United States Fire Sprinklers Market Size, Share, Trends and Forecast by Component, Fire Sprinkler System, Service, Application, and Region 2026-2034

United States Fire Sprinklers Market Size, Share, Trends & Forecast (2026-2034)

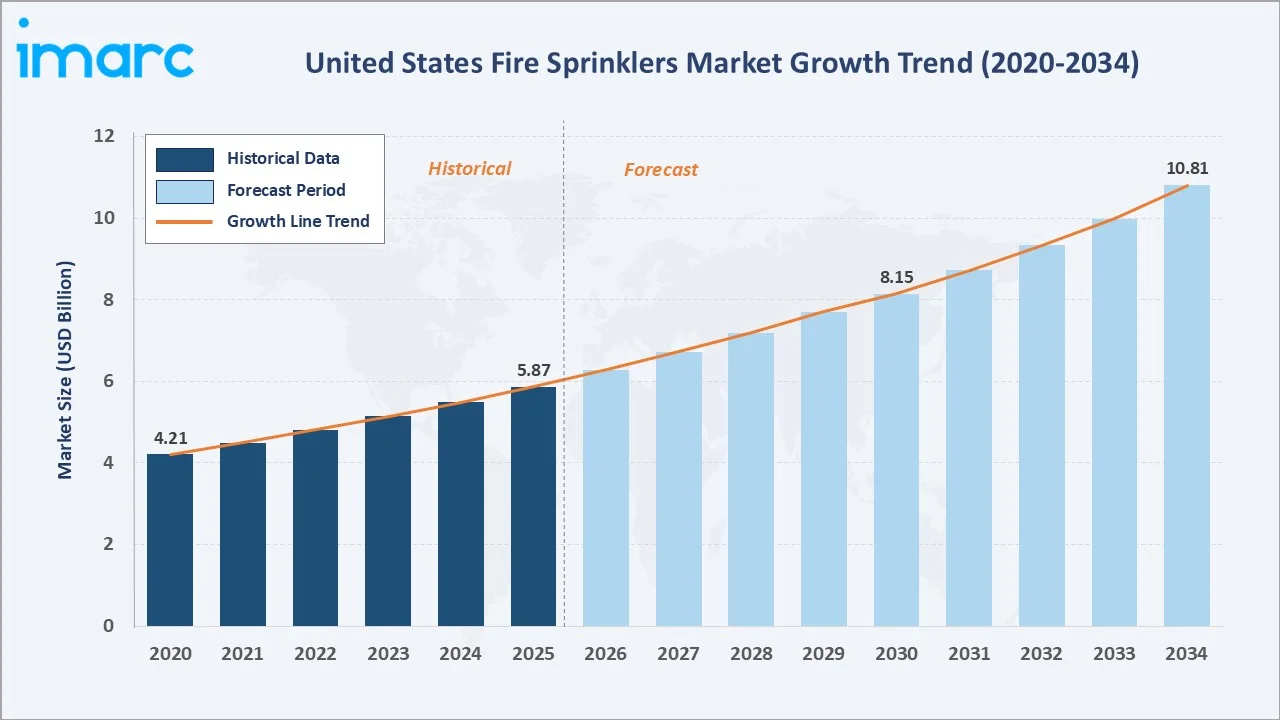

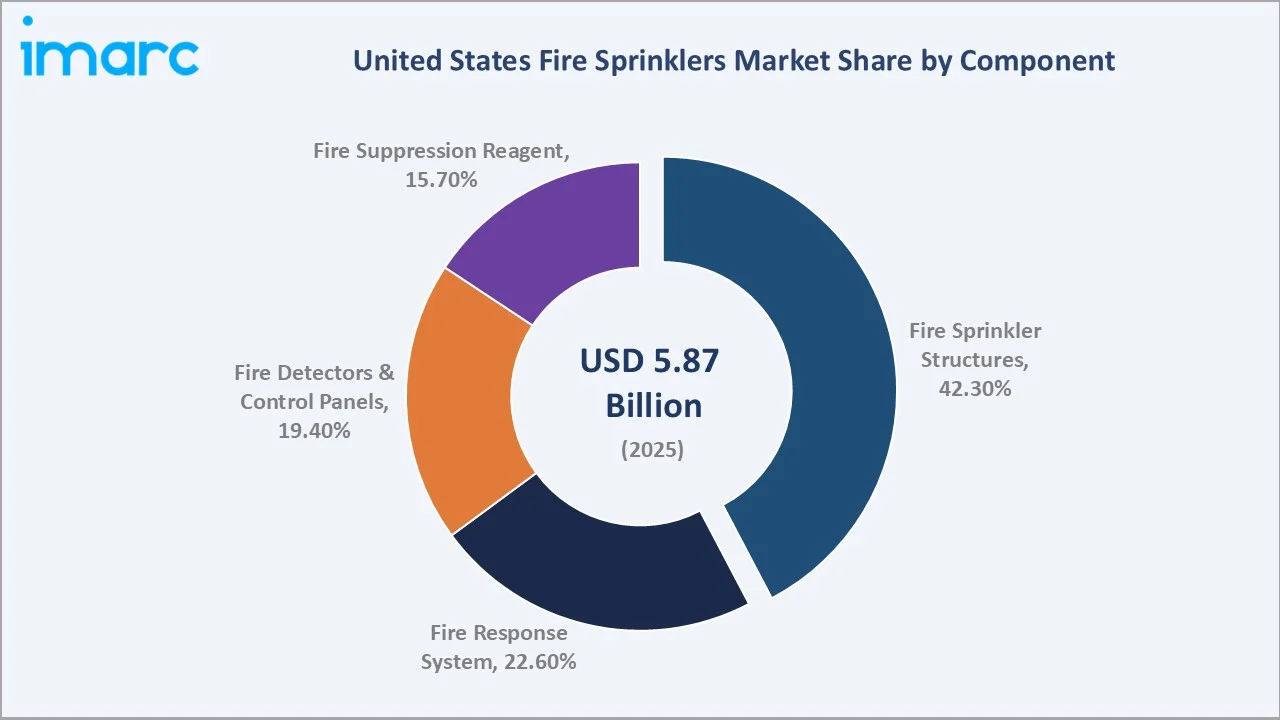

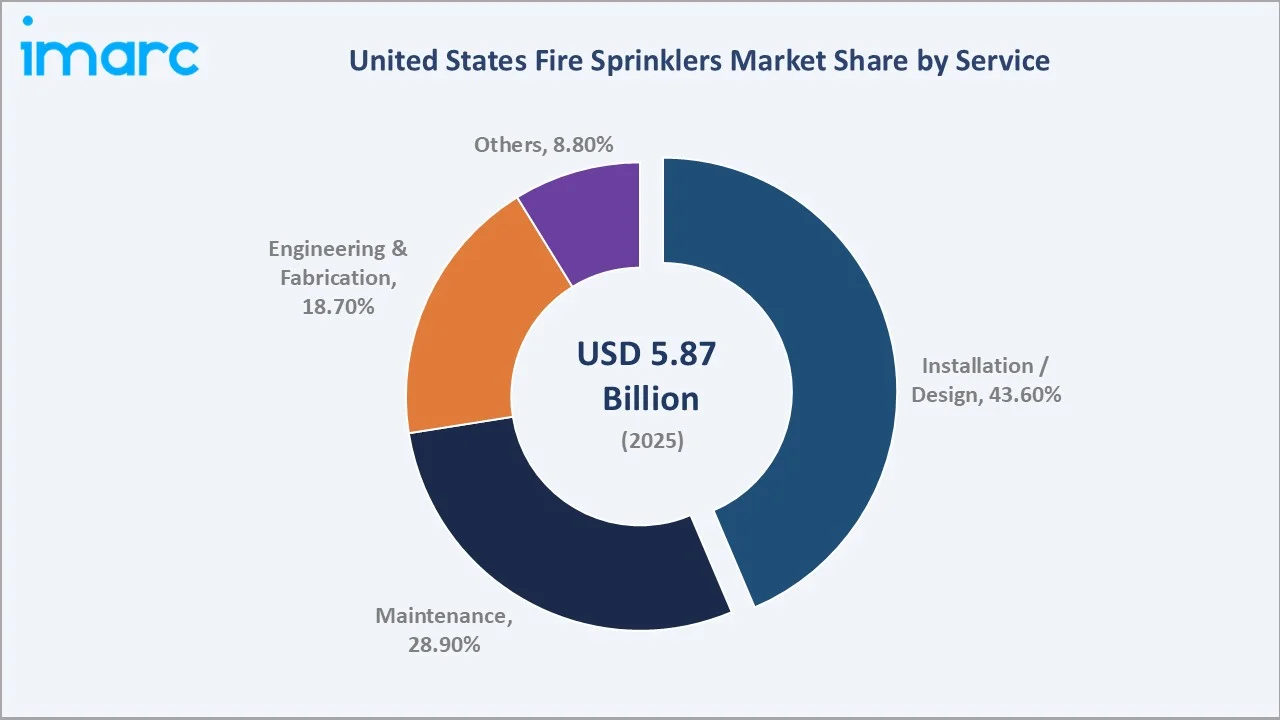

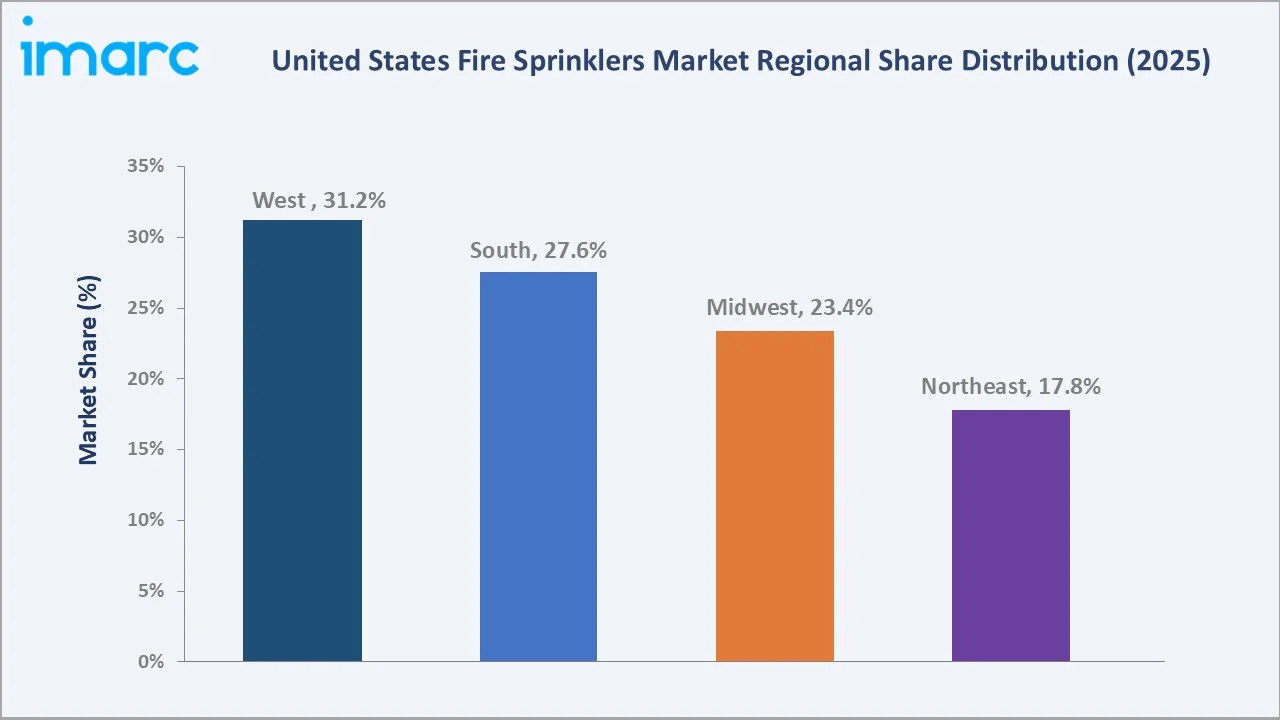

The United States fire sprinklers market size reached USD 5.87 Billion in 2025 and is projected to reach USD 10.81 Billion by 2034, exhibiting a CAGR of 6.82% during 2026-2034. According to the National Fire Protection Association (NFPA), a single sprinkler controls a fire in a home 90% of the time, protecting most of the home's possessions. Sprinkler systems can reduce fire damage by as much as 97%. Fire Sprinkler Structures lead the component mix at 42.3% in 2025, while Installation/Design dominates the service segment at 43.6%. The West region commands the largest share at 31.2% in 2025, driven by California's stringent fire safety mandates.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 5.87 Billion |

