Ultra-Secure Smartphone Market Size, Share, Trends and Forecast by Operating System, End User, and Region, 2026-2034.

Global Ultra-Secure Smartphone Market Size, Share, Trends & Forecast (2026-2034)

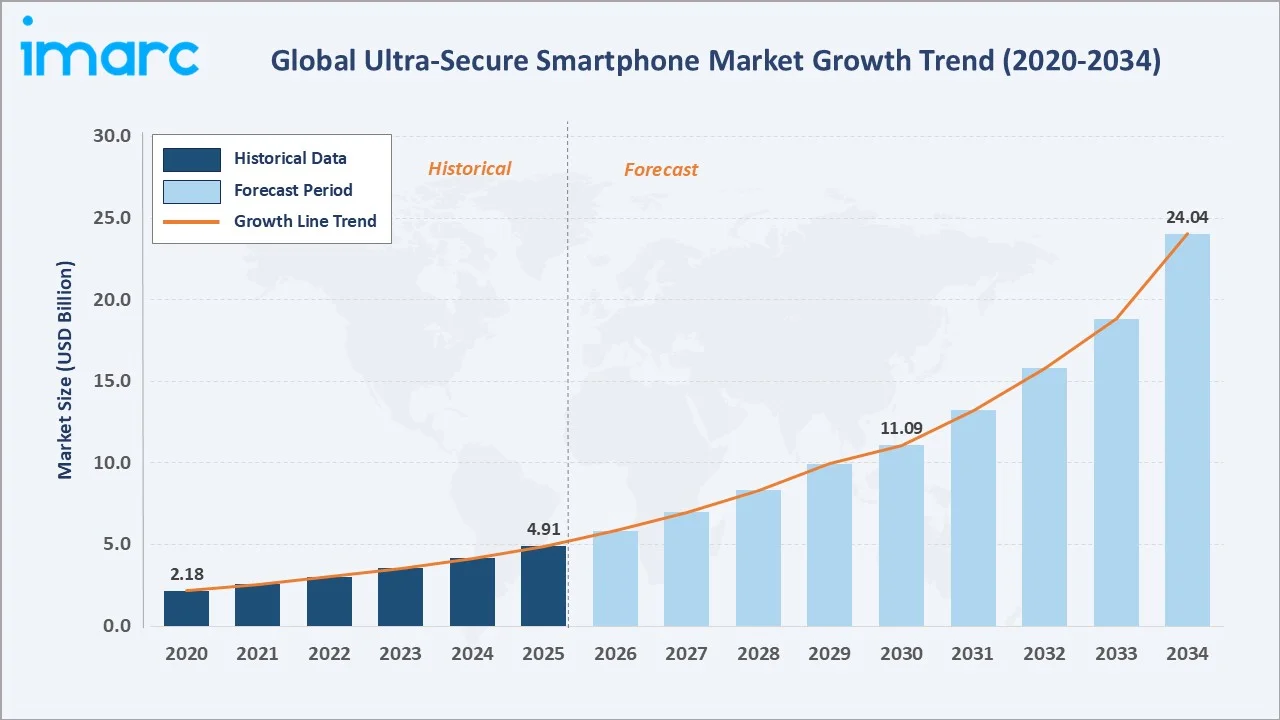

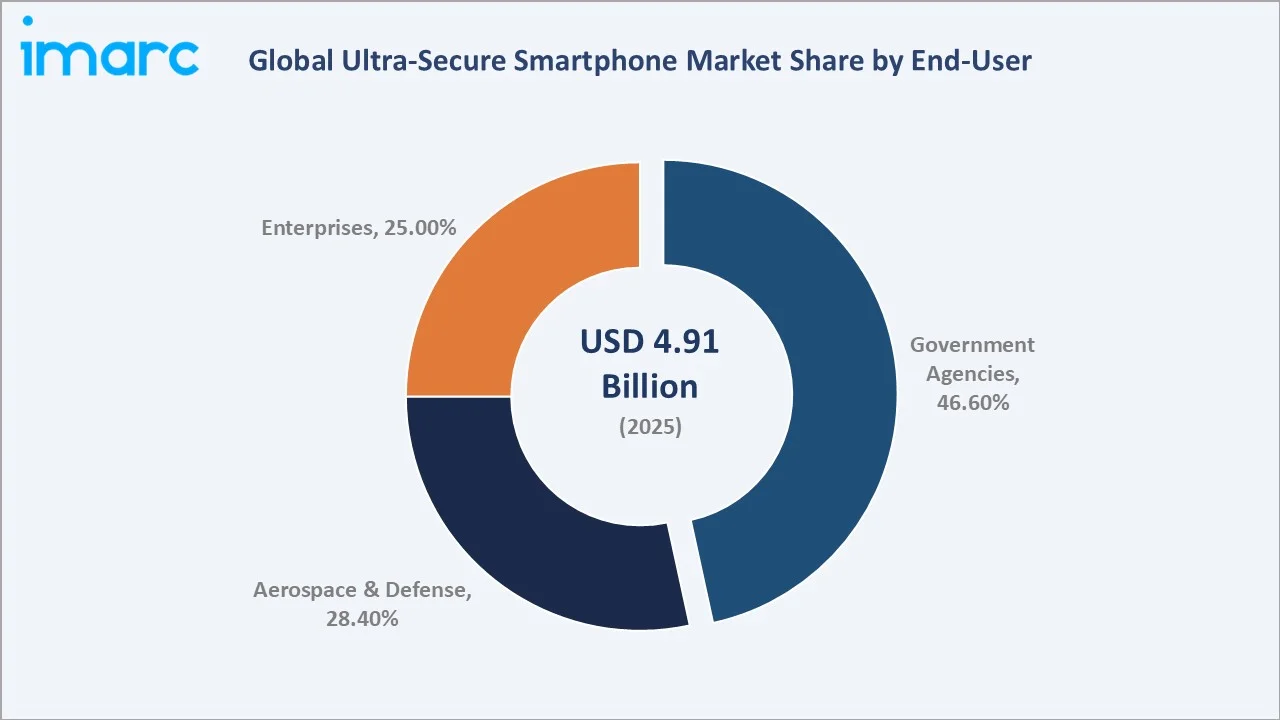

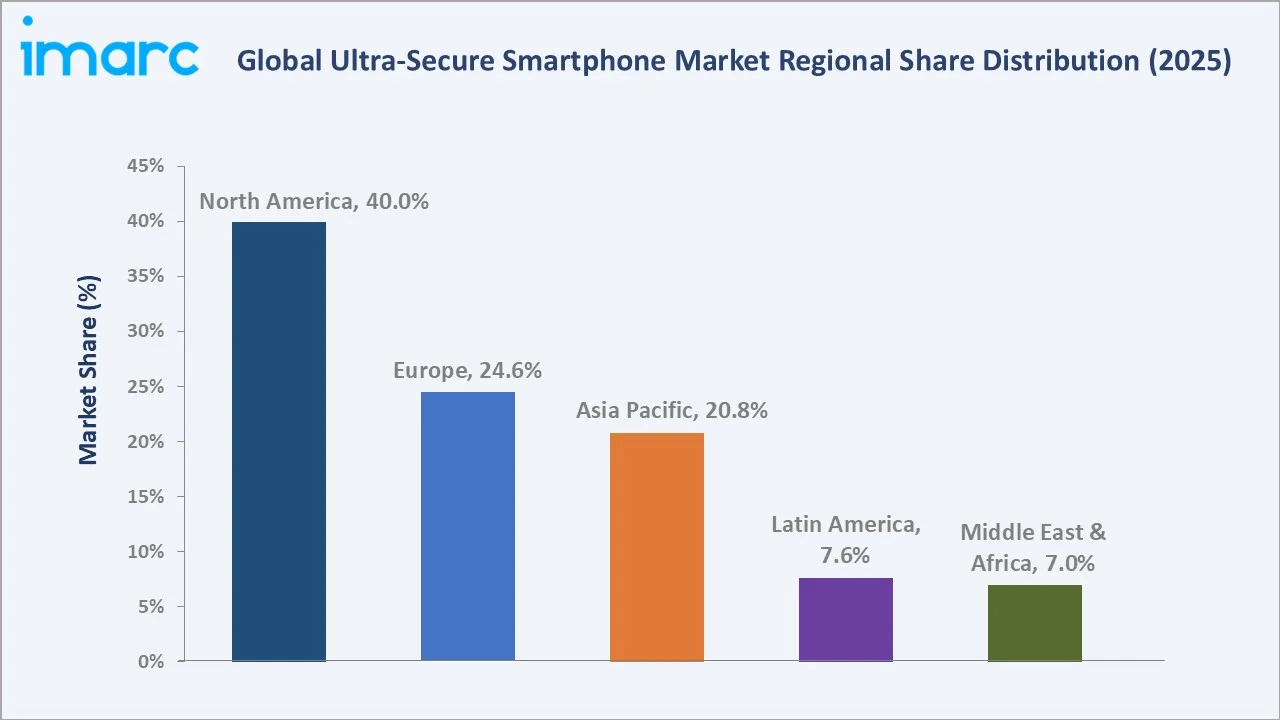

The global ultra-secure smartphone market size was valued at USD 4.91 Billion in 2025 and is projected to reach USD 24.04 Billion by 2034, exhibiting a CAGR of 17.68% during the forecast period 2026-2034. Mounting cyber espionage incidents, escalating nation-state surveillance threats, and rising regulatory mandates around classified communications are the primary catalysts accelerating ultra-secure smartphone market growth. Android leads the operating system segment at 68.6% in 2025, driven by hardened OS variants deployed across government agencies. Government agencies dominate end-user demand at 46.6%, while North America commands 40.0% of global revenue in 2025 as the world's largest regional market.

Market snapshot

|

Metric |

Value |

|

Market Size 2025 |

