United States Calcium Chloride Market Size, Share, Trends and Forecast by Application, Product Type, Raw Material, Grade, and Region, 2026-2034

United States Calcium Chloride Market Size, Share, Trends & Forecast (2026-2034)

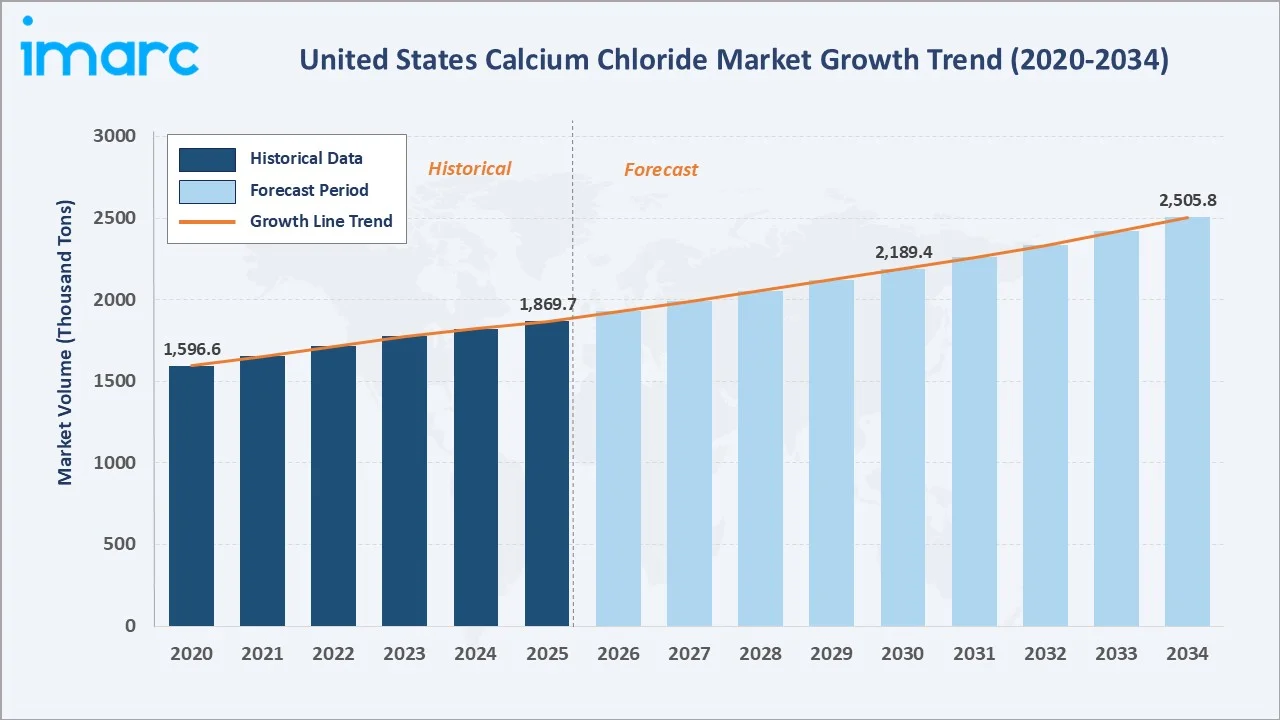

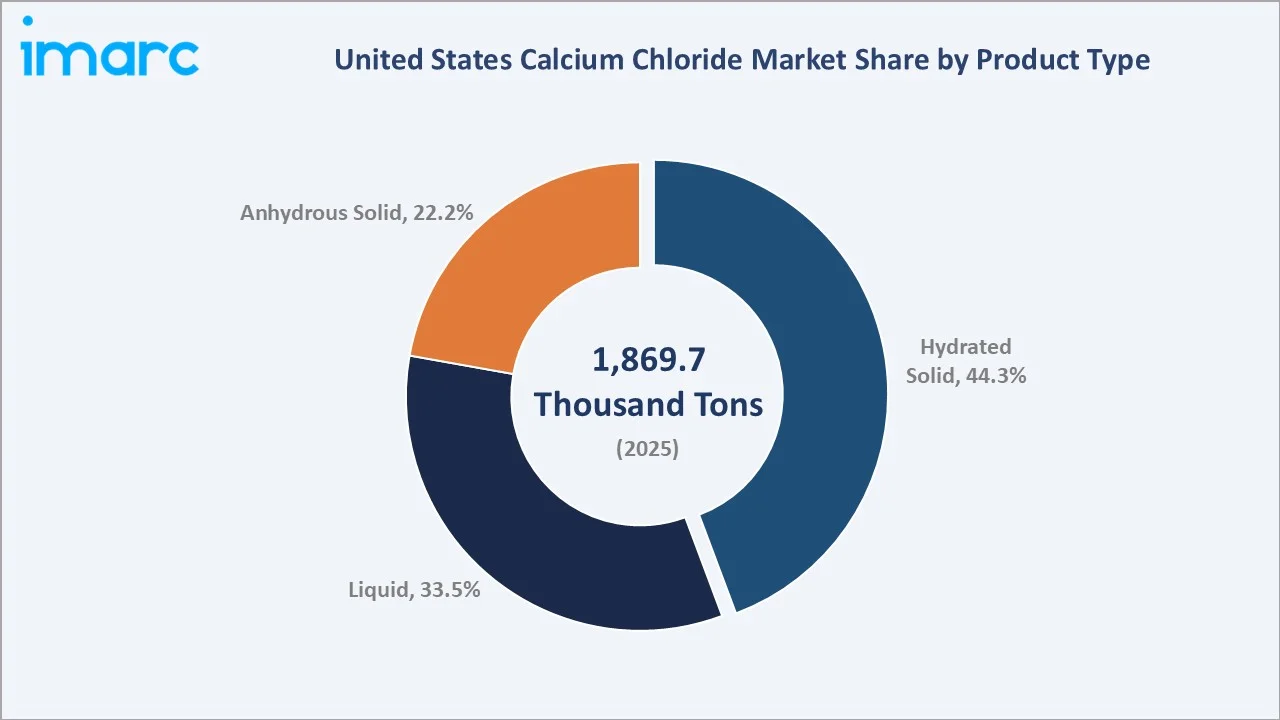

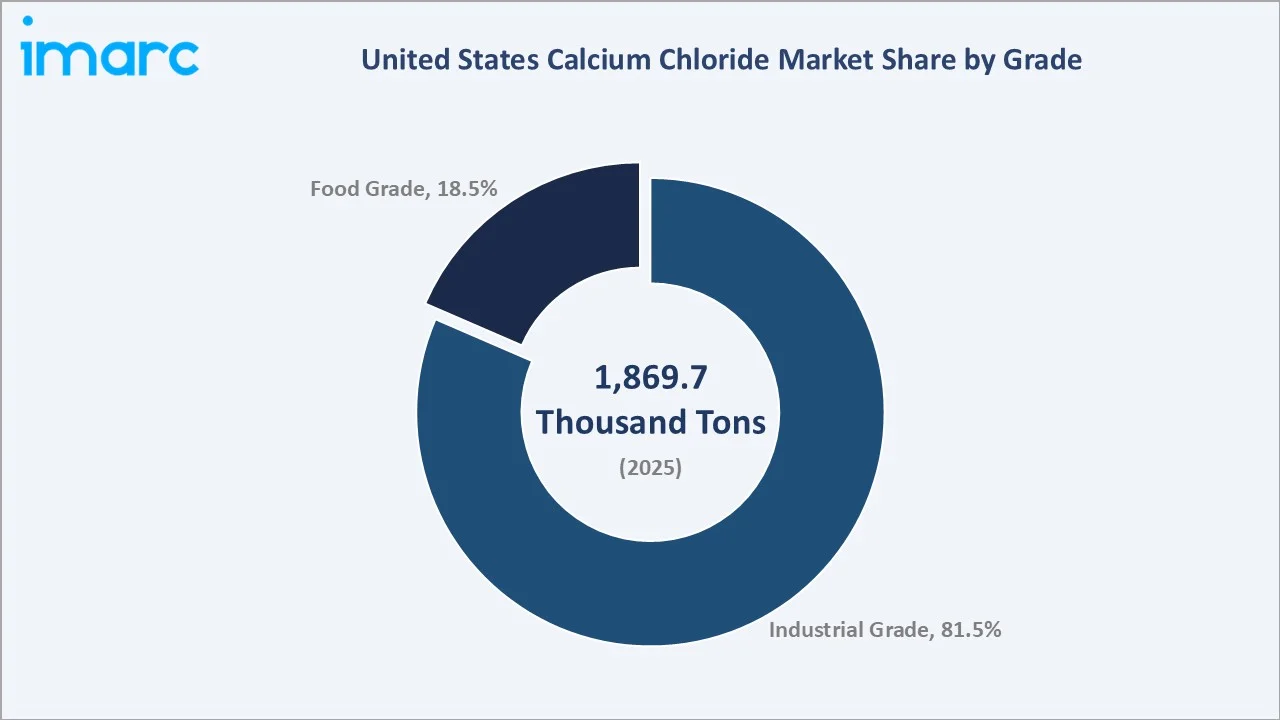

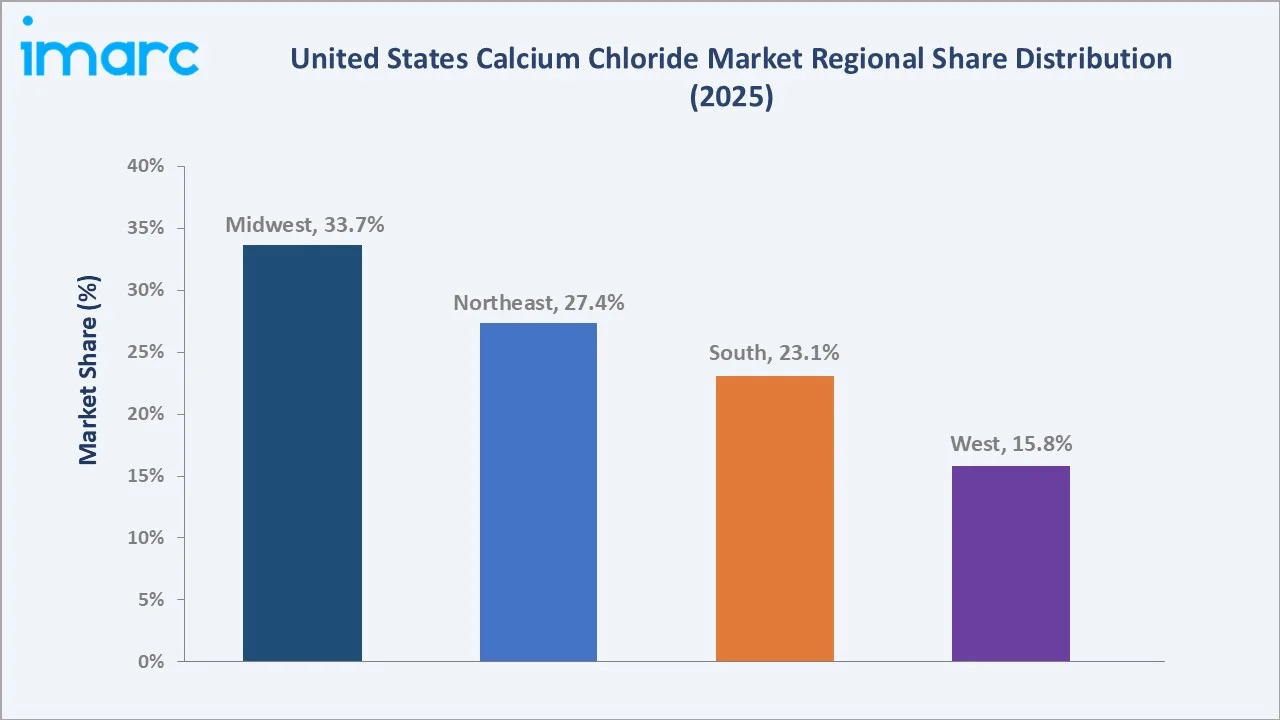

The United States calcium chloride market reached 1,869.7 Thousand Tons in 2025 and is projected to reach 2,505.8 Thousand Tons by 2034, growing at a CAGR of 3.21% during 2026-2034. The market is driven by strong demand from de-icing and dust-control applications, supported by cold-weather road maintenance needs and infrastructure activity. In 2025, the United States exported calcium chloride worth USD 176 Million, ranking it as the country’s 1,133rd most exported product out of 5,527 products. During the same year, the US imported calcium chloride valued at USD 71.5 Million, making it the 2,398th most imported product out of 5,494 products. This trade surplus indicates strong domestic production capacity and international competitiveness. Hydrated solid leads product type at 44.3%. Industrial grade leads at 81.5%. Midwest leads regionally at 33.7%.

