United States Dry Eye Syndrome Market Size, Share, Trends and Forecast by Disease Type, Drug Type, Product, Distribution Channel, and Region, 2026-2034

United States Dry Eye Syndrome Market Size, Share, Trends & Forecast (2026-2034)

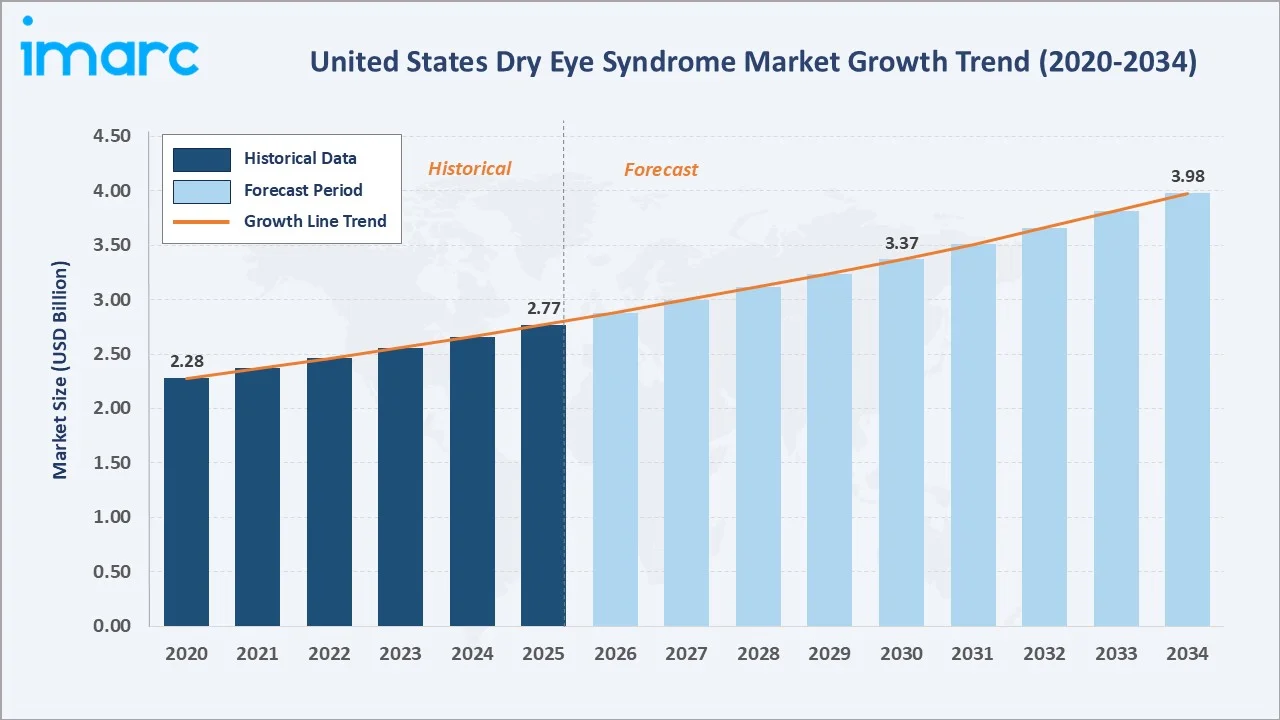

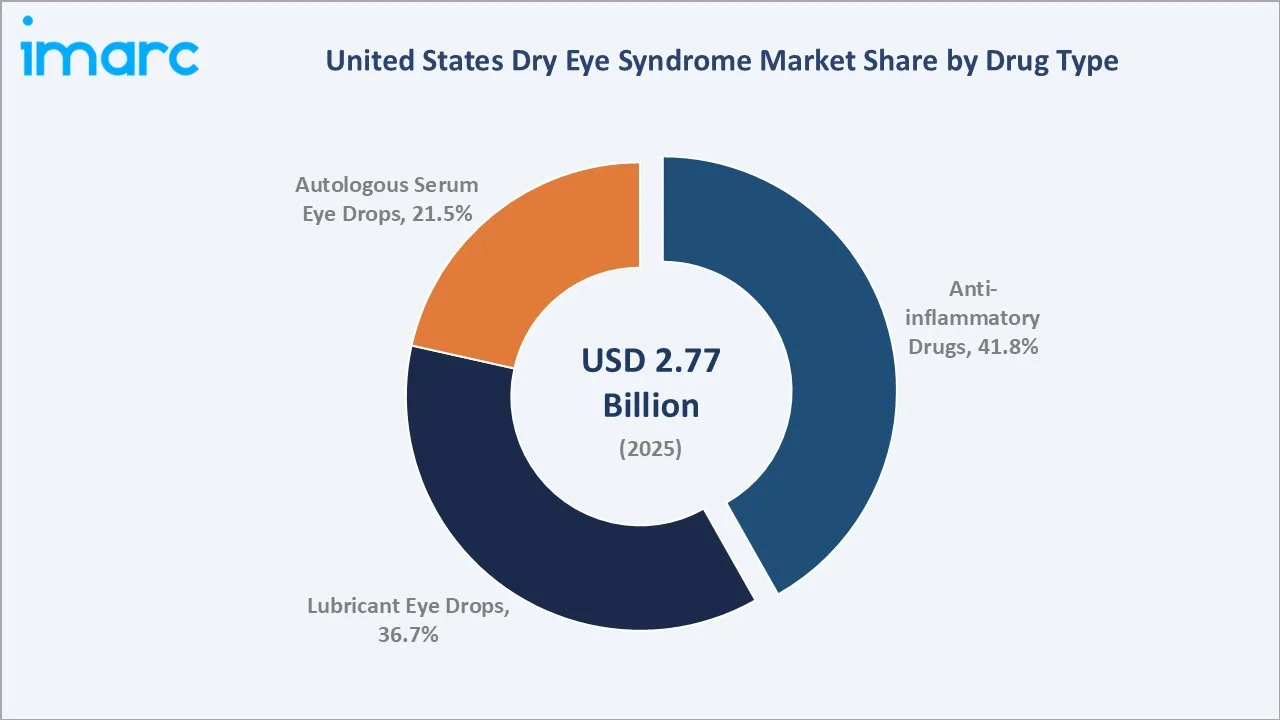

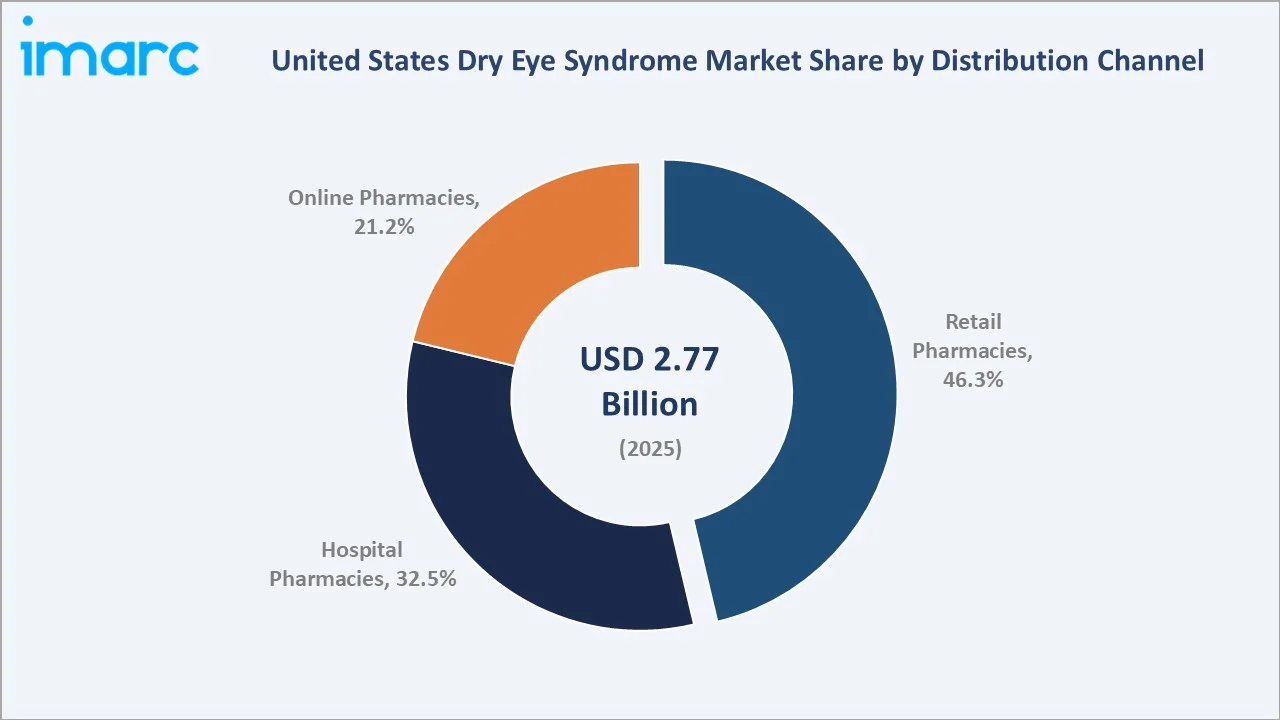

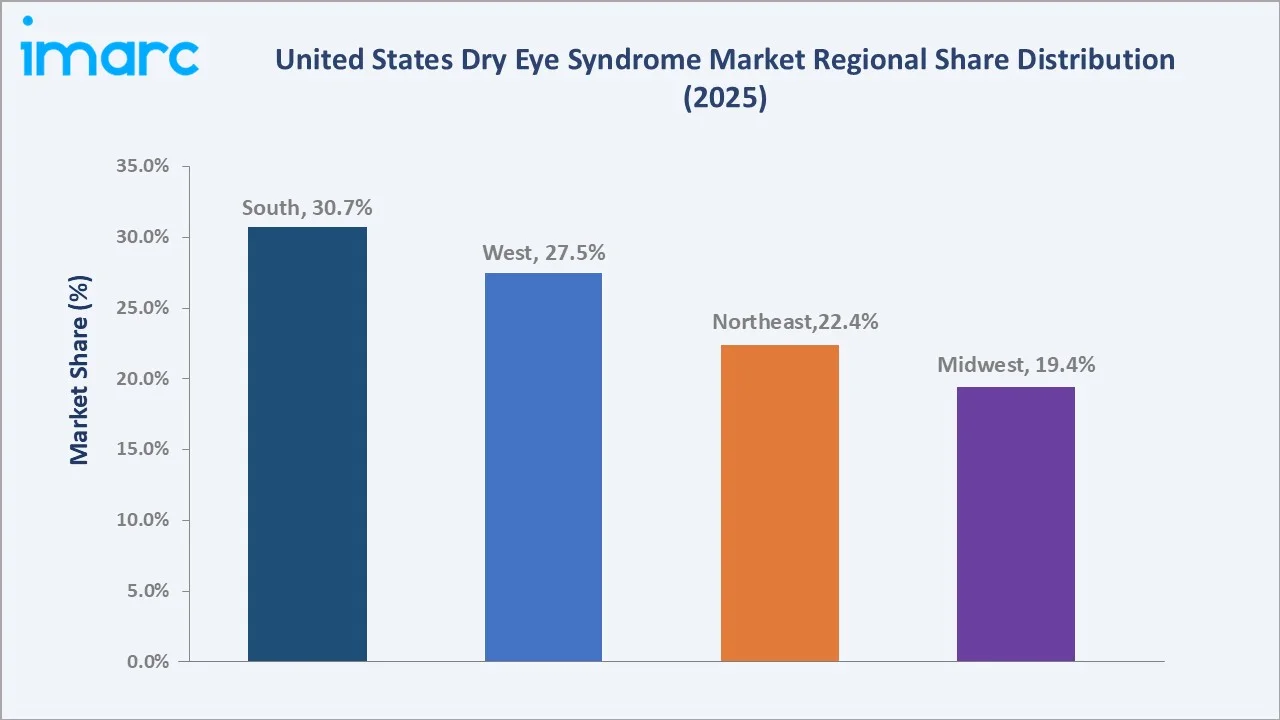

The United States dry eye syndrome market size was valued at USD 2.77 Billion in 2025 and is projected to reach USD 3.98 Billion by 2034, exhibiting a CAGR of 3.98% during 2026-2034. Rising prevalence among aging populations, growing digital screen exposure, expanding tele-ophthalmology platforms, and recent novel drug launches are collectively driving market growth. Anti-inflammatory drugs lead the United States dry eye syndrome market with a 41.8% share in 2025, while retail pharmacies dominate distribution at 46.3%. The Southern region commands the largest regional share at 30.7%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2.77 Billion |

|

Forecast Market Size (2034) |

USD 3.98 Billion |

|

CAGR (2026-2034) |

3.98% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

South (30.7% share, 2025) |

|

Fastest Growing Region |

West |

|

Leading Drug Type |

Anti-inflammatory Drugs (41.8%, 2025) |

|

Leading Distribution Channel |

Retail Pharmacies (46.3%, 2025) |

The chart below illustrates United States dry eye syndrome market size trends from 2020 through 2034, showing steady historical recovery and forecast expansion driven by therapy innovation.

