United States Factoring Market Size, Share, Trends and Forecast by Type, Organization Size, Application, and Region, 2026-2034

United States Factoring Market Size, Share, Trends & Forecast (2026-2034)

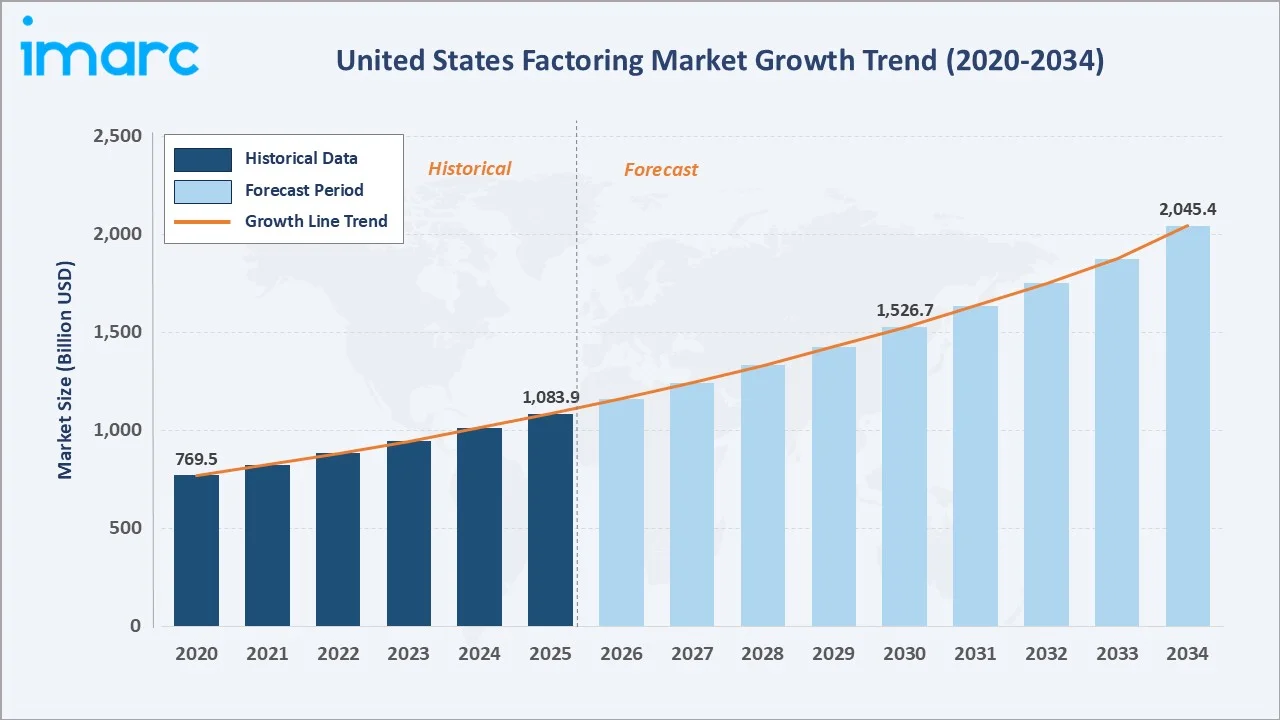

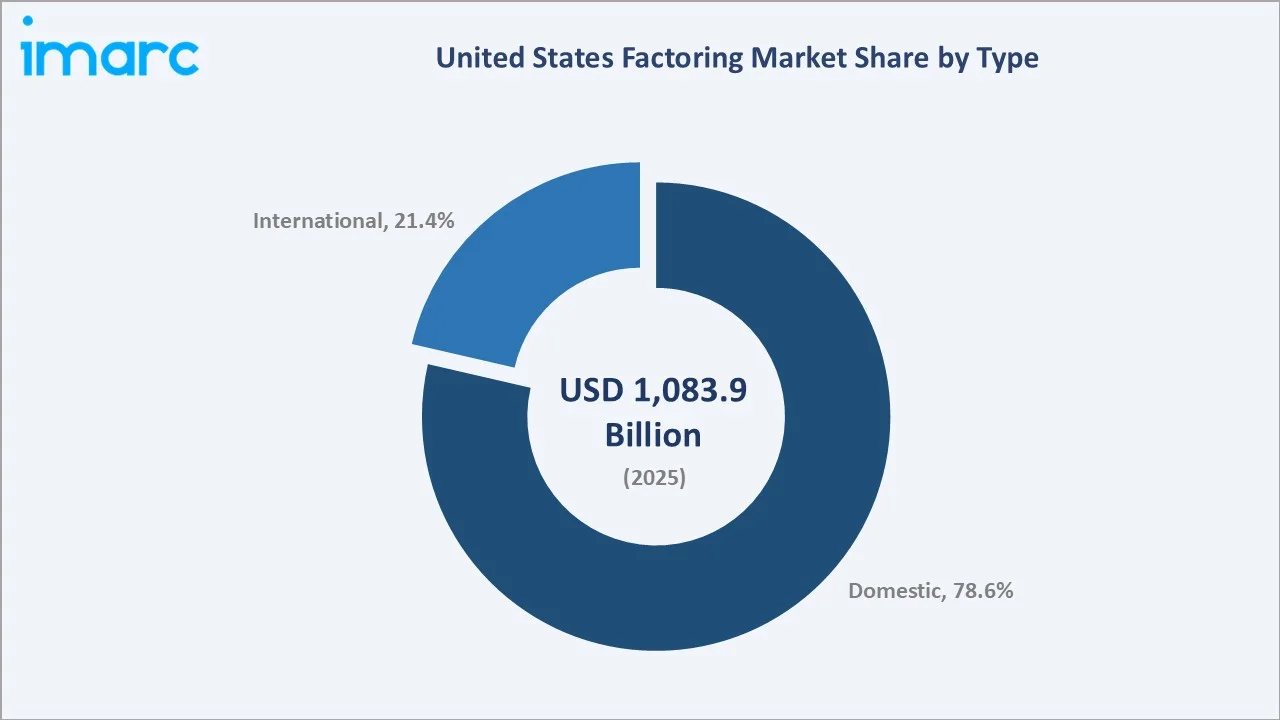

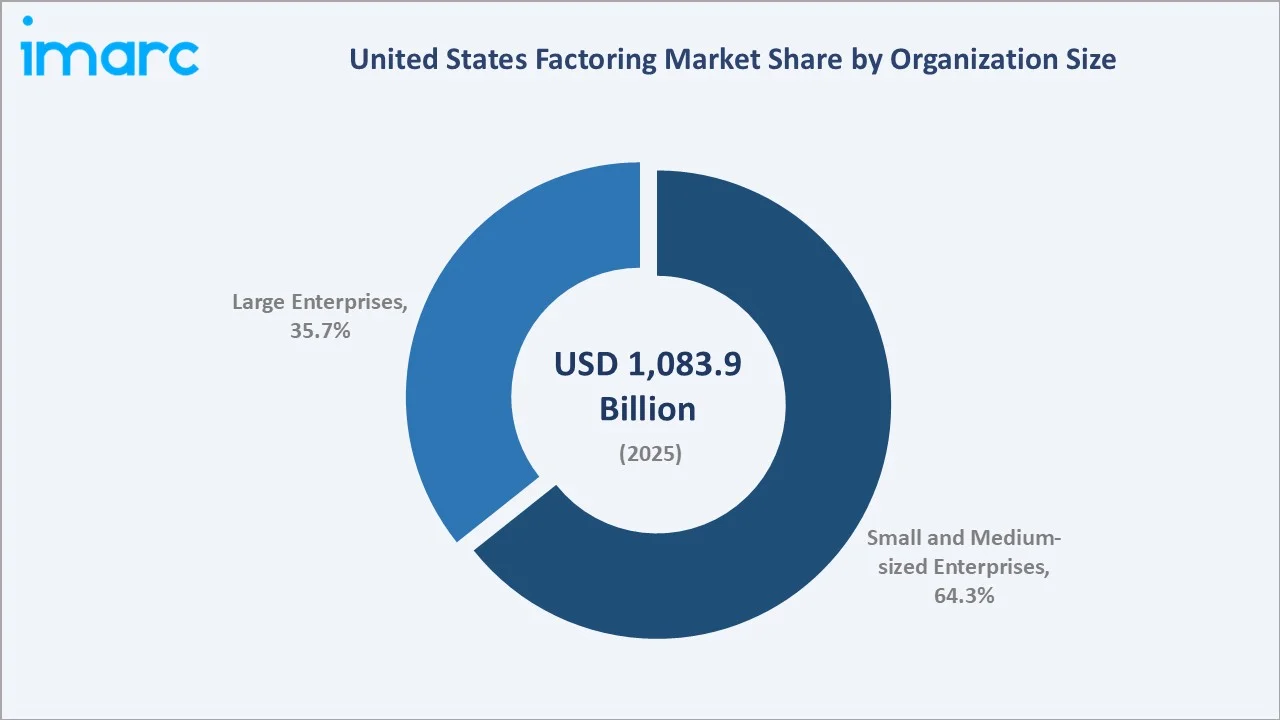

The United States factoring market reached USD 1,083.9 Billion in 2025 and is projected to reach USD 2,045.4 Billion by 2034, growing at