United States Energy as a Service Market Size, Share, Trends and Forecast by Service Type, End User, and Region, 2026-2034

United States Energy as a Service Market Size, Share, Trends & Forecast (2026-2034)

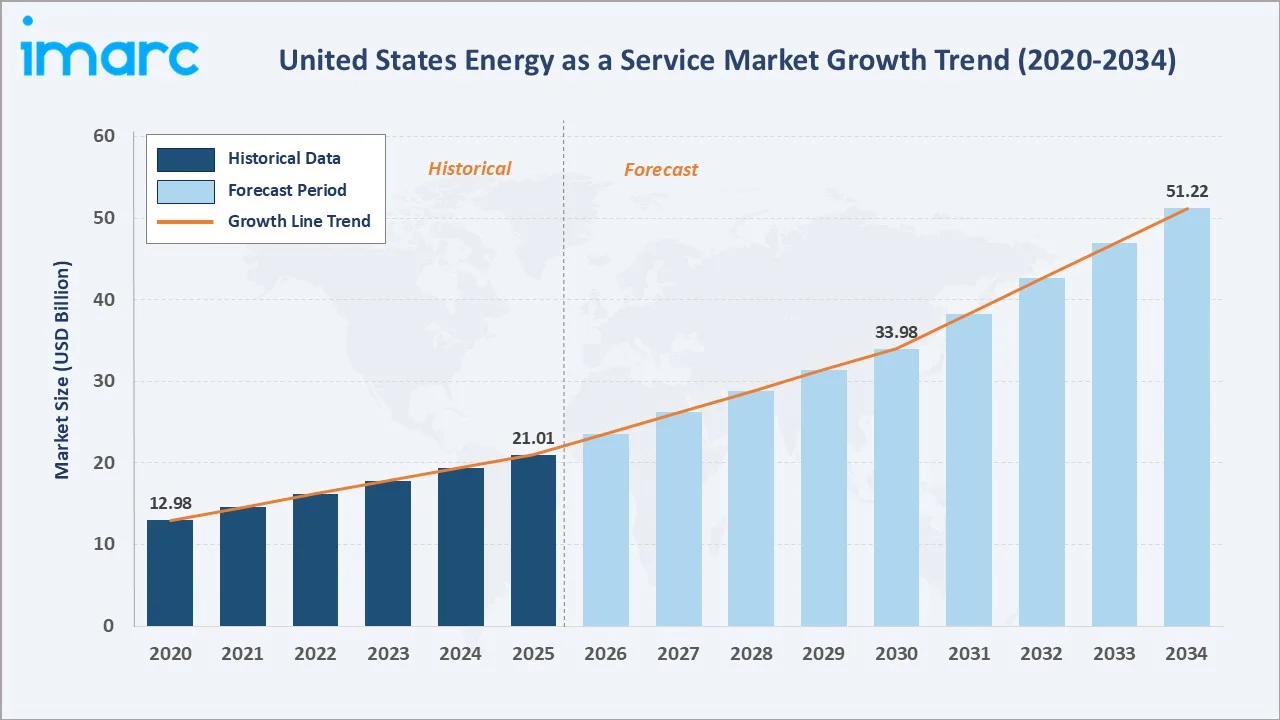

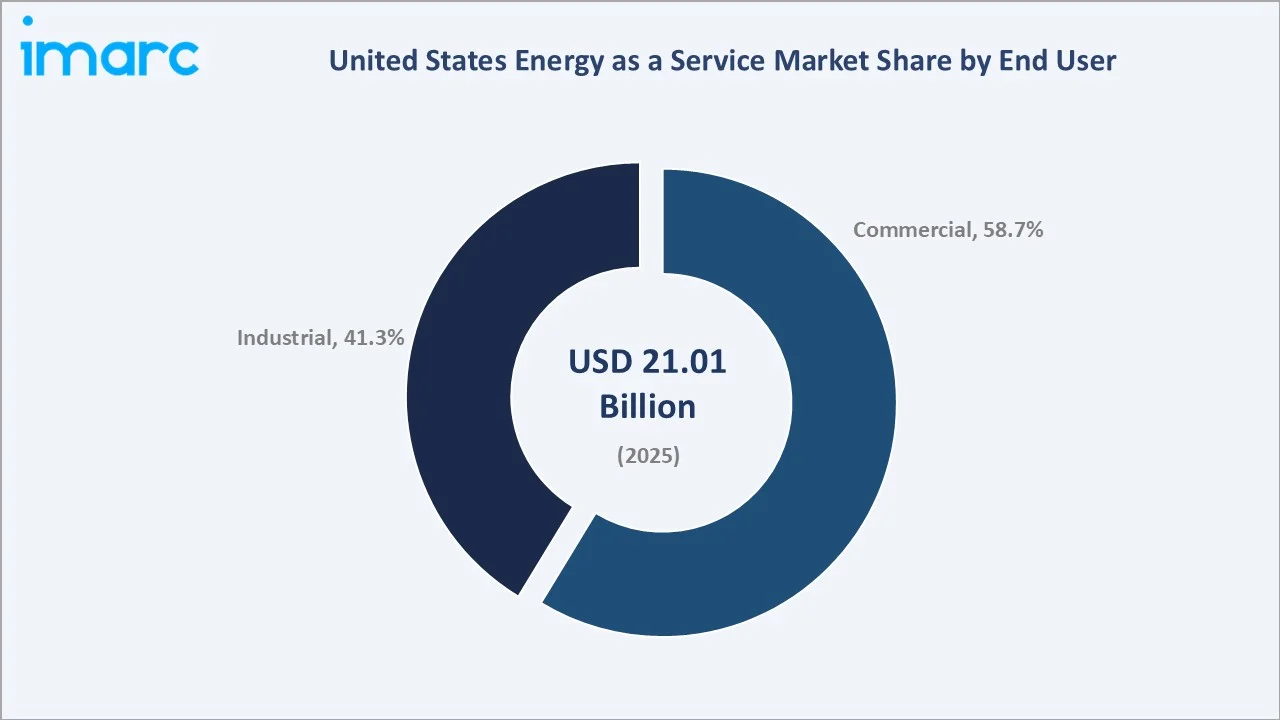

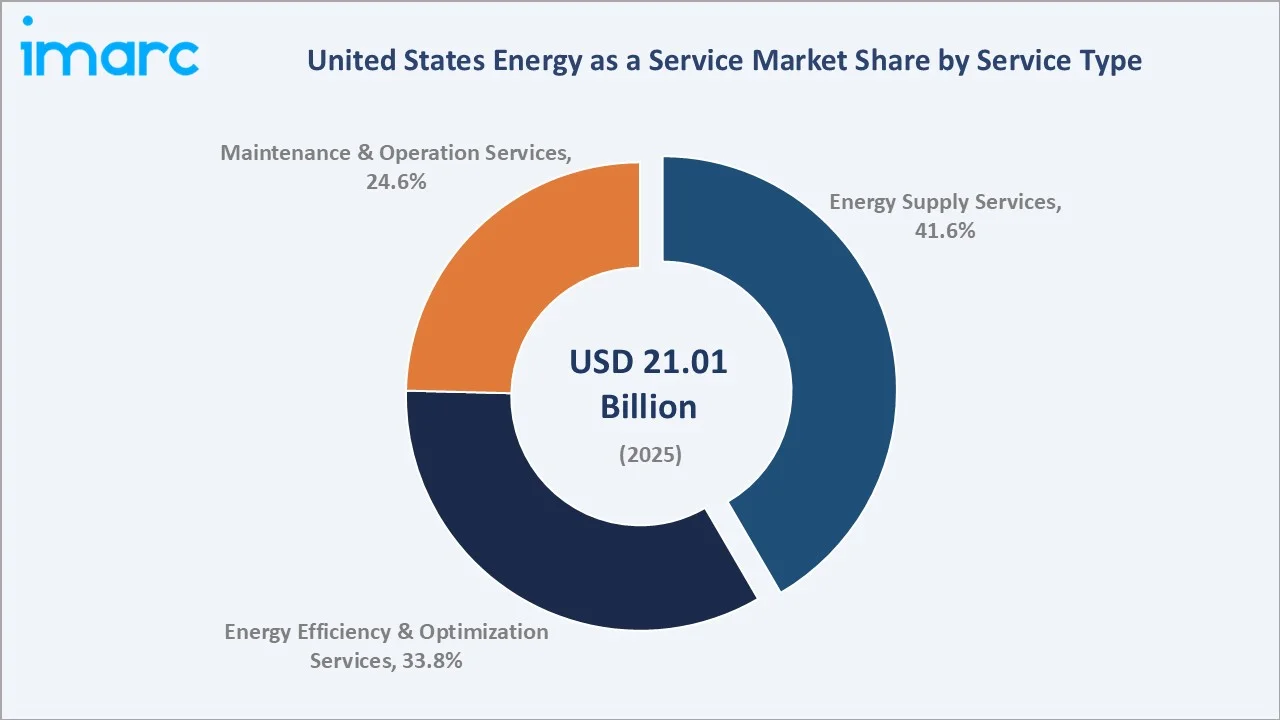

The United States energy as a service market reached USD 21.01 Billion in 2025 and is projected to reach USD 51.22 Billion by 2034, growing at a CAGR of 10.10% during 2026-2034. Accelerating corporate decarbonization commitments, rising energy cost volatility, and the rapid adoption of subscription-based energy management solutions across commercial and industrial end users are key growth drivers.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 21.01 Billion |

|

Forecast Market Size (2034) |

USD 51.22 Billion |

