UK Online Grocery Market Size, Share, Trends and Forecast by Product Type, Business Model, Platform, Purchase Type, and Region, 2026-2034

UK Online Grocery Market Size & Forecast 2026-2034

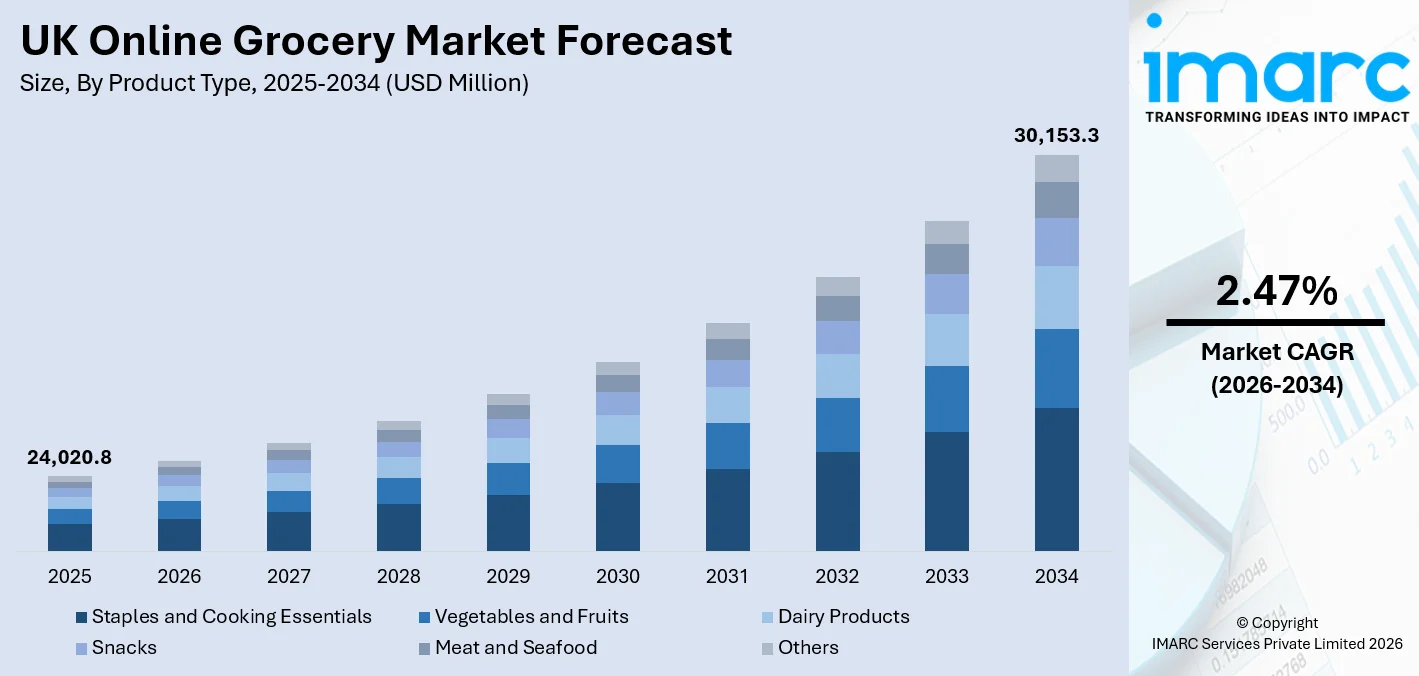

The UK online grocery market was valued at USD 24,020.8 Million in 2025 and is projected to reach USD 30,153.3 Million by 2034, exhibiting a CAGR of 2.47% during 2026-2034. The market is being driven by rising consumer preference for convenience-led digital shopping, accelerated deployment of rapid last-mile delivery infrastructure across UK urban centres, and deepening investment in artificial intelligence (AI) and machine learning (ML) tools to personalise online grocery experiences and optimise supply chain operations.

To get more information on this market Request Sample

UK Online Grocery Industry Analysis: Key Insights

- Staples and cooking essentials commands 27.3% of product type share in 2025 - its role as a daily household necessity anchors consistent demand, making it the backbone of repeat online grocery purchases across UK households.

