U.S. Eyewear Market Size, Share, Trends and Forecast by Product, Gender, Distribution Channel, and Region, 2026-2034

U.S. Eyewear Market Size, Share, Trends & Forecast (2026-2034)

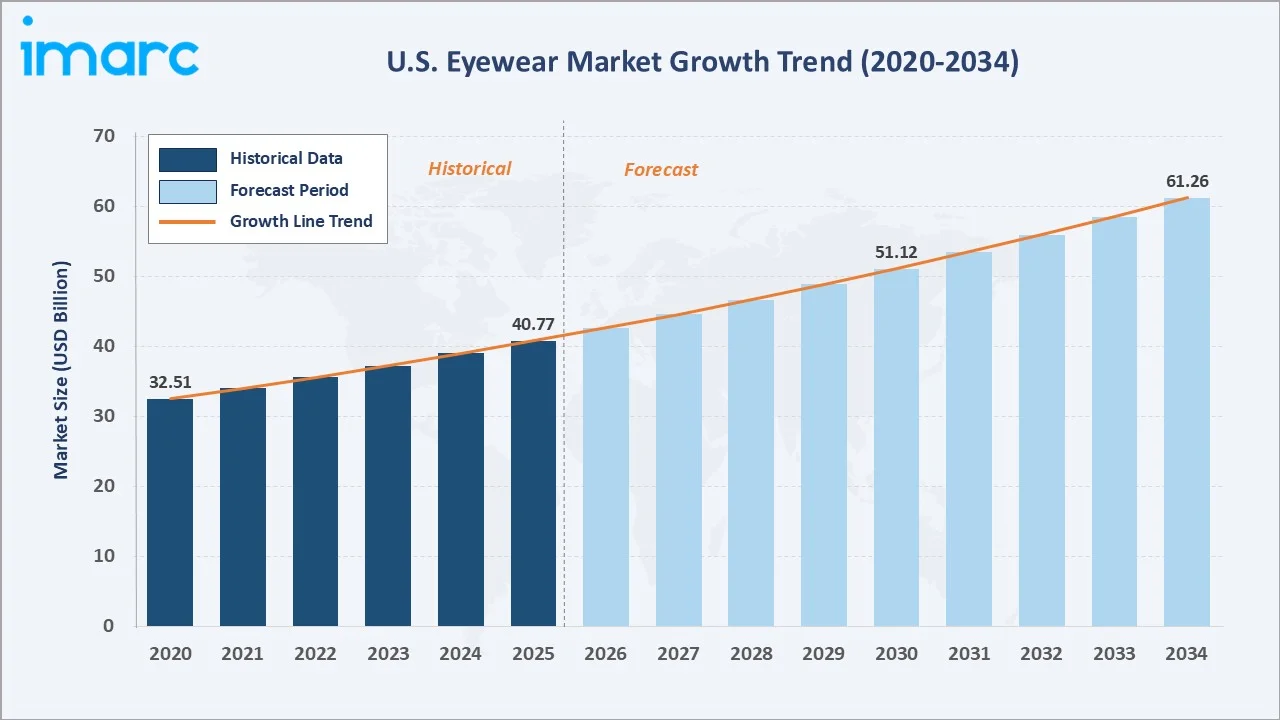

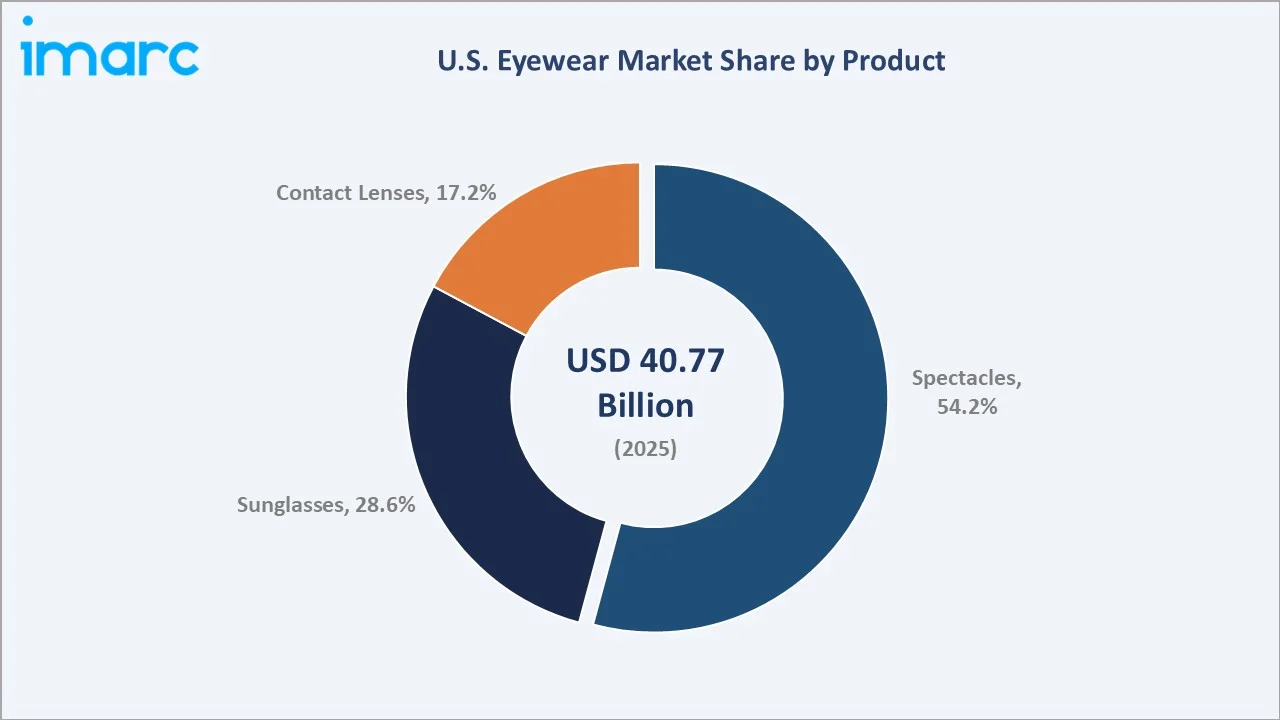

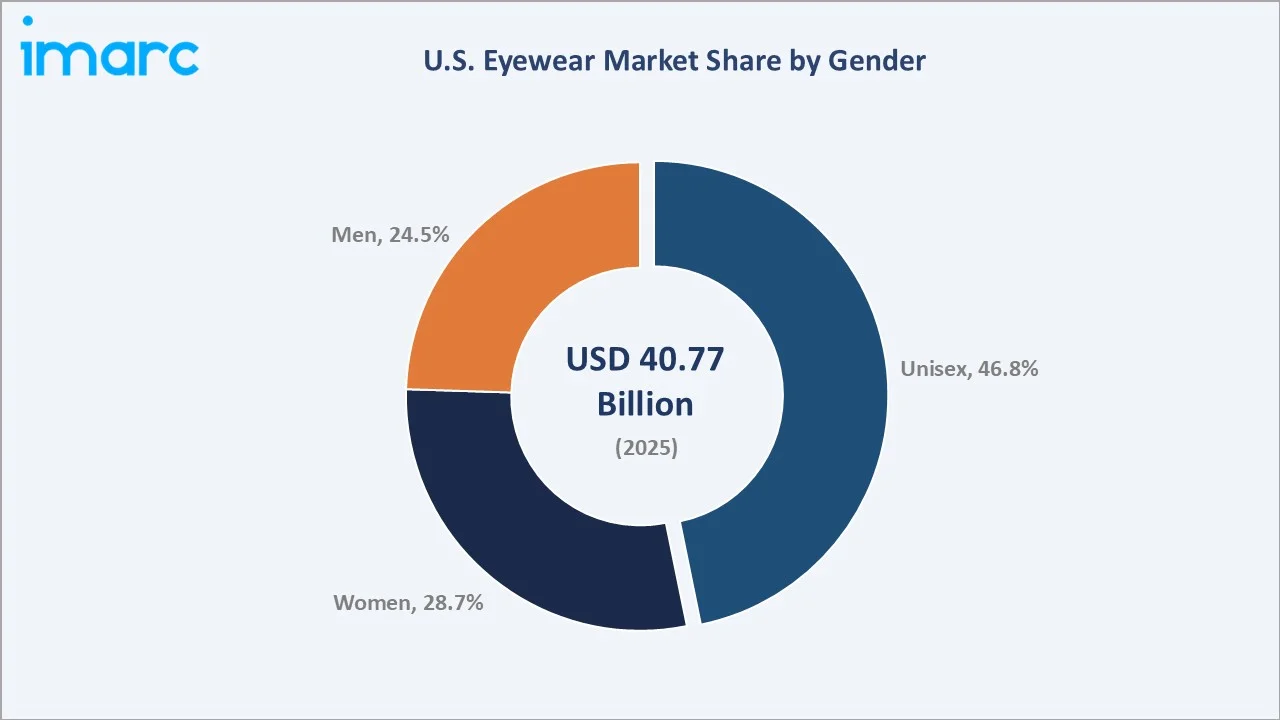

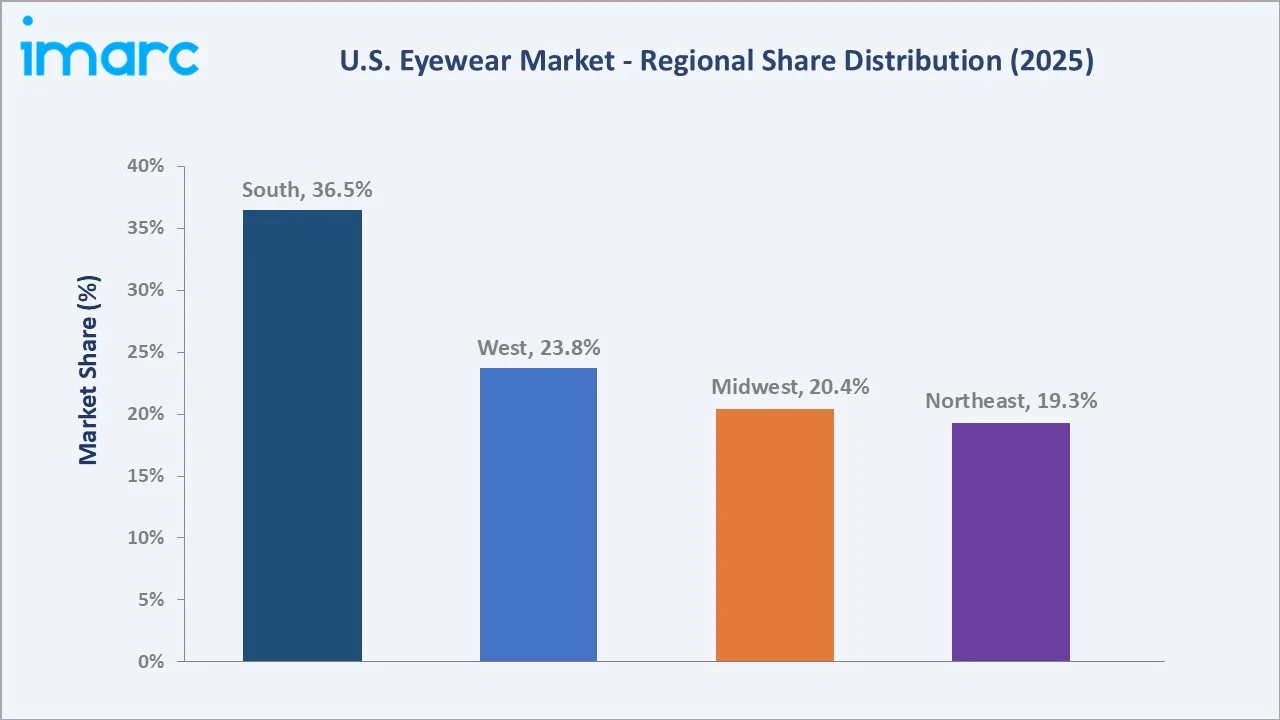

The U.S. eyewear market reached USD 40.77 Billion in 2025 and is projected to reach USD 61.26 Billion by 2034, growing at a CAGR of 4.63% during 2026-2034. The market is driven by rising vision disorders, increasing screen time, and growing demand for fashion-forward and premium eyewear products. According to the 2024 National Health Interview Survey, about 49.5 million U.S. adults aged 18+ reported some level of vision difficulty. Spectacles lead at 54.2% product share. Unisex eyewear dominates gender at 46.8%. The South commands 36.5% of market revenues.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 40.77 Billion |