|

CAGR (2026-2034) |

10.10% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Segment (End User) |

Commercial – 58.7% share (2025) |

|

Largest Segment (Service Type) |

Energy Supply Services – 41.6% share (2025) |

|

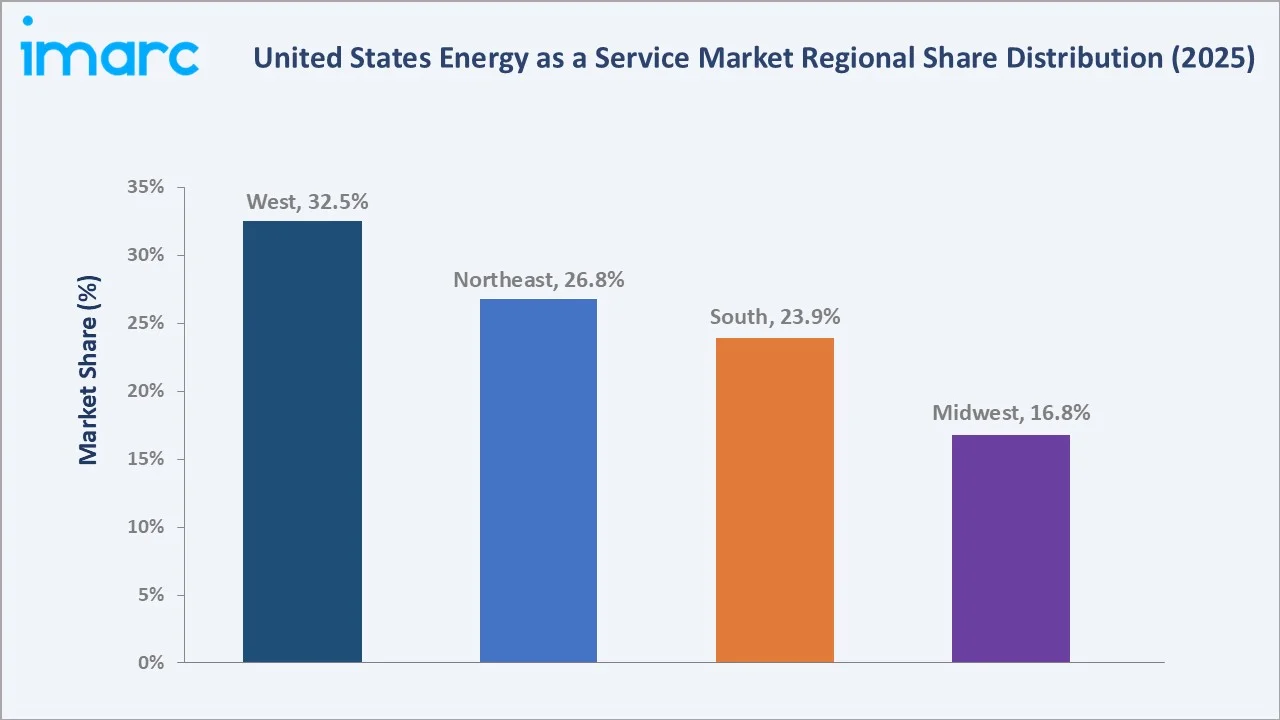

Largest Region |

West – 32.5% share (2025) |

The West region dominates, holding a 32.5% market share in 2025, while the commercial segment leads end user demand at 58.7%. Energy Supply Services remains the dominant service type with a 41.6% share. Energy as a Service (EaaS) enables commercial and industrial customers to consume energy infrastructure, including solar, storage, microgrids, and energy management systems, as a subscription or performance-based service, eliminating upfront capital expenditure and transferring operational complexity to specialized providers.

