UK Logistics Market Size, Share, Trends and Forecast by Model Type, Transportation Mode, End Use, and Region 2026-2034

UK Logistics Market Size, Share, Trends & Forecast (2026-2034)

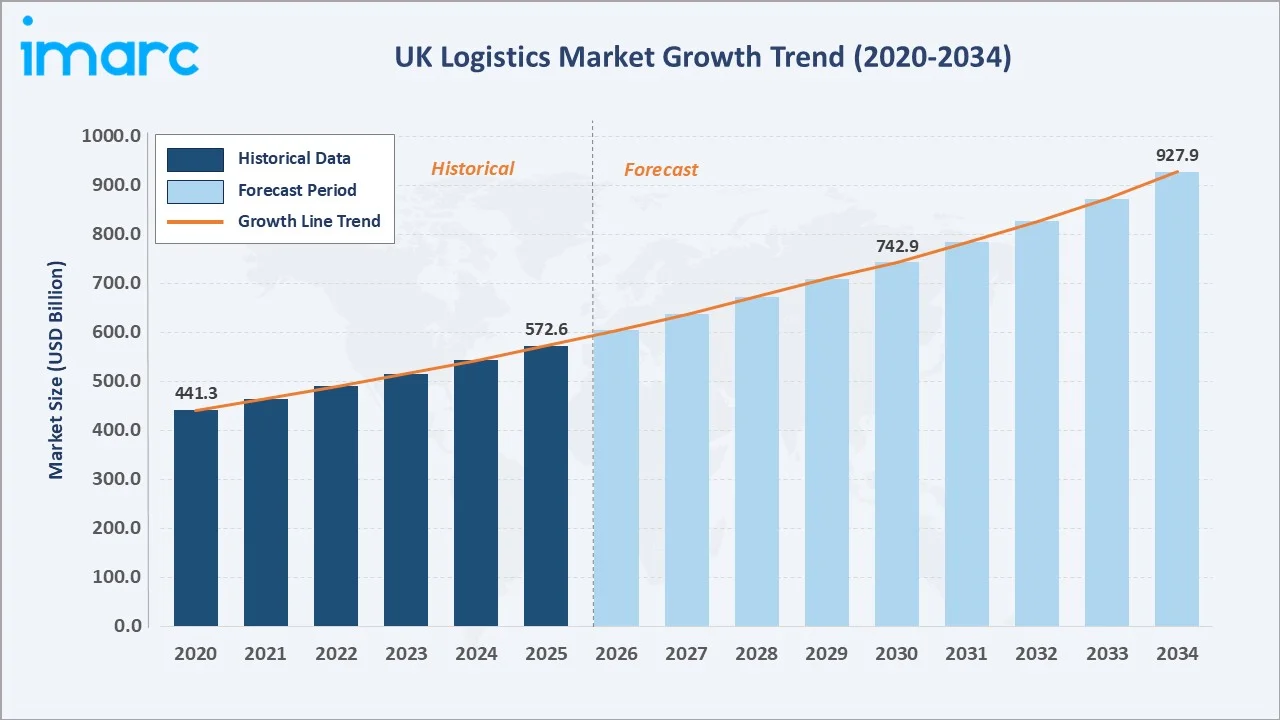

The UK logistics market size reached USD 572.6 Billion in 2025 and is projected to reach USD 927.9 Billion by 2034, exhibiting a CAGR of 5.3% during 2026-2034. Rising e-commerce volumes, expanding trade networks, and rapid technology adoption are driving this robust expansion.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 572.6 Billion |