|

Forecast Market Size (2034) |

USD 61.26 Billion |

|

CAGR (2026-2034) |

4.63% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Product |

Spectacles (54.2%, 2025) |

|

Dominant Gender |

Unisex (46.8%, 2025) |

|

Leading Region |

South (36.5%, 2025) |

The market expanded from USD 32.51 Billion in 2020 to USD 40.77 Billion in 2025, anchored at USD 51.12 Billion in 2030, and forecast to reach USD 61.26 Billion by 2034. The COVID-19 remote work acceleration permanently elevated corrective eyewear demand and created a new premium lens category that sustained market growth well above historical trend rates.

To get more information on this market, Request Sample

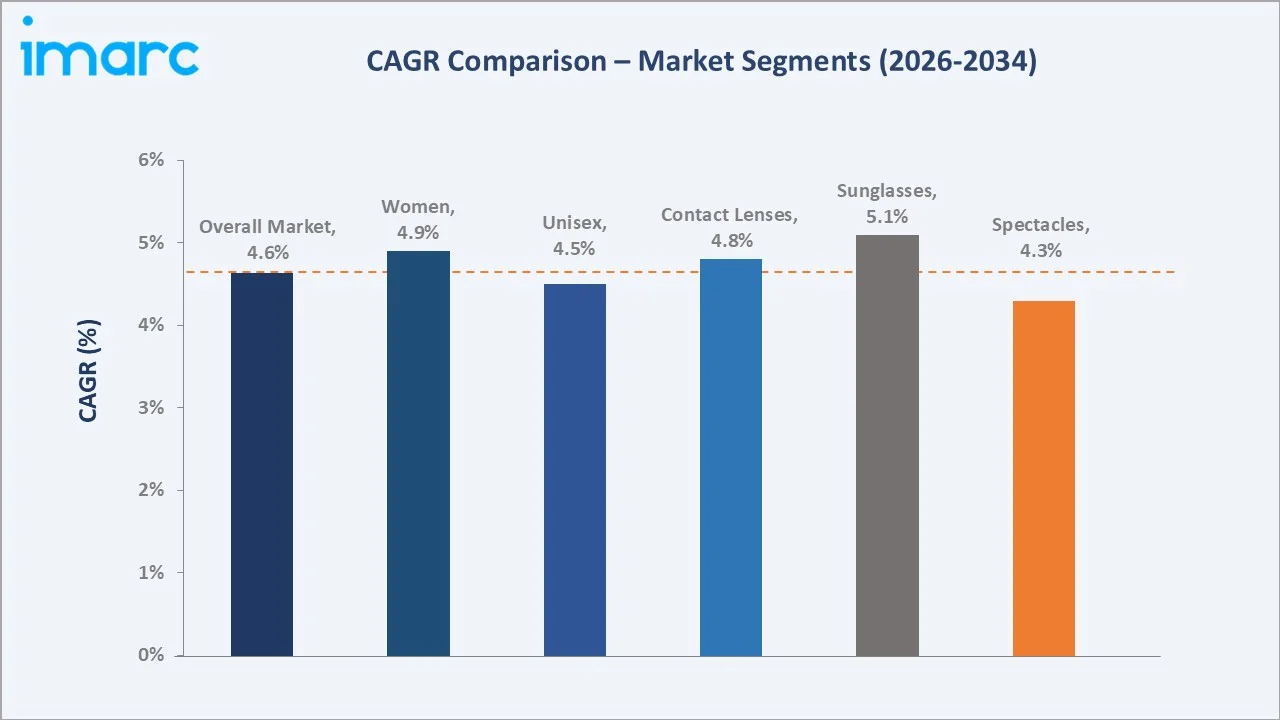

Sunglasses grow fastest at ~5.1% CAGR (2026-2034), driven by fashion-driven UV-protective eyewear premiumization, outdoor lifestyle trends (cycling, skiing, water sports), and luxury brand sunglass demand from Gen-Z and Millennial consumers. Women's segment grows at ~4.9% CAGR, the fastest gender segment, as female consumers demonstrate the highest premium frame trade-up rates and fastest online eyewear purchasing adoption.

Executive Summary

The U.S. eyewear market reached USD 40.77 Billion in 2025, one of the largest national eyewear markets, driven by Americans requiring vision correction, the world's most comprehensive commercial vision insurance system, and a fashion-accessory premiumization trend that has elevated average eyewear frame prices. The market is projected to reach USD 61.26 Billion by 2034 at 4.63% CAGR.

Spectacles command 54.2% market share (2025), anchored by prescription frames serving the US adults with refractive errors and the growing digital fatigue premium lens market. Sunglasses at 28.6% benefit from fashion brand premiumization and UV protection health awareness. Contact lenses at 17.2% are led by the US daily disposable market share and water gradient technology premium positioning. Unisex eyewear at 46.8% reflects the fashion-neutral universal frame design trend. The South at 36.5% leads regionally through Texas and Florida's combined population.