To get more information on this market, Request Sample

With applications spanning commercial real estate, healthcare, manufacturing, data centers, and government facilities, the market is expected to continue expanding, supported by AI-driven energy optimization platforms, expanding renewable distributed energy resources, and favorable federal and state policy incentives for clean energy adoption.

Executive Summary

The United States energy as a service market is on a sustained high-growth trajectory, underpinned by accelerating corporate net-zero commitments, the capital-free model that EaaS enables for energy infrastructure deployment, and the rapid scaling of AI-driven energy management platforms. The market reached USD 21.01 Billion in 2025 and is forecast to surpass USD 51.22 Billion by 2034, reflecting a robust CAGR of 10.10% over the forecast period.

The West region leads with a 32.5% revenue share in 2025, driven by California's aggressive clean energy mandates, high commercial real estate density, and a mature technology ecosystem enabling innovative EaaS business models. The Northeast follows at 26.8%, anchored by high energy costs, dense urban commercial building stock, and strong state-level renewable portfolio standards.

The commercial segment dominates end user demand at 58.7%, encompassing office buildings, retail centers, hospitals, educational institutions, and data centers seeking cost-effective, zero-capital energy solutions. Leading players, including Schneider Electric, Siemens, Johnson Controls, Honeywell International Inc., ENGIE, and Ameresco, continue to invest in AI-powered energy management platforms, integrated microgrid systems, and comprehensive performance contracting models.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (End User) |

Commercial – 58.7% share (2025) |

|

Largest Segment (Service Type) |

Energy Supply Services – 41.6% share (2025) |

|

Leading Region |

West – 32.5% revenue share (2025) |

|

Fastest Growing Region |

South (data center and industrial energy demand growth) |

|

Top Companies |

Schneider Electric, Siemens, Johnson Controls, Honeywell International Inc., ENGIE, and Ameresco |

|

Market Opportunity |

AI-driven energy optimization; industrial decarbonization contracts |

Key Analytical Observations Supporting the Above Data:

- The commercial segment accounts for 58.7% of the US EaaS market in 2025, driven by office buildings, hospitals, retail chains, and data centers adopting subscription-based energy solutions to eliminate capital expenditure and meet corporate sustainability commitments without burdening balance sheets.

- Energy supply services represent the largest service type at 41.6% in 2025, encompassing solar power purchase agreements (PPAs), on-site generation contracts, virtual power plants, and distributed energy resource management, all structured as subscription or performance-based service arrangements.

- The West region holds 32.5% of the US EaaS market in 2025, underpinned by California's leading renewable energy mandates, high commercial electricity prices creating strong economic incentive for EaaS adoption, and a dense technology company ecosystem deploying innovative energy management solutions.

United States Energy as a Service Market Overview

Energy as a Service (EaaS) is a business model that enables commercial and industrial customers to procure energy infrastructure, supply, and management capabilities as a subscription or outcome-based service, without owning or operating the underlying assets. EaaS contracts typically cover renewable energy generation (solar, wind, combined heat and power), energy storage systems, building energy management systems, demand response programs, and comprehensive maintenance and optimization services.

Macroeconomic and regulatory factors, including the Biden-era Inflation Reduction Act (IRA) tax credits for clean energy deployment, rising commercial electricity prices, and accelerating corporate net-zero pledges, are primary growth catalysts. EaaS eliminates the capital and operational barriers that have historically prevented building owners and manufacturers from deploying distributed energy resources, making it the fastest-growing clean energy procurement model in the United States commercial and industrial sectors.