a CAGR of 7.09% during 2026-2034. The market is driven by rising SME demand for alternative financing, digital platform integration, tightening bank credit, and expanding cross-border trade.

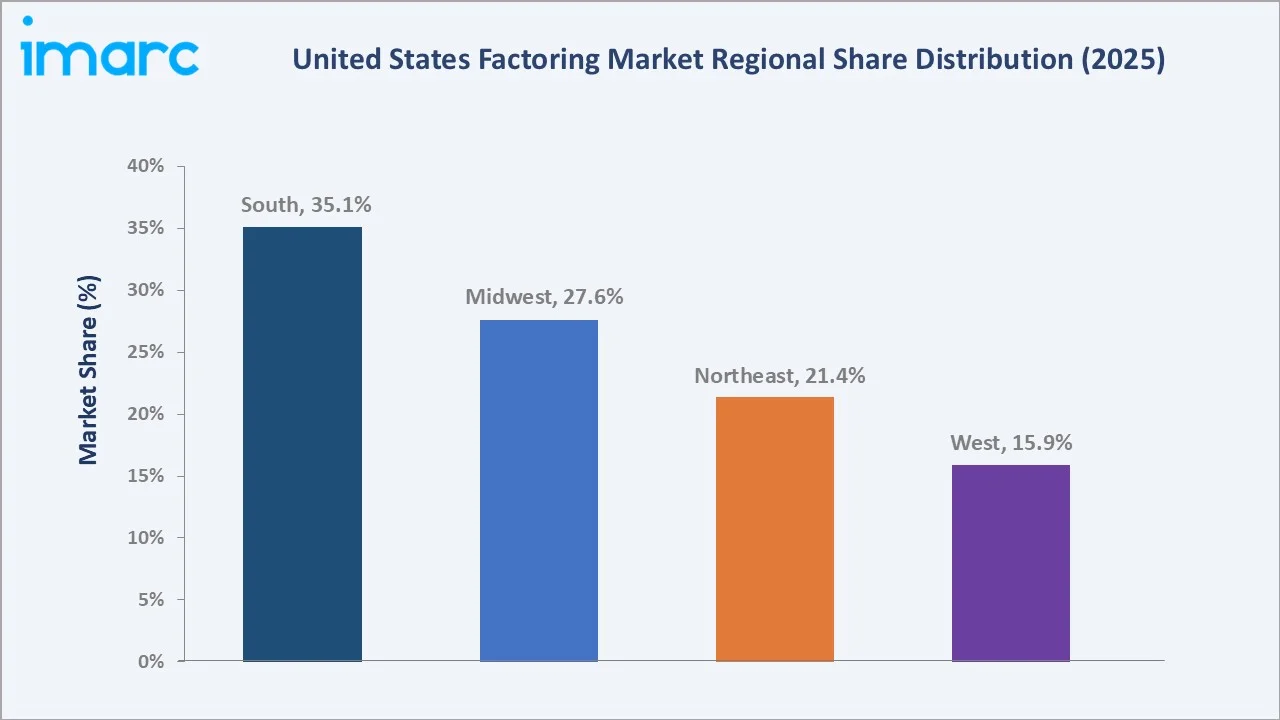

The Domestic segment dominates at 78.6% in 2025. Small and Medium-sized Enterprises lead at 64.3%. The South region commands 35.1% of the United States market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1,083.9 Billion |

