums are placing significant pressure on delivery platform margins and restaurant partner economics. The implementation of higher minimum wage thresholds and evolving gig economy regulations in the UK are increasing per-delivery operational costs, complicating profitability at the platform level and potentially constraining the sustainability of competitive fee structures that have historically driven consumer adoption and market growth.

Intensifying Platform Competition and Commission Pressures

The highly concentrated nature of the UK food delivery aggregator market, dominated by a small number of large platforms, creates intense competitive pressure that can suppress unit economics across the value chain. Restaurant partners face substantial commission charges that erode margins, while platforms must invest heavily in marketing, technology, and courier incentives to maintain market share.

Regulatory Complexity and Worker Classification Challenges

The UK food delivery market operates within an evolving regulatory framework concerning gig worker classification, right-to-work verification, and platform accountability. Legislative changes requiring enhanced identity checks and potential shifts in employment status rules for couriers could increase labor costs and operational complexity for major platforms. Navigating these regulatory requirements while maintaining the flexible workforce models that underpin current delivery economics represents a persistent structural challenge.

Competitive Landscape:

The UK food delivery market features a highly competitive structure characterized by a small number of dominant aggregator platforms competing aggressively for restaurant partnerships, courier capacity, and consumer loyalty. Market participants are investing in differentiated technology capabilities, including AI-powered personalization, real-time logistics management, and subscription membership programs, to drive order frequency and reduce churn. The market is also witnessing increasing participation from direct restaurant delivery operations and specialist quick commerce providers, diversifying the competitive landscape beyond traditional third-party platforms. Strategic consolidation, including high-profile mergers and acquisitions, is reshaping the competitive hierarchy while expanding the geographic and product scope of leading players. Competition is increasingly extending across grocery delivery, retail verticals, and cloud kitchen ecosystems, incentivizing continuous innovation and service diversification.

Recent Developments:

- December 2025: Netflix launched a Stranger Things-themed delivery-only restaurant, Hawkins Diner, across 150 UK locations via Deliveroo. The concept offers a menu of American-style comfort food inspired by the show, targeting fans ahead of the final season release. This initiative blends entertainment with food delivery, creating an at-home themed dining experience to boost engagement.

- July 2025, Amazon partnered with Gopuff to expand ultra-fast delivery across major UK cities, enabling customers to receive groceries and daily essentials within 15–60 minutes through urban micro-fulfillment centers. The service offered flexible pricing based on order value and targets dense urban areas where speed and convenience are critical. This move strengthens Amazon’s quick commerce strategy by leveraging partnerships instead of heavy infrastructure investment while increasing frequency of consumer purchases.

UK Food Delivery Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Business Models Covered | Order Focused, Logistics Based, Full-Service |

| Order Types Covered | Online, Offline |

| Payment Methods Covered | Online Payment, Cash on Delivery |

| Platform Types Covered | Mobile Applications, Websites, Others |

| Regions Covered | London, South East, North West, East of England, South West, Scotland, West Midlands, Yorkshire and The Humber, East Midlands, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the UK Food Delivery Market Report

The UK food delivery market size was valued at USD 9.3 Billion in 2025.

The UK food delivery market is expected to grow at a compound annual growth rate of 9.40% from 2026-2034 to reach USD 21.5 Billion by 2034.

The logistics-based holds the largest revenue share of 48.3% in 2025, driven by its comprehensive fulfilment capabilities and scalable courier network that supports diverse restaurant and retail delivery requirements.

Key factors driving the UK food delivery market include the rising demand for convenient yet home-style meal solutions, supported by rapid meal kit delivery models. In 2024, HelloFresh partnered with Just Eat to offer 30-minute recipe kit deliveries, enabling quick, customizable cooking experiences for consumers.

Major challenges include rising operational and labor costs driven by higher minimum wage requirements, intensifying platform competition that pressures commission structures, and evolving regulatory frameworks concerning gig worker classification and right-to-work verification obligations for delivery platforms.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)