Market Dynamics

To evaluate market opportunities, Request Sample

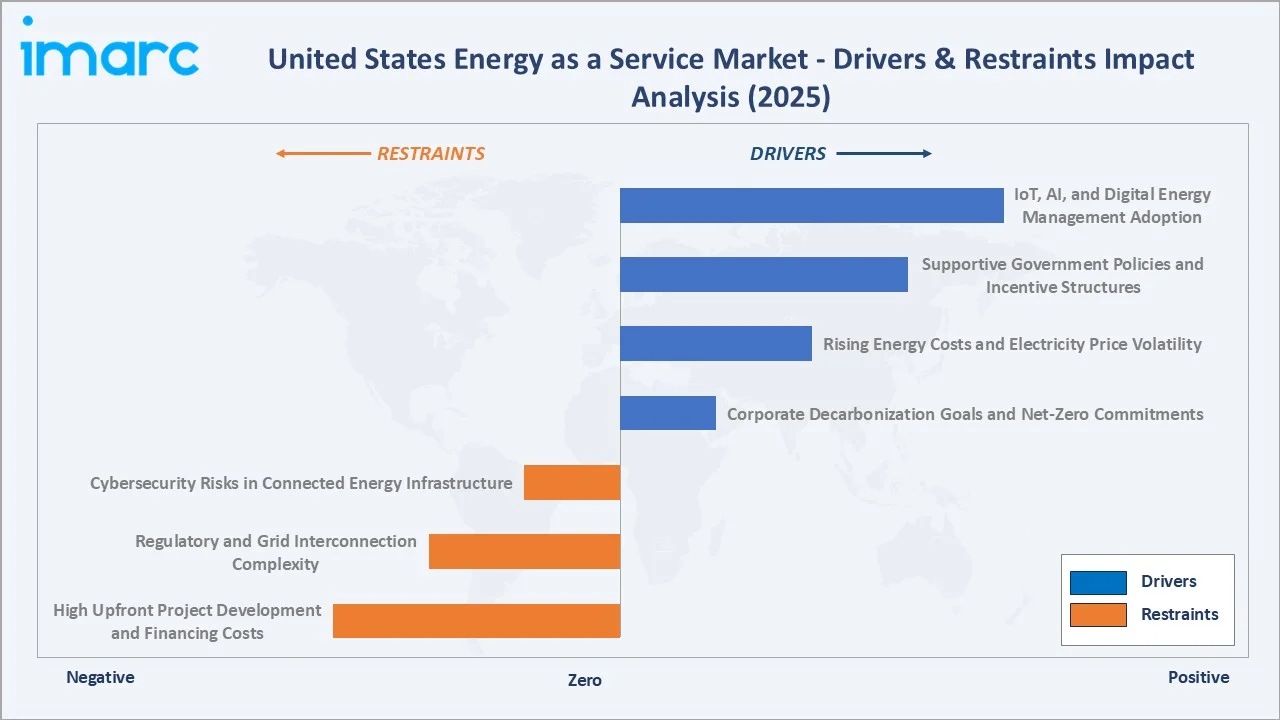

Market Drivers

- Corporate Decarbonization Goals and Net-Zero Commitments: Over 10,000 companies have now committed to the Science-Based Targets initiative (SBTi) emission reduction targets, creating structural demand for cost-effective, capital-free renewable energy solutions.

- Rising Energy Costs and Electricity Price Volatility: From 2019 to 2024, U.S. residential electricity prices increased by an average of 27%, with significant rises observed in California and Northeast states, according to a study by the Lawrence Berkeley National Laboratory.

- Supportive Government Policies and Incentive Structures: The Inflation Reduction Act extended and expanded Investment Tax Credits (ITCs) for solar, storage, and clean energy projects, significantly improving the economics of EaaS project financing.

- IoT, AI, and Digital Energy Management Adoption: In November 2025, Schneider Electric unveiled a unified, AI‑powered software platform designed to integrate energy, power, and building systems (and utilities planning and operations) to help customers modernize infrastructure and boost efficiency and grid resilience.

Market Restraints

- High Upfront Project Development and Financing Costs: Rising interest rates between 2022 and 2025 increased financing costs for EaaS providers, compressing project economics and slowing the pace of new contract deployments, particularly for smaller independent EaaS operators with limited capital access.

- Regulatory and Grid Interconnection Complexity: Navigating utility tariff structures, net metering policies, and demand response program rules across 50 state regulatory environments adds time and cost to EaaS contract development and deployment.

- Cybersecurity Risks in Connected Energy Infrastructure: The increasing digital connectivity of EaaS platforms, integrating IoT sensors, cloud energy management systems, and grid-interactive building controls, creates expanded attack surfaces for cybersecurity threats.

Market Opportunities

- Industrial Decarbonization and Heavy Industry EaaS Contracts: Industrial EaaS contracts, encompassing combined heat and power (CHP), on-site solar plus storage, and green hydrogen supply, are emerging as a high-value category capable of addressing the 41.3% industrial market share.

- Data Centre and Technology Campus Energy Solutions: In February 2025, VoltaGrid and Vantage Data Centers announced plans to deploy over 1 GW of microgrid capacity for data center campuses in constrained markets, illustrating the scale of EaaS opportunity in the technology infrastructure sector.

- AI-Powered Virtual Power Plant and Demand Response Platforms: In March 2025, Itron and Schneider Electric expanded their partnership to integrate Grid Edge Intelligence with digital grid solutions and Microsoft’s AI/data platform, enhancing real‑time visibility and control of utility distribution grids to address complexity and support reliability.

Market Challenges

- Long Contract Lifecycle and Customer Commitment Barriers: Customer uncertainty about technology evolution, organizational changes, and regulatory shifts over multi-decade contract terms creates decision-making friction that slows EaaS adoption, particularly among risk-averse commercial real estate owners and mid-market industrial operators.

- Workforce and Technical Talent Shortages: The rapid growth of EaaS is creating significant demand for specialized talent across energy engineering, digital platform development, and project finance, skill sets that are in short supply across the US clean energy sector.