|

Forecast Market Size (2034) |

USD 927.9 Billion |

|

CAGR (2026-2034) |

5.3% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

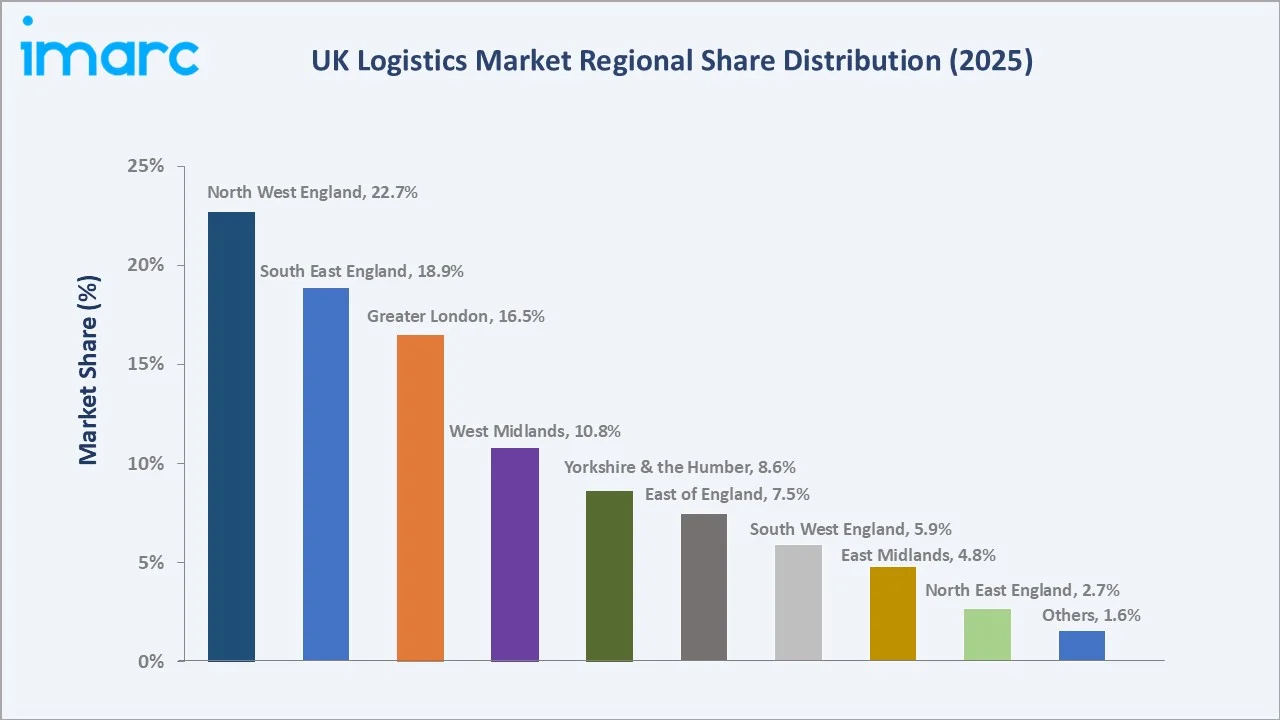

North West England (22.7% share, 2025) |

|

Fastest Growing Region |

Greater London (CAGR ~ 7.5%) |

|

Leading Model Type |

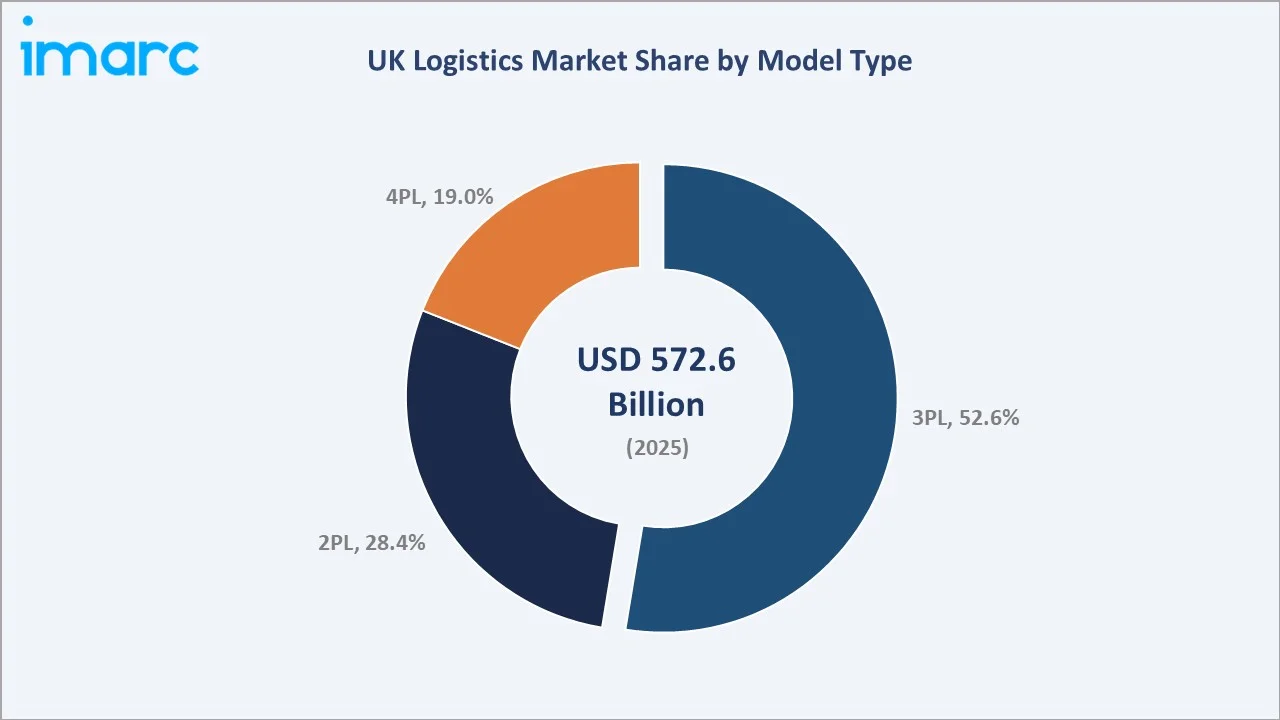

3PL (52.6%, 2025) |

|

Leading Transport Mode |

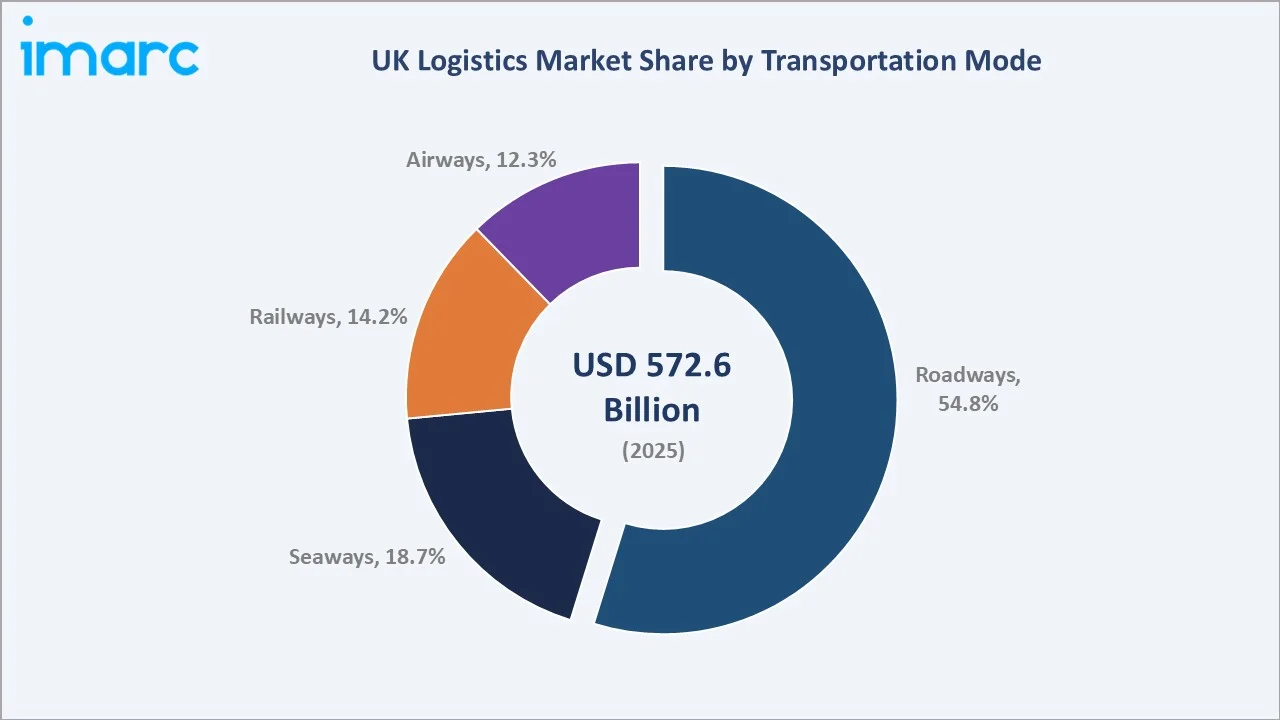

Roadways (54.8%, 2025) |

To get more information on this market, Request Sample