To get more information on this market, Request Sample

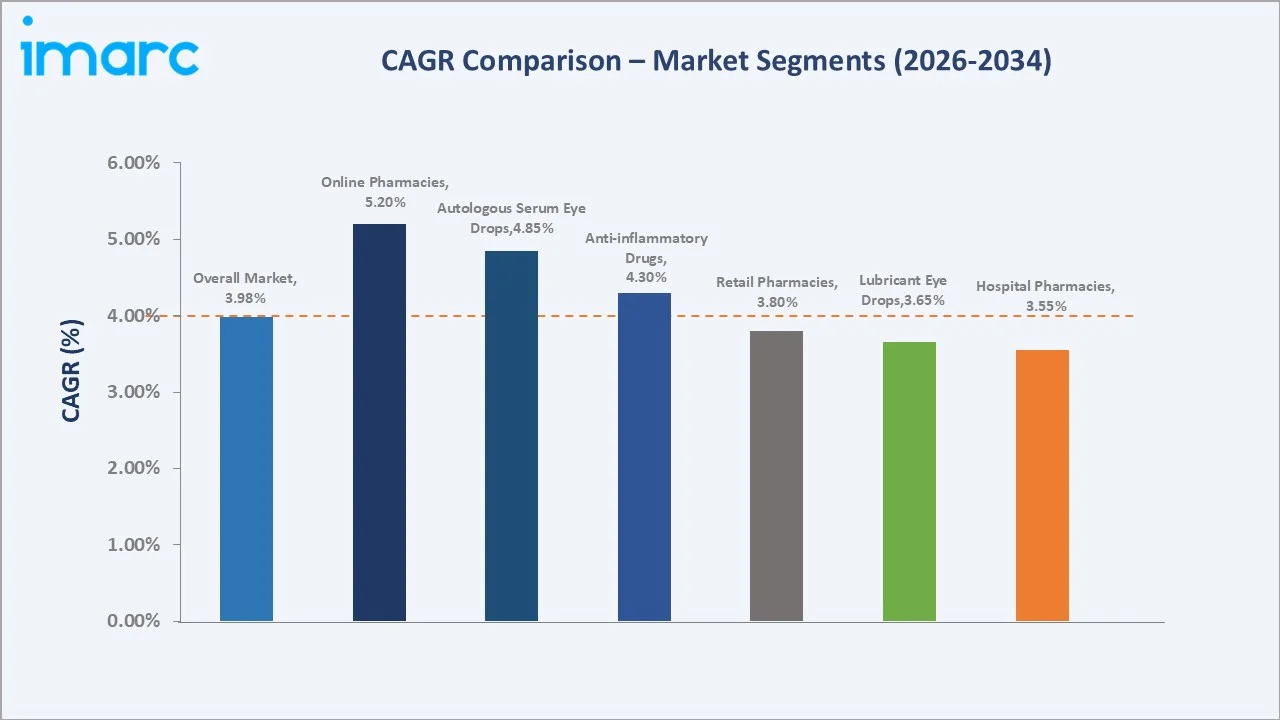

CAGR analysis identifies online pharmacies and autologous serum eye drops as the fastest-growing segments through 2034, reflecting digital adoption and personalized therapy demand.

Executive Summary

The United States dry eye syndrome market is expanding due to demographic aging, prolonged digital device use, and a steady stream of novel pharmaceutical approvals. Valued at USD 2.77 Billion in 2025, the market is projected to reach USD 3.98 Billion by 2034 at a 3.98% CAGR.

Anti-inflammatory drugs lead with a 41.8% share in 2025, driven by prescription therapies such as Restasis, Xiidra, Cequa, and newer treatments like Miebo. Lubricant eye drops hold 36.7%, supported by strong over-the-counter demand and leading brands such as Systane and Refresh, widely used for symptomatic dry eye relief. Retail pharmacies dominate distribution at 46.3%, reflecting widespread OTC availability and prescription dispensing through major chains like CVS Health, Walgreens, and Walmart.

The South leads regionally with a 30.7% share in 2025, driven by population size and high diagnostic rates. The West is the fastest-growing region, supported by digital health innovation hubs across California and Washington. Tele-ophthalmology, AI-based diagnostics, and biologic eye drops will reshape competitive dynamics through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Drug Type Segment |

Anti-inflammatory Drugs – 41.8% share (2025) |

|

Second Drug Type Segment |

Lubricant Eye Drops – 36.7% share (2025) |

|

Leading Distribution Channel |

Retail Pharmacies – 46.3% share (2025) |

|

Leading Region |

South – 30.7% (2025) |

|

Second Region |

West – 27.5% (2025) |

|

Top Companies |

AbbVie, Bausch + Lomb, Alcon, Sun Pharmaceutical |

Key Analytical Observations Supporting the Above Data:

- Anti-inflammatory drugs' 41.8% dominance in 2025 reflects strong reliance on prescription therapies including Restasis, Xiidra, Cequa, and Miebo, particularly among patients with moderate-to-severe dry eye disease.

- Lubricant Eye Drops' 36.7% share in 2025 captures over-the-counter lubricant brands such as Systane, Refresh, and TheraTears, used by patients managing mild and intermittent dry eye symptoms across all age groups.

- Retail pharmacies' 46.3% share in 2025 highlight the central role of national chains including CVS Health, Walgreens, and Walmart, which provide accessible prescription fulfillment and OTC eye drop categories nationwide.

- The South's 30.7% revenue share in 2025 reflects a high concentration of older adults in Florida and Texas, combined with elevated diabetes prevalence, both correlated with higher dry eye incidence rates.

- The West's 27.5% share and rapid growth is supported by digital workforce density in California, Washington, and Arizona, where prolonged screen exposure is accelerating evaporative dry eye case volumes.

- AbbVie's leadership through Restasis and Bausch + Lomb's 2023 acquisition of Xiidra reinforce ongoing consolidation in the United States dry eye therapeutics landscape, while smaller specialty players advance pipeline candidates.

United States Dry Eye Syndrome Market Overview

Dry eye syndrome, also called keratoconjunctivitis sicca or dry eye disease, is a multifactorial ocular surface condition causing discomfort, visual disturbance, and tear film instability with potential corneal damage.

The United States ecosystem includes pharmaceutical manufacturers, ophthalmologists, optometrists, retail and hospital pharmacies, online dispensaries, payers such as CMS and private insurers, and the FDA, which collectively shape diagnosis, prescribing, and patient access.

Prevalence is rising due to aging demographics, increasing digital screen hours, contact lens use, and post-LASIK ocular surface effects. The CDC estimates more than 16 million United States adults have been diagnosed with dry eye disease.

Market Dynamics

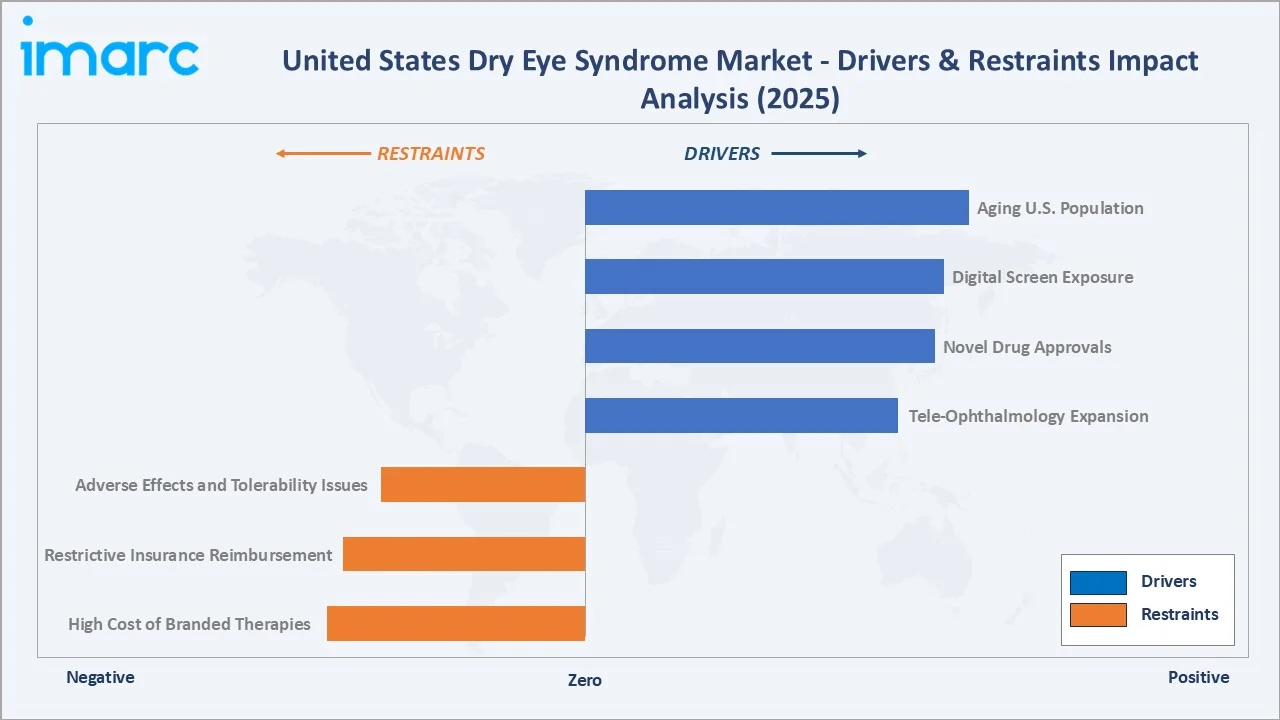

The figure below presents the relative impact of major drivers and restraints on the United States dry eye syndrome market in 2025, based on IMARC Group analytical scoring.

To evaluate market opportunities, Request Sample

Market Drivers

- Rising Prevalence Among Aging Populations: United States Census Bureau data show the population aged 65 and older surpassed 59 million in 2024 and will reach about 80 million by 2040, sharply expanding the dry eye patient pool, since prevalence increases with age-related tear film changes.

- Growing Digital Screen Exposure: Average daily screen time among United States adults exceeds 7 hours, contributing to evaporative dry eye and meibomian gland dysfunction, particularly among knowledge workers, students, and remote employees post-2020.

- Novel Drug Approvals: FDA approvals such as Bausch + Lomb's Miebo in May 2023 and Tarsus Pharmaceuticals' Xdemvy for Demodex blepharitis in July 2023 are expanding the therapeutic toolkit for ophthalmologists treating ocular surface diseases.

- Tele-Ophthalmology Expansion: Tele-ophthalmology platforms including Warby Parker virtual visits and Eyecare Live are improving early diagnosis and prescription continuity, particularly across underserved Southern and rural geographies.

Market Restraints

- High Cost of Branded Therapies: Branded prescription therapies such as Xiidra and Cequa are expensive, often resulting in high out-of-pocket costs for uninsured patients, which can limit affordability and adherence.

- Restrictive Insurance Reimbursement: Many private insurers require step therapy starting with OTC lubricants before approving prescription anti-inflammatory drugs, delaying treatment escalation for moderate-to-severe patients by several months.

- Adverse Effects and Tolerability Issues: Cyclosporine-based therapies such as Restasis and Cequa commonly cause burning or stinging upon application, while prolonged corticosteroid use may increase intraocular pressure, affecting patient adherence.

Market Opportunities

- Personalized Biologic Therapies: Autologous serum eye drops are gaining traction in the U.S. as customized biologic treatments for severe dry eye cases unresponsive to conventional therapy, with growing adoption across specialty clinics and compounding pharmacies.

- AI-Driven Diagnostic Tools: AI-based ocular surface imaging from companies including Oculus Keratograph and TearLab is enabling early-stage detection in primary care settings, expanding pre-symptomatic patient identification across optometry chains.

- Digital Pharmacy Channels: Online pharmacy platforms such as Amazon Pharmacy, GoodRx, and Mark Cuban Cost Plus Drug Company are expanding access to dry eye treatments through price transparency and convenient home delivery.

Market Challenges

- Underdiagnosis of Mild Cases: Dry eye disease remains underdiagnosed in the U.S., as mild symptoms are often mistaken for fatigue or allergies, leading to delayed clinical diagnosis and lower prescription uptake in early-stage patients.

- Generic Erosion of Legacy Brands: Loss of exclusivity for Restasis enabled generic cyclosporine alternatives from companies such as Viatris and Apotex, increasing price competition and impacting branded drug revenues.

- Patient Adherence and Persistence Issues: Patients frequently discontinue dry eye treatments due to slow onset of relief, frequent dosing requirements, and discomfort on instillation, which reduces long-term adherence and limits treatment effectiveness.

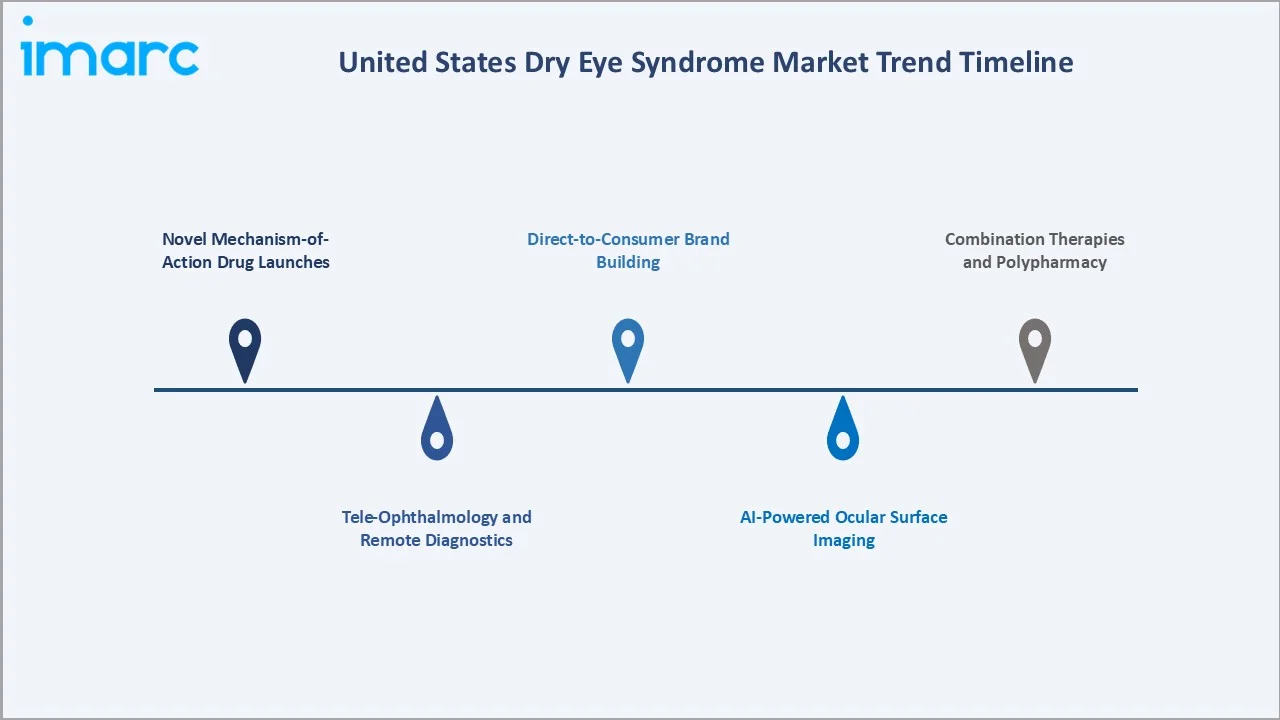

Emerging Market Trends

1. Novel Mechanism-of-Action Drug Launches

Therapies such as Miebo (perfluorohexyloctane) for evaporative dry eye and Tyrvaya (varenicline) nasal spray for tear stimulation represent breakthrough mechanisms beyond traditional lubrication and immunomodulation, expanding treatment options for refractory United States patients.

2. Tele-Ophthalmology and Remote Diagnostics

Adoption of tele-ophthalmology and remote eye care solutions has accelerated in the U.S., with platforms such as EyecareLive and DigitalOptometrics enabling virtual consultations, diagnosis, and digital prescription workflows across multiple states.

3. AI-Powered Ocular Surface Imaging

AI-enhanced devices including Oculus Keratograph 5M, TearLab Osmolarity System, and Bruder iLux are entering optometrist offices, improving objective diagnosis of meibomian gland dysfunction and accelerating early intervention.

4. Direct-to-Consumer Brand Building

Direct-to-consumer platforms such as Hims & Hers Health and Ro primarily offer subscription-based telehealth services and medication delivery across categories like hair loss and wellness, while ocular-specific offerings remain limited; Hubble focuses on vision products rather than dry eye therapies.

5. Combination Therapies and Polypharmacy

Ophthalmologists increasingly prescribe combination regimens anti-inflammatory plus lubricant plus omega-3 supplementation improving outcomes while creating bundled prescription opportunities across pharmaceutical portfolios.

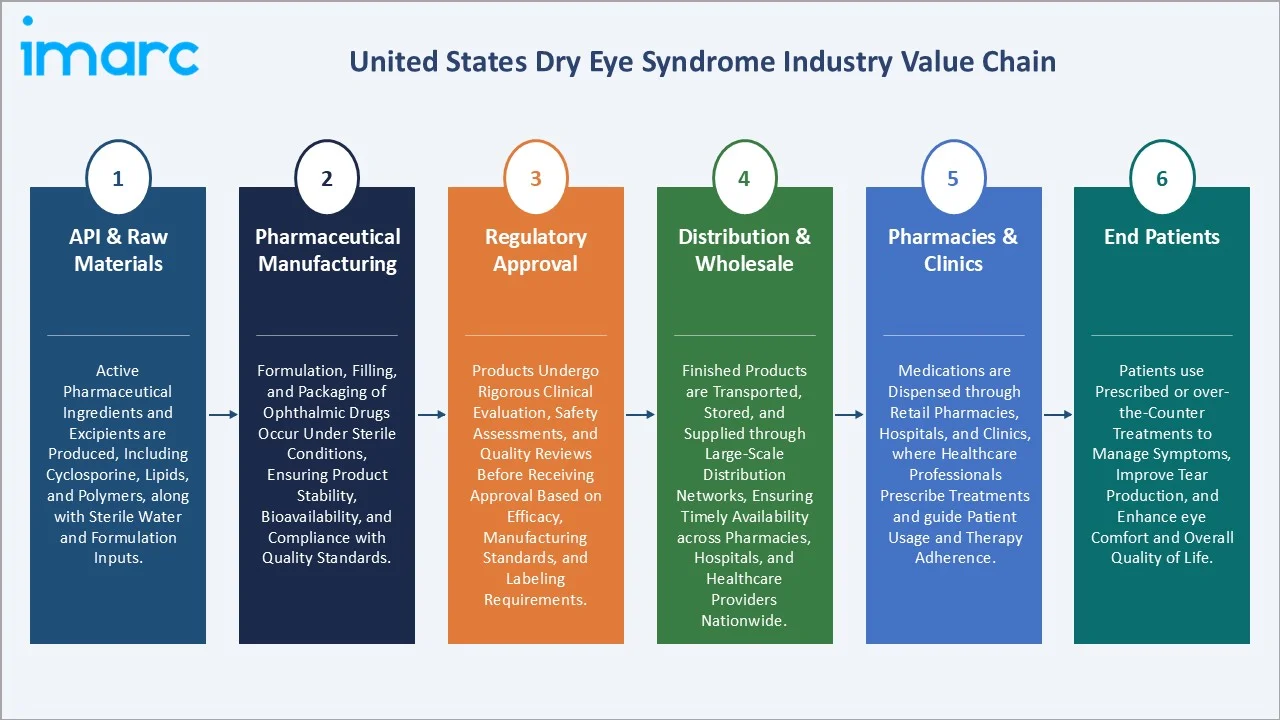

Industry Value Chain Analysis

The United States dry eye syndrome value chain spans six stages, from API sourcing through manufacturer-led distribution to clinical dispensing, each with distinct margin structures and regulatory checkpoints.

