United States Immunoassay Market Size, Share, Trends and Forecast by Technology, Product, Application, End Use, and Region, 2026-2034

United States Immunoassay Market Size, Share, Trends & Forecast (2026-2034)

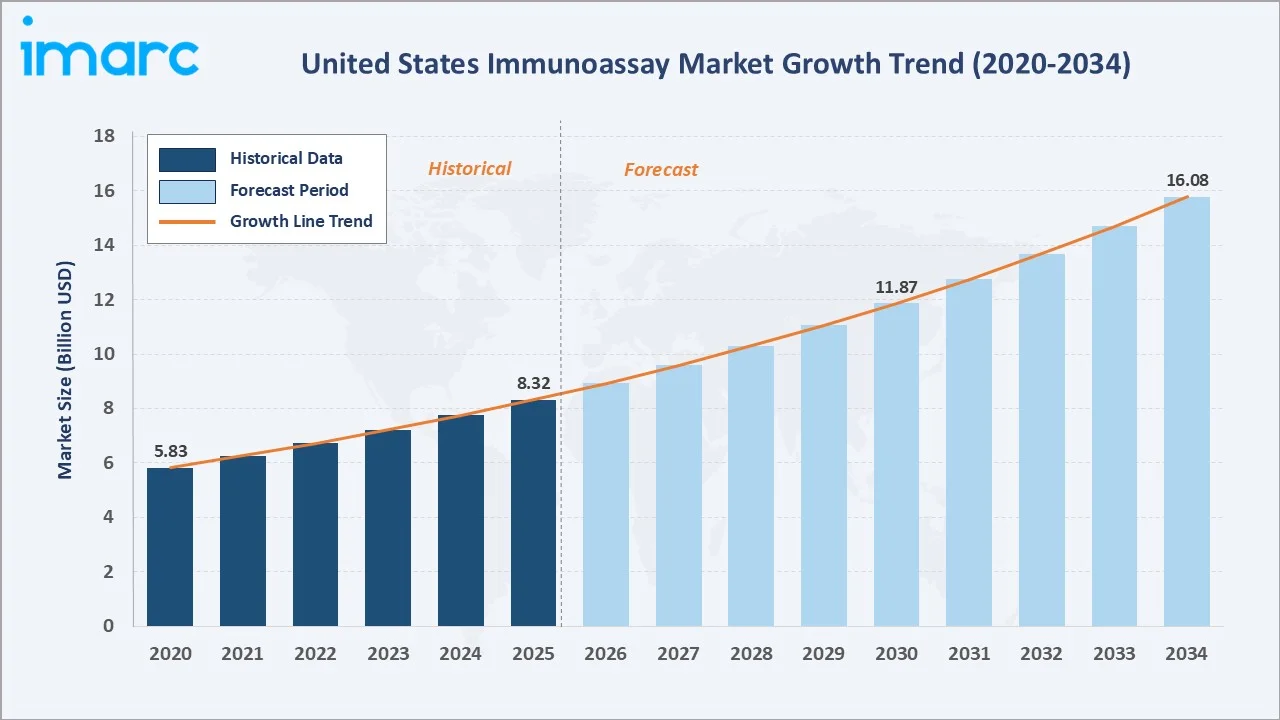

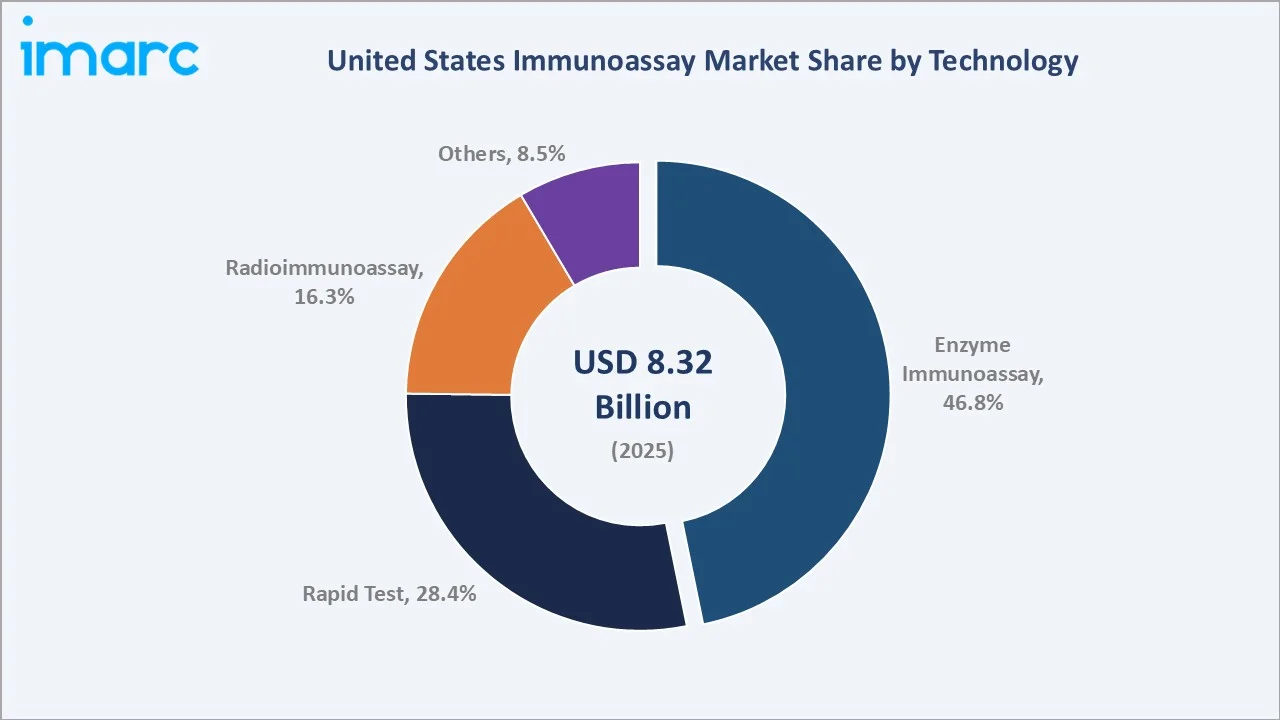

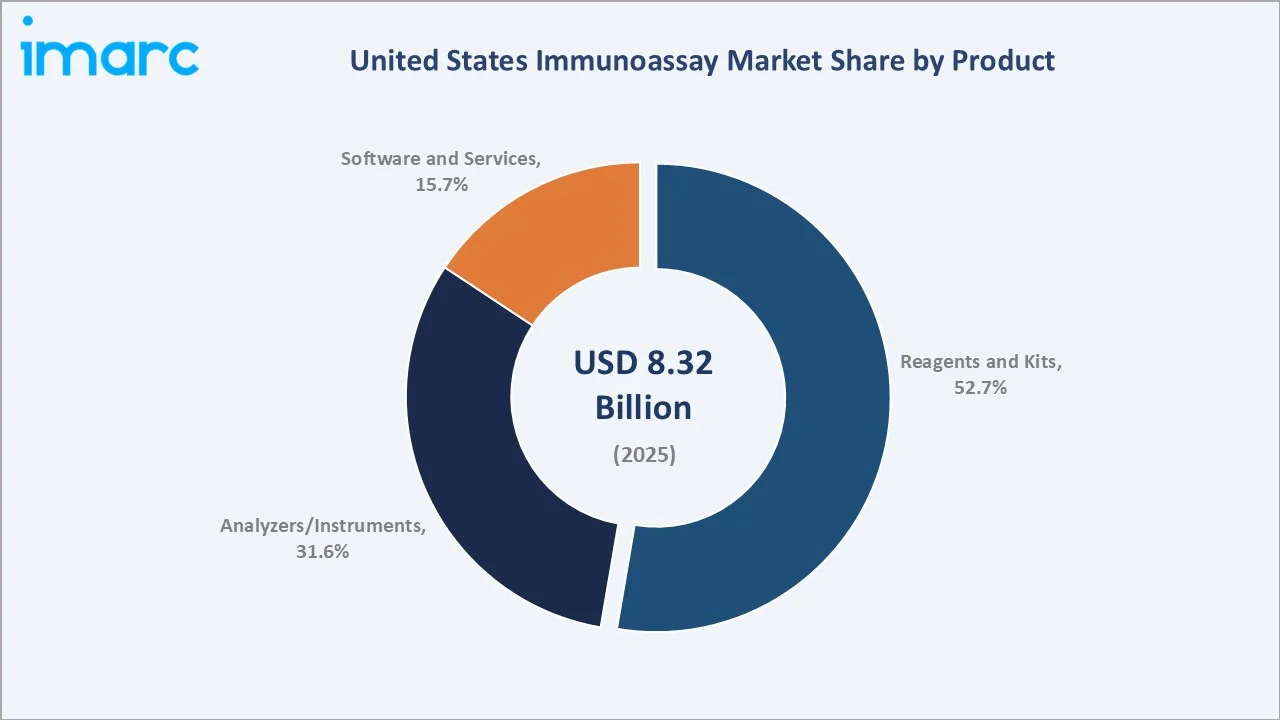

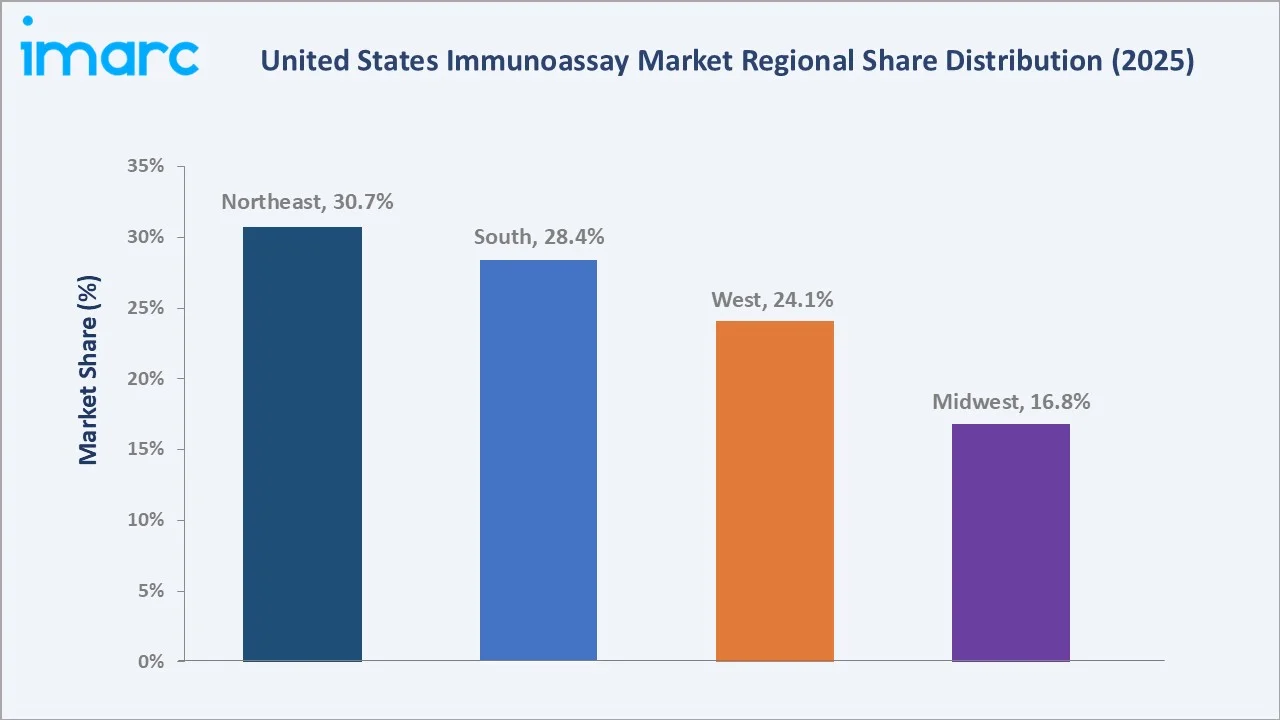

The United States immunoassay market reached USD 8.32 Billion in 2025 and is projected to reach USD 16.08 Billion by 2034, growing at a CAGR of 7.37% during 2026-2034. The rising prevalence of chronic and infectious diseases, growing demand for early and accurate diagnostics, and the increasing adoption of automated laboratory testing platforms are driving the market growth. Chronic diseases are highly prevalent across the United States, with approximately three in four American adults living with at least one chronic condition and more than half managing multiple conditions. The burden is particularly significant among older adults, where over 90% of individuals aged 65 and above have at least one chronic illness, midlife