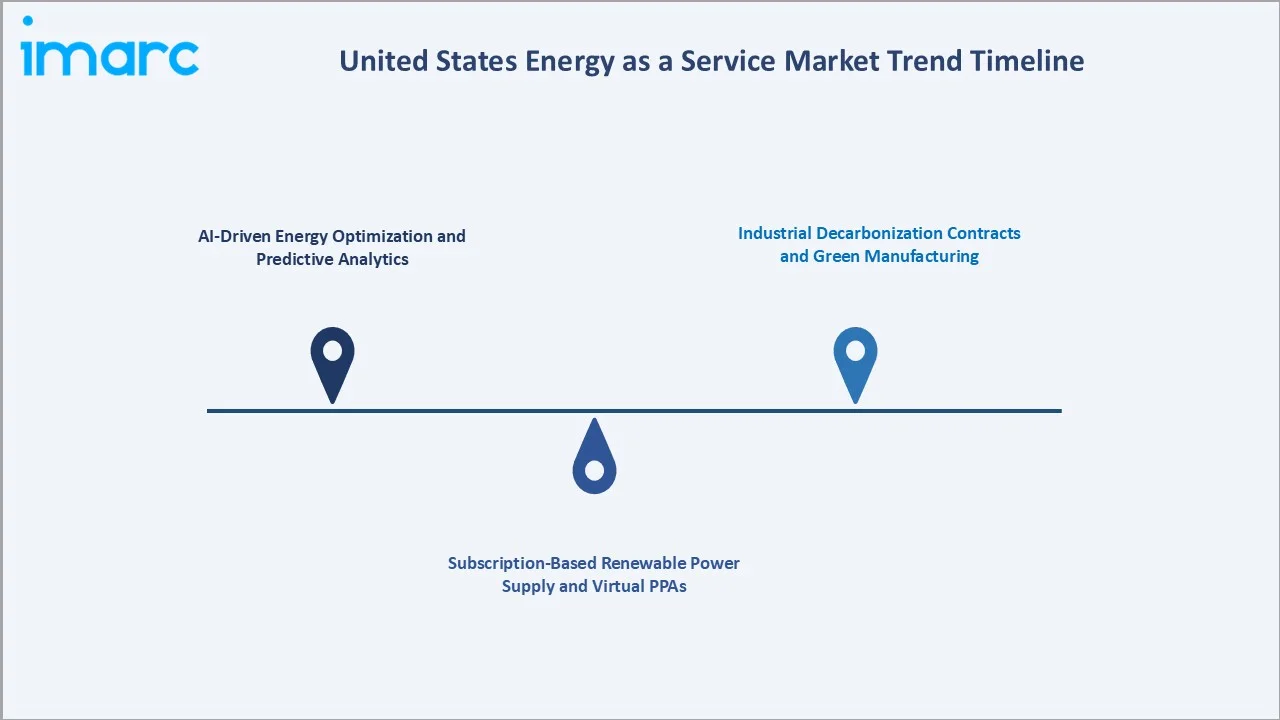

Emerging Market Trends

1. AI-Driven Energy Optimization and Predictive Analytics

In January 2026, Schneider Electric launched an advanced EaaS platform integrating AI-driven predictive analytics for real-time energy optimization in commercial buildings, delivering energy consumption reductions of up to 25% without upfront costs via a subscription model. In March 2025, Itron and Schneider Electric joined forces with Microsoft to embed distributed intelligence into grid-edge devices, upgrading utility visibility and control.

2. Subscription-Based Renewable Power Supply and Virtual PPAs

The power purchase agreement (PPA) model is evolving into a fully subscription-based, managed renewable energy supply service that bundles generation, storage, monitoring, and performance guarantees into a single monthly fee. Virtual PPAs, which allow commercial and industrial customers to claim renewable energy certificates without requiring on-site generation, are growing rapidly as an EaaS product across the Northeast and South regions.

3. Industrial Decarbonization Contracts and Green Manufacturing

Large industrial operators, including automotive manufacturers, semiconductor fabs, chemical plants, and food processors, are increasingly procuring comprehensive EaaS contracts that bundle on-site solar, CHP, storage, green hydrogen, and energy efficiency optimization into single long-term performance agreements.

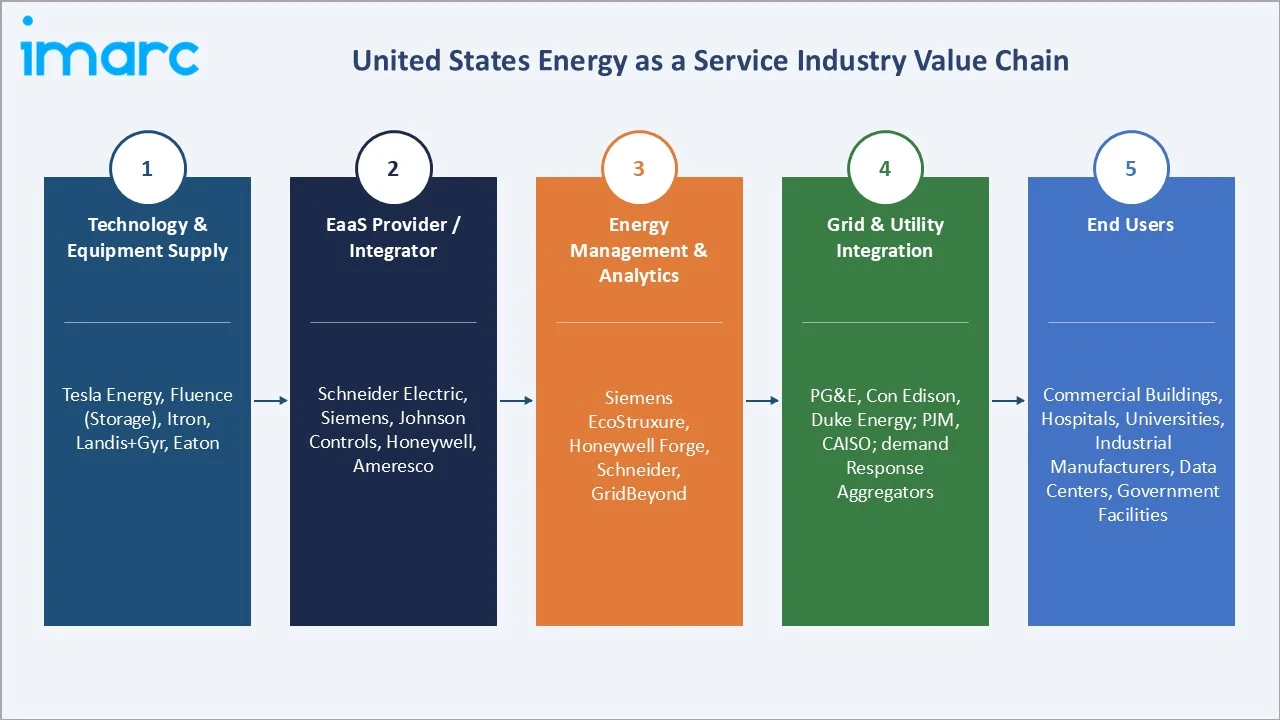

Industry Value Chain Analysis

The United States EaaS value chain spans technology and infrastructure providers through end-user energy consumption, with EaaS providers occupying the central value-creating node by integrating upstream technology components with downstream customer energy management outcomes.

|

Stage |

Key Players / Examples |

|

Technology & Equipment Supply |

Tesla Energy, Fluence (storage); Itron (metering), Landis+Gyr, Eaton Corporation |

|

EaaS Provider / System Integrator |

Schneider Electric, Siemens, Johnson Controls, Honeywell International Inc., Ameresco |

|

Energy Management & Analytics |

Siemens, Schneider Electric EcoStruxure, Honeywell Forge, GridBeyond |

|

Grid & Utility Integration |

PG&E, Con Edison, Duke Energy (utilities); PJM, CAISO (grid operators); demand response aggregators |

|

End Users |

Commercial buildings, hospitals, universities, retail chains, industrial manufacturers, data centers, government facilities |

Technology Landscape in the United States Energy as a Service Industry

AI and Machine Learning Energy Management Platforms

Machine learning algorithms continuously optimize the dispatch of on-site solar, storage, and flexible loads to minimize customer energy costs while maximizing grid services revenue. In March 2025, Hitachi Energy commenced a multi-year collaboration with Amazon Web Services to release cloud-native energy management AI that enhances grid visibility and control at the distribution level, demonstrating the enterprise-scale cloud infrastructure underpinning next-generation EaaS platforms.