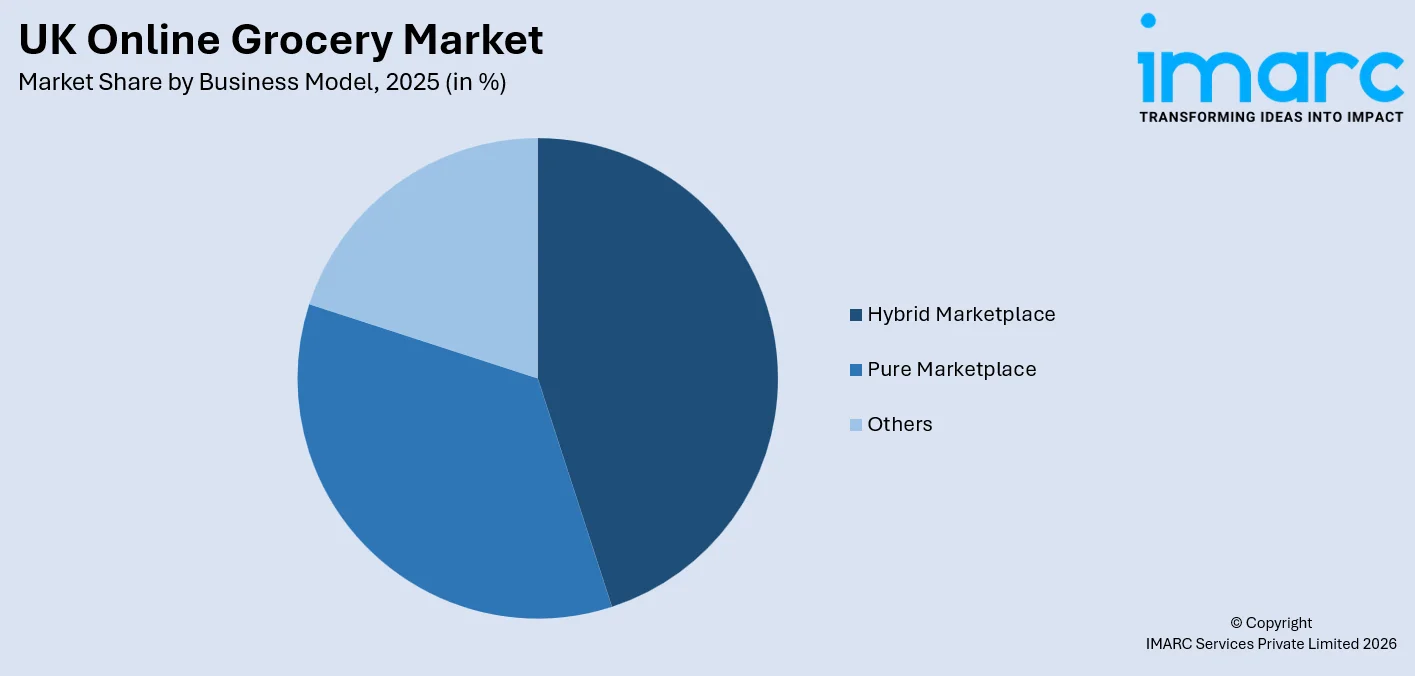

- Hybrid marketplace leads business model at 44.6% in 2025 - integrating both own-inventory and third-party fulfilment, hybrid models offer flexibility and breadth that pure-play alternatives struggle to match.

- App-based dominates revenue platform at 58.2% in 2025 - mobile-first grocery shopping reflects the UK's high smartphone penetration, with consumers favouring the speed and personalization of dedicated retail apps.

- One-time commands 68.4% of purchase type share in 2025 - flexible, on-demand ordering remains the preferred mode, reflecting consumer behaviour patterns that prioritize convenience over locked-in subscription models.

- London leads regionally at 17.8% in 2025 - high population density, fast-paced lifestyles, and advanced last-mile infrastructure make London the most active region for online grocery adoption in the UK.