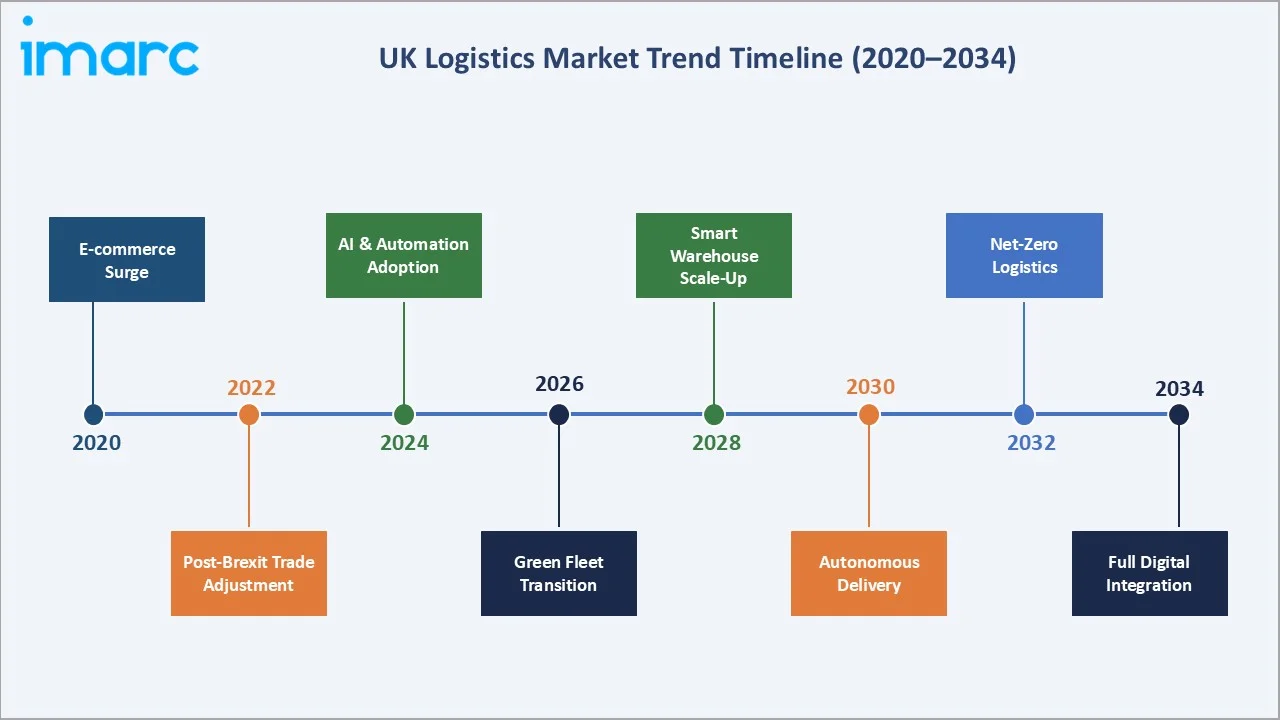

The chart below illustrates the UK logistics market growth trajectory from 2020 through 2034, contrasting historical expansion against a sustained forecast curve powered by e-commerce growth, infrastructure investment, and digital transformation of supply chains.

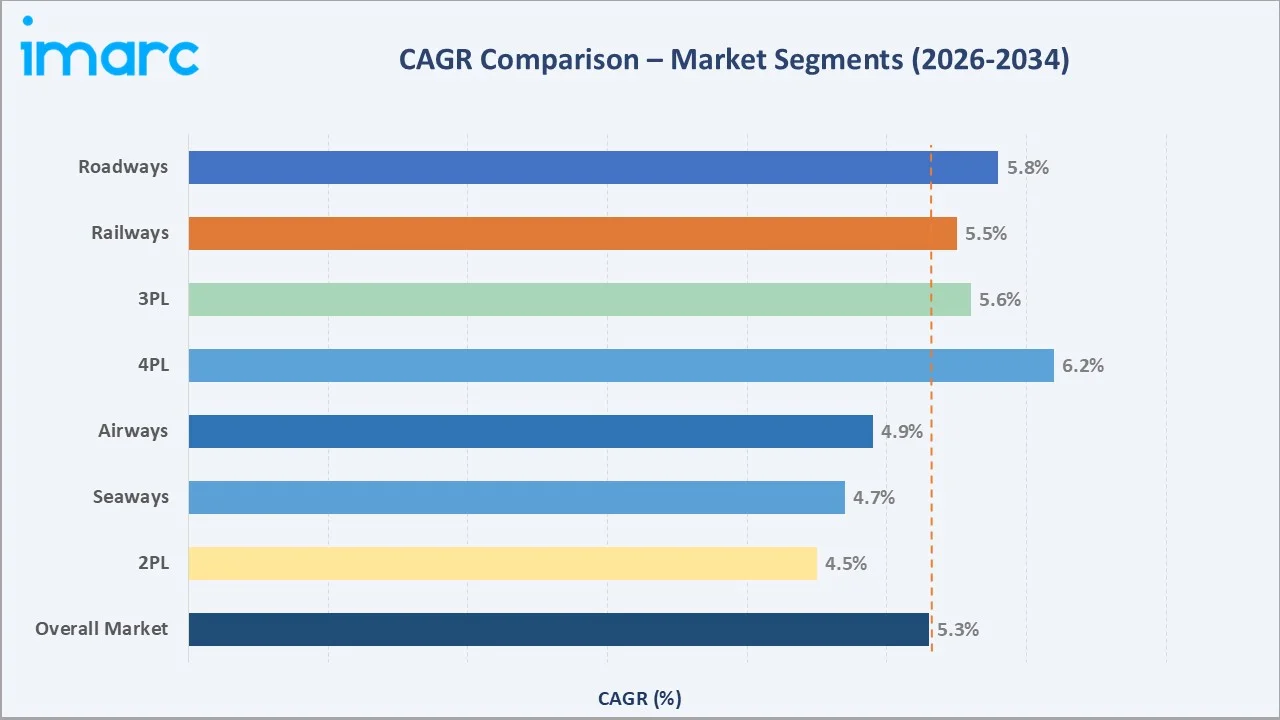

Segment-level CAGR comparisons highlighting 4PL adoption and roadways expansion as the fastest-growing sub-categories within the UK logistics market forecast through 2034.

