UK Wine Market Size, Share, Trends and Forecast by Product Type, Color, Distribution Channel, and Region, 2026-2034

UK Wine Market Size, Share, Trends & Forecast (2026-2034)

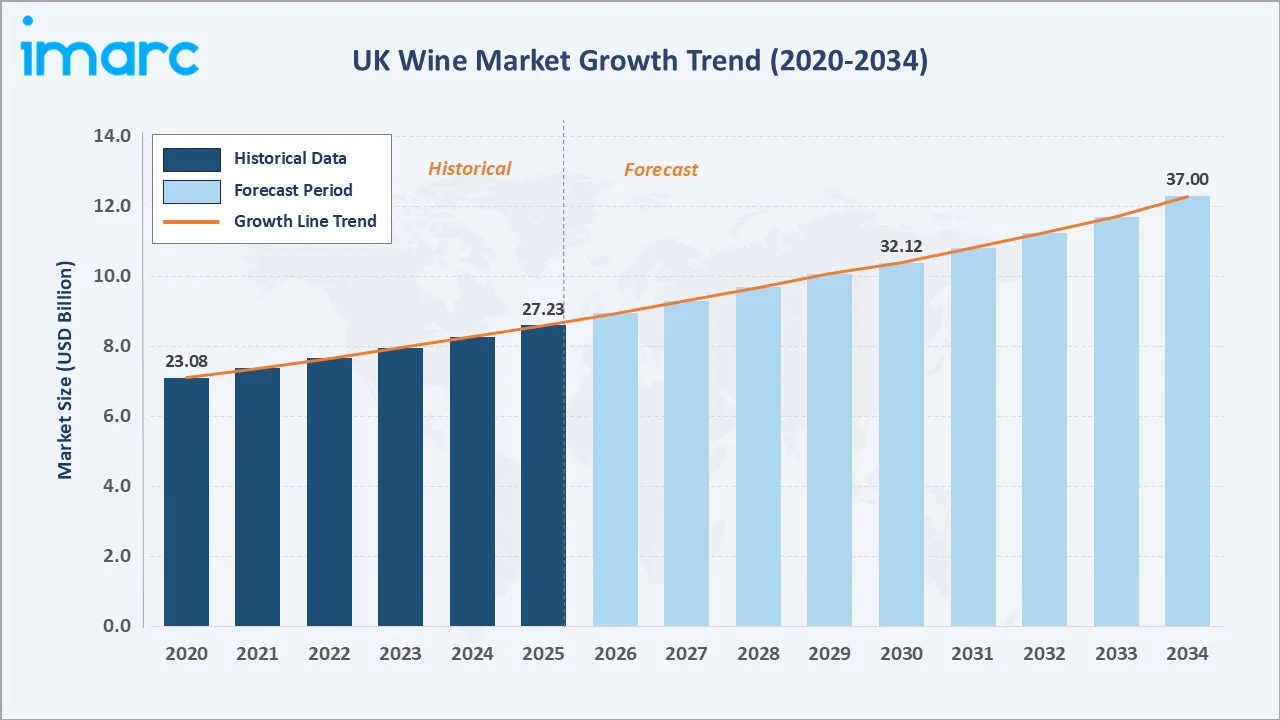

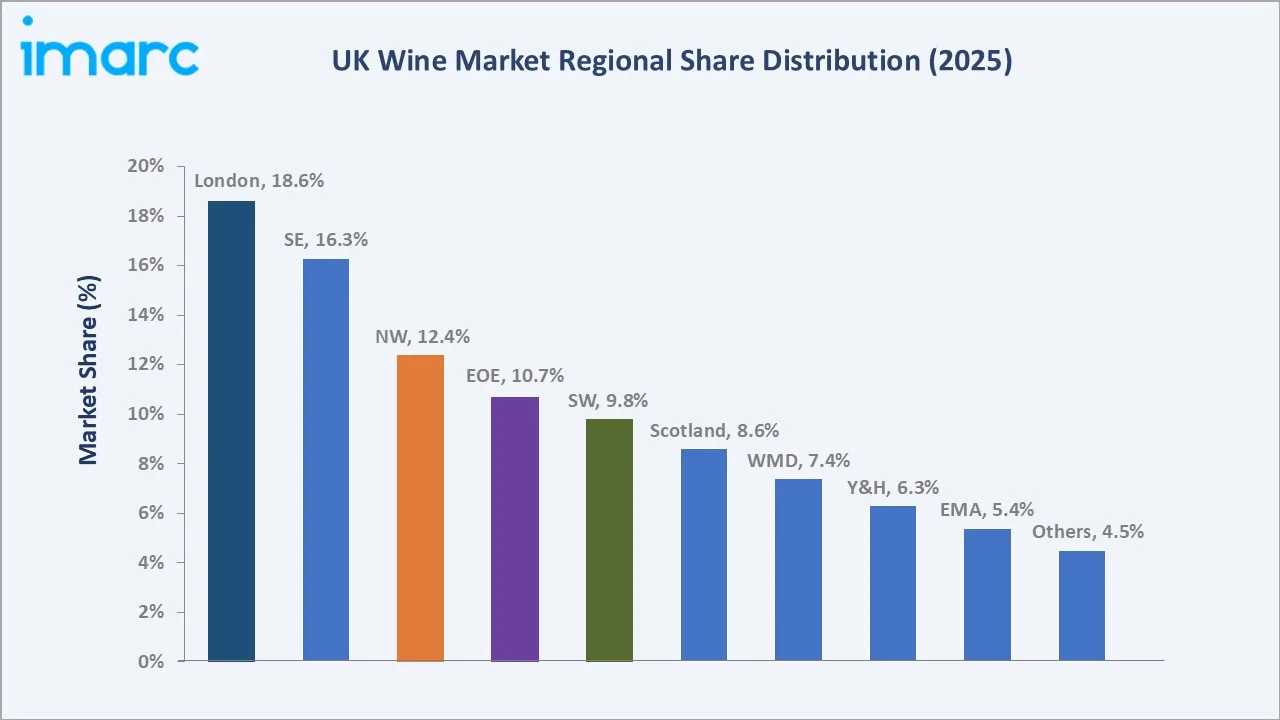

The UK wine market size reached USD 27.23 Billion in 2025 and is projected to reach USD 37.00 Billion by 2034, exhibiting a CAGR of 3.36% during the forecast period 2026-2034. Sustained consumer demand, with 67% of UK adults regularly consuming wine, combined with growing domestic vineyard output, rising disposable incomes, and premiumization of wine purchasing behavior, are the primary drivers of UK wine market growth. Still wine leads product type demand at 54.3% in 2025, while white wine commands the largest color segment at 39.3%. London dominates regional consumption with an 18.6% share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 27.23 Billion |

|

Forecast Market Size (2034) |

USD 37.00 Billion |

|

CAGR (2026-2034) |

3.36% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

London (18.6% share, 2025) |

|

Second Largest Region |

South East (16.3% share, 2025) |

|

Leading Product Type |

Still Wine (54.3%, 2025) |

|

Leading Color |

White Wine (39.3%, 2025) |