|

Forecast Market Size (2034) |

USD 2,045.4 Billion |

|

CAGR (2026-2034) |

7.09% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Type |

Domestic (78.6%, 2025) |

|

Dominant Organization Size |

Small and Medium-sized Enterprises (64.3%, 2025) |

|

Leading Region |

South (35.1%, 2025) |

The market expanded from USD 769.5 Billion in 2020 to USD 1,083.9 Billion in 2025, anchored at USD 1,526.7 Billion in 2030 and forecast to reach USD 2,045.4 Billion by 2034.

To get more information on this market, Request Sample

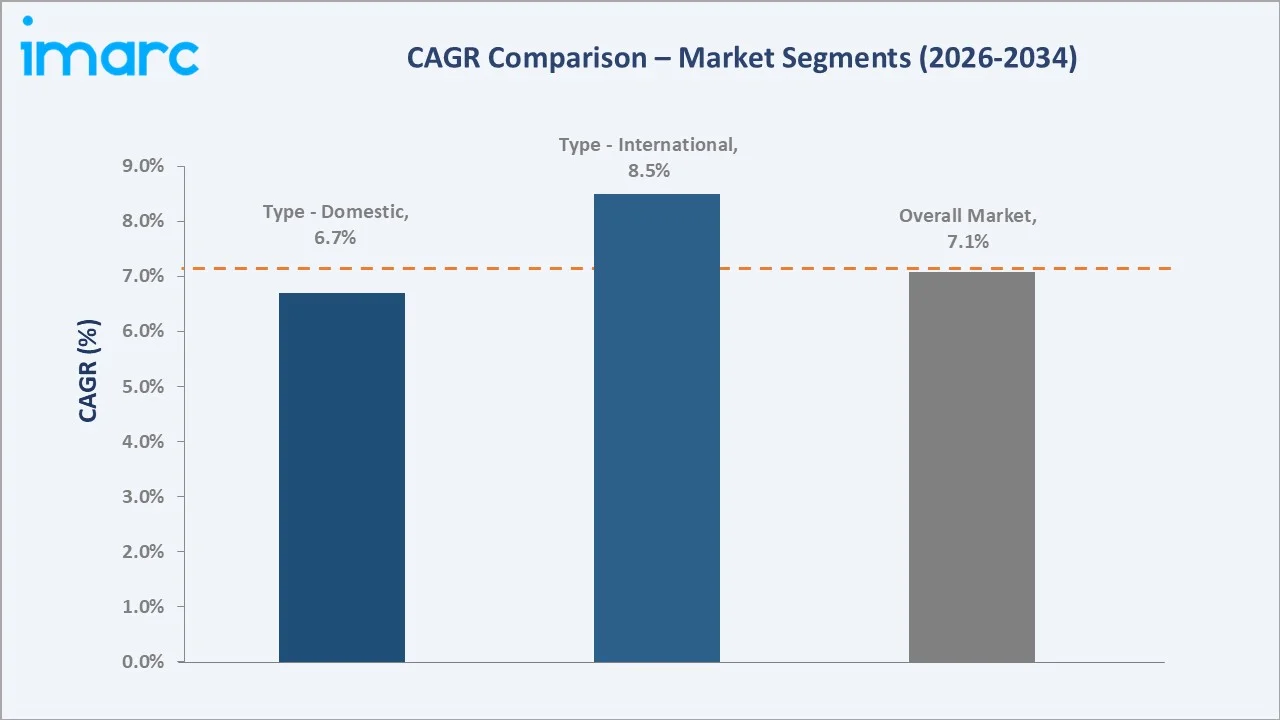

Domestic factoring grows at ~6.7% CAGR driven by SME invoice financing, while international factoring accelerates at ~8.5% CAGR as cross-border trade volumes expand and digital platforms simplify multi-currency invoice management.

Executive Summary

The United States factoring market reached USD 1,083.9 Billion in 2025, representing one of the country's most strategically significant alternative financing segments. Factoring converts receivables into immediate working capital, serving businesses across transportation, healthcare, construction, and manufacturing. The market is projected to reach USD 2,045.4 Billion by 2034.

Domestic factoring at 78.6% dominates by capturing most SME invoice financing needs. Small and Medium-sized Enterprises at 64.3% lead through their structural need for receivables-based financing as bank credit tightens. The South region at 35.1% leads through its large manufacturing, transportation, and logistics base.

Key Market Insights

|

Insight |

Data |

|

Dominant Type |

Domestic – 78.6% share (2025) |

|

Dominant Organization Size |

Small and Medium-sized Enterprises – 64.3% share (2025) |

|

Leading Region |

South – 35.1% market share (2025) |

|

Market Opportunity |

Digital embedded finance, cross-border SME factoring, healthcare receivables, and AI-driven risk analytics |

Key Analytical Observations Supporting the Above Data:

- Domestic at 78.6%: Domestic factoring dominates as it serves the largest pool of US businesses requiring receivables-based liquidity, driven by transportation, staffing, and manufacturing clients with 30–90 day payment cycles and limited access to traditional bank lines of credit.

- Small and Medium-sized Enterprises at 64.3%: SMEs lead factoring demand as they face tighter bank credit qualification requirements, longer customer payment cycles, and greater cash flow volatility, making receivables-based financing the most accessible working capital solution.