Executive Summary

The UK logistics industry is undergoing a structural transformation. Growing from USD 441.3 Billion in 2020 to USD 572.6 Billion in 2025, with the market reaching USD 742.9 Billion by 2030 and USD 927.9 Billion by 2034 at a CAGR of 5.3% during 2026-2034. Key growth catalysts include the rapid expansion of e-commerce fulfilment networks, sustained investment in warehousing infrastructure, and post-Brexit realignment of trade logistics frameworks.

Third-party logistics (3PL) providers command 52.6% of market revenue in 2025, reflecting the outsourcing trend among UK manufacturers and retailers. Roadways represent the dominant transportation mode at 54.8%, are growing demand for time-sensitive pharmaceutical and technology freight.

North West England contributes 22.7% of national revenue, anchored by major distribution hubs in Manchester and Liverpool. The competitive landscape remains dynamic, with global operators including DHL Supply Chain and XPO Logistics competing alongside specialist UK providers such as Wincanton and Clipper Logistics.

Key Market Insights

|

Insight |

Data |

|

Largest Model Type |

3PL - 52.6% share (2025) |

|

Second Model Type |

2PL - 28.4% share (2025) |

|

Fastest Growing Model Type |

4PL - est. 6.2% CAGR (2034) |

|

Leading Transport Mode |

Roadways - 54.8% share (2025) |

|

Leading Region |

North West England - 22.7% revenue share (2025) |

|

Top Companies |

DHL Group, XPO, Inc., DB Schenker, Kuehne+Nagel, Evri Limited, Royal Mail Group Limited, DFDS |

|

Market Opportunity |

Green logistics and last-mile delivery innovation |

Key Analytical Observations Supporting the Above Data:

- 3PL Dominance: 3PL's 52.6% dominance in 2025 reflects the strong outsourcing trend among UK retailers and manufacturers, driven by the need for cost efficiency, scalability, and access to specialist expertise in cross-border and last-mile fulfillment.

- 2PL Relevance: 2PL's 28.4% share underscores the continued relevance of asset-based freight providers - particularly in road haulage and port-based shipping - that manage transportation without taking ownership of inventory.

- 4PL Acceleration: 4PL is the fastest-growing model type, estimated at a CAGR of 6.2% through 2034, as large enterprises seek integrated supply chain orchestration solutions that leverage AI-driven analytics and end-to-end visibility platforms.

- Roadways Leadership: Roadways' 54.8% share is underpinned by the UK's extensive national road network and the exponential growth of home delivery demand - fuelled by e-commerce penetration rising to over 27% of total retail sales in 2024.

- North West England Hub: North West England's 22.7% regional dominance reflects strategic investment in logistics parks around Manchester, Salford, and Liverpool docks, positioning the region as the UK's primary inland and port-based distribution corridor.

UK Logistics Market Overview

Logistics encompasses the comprehensive management of goods movement from point of origin to point of consumption, integrating transportation, warehousing, inventory control, order processing, and reverse logistics. The UK logistics sector serves as a critical enabler for domestic retail, manufacturing, healthcare, and e-commerce industries.

The industry is shaped by macroeconomic forces including post-Brexit trade policy realignment, evolving consumer expectations for rapid delivery, rising infrastructure investment, and stringent environmental regulation. The UK government's Levelling Up agenda and National Infrastructure Strategy continue to direct capital toward transport corridors in the Midlands and North of England, directly influencing logistics capacity and regional market development through 2034.

