United Kingdom Continuous Glucose Monitoring Devices Market Size, Share, Trends and Forecast by Component, Demographics, End User, and Region, 2026-2034

United Kingdom Continuous Glucose Monitoring Devices Market Summary:

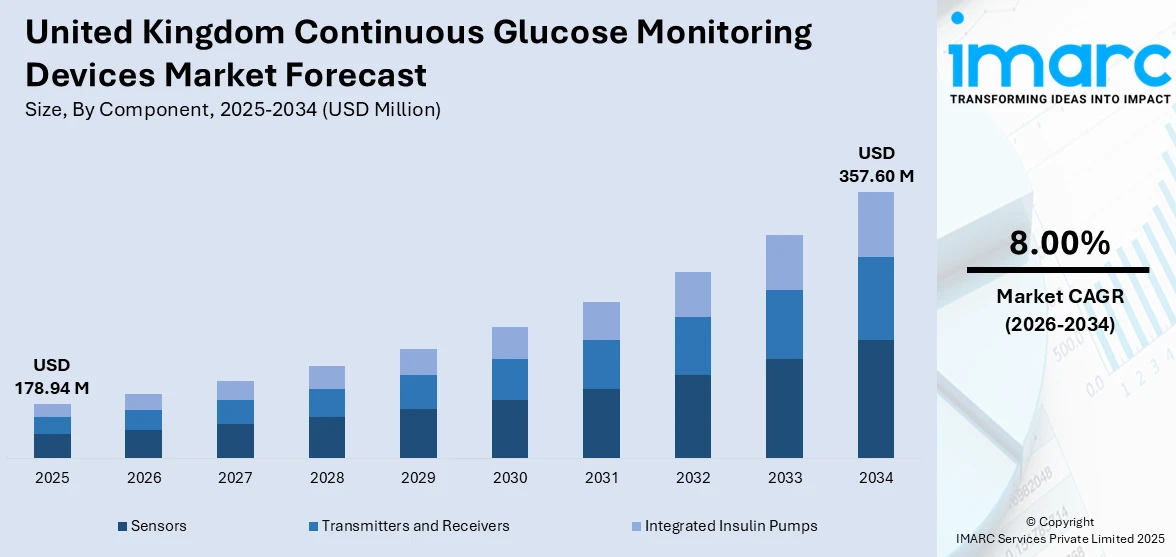

The United Kingdom continuous glucose monitoring devices market size was valued at USD 178.94 Million in 2025 and is projected to reach USD 357.60 Million by 2034, growing at a compound annual growth rate of 8.00% from 2026-2034.

The United Kingdom continuous glucose monitoring devices market is experiencing robust expansion driven by the escalating prevalence of diabetes across the nation, increasing adoption of real-time glucose monitoring solutions, and strong National Health Service support for CGM technology. The growing preference for non-invasive monitoring solutions combined with technological advancements in sensor accuracy and smartphone integration is reshaping diabetes management approaches. Enhanced NHS commissioning policies extending CGM access to both Type 1 and insulin-treated Type 2 diabetes patients, coupled with rising health awareness and digital healthcare adoption, are propelling the United Kingdom continuous glucose monitoring devices market share.

Key Takeaways and Insights:

- By Component: Sensors lead the market in 2025, because they provide real-time glucose data, improve diabetes management, enhance patient adherence, drive recurring replacement demand, and benefit from innovation and adoption.

- By Demographics: Adults dominate the market with a share of 73.2% in 2025, owing to the high prevalence of Type 2 diabetes among the adult population and expanded NHS eligibility criteria for CGM access.

