United States CBD Pouches Market Size, Share, Trends and Forecast by Content, Type, Distribution Channel, and Region, 2026-2034

United States CBD Pouches Market Summary:

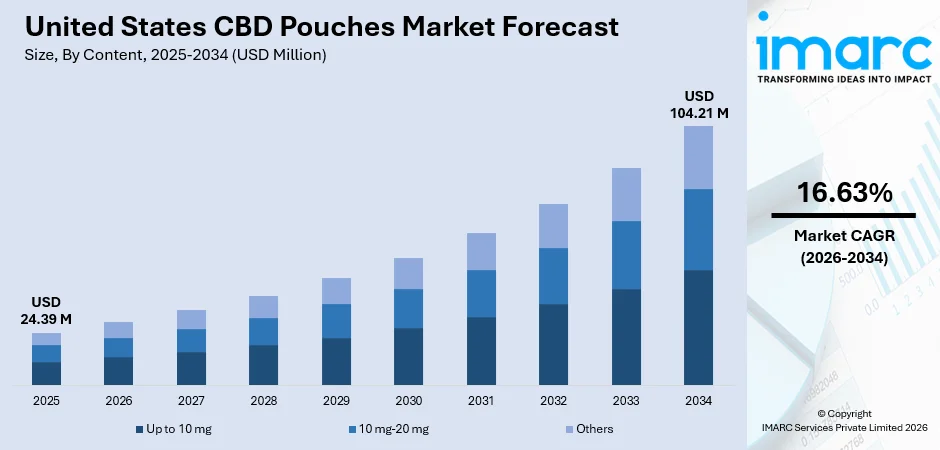

The United States CBD pouches market size was valued at USD 24.39 Million in 2025 and is projected to reach USD 104.21 Million by 2034, growing at a compound annual growth rate of 16.63% from 2026-2034.

The United States CBD pouches market is expanding as consumers shift toward smokeless, discreet wellness options instead of traditional tobacco and nicotine products. Rising awareness of cannabidiol’s potential for stress relief, anxiety support, and pain management is fueling demand across age groups. Product innovation, wider flavor choices, improved absorption technologies, and broader retail availability are enhancing accessibility and repeat purchases. Supportive regulations and interest in non-addictive oral formats continue to strengthen overall market growth and share.

Key Takeaways and Insights:

- By Content: Up to 10 mg dominates the market with a share of 46.7% in 2025, owing to its strong appeal among first-time users and health-conscious consumers who prefer low-dose, entry-level CBD products for mild stress relief and daily wellness routines without risk of overconsumption.

- By Type: Flavored leads the market with a share of 61.9% in 2025, driven by flavor innovations that mask the natural bitterness of hemp extract while enhancing user experience and encouraging repeat usage among younger and first-time consumers.