- South at 35.1%: The South leads due to its dense concentration of transportation corridors, oil and gas services, construction activity, and manufacturing operations, all sectors with high invoice volumes and extended payment terms that make factoring structurally advantageous.

United States Factoring Market Overview

The United States factoring market encompasses the purchase of commercial accounts receivable by factoring companies from businesses at a discount, providing immediate working capital in exchange for future invoice payments. The market serves transportation, healthcare, construction, manufacturing, staffing, and retail sectors through recourse and non-recourse factoring structures.

The ecosystem integrates invoice originators, bank-owned factors, independent factoring companies, fintech platforms, credit rating agencies, and regulatory bodies. Macroeconomic factors include rising prime rates constraining bank lending, digital platform adoption, SME financing gaps, and expanding cross-border trade activity.

Market Dynamics

To evaluate market opportunities, Request Sample

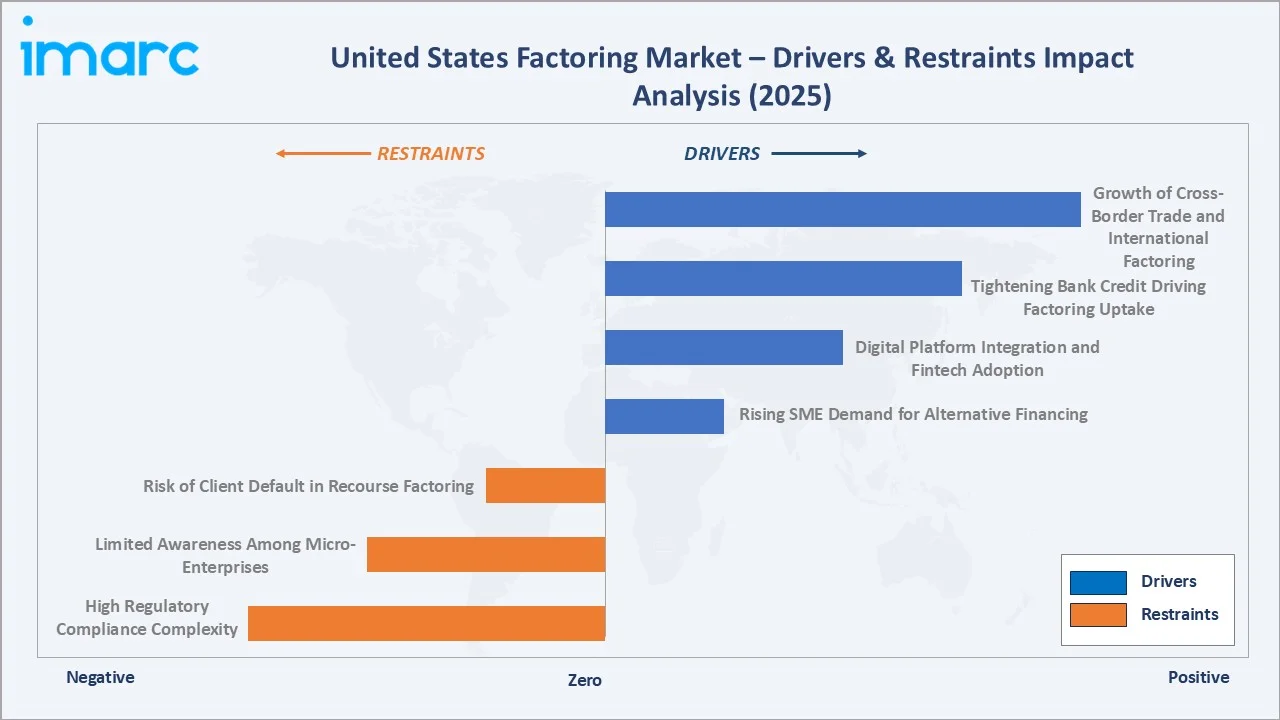

Market Drivers

- Rising SME Demand for Alternative Financing: Small and medium enterprises increasingly rely on factoring as traditional bank lending tightens. Bank prime rate increases from 2022 to 2023 elevated collateral requirements, channelling businesses toward receivables-based financing that underwrites invoice quality rather than borrower balance sheets, structurally expanding factoring market addressability.

- Digital Platform Integration and Fintech Adoption: Cutting-edge fintech technology is overhauling legacy factoring operations through real-time invoice processing, automated credit assessment, and streamlined document management. Cloud solutions, ML risk scoring, and ERP integrations compress onboarding from weeks to hours, expanding the addressable customer base for digital-first factoring providers.

- Tightening Bank Credit Driving Factoring Uptake: Federal Reserve rate policy and elevated credit standards from 2022 through 2024 reduced commercial lending availability for small businesses. Transportation fleets and SME manufacturers unable to renew revolving lines turned to factoring for same-day advances, creating structural demand growth across the factoring industry.

- Growth of Cross-Border Trade and International Factoring: Expanding global trade volumes, e-commerce internationalization, and supply chain restructuring are increasing demand for international factoring services. Digital platforms enabling multi-currency invoice management and cross-border credit verification are reducing friction in international factoring, supporting above-market CAGR for this segment.

Market Restraints

- High Regulatory Compliance Complexity: Federal and state regulatory requirements governing factoring disclosures, UCC lien filings, and consumer protection impose significant compliance costs on factoring companies. Navigating varying state-level regulations and maintaining reporting requirements increases operational overhead and limits smaller players from expanding geographically.

- Limited Awareness Among Micro-Enterprises: Many micro and small businesses remain unaware of factoring as a financing solution, defaulting to high-cost credit cards or foregoing growth opportunities due to cash flow constraints. Low financial literacy and the perception of factoring as a lender of last resort limit market penetration among the smallest business segment.

- Risk of Client Default in Recourse Factoring: In recourse factoring arrangements, the client assumes liability for non-payment by debtors, creating risk concentration for businesses with lower-quality receivables. Economic downturns, sector-specific payment disruptions, and debtor insolvencies can expose factoring clients to unexpected repayment obligations, reducing the attractiveness of factoring in volatile economic periods.