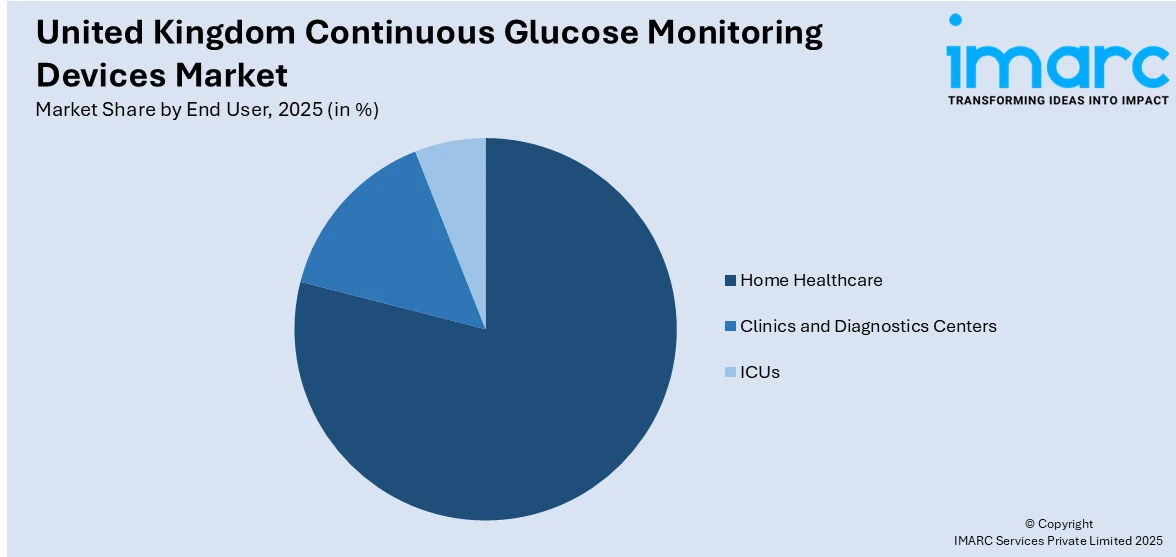

- By End User: Home healthcare leads the market with a share of 78.8% in 2025, driven by the preference for convenient self-monitoring solutions and the shift toward patient-centric diabetes management.

- By Region: London dominates the market in 2025, due to high diabetes prevalence, advanced healthcare infrastructure, strong adoption of digital health technologies, greater awareness, and higher spending on innovative diabetes management solutions.

- Key Players: The United Kingdom continuous glucose monitoring devices market exhibits moderate competitive intensity, with established multinational corporations competing alongside emerging regional manufacturers. The market is characterized by ongoing product innovation, strategic partnerships, and increasing focus on affordability to enhance patient accessibility.

To get more information on this market Request Sample

The United Kingdom continuous glucose monitoring devices market is witnessing transformative growth as diabetes management evolves toward technology-enabled, personalized care models. The integration of artificial intelligence and machine learning into CGM systems is enabling predictive analytics and customized glucose insights, fundamentally changing how patients and healthcare providers approach diabetes management. In May 2025, United Kingdom-based Urathon Europe Ltd successfully launched the Yuwell Anytime CGM at the Primary Care Show, introducing the innovative device to healthcare professionals across the country and showcasing its benefits for broader clinical and NHS use, reflecting rising industry interest and adoption. Government initiatives targeting diabetes prevention and remission programs are accelerating CGM adoption, particularly among individuals with prediabetes and early-onset Type 2 diabetes. For instance, United Kingdom-based Urathon Europe Ltd secured exclusive distribution rights for the Yuwell Anytime CGM, introducing a cost-effective device featuring a rechargeable transmitter, working in partnership with leading universities to drive prevention and remission programs.

United Kingdom Continuous Glucose Monitoring Devices Market Trends:

Rising Integration of Smartphone Applications and Connected Health Ecosystems

The United Kingdom continuous glucose monitoring devices market is experiencing significant advancement through seamless smartphone integration and connected health platforms. Modern CGM systems increasingly incorporate real-time data synchronization with mobile applications, enabling users to visualize glucose trends, receive personalized alerts, and share data with healthcare providers remotely. In 2024, Insulet Corporation announced the full commercial launch of its Omnipod 5 system in the United Kingdom with expanded sensor integrations, allowing compatibility with both Dexcom G6 and Abbott FreeStyle Libre 2 Plus CGM sensors, enhancing connected insulin delivery and glucose data flow to users’ digital platforms. This connectivity facilitates proactive care management and empowers patients to understand how lifestyle factors impact their glucose levels.

Expansion of Hybrid Closed-Loop Systems and Automated Insulin Delivery

The market is witnessing growing adoption of hybrid closed-loop systems that combine CGM technology with insulin pumps for automated glucose regulation. These artificial pancreas solutions continuously monitor glucose levels and automatically adjust insulin delivery, significantly improving glycemic control while reducing patient burden. In England, NICE guidance and NHS rollout efforts have driven rapid uptake of these systems. By March 2025, about 62% of eligible children and young people with Type 1 diabetes were reported to be using hybrid closed-loop technology, up from 36% in the previous year, reflecting the success of phased implementation and clinical integration across NHS services. The NHS gradual rollout of hybrid closed-loop systems prioritizes children, young people, and adults with Type 1 diabetes meeting specific criteria.

