United States Artificial Intelligence Market Size, Share, Trends and Forecast by Type, Offering, Technology, System, End-Use Industry, and Region, 2026-2034

United States Artificial Intelligence Market Size, Share, Trends & Forecast (2026-2034)

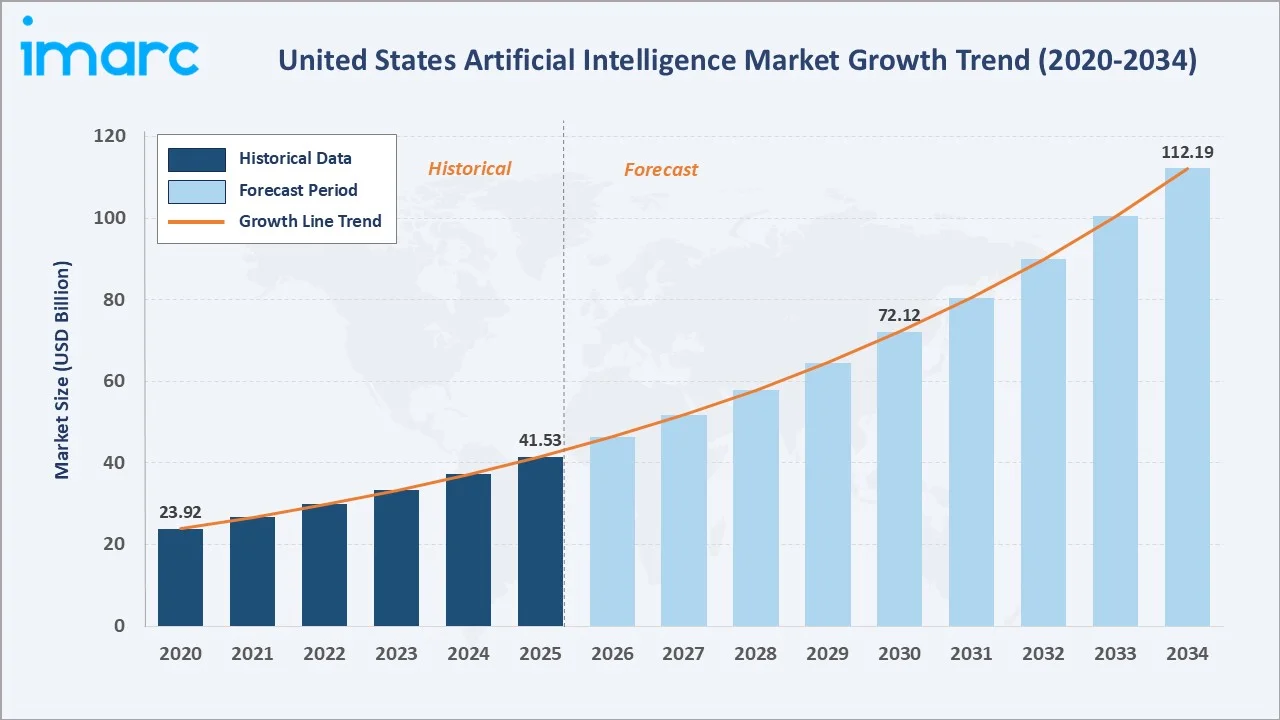

The United States Artificial Intelligence market was valued at USD 41.53 Billion in 2025 and is projected to reach USD 112.19 Billion by 2034, exhibiting a CAGR of 11.67% during the forecast period 2026-2034. The growth of the market is primarily driven by accelerating enterprise AI adoption, large-scale federal R&D investment, and surging demand for intelligent automation across healthcare, BFSI, and manufacturing.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 41.53 Billion |

|

Forecast Market Size (2034) |

USD 112.19 Billion |

|

CAGR (2026-2034) |

11.67% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

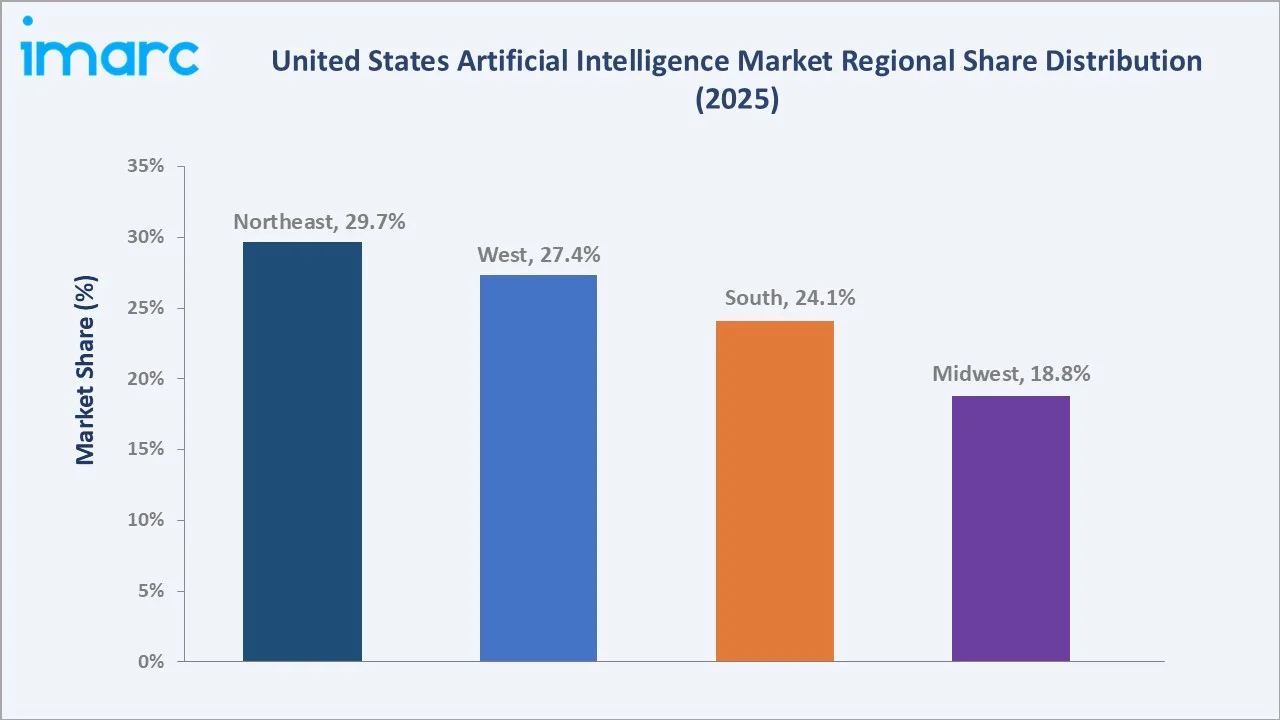

Largest Region (2025) |

Northeast (29.7%) |

|

Fastest Growing Segment |

General/Strong Artificial Intelligence |

The chart above illustrates the United States artificial intelligence market's historical growth from USD 23.92 Billion in 2020 to USD 41.53 Billion in 2025, and the forecast trajectory reaching USD 112.19 Billion by 2034. Dark bars represent the historical period; light blue bars denote the forecast phase at a CAGR of 11.67%.