adults ages 35–64, more than 75% have at least one condition, and younger adults ages 18–34, 60% have at least one condition. The widespread prevalence of chronic diseases is driving demand for immunoassay testing. Enzyme immunoassay leads technology at 46.8%. Reagents and kits lead product at 52.7%. Northeast leads regionally at 30.7%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 8.32 Billion |

|

Forecast Market Size (2034) |

USD 16.08 Billion |

|

CAGR (2026-2034) |

7.37% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Technology |

Enzyme Immunoassay (46.8%, 2025) |

|

Dominant Product |

Reagents and Kits (52.7%, 2025) |

|

Leading Region |

Northeast (30.7%, 2025) |

The US immunoassay market expanded from USD 5.83 Billion in 2020 to USD 8.32 Billion in 2025, anchored at USD 11.87 Billion in 2030, and forecast to reach USD 16.08 Billion by 2034, supported by rising diagnostic testing demand, chronic disease prevalence, and automation in laboratories.

To get more information on this market, Request Sample

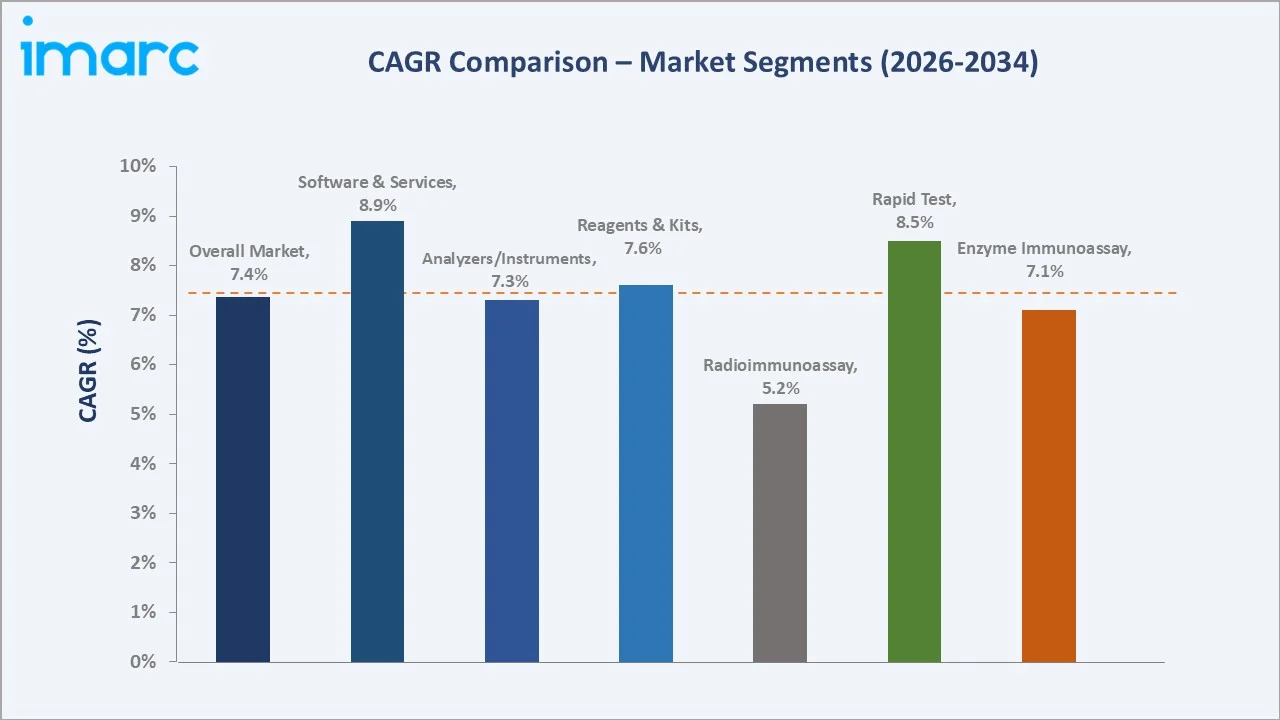

Software and services grow fastest at ~8.9% CAGR through laboratory information system (LIS) integration, AI-enhanced immunoassay analytics, quality management software, and remote diagnostics service subscription. Rapid test grows at ~8.5% CAGR through pharmacy-based POC immunoassay and near-patient diagnostics decentralization.

Executive Summary

The United States immunoassay market at USD 8.32 Billion in 2025 represents one of the most commercially advanced immunoassay markets through the US's laboratory automation penetration, stringent FDA-regulated diagnostic standards, and clinical laboratory test volume per capita. The market's 7.37% CAGR through 2034 reflects the maturing yet expanding immunoassay landscape. The market is projected to reach USD 16.08 Billion by 2034.

Enzyme immunoassay at 46.8% leads through ELISA and chemiluminescent immunoassay’s established central laboratory dominance. Reagents and kits at 52.7% reflect consumable-driven recurring revenue above instrument one-time purchase. Northeast leads at 30.7% through academic medical center and reference laboratory concentration.

Key Market Insights

|

Insight |

Data |

|

Dominant Technology |

Enzyme Immunoassay - 46.8% market share (2025) |

|

Dominant Product |

Reagents and Kits - 52.7% market share (2025) |

|

Leading Region |

Northeast - 30.7% market share (2025) |

|

Market Opportunity |

Multiplex immunoassay panel for oncology liquid biopsy; POC home allergy testing; AI-enhanced analyzer LIS integration; cardiac troponin high-sensitivity immunoassay; infectious disease rapid immunoassay platform expansion |

Key Analytical Observations Supporting the Above Data:

- Enzyme Immunoassay at 46.8%: The enzyme immunoassay segment dominates due to its high sensitivity, cost-effectiveness, and wide use in detecting hormones, infectious diseases, cancer biomarkers, and autoimmune conditions. Its compatibility with automated lab platforms further supports large-scale diagnostic adoption.

- Reagents and Kits at 52.7%: The reagents and kits segment dominates due to their recurring use in routine diagnostics, disease screening, and biomarker testing. High test volumes across hospitals, diagnostic labs, and research facilities drive consistent demand for assay kits and consumables.

- Northeast Region at 30.7%: The Northeast region dominates due to its strong concentration of advanced hospitals, diagnostic laboratories, academic research centers, and biotechnology companies. High healthcare spending and early adoption of automated diagnostic technologies further support regional growth.

United States Immunoassay Market Overview

The United States immunoassay market operates within the broader US in vitro diagnostics (IVD) market as the fastest-growing IVD segment above commodity clinical chemistry through immunoassay's biomarker superiority. The market’s commercial uniqueness lies in its recurring revenue model, as reagents and kits are consumed repeatedly across high-volume diagnostic testing. It also benefits from strong demand across multiple applications, including infectious disease, oncology, cardiology, endocrinology, and autoimmune testing. The presence of advanced laboratories, automation-ready platforms, and continuous biomarker innovation further differentiates the market.

The US immunoassay ecosystem integrates antibody and antigen development, reagent manufacturing and QC, regulatory clearance, commercial laboratory and hospital deployment, CPT code insurance billing, and patient diagnosis and disease management. Macroeconomic factors include healthcare spending, rising insurance coverage, and expanding diagnostic infrastructure.

Market Dynamics

To evaluate market opportunities, Request Sample

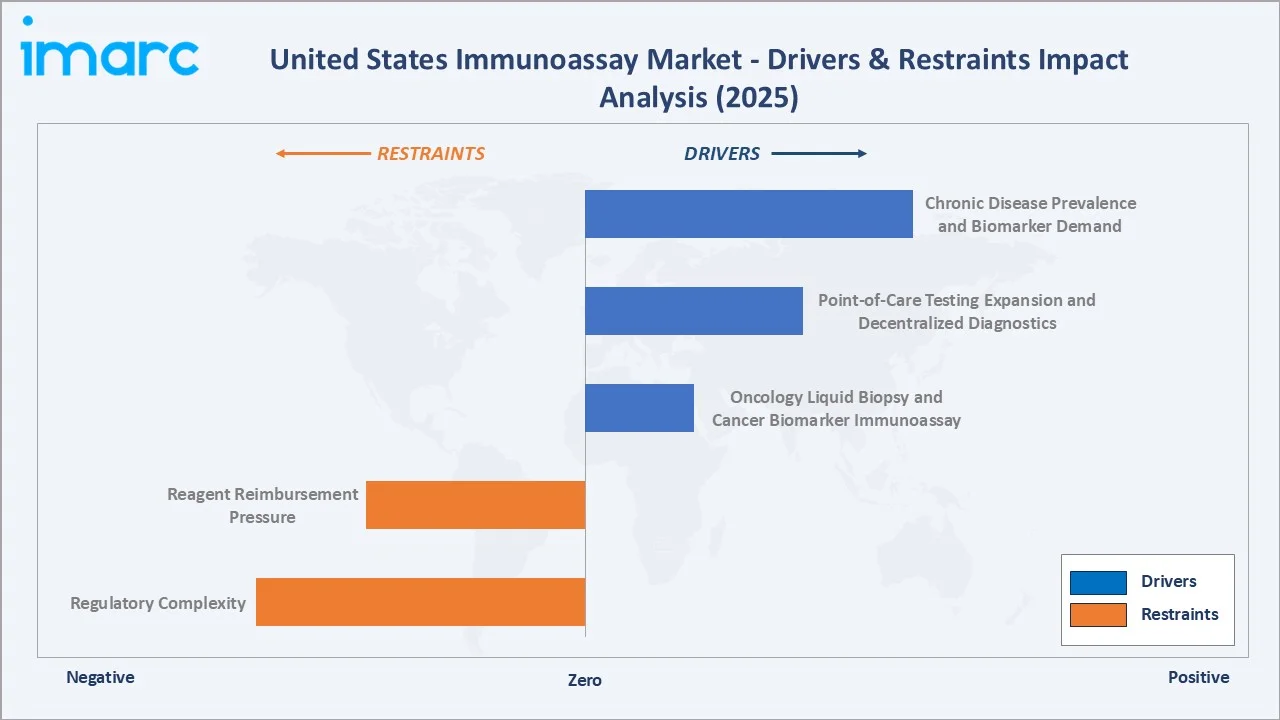

Market Drivers

- Chronic Disease Prevalence and Biomarker Demand: Three out of four adults in the United States live with at least one chronic condition, while more than half are affected by two or more. The burden is highest among adults aged 65 and above, with over 90% having at least one chronic illness, followed by more than 75% of adults aged 35–64 and 60% of younger adults aged 18–34. These rising chronic diseases are increasing the need for early diagnosis, disease monitoring, and treatment response tracking. Immunoassays are widely used to detect biomarkers linked to diabetes, cardiovascular diseases, cancer, thyroid disorders, and autoimmune conditions. As patients require repeated testing over time, demand for reagents, kits, and automated immunoassay platforms continues to rise. This recurring diagnostic need supports stable market growth across hospitals, diagnostic laboratories, and point-of-care settings.