UK Online Grocery Market Trends and Dynamics 2026

Market Trends

Rapid delivery and quick-commerce expansion are reshaping fulfilment expectations

Consumer expectations for grocery delivery speed have shifted decisively, with same-day and sub-hour services transitioning from premium niche offerings to mainstream requirements in UK urban markets. Retailers are responding by investing heavily in dark stores, micro-fulfilment centres, and strategic carrier partnerships. Ocado Retail registered 16.3% revenue growth in 2025, driven partly by increasing consumer uptake of its expedited delivery proposition. The ultra-rapid grocery delivery segment is expanding beyond London, with platforms extending coverage into regional cities, fuelling competitive pressure on traditional click-and-collect formats and reinforcing app-based UK online grocery market trends.

AI-powered personalisation and agentic shopping are redefining the digital experience

Retailers are deploying advanced artificial intelligence tools to move beyond generic product recommendations toward truly individualised shopping journeys. Predictive restocking, recipe-based basket building, and context-aware promotions are becoming standard expectations among digitally engaged UK consumers. In May 2024, Sainsbury's entered a five-year strategic technology partnership with Microsoft, aimed at embedding AI capabilities directly into its store operations and online platforms to elevate customer satisfaction. Additionally, research from Algolia in September 2025 found that a significant proportion of British shoppers indicated willingness to adopt AI-powered third-party grocery applications, warning that retailers risk losing 500 million pounds per week in potential weekly losses if they fail to match the AI shopping experience.

Sustainability and eco-conscious consumption are gaining traction online

Environmental consciousness is increasingly influencing digital grocery purchasing decisions, particularly among higher-income and younger UK consumers. Online platforms are responding with advanced sustainability filtering capabilities, carbon-neutral delivery options, and broader organic and locally sourced product assortments. According to Mintel's 2025 UK Online Grocery Retailing report, sustainability-related attitudes among online shoppers are returning to the fore, especially within wealthier demographic segments. Retailers are integrating low-emission packaging, optimised last-mile delivery routing, and partnerships with regional suppliers to meet the growing demand for eco-responsible choices, shaping the broader UK online grocery market outlook for the forecast period.

Growth Drivers

Rising consumer demand for convenience and time-saving digital solutions

The fundamental driver of UK online grocery growth remains the sustained consumer desire for time efficiency and household management convenience. E-commerce, working professionals, dual-income households, and time-constrained families are anchoring their grocery shopping online as a structural lifestyle choice rather than a situational response. For instance, as per the data reported by IMARC, the UK e-commerce market reached a value of USD 297.0 billion in 2024. Moreover, smartphone dependency and the proliferation of intuitive retail apps have removed friction from the purchasing journey, enabling consumers to fulfil grocery needs within minutes from any location. The UK online grocery market growth trajectory is closely tied to this sustained behavioural normalisation across age groups and income brackets, particularly among 25–44-year-old professionals and young families in metropolitan and suburban areas.

Expansion of rapid and ultra-rapid delivery infrastructure across UK regions

Significant capital investment by both established supermarket chains and dedicated quick-commerce operators into dark stores, automated micro-fulfilment hubs, and last-mile logistics networks is structurally expanding the addressable market for online grocery in the UK. In March 2024, Gopuff announced the extension of its 24/7 delivery services to new cities, including Liverpool and Newcastle, reflecting the platform's confidence in growing consumer appetite for around-the-clock grocery access beyond London. The deployment of automated customer fulfilment centres by pure-play operators and the conversion of urban backroom spaces into rapid picking hubs are compressing delivery windows across a broader geography. This infrastructure expansion is progressively removing the convenience gap between online and physical grocery shopping, materially increasing the share of UK households for whom online ordering represents a fully competitive alternative.