|

Stage |

Key Players / Examples |

|

API & Raw Materials |

Active pharmaceutical ingredients and excipients are produced, including cyclosporine, lipids, and polymers, along with sterile water and formulation inputs. |

|

Pharmaceutical Manufacturing |

Formulation, filling, and packaging of ophthalmic drugs occur under sterile conditions, ensuring product stability, bioavailability, and compliance with quality standards. |

|

Regulatory Approval |

Products undergo rigorous clinical evaluation, safety assessments, and quality reviews before receiving approval based on efficacy, manufacturing standards, and labeling requirements. |

|

Distribution & Wholesale |

Finished products are transported, stored, and supplied through large-scale distribution networks, ensuring timely availability across pharmacies, hospitals, and healthcare providers nationwide. |

|

Pharmacies & Clinics |

Medications are dispensed through retail pharmacies, hospitals, and clinics, where healthcare professionals prescribe treatments and guide patient usage and therapy adherence. |

|

End Patients |

Patients use prescribed or over-the-counter treatments to manage symptoms, improve tear production, and enhance eye comfort and overall quality of life. |

Manufacturers like AbbVie and Bausch + Lomb hold the highest value position, capturing branded drug margins while controlling clinical evidence generation and prescriber engagement nationwide.

Technology Landscape in the United States Dry Eye Syndrome Industry

Drug Delivery Innovation

Preservative-free drops, non-aqueous formulations, and intranasal therapies are advancing dry eye treatment, with Miebo and Tyrvaya representing recent FDA-approved delivery innovations improving tear film stability and stimulation.

Diagnostic and Imaging Platforms

AI-enhanced devices such as TearLab Osmolarity System, Oculus Keratograph 5M, and LipiView II are improving objective diagnosis of meibomian gland dysfunction and tear film instability, supporting precision therapy decisions in United States ophthalmology practices.

Digital Health and Tele-Ophthalmology

Tele-ophthalmology expanded post-2020, with platforms like DigitalOptometrics and 1-800 Contacts enabling remote eye exams, consultations, and prescription services across multiple U.S. states, improving accessibility and continuity of care.

Personalized Medicine and Biologics

Compounding pharmacies are advancing autologous serum eye drops, platelet-rich plasma drops, and umbilical cord serum drops for severe dry eye. These biologic options serve patients unresponsive to first-line cyclosporine and lifitegrast prescriptions.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Disease Type |

🔒 |

🔒 |

2025 |

|

Drug Type |

Anti-inflammatory Drugs |

41.8% |

2025 |

|

Product |

🔒 |

🔒 |

2025 |

|

Distribution Channel |

Retail Pharmacies |

46.3% |

2025 |

|

Region |

South |

30.7% |

2025 |

By Drug Type

Anti-inflammatory drugs hold a 41.8% share in 2025, supported by established therapies like cyclosporine (Restasis, Cequa), lifitegrast (Xiidra), and corticosteroid Eysuvis, widely prescribed for managing moderate-to-severe inflammatory dry eye disease in clinical practice.

To access detailed market analysis, Request Sample

Lubricant eye drops account for 36.7% in 2025, with OTC brands like Systane, Refresh, TheraTears, and Soothe commonly used as first-line therapy for mild dry eye and digital eye strain. These products improve tear film stability and provide symptomatic relief. Autologous serum eye drops represent 21.5% in 2025, growing fastest at around 4.85% CAGR, supported by increasing use in severe or refractory dry eye, particularly in conditions such as Sjögren’s syndrome and ocular surface disease.

By Distribution Channel

Retail pharmacies command 46.3% of the United States dry eye syndrome market in 2025, supported by chains like CVS Health, Walgreens, Walmart, Rite Aid, and Kroger Health, distributing prescription treatments and OTC lubricant eye drops nationwide.

Hospital pharmacies hold 32.5% in 2025, supporting patients receiving prescriptions during ophthalmic procedures, autoimmune disease management, and post-surgical care within hospital systems and academic centers. Online pharmacies hold 21.2% in 2025 and are growing fastest at 5.2% CAGR, driven by platforms like Amazon Pharmacy, GoodRx, Mark Cuban Cost Plus Drug Company, and Health & Her, improving access, pricing transparency, and prescription refill convenience.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

South |

30.7% |

Largest aged-65+ population (Florida, Texas), high diabetes prevalence, robust ophthalmology network |

|

West |

27.5% |

Digital workforce density in California; technology hubs in Seattle and Phoenix; Hispanic market expansion |

|

Northeast |

22.4% |

High insurance coverage, dense academic medical centers, strong specialty ophthalmology infrastructure |

|

Midwest |

19.4% |

Aging Rust Belt populations, Mayo Clinic and Cleveland Clinic networks, agricultural occupational exposure |

The South commands 30.7% of the United States dry eye syndrome market in 2025, supported by Florida's large retired population (over 4.6 million aged 65+) and Texas's expanding metropolitan centers. Strong ophthalmology presence and tele-medicine penetration anchor regional revenue leadership.

The West holds 27.5% in 2025 and is the fastest-growing region, supported by high digital screen exposure and telehealth adoption across states like California and Washington. Innovation ecosystems in cities such as San Francisco and Seattle accelerate uptake of advanced diagnostics. The Northeast accounts for 22.4% in 2025, anchored by leading academic institutions including Mass Eye and Ear, Wills Eye Hospital, and NYU Langone Health, with strong insurance coverage improving access to advanced therapies. The Midwest holds 19.4% in 2025, supported by major care networks like Mayo Clinic and Cleveland Clinic, alongside higher occupational exposure contributing to dry eye prevalence.