- Point-of-Care Testing Expansion and Decentralized Diagnostics: Point-of-care testing expansion enables faster diagnosis near patients in clinics, emergency rooms, pharmacies, and home-care settings. Decentralized diagnostics reduce turnaround time, support early treatment decisions, and improve access outside central laboratories. Growing use of rapid immunoassay tests for infectious diseases, cardiac markers, pregnancy, hormones, and chronic disease monitoring is increasing test volumes. This is boosting demand for portable analyzers, rapid test kits, and consumables across the country.

- Oncology Liquid Biopsy and Cancer Biomarker Immunoassay: In 2026, approximately 2,114,850 new cancer cases and 626,140 cancer deaths are projected to occur in the United States. Oncology liquid biopsy and cancer biomarker immunoassays support early cancer detection, prognosis, and treatment monitoring. These tests help measure tumor-associated biomarkers in blood and other samples, reducing dependence on invasive procedures. Rising cancer incidence and increasing use of personalized medicine are boosting demand for accurate biomarker-based diagnostics. Growing adoption in hospitals, oncology centers, and reference laboratories is further expanding immunoassay testing volumes.

Market Restraints

- Reagent Reimbursement Pressure: Reagent reimbursement pressure is reducing profit margins for diagnostic laboratories and test providers. Lower or delayed reimbursement for routine immunoassay tests makes it difficult for labs to absorb rising reagent and consumable costs. This can limit investment in advanced assay platforms and slow the adoption of premium kits. Smaller laboratories are particularly affected, as they face tighter operating budgets and lower pricing flexibility.

- Regulatory Complexity: Regulatory complexity increases the time and cost required for assay development, validation, and approval. Companies must comply with strict FDA and quality control requirements, especially for high-risk diagnostic tests. This can delay product launches and raise compliance costs for manufacturers and laboratories. Smaller players may face greater difficulty entering the market due to limited regulatory resources.

Market Opportunities

- Single-Molecule Immunoassay for Blood-Based Neurodegenerative Biomarker: Single-molecule immunoassays enable ultra-sensitive detection of neurodegenerative biomarkers in blood. These tests can support earlier diagnosis and monitoring of Alzheimer’s, Parkinson’s, and other neurological disorders. As demand rises for less invasive alternatives to cerebrospinal fluid testing and imaging, blood-based assays can gain wider clinical adoption. This opens growth opportunities for advanced platforms, specialized reagents, and neurology-focused diagnostic panels.

- Multiplex Immunoassay Panel for Respiratory and Infectious Diseases: Multiplex immunoassay panels enable the simultaneous detection of multiple respiratory and infectious disease biomarkers from a single sample. These assays improve diagnostic efficiency, reduce testing time, and support faster clinical decision-making. Growing demand for comprehensive testing of conditions such as influenza, COVID-19, RSV, and other respiratory infections is driving adoption. Their ability to enhance laboratory productivity while lowering per-test costs makes them increasingly attractive to hospitals, clinics, and diagnostic laboratories.

Market Challenges

- Cross-Reactivity and Matrix Interference: Cross-reactivity and matrix interference are significant challenges because they can affect test accuracy and reliability. Non-target substances, structurally similar molecules, or endogenous antibodies may interact with assay components, leading to false-positive or false-negative results. Variations in sample matrices such as blood, serum, or plasma can further interfere with biomarker detection and quantification. These issues increase the need for extensive assay validation, quality control measures, and confirmatory testing, adding to operational costs and complexity.

- Competition from Molecular Diagnostics: Competition from molecular diagnostics is challenging, as PCR, NGS, and other molecular tests offer higher sensitivity and specificity for many diseases. These technologies are increasingly preferred for infectious disease detection, oncology profiling, and genetic testing. As a result, some testing volumes may shift away from traditional immunoassays. This pressure pushes immunoassay companies to improve accuracy, speed, multiplexing, and cost-effectiveness.