The UK wine market growth trajectory from 2020 through 2034, capturing steady historical expansion and a modestly accelerating forecast curve underpinned by premiumization, domestic vineyard expansion, and growing e-commerce wine retail.

To get more information on this market, Request Sample

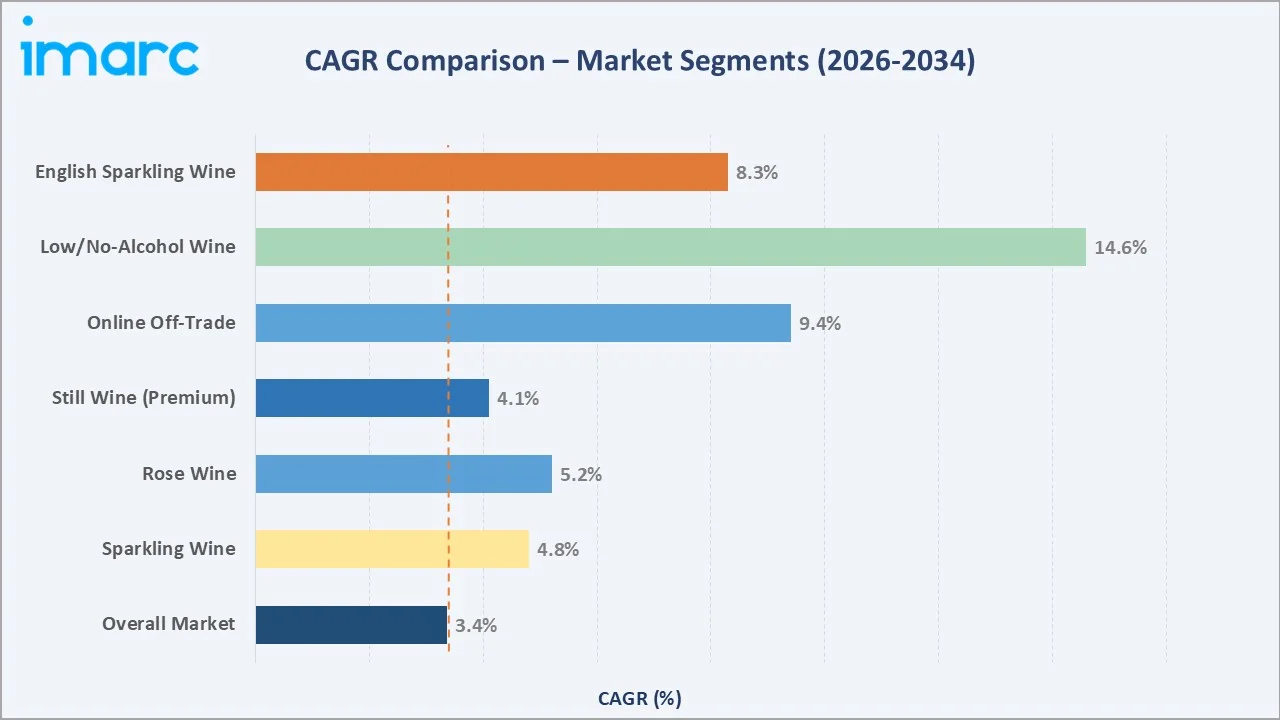

CAGR trajectories across key product, color, and channel segments, revealing low-alcohol and no-alcohol wine as the standout high-growth category within the UK wine industry analysis through 2034.

Executive Summary

The UK wine market is one of Europe's most mature and culturally embedded alcoholic beverage categories. Valued at USD 27.23 Billion in 2025, the market is on a steady growth path toward USD 37.00 Billion by 2034 at a CAGR of 3.36%. The UK ranks as the world's second-largest wine importer, which imports approximately 1.7 billion bottles annually, a testimony to the nation's deep-rooted wine consumption culture.

Still wine dominates product type demand with a 54.3% share in 2025, anchored by white wine's 39.3% color share and red wine's close 38.4% share, together accounting for 77.7% of all wine color consumption. Sparkling wine holds 28.7% of the product type mix in 2025 and is growing at ~4.8% CAGR through 2034, fueled by English sparkling wine's international reputation and continued Prosecco and Champagne popularity. Fortified wine and vermouth account for 17.0% in 2025.