Advanced Energy Storage and Microgrid Control Systems

Battery energy storage systems (BESS) are the critical enabling technology for EaaS microgrids, providing the dispatchable capacity that allows on-site renewable generation to be converted from intermittent supply into reliable power delivery. Zinc-based, lithium iron phosphate (LFP), and flow battery technologies are being deployed in EaaS microgrid configurations, with each offering distinct performance characteristics suited to different commercial and industrial applications.

IoT-Enabled Building Energy Management and Demand Response

In March 2025, Carrier Global Corporation and Google Cloud unveiled a strategic alliance to deliver AI-enabled home and commercial energy ecosystems, integrating battery-equipped HVAC equipment with cloud analytics, illustrating the convergence of building technology, clean energy, and cloud-native EaaS platforms.

Digital Twin and Performance Verification Technology

Digital twin technology, creating virtual replicas of energy systems that simulate real-time performance, predict maintenance needs, and verify energy savings, is becoming a standard tool for EaaS providers managing large portfolios of contracted energy assets. Performance verification is critical in EaaS contracts where customer payments are linked to verified energy delivery or savings, making measurement and verification (M&V) technology a commercial differentiator.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| End User | Commercial | 58.7% | 2025 |

| Service Type | Energy Supply Services | 41.6% | 2025 |

| Region | West | 32.5% | 2025 |

By End User

The commercial segment accounts for the largest share, representing 58.7% of the United States energy as a service market in 2025. Commercial end users, including office buildings, hospitals, universities, retail chains, hotels, and data centers, are the primary adopters of EaaS because the model directly addresses their structural inability to deploy energy infrastructure capital while simultaneously meeting corporate sustainability mandates and energy cost reduction targets.

To access detailed market analysis, Request Sample

The industrial segment holds a 41.3% share and represents the fastest-growing end user category, driven by manufacturers, chemical plants, food processors, and logistics operators seeking to decarbonize production facilities without diverting capital from core manufacturing investments.

By Service Type

Energy supply services represent the largest service type at 41.6% of the United States energy as a service market in 2025. This segment encompasses solar PPAs, wind energy supply contracts, virtual PPAs, on-site combined heat and power arrangements, and distributed energy resource supply agreements, all structured as outcome-based service contracts where the EaaS provider bears the capital investment and operational risk.

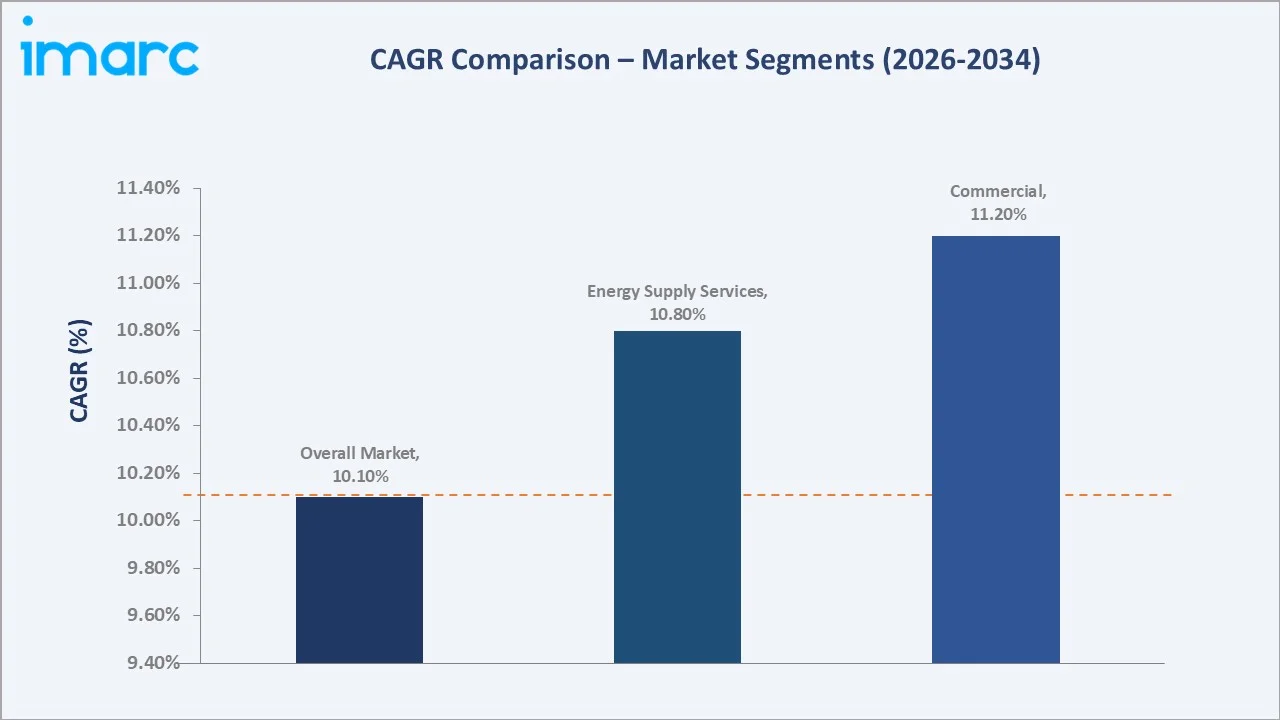

Energy efficiency and optimization services hold a 33.8% share, encompassing building energy management, AI-driven optimization, demand response participation, and guaranteed energy savings contracts. This segment is advancing at 10.8% CAGR, driven by the integration of AI analytics and IoT sensor networks that enable EaaS providers to deliver increasingly precise, measurable, and financially accountable energy savings outcomes.

Regional Market Insights

The West region's market leadership reflects California's position as the nation's most advanced clean energy market, with a combination of aggressive renewable portfolio standards, high commercial electricity prices providing strong EaaS economic incentives, and a dense technology company ecosystem deploying innovative EaaS solutions.

|

Region |

Share (2025) |

Key Growth Drivers |

|

West |

32.5% |

California clean energy mandates, high electricity prices, and tech sector ESG demand |

|

Northeast |

26.8% |

High energy costs; dense commercial stock; strong state RPSs; corporate sustainability |

|

South |

23.9% |

Data center energy demand, industrial growth, and improving renewable economics |

|

Midwest |

16.8% |

Industrial decarbonization, manufacturing energy contracts, and growing renewable capacity |

The Northeast accounts for 26.8% of the US EaaS market, anchored by some of the nation's highest commercial electricity prices and the most aggressive state-level clean energy legislation. New York's Climate Leadership and Community Protection Act mandates 70% renewable electricity by 2030, creating structural EaaS demand across the state's large commercial and industrial building stock.