To get more information on this market, Request Sample

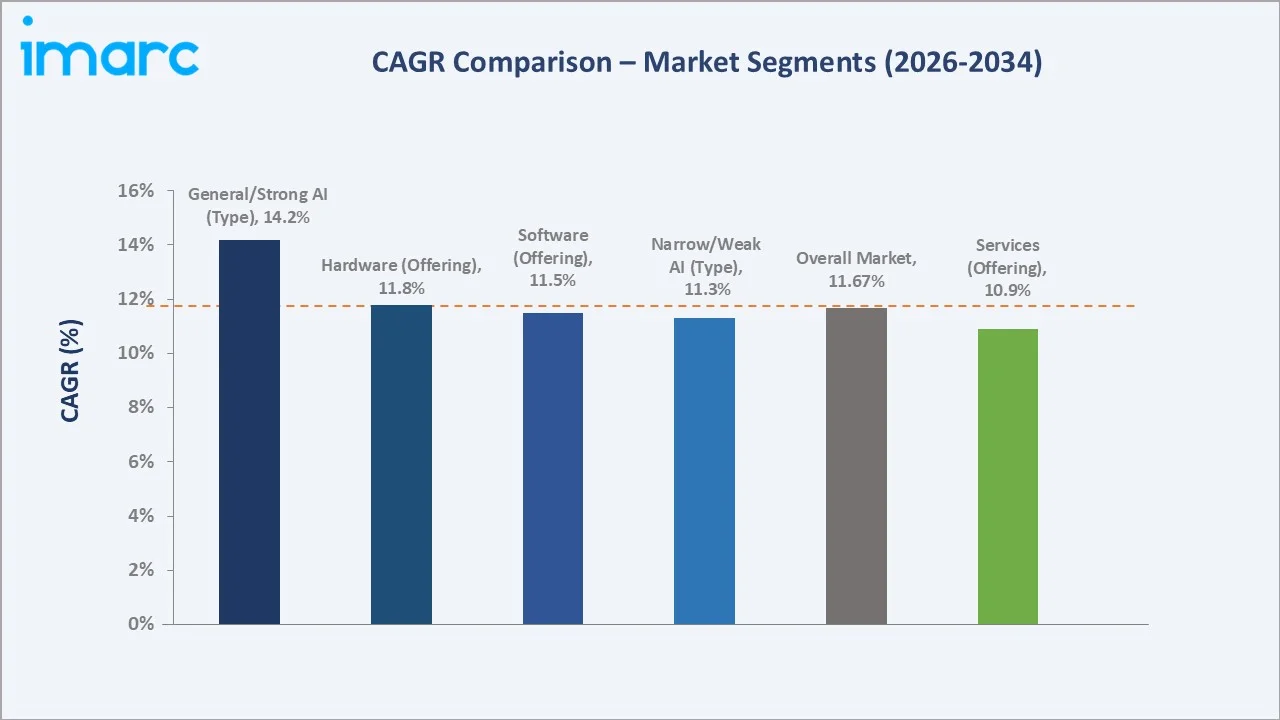

Segment-level CAGR comparisons highlighting enterprise adoption acceleration and high-growth AI sub-segments within the AI market forecast through 2030–2034.

Executive Summary

The United States Artificial Intelligence market has demonstrated consistent momentum over the historical period 2020-2025, growing from USD 23.92 Billion in 2020 to USD 41.53 Billion in 2025 – a cumulative increase of 73.6%. Looking ahead, the market is poised to nearly triple, reaching USD 112.19 Billion by 2034 at a CAGR of 11.67%. This growth is anchored in the widespread digitization of enterprise operations, increasing cloud infrastructure investment by hyperscalers, and growing availability of large-scale training datasets.

