Under Desk Treadmill Market Size, Share, Trends and Forecast by Product Type, Technology, End User, Distribution Channel, and Region, 2026-2034

Global Under Desk Treadmill Market Size, Share, Trends & Forecast (2026-2034)

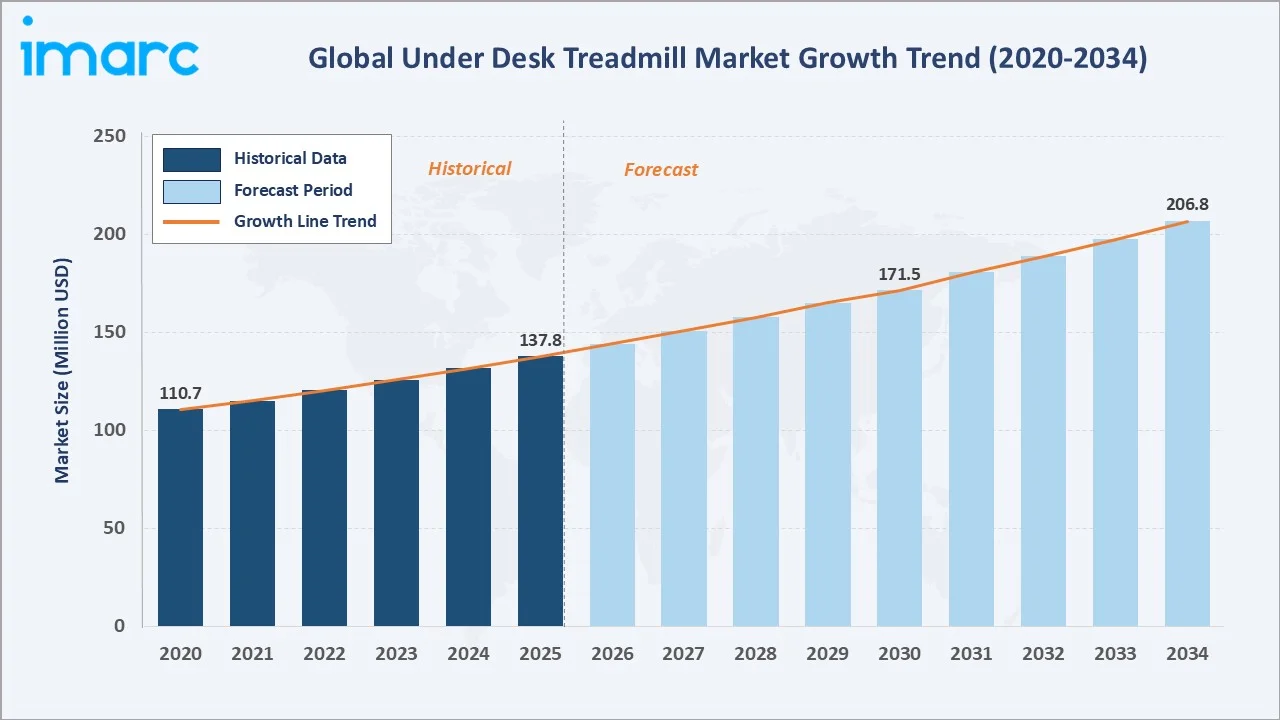

The global under desk treadmill market size reached USD 137.8 Million in 2025 and is projected to reach USD 206.8 Million by 2034, exhibiting a CAGR of 4.47% during 2026-2034. Rising health consciousness, widespread adoption of hybrid work models, and growing corporate wellness programmes are the primary forces driving market growth.