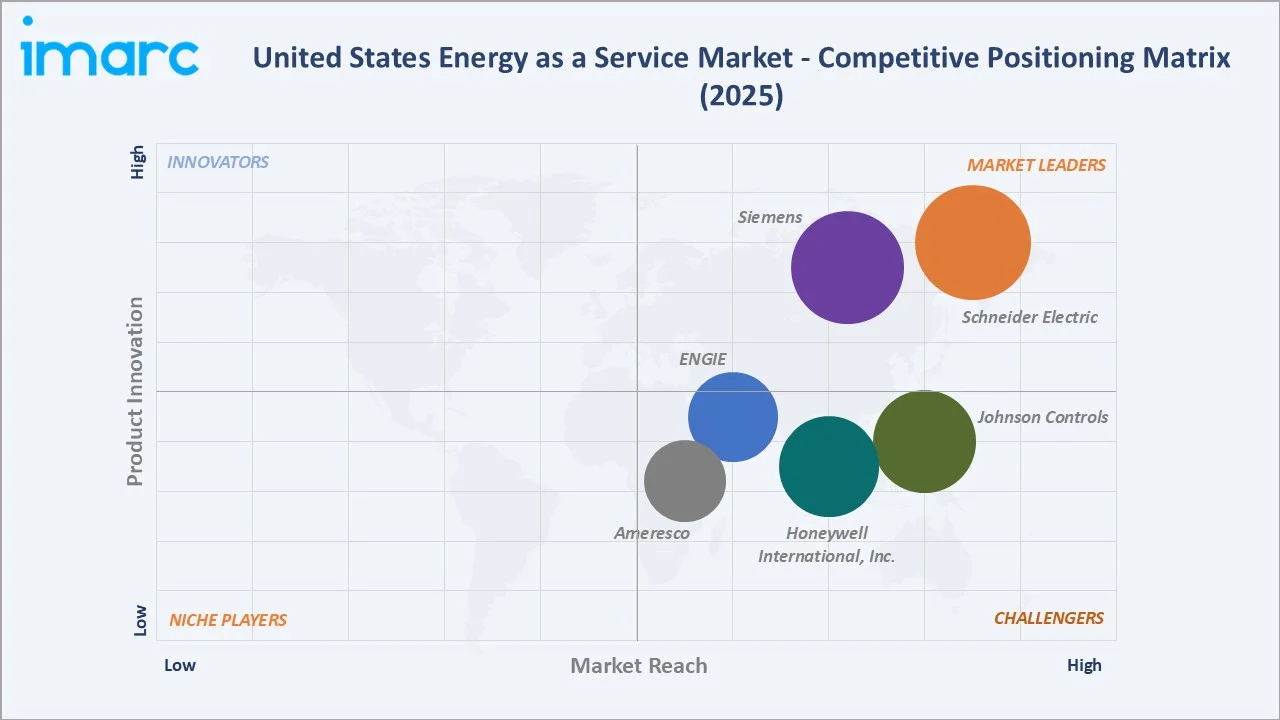

Competitive Landscape

The United States energy as a service market exhibits a moderately concentrated structure at the large-contract level, with global energy technology leaders, Schneider Electric, Siemens, Johnson Controls, Honeywell International Inc., ENGIE, and Ameresco, collectively serving a substantial share of large commercial and industrial EaaS contracts.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

Schneider Electric |

EcoStruxure, AlphaStruxure, GreenStruxure |

Market Leader |

AI-driven EaaS platforms; global scale |

|

Siemens |

Building X, Electrification X |

Market Leader |

Integrated building and grid solutions |

|

Johnson Controls |

OpenBlue |

Strong Challenger |

Building technology and energy management |

|

Honeywell International Inc. |

Honeywell Forge Sustainability+, Honeywell Forge Performance+ for Utilities |

Strong Challenger |

Industrial and commercial EaaS; IoT |

|

ENGIE |

ENGIE Resources |

Challenger |

Renewable EaaS; commercial PPAs |

|

Ameresco |

Ameresco ESPC, Ameresco Energy Assets, Ameresco Federal Solutions |

Challenger |

Government and healthcare EaaS |

A diverse ecosystem of regional EaaS specialists, independent power producers, and digital energy management startups accounts for the growing mid-market and small commercial segment.

Key Company Profiles

Schneider Electric

Schneider Electric, headquartered in France, with major US operations across multiple states, is the global leader in energy management and automation. Through its EcoStruxure platform, Schneider delivers comprehensive EaaS solutions for commercial and industrial customers across the United States.

- Services Offered: EcoStruxure-powered EaaS platform; AI predictive energy optimization; commercial building performance contracts; industrial energy management.

- Recent Developments: In November 2025, Schneider Electric introduced a unified, AI‑powered software platform, EcoStruxure Foresight Operation, that integrates energy, power, and building systems to boost efficiency, reduce engineering workloads, and enhance operational insights.

- Strategic Focus: AI and digital platform leadership in EaaS; commercial building energy optimization; industrial decarbonization performance contracts.

Siemens

Siemens, headquartered in Munich, Germany, operates one of the largest commercial and industrial energy management businesses in the United States through its Smart Infrastructure division. Siemens' EaaS offerings integrate building automation, microgrid control, digital twin technology, and renewable energy supply under long-term performance-based service agreements.

- Services Offered: Smart Infrastructure EaaS; modular microgrid systems; building energy management; digital twin-enabled performance contracts.

- Recent Developments: Siemens and Macquarie launched a joint venture, Calibrant Energy, in the U.S. to provide Energy-as-a-Service (EaaS) solutions, offering distributed energy systems like solar and batteries without upfront costs.

- Strategic Focus: Industrial microgrid EaaS; digital twin technology; grid resilience solutions; US commercial and industrial market leadership.

Johnson Controls

Johnson Controls, headquartered in Cork, Ireland, with US operations centered in Milwaukee, Wisconsin, is a leading provider of smart buildings, HVAC systems, and integrated energy solutions. Its OpenBlue EaaS platform enables commercial building operators to procure comprehensive energy management as a unified subscription service.

- Services Offered: OpenBlue EaaS platform; HVAC-integrated energy services; commercial building performance contracts; renewable energy supply.