Technological advancement and personalisation are driving platform engagement and loyalty

Investment in AI, machine learning, and data analytics is transforming UK online grocery platforms from transactional utilities into personalised retail experiences that generate habitual engagement and increase basket size. The combination of tailored product recommendations and dynamic promotions based on purchase history and AI-powered search tools results in better conversion rates and increased customer lifetime value. In June 2024, Amazon Fresh extended its fresh grocery delivery service to all eligible customers across more than 100 towns and cities in the UK, which uses personalized recommendations and a wide product range to enhance its digital grocery service. Technology is now allowing businesses to achieve better inventory control and demand forecasting results, which leads to fewer instances of stock shortages that previously stopped customers from shopping online. The total set of these innovations provides online grocery platforms with increased value, which helps the UK market to maintain its growth projection from now until 2034.

Market Restraints

High last-mile delivery costs and margin compression: The process of delivering groceries to residential locations requires extensive logistical expenditures, which include fuel expenses, driver salaries, and vehicle maintenance costs that delivery charges cannot fully recover. Online grocery services face declining profitability because of increased labor expenses following the implementation of the UK National Living Wage, which particularly impacts small businesses and their ability to invest.

Consumer resistance and in-store shopping preference among key demographics: The most significant obstacle that prevents customers from using online grocery services occurs because shoppers prefer to buy products from physical stores, which especially affects older people and shoppers who need to touch items before choosing fresh produce, meat, and bakery items. Most people use traditional grocery shopping methods because they find it easier to access physical stores instead of online grocery shopping, which has problems with tracking product availability and delivery times.

Intensifying competitive pressure and platform fragmentation: The UK online grocery market features intense rivalry between established supermarket chains and pure-play operators, and rapid delivery startups and marketplace aggregators. The financial performance of multiple well-capitalized companies suffers from price wars, promotional discounts, and high marketing costs, which result in increased expenses for acquiring new customers. The combination of proprietary applications, third-party marketplaces, and aggregator services results in platform fragmentation, which makes it more difficult for consumers and retailers who need to handle multiple delivery channels.

UK Online Grocery Market Segmentation Analysis

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product Type | Staples and Cooking Essentials | 27.3% | 2025 |

| Business Model | Hybrid Marketplace | 44.6% | 2025 |

| Platform | App-Based | 58.2% | 2025 |

| Purchase Type | One-Time | 68.4% | 2025 |

| Region | London | 17.8% | 2025 |

Product Type Insights

Staples and Cooking Essentials -27.3% Market Share (2025) | Leading Product Type

Staples and cooking essentials represent the largest product segment in the UK online grocery market, a position anchored in the category's non-discretionary consumption characteristics and high purchase frequency. Digital ordering works best for this category because its demand pattern allows customers to use automatic replenishment systems, which provide personalized alerts based on their past buying patterns and their subscription delivery services. In 2025, a growing proportion of UK households are using grocery apps specifically to manage bulk staples purchasing more cost-effectively, with AI-powered recommendation tools helping consumers identify promotional windows and own-label alternatives. Retailers, including Tesco, Sainsbury's, and Asda, have invested in deepening their own-brand staples ranges available exclusively or at improved pricing online, reinforcing category dominance in the digital channel.

|

Segment Breakdown Staples and Cooking Essentials (27.3%) · Vegetables and Fruits · Dairy Products · Snacks · Meat and Seafood · Others |

Business Model Insights

Access the comprehensive market breakdown Request Sample

Hybrid Marketplace -44.6% Market Share (2025) | Leading Business Model

The hybrid marketplace model holds the largest share of the UK online grocery market due to its integrated system, which uses both its own inventory and third-party fulfillment services creates an advantage that meets consumer demands. Hybrid operators combine the product breadth of marketplace aggregation with the speed, reliability, and quality control of direct inventory management, enabling them to serve both planned bulk grocery orders and spontaneous top-up shopping missions. Hybrid platforms are also better positioned to operate loyalty-integrated ecosystems that leverage purchase data across both own-range and marketplace categories, deepening personalisation and driving share of wallet. In May 2024, Sainsbury's partnership with Microsoft to deploy AI within its hybrid online operations exemplifies how the model is evolving from a transactional infrastructure into an intelligent, data-rich consumer engagement engine. The scalability and flexibility of hybrid architectures position them as the preferred operational model for the forecast period, as UK online grocery retailers seek to broaden product assortment without bearing the full inventory risk of pure-play models.