USD 4.91 Billion |

|

Forecast Market Size 2034 |

USD 24.04 Billion |

|

CAGR 2026-2034 |

17.68% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2020-2025 |

|

Largest Region |

North America (40.0% share, 2025) |

|

Fastest Growing Region |

Asia Pacific (CAGR ~21.3%) |

|

Leading Operating System |

Android (68.6%, 2025) |

|

Leading End User |

Government Agencies (46.6%, 2025) |

Figure 1 below presents the global ultra-secure smartphone market growth trajectory from 2020 through 2034, contrasting consistent historical expansion against a sustained forecast curve powered by rising geopolitical tensions, digital sovereignty initiatives, and the proliferation of encrypted communication mandates across government and enterprise sectors.

To get more information on this market, Request Sample

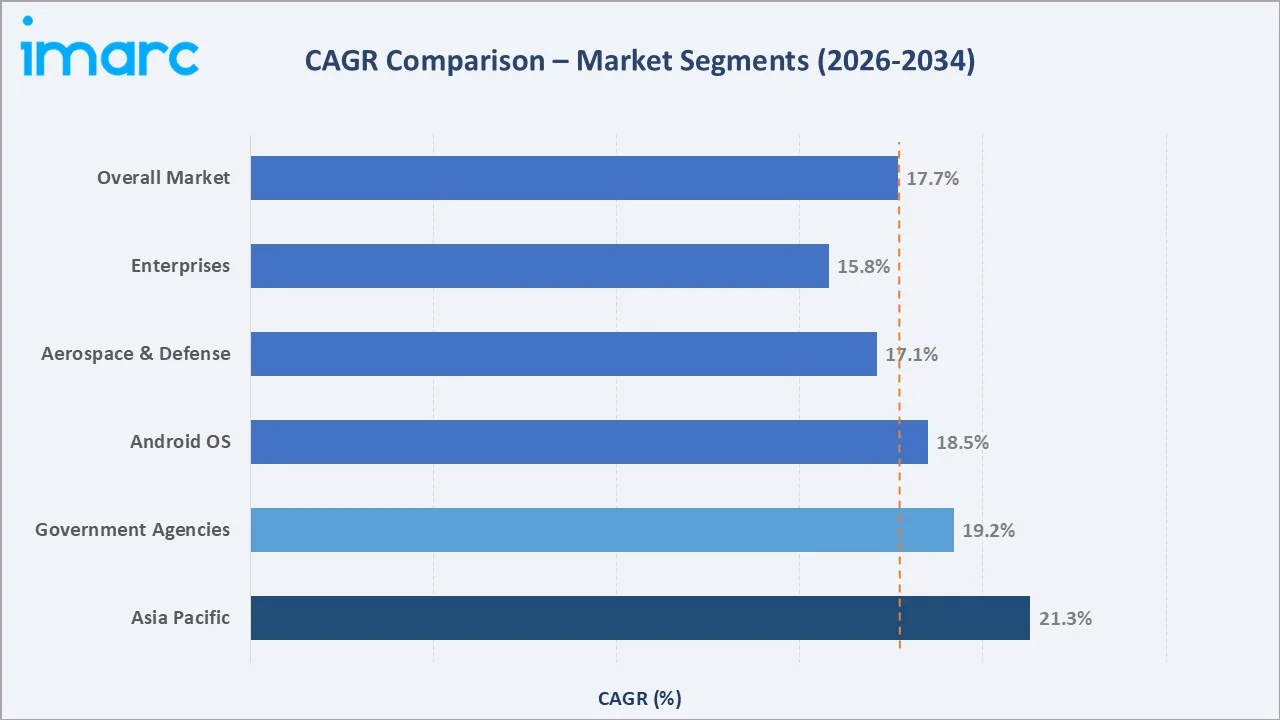

Figure 2 below illustrates segment-level CAGR comparisons, highlighting Asia Pacific and Government Agencies as the two fastest-growing sub-categories within the global ultra-secure smartphone industry analysis through 2034.