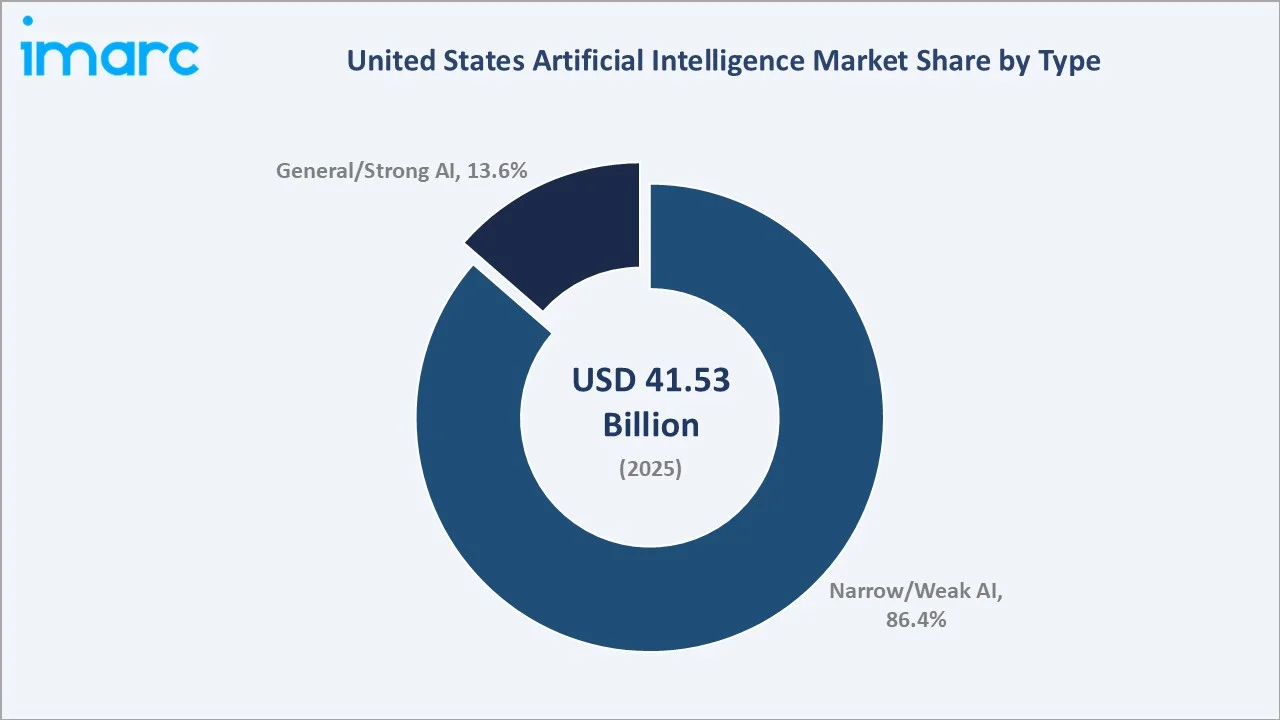

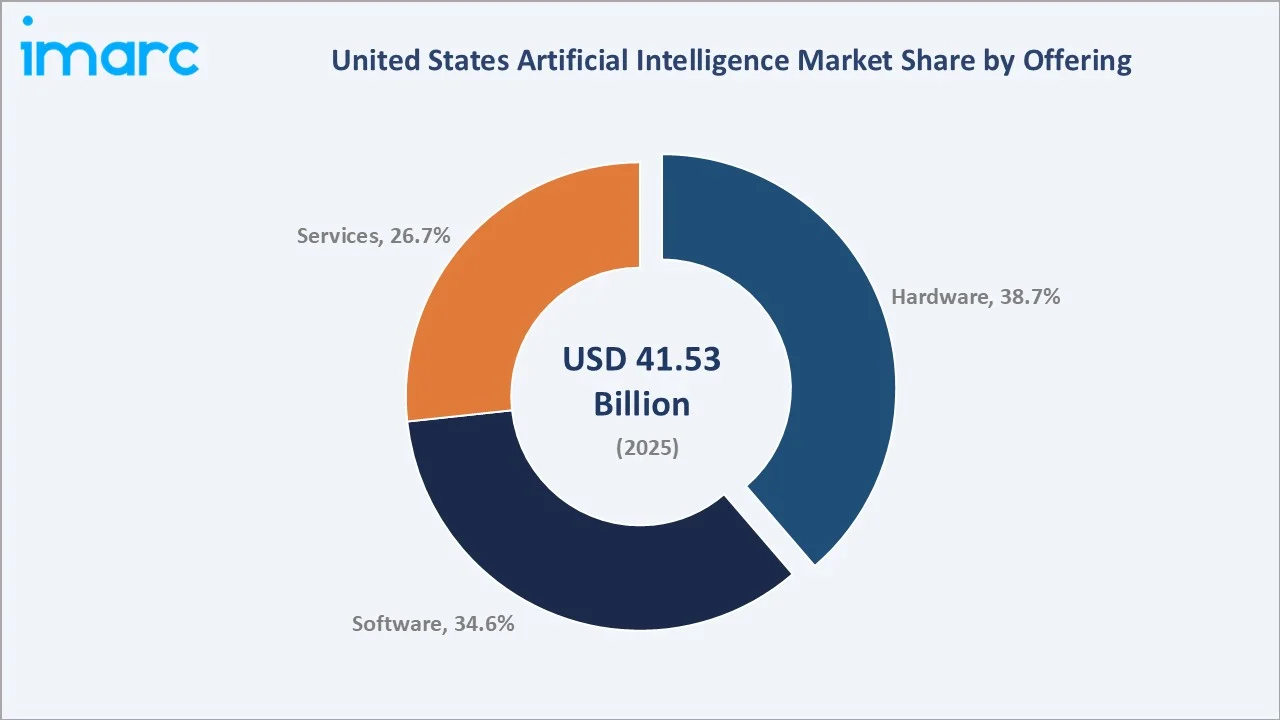

Narrow/Weak AI remains the commanding segment, capturing 86.4% of total revenue in 2025. These specialized systems – deployed across fraud detection, diagnostic imaging, autonomous vehicles, and recommendation engines – continue to define real-world AI deployment at scale. On the offering front, Hardware accounts for 38.7%, reflecting sustained capital expenditure on AI-optimized chips, GPUs, and edge computing devices. Software follows at 34.6%, powered by foundation models, MLOps platforms, and AI-as-a-Service solutions.

Geographically, the Northeast anchors national AI activity with a 29.7% market share in 2025, driven by dense concentrations of financial institutions, research universities, and technology companies in New York and Boston. The West closely trails at 27.4%, buoyed by Silicon Valley's AI ecosystem. The South (24.1%) and Midwest (18.8%) are both witnessing accelerating adoption, particularly in healthcare AI and smart manufacturing applications respectively.

Key Market Insights

|

Insight |

Data |

|

Largest Type |

Narrow/Weak AI – 86.4% (2025) |

|

Fastest Growing Type |

General/Strong AI – ~14.2% est. CAGR (2026-2034) |

|

Largest Offering |

Hardware – 38.7% (2025) |

|

Leading Region |

Northeast – 29.7% (2025) |

|

Key Technologies |

Machine Learning, NLP, Computer Vision |

|

Top Companies |

Microsoft, Alphabet Inc., Amazon.com, Inc., NVIDIA Corporation, Meta, IBM, OpenAI, Anthropic PBC |

|

Top End-Use Industries |

Healthcare, Financial Services, Manufacturing |

Key Analytical Observations Supporting the Above Data:

- Narrow/Weak AI's 86.4% dominance in 2025 reflects task-specific deployments in fraud detection, diagnostics, and NLP-driven virtual assistants. The segment grew from USD 20.66 Billion in 2020 to USD 35.88 Billion in 2025.

- Hardware's 38.7% offering share is driven by massive GPU and AI-chip procurement by cloud providers, autonomous vehicle OEMs, and edge-computing deployments globally sourced from US vendors.

- Northeast's 29.7% regional share in 2025 is anchored by New York's financial AI ecosystem and Boston's thriving AI research cluster.

- General/Strong AI is projected at approximately 14.2% CAGR through 2034, the fastest-growing sub-segment, driven by investments from OpenAI, Anthropic, Google DeepMind, and Microsoft.

United States Artificial Intelligence Market Overview

Artificial Intelligence in the United States encompasses technologies enabling machines to simulate human cognitive functions – including perception, reasoning, problem-solving, and decision-making. The ecosystem spans specialized narrow-AI applications through to foundational model development targeting general intelligence. The market is deeply intertwined with the broader digital economy, integrating with cloud computing, semiconductor manufacturing, cybersecurity, and data management industries.

Macro-level forces shaping this market include the CHIPS and Science Act (USD 52 Billion in semiconductor funding), the Executive Order on AI Safety (October 2023), and growing state-level AI procurement initiatives. The US leads globally in AI patent filings, private investment, and talent concentration.

Market Dynamics

To evaluate market opportunities, Request Sample

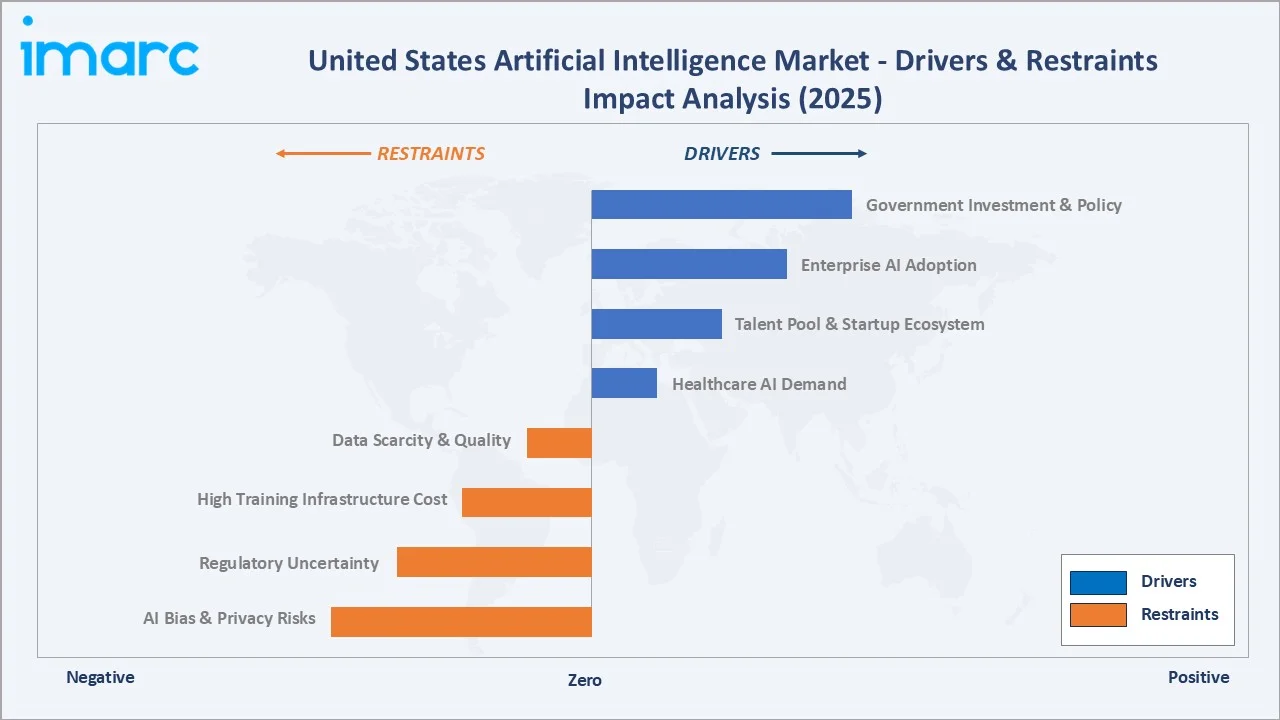

Market Drivers

- Government Investment & Policy Support: US federal and state governments committed over USD 3.3 Billion in non-defense AI-related R&D budgets in FY2025. The National AI Initiative Act and CHIPS Act together mobilize public-private AI development at unprecedented scale.

- Accelerating Enterprise AI Adoption: Enterprise AI spending in the US has grown rapidly, driven by large corporations deploying AI across core business functions such as process automation, customer service, and predictive analytics. Adoption is being fueled by the need to enhance operational efficiency, reduce costs, and improve decision-making through data-driven insights.

- Deep Talent Pool & Innovation Ecosystem: The US maintains one of the world’s most advanced AI talent ecosystems, supported by a strong base of skilled professionals and a rapidly expanding startup landscape. This environment is further strengthened by significant private investment inflows, enabling continuous innovation, accelerating AI adoption across industries, and reinforcing the country’s leadership in enterprise AI development.

- Healthcare & Life Sciences AI Demand: The healthcare sector is emerging as a key growth driver for AI adoption, supported by the increasing digitization of health records, advancements in AI-driven drug discovery, and the growing use of clinical decision support systems. Rising demand for improved patient outcomes, operational efficiency, and data-driven diagnostics is accelerating AI integration across healthcare and life sciences organizations.

Market Restraints

- Data Privacy Concerns & Regulatory Uncertainty: AI system bias, data privacy breaches, and lack of explainability create regulatory and reputational risk. CCPA and CPRA impose compliance costs on AI developers operating in the US market.

- High Infrastructure & Training Costs: Developing and deploying advanced AI models requires substantial computational power, specialized hardware, and large-scale data infrastructure. The significant investment needed for model training and maintenance creates high entry barriers for new market participants, limiting competition and concentrating capabilities among well-funded organizations with access to advanced resources.

- Data Scarcity & Quality Issues: Data scarcity in niche verticals such as rare disease diagnostics and specialized industrial manufacturing constrains model performance and slows vertical AI deployment timelines.

Market Opportunities

- Edge AI & IoT Integration: The Edge AI hardware market in the US is expanding rapidly, driven by the need for low-latency, real-time data processing across industries such as manufacturing, healthcare devices, and autonomous vehicles.

- AI-Driven Drug Discovery: AI-powered drug discovery platforms are significantly accelerating pharmaceutical innovation by enabling faster identification of drug candidates and optimizing clinical trial processes.

- Defense & Government AI Contracts: US DoD allocated USD 1.8 Billion to AI development in FY2024, creating substantial opportunity in defense AI, autonomous systems, and cybersecurity AI applications.

Market Challenges

- Workforce Displacement: AI adoption is expected to significantly disrupt administrative and data-entry roles, raising concerns around workforce displacement and job transitions. This shift is prompting increased social and legislative scrutiny, with policymakers, labor groups, and organizations.

- AI-Enabled Cyber Threats: As AI systems grow in capability, threats from adversarial AI attacks, deepfakes, and AI-enabled cyberattacks pose growing challenges for enterprise and government security frameworks.