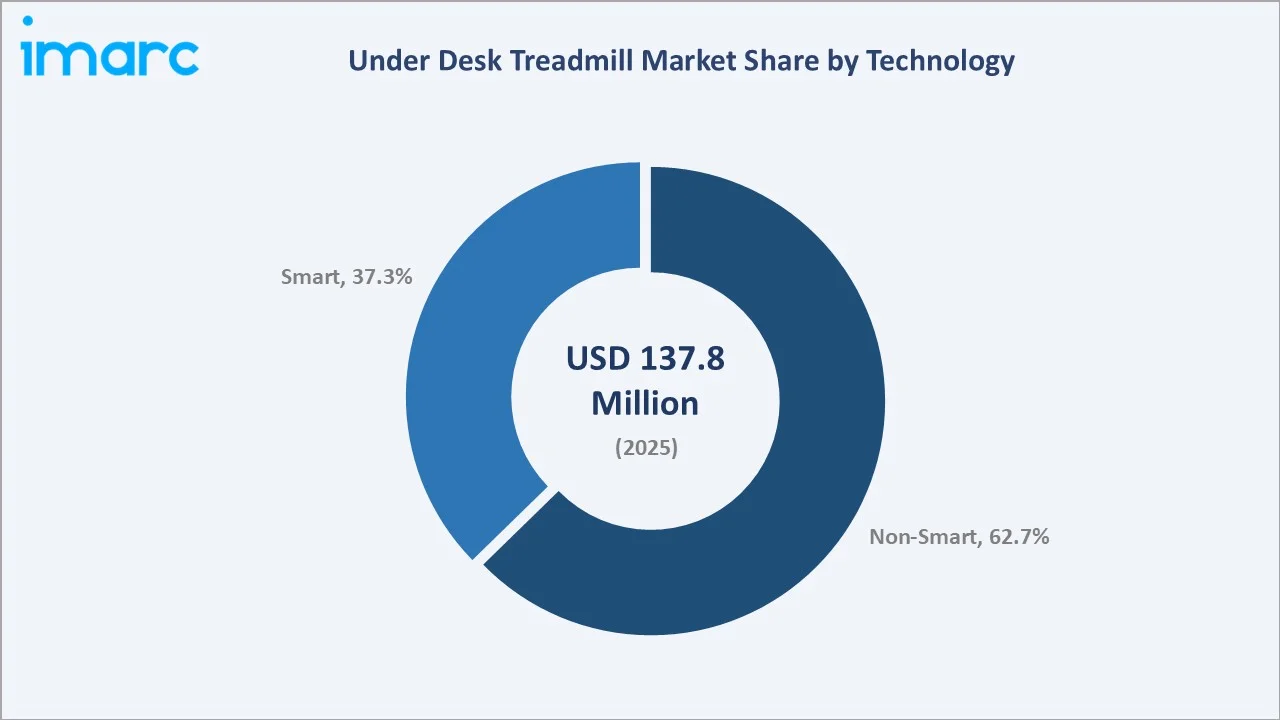

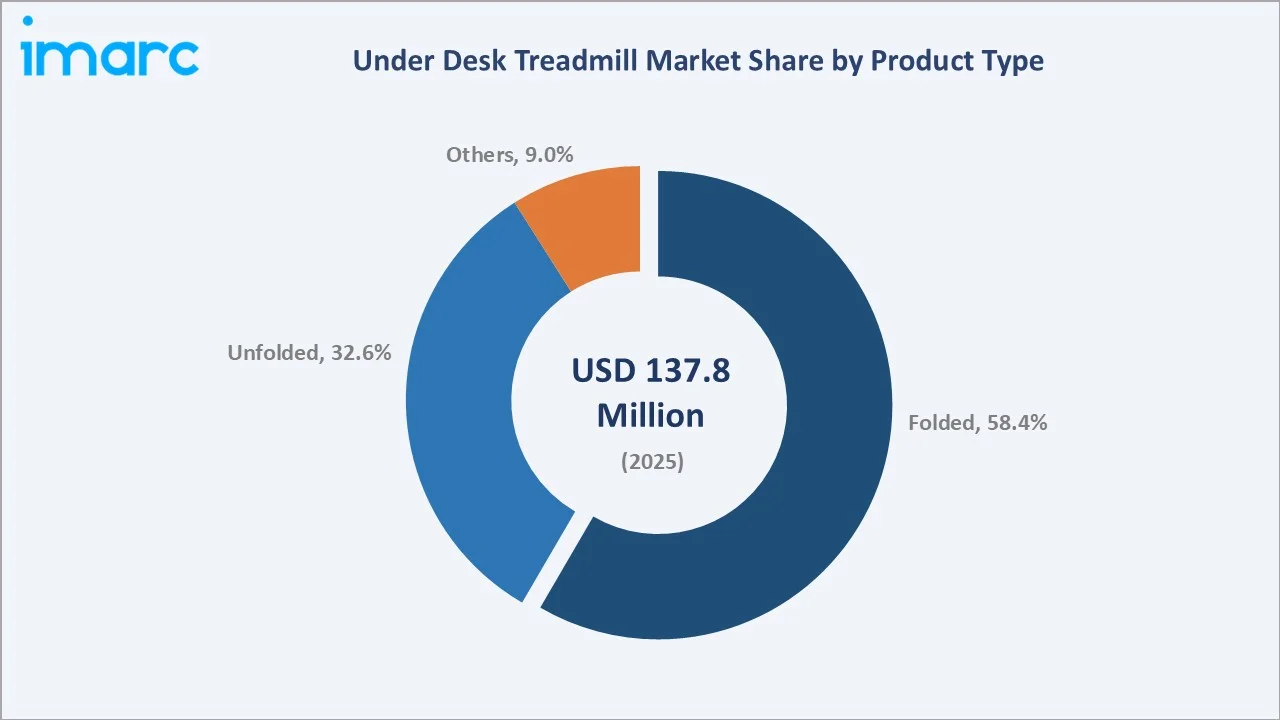

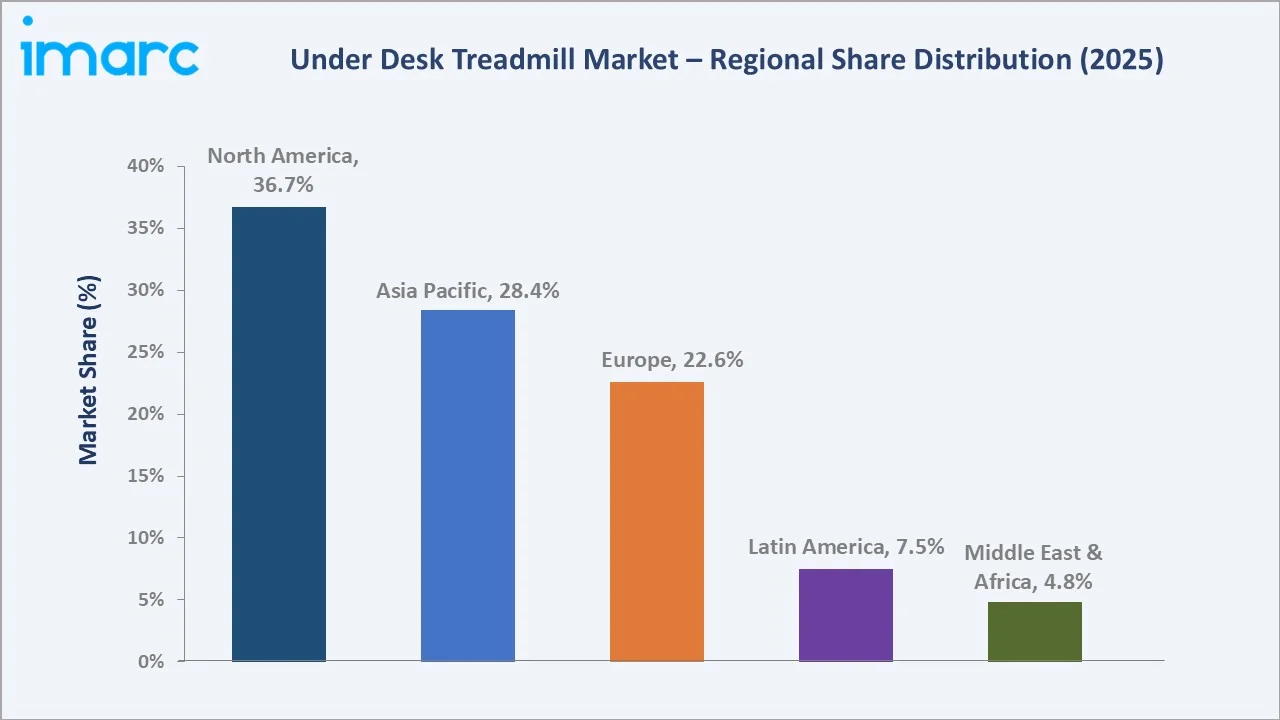

Non-smart treadmills lead technology at 62.7% in 2025, while folded product type dominates at 58.4%. North America commands the largest regional share at 36.7% in 2025, reflecting high consumer disposable income and strong workplace wellness culture.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 137.8 Million |

|

Forecast Market Size (2034) |

USD 206.8 Million |

|

CAGR (2026-2034) |

4.47% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (36.7% share, 2025) |

| Second Largest Region |

Asia Pacific (28.4% share, 2025) |

| Leading Technology |

Non-Smart (62.7%, 2025) |

| Leading Product Type |

Folded (58.4%, 2025) |

The global under desk treadmill market growth trajectory from 2020 through 2034, with historical expansion to USD 137.8 Million in 2025, reflects consistent wellness-driven demand, while the forecast to USD 206.8 Million captures accelerating hybrid work adoption, fitness technology innovation, and expanding corporate wellness programme investments.