Market Snapshot

|

Metric |

Value |

|

Market Volume (2025) |

1,869.7 Thousand Tons |

|

Forecast Market Volume (2034) |

2,505.8 Thousand Tons |

|

CAGR (2026-2034) |

3.21% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Product Type |

Hydrated Solid (44.3%, 2025) |

|

Dominant Grade |

Industrial Grade (81.5%, 2025) |

|

Leading Region |

Midwest (33.7%, 2025) |

The US calcium chloride (CaCl2) market grew steadily from 1,596.6 Thousand Tons in 2020 to 1,869.7 Thousand Tons in 2025, supported by strong demand from de-icing, dust control, oil and gas, construction, and industrial applications. The market is expected to reach 2,189.4 Thousand Tons by 2030, indicating continued expansion across infrastructure and winter road-maintenance activities. By 2034, consumption is forecast to rise to 2,505.8 Thousand Tons, reflecting stable long-term demand from municipal, industrial, and energy-sector users. This growth trajectory highlights calcium chloride’s importance as a versatile chemical across transportation, construction, and process industries.

To get more information on this market, Request Sample

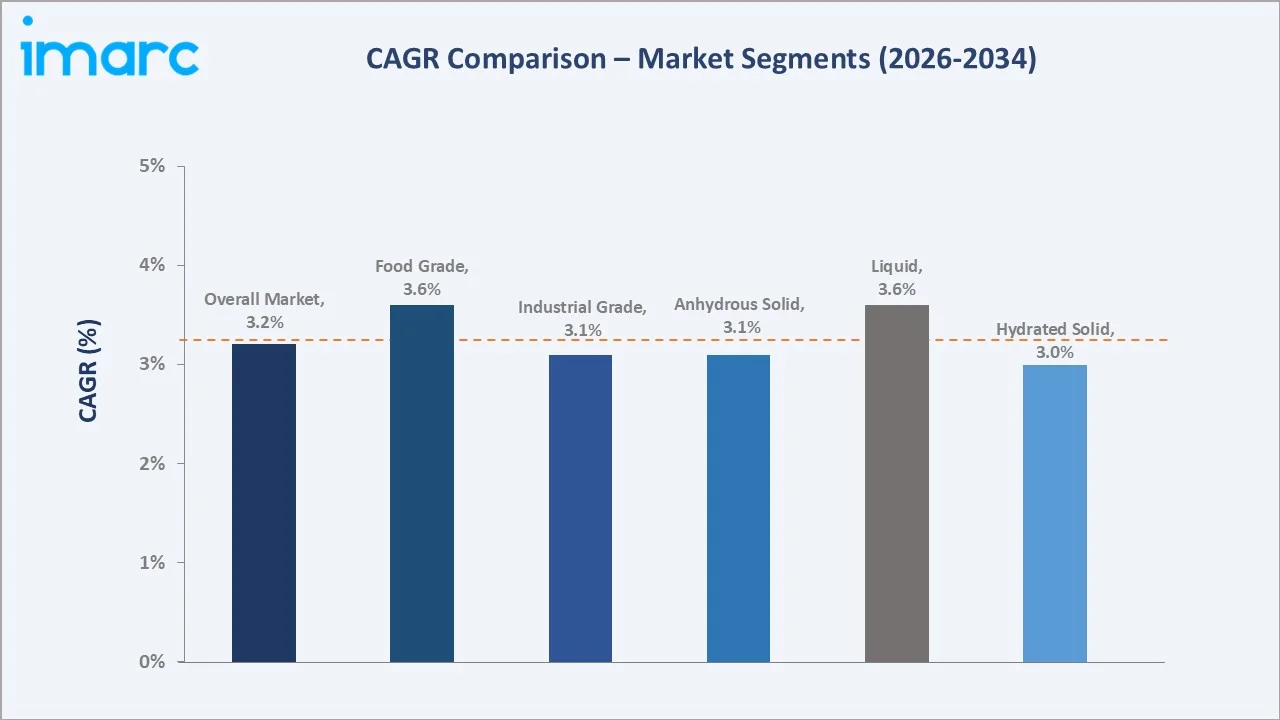

Liquid CaCl2 grows fastest at ~3.6% CAGR through liquid de-icing pre-wetting systems, oil and gas completion brine, and concrete curing fluid. Food grade grows at ~3.6% CAGR through cheese manufacturing, tofu, and food preservation.

Executive Summary

The United States calcium chloride market is expanding steadily, supported by demand from de-icing, dust control, oil and gas, construction, and industrial applications. Market volume increased from 1,596.6 Thousand Tons in 2020 to 1,869.7 Thousand Tons in 2025 and is projected to reach 2,505.8 Thousand Tons by 2034. Strong domestic production and export activity indicate a competitive supply base. Long-term growth will be driven by infrastructure development, winter road maintenance, and industrial processing demand. Hydrated solid at 44.3% leads through flake and pellet road de-icing. Industrial grade at 81.5% leads through road, oil and gas, and construction. Midwest leads regionally at 33.7% through Michigan's natural brine production.

Key Market Insights

|

Insight |

Data |

|

Dominant Product Type |

Hydrated Solid - 44.3% share (2025) |

|

Dominant Grade |

Industrial Grade - 81.5% market share (2025) |

|

Leading Region |

Midwest - 33.7% share (2025) |

|

Market Opportunity |

Liquid CaCl2 smart de-icing fleet pre-wet system; food grade cheese and tofu; dust suppression for unpaved roads; concrete acceleration infrastructure; EV battery electrolyte |

Key Analytical Observations Supporting The Above Data:

- Hydrated Solid at 44.3%: The hydrated solid is dominant due to its ease of handling, storage, transport, and application across de-icing, dust control, and industrial uses. Its longer shelf life and higher stability make it preferred over liquid forms in bulk commercial applications.

- Industrial Grade at 81.5%: The industrial grade is dominant due to its wide use in oil and gas drilling, construction, water treatment, dust control, and chemical processing. Its cost-effectiveness and suitability for bulk industrial applications support strong demand.

- Midwest at 33.7%: The Midwest region is dominant due to its harsh winter climate, which creates strong demand for calcium chloride in road de-icing and snow-control applications. The region’s industrial, construction, and agricultural activities also support steady consumption.

United States Calcium Chloride Market Overview

The United States calcium chloride market is produced through two primary manufacturing routes: natural brine extraction and the Solvay process byproduct. US calcium chloride is classified by concentration: above-94-97%-anhydrous-solid (highest purity), above-77-80%-granule-pellet, above-74-77%-flake-dihydrate, and above-28-45%-liquid-solution. Macroeconomic factors include rising infrastructure spending, road maintenance budgets, industrial production, and oil and gas activity.

Market Dynamics

To evaluate market opportunities, Request Sample

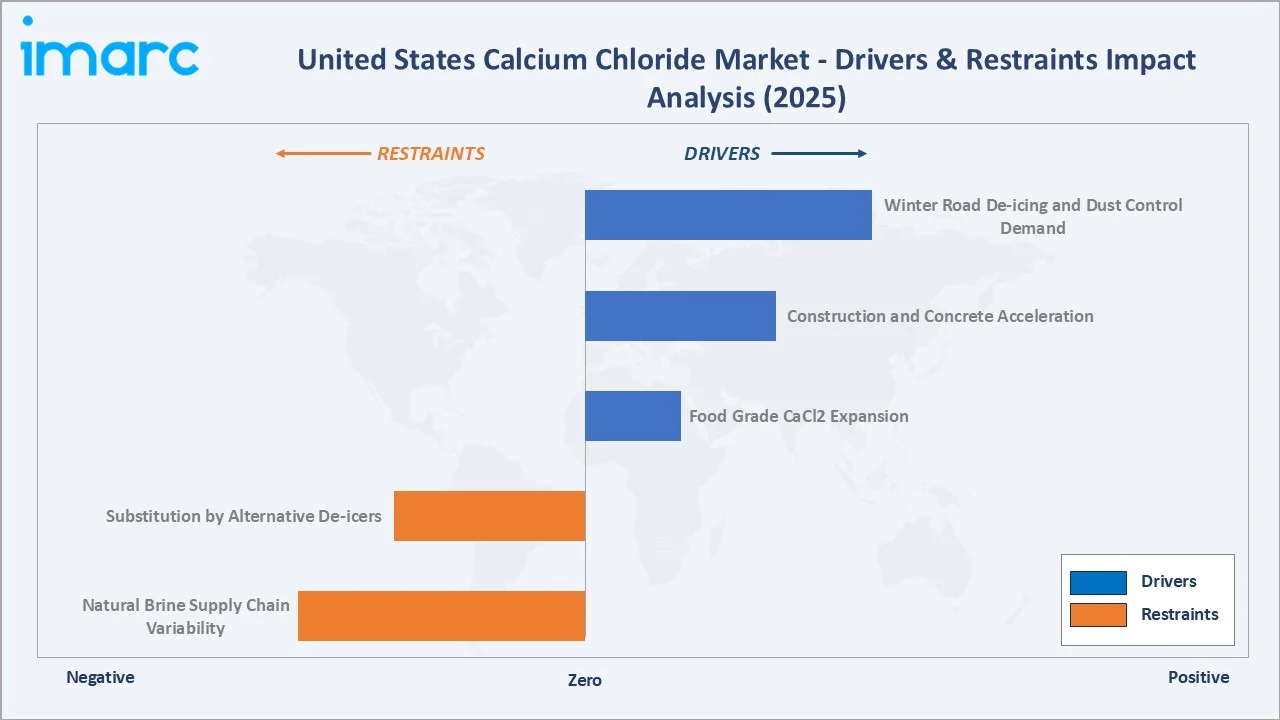

Market Drivers

- Winter Road De-icing and Dust Control Demand: Winter road de-icing and dust control demand is a major driver due to its strong effectiveness in melting ice at low temperatures and reducing road hazards. The United States consumes roughly 20 million tonnes of de-icing salt annually. In warmer and dry regions, it is also used for dust suppression on unpaved roads, construction sites, mining areas, and industrial yards. These recurring seasonal and infrastructure-related applications create stable, high-volume demand for calcium chloride across the country.

- Construction and Concrete Acceleration: Construction and concrete acceleration are driving the market as calcium chloride is widely used as a concrete accelerator to speed up setting and early strength development. This is especially useful in cold-weather construction, where low temperatures can delay curing and project timelines. The US construction sector is a key pillar of the economy, with over 919,000 construction establishments operating in the first quarter of 2023. The industry generates nearly USD 2.1 trillion worth of structures annually. Rising infrastructure, commercial, and industrial construction activity therefore strengthens demand for calcium chloride-based concrete additives.

- Food Grade CaCl2 Expansion: Food-grade CaCl2 expansion is driving the market as its use grows in food processing, beverage production, and preservation applications. It is widely used as a firming agent, stabilizer, electrolyte, and calcium fortification ingredient in products such as canned vegetables, cheese, pickles, beverages, and sports drinks. Rising demand for processed, packaged, and convenience foods is supporting higher consumption of food-grade calcium chloride. Its role in improving texture, shelf life, and product quality makes it an important growth area within the market.

Market Restraints

- Substitution by Alternative De-icers: Municipalities and commercial users may shift toward lower-cost or application-specific options such as rock salt, magnesium chloride, potassium acetate, and blended de-icing formulations. These alternatives can reduce calcium chloride demand in price-sensitive road maintenance budgets. Environmental concerns, corrosion issues, and procurement preferences also influence buyers to evaluate substitutes. As a result, calcium chloride suppliers face pricing pressure and must emphasize performance advantages such as low-temperature effectiveness and faster ice melting.

- Natural Brine Supply Chain Variability: Calcium chloride production often depends on brine extraction and processing. Changes in brine availability, mineral concentration, weather conditions, and extraction efficiency can affect output consistency. Supply disruptions may lead to price volatility, delayed deliveries, and higher production costs for manufacturers. This creates challenges for end users in de-icing, oil and gas, construction, and industrial applications that require a reliable bulk supply.

Market Opportunities

- Export Growth to International Markets: In 2025, the United States exported USD 176 Million worth of calcium chloride, ranking it as the country’s 1,133rd most exported product among 5,527 products. The leading export destinations were Mexico at USD 129 Million, Canada at USD 42.8 Million, followed by Brazil, South Korea, and the United Kingdom. Between 2024 and 2025, the fastest-growing export markets were Mexico, Canada, and South Korea. This export growth to international markets is an opportunity, as strong domestic production capacity enables suppliers to serve demand beyond local consumption. Growing infrastructure, oil and gas, dust control, and industrial applications in overseas markets create room for U.S. producers to expand sales.

- Growth in Oil and Gas Drilling Applications: Growth in oil and gas drilling applications presents a strong opportunity, as CaCl₂ is widely used in drilling fluids, completion fluids, and workover operations. It helps control fluid density, stabilize wellbores, reduce clay swelling, and improve drilling efficiency. Rising shale activity and well-maintenance operations can increase demand for industrial-grade calcium chloride. This creates opportunities for suppliers to serve energy producers with reliable bulk and high-purity calcium chloride solutions.

Market Challenges

- Environmental and Corrosion Concerns: Environmental and corrosion concerns are challenging as excessive use can contribute to soil and water salinity, affecting nearby vegetation and ecosystems. Calcium chloride can also accelerate corrosion of vehicles, bridges, road infrastructure, and metal equipment when not properly managed. These concerns have encouraged some municipalities and industries to evaluate alternative de-icing products and corrosion-mitigation strategies. As environmental regulations and sustainability requirements become stricter, calcium chloride suppliers may face additional compliance and product-performance challenges.

- Seasonal Demand Fluctuations: Seasonal demand fluctuations are a challenge as a significant portion of consumption is tied to winter de-icing activities. Mild winters with lower snowfall and ice accumulation can substantially reduce demand from municipalities, transportation agencies, and commercial users. This creates uncertainty in sales volumes, inventory management, and production planning for suppliers. Dependence on weather-driven demand can also lead to revenue volatility and uneven capacity utilization across the industry.

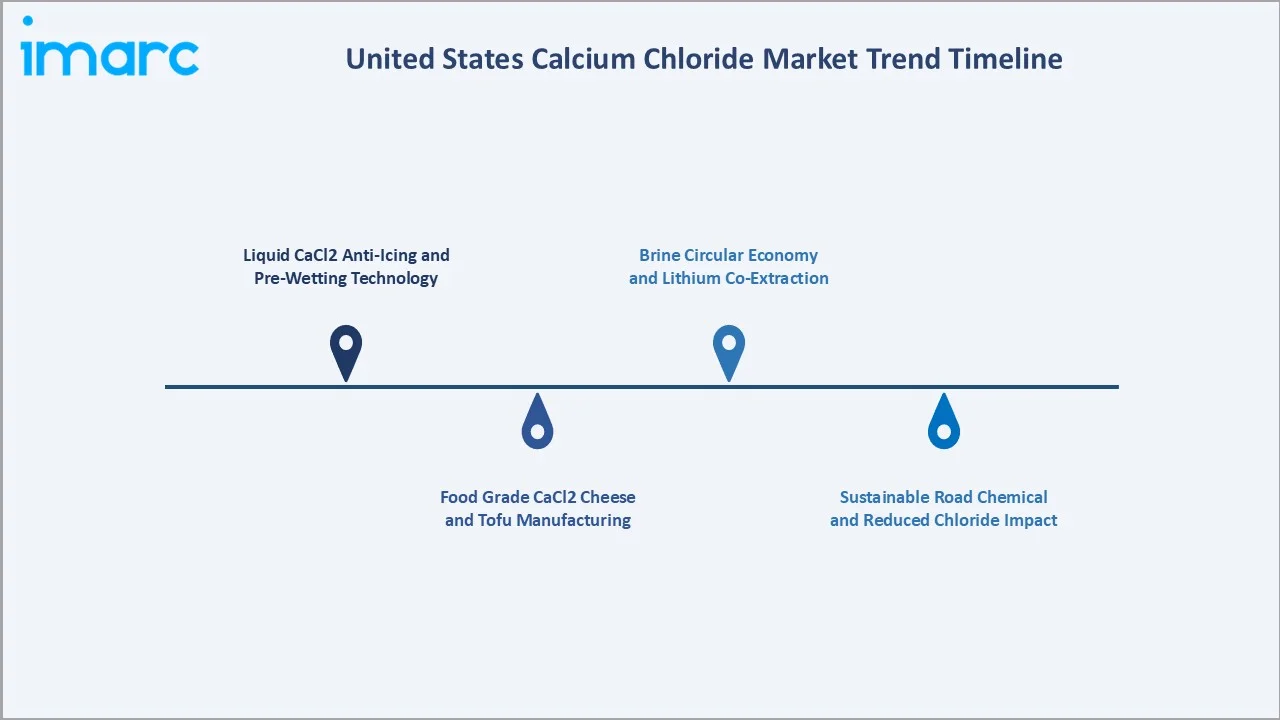

Emerging Market Trends

1. Liquid CaCl2 Anti-Icing and Pre-Wetting Technology

Liquid CaCl2 anti-icing and pre-wetting technology is emerging due to its ability to improve winter road maintenance efficiency. Transportation agencies increasingly apply liquid calcium chloride before snow and ice events to prevent ice bonding and enhance roadway safety. It is also used to pre-wet rock salt, improving salt adhesion, reducing material usage, and accelerating ice melting performance. The technology helps lower maintenance costs, optimize de-icer consumption, and support more effective snow and ice management strategies.

2. Food Grade CaCl2 Cheese and Tofu Manufacturing

Per capita consumption of natural cheese in the United States reached 39.9 pounds in 2024, encouraging dairy processors to use reliable food-grade additives that enhance yield and product quality. In cheese production, calcium chloride helps restore calcium balance in pasteurized milk, improving curd formation and consistency. In tofu manufacturing, it acts as a coagulant that supports firm texture and better product quality. Rising demand for processed dairy, plant-based foods, and high-protein convenience products is supporting the growth of food-grade calcium chloride applications.

3. Sustainable Road Chemical and Reduced Chloride Impact

Sustainable road chemicals and reduced chloride impact are emerging as municipalities seek safer and more environmentally responsible winter-maintenance solutions. Suppliers are focusing on optimized liquid formulations, pre-wetting technologies, corrosion inhibitors, and blended products that reduce total chloride application while maintaining ice-melting performance. This trend is driven by concerns over soil salinity, water contamination, infrastructure corrosion, and vehicle damage. As sustainability standards rise, calcium chloride solutions that deliver lower application rates and reduced environmental impact are gaining stronger market relevance.

4. Brine Circular Economy and Lithium Co-Extraction

Brine circular economy and lithium co-extraction are emerging as producers look to maximize value from mineral-rich brine resources. Calcium chloride can be recovered as a useful by-product while extracting lithium and other minerals, improving resource efficiency and reducing waste. This approach supports circular-economy goals by turning brine streams into multiple commercial products. As demand for lithium rises due to batteries and clean energy storage, integrated brine processing could create new supply opportunities for calcium chloride producers.

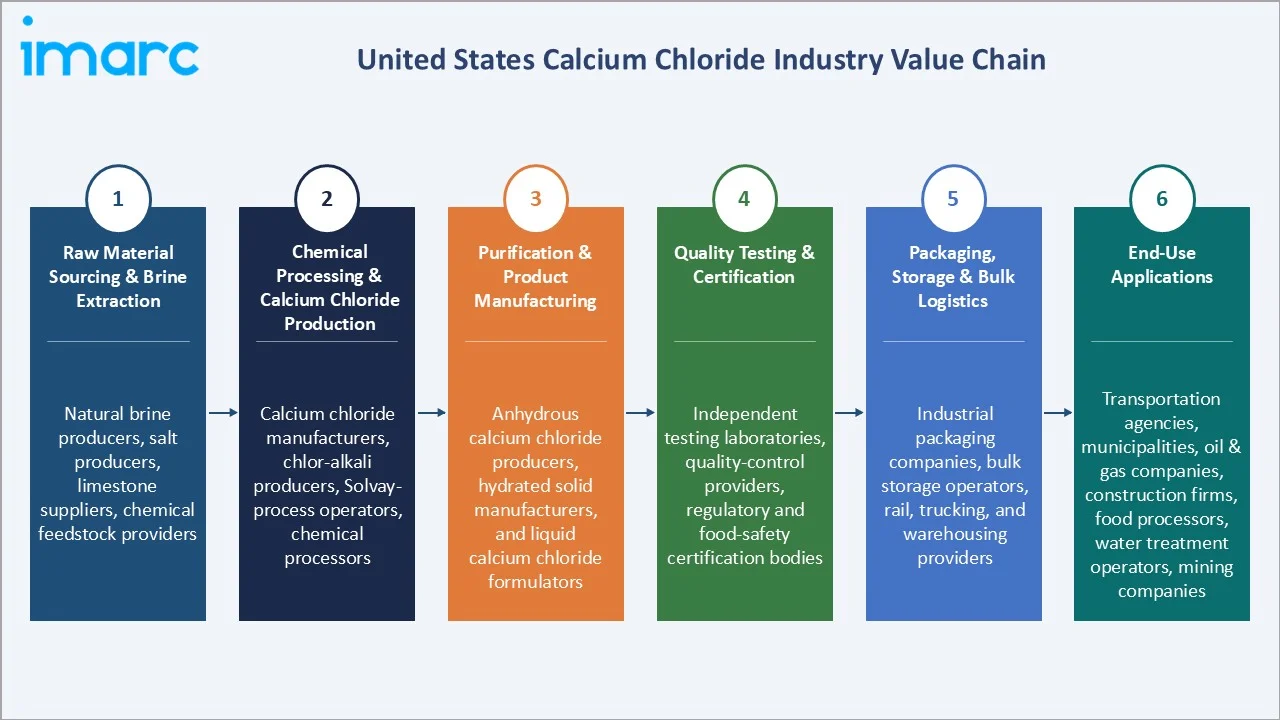

Industry Value Chain Analysis

The United States calcium chloride value chain integrates raw material sourcing & brine extraction, chemical processing & calcium chloride production, purification & product manufacturing, quality testing & certification, packaging, storage & bulk logistics, and end-use applications.

|

Stage |

Key Participants |

|

Raw Material Sourcing & Brine Extraction |

Natural brine producers, salt producers, limestone suppliers, chemical feedstock providers |

|

Chemical Processing & Calcium Chloride Production |

Calcium chloride manufacturers, chlor-alkali producers, Solvay-process operators, chemical processors |

|

Purification & Product Manufacturing |

Anhydrous calcium chloride producers, hydrated solid manufacturers, and liquid calcium chloride formulators |

|

Quality Testing & Certification |

Independent testing laboratories, quality-control providers, regulatory and food-safety certification bodies |

|

Packaging, Storage & Bulk Logistics |

Industrial packaging companies, bulk storage operators, rail, trucking, and warehousing providers |

|

End-Use Applications |

Transportation agencies, municipalities, oil & gas companies, construction firms, food processors, water treatment operators, mining companies |

The chemical processing, purification, and product manufacturing stage represents the highest value-added segment of the value chain. At this stage, raw brine and chemical feedstocks are converted into high-purity anhydrous, hydrated, and liquid calcium chloride products tailored for specific industrial, food-grade, and de-icing applications. Product quality, purity levels, formulation expertise, and regulatory compliance significantly enhance product value and profitability.

Technology Landscape in the United States Calcium Chloride Industry

Natural Brine Extraction Technology

Natural brine extraction technology is improving the efficiency and sustainability of raw material sourcing. Advanced extraction, brine concentration, and purification systems help maximize calcium recovery while reducing energy consumption and operational costs. Digital monitoring and process automation are also enhancing resource management and production consistency. These innovations support a reliable calcium chloride supply while aligning with environmental and circular-economy objectives.

Liquid CaCl2 Application Technology

Liquid CaCl2 application technology improves the efficiency of de-icing, anti-icing, and dust-control operations. Advanced spray systems, precision application equipment, and pre-wetting technologies enable more uniform distribution and optimized chemical usage. These solutions help reduce material consumption, lower operating costs, and enhance road safety during winter conditions. Growing adoption of smart road-maintenance practices is further driving innovation in liquid calcium chloride application systems.

Solvay Process and By-Product Recovery Technology

Solvay process and by-product recovery technology enable efficient recovery of calcium chloride generated during soda ash production. Advanced separation, concentration, and purification systems help convert by-products into valuable commercial-grade calcium chloride, improving resource utilization and reducing waste. These technologies lower production costs while supporting sustainable manufacturing practices. Continued improvements in process efficiency and recovery rates are strengthening the competitiveness of domestic calcium chloride production.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Application |

De-Icing |

🔒 |

2025 |

|

Product Type |

Hydrated Solid |

44.3% |

2025 |

|

Raw Material |

Natural Brine |

🔒 |

2025 |

|

Grade |

Industrial Grade |

81.5% |

2025 |

|

Region |

Midwest |

33.7% |

2025 |

By Product Type

Hydrated solid leads at 44.3% (2025), flake and pellet forms for road de-icing, dust suppression, and food grade applications.

To access detailed market analysis, Request Sample

Liquid CaCl2 at 33.5% grows fastest at ~3.6% CAGR through liquid road de-icing pre-wetting and concrete curing fluid. Anhydrous solid at 22.2% reflects the highest-purity CaCl2 for industrial desiccant, natural gas pipeline dehydration, and refrigeration brine applications.

By Grade

Industrial grade leads at 81.5% (2025), through road de-icing, dust suppression, oil and gas completion brine, construction concrete, and industrial refrigeration.

Food grade at 18.5% grows fastest at ~3.6% CAGR through US cheese manufacturing, tofu and plant-based food CaCl2 coagulant, pickle brine firming agent, and beverage mineral fortification.

Regional Market Insights

|

Region |

Share (2025) |

Key US Calcium Chloride Market Drivers & Characteristics |

|

Midwest |

33.7% |

Driven by extensive winter road de-icing requirements, high snowfall levels, strong transportation infrastructure, and significant agricultural and industrial activity. |

|

Northeast |

27.4% |

Reflects heavy demand for snow and ice control on highways, municipal roads, airports, and commercial properties, supported by dense population centers and aging infrastructure. |

|

South |

23.1% |

Supported by calcium chloride use in oil and gas drilling, dust suppression, construction activities, water treatment, and industrial processing applications. |

|

West |

15.8% |

Driven by mining operations, unpaved road dust control, environmental management applications, infrastructure development, and selective winter maintenance requirements in colder states. |

Midwest's 33.7% dominance is supported by strong winter de-icing demand, frequent snowfall, road safety needs, and agricultural applications. Northeast's 27.4% due to dense urban infrastructure, municipal snow-control programs, and airport de-icing requirements.

South's 23.1% driven more by oil and gas drilling, construction, water treatment, and industrial processing uses. West's 15.8% benefits from mining, dust suppression, unpaved road stabilization, and selective winter maintenance in colder mountain states.

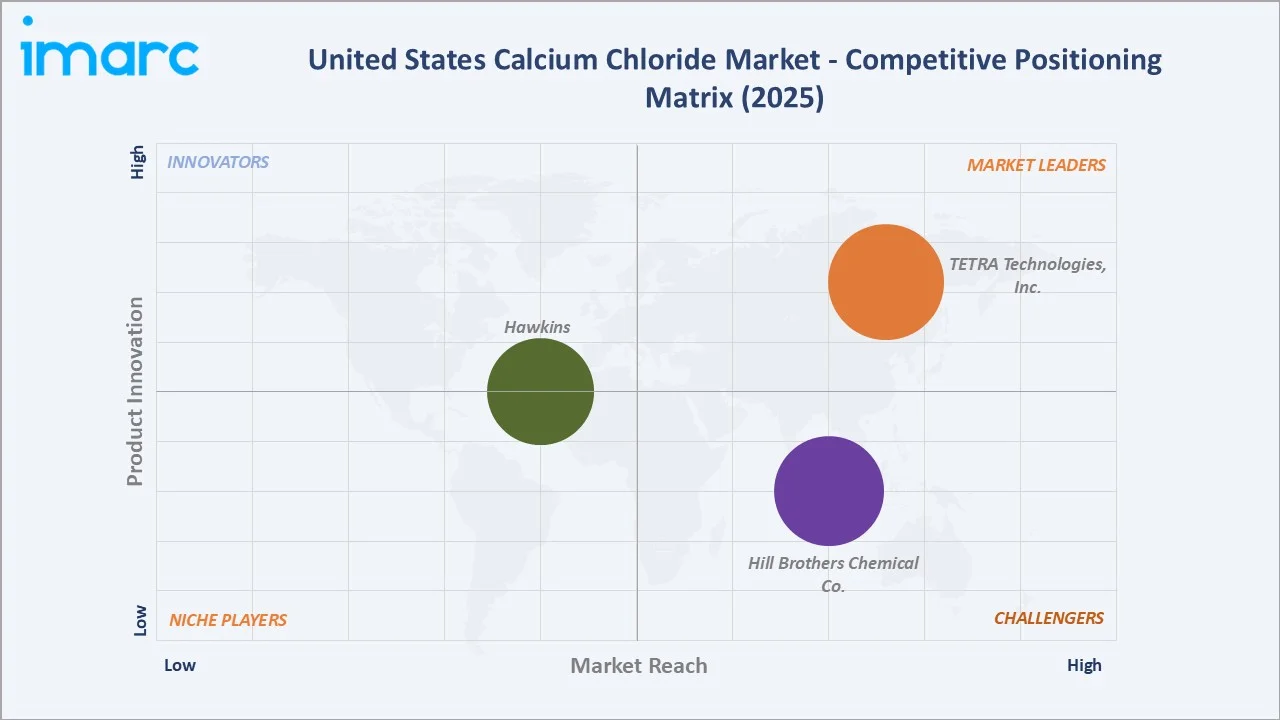

Competitive Landscape

The United States calcium chloride market is moderately concentrated, with competition led by established chemical manufacturers, specialty mineral producers, and regional suppliers. Market participants compete on product purity, production capacity, distribution networks, pricing, and supply reliability across de-icing, industrial, oil and gas, food, and construction applications.

|

Company |

Key Products |

Market Position |

Core Strength |

|

TETRA Technologies, Inc. |

Calcium Chloride Flakes, Liquid Calcium Chloride |

Market Leader |

TETRA Technologies, Inc. is a dominant, vertically integrated domestic producer and marketer of premium-grade calcium chloride for energy, industrial, agricultural, and environmental applications |

|

Hill Brothers Chemical Co. |

Liquid Calcium Chloride, Dry Calcium Chloride |

Challenger |

Hill Brothers Chemical Co. acts as a regional manufacturer and distributor of specialty and commodity chemicals in the Western United States, providing dry and liquid calcium chloride to construction, industrial, oil field, and municipal markets. |

|

Hawkins |

Dry Calcium Chloride, Liquid Calcium Chloride |

Established Player |

Hawkins, Inc. operates as a leading domestic manufacturer, supplier, and distributor of Calcium Chloride (Dry and Liquid) in the U.S. market. The company provides high-purity bulk chemicals to diverse industries. |

Companies are investing in brine extraction efficiency, by-product recovery technologies, and value-added liquid and food-grade calcium chloride products to strengthen their market positions. Strategic focus areas include expanding logistics capabilities, improving sustainability performance, and developing corrosion-inhibited formulations. Long-term customer contracts with municipalities, industrial users, and energy companies further influence competitive dynamics in the market.

Key Company Profiles

TETRA Technologies, Inc.

TETRA Technologies, Inc. is a prominent player in calcium chloride products in the United States, leveraging its extensive brine resources, processing capabilities, and chemical expertise. The company produces and markets calcium chloride in liquid, flake, and food-grade forms for applications including road de-icing, dust control, oil and gas drilling, industrial processing, and construction.

- Key Products: Calcium Chloride Flakes, Liquid Calcium Chloride.

- Strategic Focus: Strengthening its position in the US calcium chloride market through integrated brine resource management, specialty chemical production, and value-added calcium chloride solutions.

Hill Brothers Chemical Co.

Hill Brothers Chemical Co. is a leading specialty chemical distributor and supplier serving industrial, municipal, agricultural, water treatment, and construction markets across the United States. The company offers calcium chloride products in liquid and dry forms for applications such as road de-icing, dust control, concrete acceleration, and industrial processing.

- Key Products: Liquid Calcium Chloride, Dry Calcium Chloride.

- Strategic Focus: Expanding its presence in the US calcium chloride market through efficient chemical distribution, supply-chain reliability, and customer-specific solutions.

Market Concentration Analysis

The United States calcium chloride market exhibits a moderately concentrated structure, with a handful of established producers and distributors accounting for a significant share of total supply. Major participants compete through production capacity, access to brine resources, product quality, logistics networks, and long-term customer relationships. Large integrated manufacturers benefit from vertical integration, while regional distributors strengthen market reach through extensive warehousing and transportation capabilities. Competition is particularly strong in the de-icing, oil and gas, construction, and industrial segments, where supply reliability and pricing are critical purchasing factors. Market consolidation remains moderate, but high capital requirements, resource access, and distribution infrastructure create barriers for new entrants.

Investment & Growth Opportunities

Highest Growth Segments

Liquid CaCl2 (~3.6% CAGR), food grade CaCl2 (~3.6% CAGR through cheese and tofu), West region (~3.8% CAGR), and smart de-icing liquid CaCl2 (~5-6% CAGR from technology adoption) represent the US calcium chloride's highest-growth investment vectors through 2034.

Investment Themes

- Liquid CaCl2 anti-icing and pre-wetting technology: This represents an attractive investment opportunity as transportation agencies increasingly adopt liquid calcium chloride solutions to improve winter road safety and reduce de-icing material consumption. Growth in smart road maintenance programs and demand for cost-effective, environmentally optimized ice-control methods are creating opportunities for specialized application technologies and liquid CaCl₂ supply infrastructure.

- Food grade CaCl2 for US cheese and plant-based food: This opportunity is supported by rising consumption of cheese, plant-based proteins, and processed foods in the United States. Food-grade calcium chloride is widely used for texture enhancement, coagulation, and quality improvement in cheese and tofu production, creating demand for high-purity products and specialized food-processing solutions.

Future Market Outlook (2026-2034)

The United States calcium chloride market is expected to expand from 1,869.7 Thousand Tons in 2025 to 2,505.8 Thousand Tons by 2034, reflecting steady growth at a 3.21% CAGR. Market expansion is being supported by increasing demand from winter road maintenance, dust control, construction, food processing, and oil and gas applications. The projected volume of 2,189.4 Thousand Tons in 2030 marks an important inflection point as advanced liquid anti-icing technologies, food-grade applications, and sustainable chloride management practices gain wider adoption. Continued infrastructure investment and industrial activity are expected to further strengthen long-term consumption across the United States.

Three structural forces define the United States calcium chloride volume growth through 2034. First, sustained demand for winter road de-icing and anti-icing continues to support large-scale consumption by municipalities and transportation agencies. Second, expanding construction, infrastructure, and concrete acceleration activities are increasing the use of calcium chloride in cement and building applications. Third, growing adoption across industrial processing, oil and gas drilling, food-grade applications, and dust-control operations is diversifying demand and supporting steady long-term market expansion.

Research Methodology

Primary Research

Primary research comprised in-depth interviews and discussions with calcium chloride manufacturers, raw material suppliers, distributors, logistics providers, and industry experts across the United States. Insights were also gathered from municipalities, transportation agencies, construction companies, oil and gas operators, and food-processing firms to assess demand patterns, application trends, pricing dynamics, and future growth opportunities.

Secondary Research

Secondary research encompassed company reports, trade databases, government publications, industry associations, technical papers, and regulatory sources related to calcium chloride production and consumption. It also included reviewing import-export data, construction and road-maintenance indicators, oil and gas activity, and food-processing trends.

Forecasting Models

Forecasting models combined historical consumption trends, production volumes, end-use demand indicators, and macroeconomic variables to project market growth through 2034. The analysis incorporated infrastructure spending, winter weather patterns, construction activity, oil and gas drilling trends, and food-processing demand. Both top-down and bottom-up forecasting approaches were used, with scenario analysis applied to assess the impact of climate variability, industrial activity, and technological adoption on future calcium chloride consumption.

United States Calcium Chloride Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Thousand Tons |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Applications Covered | De-Icing, Dust Control and Road Stabilization, Drilling Fluids, Construction, Industrial Processing, Others |

| Product Types Covered | Liquid, Hydrated Solid, Anhydrous Solid |

| Raw Materials Covered | Natural Brine, Solvay Process (by-Product), Limestone and HCL, Others |

| Grades Covered | Food Grade, Industrial Grade |

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered | TETRA Technologies Inc., Hill Brothers Chemical Co., Hawkins, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the United States calcium chloride market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the United States calcium chloride market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the United States calcium chloride industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the United States Calcium Chloride Market Report

The US calcium chloride market reached 1,869.7 Thousand Tons in 2025, driven by strong demand from winter road de-icing, anti-icing, and dust-control applications. Growth is further supported by construction activity, concrete acceleration, oil and gas drilling, and industrial processing uses. Expanding food-grade applications in cheese, tofu, and processed foods also support steady long-term consumption.

The US calcium chloride market grows at 3.21% CAGR during 2026-2034, reaching 2,505.8 Thousand Tons by 2034. The CAGR reflects US road infrastructure demand, construction concrete acceleration, and food grade expansion.

Hydrated solid leads at 44.3% due to its ease of storage, handling, transport, and application across de-icing, dust control, and industrial uses. Its stability, longer shelf life, and suitability for bulk usage make it preferred by municipalities, contractors, and industrial buyers.

Industrial grade leads at 81.5% due to its broad use in de-icing, oil and gas drilling, construction, dust control, and industrial processing. Its cost-effectiveness, bulk availability, and suitability for large-volume applications support its dominant market position.

Midwest leads at 33.7% due to heavy winter snowfall and strong demand for road de-icing and anti-icing applications. Its large transportation network, agricultural base, and industrial activity further support steady calcium chloride consumption.

Leading companies include TETRA Technologies, Inc., Hill Brothers Chemical Co., and Hawkins, among others.

The market is projected to reach approximately 2,189.4 Thousand Tons by 2030, supported by steady demand from de-icing, construction, oil and gas, and industrial applications. This milestone reflects broader adoption of liquid anti-icing technologies, food-grade CaCl₂, and dust-control solutions.

Three priority investment opportunities include liquid CaCl₂ anti-icing and pre-wetting technologies, which improve winter road-maintenance efficiency; food-grade calcium chloride for cheese and plant-based food manufacturing, driven by growing food-processing demand; and advanced brine recovery and by-product utilization technologies, which enhance resource efficiency and support sustainable calcium chloride production.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)