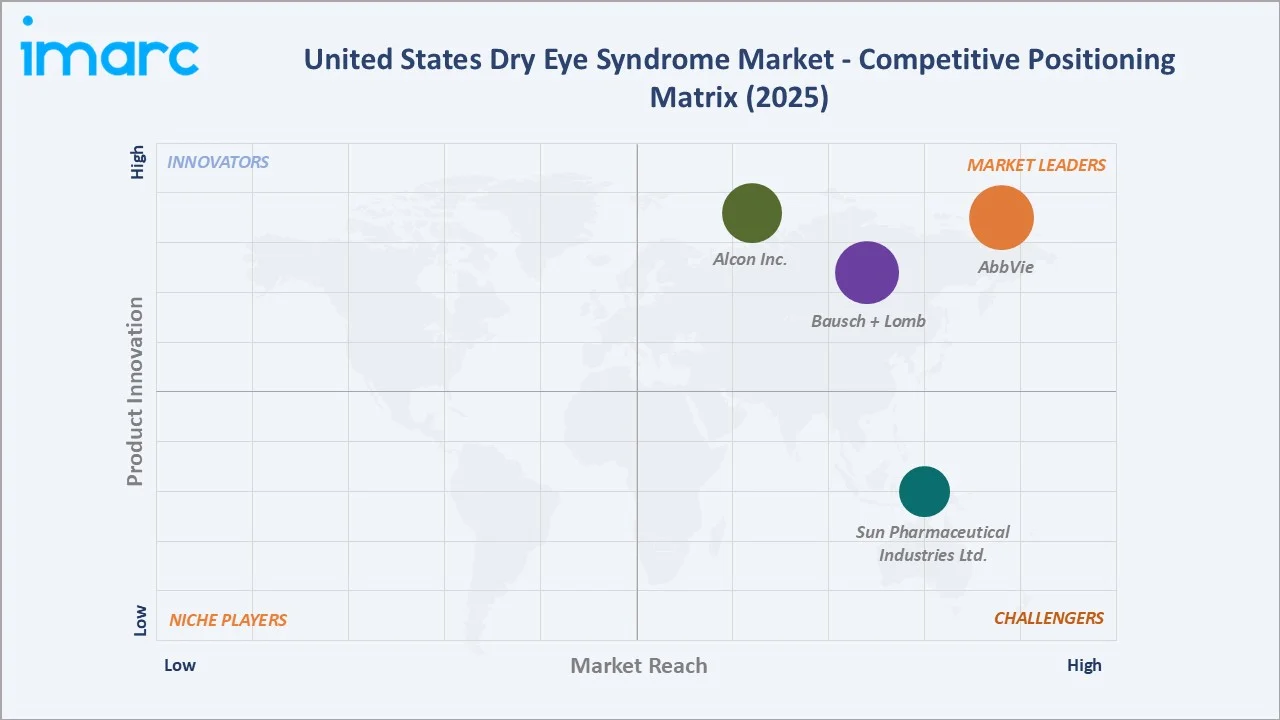

Competitive Landscape

|

Company Name |

Key Brand / Product |

Market Position |

Core Strength |

|

AbbVie |

Restasis / Refresh |

Leader |

Branded cyclosporine, OTC lubricants, broad ophthalmology portfolio |

|

Bausch + Lomb |

Xiidra / Miebo / Lumify |

Leader |

Lifitegrast leadership, breakthrough Miebo launch (2023) |

|

Alcon Inc. |

Systane |

Leader |

OTC lubricant leader, corticosteroid Eysuvis acquisition |

|

Sun Pharmaceutical Industries Ltd. |

Cequa |

Challenger |

Differentiated cyclosporine 0.09% formulation, United States specialty sales |

The United States dry eye syndrome market is dominated by key players such as AbbVie, Bausch + Lomb, and Alcon, supported by strong portfolios of prescription therapies and OTC eye care products. Bausch + Lomb's USD 1.75 billion acquisition of Xiidra from Novartis in 2023 reshaped competitive ranks materially.

Key Company Profiles

AbbVie Inc.

AbbVie, based in North Chicago, is a leading biopharmaceutical company that strengthened its eye care presence through the Allergan acquisition in 2020. Its portfolio includes dry eye therapies and OTC eye care products, contributing to its diversified immunology and neuroscience-driven revenue base.

- Product & Service Portfolio: Restasis, the Refresh® lubricating eye drop family, and glaucoma treatments such as Lumigan® and Alphagan®, addressing dry eye, ocular surface disease, and intraocular pressure management.

- Recent Developments: In 2024, AbbVie Inc. continues advancing ophthalmology innovation through its Allergan Eye Care portfolio, focusing on ocular surface disease, glaucoma, retina, and consumer eye care, while investing in next-generation therapies and early- to late-stage pipeline programs addressing unmet vision care needs.

- Strategic Focus: AbbVie focuses on retaining Restasis prescribers, expanding OTC Refresh share, and pursuing biologic and combination drug pipeline opportunities across ocular surface and aesthetics franchises.

Bausch + Lomb

Bausch + Lomb, headquartered in Vaughan, Canada, is a global eye health company with strong U.S. operations. In 2024, it generated approximately USD 4.79 billion in revenue, driven by pharmaceuticals, vision care, and surgical segments, with dry eye therapies forming a key growth pillar.

- Product & Service Portfolio: Xiidra, Miebo, Lumify redness reliever, Soothe and Biotrue lubricant eye drops, alongside contact lens and eye care solutions.

- Recent Developments: Bausch + Lomb Corporation completed the acquisition of Xiidra from Novartis AG in September 2023 for USD 1.75 billion upfront plus milestones, strengthening its prescription dry eye portfolio and expanding its ophthalmology pipeline and commercial capabilities.

- Strategic Focus: Bausch + Lomb focuses on expanding its U.S. dry eye leadership through Xiidra and Miebo commercialization, pipeline advancement, and strengthening its integrated prescription and OTC ocular surface portfolio.

Alcon Inc.

Alcon, headquartered in Geneva with major U.S. operations in Fort Worth, is a global leader in eye care. The company reported approximately USD 9.8 billion revenue in 2024, driven by surgical and vision care segments, with strong positioning in dry eye and ocular surface products.

- Product & Service Portfolio: Systane® lubricant eye drop family, Eysuvis for short-term dry eye treatment, Pataday allergy drops, and a broad range of contact lenses, solutions, and ophthalmic surgical devices.

- Recent Developments: Alcon Inc. expanded its Systane portfolio with the U.S. launch of Systane PRO Preservative-Free in 2025, featuring a triple-action formulation designed to support tear film stability and prolonged hydration, strengthening its over-the-counter dry eye leadership and reinforcing continued innovation in ocular surface care solutions.

- Strategic Focus: Alcon focuses on strengthening its dry eye leadership through Systane innovation, expanding prescription offerings like Eysuvis, and leveraging integrated surgical and vision care platforms across ophthalmology and optometry channels.

Market Concentration Analysis

The United States dry eye syndrome market is moderately concentrated. The top four companies — AbbVie, Bausch + Lomb, Alcon Inc., and Sun Pharmaceutical Industries Ltd. — collectively account for approximately 65% to 70% of branded prescription revenue in 2025, reflecting deep prescriber relationships and large commercial salesforces.