To get more information on this market, Request Sample

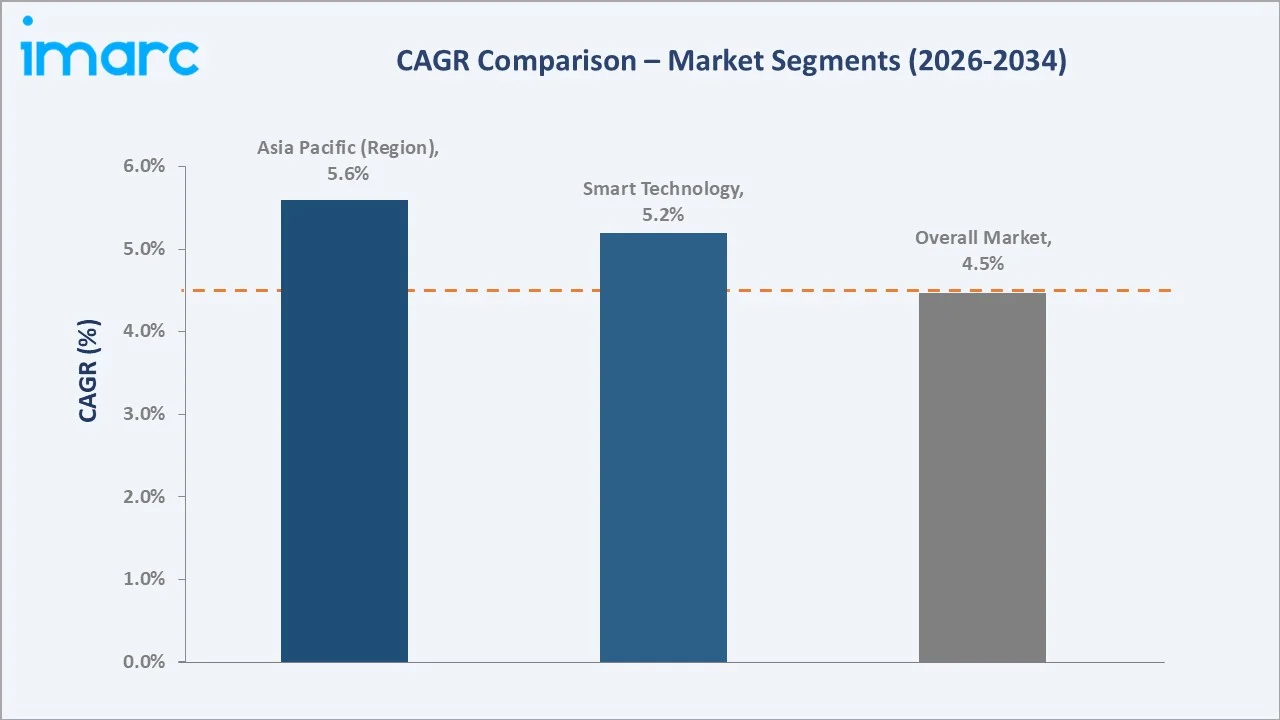

The CAGR trajectories across key technology, product type, and regional sub-segments, with Asia Pacific at ~5.6% CAGR and Smart technology at ~5.2% CAGR, represent the fastest-growing categories within the global under desk treadmill industry through 2034.

Executive Summary

The global under desk treadmill market is on a sustained growth trajectory from USD 137.8 Million in 2025 to USD 206.8 Million by 2034. Under desk treadmills, compact walking devices enabling physical activity during seated or standing work, benefit from non-discretionary wellness spending and growing employer health mandates.

Non-smart treadmills dominate the technology mix at 62.7% in 2025, owing to cost advantages and straightforward operation, while Smart treadmills (37.3%) command premium pricing through app connectivity and personalised workout programming, growing at the fastest technology CAGR of ~5.2% through 2034.

Folded product type leads at 58.4% in 2025, reflecting consumer preference for space-saving designs suited to home offices and compact commercial spaces.

North America commands 36.7% in 2025, driven by high health consciousness, remote work penetration, and HSA/FSA reimbursement eligibility that lowers effective product cost.

Key Market Insights

|

Insight |

Data |

|

Leading Technology |

Non-Smart – 62.7% share (2025) |

|

Fastest Growing Technology |

Smart – ~5.2% CAGR (2026-2034) |

|

Leading Product Type |

Folded – 58.4% share (2025) |

|

Leading Region |

North America – 36.7% share (2025) |

|

Fastest Growing Region |

Asia Pacific – ~5.6% CAGR (2026-2034) |

|

Top Companies |

KingSmith, LifeSpanFitness, Sunny Health & Fitness, HK SMARTMV LIMITED, Egofit, InMovement |

Key Analytical Observations Supporting the Above Data:

- Non-smart treadmills, with 62.7% in 2025, dominate owing to their cost-effective positioning, straightforward operation, and broad accessibility. For budget-conscious residential buyers and cost-sensitive commercial deployments, non-smart models deliver sufficient walking functionality without subscription requirements or digital infrastructure needs.

- Folded product type, with 58.4% in 2025, leads because space efficiency is the single most critical purchase criterion in the under desk treadmill market. Folding mechanisms enabling storage to sub-15cm heights make these units viable in apartments, home offices, and hot-desking environments where dedicated fitness space is unavailable.

- North America's 36.7% dominance in 2025 reflects a structurally favourable market environment combining high per-capita health and wellness expenditure, widespread adoption of standing desk ecosystems, and corporate wellness benefit programmes covering treadmill purchases.

- Asia Pacific's 28.4% share and ~5.6% CAGR reflect rapidly expanding urban middle-class health awareness, rising disposable income, and strong domestic manufacturing capabilities that support aggressive pricing strategies expanding the addressable market.

