Ultrasound Devices Market Report by Product Type (Diagnostic Ultrasound Systems, Therapeutic Ultrasound Systems), Device Display Type (Color Ultrasound Devices, Black and White (B/W) Ultrasound Devices), Device Portability (Trolley/Cart-Based Ultrasound Devices, Compact/Handheld Ultrasound Devices), Application (Radiology/General Imaging, Obstetrics/Gynecology, Cardiology, Urology, Vascular, and Others), End Use (Hospitals, Imaging Centers, Research Centers), and Region 2026-2034

Global Ultrasound Devices Market:

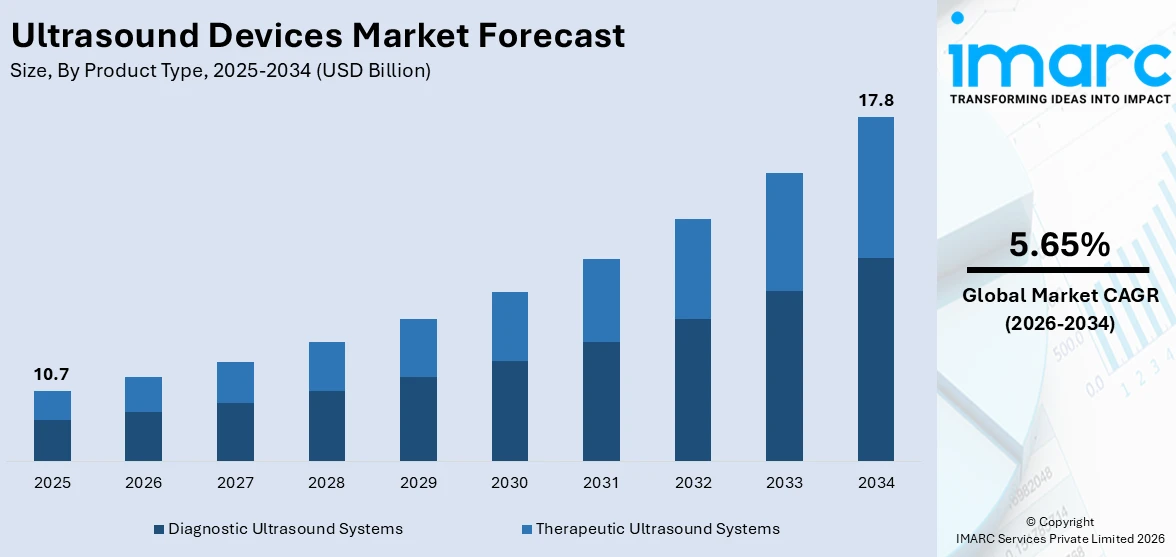

The global ultrasound devices market size reached USD 10.7 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 17.8 Billion by 2034, exhibiting a growth rate (CAGR) of 5.65% during 2026-2034. At present, North America accounted for the largest market share owing to advanced healthcare infrastructure and strong research and development (R&D) activities. The increasing demand for non-invasive medical procedures is enhancing the adoption of imaging technology, which is also stimulating the market growth.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 10.7 Billion |

| Market Forecast in 2034 | USD 17.8 Billion |

| Market Growth Rate (2026-2034) | 5.65% |

The market for ultrasound devices is witnessing dynamic growth as a result of technological advancements, growing clinical applications, and rising demand for non-invasive diagnostic tests. In addition to human healthcare, ultrasound technology is finding growing use in veterinary care and industrial uses. Portable ultrasound devices are being used in veterinary clinics for animal diagnostics, especially in companion animals and livestock. In industrial applications, ultrasound devices are finding use in material testing and quality control. These various applications are expanding the overall size of the market and bringing in additional revenue streams for makers. Healthcare systems are focusing on affordability and accessibility, and ultrasound equipment is well suited to these objectives. Makers are creating models that are low in cost yet effective for small clinics and community hospitals. Training courses are being enlarged to enhance operator competence, to facilitate broader use of the technology. This emphasis on affordability is driving wider take-up in developed economies and emerging markets.