The United States OTC lubricant eye drop market is highly fragmented. Alongside Systane (Alcon Inc.) and Refresh (AbbVie Inc.), competing brands include Xiidra / Miebo / Lumify (Bausch + Lomb), TheraTears, OPTASE, and extensive private-label offerings from major United States retailers.

Consolidation is accelerating. Bausch + Lomb's USD 1.75 billion Xiidra acquisition from Novartis in 2023 and Alcon's 2022 Eysuvis rights acquisition from Kala Pharmaceuticals demonstrate strategic moves to capture premium-priced prescription products.

Following the loss of exclusivity for Restasis, multiple generic versions of cyclosporine ophthalmic emulsion 0.05% were launched in the U.S., including by Viatris increasing competition and contributing to pricing pressure in the dry eye prescription market.

Investment & Growth Opportunities

Fastest-Growing Segments

Online pharmacies are expanding rapidly in the U.S., driven by platforms like Amazon Pharmacy, GoodRx, and Cost Plus Drug Company, improving affordability and access. Specialty treatments such as autologous serum eye drops are gaining adoption in refractory cases.

Emerging Market Sub-Segments

Pediatric and adolescent dry eye, driven by digital device exposure in school-age populations, is emerging as an underserved segment. Post-LASIK dry eye management and Sjögren's syndrome care also represent specialty opportunities for high-margin biologic therapy positioning.

Venture & Strategic Investment Trends

Investment activity is increasing in novel dry eye therapies and diagnostics. Companies such as Aldeyra Therapeutics (reproxalap) and Tarsus Pharmaceuticals (lotilaner-based treatments) are advancing clinical pipelines. Additionally, AI-based ocular surface imaging and diagnostics platforms are attracting funding and partnerships from larger ophthalmology and pharmaceutical players.

Direct-to-consumer telehealth platforms such as Hims & Hers Health and Ro have attracted significant investor interest, reflecting broader funding trends in digital health. These platforms expand online access to consultations and OTC treatments, influencing distribution models and opening partnership opportunities for pharmaceutical companies in chronic conditions, including eye care.

Future Market Outlook (2026-2034)

The United States dry eye syndrome market forecast projects steady value expansion from USD 2.77 Billion in 2025 to USD 3.98 Billion by 2034 at a 3.98% CAGR — representing a value increase of more than USD 1.21 Billion through the forecast period.

Three transformational forces will reshape the market through 2034. First, novel therapies including Miebo, Tyrvaya, and pipeline candidates such as reproxalap will expand the addressable patient pool by addressing previously untreated mechanisms of dry eye disease. Second, AI-enabled ocular imaging and tele-ophthalmology are expected to enhance early detection and monitoring of dry eye disease by improving access and diagnostic accuracy. Third, online pharmacies are expanding rapidly in the U.S., supported by rising e-commerce adoption, telehealth integration, and home delivery models.

By 2034, United States dry eye care will evolve from intermittent symptom management into a proactive, technology-driven, personalized chronic disease model, supporting durable revenue growth for innovative pharmaceutical and digital health companies.

Research Methodology

Primary Research

Primary research included structured interviews and surveys conducted in 2024–2025 with United States ophthalmologists, optometrists, retail pharmacy buyers, hospital pharmacy directors, payer formulary managers, pharmaceutical commercial leads, and dry eye disease patients across all four United States census regions.

Secondary Research

Secondary sources include FDA approval records, company SEC 10-K filings (AbbVie, Bausch + Lomb, Alcon, Viatris), CDC health data, American Academy of Ophthalmology publications, IQVIA prescription data, United States Census Bureau demographics, and peer-reviewed ophthalmology journals.

Forecasting Models

Market size estimations and growth projections were derived using top-down and bottom-up forecasting models, integrating prescription volume trends, demographic projections, OTC retail sales data, payer reimbursement evolution, and scenario analysis under base, optimistic, and conservative assumptions.

United States Dry Eye Syndrome Market Report Coverage

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Disease Types Covered | Evaporative Dry Eye Syndrome, Aqueous Dry Eye Syndrome |

| Drug Types Covered | Anti-inflammatory Drugs, Lubricant Eye Drops, Autologous Serum Eye Drops |

| Products Covered | Liquid Drops, Gel, Liquid Wipes, Eye Ointment, Others |

| Distribution Channels Covered | Hospital Pharmacies, Retail Pharmacies, Online Pharmacies |

| Region Covered | Northeast, Midwest, South, West |

| Companies Covered | AbbVie, Bausch + Lomb, Alcon Inc., Sun Pharmaceutical Industries Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the United States Dry Eye Syndrome Market Report

The United States dry eye syndrome market was valued at USD 2.77 Billion in 2025, driven by aging populations, increasing digital screen exposure, and continued novel therapy launches across ophthalmology.

The market is projected to reach USD 3.98 Billion by 2034, growing at a CAGR of 3.98% during 2026-2034, supported by therapy innovation and tele-ophthalmology expansion across all United States regions.

Anti-inflammatory drugs lead with a 41.8% share in 2025, dominated by branded therapies including Restasis, Xiidra, Cequa, and the recently launched Miebo from Bausch + Lomb.

Retail pharmacies command a 46.3% share in 2025, anchored by national chains CVS Health, Walgreens, Walmart, and Rite Aid offering both prescription dry eye drugs and OTC lubricants.

The South leads with a 30.7% share in 2025, driven by Florida and Texas's large aged-65+ populations, high diabetes prevalence, and a robust ophthalmology and optometry network.

Key drivers include rising aged-65+ populations, increasing digital screen time, novel drug launches like Miebo and Xdemvy, tele-ophthalmology expansion, and growing autoimmune disease prevalence.

The West is the fastest-growing region, fueled by digital workforce density in California, technology hubs in Seattle and Phoenix, and rapid telehealth and AI diagnostic platform adoption.

Leading companies include AbbVie, Bausch + Lomb, Alcon Inc., Sun Pharmaceutical Industries Ltd. across branded and OTC categories.

Lubricant eye drops hold a 36.7% share in 2025, led by Systane, Refresh, TheraTears, and Soothe brands serving mild dry eye and digital eye fatigue cases nationwide.

AI-based ocular imaging, tele-ophthalmology platforms, online pharmacies, and novel drug delivery formats are improving diagnosis, expanding access, and enabling personalized management of dry eye disease.

Online pharmacies hold 21.2% in 2025 and are growing at 5.2% CAGR, led by Amazon Pharmacy, GoodRx, Mark Cuban Cost Plus Drug Company, and DTC platforms like Hims & Hers.

Unmet needs in evaporative dry eye, refractory inflammation, and tear stimulation are driving launches such as Miebo, Tyrvaya, and Xdemvy, expanding mechanisms beyond traditional cyclosporine therapy.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)