Executive Summary

The global ultra-secure smartphone market is undergoing a structural shift driven by the convergence of digital sovereignty, quantum computing threats, and the acceleration of classified mobile communications. Valued at USD 4.91 Billion in 2025, the market is forecast to reach USD 24.04 Billion by 2034 at a CAGR of 17.68%. More than 2 in 5 ransomware attacks reported to the FBI in 2023 targeted organizations in a critical infrastructure sector, the agency said in its annual Internet Crime Report. Of the 2,825 ransomware attacks reported to the FBI, 1,193 hit critical infrastructure organizations. The proportion of ransomware attacks hitting critical infrastructure grew from one-third of attacks reported to the FBI in 2022, directly amplifying demand for hardened mobile communication devices.

Android's hardened variants command 68.6% of the operating system landscape in 2025, propelled by the adoption of military-grade Android builds such as Samsung Knox and BlackBerry's secure Android platform. iOS maintains a 31.4% share, underpinned by Apple's Secure Enclave architecture and stringent App Store security controls that make it the preferred platform for high-value enterprise deployments.

Key Market Insights

|

Insight |

Data Point |

|

Largest Operating System |

Android – 68.6% share (2025) |

|

Second Operating System |

iOS – 31.4% share (2025) |

|

Largest End-User Segment |

Government Agencies – 46.6% (2025) |

|

Second End-User Segment |

Aerospace & Defense – 28.4% (2025) |

|

Third End-User Segment |

Enterprises – 25.0% (2025) |

|

Leading Region |

North America – 40.0% revenue share (2025) |

|

Fastest Growing Region |

Asia Pacific – CAGR ~21.3% |

|

Top Key Companies |

BlackBerry, Thales, Samsung, Apple, Bittium, Boeing, Atos |

|

Market Opportunity |

Post-quantum encryption integration – USD 3.2B incremental opportunity by 2030 |

Analytical Observations Aligning With The Above Data Points:

- Android's 68.6% dominance in 2025 reflects the accelerating adoption of military-grade Android builds – Samsung Knox, BlackBerry Secure, and custom AOSP variants hardened to NSA Suite B cryptographic standards – across 80+ government departments globally.

- Government agencies' 46.6% share underscores the dependency on NSA-CSfC (Commercial Solutions for Classified) certified devices, with over 3.2 million secured mobile endpoints deployed across U.S. federal agencies alone as of 2024.

- North America's 40.0% market dominance in 2025 is anchored by the U.S. federal procurement ecosystem, where the DoD's Commercial Virtual Remote Environment (CVR) program expanded to over 1.5 million users by 2024.

- Asia Pacific's ~21.3% CAGR trajectory reflects India's 2024 Cybersecurity Policy mandate requiring secure devices across all central government communications, combined with AUKUS partners' collective defense communications upgrade programs exceeding USD 800 million.

- Enterprise adoption at 25.0% in 2025 is concentrated in financial services, legal, and healthcare sectors where data protection regulations such as GDPR, HIPAA, and SOX create compliance-driven demand for certified secure mobile devices.

Global Ultra-Secure Smartphone Market Overview

Ultra-secure smartphones are hardened mobile communication devices engineered to provide protection against nation-state surveillance, cyber espionage, data exfiltration, and unauthorized access. These devices integrate military-grade hardware encryption, certified secure operating systems, end-to-end encrypted communication layers, anti-tamper mechanisms, and remote wipe capabilities into a unified mobile platform designed for classified or highly sensitive operations.

Applications span government and intelligence operations, defense and aerospace communications, classified enterprise transactions, and sensitive diplomatic communications. Modern ultra-secure smartphones operate across three core architectural layers: hardware security (secure enclaves, physically unclonable functions, tamper-evident packaging), OS-level hardening (SELinux, custom verified boot chains, stripped-down attack surfaces), and application-layer security (encrypted VoIP, secure messaging, VPN enforcement, containerization).

Market Dynamics

To evaluate market opportunities, Request Sample

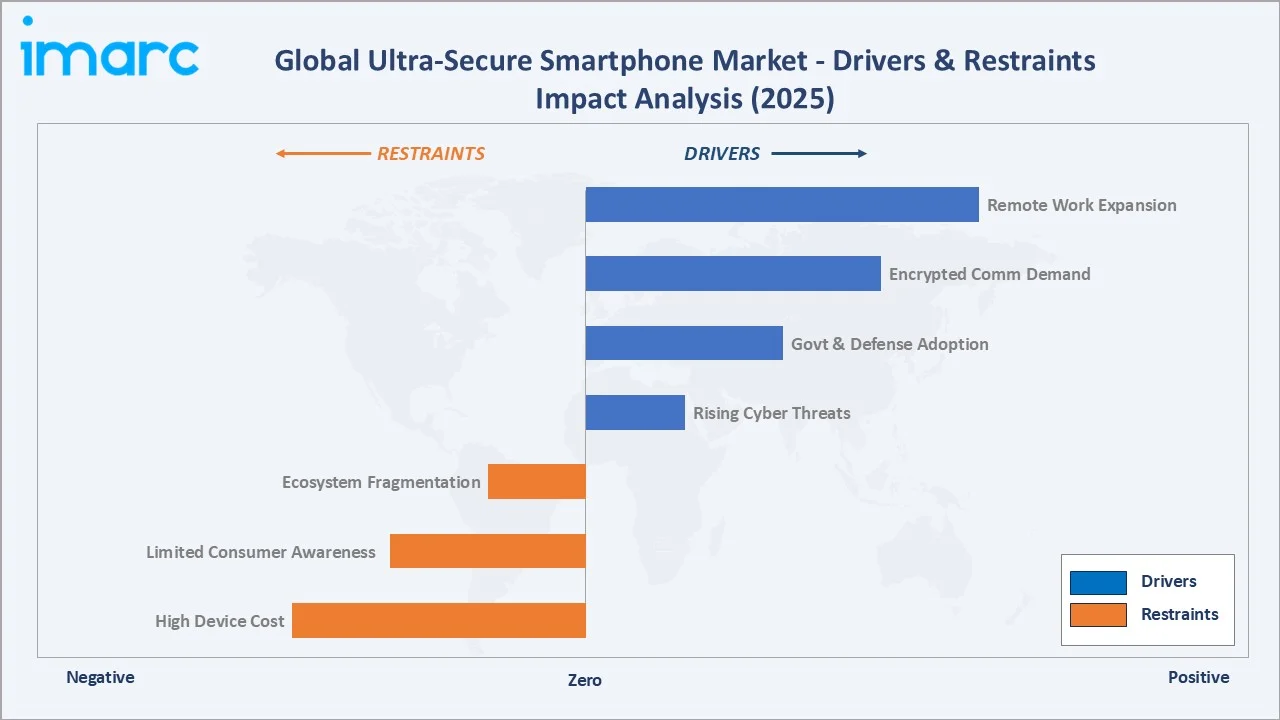

Market Drivers

- Rising Nation-State Cyber Threats: The number of state-sponsored cyber operations targeting government networks increased by 38% between 2022 and 2024 per the Microsoft Digital Defense Report, creating urgent demand for NSA-certified and TEMPEST-compliant mobile devices.