To get more information on this market Request Sample

Ultrasound Devices Market Trends:

Artificial Intelligence (AI) Integration Improves Diagnostic Accuracy

Technological advancements are driving the ultrasound devices market. Companies are continually working on developing sophisticated features like 3D and 4D imaging, elastography, and Doppler technologies, which are improving diagnostic accuracy and clinical results. Artificial intelligence integration is revolutionizing ultrasound imaging by facilitating automated image interpretation, workflow enhancement, and decision support. AI-based algorithms are helping clinicians identify subtle abnormalities, normalize image quality, and decrease operator dependence. These technologies are making ultrasound more efficient, intuitive, and accessible, even among less experienced clinicians. Portable and handheld devices are also becoming increasingly popular thanks to miniaturization and wireless connectivity. The confluence of mobility and AI is broadening the applications of ultrasound beyond the conventional hospital environment into emergency medicine, primary care, and rural telemedicine consultations. For example, in April 2024, GE HealthCare launched two new ultrasound systems, Voluson Signature 20 and 18, incorporating AI and ergonomic design. These machines operate on core tools such as voice control, fetal anatomy recognition through AI, and pelvic floor and fibroid scans automated by AI.

Growing Demand for Portable Ultrasound Devices

The demand for portable and handheld ultrasound devices is growing since healthcare delivery is moving toward flexibility and accessibility. Clinicians are opting for miniaturized systems that can be utilized beyond conventional hospital imaging departments, such as ambulances, community health centers, and even home care facilities. Portable devices are becoming increasingly popular among emergency doctors, paramedics, and midwives, who are turning to them for quick assessments in emergency care situations. Advances in miniaturization and wireless technology are guaranteeing that portable ultrasound machines are providing image quality on par with larger cart-mounted systems. This portability is also facilitating the growth of telemedicine, where ultrasound scans are being remotely transmitted for expert analysis. The portability and cost-effectiveness of handheld ultrasound devices are making them desirable in developed as well as emerging economies. With the decentralization of healthcare, adoption of portable ultrasound devices is gaining momentum, thereby supporting the market growth. For example, in 2024, Butterfly Network debuted its third generation iQ3 digital ultrasound, providing improved portability, real-time smartphone imaging, and virtually twice the processing power of the earlier version.

Advances in Non-Invasive Medical Imaging

Improvements in the technology of ultrasound continue to increase non-invasive imaging The market for ultrasound devices is growing as healthcare systems are putting more emphasis on non-invasive and radiation-free diagnostic methods. Patients are moving towards safer alternatives to imaging technologies like computed tomography (CT) scans and X-rays that are subjecting patients to ionizing radiation. Ultrasound machines are providing a radiation-free solution by using high-frequency sound waves to produce real-time images. Doctors are trusting ultrasound for diagnosis in all fields of cardiology, obstetrics, gynaecology, urology, and emergency care. Preventive health programs are also promoting regular screenings through ultrasound for the early detection of chronic diseases, cancers, and foetal development abnormalities. As concern regarding radiation exposure hazards is on the increase, patients and doctors alike are opting for ultrasound as a primary imaging modality. This is ensuring sustained demand growth, as ultrasound imaging is balancing safety, cost-effectiveness, and clinical effectiveness, making it an accepted instrument in contemporary medical diagnostics. For example, in 2024, FUJIFILM India introduced the ALOKA ARIETTA 850 endoscopic ultrasound system, which is commissioned at Fortis Hospital, Bengaluru, India. This sophisticated system beats the competition in image quality and diagnostics, which boosts cancer detection, therapeutic practices, and non-invasive treatments for gastrointestinal ailments and transforms India's healthcare.

Ultrasound Devices Market Growth Drivers:

Increasing Utilization in Image-Guided Interventions and Surgical Procedures

Ultrasound devices are being increasingly utilized in image-guided interventions and minimally invasive (MI) surgical procedures. Surgeons and interventional radiologists are relying on ultrasound for real-time visualization, enabling precise needle placements, catheter insertions, and biopsies. Compared to CT or fluoroscopy, ultrasound is offering the advantage of radiation-free guidance, which is safer for both patients and healthcare professionals. The trend toward minimally invasive surgery is accelerating the need for ultrasound in operating rooms, where it is being used to guide tumor ablations, drainage procedures, and vascular interventions. Ultrasound guidance is reducing complications, shortening recovery times, and improving procedural outcomes. With ongoing advancements in probe technology and software integration, ultrasound is becoming a standard tool in many surgical disciplines. The increasing focus on precision medicine and patient safety is ensuring that ultrasound is gaining prominence in interventional care, further bolstering the growth and expanding its clinical relevance across specialties.

Growing Emphasis on Preventive Healthcare and Early Disease Detection

The global healthcare industry is increasingly emphasizing preventive care, and ultrasound devices are playing a central role in this shift. Governments, insurers, and providers are encouraging early disease detection to reduce long-term treatment costs and improve patient outcomes. Ultrasound imaging is being applied in preventive cardiology, liver disease screening, prenatal monitoring, and cancer detection programs. Regular screening using ultrasound is enabling physicians to identify conditions such as tumors, vascular abnormalities, or fetal complications at earlier stages, when interventions are more effective. Since ultrasound is safe, repeatable, and cost-efficient, it is being integrated into large-scale health campaigns and community health programs. Preventive healthcare systems are relying on ultrasound as a frontline tool for population health management, driving sustained market demand. This focus on early diagnosis is ensuring continuous growth, as ultrasound technology is aligning perfectly with the rising global emphasis on proactive, preventive, and value-based healthcare models.

Expanding Adoption in Point-of-Care (POC) and Emerging Healthcare Markets

The adoption of ultrasound devices is expanding significantly due to the increasing role of point-of-care ultrasound (POCUS) and the growing focus on healthcare access in emerging markets. Clinicians in emergency rooms, ICUs, and rural clinics are using portable ultrasound systems to deliver quick, bedside diagnostics that are supporting immediate decision-making. POCUS is reducing patient transfers and lowering costs by providing real-time imaging in diverse care settings. At the same time, emerging economies in Asia-Pacific, Latin America, and Africa are increasing healthcare investments, with ultrasound technology being chosen for its affordability, versatility, and ease of use. Governments and NGOs are supporting the deployment of portable ultrasound systems in community health programs, maternal care initiatives, and infectious disease monitoring. This combination of POCUS growth and adoption in underserved regions is ensuring that ultrasound devices are becoming more accessible globally, expanding their market presence and supporting equitable healthcare delivery.

Global Ultrasound Devices Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with the ultrasound devices market forecast at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on product type, device display type, device portability, application, and end use.

Breakup by Product Type:

- Diagnostic Ultrasound Systems

- 2D Imaging Systems

- 3D and 4D Imaging Systems

- Doppler Imaging

- Therapeutic Ultrasound Systems

- High-Intensity Focused Ultrasound (HIFU)

- Extracorporeal Shockwave Lithotripsy (ESWL)

Diagnostic ultrasound systems currently hold the largest ultrasound devices market demand

The report has provided a detailed breakup and analysis of the market based on the product type. This includes diagnostic ultrasound systems (2D imaging systems, 3D and 4D imaging systems, and doppler imaging) and therapeutic ultrasound systems High-Intensity Focused Ultrasound (HIFU) and extracorporeal shockwave lithotripsy (ESWL)). According to the report, diagnostic ultrasound systems represented the largest market segmentation.

Diagnostic ultrasound systems, particularly handheld and portable devices, are advancing rapidly. For instance, Philips recently launched the Lumify portable ultrasound system, enhancing accessibility and ease for healthcare professionals in various settings.