London leads regional wine consumption at 18.6% in 2025, followed by the South East (16.3%) and North West (12.4%). These three regions collectively account for 47.3% of total UK wine revenue in 2025. Key market participants include Constellation Brands, Treasury Wine Estates, LVMH (Moët Hennessy), Gallo Family Vineyards, Majestic Wine, Accolade Wines, and leading English producers Chapel Down, Nyetimber, and Ridgeview.

Key Market Insights

|

Insight |

Data |

|

Largest Product Type |

Still Wine - 54.3% share (2025) |

|

Largest Color |

White Wine - 39.3% share (2025) |

|

Largest Region |

London – 18.6% revenue share (2025) |

|

Second Region |

South East – 16.3% revenue share (2025) |

|

Top Companies |

Constellation Brands, Treasury Wine Estates, LVMH, Chapel Down, Nyetimber |

Key Analytical Observations Supporting the Above Data:

- Still wine holds a 54.3% majority share in 2025, the dominant product type format by a wide margin. Its sustained dominance is anchored by everyday consumption occasions, strong supermarket shelf presence in both the off-trade and independent retail channels, and the depth of both imported and domestically produced still wine portfolios available to UK consumers.

- White wine's 39.3% color share marginally exceeds red wine's 38.4% in 2025, reflecting a UK consumer preference profile that is slightly more inclined toward crisp, food-friendly whites (Sauvignon Blanc, Chardonnay, Pinot Grigio) than red wines.

- London's 18.6% regional dominance in 2025 reflects the city's concentration of premium wine consumers, fine-dining restaurant clusters, luxury hotel bars, and wine import and distribution businesses, making it the UK's highest-value wine consumption market per capita and per-outlet.

UK Wine Market Overview

The UK wine market encompasses the importation, domestic production, distribution, and retail sale of all commercially produced wine categories, including still wine, sparkling wine, fortified wine and vermouth, across off-trade (supermarkets, specialist retailers, online) and on-trade (restaurants, pubs, hotels) channels. The UK is the world's second-largest wine importer and a significant and growing wine producer through its expanding English and Welsh vineyard sector.

Wine's role in British culture is deep and enduring. In the UK, wine is most commonly chosen for meals (64%), followed by special occasions (48%) and social gatherings with friends (48%). Fewer people opt for wine after work (17%) or during dates (16%). Wine is integral to dining occasions, celebratory events, social gatherings, and increasingly to casual everyday consumption.

Macroeconomic influences on the UK wine market include household disposable income levels, cost-of-living pressures, the impact of HMRC alcohol duty reform, post-Brexit import duty structures for EU wine, and the UK's evolving climate, which is enabling higher-quality domestic grape cultivation in southern England. Together, these factors shape both the volume and value trajectory of UK wine market growth through 2034.

Market Dynamics

To evaluate market opportunities, Request Sample

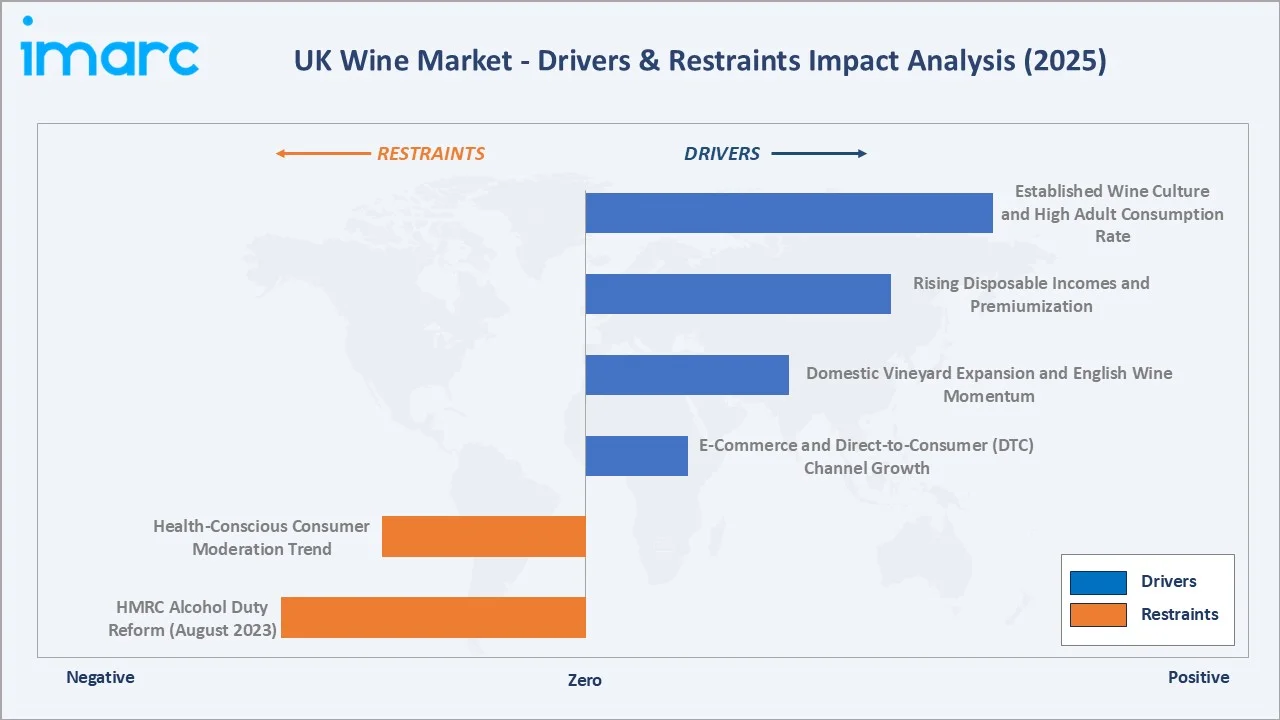

Market Drivers

- Established Wine Culture and High Adult Consumption Rate: With 67% of UK adults drinking wine in the UK, the market benefits from one of the world's highest per-capita wine consumption rates among major economies.