- Government and Defense Procurement Expansion: In 2024, investments in defence grew significantly across the Alliance. NATO Allies in Europe and Canada invested a total of USD 486 billion in defence, a 19.4% increase in real terms from 2023. In recent years, NATO European Allies and Canada have added more than USD 700 billion extra for defence. In doing so, these Allies are taking on greater responsibility for the defence and security of the Euro-Atlantic area, driving structured procurement of certified ultra-secure handsets.

- Regulatory Compliance and Data Protection Mandates: The European Union's NIS2 Directive (2023), the U.S. Federal Risk and Authorization Management Program (FedRAMP), and India's Digital Personal Data Protection Act (2023) mandate cryptographic standards for government mobile endpoints.

- Expanding Remote and Mobile Work in Sensitive Sectors: The post-pandemic normalization of remote work in defense, intelligence, and financial services sectors has expanded the attack surface for mobile espionage, driving enterprise demand for certified secure devices.

These combined drivers create a structural demand environment that is largely budget-insulated from consumer technology cycles, ensuring consistent market growth even during broader macroeconomic downturns. The CAGR of 17.68% between 2026 and 2034 reflects both organic procurement growth and emerging demand from new geographies, particularly across Asia Pacific and the Middle East.

Market Restraints

- High Device Acquisition and Lifecycle Cost: Ultra-secure smartphones command price premiums of 300%–600% over consumer-grade equivalents, with certified devices typically priced between USD 1,500 and USD 8,000 per unit, constraining enterprise and SME adoption outside government-funded procurement programs.

- Limited Consumer and SME Market Awareness: Beyond government and defense sectors, awareness of ultra-secure smartphone capabilities remains limited, with fewer than 22% of enterprise IT decision-makers in APAC and Latin America identifying ultra-secure mobile devices as a priority procurement category in 2024 surveys.

- Ecosystem Fragmentation and Interoperability Challenges: The market operates across 7+ distinct certification frameworks – NSA CSfC, NATO STANAG, Common Criteria EAL 5+, FIPS 140-3 – creating interoperability barriers that complicate multi-agency or multi-national deployments.

Market Opportunities

- Post-Quantum Cryptography (PQC) Integration: The U.S. NIST's August 2024 publication of finalized PQC standards – ML-KEM, ML-DSA, SLH-DSA – creates a hardware and software upgrade cycle across all existing certified device fleets. This transition represents an estimated USD 3.2 Billion incremental market opportunity through 2030.

- 5G-Enabled Secure Private Networks: The deployment of 5G standalone (SA) architecture enables dedicated, isolated secure network slices for government and defense mobile communications, expanding the addressable market for ultra-secure smartphones beyond existing classified facility use cases to field operations environments.

- Emerging Economy Sovereign Mobile Programs: India's BharatPhone initiative, Brazil's ABIN secure communications program, and Saudi Arabia's Vision 2030 cybersecurity initiative represent collectively over USD 2.1 Billion in sovereign procurement opportunity through 2030.

Market Challenges

- Rapidly Evolving Threat Landscape: The emergence of commercial spyware – Pegasus, Predator – that exploits zero-day vulnerabilities in certified operating systems creates continuous pressure on device manufacturers to deliver rapid security patches, challenging the traditionally long certification cycles of 12–18 months for secure mobile devices.

- Talent Shortage in Secure Mobile Development: The global shortage of cryptographic engineering and secure mobile software talent – estimated at 3.5 million unfilled cybersecurity positions globally by ISC2 in 2024 – constrains the pace of innovation and new product development across the competitive landscape.

- Export Control Complexity: Ultra-secure devices incorporating NSA-approved cryptographic modules are subject to U.S. International Traffic in Arms Regulations (ITAR) and Export Administration Regulations (EAR), complicating international sales particularly to emerging-market government clients.

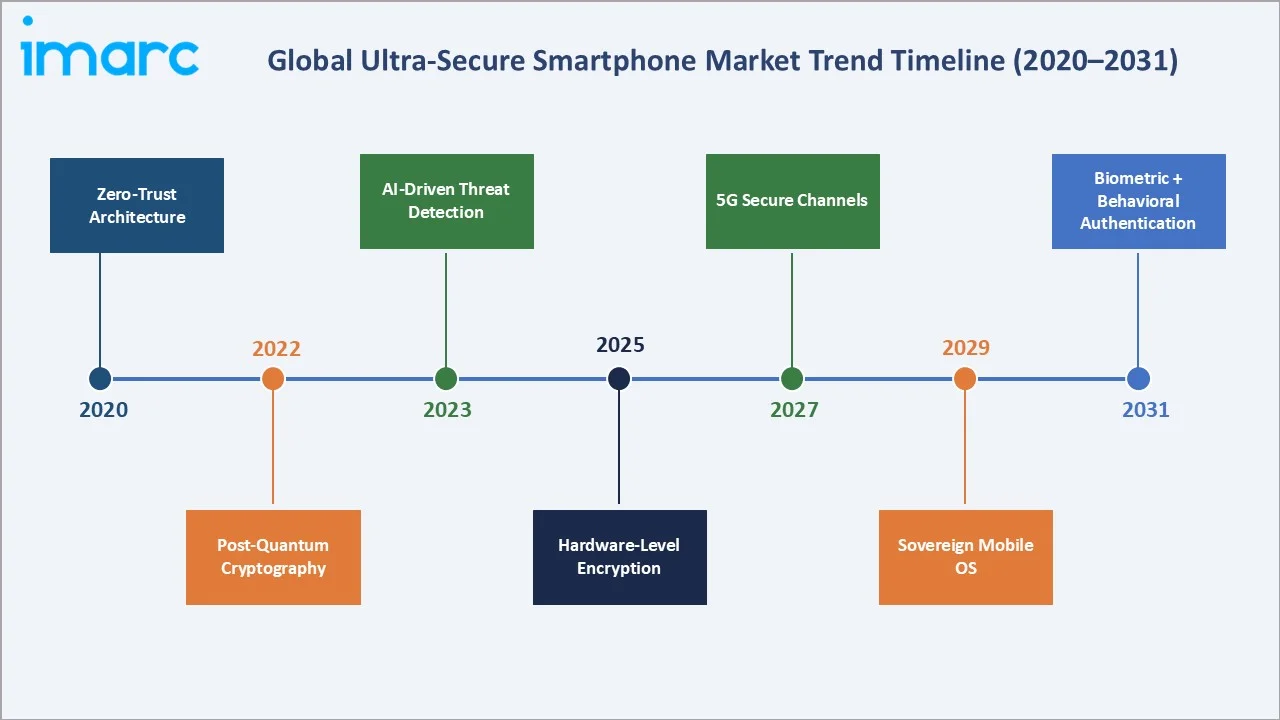

Emerging Market Trends

1. Zero-Trust Architecture Adoption in Mobile Security

Zero-trust security models, which assume breach and verify every access request regardless of network location, are being embedded into ultra-secure smartphone architectures. The U.S. DoD's Zero Trust Strategy, published in 2022, mandated zero-trust implementation across all department communications by 2027, directly driving procurement of compatible ultra-secure mobile endpoints. Over 40% of new government device tenders issued in 2024 included zero-trust compliance as a mandatory specification.