Global Under Desk Treadmill Market Overview

An under desk treadmill is a compact motorised walking device engineered for low-speed operation (0.5–4.0 km/h) enabling physical activity integration during seated or standing desk-based work. Core product attributes include ultra-low deck height, whisper-quiet motor operation, foldable form factor, and wireless remote or app-based speed control.

The global ecosystem integrates motor and belt component suppliers, OEM/ODM manufacturing facilities primarily in China, technology integration providers for smart connectivity, brand owners and distributors, and diverse end-use segments spanning residential home offices, corporate workplaces, co-working spaces, healthcare facilities, and educational institutions.

Market Dynamics

To evaluate market opportunities, Request Sample

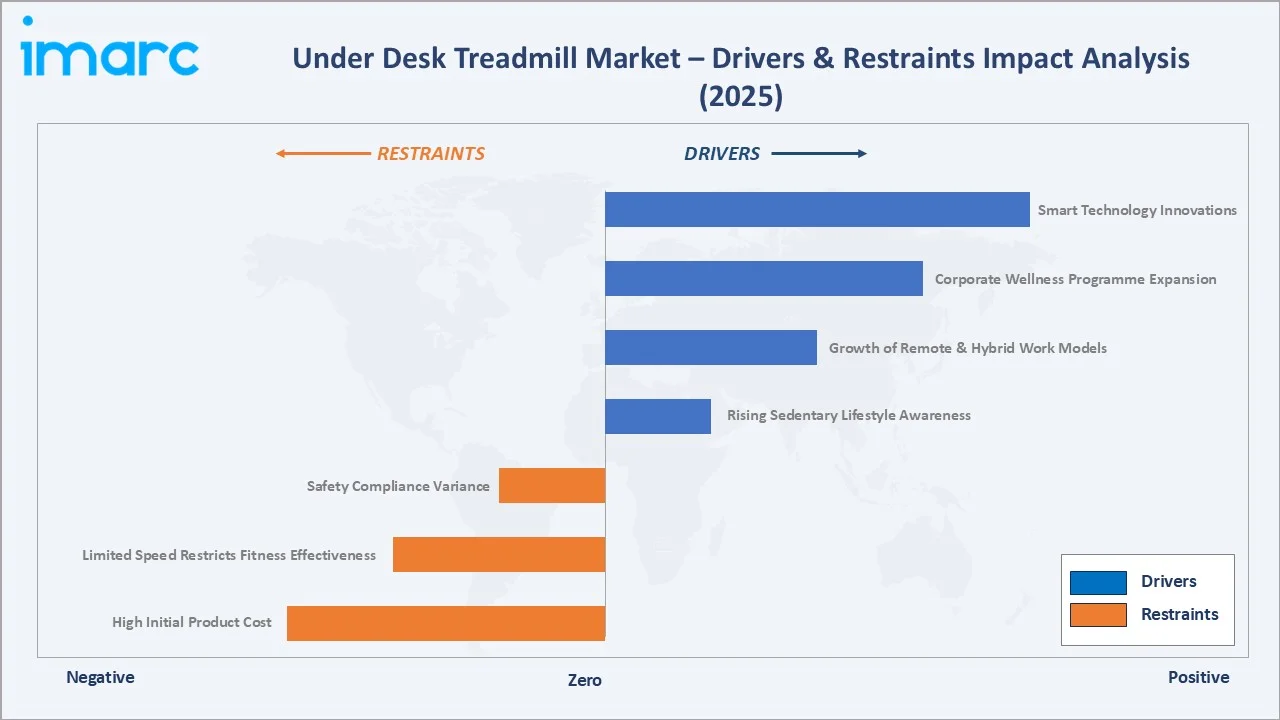

Market Drivers

- Rising Sedentary Lifestyle Awareness: The WHO estimates physical inactivity is the fourth leading risk factor for global mortality, causing approximately 3.2 million deaths annually. Growing consumer awareness of risks associated with prolonged sitting is the primary catalyst driving demand for integrated workplace fitness solutions.

- Growth of Remote and Hybrid Work Models: Post-pandemic hybrid work adoption has created a structural shift in home office equipment investment. Approximately 28% of employees worldwide worked remotely in 2023, consumers are equipping home workspaces with ergonomic and wellness-enabling devices, creating sustained demand for under desk walking solutions.

- Corporate Wellness Programme Expansion: Organizations are steadily increasing investments in employee wellness initiatives, creating broader opportunities for fitness-related products within workplace benefit structures. This trend is encouraging the inclusion of equipment subsidies and reimbursement models, which in turn improve accessibility and support bulk purchasing through corporate partnerships.

Market Restraints

- High Initial Product Cost: Quality under desk treadmills with durable motors and smart features are priced between USD 300–900, representing a significant upfront investment relative to alternative passive ergonomic solutions. Price sensitivity among value-focused buyers constrains addressable market penetration in developing economies.

- Limited Speed Restricts Fitness Effectiveness: Under desk treadmills operate at maximum speeds of 3–4 km/h, insufficient for cardiovascular training benefits. This limitation positions them as supplemental activity tools rather than primary fitness equipment, limiting purchase justification for fitness-motivated buyers with existing gym memberships.

Market Opportunities

- Standing Desk Ecosystem Integration: The expanding demand for ergonomic office setups is driving steady growth in the broader workspace solutions market. Manufacturers that ensure compatibility and integration with complementary office equipment can unlock bundled sales opportunities through specialized retailers and corporate procurement channels, strengthening their positioning in workplace wellness ecosystems.

- Healthcare and Rehabilitation Applications: Growing physician recommendation of low-impact walking for metabolic disease management, post-surgical rehabilitation, and elderly mobility maintenance is creating a clinical application segment for medically certified under desk treadmills with precise speed control and applicable safety certifications.

Market Challenges

- Safety and Liability Standards Variance: Divergent safety certification requirements across markets, UL in North America, CE marking in Europe, and PSE in Japan, create compliance complexity and cost for manufacturers targeting multi-regional distribution, particularly for smaller brands without regulatory affairs expertise.

- Motor Noise and Vibration in Office Settings: Despite technological improvements, under desk treadmills generating noise levels above 50dB create disturbance in open-plan office environments and during video conference calls, limiting adoption in professional settings and generating negative reviews that affect brand perception.

Emerging Market Trends

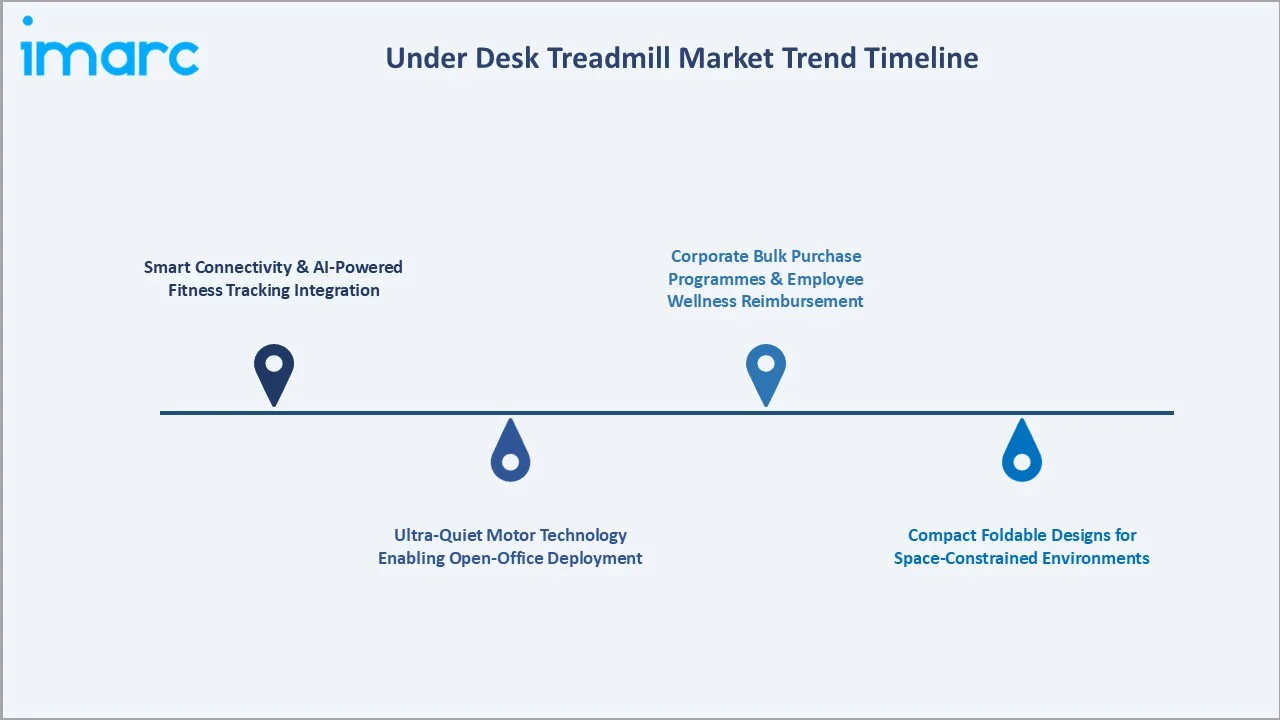

1. Smart Connectivity and AI-Powered Fitness Tracking Integration

Integration with Apple Health, Google Fit, Fitbit, and proprietary wellness platforms is transitioning under desk treadmills from passive equipment to active health data nodes. AI-powered coaching features providing gait analysis, posture alerts, and personalised activity goals are differentiating premium smart models commanding 25–35% price premiums over non-smart equivalents.

2. Ultra-Quiet Motor Technology Enabling Open-Office Deployment

Next-generation brushless DC motor architectures combined with advanced shock-absorption belt systems are achieving sub-40dB operational noise levels. This technical breakthrough is unlocking corporate bulk procurement opportunities in open-plan offices where noise-sensitive environments previously excluded treadmill deployment, fundamentally expanding the addressable B2B market.

3. Compact Foldable Designs for Space-Constrained Environments

Demand for under desk treadmills that fold to under 10cm storage height and weigh less than 25kg is driving design innovation. Models enabling fold-flat or upright storage are setting new benchmarks for space efficiency that expand addressable residential markets, particularly in dense urban apartment environments across North America and Asia Pacific.

4. Corporate Bulk Purchase Programmes and Employee Wellness Reimbursement

Fortune 1000 companies are establishing direct corporate purchasing agreements with treadmill manufacturers, driven by rising health insurance cost containment strategies. HSA and FSA reimbursement eligibility in the United States, covering fitness equipment when prescribed for medical conditions, is expanding institutional procurement volumes and shifting the purchasing decision from individual to employer.