- Rising Disposable Incomes and Premiumization: UK household disposable incomes grew at an average of 2.1% annually, supporting a consistent upward trend in wine purchasing quality.

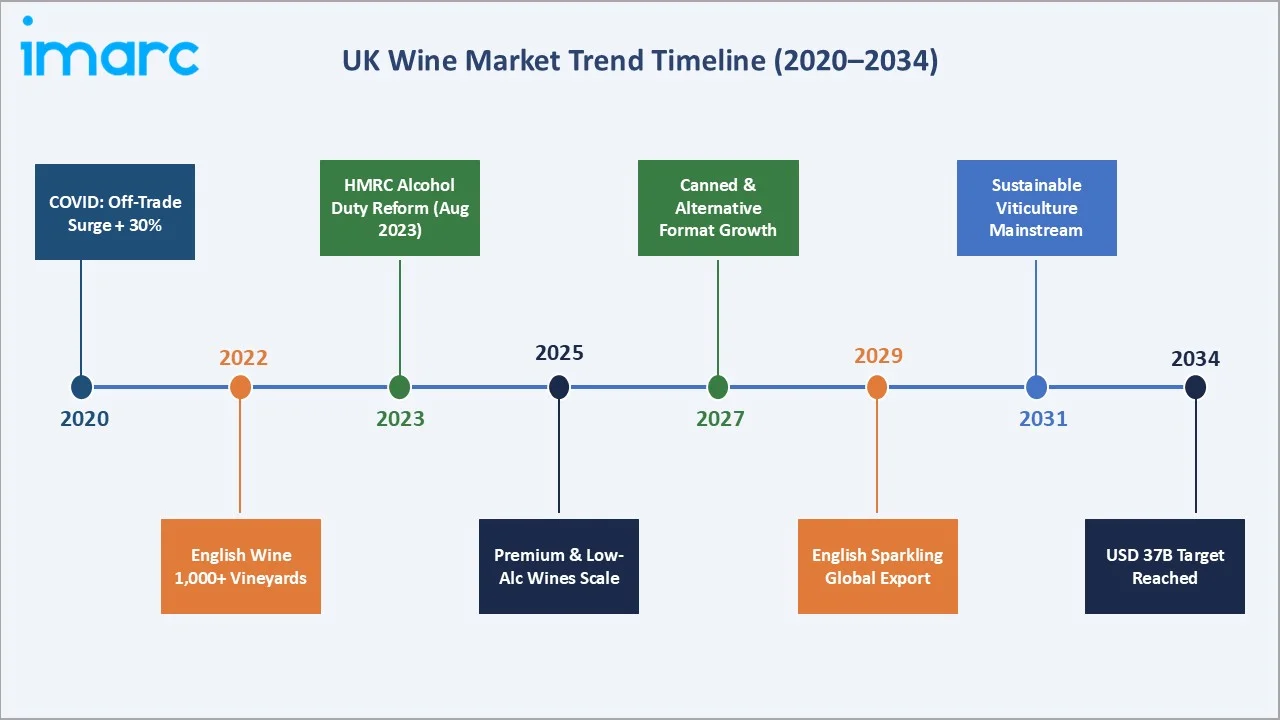

- Domestic Vineyard Expansion and English Wine Momentum: The UK crossed the milestone of 1,000 vineyards in 2023, a first in recorded history, with 87 new vineyards registered in that year alone, signaling strong indigenous production growth reshaping the domestic market landscape.

- E-Commerce and Direct-to-Consumer (DTC) Channel Growth: Online channels now account for approximately 12% of total off-trade wine volume in 2024, with Laithwaites alone serving more active customers.

Market Restraints

- HMRC Alcohol Duty Reform (August 2023): The UK government's comprehensive restructuring of alcohol duty in August 2023, replacing the previous flat-rate wine duty with strength-based tiered rates, significantly increased tax burdens on wines.

- Health-Conscious Consumer Moderation Trend: The UK's Chief Medical Officers' low-risk drinking guidelines and the growing Mindful Drinking Movement are driving a structural shift toward moderation among younger demographics.

Market Opportunities

- English Wine Export Growth: English sparkling wine is gaining international recognition comparable to Champagne among premium wine connoisseurs. Export volumes of English wine grew 28% between 2020-2024, with Nyetimber, Chapel Down, and Ridgeview wine reaching US, Japanese, and Scandinavian markets.

- Sustainable and Organic Wine Premiumization: UK consumer demand for certified organic and biodynamic wines is growing at 11% annually in 2024. Supermarkets including Waitrose and Marks & Spencer have committed to doubling their organic wine ranges by 2027.

Market Challenges

- Supply Chain Complexity Post-Brexit: The UK's exit from the EU single market created persistent logistical complexity for wine importers.

- Climate Variability Impact on UK Production: While warming UK temperatures are generally beneficial for domestic viticulture, extreme weather events, late frosts, summer flooding, and irregular harvest conditions create significant year-on-year production volatility for English and Welsh wineries.