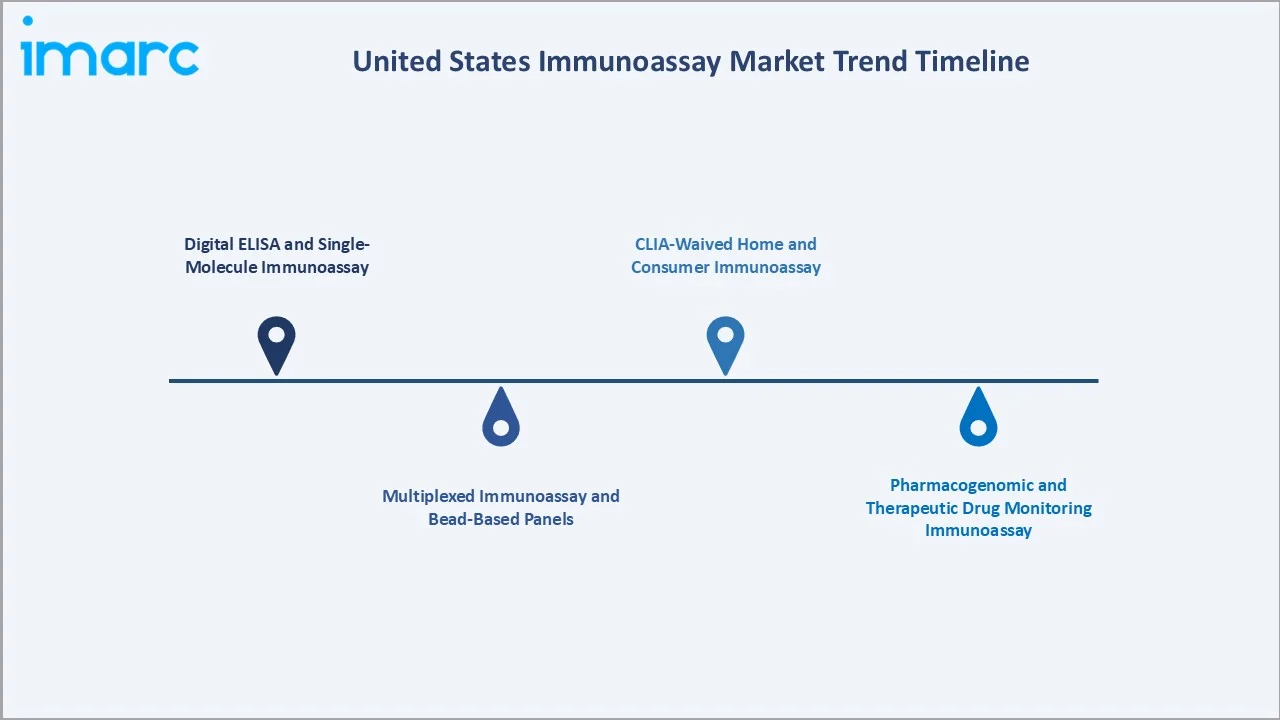

Emerging Market Trends

1. Digital ELISA and Single-Molecule Immunoassay

Digital ELISA and single-molecule immunoassays are emerging due to their ultra-high sensitivity and ability to detect very low-abundance biomarkers. These technologies are gaining use in oncology, neurology, infectious disease, and inflammatory disease testing. Their ability to support earlier diagnosis and precise disease monitoring is encouraging adoption in advanced laboratories and research settings. This trend is also driving demand for next-generation platforms, specialized reagents, and high-performance assay kits.

2. Multiplexed Immunoassay and Bead-Based Panels

Multiplexed immunoassays and bead-based panels are emerging as they allow multiple biomarkers to be measured from a single sample. They improve testing efficiency, reduce sample volume requirements, and support faster disease profiling. Their use is expanding in infectious disease, oncology, autoimmune, and inflammatory disorder testing. This trend is encouraging laboratories to adopt high-throughput platforms and advanced assay panels for more comprehensive diagnostics.

3. CLIA-Waived Home and Consumer Immunoassay

CLIA-waived home and consumer immunoassays are shifting testing from centralized labs to homes, pharmacies, and retail clinics. These tests offer faster, convenient, and easy-to-use screening for pregnancy, infectious diseases, hormones, and chronic disease monitoring. In January 2025, Roche announced that the U.S. FDA granted 510(k) clearance and CLIA waiver for its cobas liat STI multiplex assay panels. These tests allow clinicians to detect and differentiate chlamydia, gonorrhea, and Mycoplasma genitalium from a single sample. Rising demand for self-testing and decentralized care is expanding adoption. This trend is also creating growth opportunities for rapid test kits, digital readers, and connected diagnostic platforms.

4. Pharmacogenomic and Therapeutic Drug Monitoring Immunoassay

Pharmacogenomic and therapeutic drug monitoring immunoassays are emerging as they support personalized treatment and safer drug dosing. These assays help measure drug levels, toxicity risks, and patient response, especially in oncology, transplant care, infectious diseases, and psychiatry. The growing adoption of precision medicine is increasing demand for tests that guide therapy selection and dosage adjustment. This is encouraging laboratories to expand immunoassay-based monitoring panels for improved clinical outcomes.

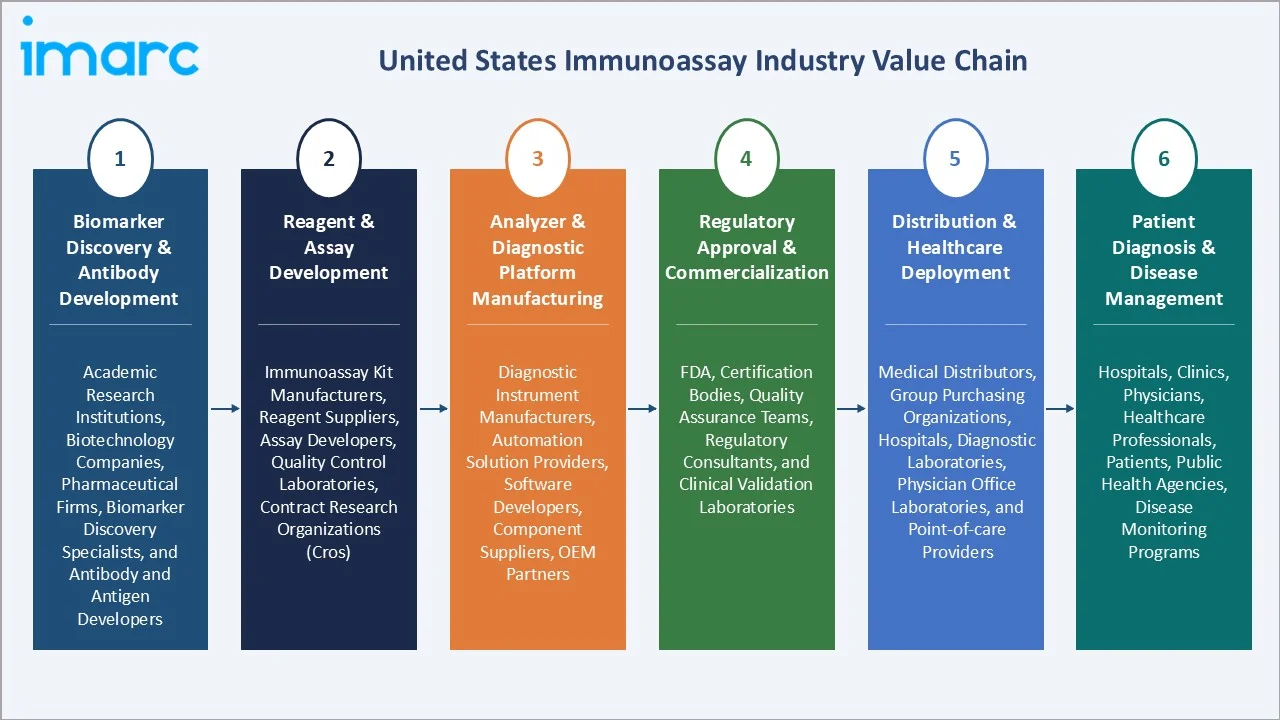

Industry Value Chain Analysis

The US immunoassay value chain integrates biomarker discovery & antibody development, reagent & assay development, analyzer & diagnostic platform manufacturing, regulatory approval & commercialization, distribution & healthcare deployment, and patient diagnosis & disease management.