Key Market Insights

|

Insight |

Data |

|

Largest Product |

Spectacles - 54.2% share (2025) |

|

Dominant Gender |

Unisex - 46.8% share (2025) |

|

Leading Region |

South - 36.5% market share (2025) |

Key Analytical Observations Supporting the Above Data:

- Spectacles at 54.2% anchored by prescription eyewear's non-discretionary demand and premium lens upsell: 3 out of 4 American adults (75%) need some form of vision correction, which requires corrective spectacles, driving the segment growth.

- Unisex at 46.8% reflecting fashion industry gender-neutral design movement: The fashion industry's gender-fluid design trend has made unisex frame styling the dominant US eyewear format.

- South at 36.5% driven by the largest US consumer population base: The South's 36.5% market share reflects the region's population, the largest US regional population. Texas and Florida each individually rank among the top 5 US state eyewear markets.

U.S. Eyewear Market Overview

The U.S. eyewear market encompasses all corrective and non-corrective optical products, including prescription spectacles (single vision, bifocal, progressive lenses), fashion and performance sunglasses, soft and rigid contact lenses, and emerging smart eyewear. The market serves Americans across all age demographics, from children's first glasses prescriptions through elderly presbyopia management, with vision correction representing a non-discretionary healthcare need for US adults.

The ecosystem integrates frame and lens manufacturers, contact lens manufacturers, eye care professionals, vision insurance networks, optical retail chains, online platforms, and employer-sponsored optical benefit programs covering all Americans. Macroeconomic factors include rising disposable incomes, healthcare spending, and insurance coverage for vision care, which improve access to corrective and premium eyewear.

Market Dynamics

To evaluate market opportunities, Request Sample

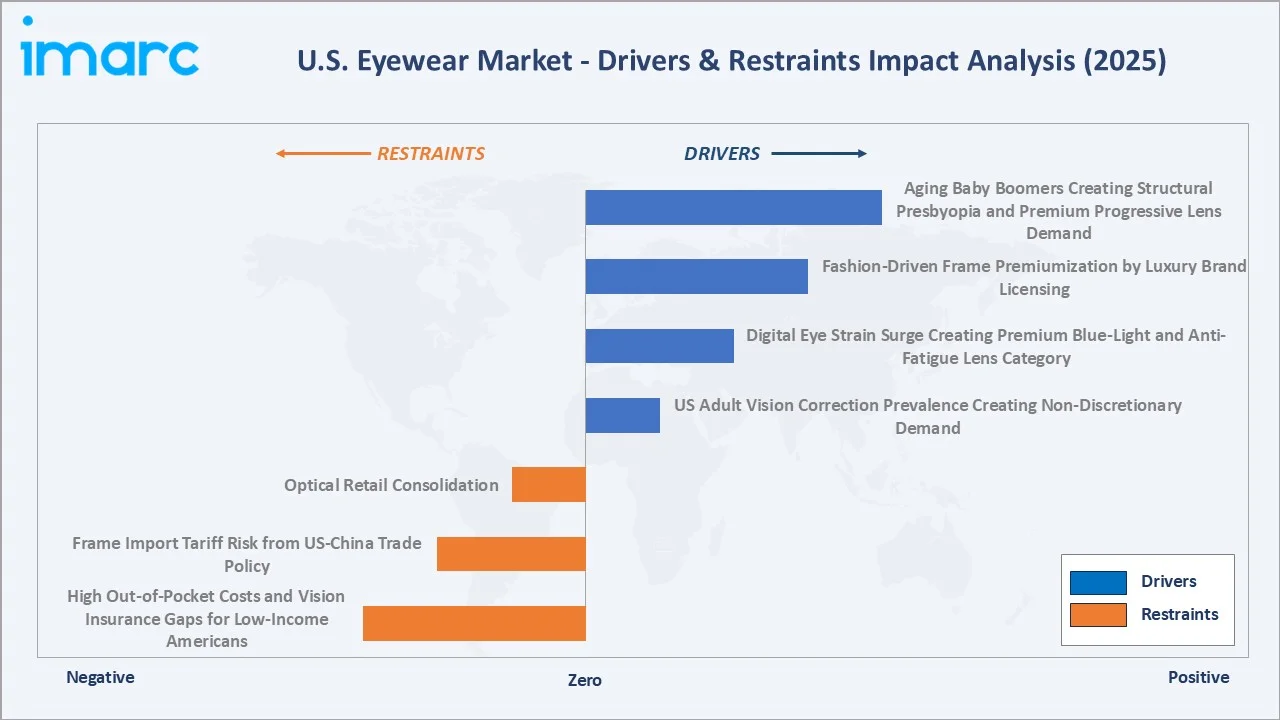

Market Drivers

- US Adult Vision Correction Prevalence Creating Non-Discretionary Demand: 75% of American adults need vision correction, requiring vision correction through prescription spectacles or contact lenses, a structural, medically defined demand base that provides recession-resistant market volume.

- Digital Eye Strain Surge Creating Premium Blue-Light and Anti-Fatigue Lens Category: As of 2023, the average American spends 7 hours and 4 minutes looking at a screen each day, driving widespread awareness of digital eye strain (computer vision syndrome), driving the demand for protective eyewear.

- Fashion-Driven Frame Premiumization by Luxury Brand Licensing: The eyewear market's evolution from medical device to fashion accessory has permanently elevated US average frame prices. US consumer willingness to purchase multiple fashion frames increases the average frames-per-consumer.

- Aging Baby Boomers Creating Structural Presbyopia and Premium Progressive Lens Demand: By 2030, all 73 million baby boomers in the United States will be age 65 or older, where presbyopia (age-related near vision loss) affects the population, creating a sustained high-value demand wave for progressive and bifocal lenses.

Market Restraints

- High Out-of-Pocket Costs and Vision Insurance Gaps for Low-Income Americans: Despite most of the Americans holding vision insurance, some of the Americans remain uninsured for vision care. Even insured patients face high out-of-pocket costs and require annual exam copays.