- Affordability Pressure in Mass-Market Segments: Duty reform and import cost inflation have squeezed the GBP 5-7 per bottle segment, the UK's highest-volume retail price point in the off-trade, compressing margins for both supermarkets and producers.

Emerging Market Trends

1. Low and No-Alcohol Wine Transforming the Category

The Mindful Drinking Movement has elevated low/no-alcohol wine from a niche health segment to a mainstream consumer choice. Dealcoholization technology has advanced substantially, with vacuum distillation and spinning cone column processes now enabling genuine quality at 0% ABV.

2. English Sparkling Wine Establishing Global Fine Wine Credentials

English sparkling wine is undergoing a renaissance that parallels Champagne's emergence as a globally recognized luxury beverage category in the 20th century. Sales grew 187% between 2018 and 2023, reaching 6.2 million bottles in 2023.

3. Canned and Alternative Format Wines Capturing Younger Consumers

Canned wine in the UK grew 25% year-on-year in 2024, driven by convenience, portability, and a lower entry price point appealing to Gen-Z and millennial consumers seeking on-the-go wine occasions. The format is particularly strong at outdoor events, festivals, and casual social settings where glass bottles are impractical.

4. Sustainable Viticulture and Organic Wine Demand Rising

UK consumers are demanding greater transparency on wine sustainability credentials, including carbon footprint per bottle, water usage, pesticide-free certification, and biodiversity-friendly vineyard management.

5. Premiumization and Fine Wine Investment Deepening

UK consumers are demonstrably trading up in their wine purchases. Lay & Wheeler and Justerini & Brooks are reporting growing client interest in English Blanc de Blancs as a cellar-worthy investment, representing a qualitative milestone for domestic UK viticulture.

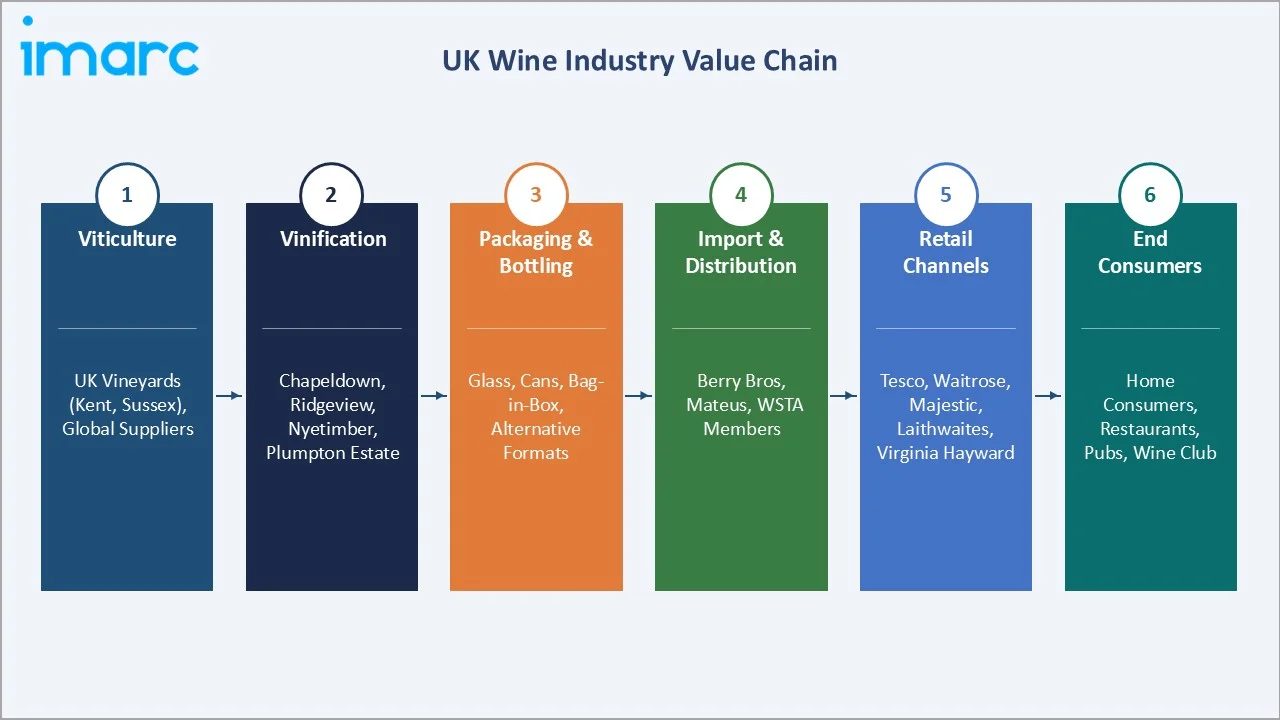

Industry Value Chain Analysis

The UK wine industry value chain spans six integrated stages from viticulture through end-consumer delivery. Each stage reflects distinct competitive dynamics, sustainability challenges, and innovation opportunities for both domestic producers and the UK's large wine import and distribution infrastructure.

|

Stage |

Key Players / Examples |

|

Viticulture & Grape Growing |

UK: Nyetimber, Chapel Down, Ridgeview (Sussex/Kent); Import: Bordeaux, Burgundy, New World estates |

|

Wine Production & Vinification |

English producers, overseas wineries; contract vinification at Plumpton Wine Estate and RidgeView |

|

Packaging & Bottling |

Ardagh Group (glass), Crown Holdings (cans), DS Smith (secondary packaging), Greenbottle |

|

Import, Negociant & Distribution |

Berry Bros & Rudd, Maisons Marques & Domaines, Bibendum, Ehrmanns, Hallgarten Druitt |

|

Retail – Off-Trade & On-Trade |

Tesco, Waitrose, M&S, Majestic Wine, Laithwaites, Naked Wines; Restaurants, pubs, hotels |

|

End Consumers |

UK adults (67% wine consumers), wine clubs, collectors, corporate events, on-trade dining |

Import agents and negociants occupy a structurally critical role in the UK wine value chain, sourcing and curating global wine portfolios that account for over 85% of UK wine volume consumption in 2025. Post-Brexit border changes are adding cost and complexity at this stage, while digital-native importers and DTC platforms are disrupting traditional intermediary layers, enabling producers to reach consumers directly at premium price points.