|

Segment Breakdown Hybrid Marketplace (44.6%) · Pure Marketplace · Others |

Platform Insights

App-Based -58.2% Market Share (2025) | Leading Platform

App-based platforms command a majority of UK online grocery transactions, a reflection of the country's high smartphone penetration and consumer preference for intuitive, mobile-first shopping experiences. Dedicated grocery apps from major retailers offer a combination of personalised push notifications, saved shopping lists, loyalty card integration, and streamlined checkout that browser-based experiences cannot replicate with the same immediacy. The rise of app-exclusive promotions, scan-and-go functionality, and real-time order tracking has incentivised consumers to migrate toward dedicated applications as their primary online grocery interface. In 2025, UK grocery spend via mobile channels accounts for most digital transactions, with grocery apps registering above-average session frequency compared to other retail categories. As smartphone capabilities continue to advance and 5G coverage expands across UK regions, the app-based share of online grocery transactions is expected to strengthen further, maintaining its dominant position through the forecast period.

|

Segment Breakdown App-Based (58.2%) · Web-Based |

Purchase Type Insights

One-Time Purchase -68.4% Market Share (2025) | Leading Purchase Type

One-time purchases dominate the UK online grocery market, reflecting consumer preference for flexibility and on-demand ordering over locked subscription commitments. Most online grocery shoppers in the UK value the ability to order at any time because they need to adjust their shopping cart and product selection according to their current household needs, available seasonal items, and active promotional deals. Customers prefer to buy fresh produce, meat, seafood, and chilled ready meals through one-time purchases because their household requirements change every week. The platform provides users with features that allow them to quickly reorder their previous purchases through their purchase history and use prebuilt shopping baskets and smart reminders to create a subscription-like experience, which maintains the convenience of single purchase transactions.

|

Segment Breakdown One-Time (68.4%) · Subscription |

Regional Insights

London -17.8% Market Share (2025) | Leading Region

London controls the biggest portion of the online grocery business, which operates throughout the United Kingdom, because the city has its particular combination of high population density, high household income, advanced last-mile delivery systems, and a digital shopping customer base that uses online platforms for all retail products. The capital's fast-paced professional lifestyle creates strong structural demand for time-saving grocery solutions, making online ordering a practical necessity rather than a lifestyle preference for a significant proportion of London households. The high concentration of tech-forward early adopters and dual-income professional families in London ensures sustained demand for premium rapid delivery services and AI-enhanced shopping experiences that are driving market innovation nationally.

Major UK Regions Covered:

- London

- South East

- North West

- East of England

- South West

- Scotland

- West Midlands

- Yorkshire and the Humber

- East Midlands

- Others

Market Outlook 2026-2034

What is the future outlook of the UK online grocery market?

The UK online grocery market is positioned for steady, sustainable growth through 2034.

The UK online grocery market is expected to reach USD 30153.3 Million by 2034, underpinned by sustained infrastructure investment by leading operators, expanding rapid delivery coverage into secondary urban centres, and the deepening integration of AI-driven personalisation across consumer-facing platforms. Continued evolution of hybrid marketplace models, growing adoption of app-based shopping by older demographics, and the gradual expansion of subscription purchasing in high-frequency staple categories will collectively support a compound annual growth rate of 2.47% over the forecast period. Technological innovation, shifting consumer expectations, and competitive intensity will drive retailers toward greater operational efficiency, smarter last-mile logistics, and more compelling digital loyalty propositions throughout the forecast horizon.