|

Forecast Market Size (2034) |

USD 10.81 Billion |

|

CAGR (2026-2034) |

6.82% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

West (31.2% share, 2025) |

|

Second Region |

South (27.6% share, 2025) |

|

Leading Component |

Fire Sprinkler Structures (42.3%, 2025) |

|

Leading Service |

Installation/Design (43.6%, 2025) |

The US fire sprinklers market growth trend from 2020 through 2034, historical expansion to USD 5.87 Billion in 2025 reflects consistent demand growth, while the forecast trajectory to USD 10.81 Billion captures accelerating construction activity, code-driven retrofits, and smart system adoption.

To get more information on this market, Request Sample

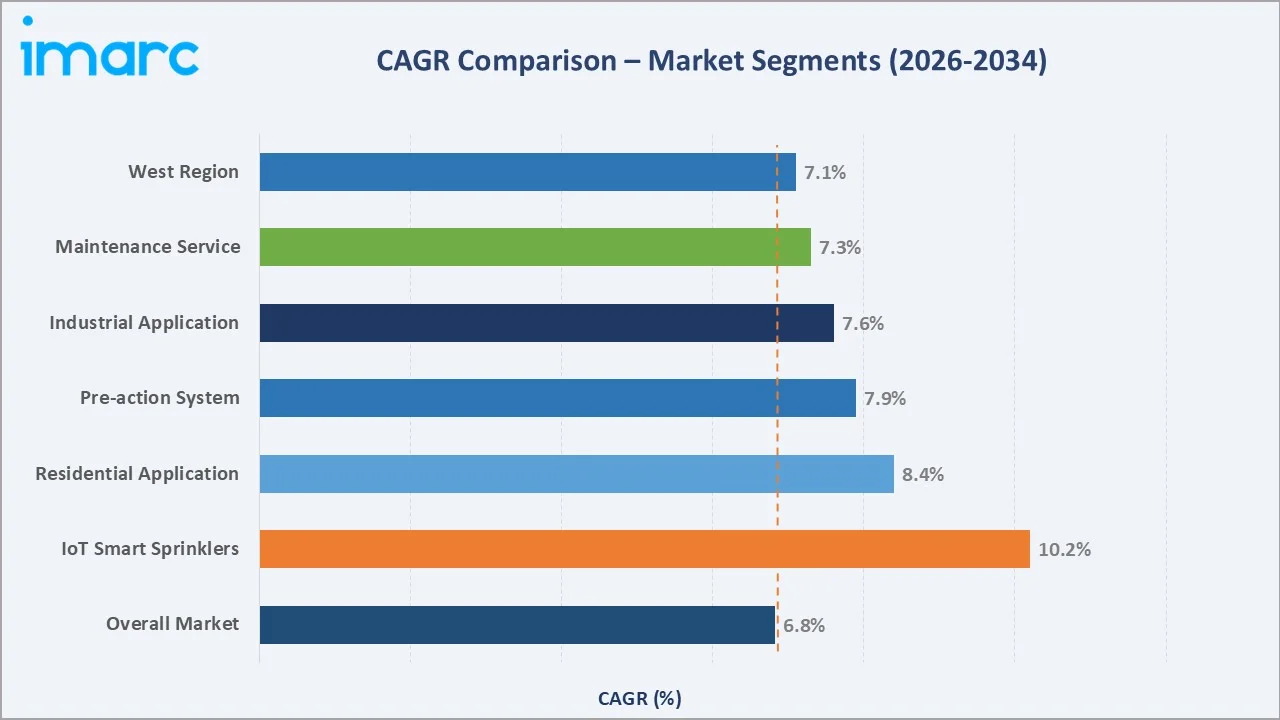

The CAGR comparisons across key segments and regions, IoT smart sprinklers at ~10.2% CAGR are the fastest-growing technology sub-category, while residential application at ~8.4% CAGR is the highest-growth end-use within the US fire sprinklers industry analysis through 2034.

Executive Summary

The United States fire sprinklers market is expanding from USD 5.87 Billion in 2025 to a projected USD 10.81 Billion by 2034, driven by the convergence of regulatory mandates, record construction investment, and transformative smart technology adoption. The National Fire Protection Association (NFPA) 13 standard, the primary US code governing sprinkler system design and installation has been adopted as mandatory or referenced in the International Building Code (IBC) across all 50 states, creating universal structural procurement demand.

Fire Sprinkler Structures dominate the component segment at 42.3% in 2025, encompassing sprinkler heads, piping, fittings, and hangers, the highest-volume material category in every installation project. Installation and Design services lead at 43.6% of total service revenue, reflecting the design-intensive nature of NFPA 13-compliant hydraulic calculation and contractor installation.

The West region leads at 31.2% in 2025, anchored by California, which mandates fire sprinklers in new single-family homes under its statewide building code since 2011 and enforces the most comprehensive fire suppression requirements in the country. The South (27.6%) and Midwest (23.4%) follow, driven by Sunbelt construction growth and industrial facility expansion respectively.

Key Market Insights

|

Insight |

Data |

|

Largest Component |

Fire Sprinkler Structures - 42.3% share (2025) |

|

Leading Service |

Installation/Design - 43.6% share (2025) |

|

Leading Region |

West - 31.2% revenue share (2025) |

|

Second Region |

South - 27.6% revenue share (2025) |

Key Analytical Observations Supporting the Above Data:

- Fire Sprinkler Structures, with 42.3% in 2025, lead because sprinkler heads, distribution piping, and structural fittings constitute the largest material cost component of every installation project. Between 2017 and 2021, in the US, local fire departments responded to an average of 52,948 structure fires annually, accounting for 11% of all structure fires, where sprinklers were installed.

- Installation/Design services at 43.6% in 2025, reflect the labor and engineering intensity of NFPA 13 compliant system delivery. A typical fire sprinkler installation requires licensed fire protection engineers (FPEs) to prepare hydraulically-calculated system designs, AutoCAD-drawn shop drawings submitted for AHJ approval, and NICET-certified technicians for field installation.

- The West region's 31.2% dominance in 2025, reflects California's unique regulatory environment. California Health & Safety Code Section 13113 requires automatic sprinklers in hotels, motels, and residential care facilities.

- The South at 27.6% in 2025 benefits from the highest US construction approvals in 2024, Texas with 133,549, Florida with 111,024, Georgia with 41,347, and North Carolina with 58,587, each requiring fire suppression assessment under local codes.

United States Fire Sprinklers Market Overview

The US fire sprinklers market encompasses the design, manufacture, installation, inspection, and maintenance of automatic fire sprinkler systems and related fire suppression components installed in commercial, industrial, residential, and institutional buildings.

Fire sprinkler systems deliver controlled water or suppression agent discharge in response to heat detection, providing automatic life safety protection compliant with NFPA 13, NFPA 13R, NFPA 13D, and applicable International Building Code requirements. Applications span office buildings, retail centers, warehouses, manufacturing facilities, data centers, healthcare institutions, hotels, multifamily residential, single-family homes, tunnels, and aviation facilities.

Macroeconomic enablers include the US record construction spending of USD 2.2 Trillion in 2024, approximately 1.48 million new residential units permitted in 2024, and universal NFPA 13 code adoption creating non-discretionary procurement demand across all new and substantially renovated buildings above threshold occupancy classifications.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

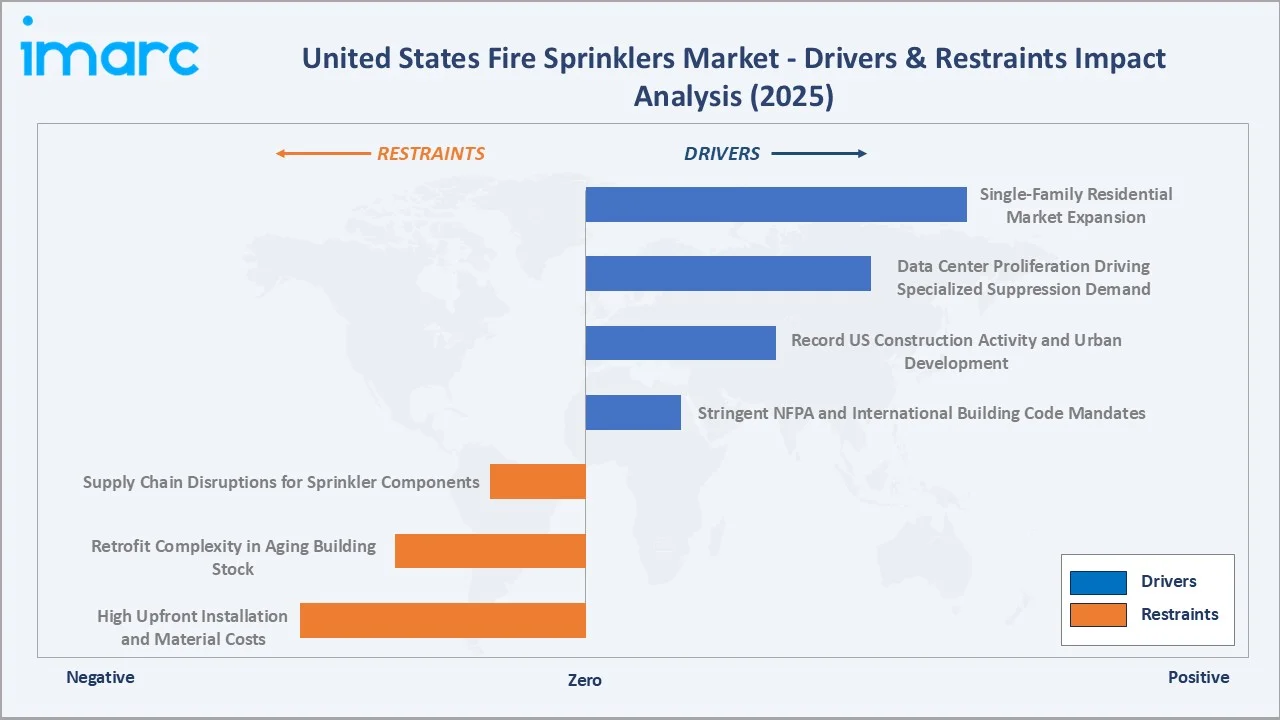

- Stringent NFPA and International Building Code Mandates: NFPA 13 is adopted by reference in the IBC, which all 50 US states have adopted as the basis for their state building codes as of 2025. This creates universal mandate coverage: every new commercial, institutional, and multifamily residential building over threshold occupancy load in the US must be equipped with an automatic fire sprinkler system before receiving a certificate of occupancy.

- Record US Construction Activity and Urban Development: US total construction spending reached a record USD 2.2 Trillion in 2024, with approximately 1.48 million housing units permitted in 2024. Each commercial project above occupancy thresholds mandates fire sprinkler installation, directly converting construction spend growth into fire sprinkler market growth at a predictable rate tied to construction value.

- Data Center Proliferation Driving Specialized Suppression Demand: Data centers require specialized fire suppression systems, clean agent systems for IT room protection alongside wet pipe systems for support areas, generating higher per-square-foot fire suppression system values versus standard commercial builds.

Market Restraints

- High Upfront Installation and Material Costs: Fire sprinkler system installation costs range from USD 1-10 per square foot for new construction, depending on system type and occupancy.

- Retrofit Complexity in Aging Building Stock: The US has approximately 5.9 million commercial buildings, the majority constructed before universal sprinkler code adoption. Retrofitting existing buildings with fire sprinklers requires significant structural disruption, ceiling demolition, pipe installation, wall penetrations, and water supply system upgrades, that can cost 3-5x per square foot versus new construction installation.

Market Opportunities

- Single-Family Residential Market Expansion: While California mandates residential sprinklers statewide, only some other US states had equivalent mandates as of 2025.

- CHIPS Act-Funded Semiconductor and Advanced Manufacturing Facilities: The CHIPS and Science Act authorized USD 53 Billion for semiconductor manufacturing in the US, with major facilities under construction or planning. These hyperscale manufacturing facilities require state-of-the-art fire suppression systems for clean rooms, chemical storage, and production equipment, generating an average fire protection system.

- Decarbonized and Sustainable Fire Suppression Agents: Environmental regulatory pressure on fluorinated suppression agents, with the EPA's SNAP Rule 21 restricting many HFC-based agents and the Kigali Amendment to the Montreal Protocol phasing down HFCs, is creating a transition opportunity for next-generation suppression agents.

Market Challenges

- NICET-Certified Technician Shortage: The fire protection industry faces shortage of NICET-certified fire protection technicians and licensed fire protection engineers (FPEs).

- Supply Chain Disruptions for Sprinkler Components: The COVID-19 pandemic exposed concentrated supply chain vulnerabilities in sprinkler head production, with Tyco/Johnson Controls, Viking Group, and Central Fire Sprinkler all experiencing lead times extending from 4-6 weeks to 6-12 months during 2021-2022.

Emerging Market Trends

1. IoT-Connected Sprinkler Systems Enabling Predictive Fire Safety

IoT-integrated fire suppression systems that continuously monitor sprinkler head condition, valve positions, pipe pressures, and water supply adequacy in real-time are transitioning from premium to standard specification in Class A commercial buildings. Johnson Controls' Metasys platform integrate fire suppression monitoring with building HVAC, access control, and energy management data into unified dashboards.

2. Pre-Action and Gaseous Suppression Systems Growing in Data Centers

Data center proliferation is driving rapid growth in pre-action sprinkler systems and clean agent gaseous suppression systems that minimize water damage risk to high-value IT equipment. Pre-action systems require both a heat signal and a smoke detection signal before releasing water, providing a safety interlock absent in standard wet pipe systems.

3. Residential Sprinkler Adoption Expanding Beyond California

The NFPA's advocacy and NFSA's state-level lobbying are progressively expanding residential sprinkler mandates beyond California's pioneering statewide requirement. The residential segment represents the market's largest untapped expansion opportunity with an estimated 1.4 million housing units started in 2025.

4. CHIPS Act Semiconductor Manufacturing Creating Premium Fire Protection Demand

The US CHIPS and Science Act's USD 53 Billion authorization and the subsequent committed private investments in semiconductor manufacturing facilities are creating a distinct high-value niche within the US fire suppression market.

5. Sustainability and PFAS-Free Suppression Agent Transition

Environmental regulatory pressure is fundamentally restructuring the fire suppression agent market. PFAS-free alternatives, including Chemours' Opteon 1234ze, Amerex's F3 foam concentrates, and ANSUL's INERGEN inert gas system, are gaining commercial specification approvals.

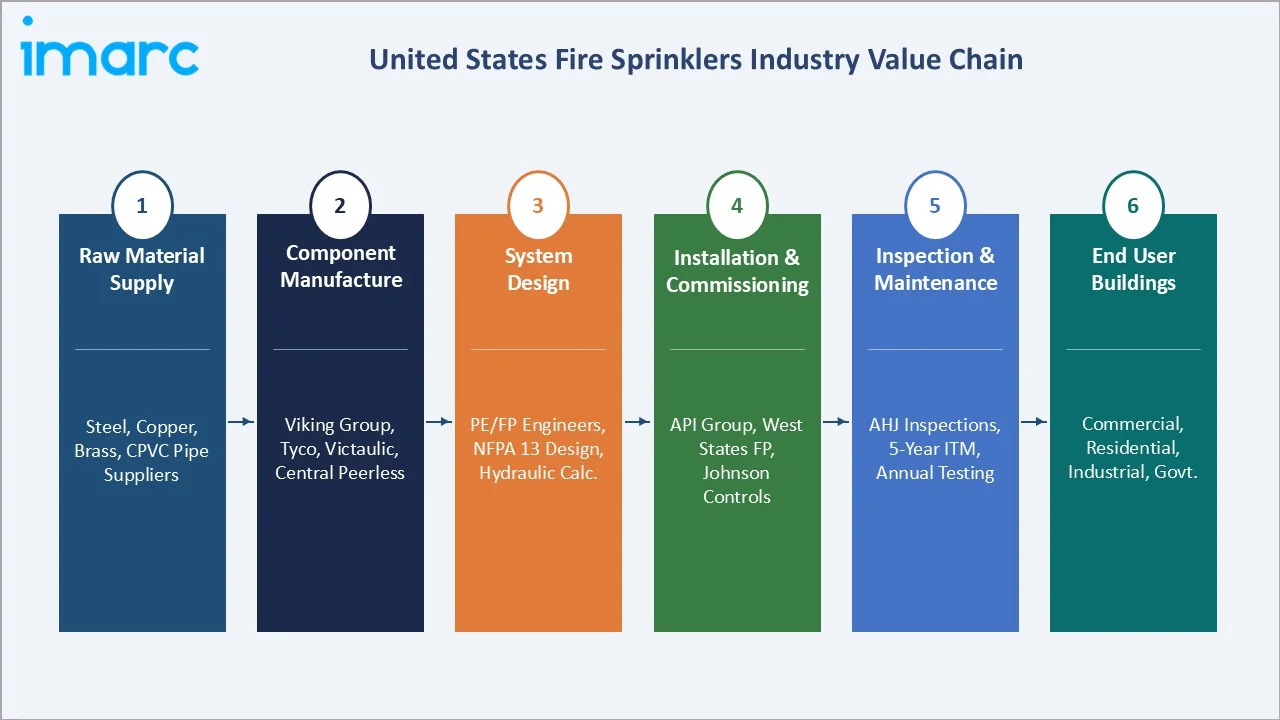

Industry Value Chain Analysis

The US fire sprinklers value chain spans six stages from raw material supply through ongoing building owner maintenance obligations. The installation and commissioning stage captures the highest per-project revenue, while ITM maintenance services represent the highest recurring revenue stream with structurally predictable NFPA 25 compliance-driven demand.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

US Steel, Nucor Corporation (steel pipe), Mueller Industries (copper/brass), Lubrizol (CPVC BlazeMaster pipe) |

|

Component Manufacture |

Viking Group, Victaulic, Tyco (Johnson Controls), Central Fire Sprinkler, Senju Sprinkler |

|

System Design & Engineering |

Fire protection engineers (SFPE members), NICET-certified designers, Autodesk Fabrication/AutoSPRINK CAD tools |

|

Installation & Commissioning |

API Group Inc., Western States Fire Protection, American Fire Protection Group, American Fire Systems |

|

Inspection & Maintenance |

Johnson Controls, Siemens Building Technologies, Hochiki, API Group, regional ITM contractors (NFSA members) |

|

End User Buildings |

Commercial (office, retail, hospitality), Industrial (manufacturing, warehouses), Residential, Healthcare, Government |

Fire protection engineering firms and licensed installation contractors capture the highest value-added margin positions in the fire sprinkler supply chain. The ITM maintenance obligation creates the most durable recurring revenue for inspection, testing, and maintenance services regardless of economic conditions, given NFPA 25 mandatory compliance requirements.

Technology Landscape in the US Fire Sprinklers Industry

Wet Pipe, Dry Pipe, and Pre-Action System Technology

Wet pipe sprinkler systems, maintaining water continuously under pressure in distribution piping, remain the dominant system type at approximately 70% of all US installations, valued for their simplicity, reliability, and low maintenance cost. Dry pipe systems, which maintain pressurized air or nitrogen in piping with water held back by a dry pipe valve, are the standard for unheated spaces where freezing risk makes wet pipe systems unsuitable.

Sprinkler Head Innovation and Coverage Technology

Modern sprinkler head technology has advanced significantly from the traditional pendant and upright configurations. Residential quick-response sprinklers with concealed cover plates, aesthetically appropriate for home installation, are critical enablers of residential code compliance. QREC (Quick Response Extended Coverage) technology approved under NFPA 13 is gaining specification in office renovation projects.

IoT and Building Management System Integration

The integration of fire suppression monitoring into building automation and IoT platforms represents the most transformative technology shift in fire protection since the transition from pneumatic to electronic detection. IoT-enabled supervisory control systems continuously monitor water pressure, valve positions, tamper switches, and flow indicators across entire building portfolios, transmitting alerts to central monitoring stations and mobile applications in real-time.

Fire Suppression Agent and Clean Agent Technology

The clean agent suppression market is undergoing a fundamental technology transition driven by PFAS regulatory pressure. PFAS-free aqueous film-forming foam (AFFF) alternatives are under active development and testing for aircraft hangars and industrial applications where AFFF has been the traditional suppression agent.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Component |

Fire Sprinklers Structures |

42.3% |

2025 |

|

Fire Sprinkler System |

Wet Sprinkler System |

54.8% |

2025 |

|

Service |

Installation/Design |

43.6% |

2025 |

|

Application |

Commercial |

51.4% |

2025 |

|

Region |

West |

31.2% |

2025 |

By Component

Fire sprinkler structures command the largest component share at 42.3% in 2025, encompassing sprinkler heads, schedule 40 and schedule 10 steel pipe, CPVC pipe, grooved fittings, hangers, and support assemblies, collectively the highest-volume physical material investment in every fire sprinkler installation project. Between 2017 and 2021, local fire departments responded to an average of 52,948 structure fires annually, which accounted for 11% of all structure fires where sprinklers were installed. In the home fires where sprinkler systems were present and the fire size triggered them, 95% of the sprinklers operated effectively.

To access detailed market analysis, Request Sample

Fire response systems at 22.6% (2025) encompass alarm valves, check valves, flow switches, pressure gauges, and supervisory devices that activate and monitor system status. Fire detectors and control panels (19.4%) include addressable fire alarm control panels (FACPs), smoke and heat detectors, pull stations, and notification appliances that initiate building evacuation and emergency response. Fire suppression reagent (15.7%) encompasses specialized suppression agents for pre-action, clean agent, foam, and gaseous suppression systems where standard water is supplemented or replaced.

By Service

Installation/design commands the largest service share at 43.6% in 2025, reflecting the labor and professional services intensity of NFPA 13-compliant system delivery. Fire sprinkler installation requires licensed contractors in most US jurisdictions, NICET-certified field technicians for installation, and fire protection engineers (FPEs) for hydraulic calculation-based system design.

Maintenance at 28.9% (2025) is the market's most structurally stable revenue stream. Quarterly, annual, 3-year, and 5-year ITM cycles create a non-cyclical, contract-based revenue stream that grows with the installed base. Engineering & fabrication (18.7%) encompasses prefabricated pipe spool fabrication, BIM-coordinated shop drawing development, and specialty system engineering for data centers, hazardous occupancies, and cleanroom applications, a premium-priced service tier. Others (8.8%) include inspection software licensing, training services, and specialty consulting.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

West |

31.2% |

California statewide residential mandate; Pacific coast construction boom; data center growth |

|

South |

27.6% |

Sunbelt construction surge; Texas/Florida/Georgia data centers; semiconductor fabs |

|

Midwest |

23.4% |

Industrial warehouse expansion; logistics facility growth; Chicago metro commercial construction |

|

Northeast |

17.8% |

High-density urban retrofits; NYC Local Law 126 inspection mandates; Boston/DC healthcare construction |

The West region commands a 31.2% market share in 2025, the largest of the four US census regions. California is the West's dominant fire protection market. In 2024, the U.S. had 941,000 construction establishments, including 93,600 in California, generating proportionally large fire sprinkler installation volumes.

The South region, with 27.6% in 2025, is the fastest-growing region, driven by the Sunbelt's disproportionate share of US population growth, housing starts, and commercial investment. Texas, the South's largest construction market, is simultaneously receiving semiconductor manufacturing investments, multiple data center mega-campus developments, and the nation's highest annual housing unit addition rate.

The Midwest (23.4%) benefits from the largest US logistics and e-commerce distribution center construction wave in history. The Northeast (17.8%) is characterized by higher-value retrofit activity in dense urban markets, driven by New York City's Local Law 126 inspection mandate and extensive hospital and university construction investment.

Competitive Landscape

The US fire sprinklers market is moderately fragmented, with large integrated fire safety conglomerates competing alongside regional fire protection contractors and specialized installation firms. The competitive landscape bifurcates between national full-service providers with engineering, installation, and ITM capabilities and regional specialists serving specific geographies or occupancy types.

|

Company Name |

Key Brand / Products |

Market Position |

US Strategic Focus |

|

Johnson Controls International |

Tyco Standard spray, Sprinklers for Residential, Sprinkler Accessories |

Leader |

Full-service fire protection; BMS integration; national ITM |

|

API Group Inc. |

Texas Sprinkler, United States Fire Protection Sprinklers |

Leader |

Installation contractor; ESFR & commercial |

|

Siemens AG |

Sinorix (Fire Sprinkler Services) |

Leader |

Addressable detection; smart systems |

|

Western States Fire Protection Co. |

Wet Pipe Systems Dry Pipe Systems Deluge Systems Pre-Action Systems |

Leader |

Western US contractor; residential & commercial; multi-state |

|

American Fire Protection Group, Inc. |

Wet Pipe Systems Dry Pipe Systems Deluge Systems In-Rack Systems Pre-Action Systems Quell Systems ESFR |

Challenger |

National franchise network; commercial & industrial |

|

Minimax GmbH & Co. KG |

Classic sprinkler systems, Undercover Sprinkler, Preaction Sprinkler |

Challenger |

Industrial fire suppression; chemical & foam suppression |

|

American Fire Systems, Inc. |

Sprinklers for Data Centers to Residential |

Emerging |

Regional commercial installation; Mid-Atlantic US focus |

The competitive positioning of key US fire sprinklers market participants in 2025 illustrates the market presence and strategic investment dimensions that separate national integrated providers from regional specialists.

Key Company Profiles

Johnson Controls International

Johnson Controls is a global leader in smart, healthy, and sustainable buildings, with fire and security as a core business segment.

- Product Portfolio: Tyco Standard Spray, Tyco Extended Coverage and Storage Systems, Residential Sprinklers, Sprinkler Accessories, Foam Sprinkler Equipment.

- Recent Developments: In June 2025, Johnson Controls reintroduced its Connected Sprinkler service, offering real-time insights and predictive maintenance to help facility managers and building owners save time and reduce costs. The service leverages digital technology to improve fire safety across the building's lifecycle by delivering data-driven maintenance information.

- Strategic Focus: Johnson Controls' fire protection strategy focuses on integrated smart building solutions where fire suppression monitoring is one component of a unified building safety and efficiency platform, leveraging cloud platforms to deepen customer relationships and expand recurring monitoring and maintenance revenue.

API Group Inc.

API Group Inc. is one of the largest fire protection and life safety companies in North America, operating through its Safety Services segment.

- Product Portfolio: Texas Sprinkler, United States Fire Protection Inc.

- Recent Developments: In December 2025, APi Group announced to acquire an Indianapolis-based provider of fire-safety services.

- Strategic Focus: API Group's strategy is to build the dominant national fire protection services platform through acquisitive consolidation of regional fire protection contractors, then leverage scale to win national account contracts with major companies and government agencies, while driving organic growth through cross-selling inspection and monitoring services to the acquired contractors' installation customer bases.

Western States Fire Protection Co.

Western States Fire Protection (WSFP) is one of the largest regionally-focused fire protection contractors in the US, specializing in full-service commercial, industrial, and residential fire sprinkler system design, installation, inspection, testing, and maintenance, with California accounting for the majority of its annual revenue.

- Product Portfolio: Offers fire sprinkler services, including Wet Pipe Systems, Dry Pipe Systems, Deluge Systems, and Pre-Action Systems

- Recent Developments: Expanding its contractor network and increasing services for multi-state fire protection across both commercial and residential sectors.

- Strategic Focus: Western States Fire Protection's strategy leverages its deep relationships with California architects, engineers, and contractors developed over decades of California-specific code expertise, while opportunistically expanding its geographic footprint into Nevada, Arizona, and the Pacific Northwest to capture the Western US construction boom driven by semiconductor manufacturing, data center, and residential construction investment.

Siemens AG

Siemens AG, a multinational conglomerate, is known for its innovation in fire safety technology, offering modern solutions for automated and smart systems.

- Product Portfolio: Offers fire sprinkler services, under Sinorix

- Recent Developments: Focused on advanced technology integration into fire systems, smart detection systems, and real-time monitoring.

- Strategic Focus: Siemens is positioning itself as a leader in intelligent fire protection systems, leveraging smart technology to provide enhanced safety features and real-time response mechanisms.

Market Concentration Analysis

The US fire sprinklers market is moderately fragmented, with large integrated fire safety companies and national contractor platforms holding meaningful revenue shares alongside thousands of regional and local fire protection contractors serving specific metropolitan areas and occupancy niches.

The fragmentation reflects the geographic nature of fire protection installation: AHJ licensing requirements (most US jurisdictions require state-specific fire protection contractor licensing), the proximity-based bidding dynamics of construction projects, and the relationship-driven nature of ITM maintenance contract renewals.

Consolidation is accelerating through two mechanisms: (1) National platform building through M&A, led by API Group's aggressive acquisition strategy and Johnson Controls' targeted regional acquisition programme; and (2) Private equity roll-up strategies, with over 15 PE-backed fire protection consolidation platforms active in the US market as of 2025.

Investment & Growth Opportunities

Fastest-Growing Segments

IoT-enabled smart fire suppression systems are the highest-growth technology tier at ~10.2% CAGR through 2034. Residential sprinkler systems at ~8.4% CAGR represent the fastest-growing traditional segment, with each new state mandate adoption potentially adding annual addressable residential installation revenue.

Emerging Sub-Markets

The US semiconductor manufacturing renaissance is the most valuable emerging sub-market in fire suppression through 2028. Fire protection contractors with semiconductor cleanroom fire suppression expertise, NFPA 318 (Standard for the Protection of Semiconductor Fabrication Facilities) compliance capability, clean agent system design experience, and chemical storage suppression expertise, are positioned to capture disproportionate revenue from this high-value niche.

Investment & Private Equity Trends

EBITDA multiples for fire protection contractors have ranged 8-14x for businesses with strong ITM revenue mix - reflecting the recurring revenue quality, code-mandated demand predictability, and low technology disruption risk that makes fire protection one of the most attractive service industry investment verticals for private equity.

Future Market Outlook (2026-2034)

The US fire sprinklers market is forecast to nearly double from USD 5.87 Billion in 2025 to USD 10.81 Billion by 2034 at a CAGR of 6.82%, adding USD 4,945 Million in incremental annual market value. This growth represents one of the strongest sustained expansion trajectories in US building infrastructure services markets.

Three technology shifts will most significantly reshape the US fire sprinklers landscape through 2034. AI-powered fire prediction and suppression timing optimization, using building sensor data, occupancy patterns, and fire behavior modeling to minimize suppression water discharge while maximizing suppression effectiveness, is in active R&D at Underwriters Laboratories and Factory Mutual Research Corporation. Hybrid water mist and inert gas suppression, combining fine water mist's high efficiency with gaseous agent's low environmental impact, is emerging.

Research Methodology

Primary Research

Primary research encompassed over 45 structured interviews conducted in 2024-2025 with fire protection industry stakeholders including fire protection engineering firm principals, NICET-certified installation contractor operations managers, Johnson Controls and Siemens fire safety product managers, Authority Having Jurisdiction (AHJ) plan check officials in California, Texas, and New York, NFSA (National Fire Sprinkler Association) policy representatives, and private equity investors in fire protection consolidation platforms. Primary data validated market sizing, regional share estimates, component and service segment splits, and technology adoption timelines.

Secondary Research

Key secondary sources include NFPA Fire Protection Research Foundation annual reports, US Census Bureau construction spending data (2020-2024), NFSA Annual Industry Market Report, IBIS World Fire Protection Services Industry Report (US), Dodge Data & Analytics US construction starts database, Factory Mutual Global Research fire protection data, UL Certification database for fire suppression products, BLS Occupational Employment Statistics (fire protection workers), and trade publications including Sprinkler Age, Fire Protection Engineering, and NFSA's FireWatch.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, urbanization indices, consumer expenditure data, and historical market evolution patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for macroeconomic uncertainty.

United States Fire Sprinklers Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Components Covered |

|

| Fire Sprinkler Systems Covered | Wet Sprinkler System, Dry Sprinkler System, Pre-action Sprinkler System, Deluge System, Others |

| Services Covered | Installation/Design, Maintenance, Engineering and Fabrication, Others |

| Applications Covered |

|

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered | Johnson Controls International, API Group Inc., Siemens AG, Western States Fire Protection Co., American Fire Protection Group Inc., Minimax GmbH & Co. KG, American Fire Systems Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the United States fire sprinklers market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the United States fire sprinklers market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the United States fire sprinklers industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the United States Fire Sprinklers Market Report

The United States fire sprinklers market reached USD 5.87 Billion in 2025, reflecting consistent demand growth driven by building code mandates and record construction spending.

The market is projected to reach USD 10.81 Billion by 2034, growing at a CAGR of 6.82% during 2026-2034, driven by NFPA 13 code expansion, data center construction, semiconductor manufacturing, and residential mandate growth.

Fire Sprinkler Structures lead with a 42.3% component share in 2025, encompassing sprinkler heads, steel and CPVC piping, fittings, and hangers - the highest-volume material category in every installation project.

Installation/Design leads at 43.6% of service revenue in 2025, reflecting the engineering-intensive nature of NFPA 13-compliant system design and the significant labor investment in licensed contractor installation.

The West region leads with a 31.2% market share in 2025, driven by California's statewide residential sprinkler mandate, the Pacific coast construction boom, and major data center development in Nevada and Washington.

IoT-connected smart sprinkler systems are growing fastest at ~10.2% CAGR through 2034, followed by residential application at ~8.4% CAGR as residential mandate adoption expands beyond California to additional US states.

Leading companies include Johnson Controls International, API Group Inc., Siemens AG, Western States Fire Protection Co., American Fire Protection Group Inc., Minimax GmbH & Co. KG, and American Fire Systems Inc.

California mandates automatic fire sprinklers in all new one- and two-family dwellings statewide under the California Building Code, the only state with a universal residential mandate.

NFPA 13 is adopted by reference in the International Building Code across all 50 US states, creating universal mandatory sprinkler installation requirements for new commercial, industrial, and multifamily buildings above occupancy thresholds.

Data center construction generates specialized fire suppression demand at 35-45% higher per-square-foot system values versus standard commercial, driving the pre-action and clean agent segments.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)