Technology Landscape in the UK Wine Industry

Precision Viticulture and Smart Vineyard Management

UK vineyard operators are increasingly adopting precision viticulture technologies to optimize yields and quality in the nation's variable climate. Drone imaging for vine health monitoring, soil moisture sensors for precision irrigation, and satellite-based NDVI analysis for yield prediction are being deployed by leading English estates including Chapel Down and Nyetimber.

Dealcoholization Technology for Low/No-Alcohol Wine

Advances in vacuum distillation, spinning cone column (SCC) technology, and reverse osmosis have transformed the quality ceiling for low and no-alcohol wine production. These processes selectively remove ethanol while preserving aroma compounds and structural complexity, addressing the fundamental challenge of low-alcohol wine's historically flat sensory profile.

E-Commerce Technology and AI-Powered Wine Recommendation

UK online wine retail platforms are deploying AI-driven recommendation engines that match consumer taste profiles to wine portfolio selections with increasing accuracy. Augmented reality label scanning, enabling instant wine provenance, review, and food-pairing data, is growing in adoption among premium wine brands targeting tech-savvy UK consumers.

Packaging Innovation: Sustainable Materials and Alternative Formats

UK wine packaging is undergoing a format revolution driven by sustainability mandates and consumer lifestyle demands. Greenbottle's paper-lined wine bottle reduces glass weight by 90% per unit.

Climate Adaptation Technology for English Viticulture

UK winemakers are investing in climate adaptation technology, including frost protection systems (wind machines, overhead sprinklers), hail netting for southern England vineyards, and varietal selection research for resilience to UK-specific climate extremes.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Still Wine |

54.3% |

2025 |

| Color |

White Wine |

39.3% |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

Region |

London |

18.6% |

2025 |

By Product Type

Still wine commands a 54.3% majority share of the UK wine market in 2025, reflecting its role as the everyday wine format for both home consumption and on-trade dining. The still wine category encompasses the full spectrum from sub-GBP 5 entry-level supermarket wines to GBP 100+ fine wine purchases, making it uniquely broad in its consumer accessibility.

To access detailed market analysis, Request Sample

Sparkling wine at 28.7% in 2025, a substantially higher proportion than most global markets, reflects the UK's unique cultural affinity for celebratory fizz. Fortified wine and vermouth at 17.0% encompasses Port, Sherry, Madeira, and vermouth, benefiting from a cocktail culture renaissance and the trend toward premium at-home mixology.

By Color

White wine leads the UK wine color market at 39.3% in 2025, narrowly ahead of red wine at 38.4%, reflecting British consumers' affinity for dry, aromatic white styles including New Zealand Sauvignon Blanc, French Chablis, Italian Pinot Grigio, and increasingly, English Bacchus.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

London |

18.6% |

Highest per-capita income, fine dining scene, premium wine import hub, wine tourism |

|

South East |

16.3% |

English vineyard heartland (Kent, Sussex), affluent suburban households, wine tourism |

|

North West |

12.4% |

Manchester metropolitan growth, restaurant culture, Liverpool independent wine trade |

|

East of England |

10.7% |

Cambridge science economy, growing vineyard sector, high household incomes |

|

South West |

9.8% |

Bristol wine culture, tourism footfall, growing English wine production |

|

Scotland |

8.6% |

Whisky heritage expanding into wine appreciation, Edinburgh premium retail |

|

West Midlands |

7.4% |

Birmingham urban renewal, growing ethnic diversity driving wine exploration |

|

Yorkshire and the Humber |

6.3% |

Leeds restaurant growth, expanding independent wine retail scene |

|

East Midlands |

5.4% |

Nottingham, Leicester urban consumption, price-sensitive market |

|

Others |

4.5% |

Wales, Northern Ireland; relatively lower per-capita wine spend |

London commands 18.6% of the UK wine market revenue in 2025, disproportionately high relative to its 13.5% share of the UK population, reflecting the capital's concentration of premium wine consumption occasions. London hosts 88 restaurants of the UK's Michelin stars, the country's largest cluster of specialist wine merchants and wine bar concepts, and the trading offices of the major international wine import and distribution businesses.

The South East, with 16.3% in 2025, is uniquely positioned as both a significant consumption market and the UK's domestic wine production heartland. Kent and Sussex together host approximately 400 of the UK's 1,000+ vineyards, with the North and South Downs chalk geology directly comparable to Champagne's terroir, a factor contributing to English sparkling wine's quality reputation.

Competitive Landscape

The UK wine competitive landscape features a complex interplay of global wine conglomerates that dominate volume imports and mass-market retail, alongside premium specialist importers, established English wine producers building global fine wine credentials, and a growing cohort of DTC subscription brands reshaping the off-trade channel.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

Constellation Brands |

Robert Mondavi, Kim Crawford |

Leader |

Premium New World imports, strong off-trade shelf |

|

Treasury Wine Estates |

Penfolds, Wolf Blass, Beringer |

Leader |

Premium Australian/global portfolio, premiumization |

|

LVMH (Moët Hennessy) |

Moët & Chandon, Veuve Clicquot |

Leader |

Champagne & fine wine, luxury on-trade focus |

|

Gallo Family Vineyards |

Gallo, Barefoot, MacMurray |

Leader |

Mass-market volume, entry-price off-trade |

|

Majestic Wine |

Majestic own-label |

Challenger |

Specialist off-trade, subscription, tasting events |

|

Accolade Wines |

Hardys, Echo Falls, Banrock |

Challenger |

Volume supermarket supply, value positioning |

|

Berry Bros & Rudd |

BBR Own Label, Fine Wines |

Challenger |

Fine wine retail, investment, DTC merchant |

|

Chapel Down |

Chapel Down English Wines |

Emerging |

English wine leader, DTC and premium on-trade |

|

Nyetimber |

Nyetimber Sparkling |

Emerging |

English fine sparkling, global prestige benchmark |

|

Ridgeview Wine Estate |

Ridgeview Sparkling |

Emerging |

English sparkling, sustainability-certified |

|

Laithwaites Wine |

Laithwaites Merchant Range |

Emerging |

Subscription DTC, 600,000+ active customers |

|

Naked Wines |

Naked Wines Exclusive |

Emerging |

Crowd-funded winemaker DTC model, premium access |

The competitive positioning across market presence and strategic investment dimensions for key UK wine market participants in 2025 illustrates the structural separation between volume-oriented global conglomerates, specialist and premium challengers, and domestic English wine producers building fine wine positioning.

Key Company Profiles

Constellation Brands

Constellation Brands is one of the world's largest wine companies. In the UK, Constellation holds leading positions in the premium imported wine segment through its New Zealand, Californian, and Italian portfolios.

- Product Portfolio: Kim Crawford, Robert Mondavi, The Prisoner Wine Company, and Ruffino.

- Recent Developments: In February 2026, Constellation Brands appointed Enotria as its new on-trade and independent retail distributor for a selection of its wine brands.

- Strategic Focus: Constellation's UK strategy focuses on premiumization of its core portfolio above GBP 10 per bottle, digital commerce expansion through supermarket loyalty app partnerships, and sustainability story-telling to capture the growing cohort of environmentally conscious UK premium wine buyers through 2030.

Chapel Down

Chapel Down is England's most commercially successful and widely recognized wine producer, headquartered in Tenterden, The company was the first English wine producer to list on the public markets and is a leading ambassador for the English wine appellation internationally.

- Product Portfolio: Sparkling: Kit's Coty Blanc de Blancs, Brut, English Sparkling Intro Case; Still: Bacchus, Pinot Blanc, Pinot Noir; Low-ABV: Chapel Down 0% range; Gin and Beer: Curious Brew from the Curious Drinks brand.

- Recent Developments: In September 2025, Chapel Down scrapped plans to build a £32mn winery as part of a strategic overhaul.

- Strategic Focus: Chapel Down's strategy is to establish the dominant English wine brand for both domestic premium retail and international export, build on-trade credentials through luxury hotel and airline partnerships, and develop the Chapel Down visitor experience as a wine tourism destination generating supplementary revenue and brand equity.

Nyetimber

Nyetimber is England's most internationally acclaimed sparkling wine producer, based in West Sussex on chalk soils that closely mirror Champagne's terroir. Founded in 1988 and relaunched in 2006 by Eric Hereema, Nyetimber has built a global fine sparkling wine reputation through consistent 91-95 point scores from Decanter, Wine Spectator, and Jancis Robinson.

- Product Portfolio: Classic Cuvée, Blanc de Blancs, Rosé, Cuvée Cherie, and Tillington Single Vineyard.

- Recent Developments: In April 2025, Nyetimber made history as the first English sparkling wine producer to offer a prestige cuvée on an airline, with its 1086 by Nyetimber Rosé 2014 and 1086 by Nyetimber 2014 now being served to passengers in British Airways’ First Class cabin.

- Strategic Focus: Nyetimber's strategy focuses on establishing itself as the definitive fine English sparkling wine, directly comparable to Prestige Champagne houses in quality, pricing (GBP 30-75 per bottle), and global distribution, while maintaining its single-estate production ethos and sustainability certifications that resonate with premium-conscious UK and international consumers.

Market Concentration Analysis

The UK wine market exhibits moderate concentration at the import and branded distribution level, with the top five global wine groups collectively commanding approximately 35-45% of total UK off-trade wine value. However, the overall market is structurally fragmented, with hundreds of import agents, specialist retailers, and an expanding domestic producer cohort.

The top 5 players collectively account for approximately 33-44% of the UK wine market in 2025. The remaining 56-67% is highly fragmented across approximately 450+ active import agents, 200+ specialist wine retailers, 1,000+ domestic producers, and a rapidly growing cohort of DTC subscription businesses, reflecting the UK wine market's structurally diverse and competitive character.

The UK wine distribution layer is undergoing consolidation, with the major grocery multiples rationalizing their wine supplier bases to fewer, larger import partners that can meet scale, traceability, and sustainability requirements. Independent wine merchant numbers have declined approximately 8% between 2020 and 2024 as operator economics become increasingly challenging without differentiated subscription or experience-led revenue streams.

Investment & Growth Opportunities

Fastest-Growing Segments

Low and no-alcohol wine represents the UK wine market's highest-growth investment opportunity at ~14.6% CAGR through 2034. The category is forecast to exceed GBP 500 Million in UK retail value by 2028. English sparkling wine production and vineyard infrastructure represents the second-highest-growth investment opportunity at ~8.3% CAGR through 2034.