Market Dynamics

To evaluate market opportunities, Request Sample

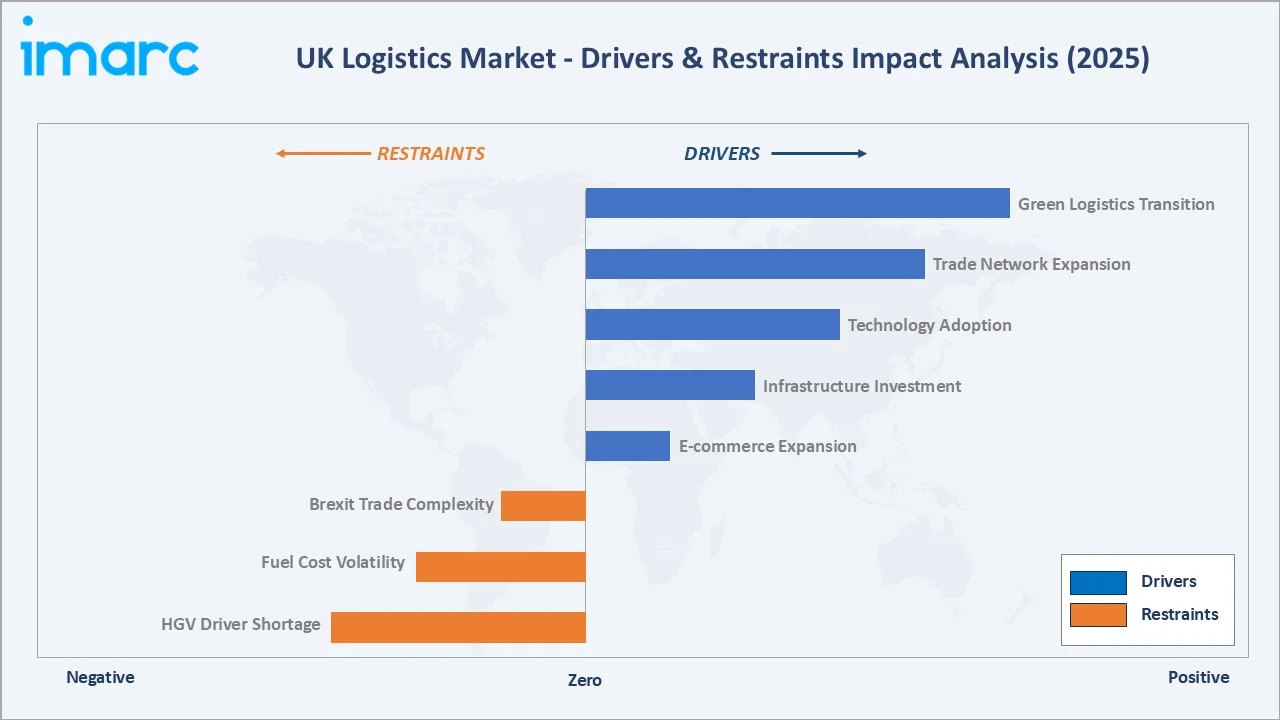

Market Drivers

- E-commerce Expansion: E-commerce penetration in the UK reached approximately 27.5% of total retail sales in 2024, creating sustained demand for last-mile delivery infrastructure, urban micro-fulfillment centers, and returns management platforms.

- Infrastructure Investment: The British Government has announced a GBP 15.6 billion (EUR 18.5 billion) funding for city region local transport projects in England’s city regions, including South Yorkshire, the North East, the East Midlands and Tees Valley.

- Technology Adoption: Automation, AI-powered route optimization, IoT-enabled fleet telematics, and robotic warehouse systems are reducing operational costs for early-adopter logistics operators, accelerating competitive differentiation.

- Trade Network Expansion: Expansion of UK trade agreements with GCC nations, Australia, and Southeast Asian economies following post-Brexit trade realignment has driven the growth of international freight volumes through UK ports and airports.

Market Restraints

- HGV Driver Shortage: The UK road haulage industry faced a shortage of approximately 60,000 HGV drivers in 2024, creating operational constraints, higher freight rates, and delivery delays that disproportionately affect time-sensitive sectors.

- Fuel Cost Volatility: Diesel price volatility has compressed margins for road freight operators, increasing cost uncertainty and accelerating the shift toward fleet electrification and alternative energy adoption to enhance efficiency and long-term operational sustainability.

- Brexit Trade Complexity: Post-Brexit customs checks, and regulatory divergence have added complexity and cost to UK-EU freight flows, increasing border dwell times and compliance costs for manufacturers dependent on just-in-time supply chains.

Market Opportunities

- Green Logistics Transition: The UK government's Road to Zero Strategy and Clean Air Zone frameworks are accelerating the transition to electric and hydrogen freight vehicles. Operators investing early in green fleet infrastructure are positioned to capture premium contracts from sustainability-committed shippers.

- Last-Mile Innovation: The rapid expansion of same-day and next-day urban delivery expectations is creating a significant last-mile innovation opportunity in the UK, encompassing drone delivery pilots, autonomous ground vehicles, and smart locker infrastructure in high-density urban areas.

Market Challenges

- Cybersecurity Risk: Cybersecurity vulnerabilities in logistics IT infrastructure - including warehouse management systems, transportation management platforms, and tracking technologies - present growing operational risk as digital integration deepens across the supply chain.

- Sustainability Investment Burden: Meeting net-zero targets while maintaining cost competitiveness requires significant capital expenditure on fleet electrification, renewable-powered warehousing, and sustainable packaging - creating a financial burden that is disproportionate for small and mid-size operators.

Emerging Market Trends

1. AI-Powered Route Optimisation and Predictive Logistics

Artificial intelligence and machine learning are reshaping UK logistics operations. Leading operators are deploying AI platforms that reduce empty running and improve on-time delivery rates. Predictive demand modelling enables dynamic inventory positioning across distributed fulfilment networks, lowering last-mile delivery costs and enhancing customer experience.

2. Rapid Electrification of Last-Mile Fleets

UK logistics operators are accelerating the adoption of electric vans and light commercial vehicles for urban delivery. Major players are committing to large-scale electric fleet deployments, while government grant schemes and Clean Air Zone incentives are accelerating transition timelines for small and mid-size operators.

3. Growth of 4PL and Integrated Supply Chain Orchestration

Demand for end-to-end supply chain visibility and integrated management is driving the transition from traditional 3PL outsourcing to 4PL models. Large retailers and manufacturers are partnering with platform-based 4PL providers that offer real-time supply chain visibility, multi-carrier management, and continuous optimisation through cloud-based control towers.

4. Expansion of Micro-Fulfillment Centers in Urban Areas

Consumer expectations for same-day and sub-2-hour delivery are driving investment in urban micro-fulfillment centers across London, Manchester, Birmingham, and other major cities. These facilities - often automated and designed for rapid order processing - are enabling grocery and general merchandise retailers to offer on-demand delivery while reducing carbon footprint compared to out-of-town distribution models.

5. Sustainability and Circular Economy Logistics

UK shippers and logistics providers are embedding circular economy principles into supply chain design. Reverse logistics networks for returns, reuse, and recycling are expanding, while sustainable packaging, carbon-neutral delivery, and offsetting programmes are becoming standard features in premium logistics contracts.