Market Opportunities

- Embedded Finance Integration with ERP and Accounting Platforms: US factoring providers integrating with QuickBooks, Xero, Shopify, and FreshBooks can access real-time invoice data and offer instant factoring approvals to SMEs within their existing financial workflows. This embedded finance model reduces customer acquisition costs and creates recurring touchpoints that deepen platform lock-in.

- Healthcare Receivables Factoring Expansion: Healthcare providers face complex billing cycles, insurance reimbursement delays, and regulatory compliance requirements that create persistent cash flow gaps. Specialized healthcare factoring addressing HIPAA compliance, medical billing complexity, and payer-specific receivables management presents a large and underserved growth opportunity within the broader factoring market.

Market Challenges

- Competitive Pressure from Bank Supply-Chain Finance Programs: Large banks offering reverse factoring and supply-chain finance programs to tier-1 corporate clients can disintermediate traditional factoring for approved supplier networks. As bank-sponsored programs offer lower cost of capital to creditworthy suppliers, independent factoring companies face margin compression in the highest-quality receivables segments.

- Technology Investment Requirements for Competitive Parity: The accelerating digitization of factoring operations requires continuous platform investment in AI underwriting, fraud detection, real-time bank statement analytics, and UCC filing automation. Smaller independent factors unable to fund technology modernization face declining competitive positioning against well-capitalized fintech-integrated competitors.

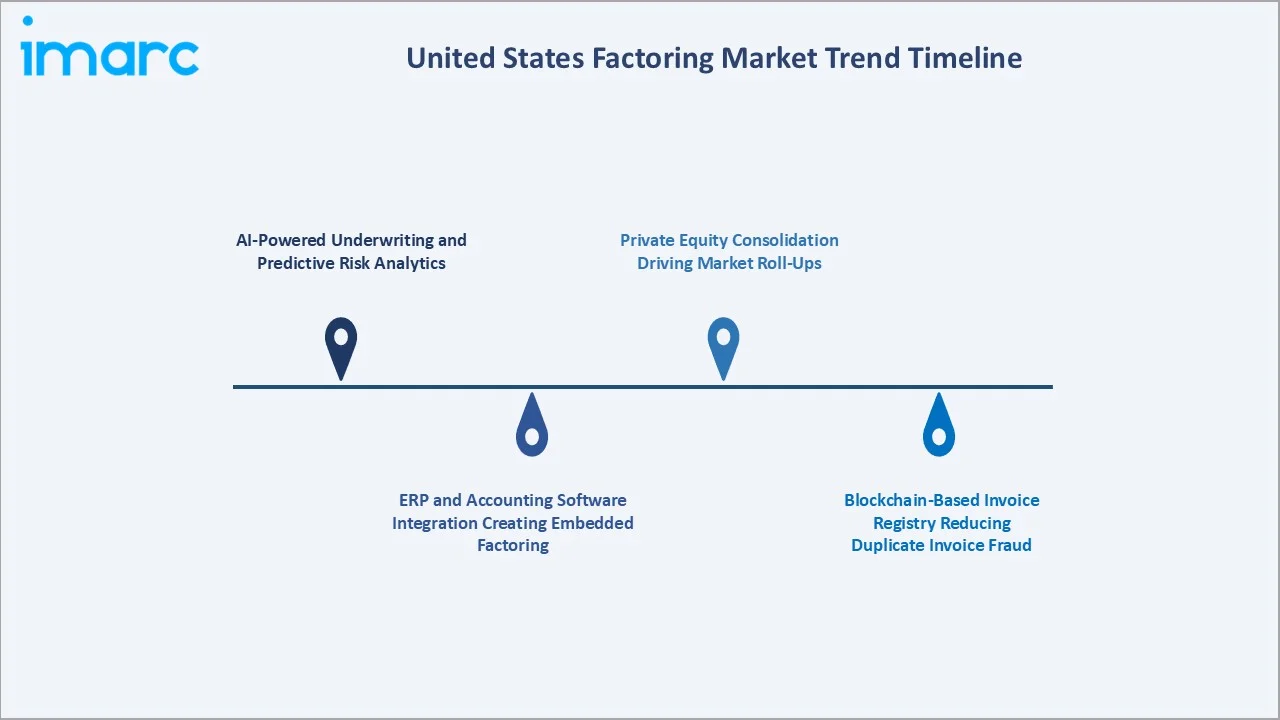

Emerging Market Trends

1. AI-Powered Underwriting and Predictive Risk Analytics

AI-driven underwriting models are transforming factoring credit decisions by analyzing bank statement data, payment history, debtor financial health, and sector-specific risk factors in real time. Machine learning algorithms reduce default rates, improve advance rate accuracy, and enable factoring companies to serve a broader SME customer base by making credit decisions based on invoice quality rather than borrower credit scores.

2. ERP and Accounting Software Integration Creating Embedded Factoring

Factoring providers integrating directly with accounting platforms such as QuickBooks, Xero, and FreshBooks can offer instant invoice funding offers within existing SME financial workflows. This embedded finance model eliminates manual document submission, reduces onboarding friction, and enables continuous monitoring of receivables quality. FundThrough and BlueVine's accounting platform integrations demonstrate how embedded factoring accelerates customer acquisition.

3. Blockchain-Based Invoice Registry Reducing Duplicate Invoice Fraud

Blockchain technology is being deployed by factoring companies to create immutable invoice registries that prevent duplicate invoice financing fraud. By recording invoice funding events on distributed ledgers, factoring platforms can verify that invoices have not been previously funded by competing providers, reducing the most significant fraud risk in the factoring industry.

4. Private Equity Consolidation Driving Market Roll-Ups

Private equity sponsors are actively acquiring independent factoring companies to build scaled platforms with diversified sector exposure, technology infrastructure, and geographic coverage. Consolidation activity creates larger, better-capitalized entities with technology investment capacity and lower cost of funds, reshaping the competitive landscape through 2034.