Breakup by Device Display Type:

- Color Ultrasound Devices

- Black and White (B/W) Ultrasound Devices

Color ultrasound devices currently hold the largest ultrasound devices market statistics

The report has provided a detailed breakup and analysis of the market based on the device display type. This includes color ultrasound devices and black and white (b/w) ultrasound devices. According to the report, color ultrasound devices represented the largest market segmentation.

Color ultrasound devices, a type of ultrasound with advanced display, provide detailed imaging using doppler technology. For example, Canon launched the Aplio i-series, offering enhanced diagnostic capabilities through superior color flow visualization in medical applications.

Breakup by Device Portability:

- Trolley/Cart-Based Ultrasound Devices

- Compact/Handheld Ultrasound Devices

Trolley/cart-based ultrasound devices currently hold the largest ultrasound devices market value

The report has provided a detailed breakup and analysis of the market based on the device portability. This includes trolley/cart-based ultrasound devices and compact/handheld ultrasound devices. According to the report, trolley/cart-based ultrasound devices represented the largest market segmentation.

Trolley/cart-based ultrasound devices provide enhanced imaging capabilities while ensuring mobility within medical settings. For example, GE Healthcare's Voluson SWIFT is offering advanced imaging and portability, thereby making it suitable for various clinical environments requiring high performance.

Breakup by Application:

Access the comprehensive market breakdown Request Sample

- Radiology/General Imaging

- Obstetrics/Gynecology

- Cardiology

- Urology

- Vascular

- Others

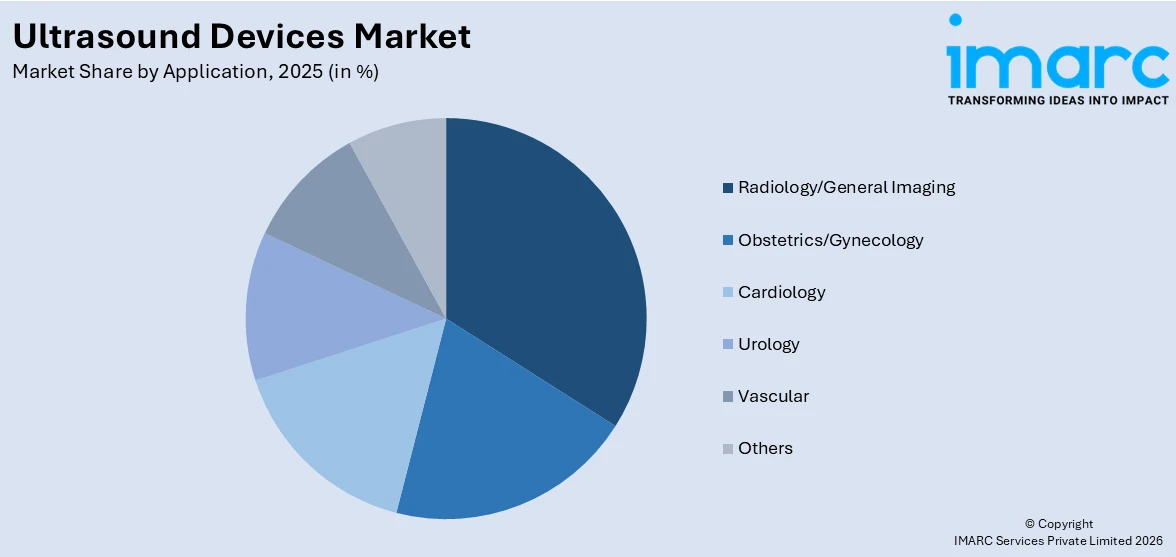

Radiology/general imaging currently holds the largest ultrasound devices market revenue

The report has provided a detailed breakup and analysis of the market based on the application. This includes radiology/general imaging, obstetrics/gynecology, cardiology, urology, vascular, and others. According to the report, radiology/general imaging represented the largest market segmentation.