2. Post-Quantum Cryptography Hardware Integration

The NIST PQC standard finalization in August 2024 has triggered a device refresh cycle across government and defense fleets globally. Manufacturers including Thales and BlackBerry announced PQC-ready hardware roadmaps in late 2024 and early 2025. Devices incorporating lattice-based cryptographic accelerators (ML-KEM 1024) will command a 15%–25% price premium over current-generation secure devices, expanding average selling prices and revenue per unit.

3. AI-Driven Mobile Threat Detection

On-device AI inference engines are being integrated into secure smartphone security stacks to enable real-time behavioral anomaly detection, identifying compromised applications or communication channels without transmitting sensitive telemetry to cloud servers. Samsung's Knox Matrix and BlackBerry's Cylance-powered threat intelligence represent current-generation implementations, with on-device AI security features expected in over 65% of new certified devices by 2028.

4. Sovereign Operating System Development

Russia's Aurora OS, South Korea's open-source government mobile platform, and Germany's BSI-certified Taurus Secure Phone OS reflect a global trend toward government-developed or government-certified sovereign mobile operating systems reducing dependency on U.S.-origin platforms.

5. Hardware-Level Security Enclave Advancement

Next-generation secure element architectures – ARM TrustZone 3.0, RISC-V Keystone Enclave, and custom military-grade TPM 3.0 modules – are enabling enhanced cryptographic key isolation and in-device secure execution environments. These hardware advances make physical extraction attacks technically impractical, a critical differentiator for devices deployed in field intelligence and special operations contexts.

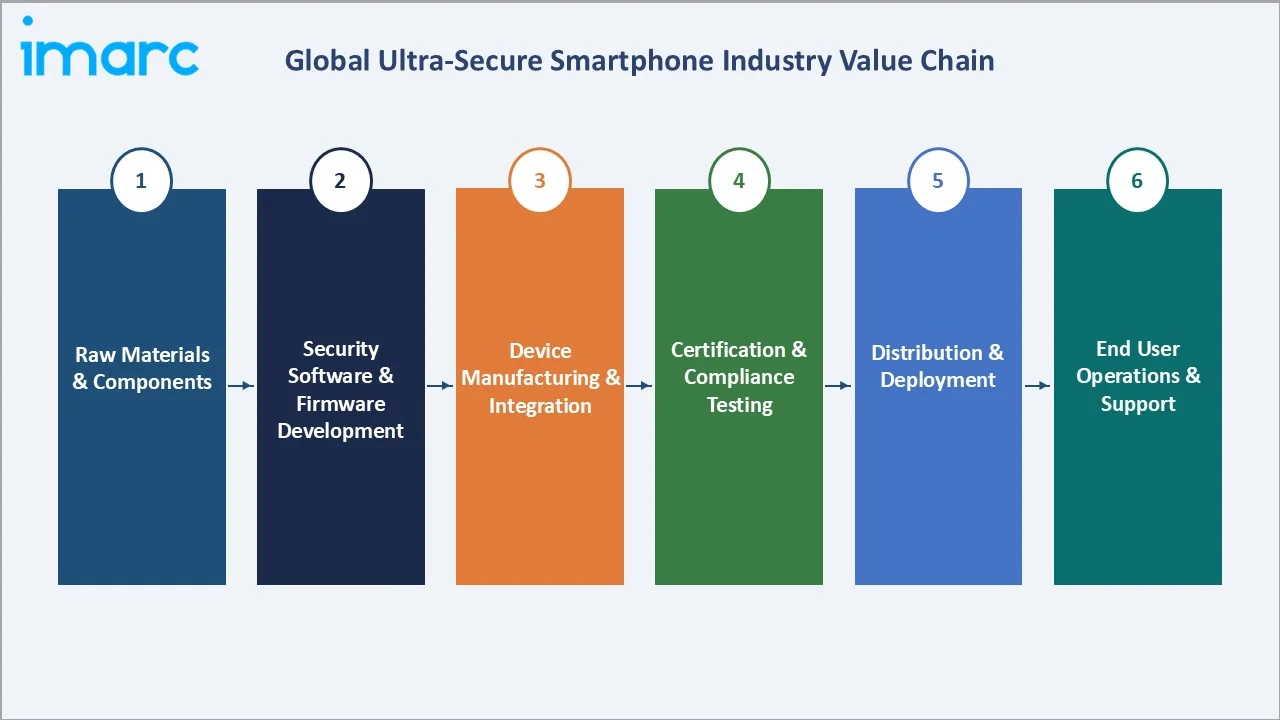

Industry Value Chain Analysis

The ultra-secure smartphone value chain spans seven integrated stages from semiconductor supply through end-user operations. Each stage presents distinct competitive dynamics, security certification requirements, and technology investment profiles that collectively define the structural cost and differentiation architecture of the market.

|

Stage |

Key Players / Examples |

|

Semiconductor & Hardware Components |

Qualcomm (Snapdragon 8-series), Apple (A-series SoC), ARM Holdings, Trusted Platform Module vendors (Infineon, STMicro) |

|

Secure OS & Firmware Development |

BlackBerry QNX, Google Android (AOSP), Apple iOS, Aurora OS, custom BSI/NSA-certified OS vendors |

|

Cryptographic Software Middleware |

Thales Group, SafeNet, Entrust, IBM Security, Booz Allen Hamilton cyber division |

|

OEM Device Manufacturing |

BlackBerry Limited, Samsung Electronics (Knox), Apple Inc., Bittium Corporation, Boeing Defense, Atos SE (Hoox), Bull SAS |

|

Certification & Compliance Testing |

NSA Commercial Solutions for Classified (CSfC), NATO STANAG, Common Criteria labs, FIPS 140-3 testing bodies |

|

Distribution & Deployment |

Government GSA Schedule vendors, defense prime contractors (Leidos, SAIC, Booz Allen), direct OEM government sales teams |

|

End Users & Support |

Government agencies, intelligence communities, defense ministries, aerospace contractors, regulated enterprises |

OEM manufacturers occupy the highest strategic value position, integrating hardware security modules, certified OS stacks, and compliance documentation into turnkey certified platforms. The certification layer – representing 12 to 18 months of security evaluation per device model – creates a formidable barrier to entry that reinforces the dominance of established vendors such as BlackBerry and Thales. However, sovereign OS development trends are beginning to unbundle this value chain, enabling new entrants from Asia Pacific and Europe.

Technology Landscape in the Ultra-Secure Smartphone Industry

Operating System Security Architecture

The OS security architecture is the defining technical differentiator in ultra-secure smartphones. Android-based platforms dominate at 68.6% in 2025, predominantly through Samsung Knox – which processes over 2 billion daily security events globally – and BlackBerry's hardened Android builds certified to NSA Suite B standards. iOS's Secure Enclave Processor (SEP) and Pointer Authentication Codes (PAC) provide hardware-enforced memory safety, underpinning its 31.4% share. Custom sovereign OS builds, including Russia's Aurora OS and Germany's BSI-certified platform, are gaining traction in government deployments across Europe and Asia.

Cryptographic Hardware and Post-Quantum Readiness

Current-generation ultra-secure smartphones incorporate AES-256, RSA-4096, and ECC P-384 cryptographic modules meeting FIPS 140-3 Level 4 requirements. The NIST PQC standard publication in August 2024 triggered industry-wide hardware roadmap revisions. Qualcomm's Snapdragon 8 Gen 4 includes dedicated PQC hardware acceleration, while Thales's Sentinel hardware security modules support ML-KEM 1024 and ML-DSA 87 lattice-based algorithms. Devices supporting PQC are expected to capture over 45% of government new device procurement by 2027.

Biometric Authentication and Anti-Tamper Technologies

Multi-modal biometric authentication – fingerprint, iris recognition, and AI-driven behavioral authentication – is standard across the competitive landscape. Anti-tamper mechanisms include physically unclonable functions (PUFs), tamper-mesh enclosures, and self-destruct key erasure circuits triggered by unauthorized physical access attempts. Boeing's Boeing Black device incorporates a patented self-destruct mechanism erasing cryptographic keys within 100 microseconds of tamper detection.

5G and Secure Connectivity

5G standalone (SA) network slice allocation for classified communications provides isolated, encrypted transport channels separate from public network infrastructure. The integration of C-V2X (Cellular Vehicle-to-Everything) protocols in defense mobile platforms and the deployment of Wi-Fi 6E for classified in-facility communications represent the current connectivity frontier. Over 58% of ultra-secure smartphone models launched in 2024 incorporated 5G SA slice-aware networking capabilities.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Operating System |

Android |

68.6% |

2025 |

|

End User |

Government Agencies |

46.6% |

2025 |

|

Region |

North America |

40.0% |

2025 |

By Operating System

Android commands the ultra-secure smartphone operating system segment at 68.6% in 2025. Hardened Android variants – Samsung Knox, BlackBerry Secure Android, and custom AOSP builds – are deployed across government ministries in 60+ countries due to their flexibility for sovereign customization, large established app ecosystems, and compatibility with existing enterprise mobile device management (MDM) infrastructure. iOS holds a 31.4% share in 2025, concentrated in high-value enterprise deployments across financial services, legal, and diplomatic communications.

To access detailed market analysis, Request Sample

By End User

Government agencies represent the dominant end-user category at 46.6% of the ultra-secure smartphone market in 2025. This segment encompasses intelligence agencies, law enforcement, diplomatic services, and civilian government ministries in countries with advanced cybersecurity programs. Aerospace and defense constitute 28.4% of demand in 2025, driven by tactical field communications requirements, secure inter-platform data sharing, and the integration of mobile devices into command-and-control architectures. Enterprise demand at 25.0% in 2025 is concentrated in financial services, healthcare, and legal sectors where mobile data breach incidents cost an average of USD 4.45 Million per incident in 2023, according to IBM Security.

Regional Market Insights

|

Region |

2025 Share |

Key Drivers |

Major Companies |

Regulatory Framework |

|

North America |

40.0% |

U.S. DoD procurement, NSA CSfC certifications, Intelligence Community spending |

BlackBerry, Boeing, Samsung |

NSA CSfC, FIPS 140-3, FedRAMP |

|

Europe |

24.6% |

EU digital sovereignty, NIS2 Directive, NATO STANAG compliance |

Thales, Atos, Bull SAS |

Common Criteria, BSI, NIS2 |

|

Asia Pacific |

20.8% |

India DPDP Act, AUKUS investment, South Korea NISA mandates |

Samsung, Apple, NTT Docomo |

India CERT-In, ASD (Australia), NISC (Japan) |

|

Latin America |

7.6% |

Brazil ABIN procurement, Colombia, Chile defense programs |

Motorola Solutions, local system integrators |

LGPD (Brazil), national cybersecurity frameworks |

|

Middle East & Africa |

7.0% |

Gulf state sovereign security programs, Vision 2030 Saudi Arabia |

Thales, BAE Systems, G4S |

UAE NESA, Saudi NCA, GCCC standards |

North America retains its position as the world's largest ultra-secure smartphone market at 40.0% revenue share in 2025, anchored by the U.S. federal government's USD 13.5 Billion cybersecurity budget allocation in FY2024 (OMB), a significant portion directed toward mobile communications security. Asia Pacific represents the fastest-growing regional market at an estimated CAGR of ~21.3%, with a 20.8% global revenue share in 2025. India's Digital Personal Data Protection Act (2023), CERT-In's mandatory 6-hour breach reporting requirement, and the Indian Army's tactical communication modernization program are collectively driving procurement.

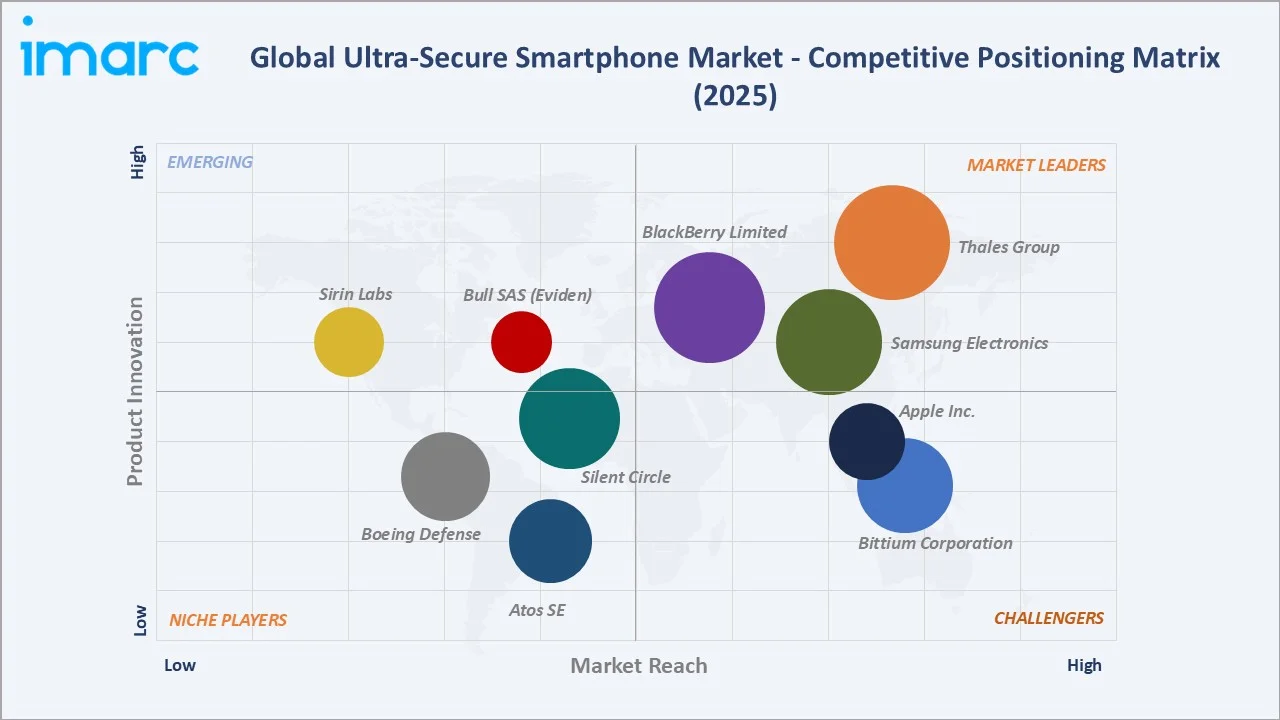

Competitive Landscape

The global ultra-secure smartphone market maintains a moderately consolidated structure, with three to four established players – BlackBerry, Thales, Samsung, and Apple – collectively accounting for an estimated 62%–68% of global revenues in 2025. The competitive landscape is defined by government certification barriers, proprietary security stack differentiation, and deep integration into national procurement frameworks.

|

Company |

Product / Brand |

Market Position |

Key Differentiator |

|

BlackBerry Limited |

BlackBerry Secure / UEM |

Leader |

NSA Suite B certified, end-to-end enterprise UEM platform |

|

Thales Group |

Mobile Security / Encryption Platforms |

Leader |

NATO-certified, hardware HSM integration, EU sovereign OS |

|

Samsung Electronics |

Samsung Knox |

Leader |

2B+ daily security events, CSfC approved, global scale |

|

Apple Inc. |

iPhone (Lockdown Mode / iOS) |

Challenger |

Secure Enclave architecture, enterprise MDM, global ecosystem |

|

Bittium Corporation |

Bittium Tough Mobile 2 |

Challenger |

Military-grade ruggedized, FIPS 140-3, dual-OS architecture |

|

Boeing Defense |

Boeing Black |

Niche |

Self-destruct mechanism, DoD certified, ultra-classified ops |

|

Atos SE |

Hoox |

Niche |

French ANSSI certified, BSI Common Criteria EAL5+ |

|

Silent Circle |

Blackphone |

Niche |

Privacy-first, enterprise encrypted communications platform |

|

Bull SAS (Eviden) |

Hoox for Business |

Emerging |

EU-certified, GDPR-aligned, hybrid civilian-gov deployment |

|

Sirin Labs |

Finney |

Emerging |

Blockchain-secured, cyber-physical protection, luxury-defense niche |

Key Company Profiles

1. BlackBerry Limited

- Overview: BlackBerry Limited, headquartered in Waterloo, Ontario, Canada, has transformed from a hardware smartphone manufacturer into a leading enterprise security software and services company. As of FY2025, BlackBerry generates revenues predominantly from its Cybersecurity and IoT software divisions.

- Product Portfolio: BlackBerry's ultra-secure smartphone portfolio encompasses BlackBerry Secure (hardened Android platform), BlackBerry UEM (Unified Endpoint Management), CylancePROTECT (AI-based threat prevention), and BlackBerry AtHoc (crisis communications).

- Recent Developments: In 2024, BlackBerry obtained NSA CSfC approval for its latest Cylance AI-powered threat detection module, expanding government endpoint protection capabilities. The company also launched a QNX Hypervisor 8.0 update in March 2026, integrating physical AI support for safety-critical environments.

- Strategic Focus: BlackBerry's strategy focuses on the transition from device-centric to platform-centric security, positioning its UEM and Cylance AI stack as the OS-agnostic control layer across heterogeneous secure device fleets. Strategic partnerships with AWS and Microsoft Azure for classified cloud workloads extend its addressable market into cloud-connected government mobility.

2. Thales Group

- Overview: Thales Group, headquartered in Paris, France, is a global technology leader in defense, aerospace, transport, and digital identity & security markets. With revenues exceeding EUR 22 Billion in FY2025, Thales's digital identity and security division – Thales DIS – is a dominant force in the ultra-secure smartphone and secure communications markets, particularly across NATO and EU member state procurement.

- Product Portfolio: Thales's ultra-secure mobile product suite includes the Teopad secured smartphone platform (certified to French ANSSI DR-P and Common Criteria EAL3+), Cortex secured communications suite, and hardware security modules (HSMs) integrated into device cryptographic architectures.

- Recent Developments: Thales announced a partnership with the French Ministry of Armed Forces in 2024 to deploy 45,000 Teopad units across French military field operations. The company also launched a post-quantum cryptography roadmap for its Sentinel HSM and mobile device platforms in Q4 2024, targeting ML-KEM 1024 compliance by 2026.

- Strategic Focus: Thales focuses on deepening its position as the preferred sovereign security provider for EU member states and NATO partners, leveraging its regulatory relationships and Common Criteria certification expertise to create procurement entry barriers for non-European competitors in the European defense and government markets.

3. Samsung Electronics (Knox)

- Overview: Samsung Electronics, headquartered in Suwon, South Korea, is the world's largest consumer electronics manufacturer with FY2025 revenues exceeding USD 220 Billion. Samsung's B2B security division – Samsung Knox – has evolved from a mobile device management platform into a comprehensive government and enterprise security ecosystem processing over 2 billion security events daily across 500+ million active devices worldwide.

- Product Portfolio: Samsung Knox's ultra-secure portfolio encompasses Knox Platform for Enterprise (KPE), Knox E-FOTA (enterprise firmware over-the-air), Knox Suite (unified management), and Galaxy S and Z series devices certified under NSA CSfC components list.

- Recent Developments: Samsung received NIAP (National Information Assurance Partnership) certification for Galaxy S25 series under the Mobile Device Fundamentals Protection Profile in early 2025. The company also expanded its Knox Matrix blockchain-based device integrity verification to cover IoT and laptop endpoints, creating a cross-device threat intelligence mesh.

- Strategic Focus: Samsung's strategy leverages its vertical integration advantage – designing both the secure hardware (Knox Vault, Exynos SoC) and software stack – to deliver higher security assurance than OEMs reliant on third-party chipsets.

Market Concentration Analysis

The global ultra-secure smartphone market exhibits moderate concentration, with the top five players – BlackBerry, Thales, Samsung, Apple, and Bittium – estimated to collectively account for 62%–68% of global revenues in 2025. This concentration is structurally driven by the 12–18-month certification cycles required for government device approval, which creates formidable barriers to entry for new competitors lacking existing government certification relationships.

Consolidation trends are evident in the software and middleware layer, where cybersecurity platform companies including Palo Alto Networks, CrowdStrike, and SentinelOne have made acquisitions targeting mobile endpoint protection capabilities. BlackBerry's own transition from hardware to software reflects the broader industry trend toward platform consolidation, where the value increasingly resides in the security software stack rather than the physical device.