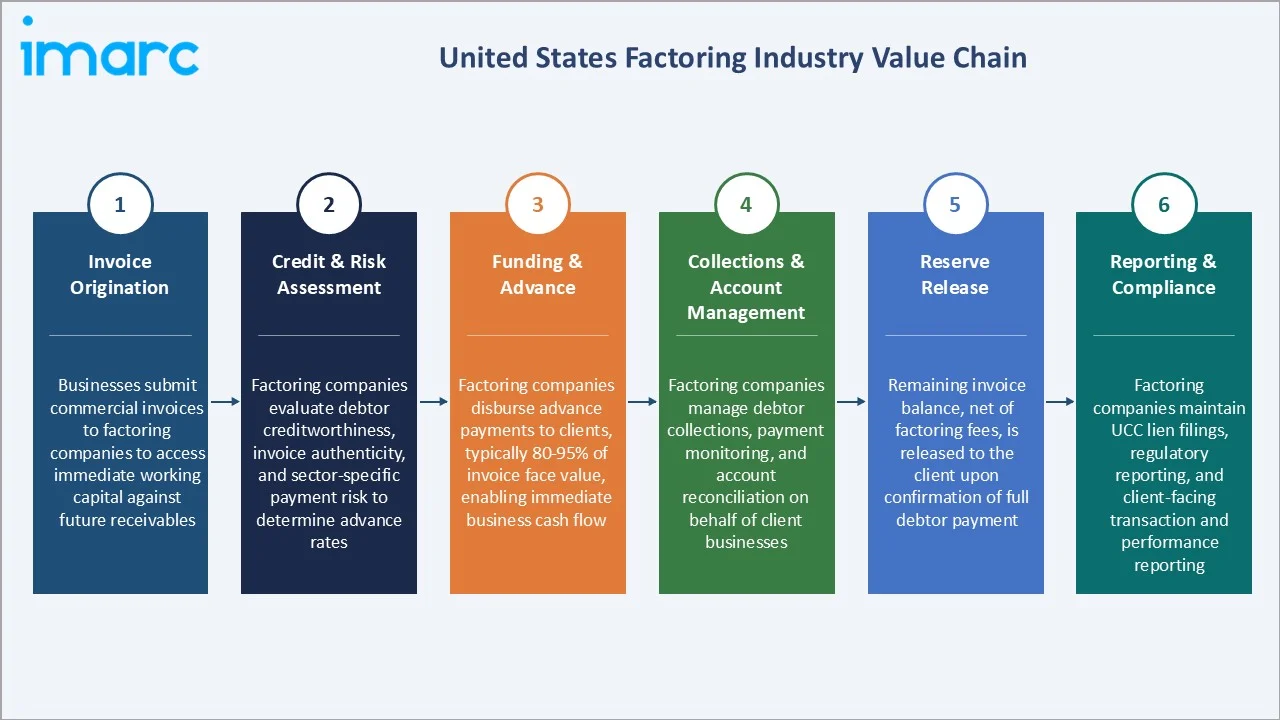

Industry Value Chain Analysis

The factoring value chain integrates invoice origination, credit and risk assessment, funding and advance disbursement, collections and account management, reserve release, and reporting and compliance. The value chain is consolidating toward digital platforms that automate multiple stages within a single integrated workflow, reducing manual processing costs and enabling same-day funding capabilities.

|

Stage |

Description |

|

Invoice Origination |

Businesses submit commercial invoices to factoring companies to access immediate working capital against future receivables |

|

Credit & Risk Assessment |

Factoring companies evaluate debtor creditworthiness, invoice authenticity, and sector-specific payment risk to determine advance rates |

|

Funding & Advance |

Factoring companies disburse advance payments to clients, typically 80-95% of invoice face value, enabling immediate business cash flow |

|

Collections & Account Management |

Factoring companies manage debtor collections, payment monitoring, and account reconciliation on behalf of client businesses |

|

Reserve Release |

Remaining invoice balance, net of factoring fees, is released to the client upon confirmation of full debtor payment |

|

Reporting & Compliance |

Factoring companies maintain UCC lien filings, regulatory reporting, and client-facing transaction and performance reporting |

Technology Landscape in the Factoring Industry

Artificial Intelligence and Machine Learning in Credit Assessment

AI and ML models analyze bank statements, payment histories, and debtor financial data to make real-time credit decisions, replacing manual underwriting processes. These systems improve accuracy, reduce human error, and enable factoring companies to serve a broader range of clients by identifying creditworthy receivables that traditional underwriting models would decline.

Cloud-Based Factoring Platform Technology

Cloud platforms enable scalable factoring operations accessible to businesses via web and mobile applications, integrating document management, invoice submission, advance tracking, and reserve management in unified portals. Cloud infrastructure reduces technology costs, enables rapid onboarding, and supports real-time integration with debtor payment systems and bank accounts.

Blockchain and Distributed Ledger for Invoice Verification

Blockchain-based invoice registries create immutable records of funded receivables, preventing duplicate invoice fraud and enabling multi-party verification of invoice authenticity. As blockchain adoption increases among factoring platforms, the technology promises to reduce fraud losses, lower the cost of risk management, and improve trust across the factoring ecosystem.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Domestic |

78.6% |

2025 |

|

Organization Size |

Small and Medium-sized Enterprises |

64.3% |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

Region |

South |

35.1% |

2025 |

By Type

The Domestic segment leads at 78.6% in 2025, capturing the dominant share of US factoring demand driven by domestic B2B transactions across transportation, manufacturing, staffing, and healthcare. Domestic factoring benefits from simpler regulatory structures, single-currency processing, and established debtor relationships within US markets.

To access detailed market analysis, Request Sample

The International segment at 21.4% reflects cross-border trade growth, US exporter adoption of two-factor systems, and expanding use of Factors Chain International (FCI) networks for multi-currency invoice management. International factoring grows at a higher CAGR (~8.5%) than domestic (~6.7%) as e-commerce exports and supply chain restructuring increase SME cross-border transaction volumes.