Emerging Market Expansion

Wine tourism is an undermonetized but rapidly growing component of the UK wine industry. Investment in vineyard visitor centers, boutique accommodation, and licensed restaurant operations at English wine estates can generate GBP 50-150 per visitor in ancillary revenue on top of direct wine sales – significantly improving whole-estate economics.

Venture Investment Trends

Private equity interest in consolidating the specialist wine merchant sector, targeting operators with 60,000-200,000 active subscribers, is growing, with deal multiples for wine subscription businesses trading at 8-12x EBITDA in 2024, reflecting strong recurring revenue quality and low churn characteristics of established wine clubs.

Future Market Outlook (2026-2034)

The UK wine market forecast projects steady expansion from USD 27.23 Billion in 2025 to USD 37.00 Billion by 2034 at a CAGR of 3.36%, a pace reflective of a mature, well-penetrated market where value growth is driven by premiumization rather than volume expansion. The UK will remain the world's second-largest wine importer throughout the forecast period, while domestic production is forecast to grow its market share from ~5% to ~10% of volume by 2034 as English wine achieves commercial scale.

Two technology shifts are most likely to reshape the UK wine industry through 2034. AI-driven personalized recommendation at scale, moving from algorithmic to genuinely individualized wine discovery for millions of UK consumers, will fundamentally alter how premium wines are discovered, trialed, and loyalized, advantaging DTC-native operators who own the consumer relationship data.

By 2034, the UK wine industry is expected to have undergone a fundamental transformation in three dimensions: the domestic production share will have more than doubled, the DTC subscription channel will rival or exceed specialist wine merchant value; and the low/no-alcohol category will have transitioned from a niche concession to a mainstream category stocked prominently by all major UK grocers and on-trade operators.

Research Methodology

Primary Research

Primary research encompassed over 50 structured interviews conducted in 2024-2025 with UK wine industry stakeholders, including import agent directors and national account managers, specialist retailer buyers, Big Four supermarket wine category managers, English winery commercial directors ,WineGB commercial development officers, and institutional investors in UK vineyard assets. Primary data validated market sizing, segmentation splits, channel dynamics, and regulatory impact assessments.

Secondary Research

Secondary sources include WSTA annual market reports (2020-2024), WineGB production and sales statistics (2020-2024), HMRC alcohol duty statistical releases, Wine Intelligence UK consumer tracking (Vinitrac survey data), IWSR Drinks Market Analysis UK database, ONS household expenditure surveys, Kantar Worldpanel off-trade wine purchase data, Decanter and Wine Spectator UK market analysis, and trade publications including Harpers Wine & Spirit, The Drinks Business, and Imbibe Magazine.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, urbanization indices, consumer expenditure data, and historical market evolution patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for macroeconomic uncertainty.

UK Wine Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Still Wine, Sparkling Wine, Fortified Wine And Vermouth |

| Colors Covered | Red Wine, Rose Wine, White Wine |

| Distribution Channels Covered |

|

| Regions Covered | London, South East, North West, East of England, South West, Scotland, West Midlands, Yorkshire and The Humber, East Midlands, Others |

| Key Companies | Constellation Brands, Treasury Wine Estates, LVMH (Moët Hennessy), Gallo Family Vineyards, Majestic Wine, Accolade Wines, Berry Bros & Rudd, Chapel Down, Nyetimber, Ridgeview Wine Estate, Laithwaites Wine, Naked Wines. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the UK wine market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the UK wine market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the UK wine industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the UK Wine Market Report

The UK wine market was valued at USD 27.23 Billion in 2025.

The UK wine market is projected to reach USD 37.00 Billion by 2034, growing at a CAGR of 3.36% during the 2026-2034 forecast period, driven by premiumization and domestic production growth.

Still wine leads with a 54.3% share in 2025, reflecting its role as the everyday wine format for both home consumption and on-trade dining across all UK income demographics.

White wine leads with a 39.3% share in 2025, marginally ahead of red wine at 38.4%, reflecting British consumers' strong preference for dry aromatic whites like Sauvignon Blanc and Pinot Grigio.

London leads with 18.6% of UK wine revenue in 2025, driven by the highest per-capita income, concentration of premium on-trade venues, and fine wine import and distribution businesses.

Key drivers include 67% adult wine consumption rate, rising disposable incomes supporting premiumization, domestic English vineyard expansion to 1,000+ sites, and growing DTC subscription channels.

The August 2023 HMRC reform restructured wine duty to strength-based rates, adding GBP 0.44 per bottle average for standard wines. This is encouraging lower-ABV reformulations and reshaping pricing strategies.

Low and no-alcohol wine is growing at ~14.6% CAGR through 2034, driven by the UK's Mindful Drinking Movement, Dry January (4.5 million participants in 2024), and improving dealcoholization technology quality.

Leading companies include Constellation Brands, Treasury Wine Estates, LVMH Moët Hennessy, Gallo Family Vineyards, Majestic Wine, Accolade Wines, Chapel Down, and Nyetimber.

The UK exceeded 1,000 vineyards in total for the first time in 2023, covering 4,209 hectares – a 123% increase over the prior decade, with 87 new vineyards registered in 2023 alone.

The UK is the world's second-largest wine importer with approximately 1.7 billion bottles imported in 2022, and the top global exporter of spirits, shipping approximately 1.8 billion bottles overseas in 2022.

The UK wine market is forecast to grow at a CAGR of 3.36% from 2026-2034, expanding from USD 27.20 Billion in 2025 to USD 37.00 Billion by 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)