Ultrasound devices in radiology provide non-invasive imaging for diagnostic purposes, including organ and soft tissue assessments. For instance, GE Healthcare's Vscan Air offers handheld, wireless ultrasound for point-of-care applications, thereby enhancing mobility and diagnostic efficiency.

Breakup by End Use:

- Hospitals

- Imaging Centers

- Research Centers

Hospitals currently holds the largest ultrasound devices market outlook

The report has provided a detailed breakup and analysis of the market based on the end use. This includes hospitals, imaging centers, and research centers. According to the report, hospitals represented the largest market segmentation.

Hospitals are major users of ultrasound devices, utilizing them for diagnostic imaging and patient monitoring. For example, GE Healthcare recently launched its LOGIQ E10 system, which is enhancing hospitals' capabilities in real-time imaging and patient care.

Breakup by Region:

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America currently dominates the market

The market research report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada), Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others), Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others), Latin America (Brazil, Mexico and others), and the Middle East and Africa. According to the report, North America accounted for the largest market share.

According to the ultrasound devices market overview, North America exhibits clear dominance in the market due to advanced healthcare infrastructure and strong R&D activities. For instance, GE Healthcare launched its Voluson SWIFT, a high-performance ultrasound system focused on women’s health. Such innovations, coupled with increased demand for imaging solutions, continue to bolster the region’s leadership in the market. Furthermore, the high adoption of innovative technologies, and a strong presence of key industry players, driving consistent market growth in the region.

Competitive Landscape:

The ultrasound devices market research report has provided a comprehensive analysis of the competitive landscape. Detailed profiles of all major market companies have also been provided. Some of the key players in the market include:

- Canon Medical Systems Corporation

- CHISON Medical Technologies Co. Ltd.

- Esaote SpA

- Fujifilm India Private Limited

- GE HealthCare

- Konica Minolta Inc.

- Koninklijke Philips N.V.

- Samsung Healthcare

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd

- Siemens Healthineers

(Please note that this is only a partial list of the key players, and the complete list is provided in the report.)

Ultrasound Devices Market Recent Developments:

- August 2025: Sonio has introduced a new range of ultrasound equipment for maternal health in the U.S. The new devices are named Sonio Start, Sonio Plus, Sonio Premium, and Sonio Enterprise. The company stated that each was created to "seamlessly incorporate with current technology frameworks while enhancing diagnostic and operational results." It anticipates that the new devices will tackle "persistent problems with the current technology … such as inefficient workflows, gaps in quality, incomplete scans, and risks of liability."

- August 2025: Philips is putting $150 million into growing two US facilities that produce its AI-driven ultrasound systems and software. Enhancing its current annual $900m R&D investment in the US, the medtech leader stated that the fund distribution for expanding its Pennsylvania plant, which manufactures ultrasound systems, would aid its continuous growth in the US.

- August 2025: Having been launched internationally, these advanced systems are now accessible in the United States, highlighting a significant milestone in Esaote’s goal to provide innovative diagnostic solutions globally. Engineered for flexibility and mobility, the MyLab™ A50 and A70 systems are small, lightweight, and can operate on battery power, enabling healthcare professionals to deliver advanced ultrasound features in diverse care environments. From hospital units to outpatient facilities and point-of-care settings, the systems are designed to adjust to changing mobility requirements.

- June 2025: Flosonics Medical, a pioneer in wearable ultrasound for critical care, today revealed that The Mount Sinai Hospital has implemented FloPatch, the first wireless Doppler ultrasound device, in its intensive care units for surgery and transplants. This milestone signifies the company's inaugural East Coast deployment, broadening its U.S. presence and strengthening the increasing need for real-time, customized fluid management in ICUs.

- March 2025: Wipro GE Healthcare has unveiled the Versana Premier R3, a sophisticated AI-powered ultrasound system aimed at boosting clinical efficiency and precision, optimizing workflows, and enhancing patient outcomes. This cutting-edge ultrasound system is an enhanced model of the Versana ultrasound series, featuring AI-driven productivity tools to refine workflow and clinical characteristics focused on improving efficiency and accuracy.

- September 2024: Samsung Medison unveiled the HERA Z20, a premium OB/GYN ultrasound system, at the ISUOG World Congress, which features advanced AI-assisted diagnostics, enhanced image quality, and eco-friendly design.

- September 2024: Exo launched SweepAI, an FDA-cleared AI-powered cardiac and lung scanning application for its Iris handheld ultrasound system. It provides real-time diagnostic feedback without internet reliance, improving accuracy and ease in detecting heart failure, stroke volume, and left ventricular hypertrophy.

- February 2024: FUJIFILM India launched the ALOKA ARIETTA 850 endoscopic ultrasound devices, installed at Fortis Hospital, Bengaluru, which offers image quality and diagnostics, enhancing cancer detection, therapeutic procedures, and non-invasive treatments for gastrointestinal conditions.

Ultrasound Devices Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered |

|

| Device Display Types Covered | Color Ultrasound Devices, Black and White (B/W) Ultrasound Devices |

| Device Portabilities Covered | Trolley/Cart-Based Ultrasound Devices, Compact/Handheld Ultrasound Devices |

| Applications Covered | Radiology/General Imaging, Obstetrics/Gynecology, Cardiology, Urology, Vascular, Others |

| End Uses Covered | Hospitals, Imaging Centers, Research Centers |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Canon Medical Systems Corporation, CHISON Medical Technologies Co. Ltd., Esaote SpA, Fujifilm India Private Limited, GE HealthCare, Konica Minolta Inc., Koninklijke Philips N.V., Samsung Healthcare, Shenzhen Mindray Bio-Medical Electronics Co., Ltd, Siemens Healthineers, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the ultrasound devices market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global ultrasound devices market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the ultrasound devices industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Ultrasound Devices Market Report

The global ultrasound devices market was valued at USD 10.7 Billion in 2025.

We expect the global ultrasound devices market to exhibit a CAGR of 5.65% during 2026-2034.

The sudden outbreak of the COVID-19 pandemic had led to the postponement of numerous elective treatments and diagnostic imaging of kidneys, liver, ovaries, etc., related ailments for reducing the risk of the coronavirus infection upon hospital visits, thereby negatively impacting the global market for ultrasound devices.

The rising integration of Al in ultrasound devices to automate time-consuming processes, such as quantification and selecting the best image slice from a 3D dataset, is primarily driving the global ultrasound devices market.

Based on the product type, the global ultrasound devices market can be segmented into diagnostic ultrasound systems and therapeutic ultrasound systems. Currently, diagnostic ultrasound systems hold the majority of the total market share.

Based on the device display type, the global ultrasound devices market has been divided into color ultrasound devices and Black and White (B/W) ultrasound devices, where color ultrasound devices currently exhibit a clear dominance in the market.

Based on the device portability, the global ultrasound devices market can be categorized into trolley/cart-based ultrasound devices and compact/handheld ultrasound devices. Currently, trolley/cart-based ultrasound devices account for the majority of the global market share.

Based on the application, the global ultrasound devices market has been segregated into radiology/general imaging, obstetrics/gynecology, cardiology, urology, vascular, and others. Among these, radiology/general imaging currently holds the largest market share.

Based on the end use, the global ultrasound devices market can be bifurcated into hospitals, imaging centers, and research centers. Currently, hospitals exhibit a clear dominance in the market.

On a regional level, the market has been classified into North America, Asia-Pacific, Europe, Latin America, and Middle East and Africa, where North America currently dominates the global market.

Some of the major players in the global ultrasound devices market include Canon Medical Systems Corporation, CHISON Medical Technologies Co. Ltd., Esaote SpA, Fujifilm India Private Limited, GE HealthCare, Konica Minolta Inc., Koninklijke Philips N.V., Samsung Healthcare, Shenzhen Mindray Bio-Medical Electronics Co., Ltd, and Siemens Healthineers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)