Growing Focus on Type 2 Diabetes and Preventive Health Applications

The United Kingdom market is experiencing a paradigm shift with CGM technology extending beyond Type 1 diabetes to address the substantial Type 2 diabetes population and prediabetes prevention. Manufacturers are developing cost-effective devices specifically targeting individuals not on insulin, enabling them to understand how dietary and lifestyle choices affect glucose levels, aligning with NHS objectives to reduce diabetes-related complications. Recent developments include a United Kingdom expansion of Abbott’s FreeStyle Libre 2 real-time continuous glucose monitoring capability through a software upgrade, allowing glucose readings to be transmitted automatically to smartphones without scanning, broadening the practical usability of CGM systems for people with Type 2 diabetes and those aiming to optimise lifestyle management.

Market Outlook 2026-2034:

The United Kingdom continuous glucose monitoring devices market is poised for large growth and development with technology advancement, favorable government regulations, and a growing pool of diabetic patients in the region. The advancement in innovative technologies with extended sensor lifespan and support and compatibility with digital technologies continues to entice both healthcare service providers and patients in the region in a bid to improve diabetes management results and success. Growing NHS spending on diabetes preventive interventions and the development of inexpensive CGM systems for underserved patients will improve market coverage and saturation in this region. The market generated a revenue of USD 178.94 Million in 2025 and is projected to reach a revenue of USD 357.60 Million by 2034, growing at a compound annual growth rate of 8.00% from 2026-2034.

United Kingdom Continuous Glucose Monitoring Devices Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Demographics |

Adults |

73.2% |

|

End User |

Home Healthcare |

78.8% |

Component Insights:

- Sensors

- Transmitters and Receivers

- Integrated Insulin Pumps

The sensors dominates the total United Kingdom continuous glucose monitoring devices market in 2025.

The sensor component represents the core technological element of continuous glucose monitoring systems, utilizing advanced electrochemical technology to measure glucose concentrations in interstitial fluid beneath the skin. These miniaturized sensors are designed for comfortable subcutaneous insertion, typically on the upper arm or abdomen, where they continuously detect glucose levels and transmit data to connected devices. Reflecting ongoing innovation, in 2025 Dexcom received clearance for its next‑generation G7 sensor that extends wear time up to approximately 15.5 days while maintaining enhanced accuracy over previous versions, reducing the frequency of replacements and improving user experience. Modern sensors feature enhanced accuracy through improved enzyme-based detection mechanisms, extended wear durations that reduce the frequency of replacements, and simplified applicator designs that enable painless self-insertion with minimal discomfort for users.

Ongoing innovation in sensor technology is driving market advancement through the development of smaller form factors, improved biocompatibility materials, and enhanced signal processing algorithms that deliver more reliable glucose readings. Manufacturers are focusing on extending sensor lifespan while maintaining measurement precision, reducing calibration requirements, and minimizing skin irritation issues that have historically affected user compliance. The emergence of factory-calibrated sensors has eliminated the need for routine finger-prick confirmations, significantly improving user convenience and encouraging broader adoption among individuals seeking seamless diabetes management solutions without disrupting their daily activities.

Demographics Insights:

- Child Population (≤14 years)

- Adult Population (>14 years)

The adult population (>14 years) leads with a share of 73.2% of the total United Kingdom continuous glucose monitoring devices market in 2025.

The adult population segment's market leadership reflects the substantial burden of diabetes among the working-age and elderly population in the United Kingdom, where a significant proportion of diagnosed cases comprise Type 2 diabetes. Adults benefit from CGM technology's ability to provide continuous glucose insights that support lifestyle modifications, medication optimization, and prevention of both acute complications and long-term health consequences. The expansion of NHS CGM eligibility criteria to include adults with Type 2 diabetes on intensive insulin therapy who experience recurrent hypoglycemia or have impaired awareness has significantly broadened the accessible patient population, driving sustained demand growth.

The pediatric segment represents a critical focus area as NICE guidelines recommend CGM for all children and young people with Type 1 diabetes in England and Wales. Children face unique challenges in diabetes management including variable activity levels, growth-related metabolic changes, and the psychological burden of frequent finger-prick testing. CGM technology offers significant benefits for pediatric patients by reducing hypoglycemia episodes, improving time-in-range metrics, and alleviating caregiver anxiety through remote monitoring capabilities and customizable alerts.

