United States Hot Sauce Market Size, Share, Trends and Forecast by Product Type, Application, End Use, Packaging, Distribution Channel, and Region, 2026-2034

United States Hot Sauce Market Size, Share, Trends & Forecast (2026-2034)

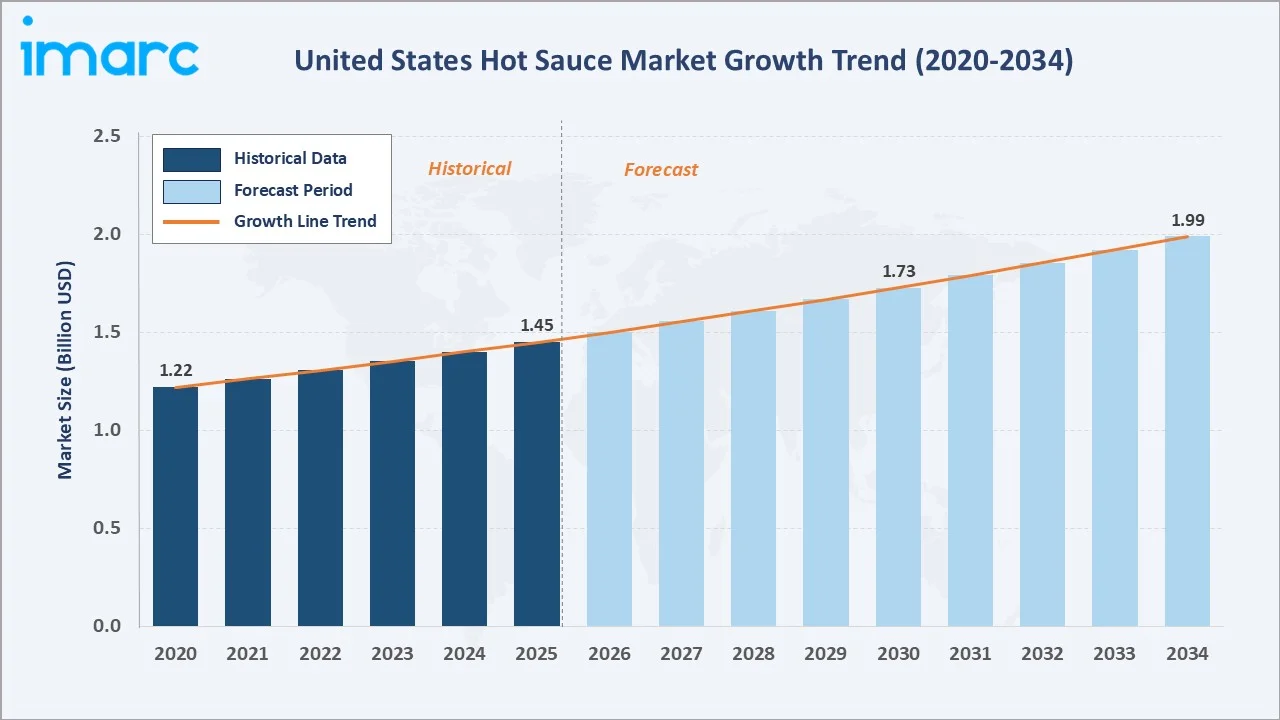

The United States hot sauce market was valued at USD 1.45 Billion in 2025 and is projected to reach USD 1.99 Billion by 2034, exhibiting a CAGR of 3.58% during 2026-2034. The market is primarily driven by evolving consumer taste preferences toward bold, spicy flavors, the growing multicultural population, and rising integration of hot sauce across household cooking and food service applications.