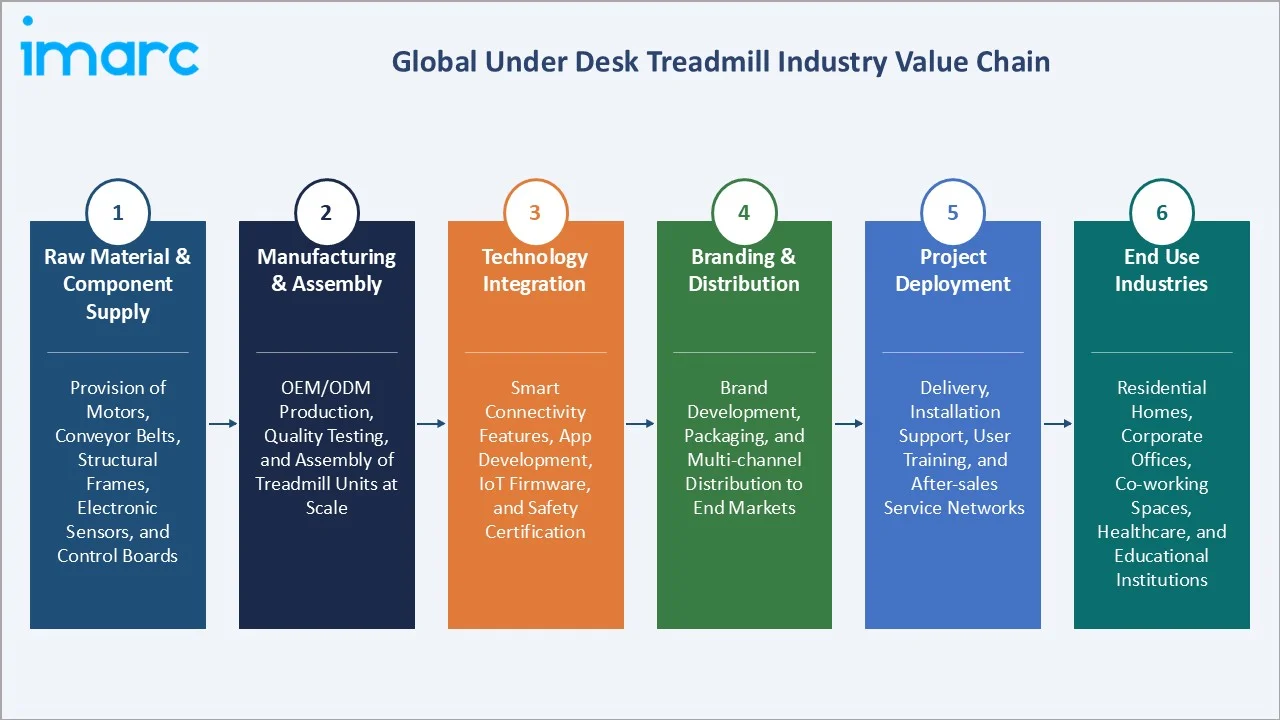

Industry Value Chain Analysis

The under desk treadmill value chain spans six stages from component supply through end-user deployment. Motor and belt manufacturing captures the highest technical complexity, while brand differentiation and digital platform integration generate premium margin capture in consumer-facing stages.

|

Stage |

Description |

| Raw Material & Component Supply |

Provision of motors, conveyor belts, structural frames, electronic sensors, and control boards |

| Manufacturing & Assembly |

OEM/ODM production, quality testing, and assembly of treadmill units at scale |

| Technology Integration |

Smart connectivity features, app development, IoT firmware, and safety certification |

| Branding & Distribution |

Brand development, packaging, and multi-channel distribution to end markets |

| Project Deployment |

Delivery, installation support, user training, and after-sales service networks |

| End Use Industries |

Residential homes, corporate offices, co-working spaces, healthcare, and educational institutions |

Integrated manufacturers with captive component sourcing and in-house smart platform development achieve lower cost bases than assemblers reliant on spot-market procurement. This vertical integration is a meaningful competitive advantage in value-sensitive market segments where price competition is intense and brand loyalty is still developing.

Technology Landscape in the Under Desk Treadmill Industry

Motor Technology: Brushless DC to Hub-Drive Systems

Brushless DC motors (BLDC) are the dominant drivetrain technology, offering higher efficiency, lower noise, and greater longevity compared to brushed alternatives. Hub-drive motor architectures, integrating the motor directly into the belt roller, reduce overall unit thickness — a critical dimension constraint for sub-desk clearance requirements of under 20cm.

Belt and Deck Innovation: Multi-Layer Shock Absorption

Multi-layer belt systems combining PVC outer surfaces with EVA foam mid-layers and rigid base plates are achieving sub-40dB operational noise while extending belt service life beyond 5,000 operating hours. Low-friction silicone lubrication systems reducing deck-belt friction at walking speeds are progressively replacing manual lubrication requirements, reducing maintenance burden.

Smart Connectivity: IoT Integration and App Ecosystems

Bluetooth 5.0 and ANT+ protocol integration enables real-time synchronisation with iOS and Android fitness applications. Leading smart models provide step counting, calorie estimation, walking distance tracking, and session history logging. Voice assistant compatibility with Amazon Alexa and Google Assistant provides hands-free speed control for users engaged in concurrent work tasks.

Safety Technology: Anti-Slip and Auto-Stop Mechanisms

Infrared sensor arrays enabling automatic deceleration when no user presence is detected above the belt represent the standard safety architecture in premium models. Magnetic safety key systems providing instantaneous motor cutoff and side-rail pressure sensors triggering emergency stop are increasingly standard features specified in corporate-grade procurement requirements.

Market Segmentation Analysis

The report includes following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Folded |

58.4% |

2025 |

|

Technology |

Non-Smart |

62.7% |

2025 |

|

End User |

Residential |

🔒 |

2025 |

|

Distribution Channel |

Specialty Stores |

🔒 |

2025 |

|

Region |

Specialty Stores |

36.7% |

2025 |

By Technology

Non-smart under desk treadmills commands a 62.7% majority share in 2025 owing to their fundamental cost-competitiveness and accessibility across diverse buyer demographics. Non-smart models provide core walking functionality meeting the needs of most residential and entry-level commercial buyers without app or subscription dependencies.

To access detailed market analysis, Request Sample

Smart under desk treadmills at 37.3% in 2025, growing fastest, are preferred by health-data-oriented consumers seeking quantified wellness integration. Premium smart models provide comprehensive app ecosystems creating customer retention through data continuity, personalised coaching, and seamless synchronisation with wearable devices and corporate wellness tracking platforms.

By Product Type

Folded under desk treadmills dominate the product type segment at 58.4% in 2025, representing the highest-volume, most space-efficient design for residential and compact commercial applications. Fold-flat designs storing to less than 15cm height are the de facto standard for home office deployments in urban apartment environments where storage space is at a premium.

Unfolded product types, with 32.6% in 2025, provide a stable, continuously operational platform preferred for high-utilisation commercial environments including corporate wellness centres, hotel fitness rooms, and rehabilitation facilities where permanent installation justifies the larger floor footprint. Others (9.0%) encompasses hybrid and emerging format configurations.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

| North America |

36.7% |

High disposable income; corporate wellness culture; hybrid work adoption; HSA/FSA eligibility |

| Asia Pacific |

28.4% |

Rising urban health awareness; growing middle class; domestic manufacturing strength |

| Europe |

22.6% |

Workplace ergonomics regulation; health-conscious culture; growing e-commerce channels |

| Latin America |

7.5% |

Urban wellness trends; growing online retail; rising health consciousness in key markets |

| Middle East & Africa |

4.8% |

GCC premium lifestyle adoption; growing wellness market; expanding retail infrastructure |

North America's 36.7% market dominance in 2025 is driven by a structurally favourable combination of high per-capita wellness expenditure, established corporate wellness culture, and the world's highest penetration of hybrid and remote working models. HSA/FSA reimbursement eligibility in the United States significantly lowers effective consumer price barriers.