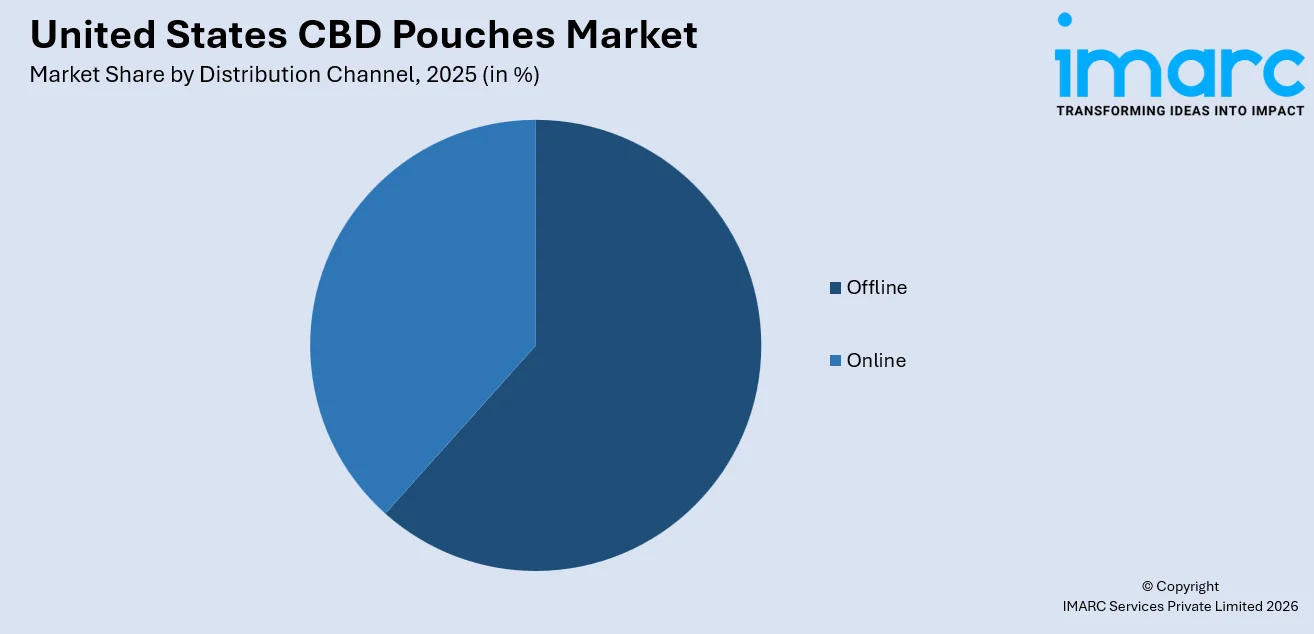

- By Distribution Channel: Offline represents the largest segment with a market share of 54.3% in 2025, reflecting consumer preference for in-person purchases where they can receive product guidance, verify authenticity, and avoid shipping delays or legal uncertainties.

- By Region: South comprises the largest region with 35.1% share in 2025, driven by the deep-rooted culture of smokeless oral product usage in southern states, higher tobacco consumption rates, and growing consumer transition toward healthier alternatives.

- Key Players: The market is facing intense competition as hemp brands, nicotine-pouch players, and wellness startups race to win shelf space and online visibility. Differentiation centers on dosage clarity, rapid-absorption tech, flavor variety, clean-label claims, and third-party testing. Strong distribution partnerships, compliant marketing, and pricing tiers drive scale and customer loyalty.

To get more information on this market Request Sample

The United States CBD pouches market is advancing as consumers, wellness brands, and retailers embrace smokeless cannabidiol delivery formats that offer convenience, discretion, and functional wellness benefits. A major driver shaping this progress is the country’s growing acceptance of CBD as a mainstream wellness product, supported by widening consumer awareness and favorable regulatory developments. For instance, in December 2025, President Trump directed the attorney general to expedite moving marijuana to Schedule III, easing research and tax restrictions for cannabis businesses. The change would not legalize marijuana federally and is expected to have limited impact on employers. This federal policy shift is expected to enhance research infrastructure, improve product safety standards, and boost consumer confidence. The expansion of retail channels, increasing adoption among health-conscious demographics, and continuous product innovations in flavor profiles and dosing precision are further reinforcing growth across the market.

United States CBD Pouches Market Trends:

Growing Consumer Preference for Smokeless Wellness Alternatives

The United States is witnessing a significant shift toward smokeless, non-addictive wellness products as consumers increasingly seek healthier alternatives to traditional tobacco and nicotine formats. CBD pouches are gaining traction as a discreet, convenient oral delivery method that aligns with the broader wellness movement. For instance, as of 2024, approximately 60% of American adults have tried CBD products, a substantial increase from just 6% in 2018, according to consumer surveys. Rising health consciousness, anti-smoking campaigns, and preference for functional products that support relaxation and stress management are collectively driving United States CBD pouches market growth.

Accelerating Product Innovation and Flavor Diversification

Manufacturers are intensifying efforts to differentiate CBD pouches through innovative flavor profiles, enhanced formulations, and precise dosing technologies. Brands are launching diverse options ranging from mint and citrus to coffee and fruit blends, appealing to a wide range of consumer preferences. For example, Cannadips, a leading CBD pouch brand, offers a standard tin containing 15 pouches with 10 mg of water-dispersible CBD each, alongside a premium 5x line delivering 50 mg per pouch in flavors. These innovations are making CBD pouches more accessible and enjoyable, encouraging trial and repeat usage.

Expansion of Retail Distribution and E-Commerce Channels

The accessibility of CBD pouches is improving rapidly as brands secure placements in specialty stores, wellness outlets, convenience chains, and online platforms. Brick-and-mortar retailers provide tactile product experiences and staff guidance, while e-commerce platforms enable wider geographic reach and consumer education. For instance, Cannadips’ hemp pouches were available in over 6,000 retail stores across the United States as of late 2024, demonstrating the expanding retail footprint. The dual-channel distribution strategy is strengthening market penetration, enabling CBD pouch brands to capture both impulse buyers and informed online shoppers across the country.

Market Outlook 2026-2034:

The United States CBD pouches market is poised for robust expansion over the forecast period, supported by accelerating consumer adoption of smokeless wellness formats, evolving federal regulatory frameworks, and continuous product innovations in flavor, dosing, and bioavailability. As such, Brandmydispo introduced advanced CBD pouch packaging which includes QR codes, NFC technology and freshness indicators to improve consumer engagement, product transparency and safety while the packaging solution maintains regulatory compliance and sustainable smart interactive cannabis packaging. In line with this, growing mainstream acceptance of CBD-based oral products, strategic expansion of retail and e-commerce distribution networks, and rising preference for non-addictive alternatives to nicotine pouches are expected to sustain strong revenue growth. Federal efforts to establish clearer regulatory pathways for hemp-derived cannabinoid products, combined with increasing investments in clinical research and product quality standards, are anticipated to further strengthen consumer confidence and broaden market accessibility across the United States. The market generated a revenue of USD 24.39 Million in 2025 and is projected to reach a revenue of USD 104.21 Million by 2034, growing at a compound annual growth rate of 16.63% from 2026-2034.

United States CBD Pouches Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Content |

Up to 10 mg |

46.7% |

|

Type |

Flavored |

61.9% |

|

Distribution Channel |

Offline |

54.3% |

|

Region |

South |

35.1% |

Content Insights:

- Up to 10 mg

- 10 mg-20 mg

- Others

Up to 10 mg dominates with a market share of 46.7% of the total United States CBD pouches market in 2025.

The up to 10 mg content segment has established itself as the preferred entry point for consumers exploring CBD pouches in the United States. This low-dose format appeals strongly to first-time users, health-conscious individuals, and older adults who seek gentle, controlled wellness benefits without the risk of overconsumption or sedation. The microdosing trend has gained substantial traction as consumers increasingly favor precise, manageable doses that can be seamlessly incorporated into daily routines for mild stress relief, improved focus, and general well-being. For instance, FlowBlend, a prominent nicotine-free pouch brand founded in 2020, offers CBD pouches delivering exactly 10 mg of hemp-derived isolate per pouch across distinct flavors, targeting consumers transitioning away from nicotine.

Brands are increasingly developing clean-label formulations within this dosage range, emphasizing natural ingredients, organic certifications, and transparent labeling to build consumer trust and loyalty. The segment’s growth is further fueled by the rising popularity of CBD as a smoking cessation aid, where low-dose pouches serve as a behavioral replacement for nicotine rituals without introducing new dependencies. For example, in January 2025, the United States FDA approved the sale of 20 ZYN nicotine pouch products through the premarket tobacco product application process, marking the first federal approval of nicotine pouches and further legitimizing the oral pouch format as a recognized consumer category, which indirectly benefits CBD pouch adoption.

Type Insights:

- Flavored

- Unflavored

Flavored leads with a share of 61.9% of the total United States CBD pouches market in 2025.

The United States market now sees flavored CBD pouches as its leading product type because these pouches successfully solve the main problem that prevents people from using CBD which is the unpleasant natural taste of hemp extract. The introduction of appealing flavor profiles, including mint, citrus, mango, coffee, cherry, and cinnamon, enables manufacturers to transform CBD pouches from their initial purpose as wellness products into products that provide users with enjoyable lifestyle experiences. The product's sensory features attract first-time customers to try it, while younger users aged 18 to 34 who want both taste and functional advantages will keep buying it.

The competitive landscape within the flavored segment is intensifying as brands invest in novel flavor combinations, seasonal editions, and premium taste profiles to differentiate their offerings. Clean-label formulations using natural flavors, plant-based sweeteners like xylitol and stevia, and organic ingredients are becoming industry standards as consumers demand transparency in product composition. The flavored format also serves as a critical gateway for consumers transitioning from traditional nicotine pouches, as familiar flavor profiles reduce the psychological barriers associated with switching to an entirely new product category. According to the November 2025 U.S. Tobacco Atlas released by the American Cancer Society, cigarette smoking among United States adults declined from 42% in 1965 to 11% in 2023, creating a growing pool of health-conscious former smokers seeking alternative oral products.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Offline

- Online

The offline segment exhibits a clear dominance with a 54.3% share of the total United States CBD pouches market in 2025.

The United States CBD pouches market exhibits strong dominance through offline distribution channels because customers prefer to buy products in-store, which allows them to confirm product authenticity, verify product quality, and receive customized shopping help. The specialty wellness stores and vape shops, pharmacies and convenience chains function as reliable retail locations where new customers and health-focused shoppers can test products and examine product information while getting help from expert staff. The CBD product category needs to have customers experience physical product testing because they want proof that all products meet legal requirements.

The offline channel also benefits significantly from impulse purchasing behavior, as prominently placed CBD pouches near checkout counters and within dedicated wellness sections attract spontaneous trial among curious consumers. Retail partnerships with national convenience chains and wellness franchises are enabling broader geographic coverage, particularly in regions with established smokeless product consumption cultures. Physical retail visibility also helps normalize CBD pouches as a mainstream wellness product rather than a niche supplement, building brand familiarity and consumer trust. Additionally, in-store promotional activities, product sampling, and staff training programs by leading brands are enhancing consumer education and accelerating conversion rates across retail touchpoints.

Regional Insights:

- Northeast

- Midwest

- South

- West

South represents the leading segment with a 35.1% share of the total United States CBD pouches market in 2025.

The South region commands the largest share of the United States CBD pouches market, underpinned by a deeply rooted cultural affinity for smokeless oral products and higher rates of tobacco and nicotine consumption compared to other regions. Southern states have historically maintained the strongest consumer base for chewing tobacco, snuff, and dip products, creating a natural transition pathway toward CBD pouches as healthier alternatives gain prominence. The 2024 Surgeon General’s report highlighted that adults in Midwestern and Southern states are more likely to smoke cigarettes than those in other regions, with “Tobacco Nation” states showing smoking rates over 40% higher than the national average. This established user base, combined with growing health awareness and demand for non-addictive alternatives, is fueling CBD pouch adoption across the region.

The South’s dominance is further reinforced by expanding retail infrastructure, increasing availability of CBD products in convenience stores and wellness outlets, and favorable hemp cultivation conditions that support regional supply chains. The presence of a large rural population familiar with oral pouch formats, along with rising consumer education about CBD’s potential benefits for pain relief, stress management, and relaxation, is broadening the addressable market across diverse demographic groups. Strategic market entries by leading brands are also prioritizing southern states to capitalize on this receptive consumer base, further strengthening the region’s market leadership.

Market Dynamics:

Growth Drivers:

Why is the United States CBD Pouches Market Growing?

Rising Consumer Awareness of CBD Health Benefits

The United States is experiencing a substantial increase in consumer awareness regarding the potential therapeutic and wellness benefits of cannabidiol, which is driving strong demand for convenient CBD delivery formats such as pouches. Growing recognition of CBD’s role in alleviating stress, managing chronic pain, improving sleep quality, and reducing anxiety is motivating consumers across age groups and demographics to explore CBD-based products as part of their daily wellness routines. The shift toward self-care and preventive health management, particularly among millennials and older adults, is creating a large and expanding addressable market for CBD pouches. Federal acknowledgment of CBD’s potential medical benefits has further strengthened consumer confidence. For instance, CBD research cited that one in five United States adults and nearly 15% of seniors reported using CBD in the past year, with chronic pain patients reporting improvements in clinical studies. This growing body of evidence and federal support is encouraging more Americans to view CBD pouches as a legitimate wellness tool, reinforcing market expansion across the country.

Accelerating Transition from Traditional Tobacco and Nicotine Products

A significant and sustained shift away from combustible cigarettes and traditional smokeless tobacco products is creating favorable conditions for the adoption of CBD pouches as a healthier alternative. Public health campaigns, rising cigarette prices, expanding smoke-free zones, and increased awareness of tobacco-related diseases are collectively driving consumers toward non-addictive oral formats. CBD pouches effectively replicate the familiar hand-to-mouth ritual and oral fixation associated with tobacco use while delivering potential wellness benefits without nicotine dependency. The normalization of oral pouch formats has been further accelerated by developments in the nicotine pouch category. This regulatory milestone has elevated consumer familiarity and acceptance of the oral pouch format broadly, indirectly benefiting CBD pouch manufacturers by legitimizing the product category and expanding shelf space across retail environments nationwide.

Rising Demand for Discreet and Portable Wellness Products

Modern consumers increasingly prefer wellness solutions that fit seamlessly into busy lifestyles. A USA Today survey found that Americans feel increasingly time-pressed, with 69% describing themselves as “busy” or “very busy,” while only 8% said they were “not very busy.” CBD pouches offer a smoke-free, odorless, and easy-to-carry format that can be used anytime without drawing attention. This discretion appeals strongly to working professionals, travelers, and younger adults seeking stress relief or calm support in social and public settings. The convenience of on-the-go consumption, combined with the growing preference for non-invasive oral supplements, is expanding adoption and fueling steady market growth across the United States.

Market Restraints:

What Challenges the United States CBD Pouches Market is Facing?

Regulatory Uncertainty and Fragmented State-Level Compliance

Despite recent federal efforts to establish clearer regulatory pathways, the United States CBD pouches market continues to face significant challenges stemming from inconsistent state-level regulations governing the sale, labeling, and distribution of hemp-derived CBD products. The absence of a unified federal regulatory framework creates compliance complexity for manufacturers operating across multiple jurisdictions, increasing operational costs and limiting market scalability. Additionally, evolving definitions of hemp and THC content thresholds, such as the November 2025 legislative changes imposing stricter container-level THC caps, introduce uncertainty for product formulations and supply chain planning.

Persistent Consumer Misconceptions and Stigma

A substantial portion of the American population continues to associate CBD with marijuana and its psychoactive effects, creating barriers to wider adoption of CBD pouches as a mainstream wellness product. Misinformation about CBD’s legal status, safety profile, and potential side effects discourages trial among risk-averse consumers, particularly older demographics and individuals in conservative communities. Furthermore, concerns about potential positive drug test results from CBD product usage deter adoption among professionals and individuals subject to workplace drug testing, limiting the addressable consumer base despite growing product availability and brand awareness.

Premium Pricing and Limited Insurance Coverage

CBD pouches typically command higher price points compared to conventional nicotine pouches, chewing tobacco, and other smokeless alternatives, which restricts adoption among price-sensitive consumers. The premium positioning reflects the costs associated with high-quality hemp sourcing, advanced extraction and formulation technologies, rigorous third-party testing, and regulatory compliance. Unlike pharmaceutical CBD products such as Epidiolex, over-the-counter CBD pouches are not covered by health insurance or eligible for medical reimbursement, placing the full financial burden on consumers and limiting long-term affordability for regular users.

Competitive Landscape:

The United States CBD pouches market features an increasingly competitive landscape characterized by a mix of established pioneers and emerging challengers vying for market share through product innovation, brand differentiation, and strategic distribution expansion. Companies are investing heavily in flavor diversification, precise dosing technologies, clean-label formulations, and enhanced bioavailability to attract health-conscious consumers seeking alternatives to traditional tobacco and nicotine products. Competition is further intensified by strategic retail partnerships, e-commerce optimization, and targeted marketing campaigns that position CBD pouches as lifestyle-oriented wellness products. As the regulatory environment evolves and consumer awareness deepens, market players are continuously refining their strategies to strengthen brand loyalty, expand geographic reach, and capitalize on the growing demand for smokeless, non-addictive oral wellness formats.

Recent Developments:

- In February 2026, Kazmira Therapeutics opened the first U.S. licensed, prescription-only CBD compounding pharmacy in Colorado. Launched in January 2026, it produces ultra-pure, THC-free medical-grade cannabidiol for customized patient prescriptions. The move addresses regulatory uncertainty and positions CBD as a pharmaceutical-grade treatment option nationwide.

- In January 2026, Dark Horse Cannabis partnered with Cannadips to launch smokeless cannabis pouches in Arkansas, marking Cannadips’ first cannabis expansion outside California. The collaboration will introduce flavored, discreet alternatives aimed at consumers seeking fast-acting options and substitutes for traditional smokeless tobacco and nicotine products.

United States CBD Pouches Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Contents Covered |

Up to 10 mg, 10 mg-20 mg, Others |

|

Types Covered |

Flavored, Unflavored |

|

Distribution Channels Covered |

Offline, Online |

|

Regions Covered |

Northeast, Midwest, South, West |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the United States CBD Pouches Market Report

The United States CBD pouches market size was valued at USD 24.39 Million in 2025.

The United States CBD pouches market is expected to grow at a compound annual growth rate of 16.63% from 2026-2034 to reach USD 104.21 Million by 2034.

Up to 10 mg dominated the market with a share of 46.7%, driven by its strong appeal among first-time users and health-conscious consumers seeking low-dose, entry-level CBD products for mild stress relief, daily wellness routines, and controlled microdosing without overconsumption risks.

Key factors driving the United States CBD pouches market include rising consumer awareness of CBD wellness benefits, accelerating transition from traditional tobacco products, expanding retail distribution networks, continuous flavor and formulation innovations, and evolving federal regulatory support for hemp-derived cannabinoid products.

Major challenges include regulatory uncertainty and fragmented state-level compliance requirements, persistent consumer misconceptions and stigma associating CBD with psychoactive marijuana, premium product pricing limiting mass-market adoption, inconsistent product quality standards, and evolving federal hemp definitions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)