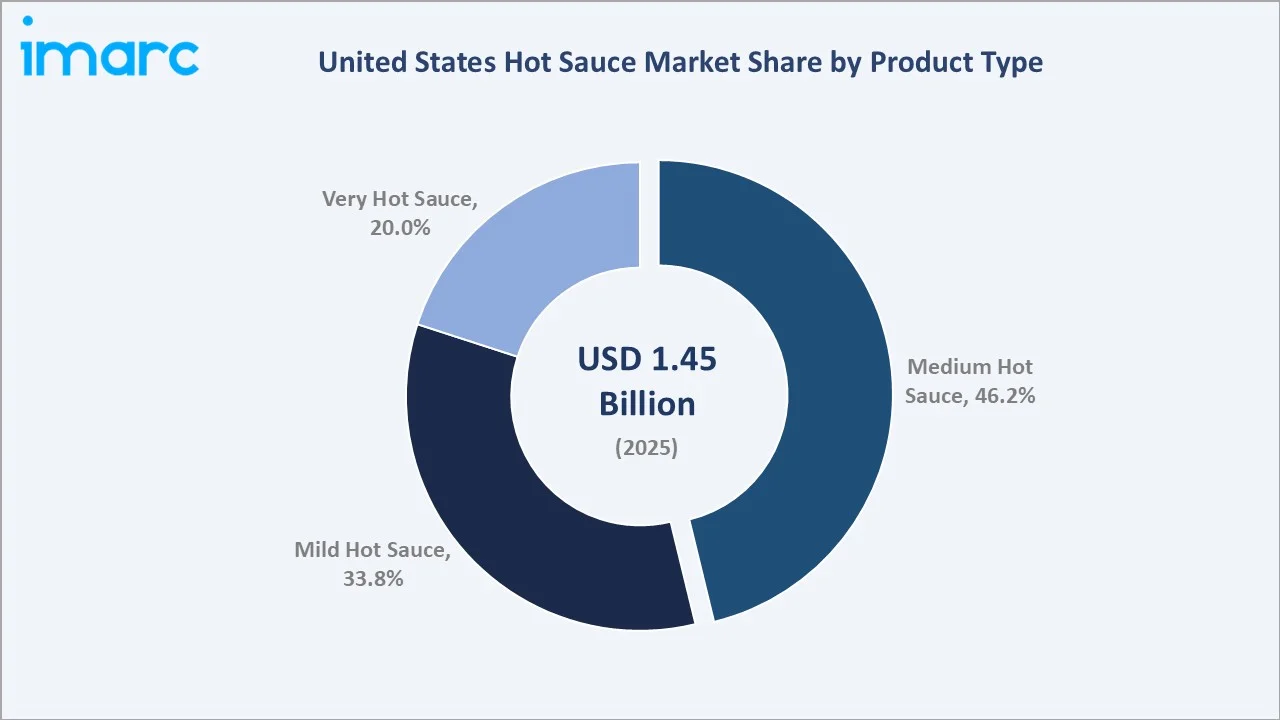

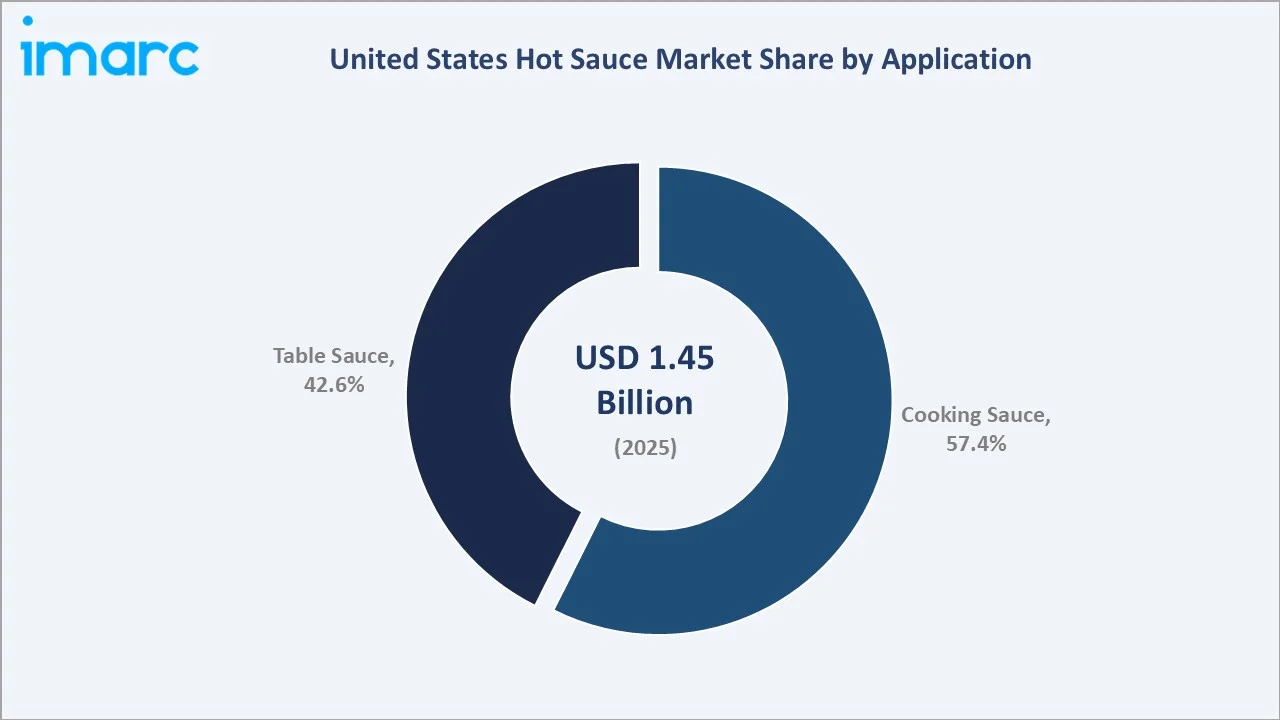

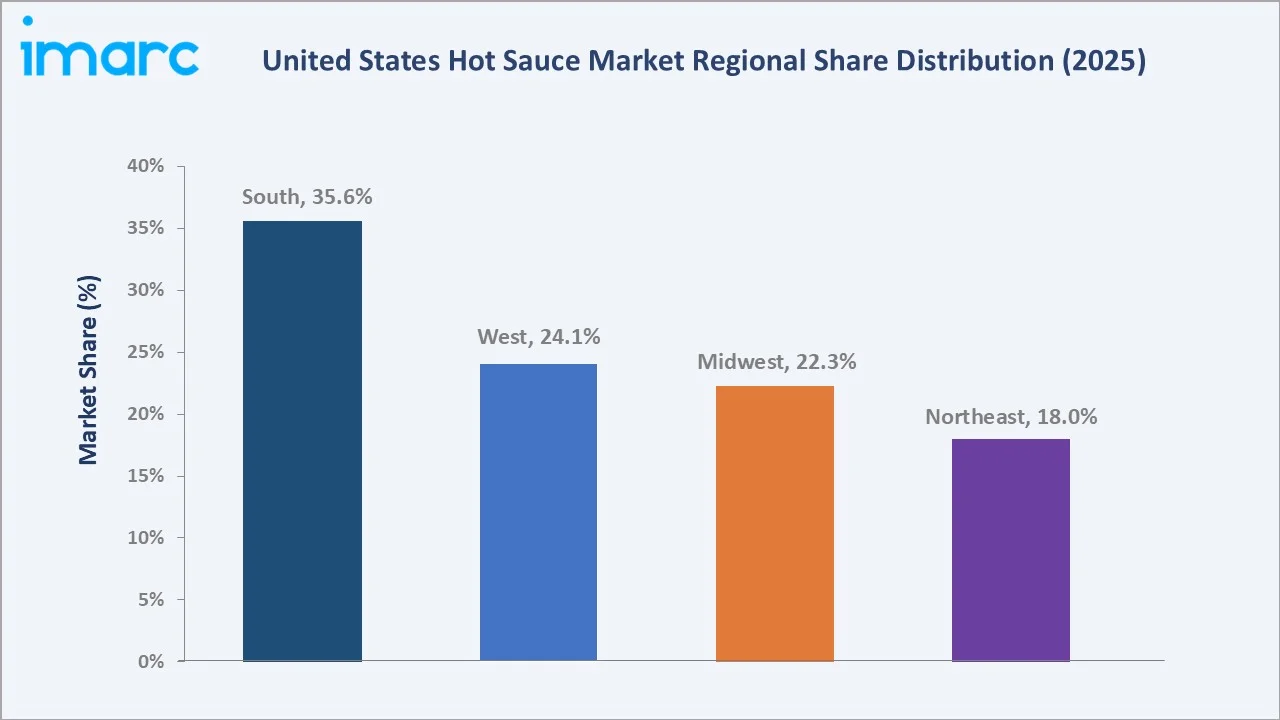

Medium hot sauce leads the product type segment at 46.2%, cooking sauce dominates the application segment at 57.4%, and South commands the largest regional share at 35.6% in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.45 Billion |

|

Forecast Market Size (2034) |

USD 1.99 Billion |

|

CAGR (2026-2034) |

3.58% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

South (35.6%, 2025) |

|

Second Largest Region |

West (24.1%, 2025) |

|

Leading Product Type |

Medium Hot Sauce (46.2%, 2025) |

|

Leading Application |

Cooking Sauce (57.4%, 2025) |

The United States hot sauce market expanded from USD 1.22 Billion in 2020 to USD 1.45 Billion in 2025, driven by rising consumer preferences for bold and spicy flavors and increasing product innovation across premium and specialty sauce categories. The market is projected to continue on this growth trajectory, reaching USD 1.73 Billion by 2030 and USD 1.99 Billion by 2034, underpinned by consistent demand expansion across both household and food service channels.

To get more information on this market, Request Sample

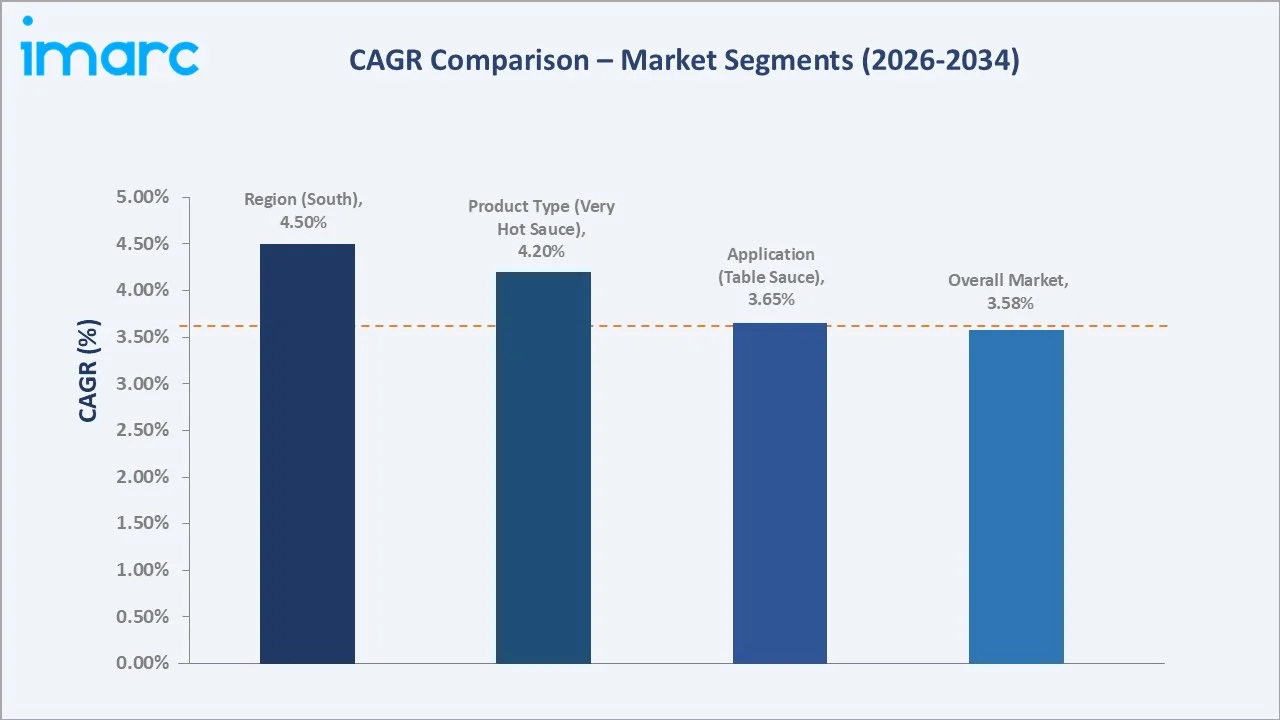

CAGR trajectories across product type and application sub-segments show very hot sauce and table sauce expanding at rates above the overall 3.58% market CAGR, driven by growing consumer enthusiasm for extreme heat products, artisan craft launches, and rising on-table condiment adoption across food service and casual dining environments.

Executive Summary

The United States hot sauce market is on a consistent growth trajectory, expanding from USD 1.22 Billion in 2020 to USD 1.99 Billion by 2034. The category has evolved from a regional condiment staple into a mainstream food product, driven by shifting demographics, multicultural cuisine adoption, and the proliferation of artisan and craft hot sauce brands across retail and e-commerce channels.

Medium hot sauce commands 46.2% product type share in 2025, supported by its broad consumer acceptance and versatility across cooking and table use occasions. Cooking sauce dominates the application segment at 57.4%, fueled by its widespread use as a flavoring ingredient in home cooking, foodservice preparation, marinades, and ready-to-eat (RTE) meal formulations. South holds the largest regional share at 35.6%, anchored by culturally embedded spicy food preferences and a dense base of regional hot sauce manufacturers.

Key Market Insights

|

Insight |

Data |

|

Largest Product Type |

Medium Hot Sauce - 46.2% share (2025) |

|

Second Largest Product Type |

Mild Hot Sauce - 33.8% share (2025) |

|

Leading Application |

Cooking Sauce - 57.4% share (2025) |

|

Second Largest Application |

Table Sauce - 42.6% share (2025) |

|

Leading Region |

South - 35.6% share (2025) |

|

Second Largest Region |

West - 24.1% share (2025) |

|

Top Companies |

McIlhenny Company, Huy Fong Foods, Inc., McCormick & Company, Inc., B&G Foods, Inc., TW Garner Food Company |

Key Analytical Observations Supporting the Above Data:

- Medium hot sauce leadership at 46.2% is supported by its broad consumer acceptance across varying heat preferences, versatility in both cooking and table use applications, and strong shelf presence across supermarkets, convenience stores, and food service channels.

- Mild hot sauce share at 33.8% is sustained by demand from family-oriented households, older consumers, and first-time users seeking enhanced flavor with lower heat intensity, supporting consistent consumption across mainstream retail markets.

- Cooking sauce dominance at 57.4% is fueled by widespread use in meal preparation, marinades, recipe enhancement, and foodservice applications, making hot sauce an increasingly important ingredient rather than solely a table condiment.

- Table sauce share at 42.6% is propelled by its widespread use as a condiment for RTE meals, snacks, sandwiches, and fast-food items, with consumers valuing the convenience of adding heat and flavor directly at the point of consumption.

- South at 35.6% is anchored by culturally embedded spicy food preferences, strong consumption across household and restaurant channels, and a concentrated presence of regional hot sauce producers that support product availability and innovation. Asper WalletHub's 2025 ‘Most & Least Diverse States in America’ study, Texas stood out as the second most diverse state in the United States. The report indicated that the state's demographic consisted of roughly 40% white, 40% Hispanic, around 12% Black, and about 5% Asian.

United States Hot Sauce Market Overview

Hot sauce refers to a liquid condiment made from chili peppers, vinegar, and spices, designed to add heat and flavor to food. The United States hot sauce market encompasses a broad range of products from mild pepper sauces and Louisiana-style blends to artisan craft hot sauces and extreme heat varieties. The market serves a diverse ecosystem of manufacturers, food service operators, retail chains, specialty condiment stores, and direct-to-consumer e-commerce platforms.

Macroeconomic drivers, including demographic diversity, rising disposable income, and the premiumization trend within the condiment category, are underpinning steady market expansion. The industry integrates chili pepper growers, spice processors, ingredient suppliers, bottling and packaging companies, hot sauce manufacturers, retail distributors, and food service operators. Growing influence of social media, food content creators, and chef-driven collaborations has further elevated brand awareness and consumer discovery within the hot sauce category.

Market Dynamics

To evaluate market opportunities, Request Sample

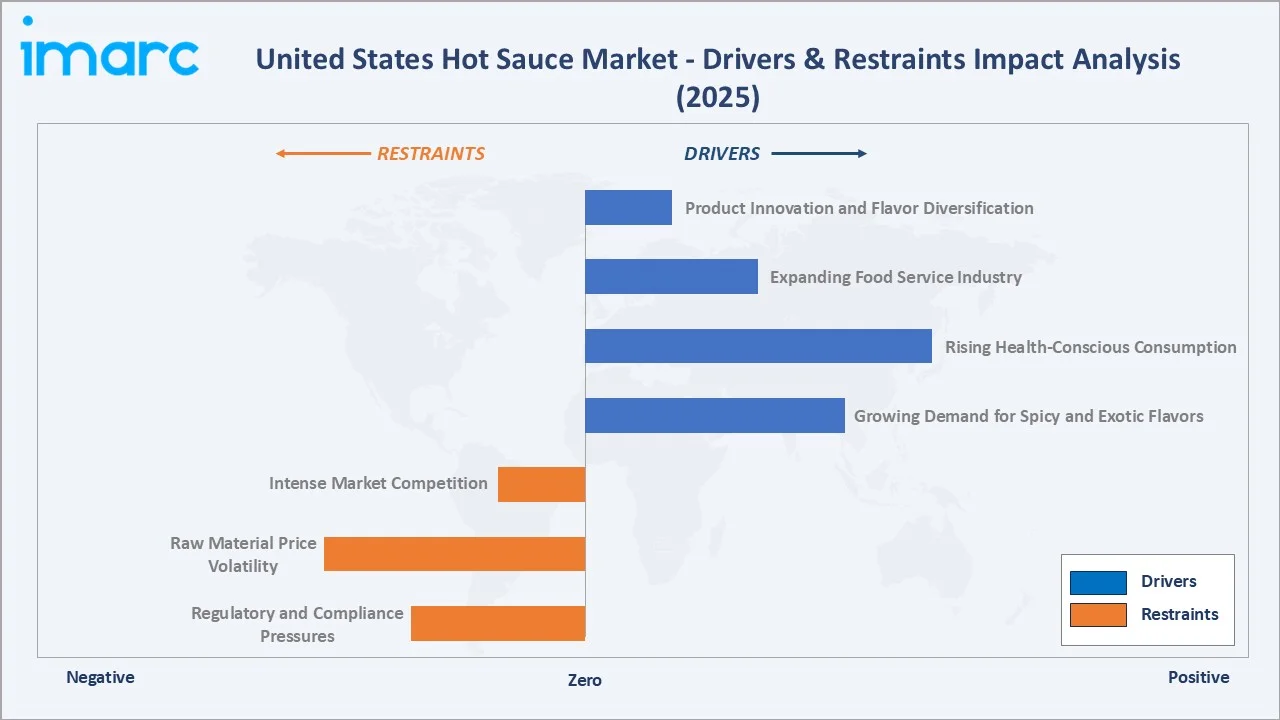

Market Drivers

- Growing Demand for Spicy and Exotic Flavors: Evolving consumer taste preferences toward bold, globally inspired flavors are significantly driving the United States hot sauce market. The growing multicultural population and increased exposure to international cuisines, such as Mexican, Thai, and Korean, have elevated demand for spicy condiments across household and food service segments.

- Rising Health-Conscious Consumption: The health and wellness trend has created a new consumer segment seeking hot sauce products perceived as natural, low-calorie, and additive-free. As per IMARC Group, the global health and wellness market reached USD 3,939.3 Billion in 2025. Capsaicin - the active compound in chili peppers - is associated with metabolism-boosting and anti-inflammatory properties, supporting demand among health-conscious consumers.

- Expanding Food Service Industry: The continued expansion of quick service restaurants, casual dining chains, and delivery platforms across the United States is creating sustained volume demand for hot sauce as a core condiment and cooking ingredient, supporting both private label and branded product growth in the food service channel.

- Product Innovation and Flavor Diversification: Manufacturers are actively launching new product formats, including fruit-infused sauces, fermented varieties, and globally inspired blends, to capture emerging consumer segments. Limited-edition collaborations and trending social media-driven flavors are further driving trial and repeat purchase.

Market Restraints

- Regulatory and Compliance Pressures: Hot sauce manufacturers in the United States operate under stringent FDA and USDA food safety regulations covering ingredient labeling, pH levels, and allergen disclosures. Compliance with evolving food safety standards increases operational costs and may constrain smaller artisan producers from scaling rapidly.

- Raw Material Price Volatility: Chili pepper prices are subject to weather-related supply shocks and agricultural disruptions, particularly in key growing regions such as New Mexico and California. Raw material price volatility directly impacts production cost structures and can compress margins for manufacturers dependent on specific chili varieties.