Asia Pacific, with 28.4% in 2025, is the fastest-growing region at ~5.6% CAGR through 2034. China's dual role as both the primary global manufacturing centre and a rapidly expanding domestic consumer market for wellness technology creates a structurally advantageous position for Chinese-origin brands.

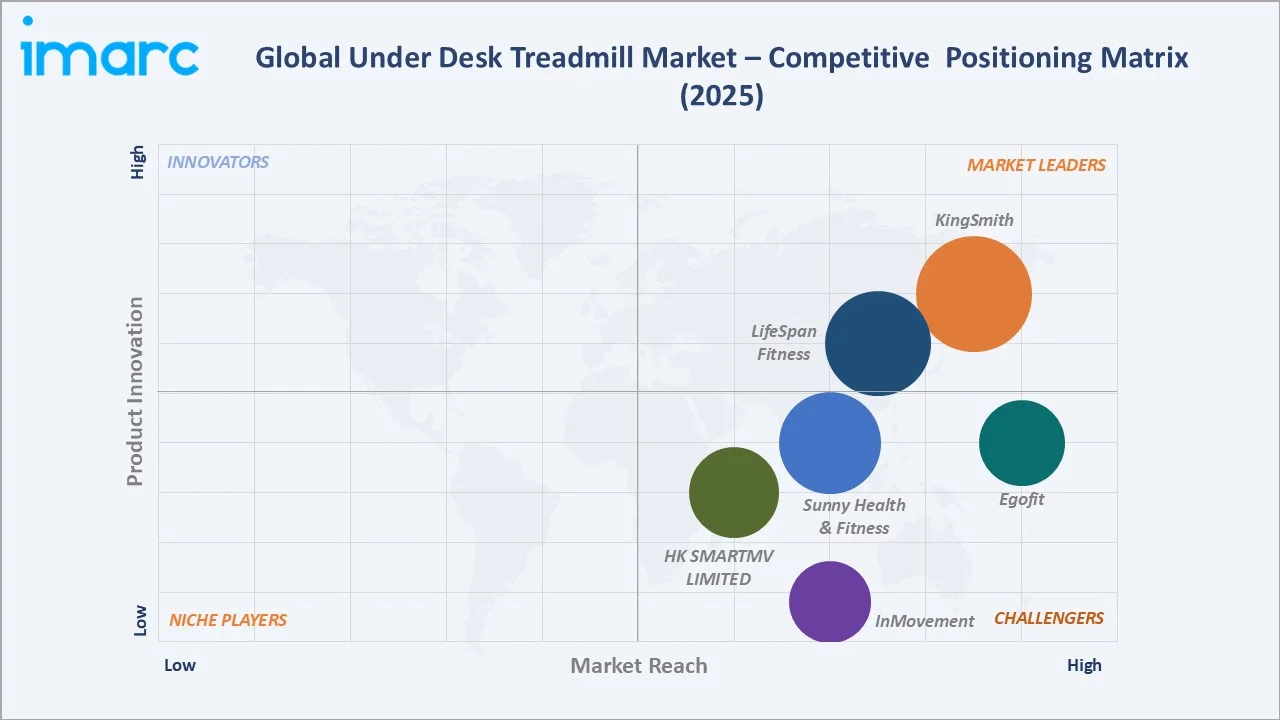

Competitive Landscape

The global under desk treadmill market is moderately fragmented, with a mix of dedicated fitness technology brands, broader fitness equipment manufacturers, and value-oriented consumer goods companies.

|

Company Name |

Key Products |

Market Position |

Global Strategic Focus |

| KingSmith | WalkingPad A1, C2, R2 Pro |

Leader |

Asia/Global; foldable design leadership; category pioneer |

| LifeSpanFitness | TR1200Pro-GlowUp, TR5000-Pro-GlowUp, TX6-GlowUp |

Leader |

North America commercial; desk treadmill specialist; enterprise sales |

| Sunny Health & Fitness | Treadpad 100, Pacer Auto, Pacer 2 in 1 Auto, Under Desk Smart TreadPad | Challenger |

North America value; broad fitness range; retail distribution |

| HK SMARTMV LIMITED | Mobvoi Home Treadmill | Challenger |

China/Asia; AI & smart connectivity; wearable ecosystem |

| Egofit | Egofit Walker Pro, Egofit Walker Plus, Egofit ComfortDeck-M2, Egofit ComfortDeck-M2T | Challenger |

Global value; compact design; entry-level price leadership |

| InMovement | Unsit |

Challenger |

North America; integrated treadmill-desk; commercial ergonomics |

Key players include KingSmith, LifeSpanFitness, Sunny Health & Fitness, HK SMARTMV LIMITED, Egofit, InMovement, and others.

Key Company Profiles

KingSmith

KingSmith, operating through its brand WalkingPad, is the category-defining under desk treadmill manufacturer headquartered in China. WalkingPad's patented fold-in-half technology enabling sub-10cm storage height established the modern foldable under desk treadmill category and drives its global brand recognition.

- Product Portfolio: WalkingPad A1, C2, R2 Pro, and others

- Recent Developments: In September 2025, KingSmith unveiled its latest innovation, the WalkingCase treadmill, at IFA Berlin 2025, introducing a new approach to compact home fitness equipment. The product emphasizes portability and space efficiency, featuring a foldable design inspired by carry-on luggage, along with wheels and a telescopic handle for easy movement and storage.

- Strategic Focus: WalkingPad's strategy centres on design-led foldable treadmill innovation, expanding smart feature capabilities, and international distribution growth across North America and European markets while maintaining cost leadership through vertically integrated Chinese manufacturing.

LifeSpanFitness

LifeSpanFitness is North America's leading dedicated desk treadmill specialist, headquartered in Salt Lake City, Utah. The company focuses exclusively on active workstation solutions and has the broadest enterprise-certified product range for corporate bulk procurement, with tested compatibility across major sit-stand desk brands.

- Product Portfolio: TR1200Pro-GlowUp, TR5000-Pro-GlowUp, TX6-GlowUp, and others

- Strategic Focus: LifeSpanFitness differentiates on enterprise-grade durability, corporate safety certifications, fleet management capabilities, and dedicated B2B sales support addressing procurement requirements of large-scale corporate wellness programme deployments.

Sunny Health & Fitness

Sunny Health & Fitness is a leading mass-market fitness equipment manufacturer distributing through major North American retail channels including Amazon, Walmart, and Target. The company's broad portfolio provides extensive distribution infrastructure supporting under desk treadmill market penetration across value and mid-tier price points.