|

Stage |

Key Participants |

|

Biomarker Discovery & Antibody Development |

Academic research institutions, biotechnology companies, pharmaceutical firms, biomarker discovery specialists, and antibody and antigen developers |

|

Reagent & Assay Development |

Immunoassay kit manufacturers, reagent suppliers, assay developers, quality control laboratories, contract research organizations (CROs) |

|

Analyzer & Diagnostic Platform Manufacturing |

Diagnostic instrument manufacturers, automation solution providers, software developers, component suppliers, OEM partners |

|

Regulatory Approval & Commercialization |

FDA, certification bodies, quality assurance teams, regulatory consultants, and clinical validation laboratories |

|

Distribution & Healthcare Deployment |

Medical distributors, group purchasing organizations, hospitals, diagnostic laboratories, physician office laboratories, and point-of-care providers |

|

Patient Diagnosis & Disease Management |

Hospitals, clinics, physicians, healthcare professionals, patients, public health agencies, disease monitoring programs |

Reagent & assay development is typically the most value-added segment in the US immunoassay value chain. This stage involves the development of proprietary antibodies, antigens, assay chemistries, and diagnostic kits that determine test accuracy, sensitivity, and specificity. Companies generate recurring revenue from reagent and kit sales, which are consumed continuously for diagnostic testing. Strong intellectual property, high margins, and frequent product innovation make this the most commercially attractive segment of the value chain.

Technology Landscape in the United States Immunoassay Industry

Chemiluminescent Immunoassay Technology

Chemiluminescent immunoassay technology offers high sensitivity, broad dynamic range, and rapid test processing. The technology enables accurate detection of low-concentration biomarkers, making it widely used in infectious disease, oncology, cardiac, and endocrine diagnostics. Its compatibility with fully automated, high-throughput analyzers supports large-scale laboratory operations and faster turnaround times. In May 2025, Revvity, Inc. launched EUROIMMUN’s IDS i20 analytical random access platform, designed to fully automate chemiluminescence immunoassays (ChLIA). The CE-marked and FDA-listed system enables laboratories to consolidate multiple specialty assays on one instrument, offering higher reagent capacity and improved throughput. Continuous advancements in chemiluminescent immunoassay platforms are further enhancing diagnostic precision, workflow efficiency, and laboratory productivity across the healthcare sector.

Lateral Flow and Rapid Immunoassay Platform

Lateral flow and rapid immunoassay platforms enable fast, portable, and user-friendly diagnostic testing. These platforms support point-of-care and home-based applications, delivering results within minutes without requiring complex laboratory infrastructure. Their growing adoption in infectious disease screening, pregnancy testing, cardiac marker detection, and chronic disease monitoring is expanding access to diagnostics. Advances in digital readers, connectivity features, and assay sensitivity are further enhancing the clinical utility of rapid immunoassay solutions.

Microfluidics-Based Immunoassay Technologies

Microfluidics-based immunoassay technologies enable highly sensitive testing with minimal sample and reagent volumes. These lab-on-a-chip platforms support faster assay processing, reduced costs, and greater portability compared to conventional systems. Their compact design makes them well-suited for point-of-care diagnostics, emergency settings, and decentralized healthcare applications. Ongoing advancements in microfluidics are improving multiplexing capabilities, automation, and real-time biomarker analysis, driving innovation across the immunoassay market.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Technology |

Enzyme Immunoassay |

46.8% |

2025 |

|

Product |

Reagents and Kits |

52.7% |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

End Use |

🔒 |

🔒 |

2025 |

|

Region |

Northeast |

30.7% |

2025 |

By Technology

Enzyme immunoassay leads at 46.8% (2025), through ELISA (enzyme-linked immunosorbent assay) and chemiluminescent immunoassay formats, dominating US hospital central laboratory and reference laboratory.

To access detailed market analysis, Request Sample

Rapid test at 28.4% grows fastest at ~8.5% CAGR through CLIA-waived lateral flow and POC analyzer expansion. Radioimmunoassay at 16.3% reflects declining but non-zero specialized reference laboratory RIA. Others at 8.5% include single-molecule immunoassay, ELISA plate reader, and fluorescence immunoassay.

By Product

Reagents and kits lead at 52.7% (2025), due to their recurring use in every immunoassay test, unlike instruments that are purchased less frequently. High testing volumes across hospitals, diagnostic labs, and research centers create continuous demand for assay kits, controls, buffers, and consumables.

Analyzers/instruments at 31.6% encompass a high-throughput immunoassay analyzer, POC analyzer, and multiplex platform. Software and services at 15.7% grow fastest at ~8.9% CAGR through LIS integration, AI analytics, and remote monitoring subscription service.

Regional Market Insights

|

Region |

Share (2025) |

Key US Immunoassay Market Drivers & Characteristics |

|

Northeast |

30.7% |

Supported by a high concentration of leading hospitals, academic medical centers, biotechnology companies, and diagnostic laboratories. |

|

South |

28.4% |

Driven by its large population base, growing chronic disease burden, expanding healthcare infrastructure, and increasing demand for routine diagnostic testing across hospitals and clinics. |

|

West |

24.1% |

Reflecting the presence of major biotechnology hubs, innovative healthcare systems, and significant investments in precision medicine, laboratory automation, and advanced diagnostic research. |

|

Midwest |

16.8% |

Supported by a well-established healthcare network, strong clinical laboratory presence, and rising demand for cost-effective diagnostic solutions across urban and rural healthcare facilities. |

Northeast's 30.7% leadership is supported by advanced hospitals, research centers, and biotechnology hubs. South's 28.4% driven by its large patient pool, chronic disease burden, and expanding healthcare infrastructure.