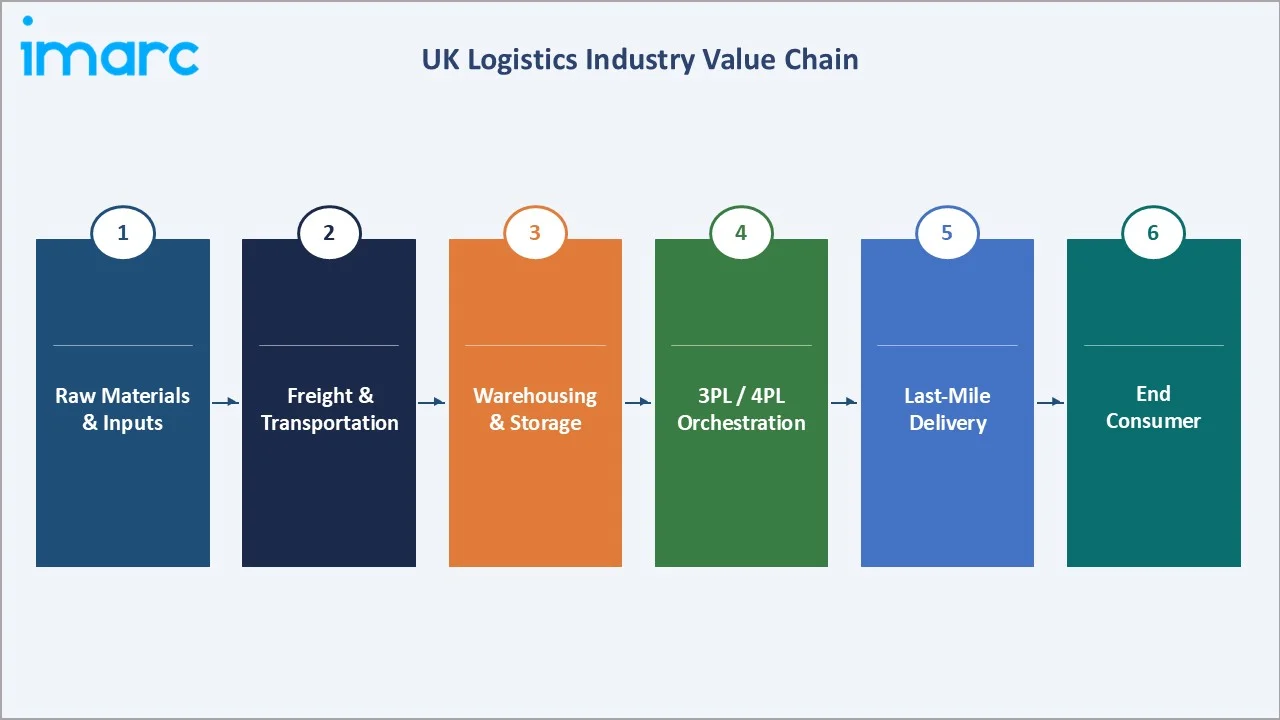

Industry Value Chain Analysis

The UK logistics industry value chain spans six integrated stages from raw material supply through final consumer delivery. Each stage presents distinct competitive dynamics, investment requirements, and technology adoption profiles relevant to the overall logistics market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Raw Materials & Inputs |

Fuel suppliers, packaging manufacturers, commercial vehicle OEMs, racking and MHE suppliers, warehouse technology vendors |

|

Freight & Transportation |

Road hauliers, sea freight operators (DFDS, P&O), rail freight operators (DB Cargo, Freightliner), air freight carriers (British Airways Cargo, DHL Aviation) |

|

Warehousing & Storage |

Third-party warehousing operators, bonded warehouses near ports (Tilbury, Felixstowe), temperature-controlled facilities for food and pharma |

|

3PL / 4PL Orchestration |

DHL Supply Chain, XPO Logistics, Kuehne + Nagel, DB Schenker, Wincanton - providing integrated logistics management and control tower services |

|

Last-Mile Delivery |

Royal Mail, Evri, DPD, Amazon Logistics, Yodel - offering parcel, next-day, same-day and click-and-collect fulfillment across UK postcodes |

|

End Consumer |

Retail consumers, B2B commercial buyers, industrial facilities, healthcare institutions, and public sector organisations |

Third-party and fourth-party logistics providers hold the highest strategic value by integrating transportation, warehousing, and technology into scalable solutions. Meanwhile, last-mile delivery operators are the fastest-evolving segment, with consumer expectations for speed and sustainability reshaping the competitive landscape.

Technology Landscape in the UK Logistics Industry

AI and Data Analytics

Artificial intelligence is transforming logistics operations through route optimisation, demand forecasting, and real-time exception management. UK logistics leaders are deploying machine learning algorithms to dynamically optimise delivery routes and reduce fuel consumption while improving overall operational efficiency.

IoT Fleet Telematics and Real-Time Tracking

Internet of Things (IoT) devices embedded in freight vehicles and shipping containers are enabling real-time GPS tracking, engine diagnostics, driver behaviour monitoring, and cargo condition visibility. UK road hauliers using advanced telematics are improving fleet utilisation and reducing accident-related costs through proactive intervention capabilities.

Warehouse Automation and Robotics

Automated storage and retrieval systems, autonomous mobile robots, and goods-to-person picking technologies are being deployed at scale across UK distribution centers. Major operators are expanding robotic fulfillment networks, with automated systems significantly reducing order picking times compared to manual operations.

Blockchain for Supply Chain Transparency

Distributed ledger technology is gaining adoption in UK import/export documentation management, pharmaceutical cold chain traceability, and food safety tracking. Blockchain platforms enable secure audit trails across multi-party supply chains, reducing documentation fraud, accelerating customs clearance, and ensuring end-to-end product provenance for regulatory compliance.

.webp)

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Model Type |

3PL |

52.6% |

2025 |

|

Transportation Mode |

Roadways |

54.8% |

2025 |

|

End Use |

Manufacturing |

🔒 |

2025 |

|

Region |

North West England |

22.7% |

2025 |

By Model Type

To access detailed market analysis, Request Sample

The 3PL model leads the UK logistics market with a 52.6% share in 2025. Demand is driven by the growing preference among UK retailers and manufacturers for outsourced logistics operations that offer scalability, specialised expertise, and technology-enabled supply chain management. The rise of e-commerce and omnichannel retail has particularly accelerated 3PL adoption.

