United States Chestnut Market Size, Share, Trends and Forecast by Species Type, Distribution, and Region, 2026-2034

United States Chestnut Market Size and Share:

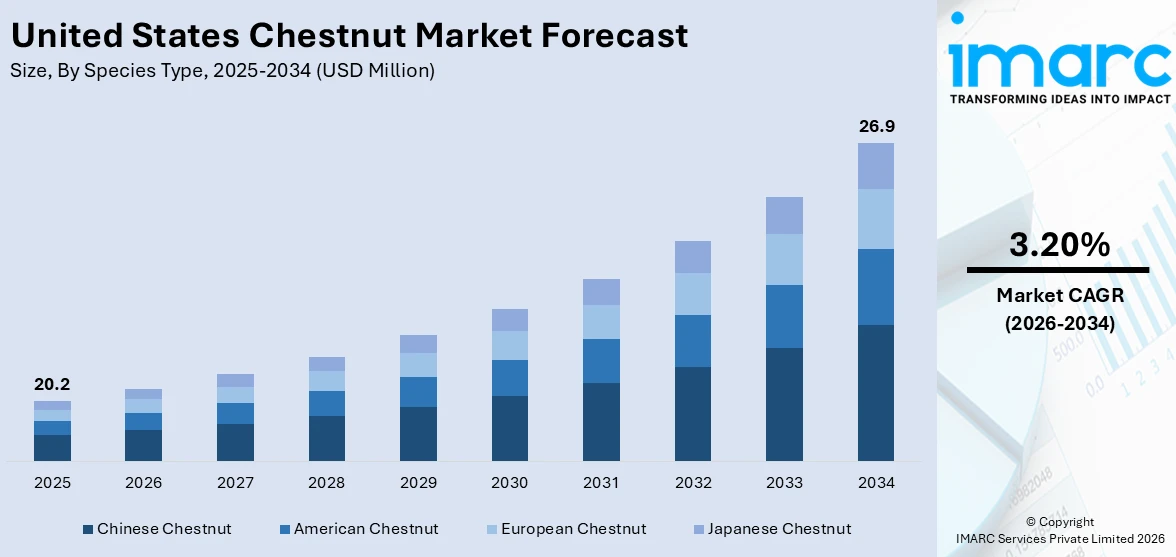

The United States chestnut market size was valued at USD 20.2 Million in 2025. Looking forward, IMARC Group estimates the market to reach USD 26.9 Million by 2034, exhibiting a CAGR of 3.20% from 2026-2034. The market is driven by growing consumer demand for healthy, plant-based, and gluten-free foods, positioning chestnuts as a nutritious alternative in snacks, flours, and baked goods. Expanding interest in ethnic and gourmet cuisines boosts their use in diverse recipes, while rising domestic production improves availability and reduces reliance on imports. Additionally, advancements in processing, storage, and direct-to-consumer (D2C) e-commerce channels make chestnuts more accessible year-round, supporting broader market penetration and catering to health-conscious and sustainability-focused consumers thus aiding the United States chestnut market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 20.2 Million |

| Market Forecast in 2034 | USD 26.9 Million |

| Market Growth Rate (2026-2034) | 3.20% |

As plant-based eating gains traction, chestnuts are emerging as a valuable ingredient for alternative flours and gluten-free products. Chestnut flour is increasingly used in baking, pasta, and confectionery, appealing to consumers with celiac disease or gluten sensitivity. Its naturally sweet flavor and high carbohydrate content make it a preferred option for clean-label, allergen-friendly products. With the surge in vegan and vegetarian diets, food manufacturers are exploring chestnut-based ingredients for snacks and processed foods. This trend expands the market beyond traditional whole nuts, creating opportunities in packaged goods and health-oriented food products.

To get more information on this market Request Sample

The growth of online retail significantly boosts chestnut accessibility across the U.S. Small orchards, cooperatives, and specialty producers increasingly sell directly through e-commerce platforms, bypassing traditional distribution bottlenecks. Online marketplaces such as Amazon, farm-to-door websites, and subscription snack boxes help expand chestnut reach to health-conscious and niche consumers nationwide. These channels also allow producers to offer value-added products like roasted chestnuts, purees, and flours directly to households and small businesses. Digital marketing campaigns highlighting chestnut health benefits and recipe versatility further drive awareness. This shift toward D2C sales makes chestnuts more available year-round while supporting small-scale farmers and increasing overall market penetration.

United States Chestnut Market Trends:

Rising Health and Wellness Trends

The growing awareness of healthy eating habits significantly drives the United States chestnut market outlook. Chestnuts are uniquely nutrient-dense, offering high fiber, vitamin C, and antioxidants while remaining low in fat compared to other nuts. In a 100 g serving, chestnuts provide approximately 43 mg of vitamin C (≈70 % DV) and 8 g of fiber (~21 % DV)—nutritional levels uncommon in tree nuts—supporting their positioning as heart‑healthy and digestion-friendly foods. As consumers increasingly seek plant-based, gluten-free, low-fat, and minimally processed alternatives, chestnuts perfectly align with these dietary preferences. Health-conscious individuals view them as wholesome snacks and a substitute for refined carbohydrates, fueling their use in functional foods, snacks, and clean-label products. Additionally, their suitability for diabetic-friendly and heart-healthy diets, along with strategic marketing as superfoods, continues to boost their appeal, driving consumption and expanding opportunities in the evolving health-focused food market.

Expanding Domestic Production & Supply Chain Improvements

Historically, the U.S. chestnut market relied heavily on imports, but domestic production is increasing due to advancements in farming practices and investments in orchards. States like Michigan, Ohio, and California have seen growth in chestnut cultivation, reducing dependency on imports and improving supply reliability. Modern processing facilities and better cold storage technologies also ensure longer shelf life and consistent product availability. Additionally, farmer cooperatives and industry groups are promoting awareness about chestnut farming, improving distribution channels, and creating value-added products like chestnut flour and purees. These supply chain improvements support cost efficiency, making chestnuts more accessible to retailers and consumers. With rising interest in locally sourced and sustainable products, U.S.-grown chestnuts attract both environmentally conscious consumers and businesses seeking to reduce reliance on foreign suppliers.

Growth of Ethnic and Gourmet Cuisine

The popularity of multicultural cuisine is a key United States chestnut market trend. The U.S. consumes about 7.5 million pounds (~3,400 metric tons) of imported chestnuts annually, primarily for traditional and gourmet dishes, as domestic production remains limited. Chestnuts play an important role in European, Asian, and Mediterranean cooking, often featured in stuffing, roasted dishes, and desserts. With the rise of gourmet dining, fusion cuisine, and ethnic food trends, chefs and home cooks increasingly incorporate chestnuts into recipes. Restaurants, bakeries, and specialty food producers value them for their unique flavor and texture, while food enthusiasts experiment with chestnuts in sauces, soups, and pastries. Additionally, demand for artisanal and premium products has boosted chestnut use in confectionery and bakery applications. Seasonal consumption, especially during holidays, further supports steady, year‑round demand.

United States Chestnut Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the United States chestnut market, along with forecast at the regional, and country levels from 2026-2034. The market has been categorized based on species type and distribution.

Analysis by Species Type:

- American Chestnut

- Chinese Chestnut

- European Chestnut

- Japanese Chestnut

Based on the United States chestnut market forecast, the Chinese chestnuts account for nearly 80% primarily due to their adaptability, high yield, and consumer-preferred qualities. These varieties are favored for their naturally sweet flavor, larger nut size, and ease of peeling, making them popular for both direct consumption and processing into flours, purees, and snacks. Their compatibility with U.S. growing conditions, particularly in states like Michigan, Ohio, and California, encourages widespread cultivation, reducing reliance on imports. Additionally, Chinese chestnuts’ resistance to chestnut blight, compared to American varieties, ensures stable production and supply. Their affordability and suitability for a variety of culinary applications—from roasting to use in gourmet dishes further reinforce their dominant position in the market, driving consistent demand among consumers and food manufacturers.

Analysis by Distribution:

Access the comprehensive market breakdown Request Sample

- Food and Beverage Industry

- Food Service

- Retail

- Others

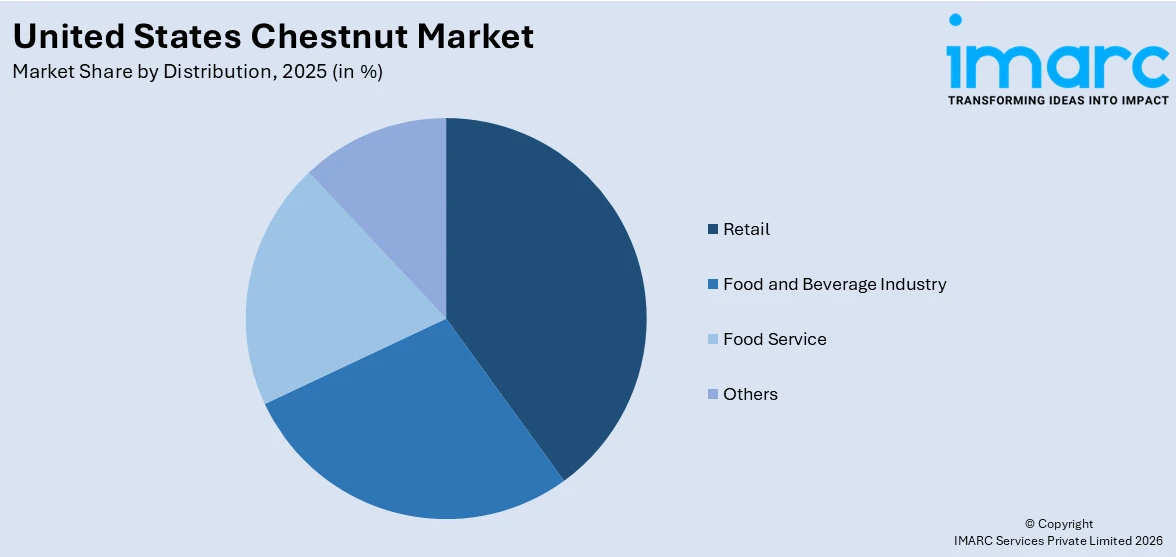

Retail channels dominate the U.S. chestnut market with a 40.8% share, driven by their wide accessibility, diverse product offerings, and seasonal demand spikes. Supermarkets, specialty stores, and health food outlets provide consumers with convenient access to fresh, roasted, and value-added chestnut products, especially during the holiday season when demand peaks. Retailers also benefit from strong in-store promotions, recipe-driven marketing, and attractive packaging that enhances consumer appeal. The growing presence of chestnuts in organic and health-focused sections caters to wellness-oriented shoppers, further strengthening sales. Additionally, retail channels support both domestic and imported chestnut varieties, ensuring year-round availability. This broad distribution network and ability to reach mass-market consumers make retail the leading channel for chestnut sales in the United States.

Regional Analysis:

- Northeast

- Midwest

- South

- West

The Northeast market benefits from strong holiday-driven demand, with chestnuts being a traditional favorite in festive meals. Urban centers and specialty stores support premium and imported varieties. Growing interest in gourmet and ethnic cuisines also drives consumption, making this region a key market for value-added chestnut products.

Additionally, the Midwest has a strong emphasis on production, with states like Michigan and Ohio leading domestic chestnut cultivation. Favorable growing conditions and cooperative farming initiatives ensure a steady supply. Local marketing, farm-to-table movements, and strong participation in farmers’ markets boost regional sales, making the Midwest both a production hub and a growing consumer market.

Furthermore, in the South, chestnut demand is growing due to expanding culinary diversity and increasing awareness of their health benefits. Regional interest in alternative flours and plant-based diets supports processed chestnut products. Seasonal festivals and local retail channels further enhance market growth, strengthening chestnuts’ presence in southern food culture.

Besides this, the West benefits from robust agricultural infrastructure, with California contributing significantly to production. Health-conscious consumers, strong organic food markets, and widespread adoption of ethnic cuisines drive demand. The region also sees high e-commerce sales and innovative product development, making it a dynamic growth area for both fresh and processed chestnut products.

Competitive Landscape:

The U.S. chestnut market’s competitive landscape is characterized by a mix of small-scale growers, cooperatives, and specialty producers, alongside a few larger players involved in processing and distribution. Competition largely centers on product quality, freshness, and value-added innovations such as chestnut flour, purees, and ready-to-eat roasted products. Seasonal demand peaks, especially during the holidays, intensify competition among suppliers, while off-season sales rely on processed and preserved formats. Market players focus on sustainable farming practices, regional branding, and direct-to-consumer strategies to differentiate themselves. Additionally, partnerships with retailers, gourmet food producers, and e-commerce platforms are crucial for expanding reach. Innovation in packaging and marketing plays a key role in gaining consumer loyalty within this evolving, health-driven market.

The report provides a comprehensive analysis of the competitive landscape in the United States chestnut market with detailed profiles of all major companies.

Latest News and Developments:

- July 2025: Researchers at SUNY-ESF advanced their Darling-54 genetically engineered chestnut tree toward public release after the USDA concluded it posed no plant pest risk. Designed for blight resistance, Darling-54 awaited additional approvals from the FDA and EPA. Critics questioned its performance, but developers affirmed its safety and survival potential in the wild.

- May 2025: Chestnut Carbon completed planting over 17 million native trees on 30,000 acres in the Southeastern U.S., establishing the largest U.S.-based afforestation project on the Gold Standard® registry. The project enhanced biodiversity, air and water quality, and supported local economies. Carbon credits were pre-sold to major corporations with a focus on sustainability.

United States Chestnut Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Species Types Covered | American Chestnut, Chinese Chestnut, European Chestnut, Japanese Chestnut |

| Distributions Covered | Food and Beverage Industry, Food Service, Retail, Others |

| Regions Covered | Northeast, Midwest, South, West |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the United States chestnut market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the United States chestnut market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the United States chestnut industry and its attractiveness.

- A competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the United States Chestnut Market Report

The chestnut market in the United States was valued at USD 20.2 Million in 2025.

The United States chestnut market is projected to exhibit a CAGR of 3.20% during 2026-2034, reaching a value of USD 26.9 Million by 2034.

Key factors driving the U.S. chestnut market include rising demand for healthy, plant-based, and gluten-free foods, increased use in ethnic and gourmet cuisines, expanding domestic production, and improved processing and storage. Growth in e-commerce and direct-to-consumer sales also boosts accessibility, supporting year-round availability and broader consumer adoption.

The Chinese chestnuts account for nearly 80% of the U.S. chestnut market share, primarily due to their high yield, larger nut size, and sweeter flavor, making them ideal for diverse culinary uses. Their competitive pricing, consistent quality, and strong import supply chains further reinforce their dominance in meeting U.S. consumer and commercial demand.

Retail channels dominate the U.S. chestnut market with a 40.8% share, driven by strong consumer demand for fresh, roasted, and packaged chestnuts through supermarkets, specialty stores, and farmers’ markets. Easy accessibility, holiday-season promotions, and the availability of value-added products like chestnut flour and purees further boost retail sales.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade