United States Dairy Market Size, Share, Trends and Forecast by Product, Application, Distribution Channel, and Region, 2026-2034

United States Dairy Market Size, Share, Trends & Forecast (2026-2034)

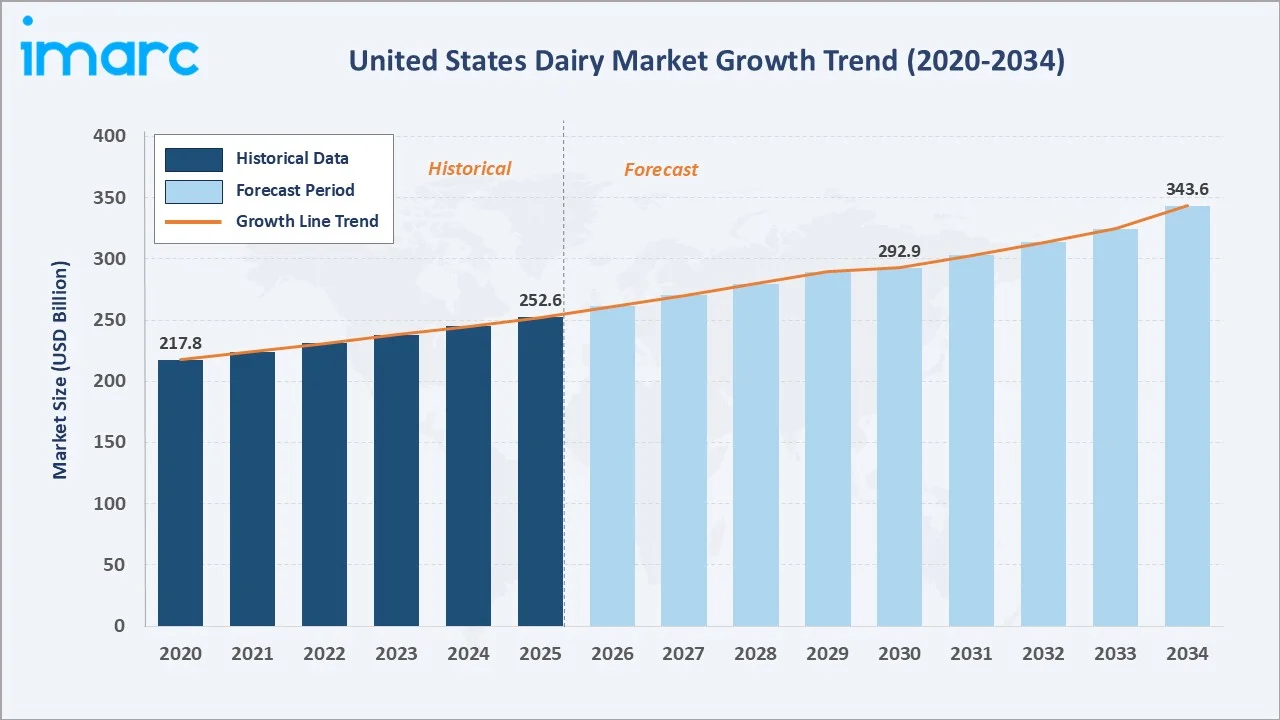

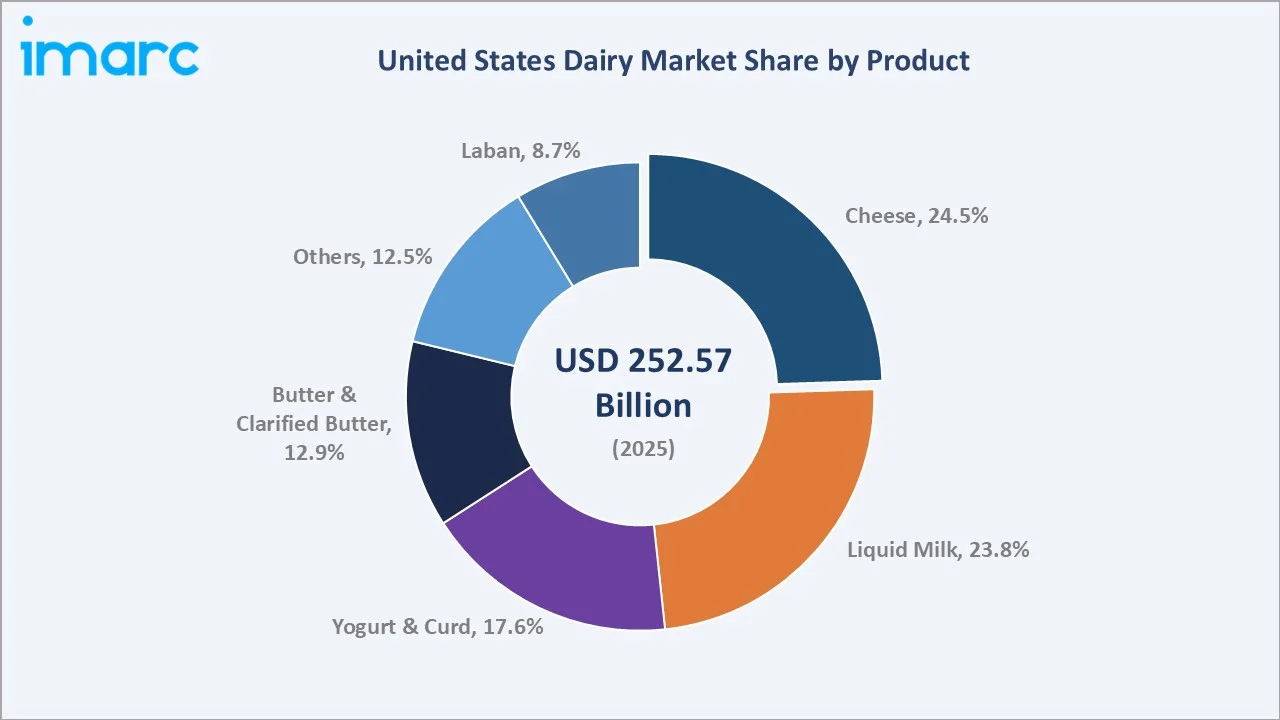

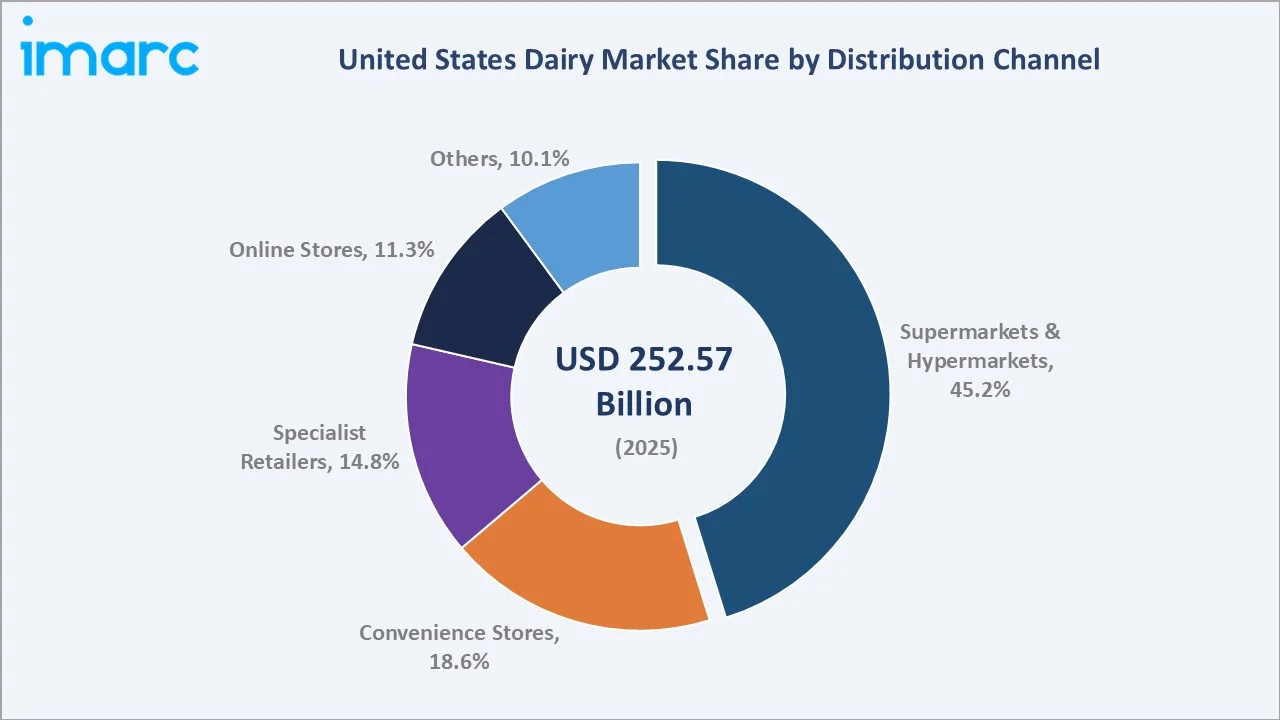

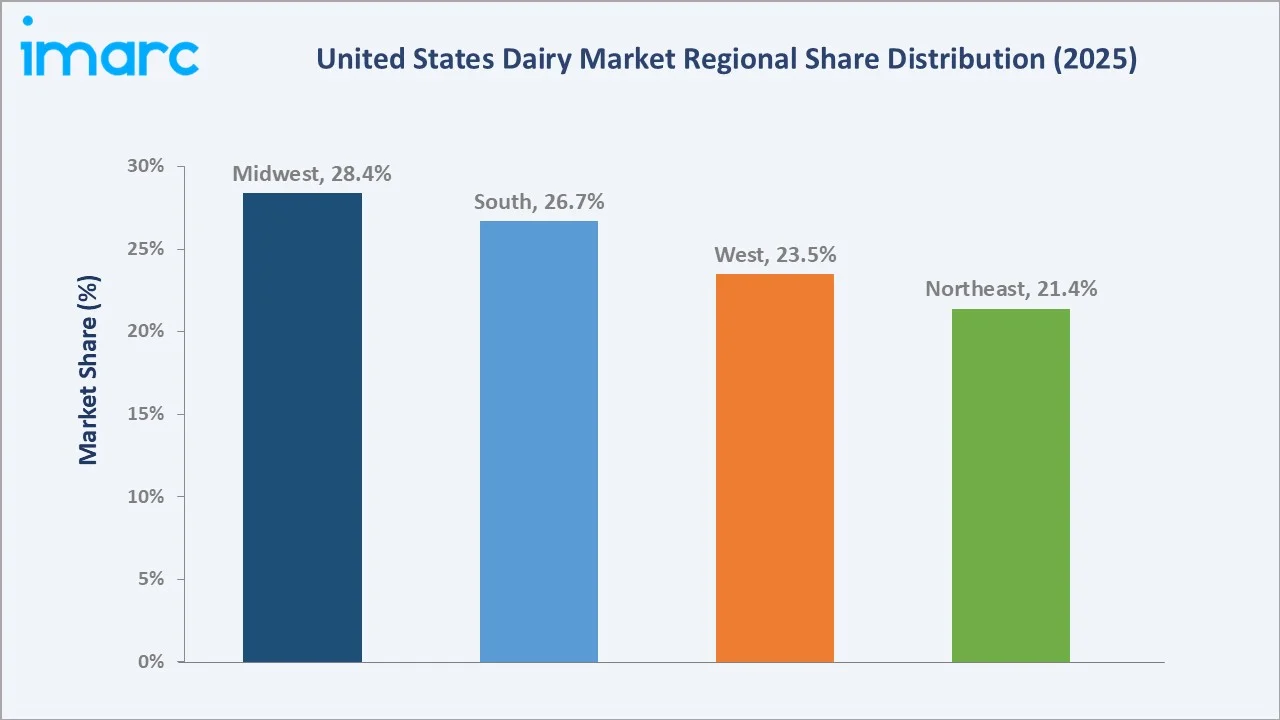

The United States dairy market size was valued at USD 252.57 Billion in 2025 and is projected to reach USD 343.65 Billion by 2034, exhibiting a CAGR of 3.00% during the forecast period 2026-2034. Strong household consumption, expanding cheese and yogurt categories, and a robust foodservice rebound are driving the United States dairy market growth. Cheese leads at 24.5% share in 2025, while liquid milk follows at 23.8%. Supermarkets and hypermarkets dominate distribution with a 45.2% revenue share, and the Midwest region accounts for 28.4% of national demand.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 252.57 Billion |

|

Forecast Market Size (2034) |

USD 343.65 Billion |

|

CAGR (2026-2034) |

3.00% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Midwest (28.4% share, 2025) |

|

Leading Product Segment |

Cheese (24.5% share, 2025) |

|

Leading Distribution Channel |

Supermarkets & Hypermarkets (45.2%, 2025) |

The United States dairy market growth trajectory from 2020 through 2034 contrasts a steady historical expansion against a sustained forecast curve, supported by rising per-capita cheese intake, expanding yogurt portfolios, and recovery in away-from-home consumption channels.

To get more information on this market, Request Sample

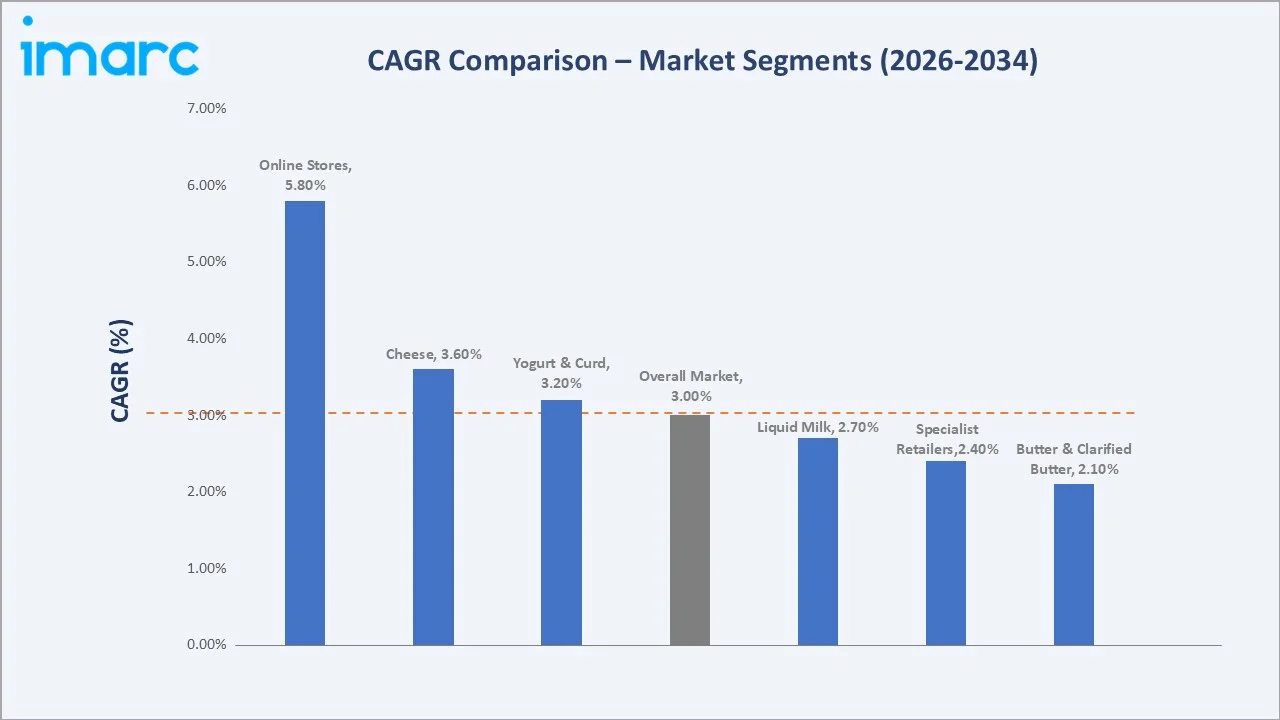

Segment-level CAGR comparisons highlight online retail and the cheese category as the fastest-growing sub-categories within the broader United States dairy market forecast through 2034, while traditional staples such as butter and liquid milk grow at a slower pace.

Executive Summary

The United States dairy market is undergoing a measured but meaningful transformation. It is shaped by shifting consumer preferences, the rise of high-protein and functional dairy, and a strong rebound in foodservice consumption. Valued at USD 252.57 Billion in 2025, the market is projected to reach USD 343.65 Billion by 2034 at a CAGR of 3.00%, expanding from USD 217.81 Billion recorded in 2020.

Cheese commands 24.5% of product revenue in 2025, supported by snacking demand and pizza-led foodservice volumes. Liquid milk follows at 23.8%, while yogurt and curd account for 17.6% on the back of high-protein Greek and Icelandic-style variants. Supermarkets and hypermarkets dominate distribution at 45.2%, though online stores are advancing fastest at an estimated 5.8% CAGR through 2034.

The Midwest leads with a 28.4% revenue share in 2025, followed by the South at 26.7% and the West at 23.5%. The United States dairy market outlook remains constructive as premiumization, clean-label reformulation, and expanding cheese exports converge with steady consumer demand across both retail and foodservice channels.

Key Market Insights

|

Insight |

Data |

|

Largest Product Segment |

Cheese – 24.5% share (2025) |

|

Second Product Segment |

Liquid Milk – 23.8% share (2025) |

|

Largest Distribution Channel |

Supermarkets & Hypermarkets – 45.2% (2025) |

|

Fastest-Growing Channel |

Online Stores – ~5.8% CAGR (2026-2034) |

|

Leading Region |

Midwest – 28.4% revenue share (2025) |

|

Top Companies |

Dairy Farmers of America, Nestle, Saputo Inc., Land O'Lakes Inc., Schreiber Inc., Leprino Foods Company |

|

Forecast Market Size (2034) |

USD 343.65 Billion |

Key Analytical Observations Supporting the Above Data:

- Cheese's 24.5% dominance in 2025 reflects sustained pizza-driven foodservice demand and the rapid rise of cheese-based snacking products such as string cheese, mini-rounds, and shredded blends across United States supermarkets.

- Liquid milk's 23.8% share is anchored by school-meal programmes and family-household consumption, even as flavoured and lactose-free variants continue to capture incremental volume from traditional white milk.

- Yogurt and curd's 17.6% position is supported by high-protein Greek and Icelandic skyr formats. Per-capita yogurt consumption in the United States reached approximately 14.7 pounds in 2024, according to USDA Dairy Data.

- Supermarkets and hypermarkets' 45.2% lead reflects entrenched cold-chain infrastructure, private-label dominance from chains like Kroger and Walmart, and weekly basket-shopping habits that favour large-format retail.

- Online stores' 11.3% share is the fastest-rising channel. Subscription milk delivery, click-and-collect cheese, and Amazon Fresh dairy aisles have meaningfully expanded since 2021, particularly in metro markets.

- Midwest's 28.4% regional dominance is underpinned by Wisconsin's cheese-making heritage and intensive dairy herds across Minnesota, Iowa, and Illinois that supply both retail and ingredient markets.

United States Dairy Market Overview

Dairy products are nutrient-dense food items derived from cow, goat, and buffalo milk. The United States dairy market includes liquid milk, cheese, yogurt and curd, butter and clarified butter, laban, and a range of cultured and processed variants. These products serve households, foodservice operators, and industrial buyers including bakers, confectioners, and ready-meal manufacturers.

The industry sits at the intersection of agriculture, food manufacturing, and retail. Macroeconomic drivers include household disposable income, foodservice traffic, school-meal participation, and federal nutrition programmes. The United States dairy industry analysis must also factor in feed-cost cycles, federal milk marketing orders, and a steady shift toward high-protein, lactose-free, and clean-label dairy formats.

Market Dynamics

To evaluate market opportunities, Request Sample

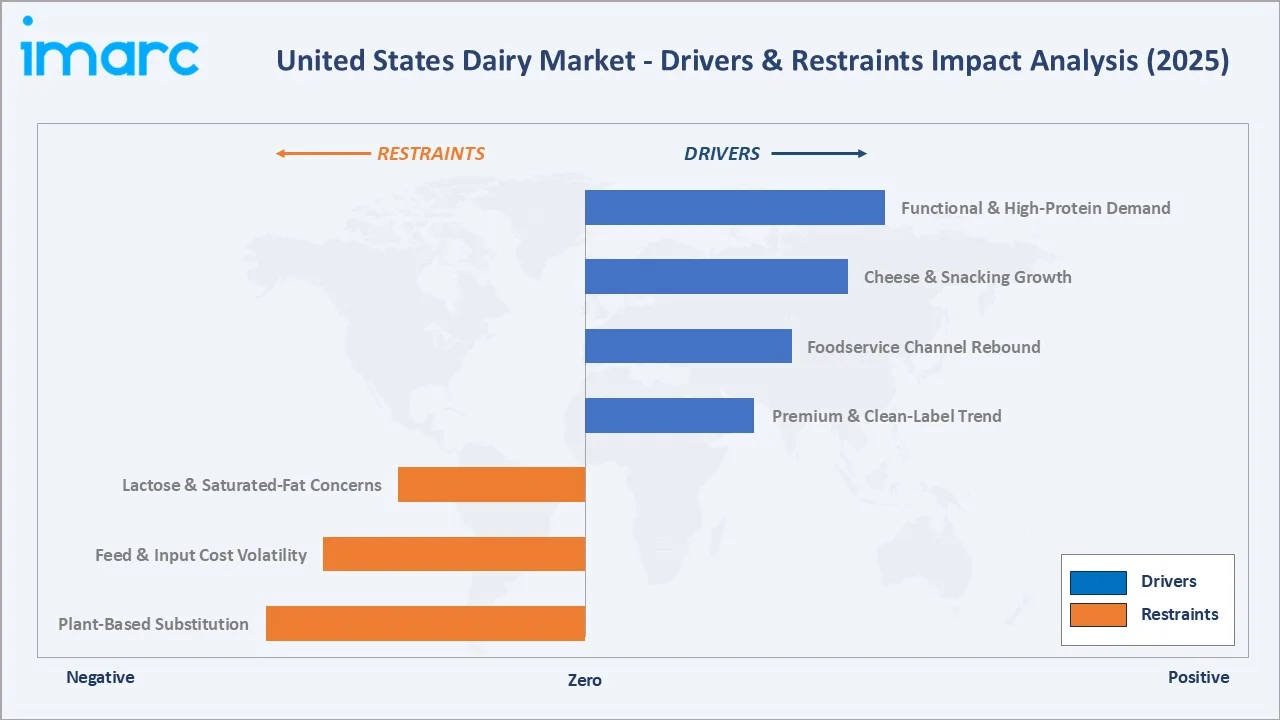

Market Drivers

- Functional and High-Protein Demand: Consumer interest in protein-rich, gut-friendly, and fortified dairy is rising sharply. Greek yogurt, cottage cheese, and protein-enriched milk have together added meaningful volume since 2022, with cottage cheese sales jumping double digits in 2024.

- Cheese and Snacking Growth: Cheese remains the single largest product category at 24.5% in 2025. Per-capita United States cheese consumption reached approximately 41.8 pounds in 2024, a multi-decade high, fuelled by pizza, snacks, and Mexican-style dishes.

- Foodservice Channel Rebound: Quick-service restaurants, casual dining, and coffee chains have rebuilt dairy demand to above pre-2020 levels. Coffee-shop chains in 2024-2025 introduced new milk-based and cream-based beverages that supported additional volume across milk and cream segments.

- Premium and Clean-Label Trend: Grass-fed butter, A2 milk, lactose-free yogurt, and organic cheese are commanding price premiums. The United States Census Bureau food-at-home expenditure data through 2024 highlights consistent up-trading toward branded, premium dairy SKUs across major retailers.

Market Restraints

- Plant-Based Substitution: Almond, oat, and soy beverages continue to capture share from traditional fluid milk in selected demographics, particularly younger urban consumers.

- Feed and Input Cost Volatility: Corn, soy, and energy-cost swings translate directly into farmgate milk prices. The 2022-2023 price cycle compressed processor margins and slowed promotional activity at retail.

- Lactose and Saturated-Fat Concerns: Health-led narratives around saturated fat and lactose intolerance continue to push a slice of consumption toward lactose-free formats and non-dairy alternatives.

Market Opportunities

- Lactose-Free and Functional Dairy: Lactose-free milk, A2 protein milk, and probiotic-fortified yogurts represent the highest-margin growth tier. Several major United States dairies expanded lactose-free SKUs across both private-label and branded ranges in 2024.

- United States Cheese Exports and Foodservice Innovation: United States cheese exports reached record volumes in 2024, with mozzarella, cheddar, and processed slices leading shipments to Mexico, South Korea, and Japan. This export pull supports domestic cheese-plant utilization and price stability.

Market Challenges

- Labelling and Regulatory Pressure: FDA reviews of "milk" labelling on plant-based beverages, evolving sodium and added-sugar guidelines, and state-level packaging mandates require continuous reformulation and labelling updates.

- Sustainability and Methane Reporting: Investors and major retail buyers increasingly demand transparent farm-level emissions data. Smaller cooperatives face capability gaps in measuring and reporting Scope 3 dairy-supply emissions through 2030.

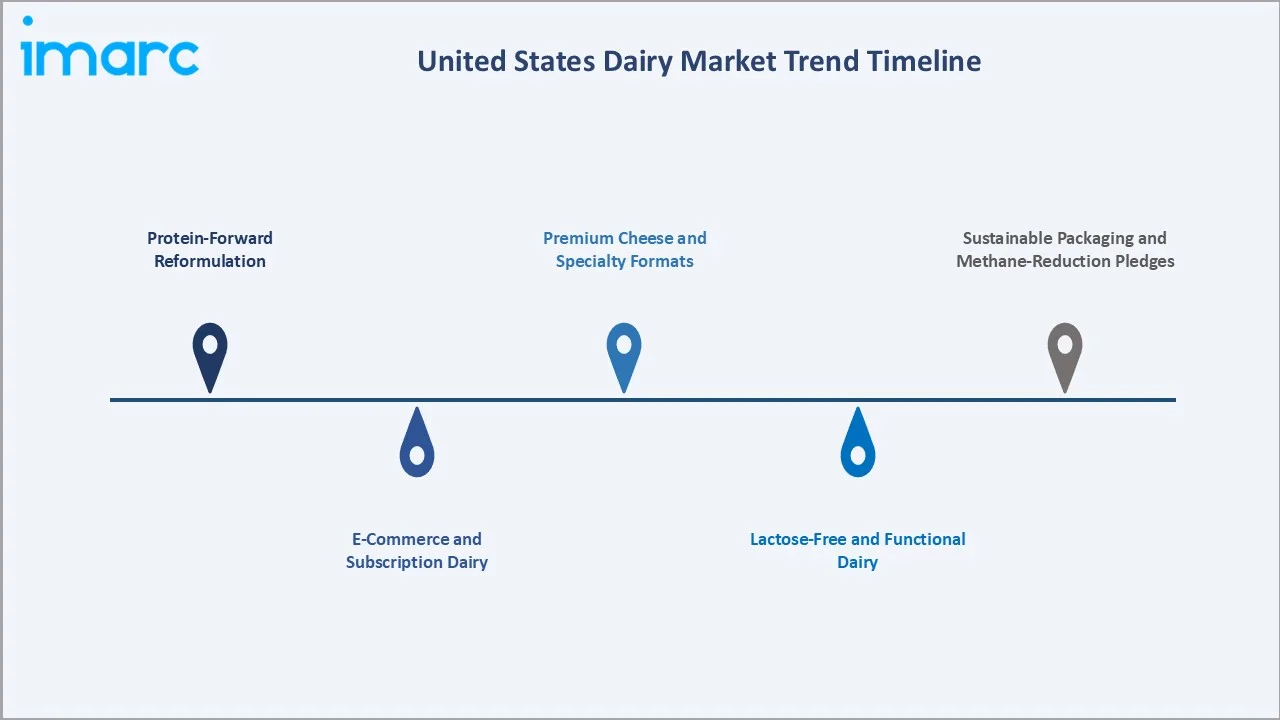

Emerging Market Trends

1. Protein-Forward Reformulation

Brands are reformulating yogurts, milk, and cottage cheese to deliver 15-25 grams of protein per serving. This shift is driving incremental sales among gym-goers, GLP-1 medication users, and active older consumers across the United States in 2024-2025.

2. E-Commerce and Subscription Dairy

Online dairy sales are growing exponentially. Amazon Fresh, Walmart+, Instacart, and direct-to-consumer milk-delivery start-ups are reshaping how households source dairy, particularly in metropolitan markets.

3. Premium Cheese and Specialty Formats

Aged cheddar, artisanal blue cheese, fresh mozzarella, and Hispanic-style cheese are commanding share gains within the cheese aisle. Specialist retailers and natural-food chains have expanded dedicated cheese counters during 2023-2025.

4. Lactose-Free and Functional Dairy

Lactose-free milk accounted for 4% of United States fluid-milk sales, up sharply from a decade earlier. Probiotic and fibre-fortified yogurts continue to gain shelf space across mainstream supermarkets.

5. Sustainable Packaging and Methane-Reduction Pledges

Carton-based milk packaging, mono-material plastic tubs, and recyclable cheese wraps are becoming retail-buyer requirements. Several United States dairy cooperatives have signed Net-Zero 2050 pledges and started feed-additive trials to lower enteric methane emissions.

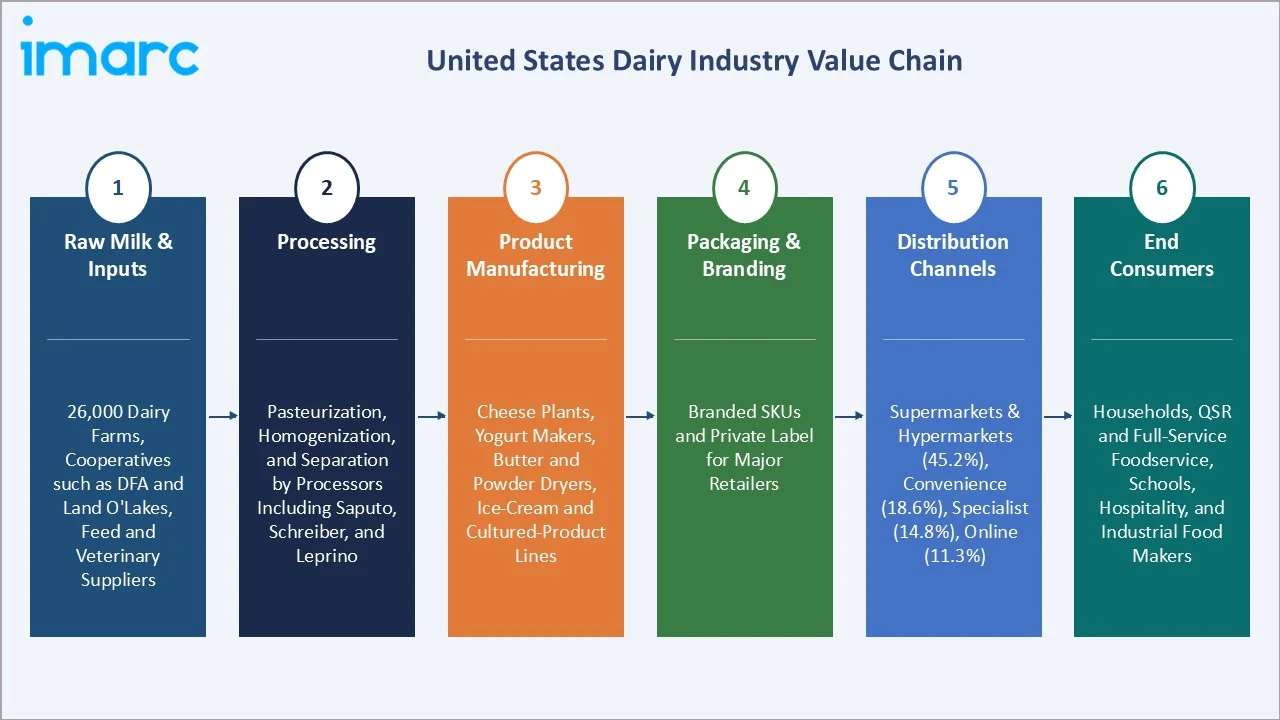

Industry Value Chain Analysis

The United States dairy industry value chain spans six integrated stages from raw-milk supply through end-consumer purchase. Each stage shows distinct margin profiles, scale economics, and capital intensity that shape the broader United States dairy market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Raw Milk & Inputs |

26,000 dairy farms, cooperatives such as DFA and Land O'Lakes, feed and veterinary suppliers |

|

Processing |

Pasteurization, homogenization, and separation by processors including Saputo, Schreiber, and Leprino |

|

Product Manufacturing |

Cheese plants, yogurt makers, butter and powder dryers, ice-cream and cultured-product lines |

|

Packaging & Branding |

Branded SKUs and private label for major retailers |

|

Distribution Channels |

Supermarkets & hypermarkets (45.2%), convenience (18.6%), specialist (14.8%), online (11.3%) |

|

End Consumers |

Households, QSR and full-service foodservice, schools, hospitality, and industrial food makers |

Cooperatives and large branded processors capture the highest strategic value by combining farm-side milk pooling with downstream branding and distribution. E-commerce and specialty retail are reshaping distribution by enabling smaller premium brands to reach consumers without nationwide cold-chain footprints.

Technology Landscape in the United States Dairy Industry

Processing and Membrane Filtration

Ultra-filtration and reverse-osmosis technologies are now standard for protein-concentrated milk and skim formats. Filtered milks such as Fairlife have grown into a multi-billion-dollar United States sub-category since their introduction, supporting higher-protein liquid milk formats across the country.

Materials and Packaging Innovation

Aseptic carton packaging, mono-material PET tubs, and lighter-weight HDPE bottles are reducing per-unit packaging weight by 8-15% across major dairy SKUs. Several leading processors committed to 100% recyclable or compostable packaging by 2030 in their 2024 sustainability reports.

Smart Connectivity and Cold-Chain Telemetry

IoT-enabled cold-chain monitoring is now embedded in most national dairy distribution networks. Real-time temperature dashboards, predictive-maintenance sensors on processors, and AI-based demand forecasting tools have improved freshness and reduced shrink at major United States grocery chains during 2023-2025.

Automation and Plant Modernization

Robotic case-packing, automated CIP (clean-in-place) systems, and computer-vision quality inspection are spreading across high-volume cheese and yogurt plants. Capital investment in United States dairy-plant automation rose materially in 2024, helping mitigate persistent processing-labour shortages.

Market Segmentation Analysis

IMARC Group provides an analysis of the key trends in each segment of the United States dairy market, along with forecasts at the national and regional level from 2026 to 2034. The market has been categorized based on product and distribution channel.

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product | Cheese | 24.5% | 2025 |

| Application | Bakery and Confectionary | 32.6% | 2025 |

| Distribution Channel | Supermarkets and Hypermarkets | 45.2% | 2025 |

| Region | Midwest | 28.4% | 2025 |

By Product

Cheese leads the United States dairy market product mix with a 24.5% share in 2025. Demand is anchored by pizza-driven foodservice volumes and a wave of cheese-based snacking innovations across major supermarket chains. Per-capita United States cheese consumption reached approximately 41.8 pounds in 2024, the highest level on record. Mozzarella, cheddar, and Hispanic-style cheeses contribute the majority of category volume, while specialty and aged cheeses drive premium-tier value growth.

To access detailed market analysis, Request Sample

Liquid milk holds 23.8% of product revenue and remains a household staple supported by school-meal programmes and family consumption. Yogurt and curd contribute 17.6%, with high-protein Greek and Icelandic skyr formats leading category innovation. Butter and clarified butter account for 12.9%, supported by retail baking and clean-label cooking trends, while laban contributes 8.7% on the strength of ethnic-store and natural-channel placement. The Others segment, at 12.5%, includes cream, ice cream, condensed milk, and dry powders.

By Distribution Channel

Supermarkets and hypermarkets are the dominant distribution channel at 45.2% of United States dairy revenue in 2025. This share reflects entrenched cold-chain infrastructure across chains such as Kroger, Walmart, Albertsons, and Publix, alongside strong private-label penetration in milk, cheese, and yogurt. Weekly basket-shopping habits and Sunday-circular promotions continue to anchor large-format retail as the consumer's primary dairy-purchase venue.

Convenience stores represent 18.6% of channel value, supported by single-serve milk, yogurt, and cheese-based snack purchases tied to fuel-station and quick-stop occasions. Specialist retailers, at 14.8%, include cheese counters, natural-food chains such as Whole Foods Market and Sprouts, and ethnic supermarkets that drive premium and specialty volume. Online stores account for 11.3% and are the fastest-growing channel, advancing at an estimated 5.8% CAGR through 2034 on the back of Amazon Fresh, Walmart+, Instacart, and direct-to-consumer milk-delivery models. The Others segment (10.1%) covers vending, military commissaries, and institutional contracts.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Midwest |

28.4% |

Wisconsin cheese hub, intensive dairy herds in Minnesota, Iowa, and Illinois, ingredient export lanes |

|

South |

26.7% |

Population growth in Texas, Florida, Georgia; expanding Hispanic-style cheese and yogurt categories |

|

West |

23.5% |

California's largest milk-producing state status, premium organic and lactose-free demand |

|

Northeast |

21.4% |

Dense urban consumption, premium specialty cheese and yogurt, strong foodservice base in NYC, Boston, Philadelphia |

The Midwest leads with a 28.4% revenue share in 2025. Wisconsin remains the country's premier cheese-making cluster, while Minnesota, Iowa, and Illinois support large-scale milk processing and ingredient supply to industrial buyers. The region also serves as the export gateway for United States cheese shipments to Mexico, Canada, and key Asian markets, reinforcing its structural cost and scale advantages.

The South holds 26.7% of revenue, supported by sustained population inflows into Texas, Florida, and Georgia. Hispanic-style cheese, drinkable yogurts, and ready-to-drink dairy beverages have all expanded faster than the national average across Southern retail formats during 2023-2025.

The West contributes 23.5%, anchored by California's position as the largest milk-producing state and home to several of the country's largest dairy processors. Premium organic, grass-fed, and lactose-free dairy SKUs over-index in the region, particularly in California, Oregon, and Washington. The Northeast accounts for 21.4%, driven by dense metropolitan consumption, vibrant foodservice activity, and a strong appetite for premium specialty cheese, artisanal yogurt, and high-end ice cream across New York, Boston, and Philadelphia.

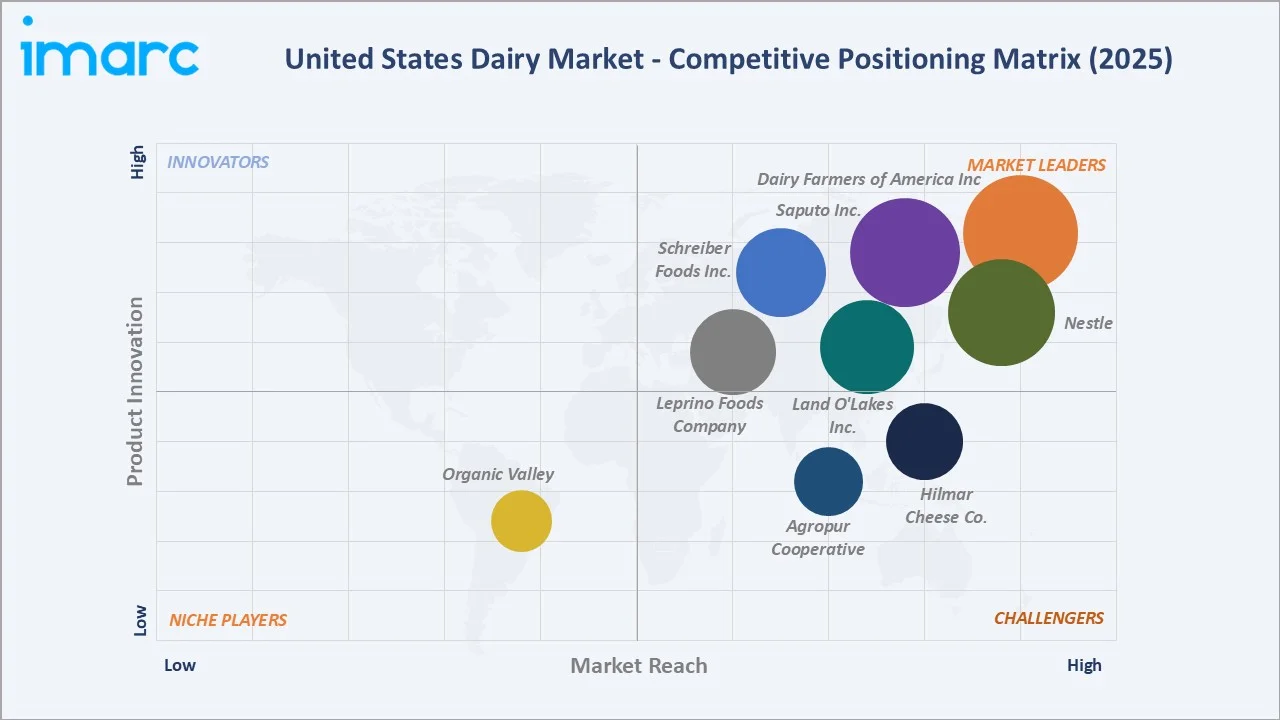

Competitive Landscape

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

|

Dairy Farmers of America Inc |

Borden, Alta Dena, Breakstone’s |

Leader |

Largest United States milk cooperative, ingredient and branded scale |

|

Nestle |

Carnation |

Leader |

Branded creamers, premium ice cream, distribution scale |

|

Saputo Inc. |

Frigo, Montchevre, Dairystar |

Leader |

Cheese specialist, mozzarella and specialty cheese leadership |

|

Land O'Lakes Inc. |

Land O'Lakes |

Leader |

Iconic butter brand, deli cheese, cooperative model |

|

Schreiber Foods Inc. |

Schreiber Foods |

Leader |

Largest private-label cheese supplier in the US |

|

Leprino Foods Company |

Leprino Cheese, Leprino Nutrition |

Leader |

World's largest mozzarella producer, foodservice supply |

|

Hilmar Cheese Company Inc. |

Hilmar Cheese |

Challenger |

Cheese and whey-protein scale, West Coast operations |

|

Agropur Cooperative |

Natrel, Oka, Grand Cheddar |

Challenger |

Cheese, whey, and protein ingredients in United States plants |

|

Organic Valley |

Organic Valley |

Emerging |

Largest United States organic dairy cooperative, premium positioning |

The competitive landscape in the United States dairy market is moderately fragmented. Large national cooperatives compete with branded processors, private-label specialists, and a long tail of regional creameries. Players differentiate through cheese specialization, branded yogurt portfolios, organic and grass-fed positioning, and ingredient-grade dairy supply to industrial buyers. Strategic acquisitions remain active - Lactalis, Saputo, and Agropur have all completed United States dairy bolt-on deals in recent years to extend scale and category coverage.

Key Company Profiles

Dairy Farmers of America Inc.

Dairy Farmers of America is the largest dairy cooperative in the United States, headquartered in Kansas City, Kansas. Founded in 1998 through the merger of four regional cooperatives, DFA represents thousands of family farms across more than 45 states.

- Product & Platform Portfolio: DFA's portfolio spans branded fluid milk (Borden, Kemps), butter (Plugra, Keller's), cultured products, and a broad ingredient business covering milk powders, cheese, and whey for industrial buyers.

- Recent Developments: In 2023, Dairy Farmers of America secured over $22 million in USDA funding to implement a pilot program across member farms, supporting the adoption of feed additives to reduce enteric methane emissions and enabling farmer participation in carbon credit markets.

- Strategic Focus: DFA's strategy centres on scaling value-added branded businesses, expanding ingredient exports, and supporting member farms with sustainability, technology, and animal-welfare programmes through 2034.

Nestle

Nestle USA is the American arm of the global Nestle group, headquartered in Arlington, Virginia. Its dairy operations span coffee creamers, ice cream, sweetened condensed milk, and infant nutrition, supported by an extensive United States manufacturing and distribution footprint.

- Product & Platform Portfolio: Key dairy brands include Coffee-mate creamers, Carnation evaporated and condensed milks, Haagen-Dazs ice cream (United States distribution), and Nesquik flavoured milks. The portfolio targets retail, foodservice, and convenience-channel buyers.

- Recent Developments: In 2024–2025, Nestlé USA strengthened its position in the United States coffee creamer market by expanding product innovation—particularly with new formats like cold foam and reduced-sugar variants—while ramping up manufacturing capacity through major investments, including a new large-scale creamer facility to support growing demand and future innovation.

- Strategic Focus: Nestle USA's strategy focuses on premiumization of creamers and ice cream, hybrid dairy and plant-based formats, and aggressive innovation across away-from-home coffee partnerships and direct-to-consumer e-commerce platforms.

Saputo Inc

Saputo is the United States subsidiary of Canadian dairy major Saputo Inc., one of the largest cheese producers in the world. Its United States operations are headquartered in Lincolnshire, Illinois, and span more than 25 manufacturing plants across the country.

- Product & Platform Portfolio: Saputo's United States cheese portfolio includes Frigo, Stella, Treasure Cave, Black Creek, and Friendship Dairies, alongside extensive private-label and foodservice cheese production for major QSR and retail chains.

- Recent Developments: In 2024, Saputo advanced its U.S. network optimization strategy by closing and consolidating selected facilities, streamlining production, and scaling automated operations—particularly in its cheese network—to improve efficiency and capacity utilization, while prioritizing investments aligned with higher-value product segments.

- Strategic Focus: Saputo's strategic focus centres on premium specialty cheese, whey-protein ingredient growth, foodservice partnerships, and operational efficiency across its United States cheese-manufacturing footprint through 2034.

Market Concentration Analysis

The United States dairy market exhibits moderate concentration. The top five players - Dairy Farmers of America, Nestle USA, Saputo Dairy USA, Land O'Lakes, and Schreiber Foods - collectively account for an estimated 32-38% of United States dairy market revenue in 2025. The remaining share is distributed across Leprino, Hilmar, Agropur, Organic Valley, and a long tail of regional cooperatives, branded creameries, and private-label specialists.

The market is experiencing a bifurcated dynamic. At the cheese and ingredient tier, consolidation is accelerating around scale, automation, and export capability. Within branded dairy, premium and specialty players such as Chobani, Tillamook, and Organic Valley are gaining shelf space against legacy national brands. This dual trend is intensifying competition across all product categories and price tiers through 2034.

Investment & Growth Opportunities

Fastest-Growing Segments

Online distribution represents the highest-growth channel sub-segment at approximately 5.8% CAGR through 2034. Cheese remains the largest absolute-dollar growth product category, while yogurt's high-protein and probiotic sub-segments deliver some of the strongest unit-volume gains across United States retail.

Emerging Sub-Markets

Lactose-free dairy, A2 protein milk, organic and grass-fed butter, and Hispanic-style cheese all represent above-trend growth pockets for incumbent players and venture-backed entrants. Cottage cheese, after a multi-year decline, returned to strong double-digit retail growth in 2024 on the back of social-media-led brand revival.

Venture and Strategic Investment Trends

Strategic acquisitions continue to reshape the competitive set. Saputo, Lactalis, and Agropur have completed multiple United States dairy bolt-on deals in recent years. Venture and growth-equity capital is being directed at lactose-free brands, hybrid dairy and plant-based formats, AI-led demand-forecasting tools, and on-farm methane-reduction technologies through 2034.

Future Market Outlook (2026-2034)

The United States dairy market forecast projects steady value expansion from USD 252.57 Billion in 2025 to USD 343.65 Billion by 2034 at a CAGR of 3.00%. The Midwest is expected to retain regional leadership, while the South continues to add population-led volume. Premium cheese, high-protein yogurt, and lactose-free milk are forecast to outpace overall category growth.

Three structural shifts will shape the United States dairy market through 2034. First, protein-forward and functional dairy will move from niche to mainstream across milk, yogurt, and cottage cheese. Second, online and quick-commerce channels will keep gaining share at the expense of traditional convenience formats. Third, sustainability commitments and federal climate policy will reshape on-farm practices, packaging design, and supply-chain transparency requirements across major United States dairy processors.

Research Methodology

Primary Research

Primary research included structured interviews conducted in 2024-2025 with United States dairy stakeholders, including category managers at major retailers, plant directors at processors, foodservice procurement leads, and dairy-cooperative executives. These interviews validated market sizing, segmentation estimates, and category-growth assumptions.

Secondary Research

Secondary sources included USDA Dairy Data, United States Census Bureau food expenditure surveys, Federal Milk Marketing Order publications, BLS price indices, the IDFA Dairy Delivers reports, company annual reports, and trade publications such as Dairy Foods, Cheese Market News, and Hoard's Dairyman.

Forecasting Models

Market size estimates and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating per-capita consumption trends, household disposable income, foodservice traffic indicators, and historical category-evolution patterns. Scenario analysis was performed across base, optimistic, and conservative cases.

United States Dairy Market Report Scope

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Liquid Milk, Cheese, Laban, Yogurt and Curd, Butter and Clarified Butter, Others |

| Applications Covered | Bakery and Confectionary, Clinical Nutrition, Frozen Food, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Convenience Stores, Specialist Retailers, Online Stores, Others |

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered | Dairy Farmers of America Inc, Nestle, Saputo Inc., Land O'Lakes Inc., Schreiber Foods Inc., Leprino Foods Company, Hilmar Cheese Company Inc., Agropur Cooperative, Organic Valley, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the United States Dairy Market Report

The United States dairy market was valued at USD 252.57 Billion in 2025, supported by strong cheese demand, school-meal milk programmes, foodservice rebound, and steady household consumption across all four United States census regions.

The market is projected to reach USD 343.65 Billion by 2034, growing at a CAGR of 3.00% during 2026-2034, supported by protein-forward dairy, e-commerce expansion, and sustained cheese export growth from United States processors.

Cheese leads with a 24.5% share in 2025, driven by pizza-driven foodservice volumes, surging cheese-snacking innovation across supermarkets, and record-high United States per-capita cheese consumption near 41.8 pounds annually.

Supermarkets and hypermarkets dominate at 45.2% in 2025, supported by entrenched cold-chain infrastructure, deep private-label penetration across Kroger, Walmart, and Albertsons, and weekly basket-shopping habits among United States households.

Online stores are the fastest-growing channel, advancing at an estimated 5.8% CAGR through 2034, supported by Amazon Fresh, Walmart+, Instacart, and a wave of direct-to-consumer milk and yogurt subscription models.

The Midwest leads with a 28.4% share in 2025. Wisconsin's cheese cluster and intensive dairy herds in Minnesota, Iowa, and Illinois underpin the region's structural production and export advantages within the country.

Key drivers include high-protein dairy demand, record cheese and yogurt consumption, foodservice channel rebound, premiumization of creamers and butter, and continued growth in lactose-free, organic, and clean-label dairy formats.

Major players include Dairy Farmers of America Inc, Nestle, Saputo Inc., Land O'Lakes Inc., Schreiber Foods Inc., Leprino Foods Company, Hilmar Cheese Company Inc., Agropur Cooperative, Organic Valley.

Plant-based beverage competition, feed and energy cost volatility, lactose and saturated-fat health perceptions, and evolving FDA labelling and packaging requirements are the main near-term restraints facing United States dairy market participants.

High-protein Greek and Icelandic-style yogurt formats are the fastest-growing yogurt sub-segments, advancing well above the broader category average and supported by GLP-1 medication users, gym-goers, and active-aging consumers.

Sustainability is reshaping packaging, on-farm methane reduction, and Scope 3 reporting. Major cooperatives have committed to Net-Zero 2050 pathways, recyclable packaging, and feed-additive trials to reduce enteric methane through 2034.

Investment opportunities include lactose-free and A2 milk, premium specialty cheese, high-protein cottage cheese and yogurt, online dairy retail, and digital cold-chain monitoring platforms across the United States dairy supply chain.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)