- Product Portfolio: Treadpad 100, Pacer Auto, Pacer 2 in 1 Auto, Under Desk Smart TreadPad, and others.

- Recent Developments: In April 2025, Sunny Health & Fitness expanded its connected home fitness lineup with the introduction of new Wi-Fi-enabled treadmills, reinforcing its focus on delivering more interactive and accessible workout solutions. These treadmills are designed to integrate seamlessly with the SunnyFit app, providing users with access to a wide range of guided workouts, virtual training experiences, and performance tracking features.

- Strategic Focus: Sunny Health & Fitness focuses on accessible pricing, broad multi-channel retail distribution, and a comprehensive fitness equipment portfolio that cross-sells treadmills alongside other fitness products to value-conscious wellness consumers.

Market Concentration Analysis

The global under desk treadmill market is moderately fragmented at the global level, with no single company holding more than 20–25% of total global market revenue. WalkingPad holds the strongest brand position globally, estimated at approximately 25–30% unit volume share, driven by category pioneer status and strong digital marketing execution.

Consolidation at the regional level is more advanced than global data suggests. LifeSpanFitness and iMovR together command a disproportionate share of North America's premium corporate segment, while WalkingPad and Mobvoi dominate Asia Pacific's smart consumer tier. E-commerce platform algorithms increasingly favour established brands with large review volumes, creating structural barriers to new market entrants.

Investment & Growth Opportunities

Fastest-Growing Segments

Smart under desk treadmills at ~5.2% CAGR through 2034 represent the highest-growth technology segment, driven by health data integration demand, app connectivity, and AI coaching feature expectations from health-conscious premium consumers. Asia Pacific at ~5.6% CAGR is the fastest-growing region, fuelled by rising urban health awareness and expanding middle-class disposable income.

Emerging Markets

Asia Pacific presents the most dynamic emerging market opportunity within the under desk treadmill sector. India's rapidly growing urban professional class, South Korea's technology adoption culture, and Australia's established wellness market combine to offer strong growth opportunities beyond China's already developed domestic consumer segment for early-mover international brands.

Venture & Investment Trends

Private equity interest in ergonomic workplace wellness equipment categories is increasing, with strategic acquirers from larger fitness equipment groups and consumer electronics companies viewing under desk treadmill brands as adjacent category expansion opportunities. Software subscription revenue potential from smart treadmill app platforms is attracting SaaS-oriented investor interest beyond traditional hardware valuation frameworks.

Future Market Outlook (2026-2034)

The global under desk treadmill market is forecast to expand from USD 137.8 Million in 2025 to USD 206.8 Million by 2034 at a CAGR of 4.47%, adding USD 69.0 Million in incremental annual market value over the forecast period. This steady growth reflects the market's wellness-linked demand fundamentals and expanding addressable market through accelerating corporate adoption.

Three technological forces will most significantly shape the under desk treadmill industry through 2034. AI-powered gait analysis and posture correction will elevate smart models from activity trackers to preventive health tools. Whisper-quiet motor technology achieving sub-35dB operation will unlock mass corporate office deployment. Integration with workplace productivity platforms will create employer ROI documentation supporting wellness programme budget allocation.

Research Methodology

Primary Research

Primary research encompassed structured interviews with under desk treadmill industry stakeholders including commercial managers at leading brands, corporate wellness procurement officers, ergonomics consultants, and retail buyers at specialty fitness and e-commerce channels. Primary data validated market sizing, technology and product type segment shares, regional demand estimates, and competitive positioning assessments.

Secondary Research

Key secondary sources include WHO Global Status Report on Physical Activity, Global Wellness Institute Economy Report, Business of Fitness industry publications, Consumer Technology Association fitness equipment data, US Bureau of Labor Statistics remote work surveys, and trade publications including Sporting Goods Intelligence and Fitness Industry Technology Council reports.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models incorporating global wellness expenditure growth rates, hybrid work adoption indices, consumer electronics spending data, and historical under desk treadmill market evolution patterns. Scenario analysis across base, optimistic, and conservative cases was performed to account for macroeconomic uncertainty.

Under Desk Treadmill Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Folded, Unfolded, Others |

| Technologies Covered | Smart, Non-Smart |

| End Users Covered | Residential, Commercial, Institutional |

| Distribution Channels Covered | Supermarket and Hypermarkets, Specialty Stores, Online Stores, Others |

| Region Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico, Turkey, Saudi Arabia |

| Companies Covered | KingSmith, LifeSpanFitness, Sunny Health & Fitness, HK SMARTMV LIMITED, Egofit, InMovement, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Under Desk Treadmill Market Report

The global under desk treadmill market reached USD 137.8 Million in 2025, reflecting consistent demand driven by rising health consciousness, remote and hybrid work adoption, and growing corporate wellness programme investments globally.

The market is projected to reach USD 206.8 Million by 2034, growing at a CAGR of 4.47% during 2026-2034, driven by smart technology adoption, Asia Pacific urbanisation, and accelerating corporate bulk procurement of wellness equipment.

Non-smart treadmills lead with a 62.7% share in 2025, valued for cost-effectiveness and simplicity. Smart treadmills (37.3%) are the fastest-growing technology segment at ~5.2% CAGR through 2034, driven by app connectivity and AI-powered fitness tracking demand.

Folded under desk treadmills dominate at 58.4% in 2025, representing the most space-efficient design for residential and compact commercial applications. Their fold-flat storage capability is the primary purchase driver in urban home office environments.

North America commands the largest regional share at 36.7% in 2025, driven by high consumer disposable income, widespread corporate wellness programmes, HSA/FSA fitness equipment reimbursement eligibility, and strong hybrid work adoption rates.

Asia Pacific is the fastest-growing region at ~5.6% CAGR through 2034, fuelled by rapidly expanding urban middle-class health awareness, rising disposable income in China, South Korea, and India, and strong domestic manufacturing capabilities supporting competitive pricing.

Leading companies include KingSmith, LifeSpanFitness, Sunny Health & Fitness, HK SMARTMV LIMITED, Egofit, InMovement, and others

The primary drivers include rising sedentary lifestyle awareness, growth of remote and hybrid work models creating home office equipment investment, corporate wellness programme expansion, and technological innovations in smart connectivity and ultra-quiet motor design.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)