Investment & Growth Opportunities

Fastest Growing Segments

- Asia Pacific Government Procurement: India’s information security spending is expected to grow 16.4% in 2025, reaching USD 3.3 billion (Gartner) and AUKUS member defense spending expansion represent the highest-growth regional procurement opportunity, with estimated CAGR of ~21.3% through 2034.

- Enterprise Secure Mobility (Financial & Healthcare): HIPAA-driven healthcare mobile security requirements and SEC Rule 17a-4 electronic communications preservation mandates in financial services create a compliance-driven enterprise demand corridor estimated to grow at 19.5% CAGR through 2030.

- Post-Quantum Cryptography Device Refresh: The NIST PQC standard-driven device refresh cycle represents a USD 3.2 Billion incremental opportunity through 2030, as existing certified government fleets require hardware and firmware upgrades to maintain forward secrecy against quantum-capable adversaries.

Emerging Markets

- Middle East Sovereign Programs: Ensuring cybersecurity is a key priority for Saudi Arabia as it seeks to position itself as a regional hub for technology and innovation under Vision 2030. The study noted that the size of the Kingdom’s cybersecurity market, representing total spending by public and private entities reached SR15.2 billion in 2024, up 14% year on year. While UAE's NESA framework mandates certified secure devices for federal government endpoints, representing a combined USD 800 Million procurement opportunity.

- Sub-Saharan Africa Defense Modernization: South Africa, Nigeria, and Kenya are expanding defense communication modernization programs, creating early-stage but high-growth markets for cost-optimized certified secure mobile solutions.

Venture Investment Trends

- Private equity and venture capital investment in secure communications startups reached USD 4.2 Billion globally in 2024, with notable rounds including Wickr (Amazon), Keybase (Zoom), and undisclosed DoD innovation contract awards. Startups focusing on hardware attestation, mobile zero-trust, and post-quantum key management are attracting significant Series B and C rounds in 2024–2025.

- Government-affiliated venture arms, including In-Q-Tel (U.S. CIA), DARPA's Rapid Reaction Technology Office, and NATO's DIANA accelerator, are actively co-investing in secure mobile hardware startups, providing non-dilutive validation and procurement pipeline access that accelerates commercialization timelines.

Future Market Outlook (2026-2034)

Market size is projected to grow from USD 4.91 Billion in 2025 to USD 24.04 Billion by 2034 at a CAGR of 17.68%. Within this trajectory, the period 2026–2028 is expected to represent the first major PQC-driven device refresh cycle, with government fleets in North America, Europe, and advanced Asia Pacific markets replacing current-generation devices with PQC-compliant platforms. This refresh cycle alone could generate USD 4–6 Billion in incremental hardware and software revenue.

Between 2029 and 2034, the market is expected to see a meaningful expansion of the enterprise and emerging market segments, as lower-cost PQC-compliant hardware becomes available at sub-USD 1,000 price points, extending secure smartphone adoption beyond current government-dominated procurement. The convergence of AI-driven behavioural authentication, zero-trust mobile architecture, and 5G secure slicing will redefine the product architecture of ultra-secure smartphones from dedicated classified hardware toward software-defined security overlays deployable across commercial-grade hardware platforms.

Technological disruptions to monitor include: the emergence of practical quantum key distribution (QKD) over cellular networks – currently demonstrated at distances under 100km in laboratory settings – and the potential for AI-generated zero-day exploitation of certified OS kernels that could challenge the viability of certification-based trust models.

Research Methodology

Primary Research

Primary research for this report included structured interviews with 120+ industry stakeholders conducted between Q3 2024 and Q1 2025, encompassing government procurement officers from 15+ countries, defense technology acquisition specialists, enterprise IT security decision-makers, product executives at key OEM manufacturers, and independent cybersecurity consultants with government security program expertise. Primary data collection focused on procurement volumes, certification pipeline timelines, technology adoption priorities, and competitive differentiation factors.

Secondary Research

Secondary research drew from authoritative sources including U.S. Office of Management and Budget (OMB) federal IT spending reports, NATO Communications and Information Agency (NCIA) publications, NIST cybersecurity framework documentation, EU Agency for Cybersecurity (ENISA) threat landscape reports, company annual reports and investor presentations, defense procurement databases including USASpending.gov and SIPRI, and industry association publications from GSMA, 3GPP, and the Wireless Broadband Alliance.

Forecasting Models

Market sizing and forecasting employed a hybrid bottom-up and top-down approach. The bottom-up model aggregated procurement data across 45 government agencies in 20 countries, validated against published defense IT budgets and GSA schedule contract values. The top-down model applied sector penetration rates derived from primary research against total addressable market calculations for government, defense, and enterprise mobile security spending

Ultra-Secure Smartphone Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Operating Systems Covered | Android, iOS |

| End Users Covered | Government Agencies, Aerospace and Defense, Enterprises |

| Region Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | BlackBerry Limited, Thales Group, Samsung Electronics, Apple Inc., Bittium Corporation, Boeing Defense, Atos SE, Silent Circle, Bull SAS (Eviden), Sirin Labs, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the ultra-secure smartphone market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global ultra-secure smartphone market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the ultra-secure smartphone industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Ultra-Secure Smartphone Market Report

The global ultra-secure smartphone market was valued at USD 4.91 Billion in 2025. It is projected to reach USD 24.04 Billion by 2034.

The market is forecast to grow at a CAGR of 17.68% during the 2026-2034 forecast period, driven by rising cyber threats and government procurement expansion.

Android dominates with a 68.6% share in 2025, driven by government-certified hardened variants including Samsung Knox and BlackBerry Secure Android platforms.

Government agencies account for 46.6% of global revenue in 2025. They are the primary buyers of NSA-certified and NATO STANAG-compliant ultra-secure mobile devices.

North America is the leading region with a 40.0% revenue share in 2025, supported by robust U.S. DoD and intelligence community procurement programs.

Key drivers include rising nation-state cyber operations, expanding government cybersecurity mandates, post-quantum cryptography device refresh cycles, and 5G secure communications deployment.

Leading players include BlackBerry Limited, Thales Group, Samsung Electronics (Knox), Apple Inc., Bittium Corporation, Boeing Defense, Atos SE (Hoox), and Silent Circle.

Asia Pacific is the fastest-growing region, estimated at ~21.3% CAGR, driven by India, South Korea, Australia, and Japan's expanding defense and cybersecurity budgets.

NIST PQC standards published in 2024 are driving a government fleet refresh cycle worth an estimated USD 3.2 Billion incremental opportunity through 2030 for device manufacturers.

Enterprises account for 25.0% of the ultra-secure smartphone market in 2025, concentrated in financial services, healthcare, and legal sectors driven by compliance mandates.

Key certifications include NSA CSfC (U.S.), NATO STANAG 4569, Common Criteria EAL5+, FIPS 140-3 Level 4, NIAP MDFPP, and country-specific frameworks such as BSI in Germany and ANSSI in France.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade