United States High-Speed Blowers Market Size, Share, Trends and Forecast by Technology, End Use, and Region, 2026-2034

United States High-Speed Blowers Market Summary:

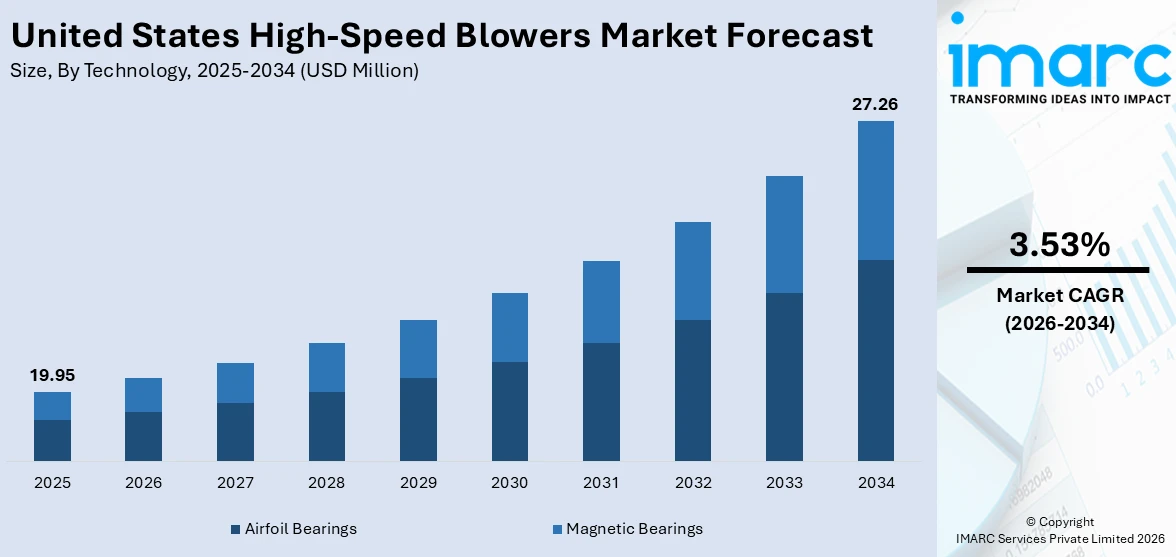

The United States high-speed blowers market size was valued at USD 19.95 Million in 2025 and is projected to reach USD 27.26 Million by 2034, growing at a compound annual growth rate of 3.53% from 2026-2034.

The United States high-speed blowers market is gaining momentum as industries prioritize energy-efficient, oil-free air delivery systems to reduce operational costs and meet tightening environmental standards. Growing infrastructure modernization across wastewater treatment facilities, rising adoption in chemical and petrochemical processing, and increasing integration of smart monitoring technologies are accelerating demand. Advancements in bearing technologies and compact design configurations are reinforcing the shift toward high-performance blower systems, positioning the market for sustained expansion across municipal and industrial applications and strengthening the United States high-speed blowers market share.

Key Takeaways and Insights:

- By Technology: Airfoil bearings dominate the market with a share of 54.2% in 2025, driven by their oil-free operation, minimal maintenance requirements, and proven reliability in contamination-sensitive industrial environments.

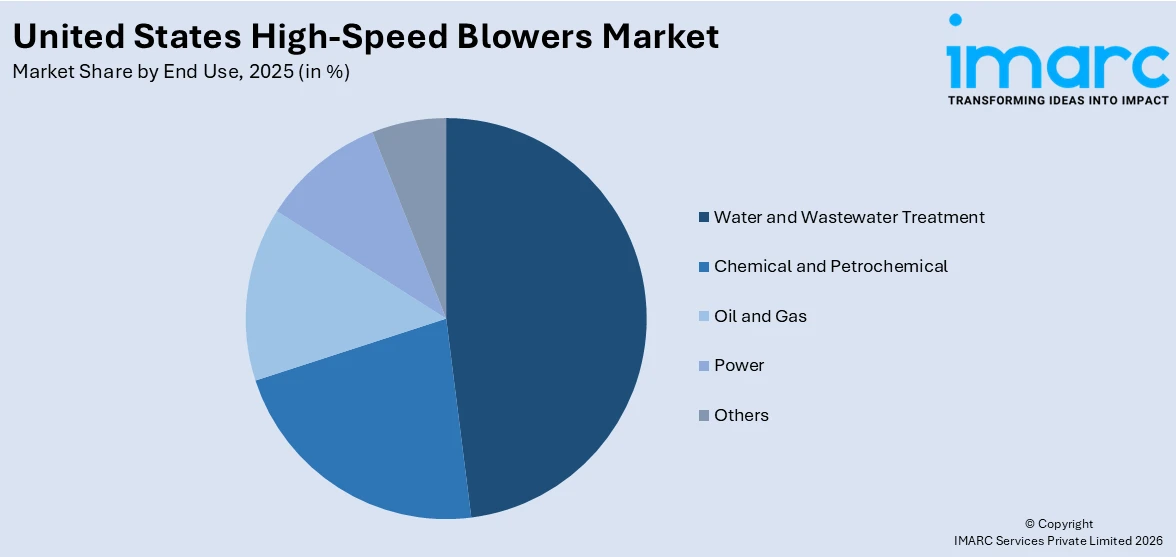

- By End Use: Water and wastewater treatment leads the market with a share of 47.9% in 2025, reflecting widespread adoption of high-speed blowers for energy-efficient aeration in biological treatment systems across municipal facilities.

- By Region: South represents the largest segment with a market share of 36.5% in 2025, supported by dense petrochemical corridors, expanding wastewater infrastructure, and robust industrial activity across key states.

- Key Players: The United States high-speed blowers market features a moderately consolidated competitive landscape, with established manufacturers leveraging advanced bearing technologies, expanding product portfolios, and investing in digital integration capabilities to strengthen market positioning across wastewater treatment, chemical processing, and power generation applications.

To get more information on this market Request Sample

The United States high-speed blowers market is experiencing rapid growth as industries focus on modernizing air delivery systems with energy-efficient, low-maintenance technologies. High-speed blowers equipped with airfoil or magnetic bearing systems provide oil-free airflow, which is essential for applications such as aeration, gas handling, and process air across municipal and industrial facilities. Municipal wastewater treatment remains the largest end-use segment, driven by ongoing upgrades to aging infrastructure and the need for precise airflow control in biological treatment processes. At the same time, expansion in petrochemical manufacturing, particularly along major industrial hubs, is increasing demand for reliable, contamination-free air delivery systems. The integration of IoT-enabled monitoring and predictive maintenance features is further transforming the market, enabling operators to optimize performance, reduce downtime, and improve energy efficiency. Collectively, these factors are fueling long-term growth, positioning high-speed blower systems as critical components in the modernization of industrial and municipal air handling infrastructure.

United States High-Speed Blowers Market Trends:

Integration of IoT-Enabled Smart Monitoring Systems

The United States high-speed blowers market is increasingly incorporating IoT-enabled monitoring and control capabilities, allowing real-time performance tracking, predictive maintenance, and remote diagnostics. These smart systems help operators optimize airflow, minimize unplanned downtime, and improve energy management across facilities. The adoption of digital integration in aeration and industrial blower systems is enhancing operational efficiency and reliability while meeting the growing industry demand for intelligent, automated solutions in critical infrastructure. This trend is driving broader market growth as high-speed blower technologies evolve to support smarter, data-driven operations.

Shift Toward Oil-Free and Sustainable Air Systems

There is a clear industry-wide shift toward oil-free blower systems in the United States, driven by the need for contamination-free operations and reduced environmental impact. High-speed blowers using airfoil or magnetic bearings eliminate the need for lubrication, cutting waste and lowering lifecycle costs. Energy efficiency regulations, such as California’s Title 20 standards, are encouraging the adoption of sustainable blower technologies. As a result, industries and municipal operators are increasingly transitioning from conventional multi-stage blowers to high-speed turbo systems, benefiting from improved efficiency, lower maintenance, and environmentally responsible operation across diverse applications.

Advancement of High-Capacity Turbo Blower Platforms

Manufacturers are increasingly enhancing the capacity and efficiency of turbo blower systems to meet the needs of larger municipal and industrial facilities. High-capacity single-motor designs allow treatment plants and industrial operators to replace multiple smaller units with fewer, more efficient blowers, improving reliability and reducing maintenance requirements. These advancements support broader adoption of consolidated blower systems for wastewater aeration and critical industrial air applications, demonstrating how technological improvements are enabling higher performance, operational flexibility, and energy efficiency across large-scale facilities.

Market Outlook 2026-2034:

The United States high-speed blowers market is set for steady growth, driven by ongoing modernization of wastewater infrastructure, stricter energy efficiency requirements, and rising industrial demand for reliable oil-free air delivery systems. Government initiatives supporting water infrastructure improvements are creating sustained opportunities for advanced aeration blower deployments across municipal treatment facilities. As utilities and industrial operators prioritize energy-efficient, high-performance blower solutions, the market is experiencing increased adoption of innovative technologies that enhance operational reliability, reduce energy consumption, and meet evolving environmental and regulatory standards. The market generated a revenue of USD 19.95 Million in 2025 and is projected to reach a revenue of USD 27.26 Million by 2034, growing at a compound annual growth rate of 3.53% from 2026-2034.

United States High-Speed Blowers Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Technology |

Airfoil Bearings |

54.2% |

|

End Use |

Water and Wastewater Treatment |

47.9% |

|

Region |

South |

36.5% |

Technology Insights:

- Airfoil Bearings

- Magnetic Bearings

Airfoil bearings dominate with a market share of 54.2% of the total United States high-speed blowers market in 2025.

Airfoil bearings have established themselves as the preferred bearing technology in the United States high-speed blowers market, owing to their oil-free, non-contact operation that eliminates lubrication requirements and substantially reduces maintenance costs. These bearings leverage aerospace-derived gas foil technology, where a thin, compliant foil structure supports the rotating shaft on a cushion of air during operation. This design delivers exceptional reliability and longevity, making airfoil bearing blowers ideal for contamination-sensitive applications such as pharmaceutical manufacturing, semiconductor fabrication, and municipal wastewater aeration.

The technology’s leading position is strengthened by its widespread use in aeration systems, where continuous, reliable operation is critical. APG-Neuros has developed a product portfolio based on patented third-generation bump foil air bearings, originally created for military aviation applications, and has deployed blower systems across numerous industrial and municipal wastewater treatment facilities. The exceptional durability of these airfoil bearing systems, coupled with significant energy efficiency advantages over conventional blowers, continues to reinforce their dominance in the market and drives ongoing adoption among operators seeking reliable, high-performance aeration solutions.

End Use Insights:

Access the comprehensive market breakdown Request Sample

- Water and Wastewater Treatment

- Chemical and Petrochemical

- Oil and Gas

- Power

- Others

Water and wastewater treatment leads with a share of 47.9% of the total United States high-speed blowers market in 2025.

Water and wastewater treatment represents the largest end-use segment in the United States high-speed blowers market, as these systems are essential for delivering efficient, oil-free air to aeration processes in biological treatment systems. Approximately 17,500 publicly owned treatment works operate across the country, many of which require modernization to meet evolving regulatory requirements and capacity demands. High-speed blowers provide the precise airflow needed to support microbial activity in secondary treatment, while their energy efficiency helps facilities manage rising operational costs.

Federal investment is creating significant opportunities for blower system upgrades. The EPA's 2024 wastewater infrastructure needs assessment estimated USD 630 billion in national requirements over twenty years, representing a 45 percent increase from the previous assessment. Major treatment facility expansion projects are underway, including the City of Austin's Walnut Creek Wastewater Treatment Plant expansion, illustrating the scale of infrastructure investments that are driving demand for advanced aeration equipment.

Regional Insights:

- Northeast

- Midwest

- South

- West

South represents the largest share at 36.5% of the total United States high-speed blowers market in 2025.

The South region commands the largest share of the United States high-speed blowers market, driven by the concentration of petrochemical processing facilities, oil and gas operations, and expanding municipal wastewater treatment infrastructure across states such as Texas, Louisiana, and Florida. The Gulf Coast corridor houses a substantial portion of the nation's refining and chemical manufacturing capacity, generating consistent demand for high-purity, pressurized air in process applications including gas compression, drying, and vapor recovery.

The region's industrial expansion continues to strengthen blower demand. As of February 2024, researchers identified 114 oil and gas-related projects proposed at 89 locations in Texas alone, including refineries and petrochemical facilities that require advanced wastewater treatment and air handling systems. Additionally, major treatment plant upgrades such as the Whites Creek Wastewater Treatment Plant project in Nashville, Tennessee, reflect the broader trend of infrastructure modernization that is sustaining high-speed blower adoption across the Southern United States.

Market Dynamics:

Growth Drivers:

Why is the United States High-Speed Blowers Market Growing?

Accelerating Wastewater Infrastructure Modernization

The United States is undergoing a significant wave of wastewater infrastructure modernization driven by aging treatment facilities, growing population demands, and increasingly stringent environmental regulations. High-speed blowers are integral to these upgrade programs, as they provide the efficient, oil-free aeration required for modern biological treatment processes. The Bipartisan Infrastructure Law delivered more than USD 50 billion to the EPA for water infrastructure improvements, representing the largest federal water investment in history. In fiscal year 2024, EPA announced USD 11.5 billion in combined State Revolving Fund allocations, enabling communities nationwide to pursue critical treatment plant upgrades. This unprecedented federal commitment is generating sustained demand for advanced aeration technologies, including high-speed turbo blowers that offer superior energy efficiency and reduced lifecycle costs compared to conventional multistage systems.

Rising Industrial Demand for Energy-Efficient Air Systems

Energy efficiency has become a key factor for industrial operators when selecting air delivery systems, as rising operational costs and corporate sustainability goals encourage a shift from conventional blowers to high-speed alternatives. Regulatory frameworks, such as California’s Title 20 standards for commercial and industrial fans and blowers, are setting benchmarks that guide energy-efficient equipment selection across the US market. These policies, combined with growing awareness of operational cost savings and environmental impact, are driving companies to adopt high-speed blower systems that offer improved energy performance, lower electricity consumption, and enhanced operational efficiency for large-scale industrial applications.

Expansion of Petrochemical and Chemical Processing Activities

The expanding US petrochemical and chemical processing industry is driving strong demand for high-speed blower systems that provide high-purity, pressurized air for critical operations such as gas compression, drying, vapor recovery, and other process applications. Industrial hubs along the Gulf Coast are seeing rapid growth in refining and chemical production capacity, increasing the need for reliable, contamination-free air delivery solutions. Large-scale industrial and municipal developments, including wastewater treatment and process air systems, are directly supporting the adoption of high-speed blower technologies, as operators prioritize efficiency, performance, and operational reliability across complex process environments.

Market Restraints:

What Challenges the United States High-Speed Blowers Market is Facing?

High Initial Capital Investment Requirements

Initial purchase and installation of high-speed blower systems are found to be enormously higher than the traditional positive displacement and multistage centrifugal blowers. Although the higher capital cost is usually compensated by long-term savings in operation by saving energy and reduced maintenance costs, the higher capital cost of the system means that it cannot be readily adopted by smaller municipalities and industrial operators with tight budgets, especially where federal financing programs are inaccessible.

Technical Complexity and Skilled Workforce Limitations

The blower systems with high speed include new technologies such as accuracy bearings, variable frequency, and in-built digital control platforms, which demand expertise in installing, commissioning, and maintenance. Any shortage of technically trained personnel in some areas limits the rate of adoption because the facility needs to ensure that it has sufficient in-house skills or service agreements to sustain the performance and reliability of the system.

Competition from Established Conventional Blower Technologies

Conventional blower technologies, including positive displacement and multistage centrifugal blowers, continue to hold a significant installed base across the United States wastewater and industrial facilities. Operators familiar with these established systems may resist transitioning to high-speed alternatives due to perceived risks associated with newer technologies, concerns about integration with existing infrastructure, and the availability of mature service and support networks for legacy equipment.

Competitive Landscape:

The United States high-speed blowers market exhibits a moderately concentrated competitive structure, with both multinational industrial equipment manufacturers and specialized blower technology providers vying for market share across municipal and industrial applications. Leading participants compete based on bearing technology innovation, energy efficiency performance, product capacity range, and digital integration capabilities. Strategic emphasis on expanding product portfolios to address higher-capacity requirements, integrating IoT-enabled monitoring and predictive maintenance features, and securing positions in federally funded wastewater infrastructure projects defines the current competitive dynamics. Partnerships with engineering firms and distribution networks further strengthen market positioning as companies seek to capitalize on the long-term growth trajectory driven by infrastructure modernization and industrial expansion.

Recent Developments:

- In June 2024, Fuji Electric Corp. of America announced the launch of its new EXV1000-7W 10 HP Explosion-Proof Blower, specifically designed for hazardous environments. The product addresses the growing need for reliable air delivery systems in chemical processing and oil and gas applications, where explosive atmosphere conditions require specialized equipment certifications.

- In October 2024, APG-Neuros announced that its APGN1500 turbo blower, designated as the 1MW model, achieved UL listing compliant with both United States and Canadian standards. The 1MW unit is recognized as the largest single-motor turbo blower of its kind, offering a smaller footprint, higher wire-to-air efficiency, and flexible variable speed control for large-scale wastewater aeration applications.

United States High-Speed Blowers Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Technologies Covered |

Airfoil Bearings, Magnetic Bearings |

|

End Uses Covered |

Water and Wastewater Treatment, Chemical and Petrochemical, Oil and Gas, Power, Others |

|

Regions Covered |

Northeast, Midwest, South, West |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the United States High-Speed Blowers Market Report

The United States high-speed blowers market size was valued at USD 19.95 Million in 2025.

The United States high-speed blowers market is expected to grow at a compound annual growth rate of 3.53% from 2026-2034 to reach USD 27.26 Million by 2034.

Airfoil bearings, representing the largest revenue share of 54.2% in 2025, dominate the United States high-speed blowers market due to their oil-free operation, minimal maintenance needs, and proven reliability in contamination-sensitive environments, making them indispensable for wastewater treatment and advanced manufacturing applications.

Key factors driving the United States high-speed blowers market include accelerating wastewater infrastructure modernization supported by federal investment, rising industrial demand for energy-efficient air delivery systems, expansion of petrochemical and chemical processing activities, and growing adoption of smart monitoring technologies.

Major challenges include high initial capital investment requirements, technical complexity requiring specialized maintenance expertise, competition from established conventional blower technologies, space constraints in existing facilities, and limited awareness among smaller operators about long-term cost benefits.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)