- Frame Import Tariff Risk from US-China Trade Policy: Approximately 95% of eyewear frames are made outside of America, with more than 90% produced in China, creating significant cost exposure from US-China trade policy developments. Any further tariff escalation creates pricing pressure that either reduces brand owner margins or requires retail price increases that could dampen unit volume growth in price-sensitive market segments.

Market Opportunities

- Augmented Reality and Smart Eyewear Creating the Next Prescription Eyewear Category: Augmented reality (AR) and smart eyewear are opening a new prescription category by integrating vision correction with digital overlays, health tracking, and connectivity features. This creates opportunities for premium pricing, partnerships with tech firms, and expansion into applications such as navigation, remote assistance, and immersive experiences.

- Myopia Management Creating Premium Pediatric Eyewear Sub-Category: US childhood myopia rates are increasing, creating growing demand for specialized myopia management contact lenses and spectacles that slow myopia progression in children.

Market Challenges

- Optical Retail Consolidation Creating Competitive Intensity and Margin Pressure: Private equity-backed optical retail consolidation is creating a competitive environment with fewer independent optical practices and more corporate chain locations competing on price. This consolidation reduces premium pricing power and compresses independent optometrist margins that previously supported premium frame dispensing.

- Contact Lens Price Transparency Compressing E-Commerce and Optometrist Revenue: Online contact lens pricing provides immediate price comparison for identical contact lens SKUs - enabling consumers to compare prices across channels and purchase from the lowest-cost provider. This price transparency has compressed US contact lens retail margins significantly, reducing average practitioner revenue.

Emerging Market Trends

1. Smart and AR Eyewear Entering Mainstream Commercial Phase

In March 2026, Meta Platforms launched two new Ray-Ban prescription smart glasses. The new glasses, which are available for pre-order in the U.S. starting at $499, broaden options for prescription eyewear users, indicating the premium prescription eyewear market's role in spatial computing adoption. Prescription-compatible smart eyewear is expected to reach 5%+ of US premium eyewear sales by 2030.

2. Blue-Light Blocking and Functional Lens Premium Category Scaling

Blue-light blocking and functional lenses are scaling as consumers seek protection from prolonged screen exposure, driving demand for premium, value-added eyewear solutions. This is increasing average selling prices and encouraging brands to expand into specialized lens categories with health and performance benefits.

3. Premium Progressive Lens Customization Through Digital Technology

Premium progressive lens customization through digital technology is advancing as manufacturers use AI-driven measurements and digital surfacing to deliver highly personalized vision correction. This improves visual comfort and precision, enabling higher-value offerings and boosting demand for tailored, premium eyewear solutions.

4. Telehealth Eye Exams Expanding Prescription Access and Market Reach

Telehealth eye exams are expanding prescription access by enabling remote vision testing and consultations, especially in underserved and rural areas. This broadens market reach for eyewear brands, accelerates online sales, and supports faster prescription renewals and customer acquisition.

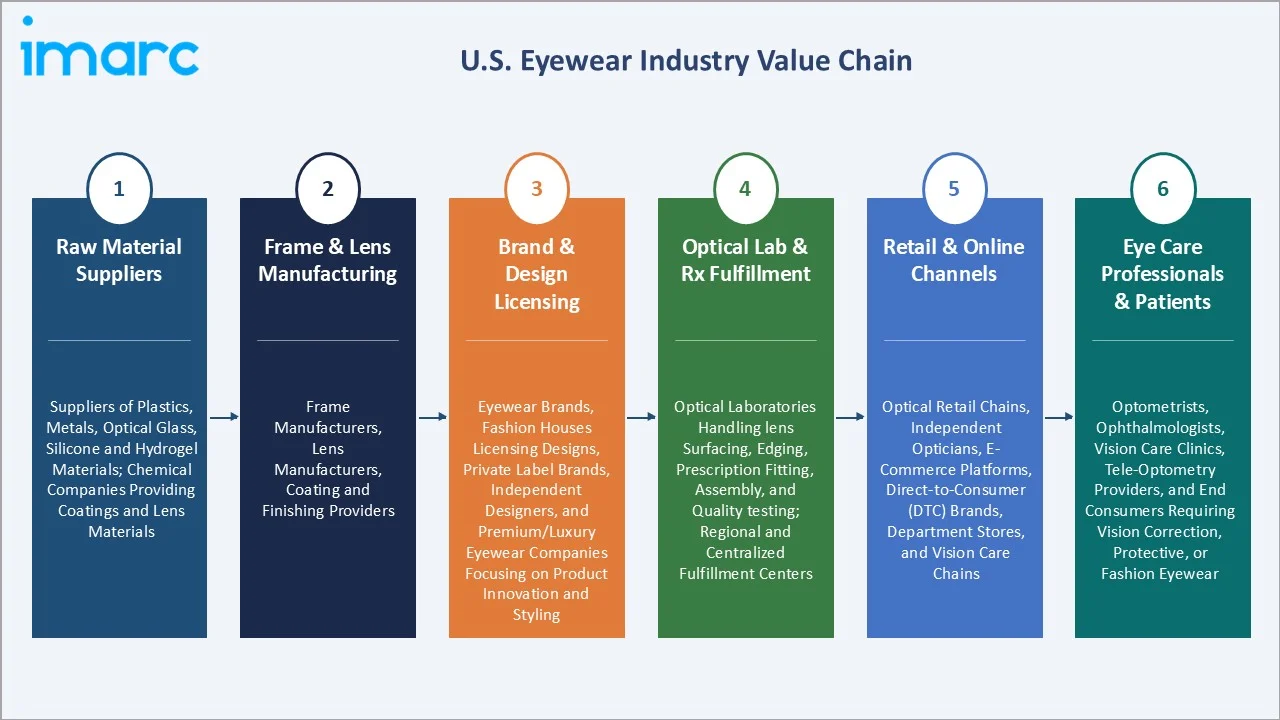

Industry Value Chain Analysis

The U.S. eyewear value chain spans raw material supply through frame and lens manufacturing, brand licensing, optical laboratory prescription fulfillment, and retail dispensing to US corrective eyewear patients.

|

Stage |

Key Participants |

|

Raw Material Suppliers |

Suppliers of plastics, metals, optical glass, silicone and hydrogel materials; chemical companies providing coatings and lens materials |

|

Frame & Lens Manufacturing |

Frame manufacturers, lens manufacturers, coating and finishing providers |

|

Brand & Design Licensing |

Eyewear brands, fashion houses licensing designs, private label brands, independent designers, and premium/luxury eyewear companies focusing on product innovation and styling |

|

Optical Lab & Rx Fulfillment |

Optical laboratories handling lens surfacing, edging, prescription fitting, assembly, and quality testing; regional and centralized fulfillment centers |

|

Retail & Online Channels |

Optical retail chains, independent opticians, e-commerce platforms, direct-to-consumer (DTC) brands, department stores, and vision care chains |

|

Eye Care Professionals & Patients |

Optometrists, ophthalmologists, vision care clinics, tele-optometry providers, and end consumers requiring vision correction, protective, or fashion eyewear |

The optical laboratory tier represents a critical but largely invisible value chain layer. Lab consolidation is reducing the independent lab count while improving processing technology and turnaround time, further extending value chain control.

Technology Landscape in the U.S. Eyewear Industry

Advanced Lens Technology and Photonics

Advanced lens technology and photonics are transforming the U.S. eyewear industry by enabling high-precision optics, improved light management, and enhanced visual clarity through innovations like digital surfacing and adaptive lenses. These advancements support the development of smart, performance-driven eyewear with features such as blue-light filtering, light-adjusting lenses, and integration with AR/AI technologies.

Digital Eye Examination and AI-Powered Refraction

Digital eye examination and AI-powered refraction are transforming the U.S. eyewear industry by enabling faster, more accurate vision testing through automated diagnostics and remote assessment tools. These technologies expand access to eye care, support tele-optometry, and streamline prescription generation, driving efficiency across clinical and retail eyewear ecosystems.

Contact Lens Material and Design Innovation

Contact lens material and design innovation are advancing the eyewear industry by introducing high-oxygen, moisture-retaining materials and ergonomic designs that enhance comfort, vision clarity, and wear time. These developments enable specialized lenses for astigmatism, presbyopia, and myopia control, while supporting premium product differentiation and improved patient outcomes.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Spectacles |

54.2% |

2025 |

|

Gender |

Unisex |

46.8% |

2025 |

|

Distribution Channel |

Optical Stores |

🔒 |

2025 |

|

Region |

South |

36.5% |

2025 |

By Product

Spectacles lead at 54.2% market share (2025). This segment encompasses prescription frames (single vision, progressive, bifocal) plus non-prescription fashion readers and computer glasses. Premium progressive lenses for baby boomers represent the highest per-transaction revenue spectacle category. Spectacles grow at ~4.3% CAGR (2026-2034), supported by US myopia prevalence growth, baby boomer presbyopia wave, and digital eye strain premium lens demand.

To access detailed market analysis, Request Sample

Sunglasses at 28.6% grow fastest at ~5.1% CAGR, driven by brand fashion premiumization and outdoor lifestyle trends. Contact lenses at 17.2% grow at ~4.8% CAGR, led by market leadership in daily disposable silicone hydrogel lenses and premium daily lens adoption growth.

By Gender

Unisex eyewear leads at 46.8% market share (2025). The fashion industry's gender-neutral frame design trend, oversized acetate, geometric metal, and clear/translucent structures, has made unisex styling the dominant U.S. eyewear category at premium optical retail.

Women at 28.7% grow at ~4.9% CAGR, the fastest gender segment, reflecting women's higher eyewear purchase frequency, higher luxury brand fashion frame adoption, and leadership in DTC online eyewear purchasing. Premium women's fashion license frames are the highest per-unit revenue optical retail products. Men at 24.5% grow at ~4.3% CAGR, supported by sport and outdoor sunglass premiumization and progressive lens demand as the male boomer demographic enters peak presbyopia years.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers & Characteristics |

|

South |

36.5% |

Large and growing population base driving demand for vision correction; strong presence of optical retail chains and franchise networks; rising prevalence of vision disorders and increasing access to affordable eyewear |

|

West |

23.8% |

High consumer spending power and preference for premium and designer eyewear; strong adoption of digital and smart eyewear; high awareness of eye health and preventive care |

|

Midwest |

20.4% |

Established healthcare infrastructure and steady demand for prescription eyewear; strong insurance coverage penetration supporting routine eye exams |

|

Northeast |

19.3% |

High urban population density with strong demand for premium and fashion eyewear; high insurance coverage and access to eye care professionals; growth of e-commerce and DTC eyewear brands |

The South's 36.5% dominance is structurally reinforced by Texas and Florida, the most populous states, forming the two anchoring markets of a Southern regional eyewear economy generating high revenue. Texas's high concentration of Hispanic consumers creates distinctive eyewear fashion demand.

The West's 23.8% reflects California's population, providing the nation's single largest state eyewear market, generating high revenue annually. Silicon Valley and Pacific Northwest technology workers are the primary US demographic for premium blue-light blocking and computer-optimized lens adoption, with employer-sponsored vision benefit programs at tech companies providing generous annual frame allowances that support premium lens and frame purchases.

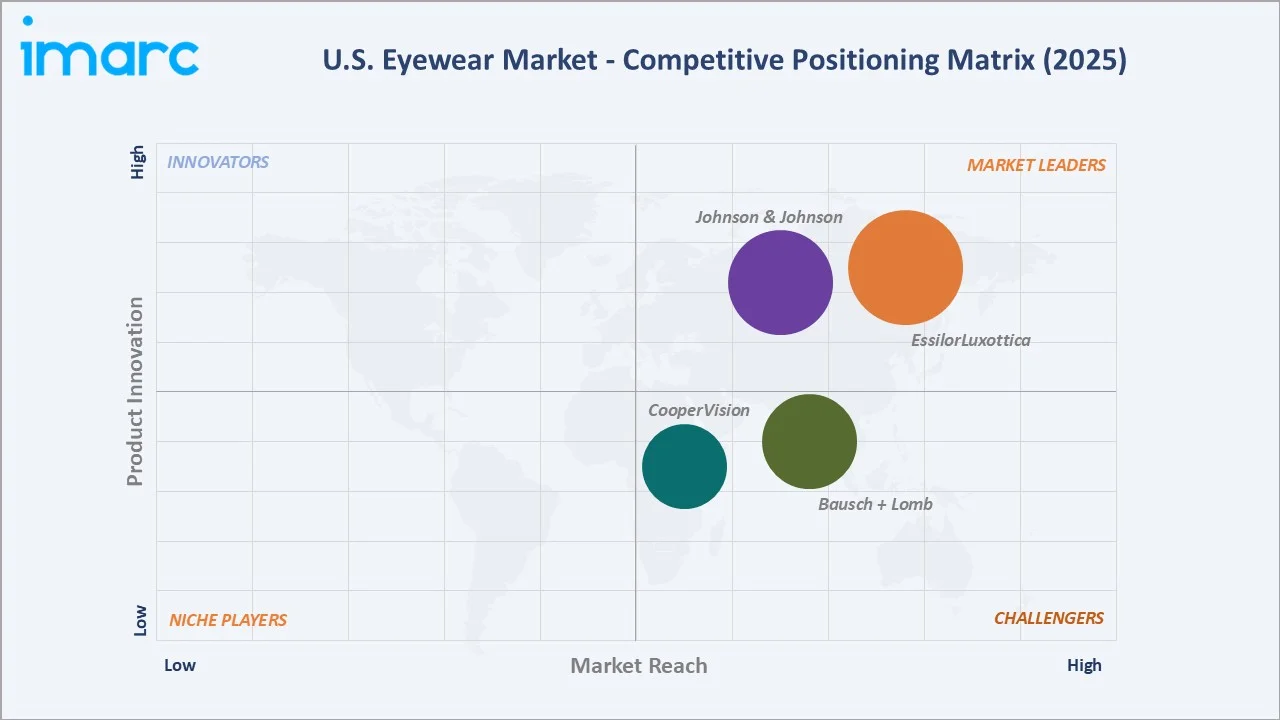

Competitive Landscape

The U.S. eyewear market is highly concentrated at the premium optical retail and lens manufacturing level. This market concentration is unprecedented in US consumer markets. No other U.S. eyewear player holds more than 8% total market value share.

|

Company Name |

Brand |

Market Position |

Core Strength |

|

EssilorLuxottica |

Ray-Ban, Oakley, Persol, Oliver Peoples, Vogue Eyewear, Arnette, Alain Mikli, Costa, Native Eyewear, and Bolon, among others |

Market Leader |

EssilorLuxottica offer exclusive eyewear that stands as a testament to highly skilled artistry and innovation. |

|

Johnson & Johnson |

ACUVUE Contact Lenses |

Market Leader |

ACUVUE is unbeaten in comfort in 47 clinical studies. |

|

Bausch + Lomb |

Biotrue, SofLens, ULTRA, PureVision |

Strong Challenger |

Bausch + Lomb offers soft, specialty, and gas-permeable contact lenses with breakthrough technologies in all modalities. |

|

CooperVision |

MyDay, clariti 1 day, MiSight 1 day, Biofinity, Avaira Vitality |

Strong Challenger |

CooperVision offers a comprehensive array of 1-day and reusable contact lenses to suit any lifestyle, budget and vision correction needs. |

The DTC digital disruption represents the most structurally significant competitive shift in U.S. eyewear since managed vision care's emergence in the 1980s. DTC platforms collectively serve US annual eyewear purchasers at 40-80% lower price points than optical retail chains, establishing a dual-market structure where premium and DTC channels serve distinct but occasionally overlapping consumer segments.

Key Company Profiles

EssilorLuxottica

EssilorLuxottica is one of the largest eyewear companies and the undisputed US market leader.

- Brands: Ray-Ban, Oakley, Persol, Oliver Peoples, Vogue Eyewear, Arnette, Alain Mikli, Costa, Native Eyewear and Bolon.

- Recent Developments: In April 2025, EssilorLuxottica launched its over-the-counter Nuance Audio Glasses in the US at a launch event in New York City.

- Strategic Focus: Smart eyewear transition through Meta partnership leveraging the Ray-Ban brand; protecting the US market dominance against DTC disruption through private-label and entry-price eyewear.

Johnson & Johnson

Johnson & Johnson provides eyewear under J&J Vision, the US contact lens market's undisputed leader through its Acuvue franchise.

- Brands: ACUVUE Contact Lenses.

- Recent Developments: In June 2025, Johnson & Johnson launched ACUVUE OASYS MAX 1-Day MULTIFOCAL for ASTIGMATISM, the first and only daily disposable contact lens for people with both astigmatism and presbyopia.

- Strategic Focus: Acuvue franchise premiumization through transitions and specialty contact lens extensions.

Market Concentration Analysis

The U.S. eyewear market is highly concentrated at the premium segment level. EssilorLuxottica alone holds an estimated 35-40% of the total U.S. eyewear market value, an extraordinary concentration facilitated by the unique vertical integration of manufacturing, brands, retail, and optical lab networks. No other US consumer market of comparable scale exhibits this level of single-entity value chain control. Contact lens market concentration is more moderate with J&J Acuvue (38% US market value share), CooperVision (22%), and Bausch + Lomb (12%) in the US branded contact lens market, with three manufacturers competing on technology and practitioner relationships. The optical retail market is moderately concentrated, serving approximately 55% of US optical retail visits.

Investment & Growth Opportunities

Fastest Growing Segments

Sunglasses (~5.1% CAGR), women's eyewear (~4.9% CAGR), smart eyewear/AR glasses (~25%+ CAGR from small base), myopia management contact lenses (~35% CAGR), premium personalized progressive lenses (~12% CAGR), and telehealth vision testing platforms (~20% CAGR) represent the U.S. eyewear market's highest-growth investment vectors through 2034. Smart eyewear represents the highest CAGR opportunity from its current small base, with the US corrective lens users providing a captive addressable market as smart eyewear quality and affordability improve.

Emerging Market Opportunities

The uninsured-for-vision Americans represent the largest underserved U.S. eyewear market segment. Telehealth eye exam platforms combined with value DTC pricing are creating accessible pathways for previously excluded consumers. IMARC estimates that converting 20-30% of currently uninsured non-purchasers to annual eyewear purchasers at an average USD 100 transaction value would add USD 3-4 Billion to the US annual eyewear market, representing the largest single accessible expansion opportunity.

Investment Themes

- Smart and AR prescription eyewear manufacturing: EssilorLuxottica's Meta partnership demonstrates the commercial model for smart prescription eyewear. Investment in prescription-compatible smart glass manufacturing capabilities creates a differentiated production capability serving both current smart eyewear products and future AR eyewear as optical quality requirements increase.

- Myopia management pediatric specialty practice: Building myopia management specialty practice platforms, providing optometrist training, practice management software, patient communication tools, and lens supply, represents a high annual revenue opportunity as US pediatric myopia rates continue increasing.

Future Market Outlook (2026-2034)

The U.S. eyewear market is projected to grow from USD 40.77 Billion in 2025 to USD 61.26 Billion by 2034, delivering a 4.63% CAGR over the forecast period. The market's anchor value of USD 51.12 Billion in 2030 represents a fundamentally transformed US optical industry, where smart eyewear has achieved mainstream adoption among early majority consumers, DTC telehealth vision testing annual users, and AI-personalized progressive lenses have become the standard-of-care rather than a premium option at leading US optical chains.

Three structural forces define the U.S. eyewear market's trajectory with high certainty through 2034: demographic inevitability, the baby boomers collectively progressing through peak presbyopia years (ages 55-75) creates a permanent, expanding demand wave for progressive lens and premium frame adoption that cannot be reversed by competitive or economic factors; the smart eyewear transition establishing prescription-compatible smart eyewear as the next U.S. eyewear category, benefiting EssilorLuxottica and creating new entry points for tech-savvy optical manufacturers; and the DTC democratization effect expanding total eyewear market size by bringing price-sensitive consumers back to annual eyewear replacement cycles.

Research Methodology

Primary Research

Primary research comprised structured interviews with 70+ industry stakeholders (2025), including US optometrists and ophthalmologists from leading academic optical practices; optical retail chain category managers; product marketing executives; VSP Vision and EyeMed insurance product directors; and Vision Council of America research committee members.

Secondary Research

Secondary research encompassed Vision Council of America VisionWatch retail data 2024, American Optometric Association US optometric practice economic survey 2024, FDA medical device registration data for contact lenses, NPD Group U.S. eyewear retail tracking (2020-2025), company investor presentations and earnings disclosures, AAO Eye Health Statistics 2024, and VSP Vision Care annual report 2024. Over 115 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using bottom-up product segment models incorporating US prescription dispensing volume projections, average selling price trajectories by segment (premium spectacles, entry contact lenses, fashion sunglasses), vision insurance benefit utilization rates, DTC online channel share gain models, and demographic aging curves for presbyopia lens demand. Key inputs include US Census Bureau aging population projections, US myopia prevalence forecasts, smart eyewear adoption S-curve modeling, and DTC optical platform subscription and repeat purchase rate data.

U.S. Eyewear Market Report Scope

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Products Covered | Spectacles, Sunglasses, Contact Lenses |

| Genders Covered | Men, Women, Unisex |

| Distribution Channels Covered | Optical Stores, Independent Brand Showrooms, Online Stores, Retail Stores |

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered | EssilorLuxottica, Johnson & Johnson, Bausch + Lomb, CooperVision, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the U.S. eyewear market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the U.S. eyewear market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the U.S. eyewear industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the U.S. Eyewear Market Report

The US eyewear market reached USD 40.77 Billion in 2025, driven by US adult vision correction prevalence, baby boomer presbyopia wave, digital eye strain blue-light lens demand, and fashion premiumization of sunglasses and prescription frames.

The market grows at 4.63% CAGR during 2026-2034, reaching USD 61.26 Billion by 2034, driven by smart eyewear adoption, personalized progressive lens premiumization, myopia management contact lenses, and DTC telehealth expansion, increasing market access for underinsured Americans.

Spectacles lead at 54.2% (2025), serving US prescription eyewear users. Sunglasses at 28.6% grow fastest at ~5.1% CAGR through luxury brand and outdoor sport premiumization. Contact lenses at 17.2% are led by daily disposable market share.

Unisex eyewear leads at 46.8% (2025), reflecting the fashion industry's gender-neutral design trend adopted by premium frame brands.

The South leads at 36.5% (2025), anchored by Texas and Florida's combined population, the highest Sun Belt optical retail expansion, Florida's elderly presbyopia population, and Texas's Hispanic consumer high-frequency frame replacement purchasing patterns.

Leading companies include EssilorLuxottica, Johnson & Johnson, Bausch + Lomb, and CooperVision, among others.

The market reaches approximately USD 51.12 Billion by 2030, driven by smart eyewear premium sales, personalized AI progressive lenses becoming standard, myopia management contact lenses reaching most of the US pediatric patients, and DTC platforms serving high US prescription eyewear volume.

Daily disposable silicone hydrogel lenses are growing at an 8-10% CAGR as comfort improvements drive upgrading from monthly lenses. Myopia management contact lenses are growing 35%+ annually in the pediatric specialty segment.

Sunglasses grow at ~5.1% CAGR versus 4.63% overall, driven by brand premiumization, outdoor lifestyle trends (cycling, skiing, running) driving performance sunglass demand, and Gen-Z luxury brand sunglass adoption creating sustainable premium pricing growth.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)