- Intense Market Competition: The United States hot sauce category is intensely competitive, with several active brands competing across mainstream retail, specialty food stores, and e-commerce. Price competition from private label products and the proliferation of new entrants can compress margins for established players.

Market Opportunities

- Premium and Artisan Segment Growth: The premiumization trend presents significant growth opportunities for artisan and craft hot sauce producers. Consumers are increasingly willing to pay premium prices for small-batch, single-origin, and organic certified hot sauces with unique chili varieties and clean-label ingredient profiles.

- E-Commerce and Direct-to-Consumer Expansion: The rapid growth of e-commerce and direct-to-consumer subscription models creates new distribution pathways for hot sauce brands. Online platforms enable smaller and emerging brands to reach national audiences without dependency on traditional retail placement, supporting long-tail market growth.

Market Challenges

- Managing Heat Level Expectations: Balancing heat levels to cater to mainstream consumers while satisfying the extreme heat enthusiast niche presents an ongoing formulation and branding challenge for manufacturers targeting broad shelf placement and diverse consumer demographics.

- Brand Differentiation in a Crowded Market: As the hot sauce category becomes more crowded, achieving and maintaining strong brand differentiation through packaging, flavor storytelling, and authentic brand origin narratives is increasingly challenging for both established and emerging players.

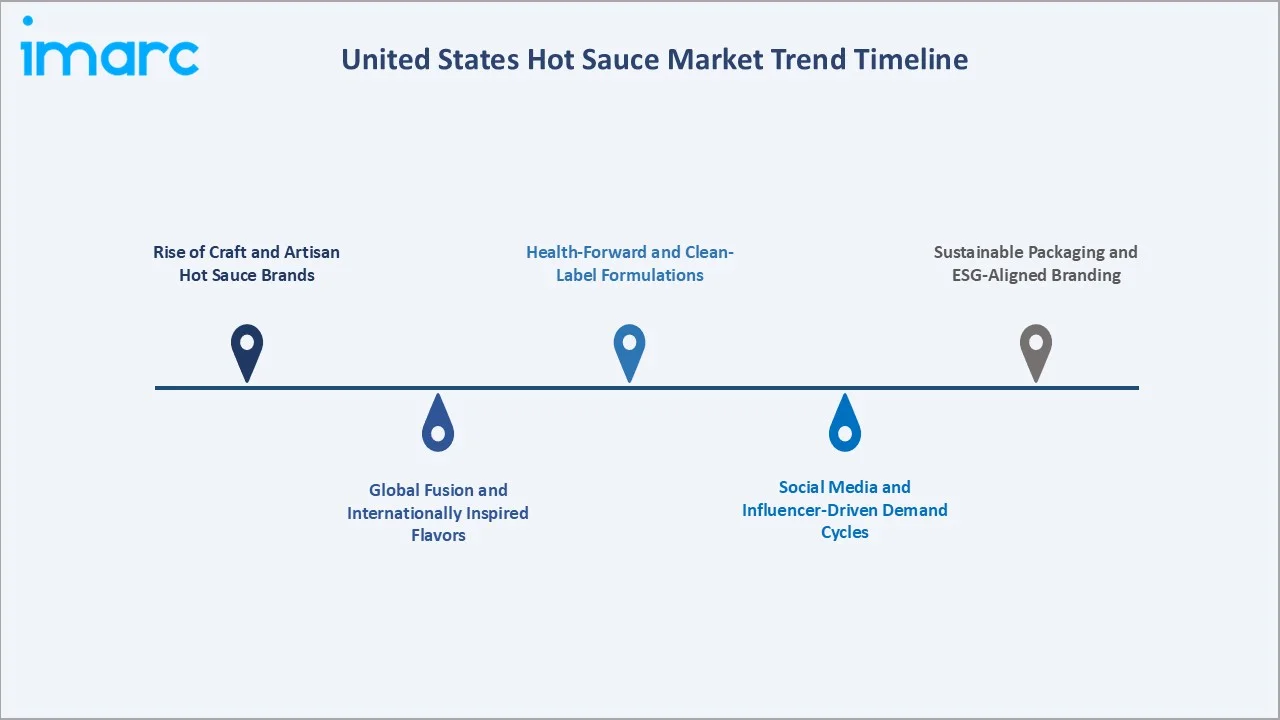

Emerging Market Trends

1. Rise of Craft and Artisan Hot Sauce Brands

The United States hot sauce market is experiencing a significant shift toward small-batch, artisan production. Consumers are increasingly seeking authentic flavor experiences rooted in regional chili traditions, unique fermentation methods, and transparent sourcing. Craft hot sauce brands are leveraging farmers' market exposure, e-commerce platforms, and food festival presence to build loyal followings and transition into mainstream retail distribution.

2. Global Fusion and Internationally Inspired Flavors

Demand for globally inspired hot sauce flavors, including Korean gochujang blends, West African peri-peri, and Caribbean scotch bonnet varieties, is rapidly expanding the traditional American hot sauce flavor palette. This trend is accelerated by the growing multicultural consumer base, food tourism, and increasing exposure to international cuisines through streaming platforms and food media content.

3. Health-Forward and Clean-Label Formulations

A growing segment of health-conscious consumers is prioritizing hot sauce products with clean-label attributes including organic certification, no artificial preservatives, non-GMO ingredients, and low-sodium profiles. Brands investing in transparent labeling and wellness-aligned positioning are capturing increased shelf space and premium price points across natural food retail channels.

4. Social Media and Influencer-Driven Demand Cycles

Viral food challenges, social media trends, and celebrity-endorsed hot sauce collaborations are generating rapid consumer interest and short-cycle demand spikes. Platforms are amplifying product discovery, enabling emerging brands to achieve nationwide visibility and accelerate sales growth through user-generated content and influencer engagement.

5. Sustainable Packaging and ESG-Aligned Branding

Environmental sustainability is becoming an increasing purchasing consideration for United States hot sauce consumers. Brands adopting recyclable glass bottles, reduced-plastic packaging, and carbon footprint reduction commitments are gaining preference among millennial and Gen Z consumers who align brand values with purchasing decisions.

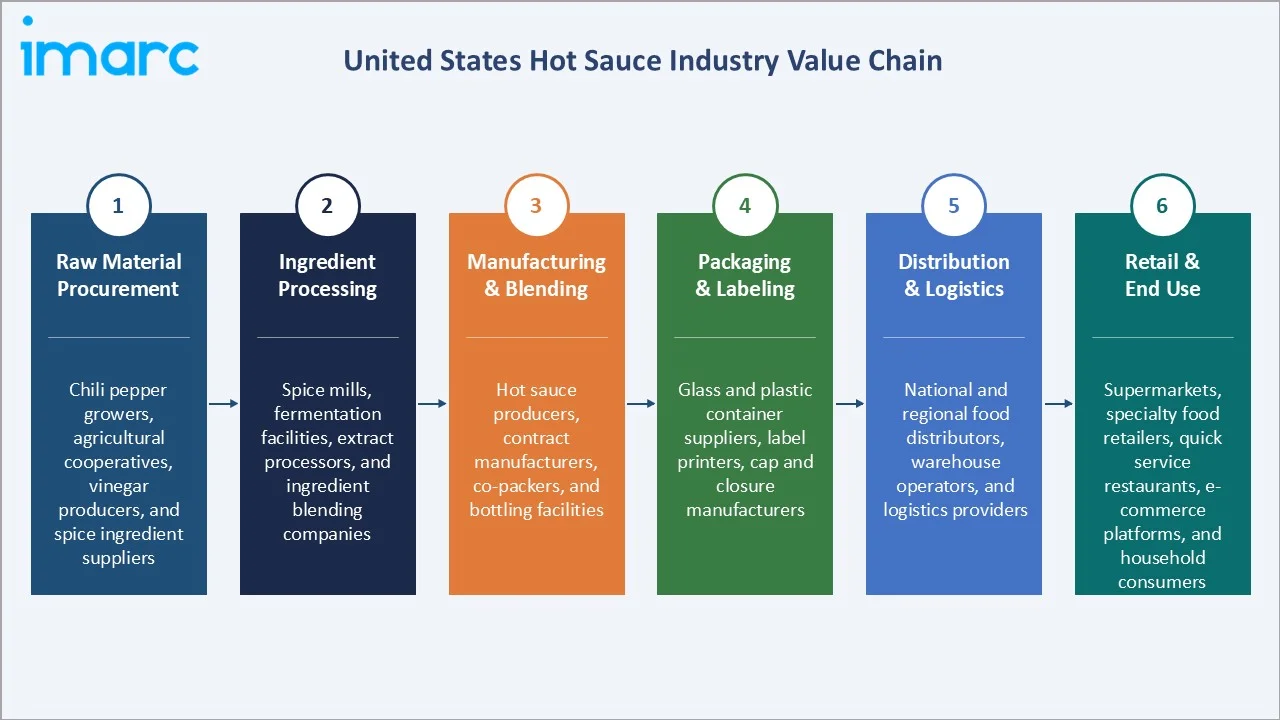

Industry Value Chain Analysis

The United States hot sauce value chain spans six stages from raw material procurement to retail and end-user consumption. Manufacturing, flavor development, and branding capture the highest value-add, while distribution efficiency and shelf placement are critical competitive levers in the retail environment.

|

Stage |

Key Players / Examples |

|

Raw Material Procurement |

Chili pepper growers, agricultural cooperatives, vinegar producers, and spice ingredient suppliers |

|

Ingredient Processing |

Spice mills, fermentation facilities, extract processors, and ingredient blending companies |

|

Manufacturing & Blending |

Hot sauce producers, contract manufacturers, co-packers, and bottling facilities |

|

Packaging & Labeling |

Glass and plastic container suppliers, label printers, cap and closure manufacturers |

|

Distribution & Logistics |

National and regional food distributors, warehouse operators, and logistics providers |

|

Retail & End Use |

Supermarkets, specialty food retailers, quick service restaurants, e-commerce platforms, and household consumers |

Vertically integrated players with proprietary chili sourcing, in-house manufacturing, and direct-to-consumer capabilities are positioned to capture greater margin and supply chain resilience than brands relying on co-packers and third-party distribution networks.

Technology Landscape in the United States Hot Sauce Industry

Advanced Fermentation Technology

Fermentation is an evolving area of product development within the United States hot sauce industry. Manufacturers are deploying controlled fermentation processes that enhance flavor complexity, develop umami profiles, and produce probiotic-associated benefits. The integration of precision fermentation techniques allows producers to achieve consistent flavor profiles at scale while maintaining artisan-quality taste attributes.

Flavor Science and Encapsulation

Advances in flavor encapsulation technology are enabling manufacturers to create hot sauce products with controlled heat release, extended shelf life, and enhanced flavor stability. These technologies allow brands to formulate new product variants with broad consumer reach, including low-heat-intensity sauces that maintain the flavor profile without the full capsaicin effect.

E-Commerce Personalization and Data Analytics

Leading hot sauce brands are leveraging consumer data analytics, purchase history modeling, and AI-driven recommendation algorithms to personalize product discovery on direct-to-consumer platforms. Data-driven insights are informing new flavor development cycles, packaging design decisions, and targeted marketing investments across digital channels.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Medium Hot Sauce |

46.2% |

2025 |

|

Application |

Cooking Sauce |

57.4% |

2025 |

|

End Use |

Commercial |

🔒 |

2025 |

|

Packaging |

Jars |

🔒 |

2025 |

|

Distribution Channel |

Supermarkets and Hypermarkets |

🔒 |

2025 |

|

Region |

South |

35.6% |

2025 |

By Product Type

Medium hot sauce commands a 46.2% majority share in 2025, driven by its broad consumer appeal across demographics, compatibility with both cooking and table use, and strong presence in mainstream retail and food service. The segment benefits from wide flavor variety, moderate price accessibility, and its role as the default category entry point for new hot sauce consumers.

To access detailed market analysis, Request Sample

Mild hot sauce at 33.8% in 2025 captures family-oriented households, institutional food service buyers, and first-time consumers seeking flavor without intense heat.

By Application

Cooking sauce leads the application segment at 57.4% in 2025, reflecting the deeply embedded practice of using hot sauce as a primary cooking ingredient across United States households. The segment is supported by the meal kit boom, social media cooking content, and recipe-driven product marketing by leading hot sauce brands.

Table sauce at 42.6% in 2025 covers on-table condiment usage in households, restaurants, and quick service operations. The segment benefits from product portability, miniature bottle formats, and strong brand loyalty driven by iconic products in the United States hot sauce category.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

South |

35.6% |

Deep-rooted spicy food culture, high density of regional hot sauce brands, strong food service demand, and leading retail penetration |

|

West |

24.1% |

Health-conscious consumers, multicultural population, growing artisan condiment segment, and expanding specialty food retail |

|

Midwest |

22.3% |

Established mainstream retail presence, growing interest in bold flavors, and expanding food service and quick service restaurant sector |

|

Northeast |

18.0% |

Rising multicultural demographics, premium and specialty food retail expansion, growing demand for artisan and international hot sauce variants |

South commands 35.6% of the United States hot sauce market in 2025, reflecting the region's long-standing culinary affinity for spicy flavors, a high density of regional hot sauce manufacturers, and strong retail and food service demand.

West at 24.1% is supported by California's diverse and health-conscious consumer base, rapid adoption of artisan and craft food products, and a large multicultural population driving demand for globally inspired hot sauce varieties.

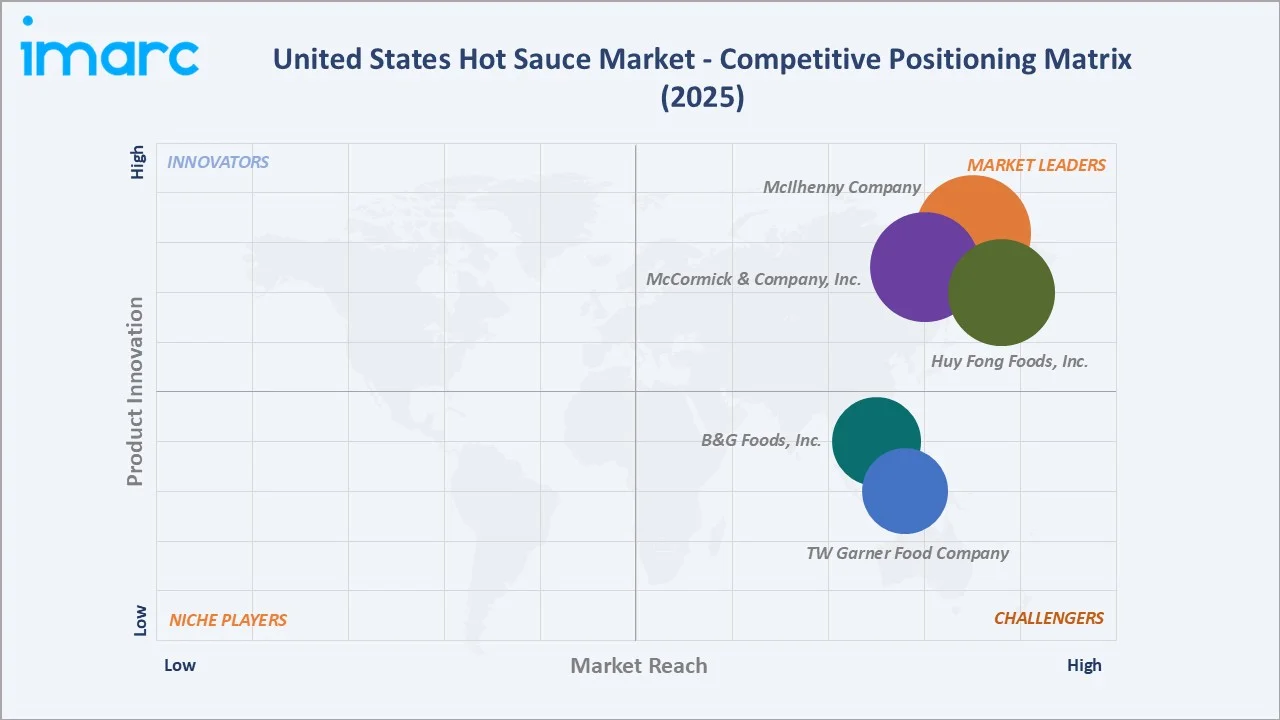

Competitive Landscape

The United States hot sauce market is moderately fragmented, with established multinational food companies and iconic domestic brands competing alongside a rapidly expanding base of artisan and craft producers. Brand heritage, distribution breadth, flavor innovation, and retail shelf presence are the primary competitive differentiators across the category.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

McIlhenny Company |

Tabasco |

Leader |

Heritage brand expansion, global distribution, and new flavor line extensions |

|

Huy Fong Foods, Inc. |

Sriracha |

Leader |

Supply chain resilience, iconic brand positioning, and product quality consistency |

|

McCormick & Company, Inc. |

Frank's RedHot, Cholula |

Leader |

Multi-brand portfolio management, global reach, and multichannel distribution |

|

B&G Foods, Inc. |

Trappey's |

Challenger |

Established brand management, value segment positioning, and food service distribution |

|

TW Garner Food Company |

Texas Pete |

Challenger |

Food service focus and portfolio expansion |

Key players include McIlhenny Company, Huy Fong Foods, Inc., McCormick & Company, Inc., B&G Foods, Inc., and TW Garner Food Company, among others.

Key Company Profiles

McIlhenny Company

McIlhenny Company is a privately held American food company headquartered on Avery Island, Louisiana, founded in 1868. The company is the producer of Tabasco brand pepper sauce, one of the most recognized hot sauce brands in the world. The company is family-owned and continues to operate from its original production site on Avery Island.

- Product Portfolio: Tabasco Original Red Sauce, Tabasco Chipotle Pepper Sauce, and Tabasco Sweet & Spicy Sauce.

- Recent Developments: McIlhenny Company appointed its first CEO from outside the founding family in January 2026, bringing in an executive from the consumer packaged goods industry to lead the next phase of growth.

- Strategic Focus: Sustaining brand heritage while pursuing flavor line extensions, expanding food service and international distribution, and broadening the consumer base among younger demographics.

Huy Fong Foods, Inc.

Huy Fong Foods, Inc. is a privately held American company founded in 1980 and headquartered in Irwindale, California. The company specializes in chili-based condiments and has built a strong market presence through its focus on authentic flavor profiles, consistent product quality, and broad distribution across retail and foodservice channels.

- Product Portfolio: Sriracha, Chili Garlic, and Sambal Oelek.

- Recent Developments: The company continued to manage recurring production constraints linked to chili pepper agricultural supply challenges, resulting in periodic availability gaps across retail and food service channels in the United States.

- Strategic Focus: Maintaining product quality and consistency, stabilizing chili pepper supply chain operations, and sustaining the iconic brand positioning of Sriracha in the United States condiment market.

McCormick & Company, Inc.

McCormick & Company, Inc. is a publicly traded American flavor company headquartered in Hunt Valley, Maryland, United States. The company manufactures, markets, and distributes herbs, spices, seasonings, and condiments across several countries.

- Product Portfolio: Frank's RedHot Original Cayenne Pepper Hot Sauce, Frank's RedHot XTRA Hot Sauce, Frank's RedHot Sweet Chili Sauce, and Cholula Original Hot Sauce.

- Recent Developments: The company continues to invest in portfolio optimization, distribution expansion, supply chain efficiencies, and brand-building initiatives to strengthen its position across the global flavorings and condiments market.

- Strategic Focus: Managing and growing a dual hot sauce portfolio through brand differentiation, multichannel distribution, food service volume expansion, and leveraging global manufacturing scale to drive innovation.

Market Concentration Analysis

The United States hot sauce market exhibits moderate to low concentration. McIlhenny Company, Huy Fong Foods, Inc., and McCormick & Company, Inc. collectively anchor the leadership tier, while B&G Foods, Inc., and TW Garner Food Company hold established challenger positions in regional and value segments.

Barriers to entry are moderate, reflecting the importance of established retail distribution networks, retailer relationships, manufacturing scale, and brand recognition within the competitive condiment category. These factors favor established manufacturers with broad distribution reach, strong retailer partnerships, and the ability to support consistent product availability across national and regional markets.

Consolidation is increasing as larger food manufacturers and investment firms acquire established hot sauce brands to strengthen their portfolios and expand market presence. Strategic acquisitions, brand portfolio diversification, and investments in premium and craft offerings are reinforcing the positions of leading players while broadening their reach across consumer segments.

Investment & Growth Opportunities

Fastest-Growing Segments

Very hot sauce is expanding the fastest within the product type category, driven by growing consumer interest in extreme heat experiences and the viral social media culture around spicy food challenges. The segment is also benefiting from rising demand for premium craft sauces featuring specialty chili varieties, such as ghost pepper and scorpion pepper blends.

Emerging Markets

West presents the strongest forward growth opportunity, supported by California's health-conscious and multicultural consumer base, a dense concentration of specialty food retail, and a growing artisan food entrepreneurship ecosystem. E-commerce markets within the Northeast are also emerging as high-value growth channels for premium and direct-to-consumer hot sauce brands.

Venture & Investment Trends

Investment is concentrated in premium and craft hot sauce brands, e-commerce-native condiment companies, and hot sauce brands with plant-based, organic, or functional health positioning. Strategic acquisitions by major food companies are likely to continue driving consolidation through 2034.

Future Market Outlook (2026-2034)

The United States hot sauce market is forecast to expand from USD 1.45 Billion in 2025 to USD 1.99 Billion by 2034 at a CAGR of 3.58%, adding approximately USD 0.54 Billion in market value over the forecast period.

Four forces will shape the market through 2034: the continued premiumization of the hot sauce category; expansion of globally inspired and fusion flavor profiles; growing e-commerce and direct-to-consumer distribution; and the integration of health and wellness positioning within mainstream hot sauce product development.

By 2034, the United States hot sauce market is expected to be defined by a dual-track structure - a mainstream high-volume base anchored by iconic brands and food service distribution, alongside a premium and artisan tier driven by craft production, distinctive ingredients, and community-engaged brand building. Digital channels, subscription commerce, and social media-driven discovery will be central to consumer acquisition strategies.

Research Methodology

Primary Research

Primary research included structured interviews with hot sauce manufacturers, retail buyers, food service procurement managers, and specialty condiment distributors, validating market sizing, segment share, regional demand trends, and competitive dynamics across the United States hot sauce value chain.

Secondary Research

Secondary sources included United States Department of Agriculture trade data, FDA food industry publications, specialty food association reports, consumer panel data, company annual reports, press releases, and investor presentations from publicly traded food companies with hot sauce portfolio presence.

Forecasting Models

Market forecasts applied top-down and bottom-up modeling integrating retail scanner data, food service volume estimates, e-commerce sales trajectory, demographic consumption indicators, and macroeconomic variables. Scenario analysis addressed premiumization pace, craft segment growth, and commodity input cost dynamics.

Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Coverage | Mild Hot Sauce, Medium Hot Sauce, Very Hot Sauce |

| Applications Coverage | Cooking Sauce, Table Sauce |

| End Uses Coverage | Commercial, Household |

| Packagings Coverage | Jars, Bottles, Others |

| Distribution Channels Coverage | Supermarkets and Hypermarkets, Traditional Grocery Retailers, Online Stores, Others |

| Region Covered | Northeast, Midwest, South, West |

| Companies Covered | McIlhenny Company, Huy Fong Foods, Inc., McCormick & Company, Inc., B&G Foods, Inc., TW Garner Food Company, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the United States Hot Sauce Market Report

The United States hot sauce market was valued at USD 1.45 Billion in 2025, supported by rising multicultural food consumption, growing spicy food culture, and expanding food service demand across the country.

The market is projected to grow at a CAGR of 3.58% from 2026-2034, reaching USD 1.99 Billion, driven by premium product launches, artisan brand expansion, and e-commerce channel growth.

Medium hot sauce leads at 46.2% in 2025, propelled by broad consumer acceptance and retail versatility across household and food service segments.

Cooking sauce dominates at 57.4% in 2025, reflecting the widespread use of hot sauce as a primary cooking ingredient across United States households, restaurants, and meal kit services.

South commands 35.6% in 2025, anchored by strong regional spicy food culture and a high density of established hot sauce producers.

Leading players include McIlhenny Company, Huy Fong Foods, Inc., McCormick & Company, Inc., B&G Foods, Inc., and TW Garner Food Company, among others.

Key growth drivers include rising multicultural food preferences, health-conscious consumption trends, food service expansion, product innovation, and the broadening craft and artisan condiment segment.

Key challenges include raw material price volatility for chili peppers, intense competition from several active brands, compliance with food safety regulations, and the difficulty of brand differentiation in a crowded retail environment.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)