End User Insights:

Access the comprehensive market breakdown Request Sample

- Clinics and Diagnostics Centers

- ICUs

- Home Healthcare

The home healthcare dominates with a market share of 78.8% of the total United Kingdom continuous glucose monitoring devices market in 2025.

The home healthcare segment's dominant position underscores the fundamental shift toward patient-centric diabetes management that enables individuals to monitor and manage their condition in familiar environments without requiring frequent clinical visits. Home-based CGM utilization empowers patients with real-time glucose data and actionable insights, supporting informed decision-making regarding diet, exercise, and medication timing. In November 2025, the Yuwell Anytime continuous glucose monitoring system was added to the NHS England supply framework, enabling healthcare providers and clinics to procure the device through official NHS channels and expanding access to a real‑time CGM that supports both self‑management at home and remote clinical oversight. The growing preference for remote patient monitoring and virtual consultations has accelerated this transition, with healthcare providers and patients alike recognizing the benefits of continuous home-based monitoring for improved glycemic control and enhanced quality of life.

Hospital and clinical settings continue to play important roles in CGM adoption, particularly for device initiation, patient training, and management of complex cases requiring specialist oversight. Secondary care diabetes teams are responsible for assessing patient eligibility, recommending appropriate CGM products, and providing ongoing support to ensure optimal device utilization. The integration of CGM data into clinical decision-making enhances treatment optimization and enables healthcare professionals to identify glucose patterns that inform therapy adjustments.

Regional Insights:

- London

- South East

- North West

- East of England

- South West

- Scotland

- West Midlands

- Yorkshire and The Humber

- East Midlands

- Others

London exhibits a clear dominance in the total United Kingdom continuous glucose monitoring devices market in 2025.

London represents a significant regional market for continuous glucose monitoring devices, benefiting from its advanced healthcare infrastructure, concentration of specialist diabetes centers, and diverse population with varying diabetes management needs. The capital's extensive network of NHS trusts and private healthcare facilities ensures broad access to CGM technology, while its position as a hub for medical innovation drives early adoption of emerging diabetes management solutions.

The region's healthcare ecosystem supports comprehensive diabetes care through numerous tertiary referral centers, research institutions, and diabetes specialist teams that facilitate CGM initiation and ongoing patient support. London's multicultural population, which includes ethnic groups with elevated diabetes risk profiles, creates substantial demand for effective glucose monitoring solutions that enable personalized disease management and prevention of long-term complications across diverse patient communities.

Market Dynamics:

Growth Drivers:

Why is the United Kingdom Continuous Glucose Monitoring Devices Market Growing?

Rising Diabetes Prevalence and Associated Healthcare Burden

The United Kingdom is experiencing a substantial increase in diabetes prevalence that directly drives demand for effective glucose monitoring solutions. This growth is attributed to aging demographics, increasing obesity rates, and evolving lifestyle factors. According to reports, an estimated 4.6 million people in the United Kingdom have a diagnosis of diabetes, the highest figure on record, while another 1.3 million remain undiagnosed and 6.3 million live with prediabetes, meaning one in five adults now live with either diabetes or prediabetes. The expanding patient population creates sustained demand for CGM devices that enable improved self-management and reduce the risk of costly diabetes-related complications including cardiovascular disease, kidney failure, and vision loss. The significant NHS expenditure on diabetes-related care underscores the economic imperative driving investment in prevention and management technologies.

Favorable NHS Policies and Expanded Access Guidelines

The United Kingdom's healthcare policy environment has become increasingly supportive of CGM technology adoption through expanded eligibility criteria and standardized commissioning frameworks. Updated National Institute for Health and Care Excellence (NICE) guidance recommends CGM for all people with Type 1 diabetes and extends access to people with Type 2 diabetes on intensive insulin therapy who experience recurrent hypoglycaemia or impaired hypoglycaemia awareness, reflecting a broader, evidence‑based approach to glucose monitoring across diabetes populations. The NHS commitment to introducing hybrid closed-loop systems represents a significant policy milestone driving CGM adoption. Additionally, clear prescribing pathways enabling primary care continuation of specialist-initiated therapy have streamlined patient access.

Technological Innovation Enhancing Device Accessibility and Usability

Continuous advancements in CGM technology are transforming device performance, user experience, and affordability, thereby expanding the addressable market. Modern sensors offer extended wear periods, eliminating the burden of frequent changes while reducing ongoing consumable costs. For example, in April 2025, Dexcom received U.S. FDA clearance for its Dexcom G7 15 Day continuous glucose monitoring system, extending sensor wear to approximately 15.5 days with improved accuracy and connectivity, marking one of the longest‑lasting and most accurate CGM products cleared to date and strengthening competitive dynamics in the market. Improved accuracy metrics have enhanced clinical confidence and reduced the need for confirmatory finger-prick testing. Smartphone integration with dedicated applications provides intuitive interfaces for data visualization, personalized alerts, and seamless sharing with healthcare providers. The emergence of new market entrants offering competitive pricing is democratizing CGM access beyond traditional premium segments.

Market Restraints:

What Challenges the United Kingdom Continuous Glucose Monitoring Devices Market is Facing?

High Device Costs and Ongoing Consumable Expenses

The continuous glucose monitoring devices market faces persistent affordability challenges that limit adoption among self-funding patients and strain healthcare budgets. CGM systems require regular sensor replacement along with periodic transmitter replacements, creating substantial ongoing costs. Despite NHS coverage for eligible patients, individuals not meeting access criteria must bear these expenses personally, creating access disparities particularly affecting lower-income populations.

Healthcare Professional Training and Workflow Integration

Effective CGM implementation requires adequate training for healthcare professionals across both specialist and primary care settings to assess patient suitability, recommend appropriate products, and interpret glucose data meaningfully. Insufficient healthcare provider training and resistance to new clinical workflows remain major barriers limiting CGM benefits realization. The need for diabetes specialist involvement in device initiation creates bottlenecks that can delay patient access to technology.

Technical Limitations and Sensor Reliability Concerns

Despite significant technological improvements, CGM devices continue to face technical challenges including sensor accuracy variations, adhesion problems, and skin irritation that affect user experience and confidence. Interstitial fluid glucose measurements introduce a physiological lag compared to blood glucose levels, requiring patients to maintain finger-prick testing capabilities for driving and hypoglycemia management. Signal interference and connectivity issues can disrupt continuous monitoring.

Competitive Landscape:

The competitive scenario of the United Kingdom continuous glucose monitoring devices market is concentrated, with established multinational corporations holding significant market share, while emerging players provide cost-friendly alternatives. Key players in the market retain the leading position owing to their broad product portfolio, early benefits of market access, strong relationships with the NHS, and adopting suitable price competition. High-end real-time segments of CGM attract substantial competition, particularly in the segment of Type 1 patients using integrated pump systems. This competitive landscape is increasing competition due to the entry of new players offering cheaper options to challenge incumbent pricing models. Established players are interested in strategic partnerships and collaborations to develop integrated sensor technologies as part of holistic diabetes management solutions.

Recent Developments:

-

In September 2025, Roche announced that its Accu-Chek SmartGuide continuous glucose monitoring (CGM) system integrated with the mySugr diabetes app has received CE-mark approval, enabling rollout into multiple markets including Europe and United Kingdom-accessible regions. The AI-enabled predictive CGM lets users view real-time glucose data and forecasts within mySugr, with availability expanding to 30+ countries by end 2025.

United Kingdom Continuous Glucose Monitoring Devices Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Components Covered |

Sensor, Transmitter and Receiver, Integrated Insulin Pumps |

|

Demographics Covered |

Child Population (≤14 years), Adult Population (>14 years) |

|

End Users Covered |

Clinics and Diagnostics Centers, ICUs, Home Healthcare |

|

Regions Covered |

London, South East, North West, East of England, South West, Scotland, West Midlands, Yorkshire and Humber, East Midlands, and Others. |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the United Kingdom Continuous Glucose Monitoring Devices Market Report

The United Kingdom continuous glucose monitoring devices market size was valued at USD 178.94 Million in 2025.

The United Kingdom continuous glucose monitoring devices market is expected to grow at a compound annual growth rate of 8.00% from 2026-2034 to reach USD 357.60 Million by 2034.

The sensor component dominated the market, driven by its essential role in glucose detection, continuous technological advancements improving accuracy and wear duration, and growing demand for reliable real-time monitoring solutions among diabetes patients across the United Kingdom.

Key factors driving the United Kingdom continuous glucose monitoring devices market include rising diabetes prevalence across all age groups, expanded NHS commissioning policies and NICE guideline recommendations, technological advancements in sensor accuracy and smartphone integration, and growing focus on diabetes prevention and remission programs.

Major challenges include high ongoing device and consumable costs limiting self-funding patient access, insufficient healthcare professional training creating implementation barriers, regional disparities in CGM access across different Integrated Care Boards, and technical limitations including sensor accuracy variations and adhesion issues.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)