By Organization Size

Small and Medium-sized Enterprises lead at 64.3% through their structural reliance on receivables-based financing. SMEs face tighter bank credit qualification, longer customer payment cycles, and greater cash flow seasonality, making factoring the most accessible working capital solution. The SME segment grows at ~7.8% CAGR as digital platforms reduce onboarding friction and expand factoring accessibility.

Large enterprises at 35.7% utilize factoring primarily for supply chain finance optimization, international receivables management, and off-balance-sheet working capital strategies. Large enterprise factoring programs often involve reverse factoring arrangements coordinated with major OEM buyers and retail corporations to optimize supplier payment terms across extended supply chains.

Regional Market Insights

|

Region |

Share (2025) |

Key Factoring Market Drivers & Characteristics |

|

South |

35.1% |

Large transportation corridors, oil and gas services, manufacturing, and construction activity generate high invoice volumes and drive factoring demand |

|

Midwest |

27.6% |

Agricultural supply chains, automotive and manufacturing industries, and logistics operations support strong factoring adoption |

|

Northeast |

21.4% |

Healthcare, staffing, professional services, and financial sector receivables support high-value factoring with strong fintech platform adoption |

|

West |

15.9% |

Technology sector receivables, e-commerce suppliers, healthcare services, and construction activity drive factoring demand |

The South at 35.1% leads through its dense concentration of transportation and logistics corridors, oil and gas services companies, and manufacturing operations. Trucking owner-operators and freight brokers in the South represent the single largest factoring customer segment by volume, utilizing recourse factoring to maintain cash flow amid delayed B2B payments.

The Midwest at 27.6% reflects agricultural receivables factoring, automotive supply chain financing, and manufacturing industry demand. The Northeast at 21.4% captures high-value healthcare, staffing, and professional services factoring with strong fintech platform adoption. The West at 15.9% reflects technology sector receivables and California-based construction and healthcare factoring.

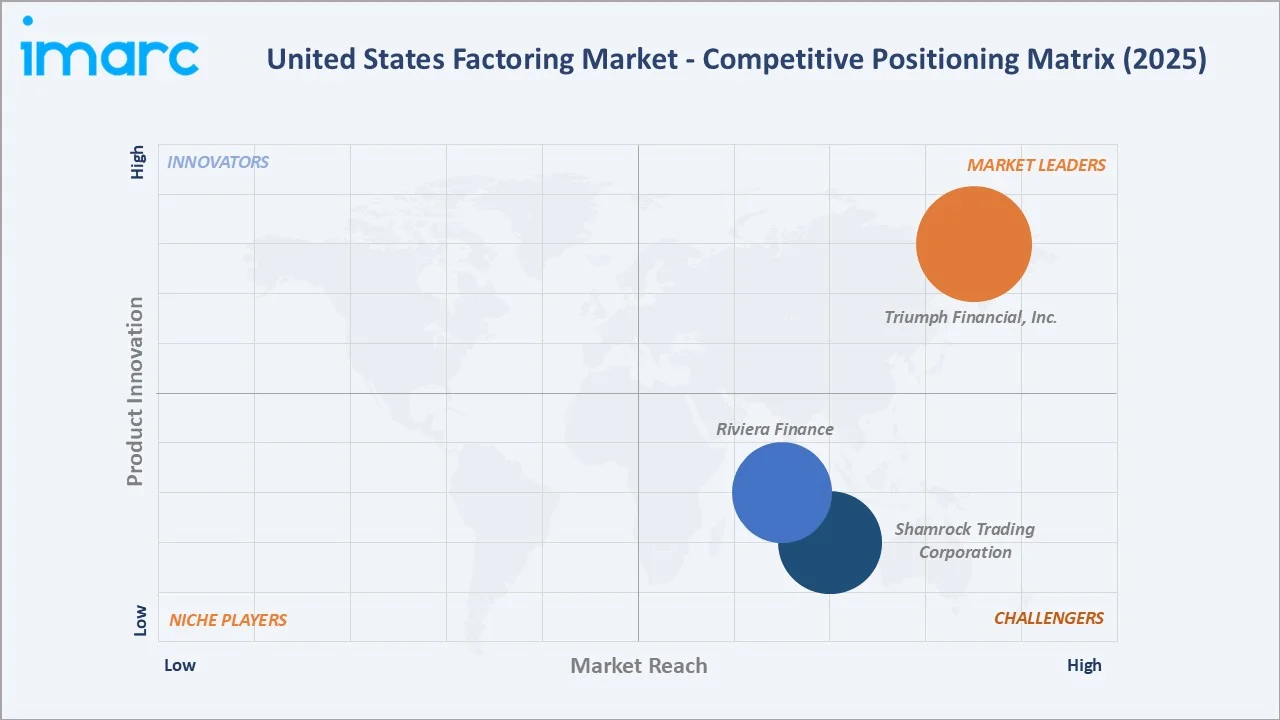

Competitive Landscape

The United States factoring market competitive landscape is fragmented with numerous regional and national players. Three competitive tiers are evident: bank-owned factors with lower cost of funds and broad sector coverage, scaled independent factors with technology platforms and sector specialization, and fintech-native factoring platforms targeting SME digital onboarding.

|

Company Name |

Key Products |

Market Position |

Core Strength |

| Triumph Financial, Inc. |

Transportation and freight invoice factoring, fuel card programs, equipment financing |

Market Leader |

Triumph Financial specializes in transportation sector factoring with integrated fuel card and insurance services. |

| Riviera Finance |

Non-recourse invoice factoring with credit guarantee across multiple industries |

Strong Challenger |

Riviera Finance offers one of the industry's most comprehensive non-recourse programs with guaranteed credit management. |

| Shamrock Trading Corporation |

Freight factoring, fuel cards, load board integration |

Strong Challenger |

RTS Financial, part of Shamrock Trading specializes in transportation and logistics factoring with real-time load verification systems. |

Key players include Triumph Financial, Inc., Riviera Finance, Shamrock Trading Corporation, and others.

Key Company Profiles

Triumph Financial, Inc.