By Transportation Mode

Roadways dominate the UK logistics market at 54.8% of revenue in 2025, underpinned by an extensive road network and rising home delivery demand. The flexibility and door-to-door accessibility of road freight make it the preferred mode across end-use sectors, with e-commerce further intensifying last-mile delivery volumes in urban and suburban areas.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North West England |

22.7% |

Manchester freight hub, Liverpool port, major 3PL operator presence, motorway network density |

|

South East England |

18.9% |

Proximity to London, cross-channel freight, Gatwick air cargo, Thames estuary port access |

|

Greater London |

16.5% |

Same-day and last-mile demand, e-commerce fulfillment density, urban delivery innovation |

|

West Midlands |

10.8% |

Automotive supply chain, NEC Birmingham freight facilities, HS2 corridor infrastructure |

|

Yorkshire & the Humber |

8.6% |

Humber ports (Hull, Immingham), manufacturing sector logistics, Northern Powerhouse investment |

|

East of England |

7.5% |

Stansted air freight, Felixstowe port (UK's largest container port), FMCG distribution |

|

South West England |

5.9% |

Bristol port expansion, regional retail distribution, tourism and seasonal freight |

|

East Midlands |

4.8% |

East Midlands Airport (UK's largest pure freight airport), DHL Express and UPS hubs |

|

North East England |

2.7% |

Teesside industry, Port of Tyne, growing logistics park investment under Levelling Up agenda |

|

Others |

1.6% |

Scotland, Wales, and Northern Ireland combined - serving regional markets via rail and coastal shipping |

North West England

North West England commands 22.7% of UK logistics market revenue in 2025 - the largest regional share nationally. The region benefits from a dense motorway network (M6, M62, M60 orbital), proximity to the Port of Liverpool (handling over 32 million tonnes annually), and Manchester's position as the UK's largest logistics hub outside London. Major 3PL operators including DHL, XPO, and Clipper Logistics operate flagship distribution centres in the Greater Manchester area, serving major retailers and FMCG manufacturers.

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

DHL Group |

DHL Supply Chain, StreetScooter |

Leader |

Global scale, green fleet leadership, end-to-end supply chain integration |

|

XPO, Inc. |

XPO |

Leader |

Technology-led logistics, Europe-wide network, contract logistics expertise |

|

DB Schenker |

DB Schenker |

Leader |

Rail-road integration, global freight forwarding, automotive sector expertise |

|

Kuehne+Nagel |

Kuehne + Nagel, KN FreightNet |

Challenger |

Sea and air freight, digital freight platforms, pharma cold chain |

|

Evri Limited |

Evri, Myhermes |

Challenger |

Parcel delivery dominance, ParcelShop network, B2C e-commerce fulfillment |

|

Royal Mail Group Limited |

Royal Mail, Parcelforce |

Established |

National postal network, SME parcel delivery, international express |

|

DFDS |

DFDS Logistics, Norfolkline |

Emerging |

North Sea and Channel ferry-freight integration, cold chain expertise |

The UK logistics market's competitive landscape is moderately fragmented, with global operators competing alongside specialist UK-focused providers. Leading players differentiate on technology integration, sector specialisation, sustainability credentials, and geographic network density.

Key Company Profiles

DHL Group

DHL Group is a leading global logistics provider headquartered in Bonn, Germany, with operations spanning over 220 countries and territories. The company offers a comprehensive portfolio of services through its key divisions, including DHL Express for international courier services, DHL Supply Chain for contract logistics and warehousing.

- Product & Platform Portfolio: DHL's UK logistics portfolio spans contract warehousing and distribution, cold chain logistics, returns management, and digital supply chain solutions via its mySupply Chain cloud platform. Its StreetScooter electric vehicle brand supports sustainable last-mile delivery.

- Recent Developments: In 2025, DHL Supply Chain secured a new multi-year transport contract with Siemens Mobility to deliver critical rail components across the UK. The partnership will support train repair, maintenance, and refurbishment operations, strengthening rail network reliability.

- Strategic Focus: DHL's strategy centres on green logistics leadership, automation investment, and digital supply chain integration - leveraging AI and IoT to drive operational efficiency gains while meeting customer sustainability commitments.

XPO Inc.

XPO Inc.is a leading provider of freight transportation and logistics services, operating one of the largest less-than-truckload (LTL) networks in North America and a significant European contract logistics business, including major UK operations.

- Product & Platform Portfolio: XPO Inc. operates large-format, highly automated distribution centres for retailers including Marks & Spencer and John Lewis. Its technology platform XPO Connect provides real-time freight tracking and digital freight brokerage capabilities.

- Recent Developments: In 2026, XPO Logistics and Arla Foods extended their strategic partnership to develop a new central distribution centre in the UK. The facility will centralise chilled product distribution, improving supply chain efficiency, resilience, and sustainability.

- Strategic Focus: XPO Inc.’s strategy emphasises advanced warehouse automation, robotics integration, and e-commerce fulfilment positioning the business as a technology-first contract logistics provider with differentiated capabilities in high-complexity retail distribution.

Kuehne + Nagel

Kuehne + Nagel is a global logistics provider headquartered in Schindellegi, Switzerland, with significant UK operations across sea freight forwarding, air freight, road logistics, and pharma supply chain management.

- Product & Platform Portfolio: Kuehne + Nagel's UK platform offers seafreight container shipping via major UK ports, air freight management through Heathrow and Manchester, temperature-controlled pharmaceutical logistics, and its digital freight platform KN FreightNet for real-time shipment booking and tracking.

- Recent Developments: In 2025, Kuehne+Nagel reported strong first-half performance driven by growth in sea and air logistics volumes, despite currency headwinds and volatile trade conditions. The company increased market share through targeted strategies, with volumes outperforming overall market growth.

- Strategic Focus: Kuehne + Nagel focuses on digital freight platform development, pharma cold chain leadership, and sustainable sea freight solutions - including investment in biofuel-powered shipping and carbon offset programmes for UK import/export customers.

Market Concentration Analysis

The UK logistics market exhibits moderate fragmentation, with the top five operators including DHL Group, XPO, Inc., DB Schenker, Kuehne+Nagel, Evri Limited, collectively accounting for an estimated 28-32% of total market revenue in 2025. This fragmentation reflects the diversity of logistics services spanning road haulage, contract warehousing, freight forwarding, parcel delivery, and specialist sector solutions.

Consolidation activity is accelerating, driven by economies of scale in technology investment, network density requirements for last-mile delivery, and the capital intensity of electric fleet transition.

Investment & Growth Opportunities

Fastest Growing Segments

- 4PL Platforms: 4PL and supply chain orchestration platforms are growing at an estimated 6.2% CAGR through 2034, driven by enterprise demand for integrated visibility and AI-powered supply chain management across complex global sourcing networks.

- Urban Last-Mile: Urban last-mile delivery and micro-fulfillment infrastructure represent the highest-growth investment opportunity in UK logistics, with the segment expected to grow at over 8% CAGR through 2030 as same-day delivery becomes standard for major retailers.