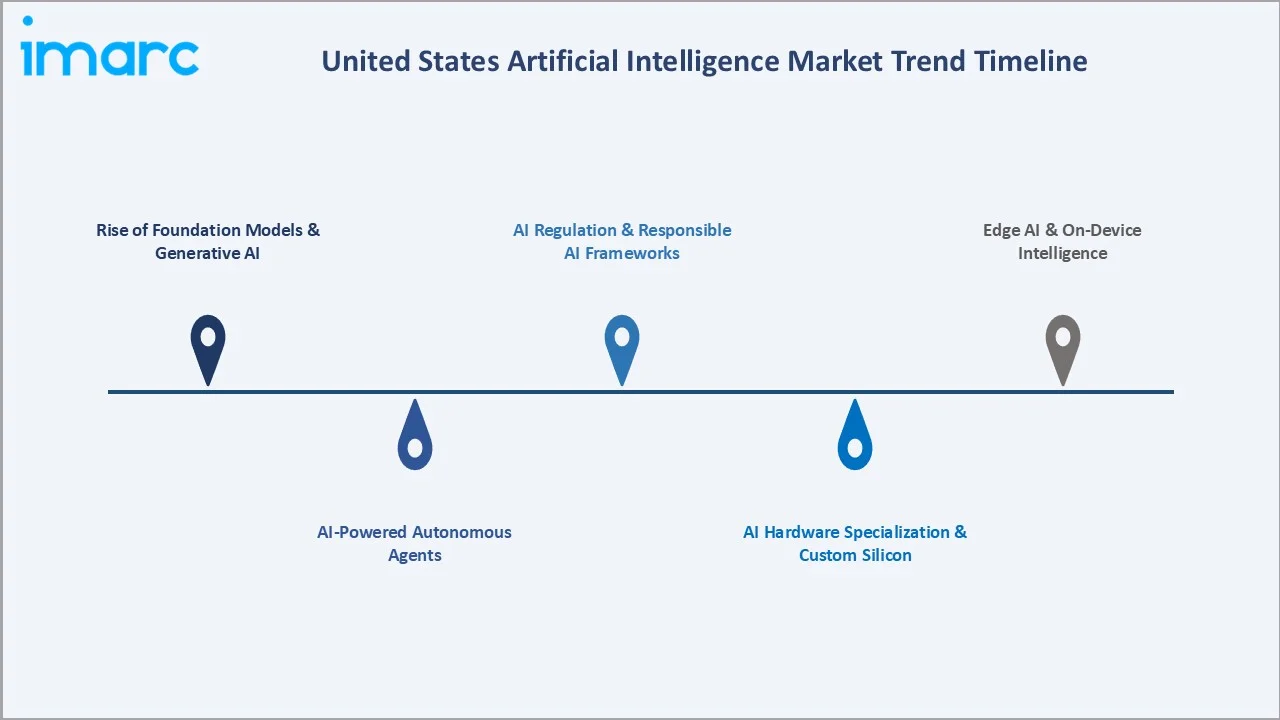

Emerging Market Trends

Rise of Foundation Models & Generative AI

Generative AI, powered by large language models such as GPT-4o, Claude 3, and Gemini, is rapidly transforming enterprise software by enabling automation across a wide range of use cases. From content creation and code generation to customer service automation, organizations are integrating generative AI into core workflows to enhance productivity, streamline operations, and improve user experiences.

AI-Powered Autonomous Agents

Agentic AI systems—capable of multi-step reasoning, tool utilization, and autonomous task execution—are emerging as the next frontier in enterprise AI. Organizations are increasingly integrating these systems into core business applications to automate complex workflows and enhance decision-making.

AI Hardware Specialization & Custom Silicon

Demand for custom AI accelerators is accelerating. NVIDIA's H100 chips accounted for over 70% of AI training compute revenue in 2024. Companies like Google (TPUs), Amazon (Trainium/Inferentia), and Apple (Neural Engine) are investing heavily in in-house silicon, reducing reliance on third-party GPUs and lowering per-inference costs.

AI Regulation & Responsible AI Frameworks

The National Institute of Standards and Technology’s AI Risk Management Framework (AI RMF 1.0) is gaining widespread adoption as organizations prioritize responsible and trustworthy AI deployment. At the same time, evolving federal regulations are expected to introduce binding requirements around algorithmic audits, transparency, and bias reporting for high-risk AI systems.

Edge AI & On-Device Intelligence

On-device AI is gaining significant traction as advancements in semiconductor performance enable more efficient processing directly on devices. This shift is driving a growing share of AI inference workloads in mobile and IoT applications to the edge, reducing reliance on cloud infrastructure.