UK Online Grocery Market -Leading Key Players

The UK online grocery market is characterised by a competitive landscape featuring dominant omnichannel supermarket groups, specialist pure-play operators, and rapidly growing platform-based entrants. Leading players are driving innovation through AI-powered shopping experiences, automated fulfilment infrastructure, rapid delivery service expansion, and enhanced digital loyalty ecosystems.

| Company | Leading Brands | Highlights |

|---|---|---|

| Tesco PLC | Tesco.com / Tesco Whoosh | Omnichannel grocer with store-based picking; largest UK market share at ~28.4% |

| Sainsbury's | Sainsbury's Online / Chop Chop | Online grocer; AI-enhanced shopping via Microsoft partnership |

| Ocado Retail Ltd. | Ocado.com | Pure online grocery platform; fastest-growing major grocer with H1 2025 revenues up 16.3% |

Some of the existing key players in the Uk Online Grocery Market are Asda Group Ltd., Morrisons, etc.

Latest Development & News

- In July 2025, Ocado Retail reported strong first-half 2025 results, with revenues rising 16.3% year-on-year. CEO Tim Steiner confirmed the company's strategic goal to continue scaling its automated fulfilment capabilities and grow at an accelerated pace, reinforcing Ocado's position as the fastest-growing major UK online grocer with increasing consumer uptake of its delivery proposition.

- In September 2025, research by Algolia warned that grocery retailers could lose up to 500 million pounds per week if they failed to match the emergence of AI-powered third-party shopping applications. The study, which surveyed 2,000 UK consumers, highlighted the urgency of AI investment for major online grocery operators.

- In June 2024, Amazon Fresh commenced fresh grocery deliveries to customers across more than 100 towns and cities throughout the UK, significantly expanding its geographic footprint. The service integration offered access to products from leading brands, local producers, and artisans, positioning Amazon Fresh as a substantial competitive force in the UK online grocery delivery market.

UK Online Grocery Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Vegetables and Fruits, Dairy Products, Staples and Cooking Essentials, Snacks, Meat and Seafood, Others |

| Business Models Covered | Pure Marketplace, Hybrid Marketplace, Others |

| Platforms Covered | Web-Based, App-Based |

| Purchase Types Covered | One-Time, Subscription |

| Regions Covered | London, South East, North West, East of England, South West, Scotland, West Midlands, Yorkshire and The Humber, East Midlands, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the UK Online Grocery Market Report

The UK online grocery market was valued at USD 24,020.8 Million in 2025.

The UK online grocery market is anticipated to reach a value of USD 30,153.3 Million by 2034.

Staples and Cooking Essentials lead the market with a share of 27.3%, driven by their non-discretionary consumption nature, high purchase frequency, and strong suitability for digital ordering with auto-replenishment and subscription functionality.

The Hybrid Marketplace model commands a 44.6% share, combining own-inventory management with third-party seller integration to offer breadth, reliability, and speed. This model is favoured by major UK grocers such as Tesco and Sainsbury's, enabling them to serve diverse consumer shopping missions through a single platform.

London currently dominates the UK online grocery market, accounting for a share of 17.8%. Its leadership reflects high consumer digital adoption, superior last-mile delivery infrastructure, professional demographic demand, and dense dark store networks that enable rapid fulfilment.

Some of the major players in the UK online grocery market include Tesco PLC, Sainsbury's, Ocado Retail Ltd., Asda Group Ltd., Morrisons, Amazon Fresh, Waitrose & Partners, Marks & Spencer, Deliveroo, Uber Eats, Aldi, and Lidl, etc.

Key trends include the rapid expansion of quick-commerce and ultra-rapid delivery services in urban regions, growing integration of AI and machine learning for personalised shopping experiences, rising consumer preference for app-based grocery ordering, and increasing focus on sustainability and eco-friendly packaging across online platforms.

Growth is driven by sustained consumer demand for convenience-led digital shopping, rapid expansion of last-mile delivery infrastructure, AI and data-driven personalisation enhancing platform engagement, rising smartphone adoption enabling mobile-first grocery experiences, and increasing investment in automated fulfilment by leading UK grocery operators.

Challenges include high last-mile delivery costs, compressing operator margins, persistent consumer preference for in-store shopping among key demographic segments, intensifying competition driving promotional discounting and elevated customer acquisition costs, and platform fragmentation creating operational complexity for multichannel grocery fulfilment strategies.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)