Triumph Financial, Inc. is a United States-based financial technology company and bank holding company with a dominant presence in transportation-focused invoice factoring and freight payment services.

- Key Products: Transportation invoice factoring, fuel card programs, freight payment and audit services, equipment financing.

- Strategic Focus: Expanding integrated freight payment and factoring ecosystem combining invoice funding, fuel purchasing, insurance, and carrier compliance services to create a comprehensive financial platform for the US transportation industry.

Shamrock Trading Corporation

Shamrock Trading Corporation operates through RTS Financial, a United States-based transportation-focused factoring company providing freight invoice financing, fuel card programs, and load board integrations.

- Key Products: Freight invoice factoring, fuel cards, insurance, load board integration, carrier compliance services.

- Strategic Focus: Deepening technology integrations with transportation management systems and load boards to create embedded factoring touchpoints within carrier and broker operational workflows, reducing friction in the invoice funding process.

Market Concentration Analysis

The US factoring market is highly fragmented, with the top five independent factoring companies collectively accounting for an estimated 15-20% of total factoring volume. Bank-owned factors account for approximately 35-40% of total market volume through their lower cost of funds and broad corporate client access. The remaining 40-50% is distributed across hundreds of regional and niche independent factors.

Market concentration is expected to increase through 2034 as private equity-backed roll-ups consolidate independent factors, fintech platforms achieve scale, and bank-owned factors deepen their SME digital offerings.

Investment & Growth Opportunities

Highest Growth Segments

International factoring (~8.5% CAGR), SME digital factoring (~7.8% CAGR), healthcare receivables (~9%+ CAGR from specialized base), embedded ERP-integrated factoring (~12% CAGR from digital adoption), and cross-border e-commerce factoring (~15%+ CAGR from near-zero commercial base) represent the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

Healthcare factoring represents a structurally underserved high-value segment with complex billing cycles, insurance reimbursement delays, and specialized compliance requirements creating persistent cash flow gaps for medical providers. Healthcare factoring generates premium per-invoice margins due to the specialized expertise required and the credit quality of institutional payers.

Investment Themes

- ERP and accounting platform integration for embedded factoring market access: Investing in API integration with QuickBooks, Xero, and FreshBooks creates continuous access to real-time invoice data and enables instant factoring offers within SME workflows, dramatically reducing customer acquisition costs while expanding the addressable factoring market.

- AI-powered underwriting for SME credit expansion: Building proprietary ML models that analyze bank statement cash flow patterns, sector-specific payment behavior, and debtor credit quality enables factoring of previously declined SME receivables, expanding the total addressable market while maintaining disciplined risk management through data-driven advance rate optimization.

Future Market Outlook (2026-2034)

The United States factoring market is projected to grow from USD 1,083.9 Billion in 2025 to USD 2,045.4 Billion by 2034, delivering a 7.09% CAGR over the forecast period. The anchor value of USD 1,526.7 Billion in 2030 represents a market at its digital transformation inflection point, with AI underwriting, ERP integration, and blockchain invoice verification expected to become standard platform capabilities.

Three structural forces define market growth through 2034: the SME financing gap driven by sustained bank credit tightening creating a structurally expanding factoring addressable market; digital platform adoption compressing onboarding and increasing factoring accessibility to micro and small businesses previously underserved; and international trade growth expanding the cross-border factoring segment above the overall market CAGR.

Research Methodology

Primary Research

Primary research comprised structured interviews with 50+ industry stakeholders (2025), including factoring company executives, SME CFOs, transportation sector operators, healthcare billing managers, fintech platform founders, and regulatory compliance specialists across the United States factoring industry.

Secondary Research

Secondary research encompassed company annual reports, Federal Reserve commercial lending surveys, US Small Business Administration financing studies, Factors Chain International annual reviews, industry association publications, fintech platform disclosures, and over 60 secondary sources reviewed including government trade data and sector-specific financial reports.

Forecasting Models

Market revenue forecasts developed using a bottom-up model: (i) total US B2B accounts receivable outstanding by sector; (ii) factoring penetration rate by sector and business size; (iii) average advance rate and factoring fee by segment; (iv) technology adoption multiplier adjusting for digital platform-driven market expansion through 2034.

United States Factoring Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | International, Domestic |

| Organization Sizes Covered | Small and Medium-sized Enterprises, Large Enterprises |

| Applications Covered | Transportation, Healthcare, Construction, Manufacturing, Others |

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered | Triumph Financial, Inc., Riviera Finance, Shamrock Trading Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the United States factoring market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the United States factoring market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the United States factoring industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the United States Factoring Market Report

The United States factoring market reached USD 1,083.9 Billion in 2025, driven by the Domestic segment at 78.6%, SME dominance at 64.3%, and South region leadership at 35.1%, supported by rising alternative financing demand and digital platform adoption.

The United States factoring market grows at 7.09% CAGR during 2026-2034, reaching USD 2,045.4 Billion by 2034, reflecting sustained SME financing demand, digital platform adoption, and expanding international factoring volumes.

Domestic factoring leads at 78.6%, capturing the largest share of SME and corporate receivables financing within the United States, driven by transportation, manufacturing, staffing, and healthcare sector demand.

Small and Medium-sized Enterprises lead at 64.3% due to their structural reliance on receivables-based financing as bank credit tightens and payment cycle challenges persist across SME-heavy sectors.

The South leads at 35.1% through its dense concentration of transportation, oil and gas services, construction, and manufacturing operations — all sectors with high invoice volumes and extended payment terms.

Leading companies include Triumph Financial, Inc., Riviera Finance, Shamrock Trading Corporation, and others.

The United States factoring market is projected to reach approximately USD 1,526.7 Billion by 2030, with AI-powered underwriting, ERP integration, and digital onboarding expected to become standard capabilities across leading factoring platforms.

Top opportunities include ERP-integrated embedded factoring, healthcare receivables financing, AI-powered SME credit expansion, international cross-border factoring, and private equity consolidation of independent factoring operators across the United States.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)