- Cold Chain & Pharma: Cold chain and pharmaceutical logistics are growing at approximately 6.5% CAGR through 2034, driven by NHS supply chain demands, biologic drug growth, and temperature-sensitive e-grocery fulfillment expansion.

Emerging Markets

- Northern Logistics Corridors: Scotland and Northern England are attracting significant logistics investment under the Levelling Up agenda, with new distribution parks in Teesside, South Yorkshire, and the Glasgow-Edinburgh corridor offering cost-competitive alternatives to South East England land prices.

- International Trade Gateway: Export logistics to GCC and Southeast Asian markets is growing rapidly following post-Brexit trade agreements, creating investment opportunities in UK-based export freight forwarding and specialist customs brokerage capabilities.

Venture Investment Trends

In 2024, the UK government committed £600m to accelerate the development of logistics and industrial sites and will establish a national Supply Chain Centre, spanning autonomous delivery vehicles and sustainability tracking platforms. UK-based startups including Arrival, Wayve, and Stuart (on-demand delivery) have attracted significant venture capital, reflecting investor confidence in logistics technology as a structural growth theme.

Future Market Outlook (2026-2034)

The UK logistics market is projected to reach USD 927.9 Billion by 2034, advancing at a CAGR of 5.3% through the forecast period. This growth trajectory is underpinned by structural tailwinds including sustained e-commerce penetration, continued trade network expansion following post-Brexit agreement implementation, and the digital transformation of supply chain operations.

Technological disruption will fundamentally reshape the logistics value chain through 2034. Autonomous delivery vehicles - including self-driving HGVs trialled on UK motorways and drone delivery networks operational in rural and suburban areas. AI-powered demand forecasting and inventory optimisation will reduce holding costs and stockout rates, improving capital efficiency for retailers and manufacturers.

Sustainability will be a defining competitive axis. The UK government's Transport Decarbonisation Plan targets net-zero domestic logistics by 2040. Operators who transition to electric and hydrogen fleets, invest in renewable-powered warehousing, and develop robust carbon accounting frameworks will be positioned to win premium contracts from the growing cohort of net-zero-committed UK retailers and manufacturers.

Research Methodology

Primary Research

IMARC Group conducts in-depth interviews with senior logistics executives, supply chain directors, freight operators, and industry association representatives across the UK. Primary research also includes structured surveys with logistics buyers, shipper organisations, and technology vendors to validate market sizing assumptions and identify emerging trends.

Secondary Research

Secondary research draws from authoritative sources including the UK Freight Transport Association (now Logistics UK), the Department for Transport, ONS trade statistics, Companies House filings, operator annual reports, port authority traffic data, and specialist trade publications including Logistics Manager and The Loadstar.

Forecasting Models

Market forecasts are developed using a combination of bottom-up segment modelling and top-down macroeconomic projection. Variables including GDP growth, e-commerce penetration rates, infrastructure investment plans, trade volume indices, and regulatory timelines are incorporated into scenario-based forecasting models that generate base, optimistic, and conservative projections through 2034.

UK Logistics Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Model Types Covered | 2 PL, 3 PL, 4 PL |

| Transportation Modes Covered | Roadways, Seaways, Railways, Airways |

| End Uses Covered | Manufacturing, Consumer Goods, Retail, Food and Beverages, IT Hardware, Healthcare, Chemicals, Construction, Automotive, Telecom, Oil and Gas, Others |

| Companies Covered | DHL Group, XPO, Inc., DB Schenker, Kuehne+Nagel, Evri Limited, Royal Mail Group Limited, DFDS, etc. |

| Regions Covered | North West England, Yorkshire and the Humber, West Midlands, East of England, South West England, South East England, East Midlands, North East England, Greater London, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the UK logistics market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the UK logistics market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the UK logistics industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the UK Logistics Market Report

The UK logistics market reached USD 572.6 Billion in 2025, reflecting consistent growth driven by e-commerce expansion, infrastructure investment, and increasing outsourcing of logistics operations by UK manufacturers and retailers.

The UK logistics market is projected to grow at a CAGR of 5.3% during 2026-2034, supported by digital transformation, trade network expansion, and last-mile delivery innovation.

Third-party logistics (3PL) is the dominant model type with a 52.6% share in 2025, driven by retailer and manufacturer outsourcing preferences for scalable, technology-enabled supply chain management solutions.

Roadways dominate with a 54.8% share in 2025, underpinned by the UK's extensive national road network and the growth of home delivery demand generated by rising e-commerce penetration exceeding 27% of total retail.

North West England holds the largest regional share at 22.7% in 2025, driven by the Manchester freight hub, Port of Liverpool volumes, and major 3PL operator presence across the region's motorway-connected distribution corridors.

Leading companies include DHL Group, XPO, Inc., DB Schenker, Kuehne+Nagel, Evri Limited, Royal Mail Group Limited, and DFDS, each offering differentiated capabilities across freight, contract logistics, and parcel delivery.

Key drivers include e-commerce penetration growth, government infrastructure investment, increasing adoption of technologies such as AI, IoT, and automation, and the expansion of international trade agreements driving freight volume growth.

Major challenges include the HGV driver shortage fuel cost volatility, post-Brexit customs complexity for UK-EU freight, and the capital investment burden of net-zero fleet transition.

The 4PL model type is the fastest-growing segment, estimated at 6.2% CAGR through 2034, as enterprises seek integrated supply chain orchestration with end-to-end visibility, AI analytics, and multi-party coordination capabilities.

Sustainability is reshaping fleet investment, warehouse energy sourcing, and service offerings. Over 40% of major UK logistics operators have set net-zero targets, with electric vehicle fleets and renewable-powered facilities becoming competitive differentiators.

Key technology trends include AI-powered route optimisation, IoT fleet telematics, warehouse robotics and automation, blockchain-based trade documentation, and autonomous delivery vehicle pilots on UK motorways and urban delivery routes.

The UK logistics market is forecast to reach USD 742.9 Billion by 2030, representing an intermediate milestone in the growth trajectory from USD 572.6 Billion in 2025 to USD 927.9 Billion by 2034 at a 5.3% CAGR.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)