- Recent Developments: Johnson Controls beat Q4 FY2025 revenue expectations, reporting approximately USD 6.4 billion in sales, slightly above analyst estimates with ~3% year‑on‑year growth.

- Strategic Focus: Commercial building EaaS integration; HVAC and energy management convergence; corporate real estate sustainability solutions.

Market Concentration Analysis

The United States energy as a service market exhibits moderate concentration at the large-contract level, with global technology and energy companies holding significant positions in the enterprise and government segments. However, the mid-market and distributed EaaS segment is highly fragmented, with hundreds of regional EaaS developers, solar developers, and digital energy platforms competing for small-to-mid commercial contracts.

Consolidation activity is accelerating, driven by the scale advantages required to finance large EaaS portfolios, manage diverse energy asset types, and deliver comprehensive digital platform capabilities. Strategic acquisitions of clean energy developers, building technology firms, and AI energy management startups are reshaping the competitive landscape.

Investment & Growth Opportunities

Fastest Growing Segments

Energy Efficiency and Optimization Services (advancing at 10.8% CAGR), AI-driven virtual power plant platforms (estimated 15%+ CAGR), and industrial decarbonization performance contracts represent the three highest-growth investment vectors through 2034. Together, these niches address a total addressable market exceeding USD 15 Billion by 2030, underpinned by structural commercial and industrial shifts toward outcome-based clean energy procurement.

Emerging Market Expansion

The South and Midwest regions represent the most significant incremental EaaS growth opportunities through 2034. The South's data center energy demand explosion, driven by AI computing infrastructure build-out, and the Midwest's industrial decarbonization imperative are creating substantial new EaaS contract pipelines that are underserved by existing provider capacity. Federal clean energy incentives from the Inflation Reduction Act are particularly effective in these regions, where corporate electricity prices and renewable resource availability are both favorable for EaaS project economics.

Venture and Institutional Investment Trends

- Key investment themes include AI-native energy management SaaS platforms, industrial EaaS developers targeting manufacturing decarbonization, demand response aggregation platforms, and data centre EaaS specialists serving the hyperscale computing sector.

- Infrastructure funds and institutional investors are increasingly targeting long-duration EaaS contracted revenue streams as an attractive inflation-protected yield asset class, driving capital into EaaS platform companies with diversified commercial and industrial contract portfolios.

Future Market Outlook (2026-2034)

The United States energy as a service market is positioned for sustained, double-digit growth through 2034. From a base of USD 21.01 Billion in 2025, the market is projected to reach USD 51.22 Billion by 2034, representing total incremental value creation of USD 30.21 Billion over the forecast decade at a CAGR of 10.10%.

Policy evolution will continue to expand the economic case for EaaS adoption across all end-user segments. EaaS providers that achieve full-stack capabilities encompassing AI optimization, renewable supply, storage management, demand response, and performance verification are positioned to capture the highest-value long-term contracts in the commercial and industrial segments.

Long-term, the market's trajectory is tied to three structural macro-themes: the corporate decarbonization imperative, the energy cost volatility crisis (creating durable commercial demand for long-term price stability through EaaS performance contracts), and the digital energy transformation. The United States EaaS market sits at the intersection of all three, ensuring above-GDP growth and sustained market expansion through 2034.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and surveys with over 110 industry participants in 2025–2026, including EaaS provider executives, commercial and industrial energy procurement managers, utility regulatory experts, building technology integrators, and investment professionals active in the US clean energy market.

Secondary Research

Secondary research encompassed a systematic review of company investor presentations, regulatory filings with state PUCs, US Department of Energy EaaS market databases, Lawrence Berkeley National Laboratory distributed energy research, EIA commercial energy consumption surveys, trade publications, and publicly available financial data across over 220 secondary sources.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting approaches, incorporating commercial and industrial EaaS contract value data, IRA incentive impact modelling, electricity price scenario analysis, and corporate sustainability commitment tracking. A base-case CAGR of 10.10% reflects consensus analyst estimates validated against reported EaaS provider revenue growth rates for 2022–2025.

United States Energy as a Service Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Service Types Covered | Energy Supply Services, Maintenance and Operation Services, Energy Efficiency and Optimization Services |

| End Users Covered | Commercial, Industrial |

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered | Schneider Electric, Siemens, Johnson Controls, Honeywell International Inc., ENGIE, Ameresco, etc. |

| Customization Scope | 10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the United States energy as a service market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the United States energy as a service market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the United States energy as a service industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the United States Energy as a Service Market Report

The United States energy as a service market reached USD 21.01 Billion in 2025. It is projected to reach USD 51.22 Billion by 2034.

The United States energy as a service market is expected to grow at a CAGR of 10.10% during the forecast period from 2026-2034, driven by corporate decarbonization commitments, rising energy costs, supportive government policy, and AI-driven energy optimization adoption.

The West region leads the market with a 32.5% revenue share in 2025, driven by California's stringent clean energy mandates, high commercial electricity prices, and a mature technology ecosystem enabling innovative subscription-based energy service delivery models.

The commercial segment dominates with a 58.7% share in 2025. Its dominance is driven by office buildings, hospitals, data centers, and retail chains adopting subscription-based energy solutions to meet sustainability mandates without capital expenditure.

Energy supply services hold the largest service type share at 41.6% in 2025, encompassing solar PPAs, on-site generation contracts, virtual power plant arrangements, and distributed energy resource supply agreements structured as performance-based service contracts.

Key players include Schneider Electric, Siemens, Johnson Controls, Honeywell International Inc., ENGIE, and Ameresco, among other regional and technology-specialist EaaS providers.

AI and machine learning are enabling EaaS providers to deliver verifiable energy savings of up to 25% for commercial buildings through predictive analytics, real-time optimization of distributed energy assets, and automated demand response participation, transforming EaaS from static supply contracts into dynamic, continuously improving energy management services.

Key challenges include high upfront EaaS project development and financing costs, regulatory complexity across 50 state utility markets, cybersecurity risks in connected energy infrastructure, long contract commitment barriers for customers, and workforce shortages in energy engineering and digital platform talent.

High-growth investment opportunities include AI-native energy management SaaS platforms, industrial decarbonization EaaS developers, data center energy supply specialists, virtual power plant aggregators, and demand response platforms.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)