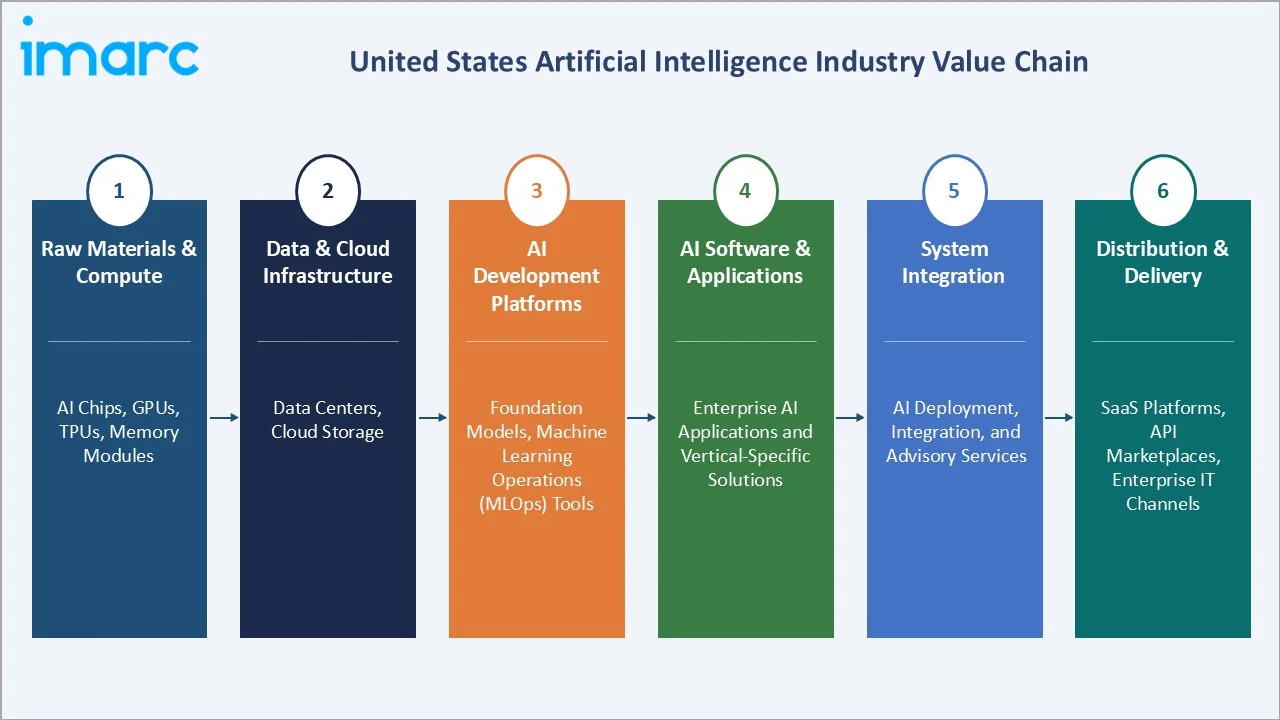

Industry Value Chain Analysis

|

Value Chain Stage |

Key Participants / Description |

|

Raw Materials & Compute |

NVIDIA, AMD, Intel– AI chips, GPUs, , memory modules, and foundational compute hardware |

|

Data & Cloud Infrastructure |

AWS, Microsoft Azure, Google Cloud– data centers, cloud storage, networking, and compute-as-a-service |

|

AI Development Platforms |

OpenAI, Anthropic– foundation models, training infrastructure, MLOps tools |

|

AI Software & Applications |

Enterprise AI applications and vertical-specific solutions |

|

System Integration & Consulting |

AI deployment, integration, and advisory services |

|

Distribution & Delivery |

SaaS platforms, API marketplaces, enterprise IT channels, resellers, and managed service providers |

|

End Users / Industries |

Healthcare, BFSI, Manufacturing, Retail, Automotive, Defense, Agriculture, and Transportation sectors |

Technology Landscape in the United States Artificial Intelligence Industry

Large Language Models and Foundation Model Architecture

Transformer-based foundation models have emerged as the defining technological paradigm of the US AI market, with organizations such as OpenAI, Anthropic, Google DeepMind, and Meta deploying increasingly capable multimodal architectures capable of processing text, image, audio, and video inputs within unified model frameworks.

AI-Optimized Silicon and Custom Compute Hardware

Demand for purpose-built AI accelerators is reshaping the semiconductor landscape, with NVIDIA's H100 and Blackwell GPU series commanding the dominant share of AI training and inference workloads across US hyperscaler data centers. Simultaneously, hyperscalers are accelerating in-house silicon development

Machine Learning Operations and AI Development Platforms

The maturation of MLOps tooling is enabling organizations to move AI workloads from experimentation to production with greater reliability and governance oversight. Platforms such as AWS SageMaker, Google Vertex AI, and Microsoft Azure Machine Learning provide end-to-end pipelines covering data labeling, model training, continuous integration, deployment orchestration, and performance monitoring.

Natural Language Processing, Computer Vision, and Multimodal AI

Natural language processing and computer vision remain the two most commercially deployed AI technology domains across the US market, underpinning applications spanning clinical documentation, fraud detection, autonomous quality inspection, and intelligent search

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Narrow/Weak Artificial Intelligence |

86.4% |

2025 |

|

Offering |

Hardware |

38.7% |

2025 |

|

Technology |

Machine Learning |

🔒 |

2025 |

|

System |

Intelligence Systems |

🔒 |

2025 |

| End-Use Industry | Manufacturing | 🔒 | 2025 |

|

Region |

Northeast |

29.7% |

2025 |

By Type

To access detailed market analysis, Request Sample

Narrow/Weak Artificial Intelligence represented the largest market share at 86.4% in 2025 due to its widespread commercial deployment across task-specific domains including fraud detection, medical imaging diagnostics, speech recognition, and product recommendation engines. These domain-constrained AI systems offer proven ROI and are supported by a mature ecosystem of enterprise vendors and integration frameworks.

By Offering

Hardware is the largest Offering segment at 38.7% of the market in 2025. The proliferation of AI-specific chips – including NVIDIA's H100/H200 GPUs, Google's TPU v5, and AMD's Instinct MI300X – has created robust demand. Data center build-outs by hyperscalers and sovereign AI initiatives sustain hardware procurement at scale.

Regional Market Insights

|

Region |

Market Share (2025) |

Key Drivers |

Major AI Hubs |

|

Northeast |

29.7% |

BFSI AI, academic research clusters, healthtech AI, defense contracts |

New York City, Boston, Washington D.C. |

|

West |

27.4% |

Big Tech HQs, venture capital, GenAI startups, autonomous vehicles |

San Francisco Bay Area, Seattle, Los Angeles |

|

South |

24.1% |

Aerospace AI, energy sector analytics, cybersecurity AI, smart cities |

Austin, Atlanta, Dallas, Miami |

|

Midwest |

18.8% |

Manufacturing AI, agri-tech, smart logistics, automotive AI adoption |

Chicago, Detroit, Columbus, Minneapolis |

Northeast – 29.7% Market Share (2025)

The Northeast leads the United States artificial intelligence market with a 29.7% revenue share in 2025. New York City is the foremost financial AI hub – JPMorgan Chase, Goldman Sachs, and Citigroup deploy AI in algorithmic trading, risk assessment, and compliance automation. Boston's Route 128 corridor hosts MIT, Harvard, and Northeastern University AI research alongside a mature biotech AI ecosystem. Total AI investment in the Northeast exceeded USD 14 Billion in 2024.

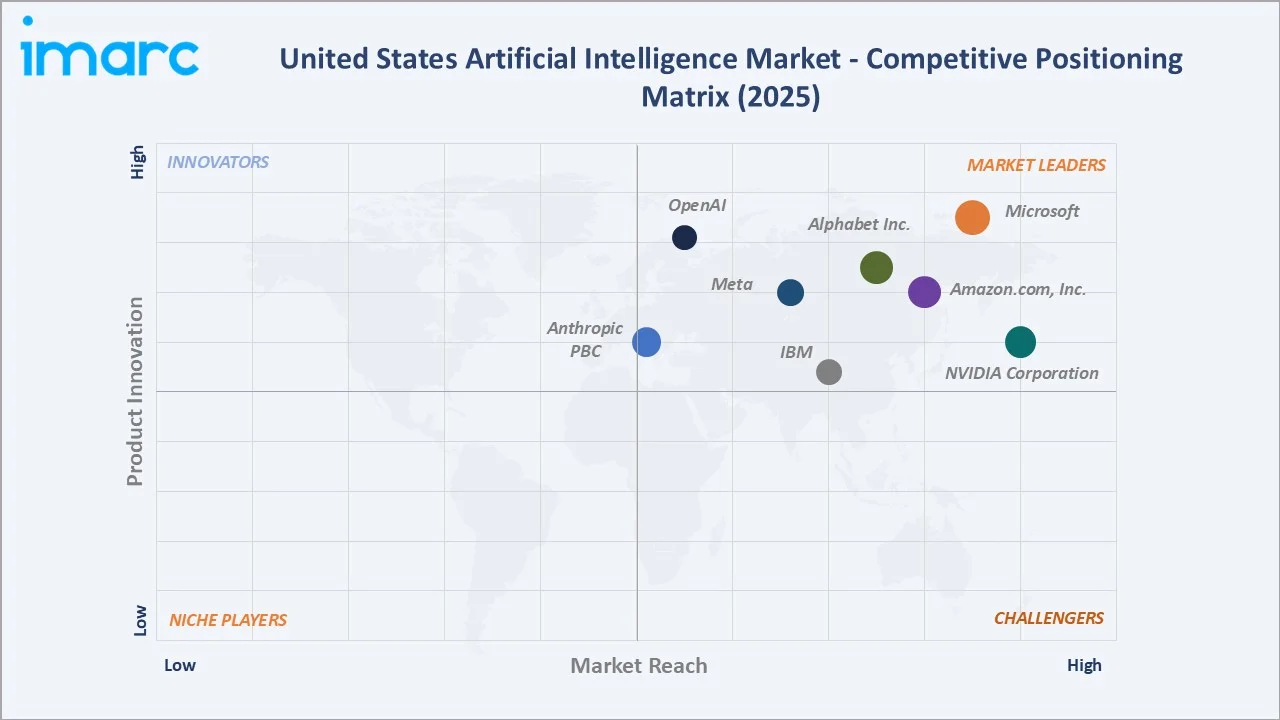

Competitive Landscape

The United States AI market features an oligopolistic core of large technology conglomerates alongside a vibrant, innovation-driven startup ecosystem. The top five players – Microsoft, Alphabet Inc., Amazon.com, Inc., NVIDIA Corporation, Meta – collectively account for approximately 55-60% of total market revenues in 2025. Intense competition is driving rapid model performance improvements, cost reductions, and vertical-specific AI solution development.

|

Company Name |

Brand / Product Line |

Market Position |

Core Strength |

|

Microsoft |

Microsoft Copilot |

Market Leader |

Enterprise AI integration, cloud AI infrastructure, M365 AI productivity suite |

|

Alphabet Inc. |

Gemini |

Market Leader |

Foundation models, Search AI, cloud AI services, DeepMind research excellence |

|

Amazon.com, Inc. |

SageMaker |

Market Leader |

Cloud AI infrastructure, ML platform-as-a-service, custom AI silicon development |

|

NVIDIA Corporation |

CUDA |

Market Leader |

AI hardware, GPU compute infrastructure, full-stack AI platform ecosystem |

|

Meta |

Llama / Meta AI |

Strong Challenger |

Open-source LLMs, social AI, AR/VR AI, multimodal foundation model research |

|

IBM |

IBM Watson / Granite Models |

Established Player |

Enterprise AI, hybrid cloud, AI governance and regulatory compliance tools |

|

OpenAI |

ChatGPT / GPT-4o / o1 |

Disruptive Innovator |

Frontier LLMs, AGI research, generative AI API platform, DALL-E, Sora |

|

Anthropic PBC |

Claude AI |

Disruptive Innovator |

Constitutional AI, safety-first LLMs, enterprise API, interpretability research |

Key Company Profiles

Alphabet Inc.

Alphabet Inc. is a U.S.-based multinational technology conglomerate and the parent company of Google. Headquartered in Mountain View, California, USA, Alphabet operates across a wide range of industries including digital advertising, cloud computing, artificial intelligence, consumer electronics, and autonomous driving.

- Product & Platform Portfolio: Google Cloud AI, Gemini Ultra/Pro/Nano/1.5 Pro, Vertex AI, Google Search AI Overview, Waymo autonomous driving AI, DeepMind AlphaFold 3, and NotebookLM.

- Recent Developments: In 2024, Google announced its next-generation AI model, Gemini 1.5, marking a major upgrade in performance and efficiency. CEO Sundar Pichai highlighted that the model achieves comparable quality to Gemini 1.0 Ultra but with lower compute usage, signaling improved cost-efficiency.

- Strategic Focus: Investing in multimodal AI, quantum AI, and edge AI via custom TPUs to maintain superiority in AI research and cloud infrastructure through the forecast period.

NVIDIA Corporation

NVIDIA Corporation is a leading U.S.-based technology company specializing in graphics processing units (GPUs), artificial intelligence (AI), and high-performance computing. Headquartered in Santa Clara, California, USA, NVIDIA initially gained prominence in gaming through its GeForce GPUs but has since evolved into a dominant player in AI and data center technologies.

- Product & Platform Portfolio: H100/H200/B100/B200 GPUs, CUDA AI framework, DGX SuperPOD systems, NVIDIA AI Enterprise software, NIM microservices, and Jetson edge AI platform.

- Recent Developments: In 2024, NVIDIA has unveiled its next-generation Blackwell GPU architecture, aimed at accelerating AI, data centers, and high-performance computing workloads. The launch signals NVIDIA’s push to dominate the AI computing market, enabling enterprises to handle increasingly complex large language models and data workloads.

- Strategic Focus: Positioning as a full-stack AI computing platform covering hardware, software, and services while expanding from data centers to sovereign AI, robotics, and automotive markets.

OpenAI

OpenAI is a U.S.-based artificial intelligence organization focused on developing advanced AI systems and ensuring they are safe and beneficial for society. Headquartered in San Francisco, California, USA. The company is best known for its generative AI models, including the GPT series (such as ChatGPT) and multimodal systems capable of understanding and generating text, images, and audio.

- Product & Platform Portfolio: ChatGPT, GPT-4o, o1/o3 reasoning models, DALL-E 3, Sora video generation, OpenAI API, Assistants API, Custom GPTs, Whisper speech recognition, and Codex.

- Recent Developments: In 2024, OpenAI introduced GPT-4o, its new flagship AI model capable of processing text, audio, and vision in real time. The model delivers GPT-4–level intelligence with significantly faster response times, improving usability for conversational and multimodal applications.

- Strategic Focus: Scaling API platform for enterprise, developing autonomous AI agents, pursuing AGI with safety-first research, and expanding Sora for video AI applications globally.

Market Concentration Analysis

The United States AI market exhibits a moderately concentrated competitive structure. The top five players – Microsoft, Alphabet Inc., Amazon.com, Inc., NVIDIA Corporation, Meta – collectively account for approximately 55-60% of total market revenues in 2025.

Market fragmentation is most evident in the AI software and services layers, where thousands of startups compete in narrow verticals such as legal AI, healthcare AI, and manufacturing AI.

Consolidation trends are accelerating through M&A activity. In recent years, AI deal-making has surged significantly in overall transaction value. Notable transactions include Amazon’s investment in Anthropic, Microsoft’s acquisition of Inflection AI talent, and Google’s talent acquisition from Character.AI. This consolidation wave is expected to intensify through the coming years.

Investment & Growth Opportunities

Fastest Growing Segments

General/Strong AI represents the fastest-growing investment frontier, with AGI-focused startups attracting significant venture and strategic funding in recent years. Healthcare AI—particularly diagnostics, drug discovery, and clinical decision support—presents the most immediately monetizable opportunity, with strong double-digit growth projected over the next decade.

Emerging Markets & White Spaces

Edge AI in industrial manufacturing represents a significant untapped opportunity by the end of the decade. Agricultural AI—covering precision farming, crop disease prediction, and autonomous harvesting—is projected to see substantial growth in the U.S. over the same period. Defense AI contracts also represent large-scale award pipelines for vendors under next-generation frameworks succeeding JEDI.

Venture Investment Trends

U.S. AI startups raised substantial venture capital in 2024, accounting for a significant share of global AI investment. Generative AI companies attracted the largest portion of funding, followed by enterprise AI automation and AI infrastructure segments. Notable raises include xAI’s Series B funding round and Scale AI’s major capital raise.

Future Market Outlook (2026-2034)

The United States Artificial Intelligence market is expected to maintain its global leadership position through the next decade, expanding steadily with strong growth momentum. Midpoint projections indicate a substantial rise by 2030, reflecting sustained structural expansion driven by increasing enterprise adoption and continued R&D investment across both public and private sectors.

Key technological disruptions expected to reshape the market include: (1) AGI-adjacent systems achieving human-level performance across multiple cognitive domains by 2028-2030; (2) quantum-classical hybrid AI systems reducing optimization costs; (3) neuromorphic chips enabling ultra-low-power AI inference for IoT and wearables; and (4) multimodal AI agents capable of reasoning and acting across text, image, audio, and physical-world data.

The broader AI transformation of the United States economy is expected to generate substantial economic value by the end of the decade, according to McKinsey Global Institute. Key sectors such as financial services, healthcare, and manufacturing are likely to see the most significant disruption and productivity gains. At the same time, the U.S. faces intensifying geopolitical competition in AI, necessitating sustained large-scale investments.

Research Methodology

Primary Research

IMARC Group's primary research methodology encompasses structured interviews and surveys with over 250 industry stakeholders including AI solution providers, enterprise AI buyers, technology executives, and government AI policy officials. Respondents are selected across all geographic regions and market segments to ensure representative coverage. Primary data accounts for 35% of final model inputs.

Secondary Research

Secondary research draws from authoritative sources including SEC filings, US Bureau of Labor Statistics, National Science Foundation AI Index, DARPA program documentation, CBO technology assessments, industry association reports from CompTIA and the AI Now Institute, trade publications, and peer-reviewed academic publications.

Forecasting Models

Market sizing employs a combination of bottom-up demand aggregation by end-use vertical, offering type, and region, alongside top-down revenue decomposition from total addressable market estimates. CAGRs are derived through multivariate regression models incorporating GDP growth, enterprise IT spending indices, AI talent supply indices, and government AI R&D expenditure trajectories.

United States Artificial Intelligence Market Report Coverage

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Narrow/Weak Artificial Intelligence, General/Strong Artificial Intelligence |

| Offerings Covered | Hardware, Software, Services |

| Technologies Covered | Machine Learning, Natural Language Processing, Context-Aware Computing, Computer Vision, Others |

| Systems Covered | Intelligence Systems, Decision Support Processing, Hybrid Systems, Fuzzy Systems |

| End-Use Industries Covered | Healthcare, Manufacturing, Automotive, Agriculture, Retail, Security, Human Resources, Marketing, Financial Services, Transportation and Logistics, Others |

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered | Microsoft, Alphabet Inc., Amazon.com, Inc., NVIDIA Corporation, Meta, IBM, OpenAI, Anthropic PBC, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the United States Artificial Intelligence Market Report

The United States artificial intelligence market was valued at USD 41.53 Billion in 2025. It is growing steadily, driven by enterprise AI adoption, cloud infrastructure expansion, and increasing government AI investment programs across federal and state levels.

The market is projected to reach USD 112.19 Billion by 2034, expanding at a CAGR of 11.67% during 2026-2034. Healthcare, BFSI, and manufacturing sectors will be the primary growth drivers throughout the forecast period.

The United States artificial intelligence market is expected to grow at a CAGR of 11.67% during the forecast period 2026-2034, reflecting sustained demand across enterprise software, hardware, and AI services segments.

Narrow/Weak AI dominates with an 86.4% market share in 2025. Task-specific AI systems for fraud detection, diagnostics, and recommendation engines drive this segment's sustained dominance.

Hardware accounts for 38.7% of total United States artificial intelligence market revenue in 2025. AI-specific chips, GPUs, and data center equipment drive strong hardware demand across cloud and enterprise AI deployments.

The Northeast leads with a 29.7% share in 2025. Dense concentrations of financial institutions, research universities, and health systems anchor the region's AI demand and investment activity.

Key drivers include federal AI policy support, enterprise digital transformation, booming generative AI adoption, healthcare AI spending, and sustained venture investment exceeding USD 50 Billion annually.

Major players include Microsoft, Alphabet Inc., Amazon.com, Inc., NVIDIA Corporation, Meta, IBM, OpenAI, and Anthropic PBC.

General/Strong AI is the fastest-growing Type segment at approximately 14.2% CAGR. Healthcare AI and defense AI are the fastest-growing end-use verticals through the forecast period.

Key challenges include AI bias and data privacy risks, high training infrastructure costs exceeding USD 100 Million per frontier model, workforce displacement concerns, and evolving federal AI regulations.

The United States artificial intelligence market was valued at USD 23.92 Billion in 2020. It grew to USD 41.53 Billion by 2025, representing 73.6% cumulative growth driven by pandemic-accelerated digitization and enterprise AI investment.

The report uses primary research with 250+ stakeholder interviews, secondary sources including NSF and DARPA data, and quantitative forecasting models combining bottom-up demand aggregation with macro-economic regression analysis.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)