West's 24.1% benefiting from strong biotech innovation and precision medicine adoption. Midwest's 16.8% supported by established healthcare networks and growing demand for affordable diagnostic testing.

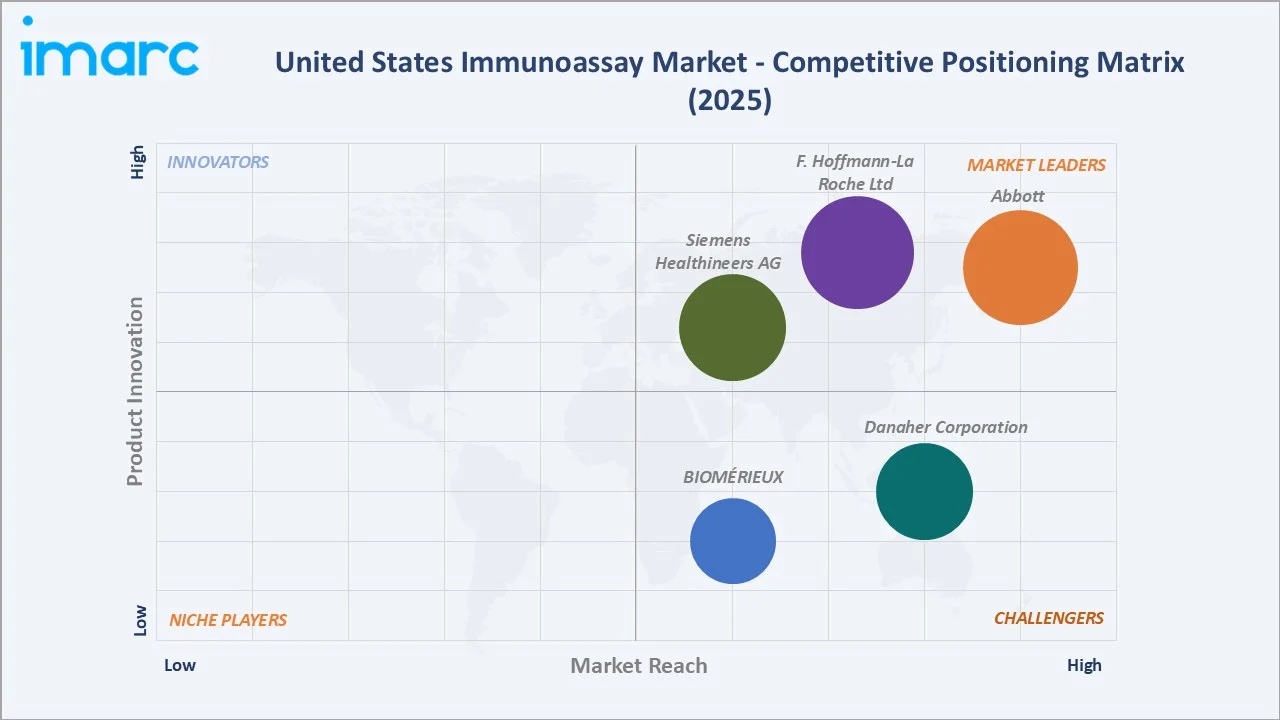

Competitive Landscape

The United States immunoassay market is moderately to highly competitive, with major players focusing on automated platforms, advanced reagents, and high-throughput diagnostic systems. Leading companies compete through product innovation, assay menu expansion, strategic partnerships, and regulatory approvals. Strong demand from hospitals, reference laboratories, and point-of-care settings continues to encourage investment in faster, more sensitive, and multiplexed immunoassay solutions.

|

Company |

Key Products |

Market Position |

Core Strength |

|

Abbott |

ARCHITECT, Alinity I, Alinity ci-series |

Market Leader |

Abbott is a major manufacturer of high-throughput laboratory instruments and rapid diagnostic tests used across infectious disease, oncology, cardiology, and neurology. |

|

F. Hoffmann-La Roche Ltd |

cobas pro integrated solutions, cobas pure integrated solutions |

Market Leader |

F. Hoffmann-La Roche Ltd is a top-tier player in the U.S. immunoassay market, dominating through Roche Diagnostics with its high-throughput, AI-powered cobas analytical platforms. |

|

Siemens Healthineers AG |

Atellica Solution, Atellica CI Analyzer, IMMULITE 2000 XPi System, ADVIA Centaur Systems, ADVIA Chemistry Systems |

Market Leader |

Siemens Healthineers AG is a major player in the U.S. immunoassay market, providing automated analyzers and a comprehensive menu of assays for cardiology, oncology, infectious diseases, and neurology. |

|

Danaher Corporation |

Access 2 + Analyzer, DxC 500i Analyzer, UniCel DxI 600 Analyzer, DxI 9000 Analyzer |

Strong Challenger |

Danaher Corporation plays a significant role in the United States immunoassay market. Danaher utilizes subsidiaries such as Beckman Coulter, Radiometer, Cepheid, and recently acquired Abcam to deliver automated analyzers, high-sensitivity reagents, and rapid diagnostic platforms. |

|

BIOMÉRIEUX |

VIDAS 3, VIDAS KUBE |

Strong Challenger |

BIOMÉRIEUX plays a pivotal role in the U.S. immunoassay market, particularly within hospital laboratories, by providing rapid, automated diagnostics for infectious diseases, critical care, and metabolic disorders. |

The US immunoassay competitive landscape is evolving through POC immunoassay disruption, novel technology differentiation, and AI integration.

Key Company Profiles

Abbott

Abbott is a leading participant in the United States immunoassay market, offering a broad portfolio of diagnostic solutions through its ARCHITECT and Alinity. The company provides immunoassay tests for infectious diseases, cardiology, oncology, and neurology, serving hospitals, clinical laboratories, and point-of-care settings nationwide.

- Key Products: ARCHITECT, Alinity I, Alinity ci-series.

- Strategic Focus: Expanding its automated diagnostic platforms, particularly the ARCHITECT and Alinity systems, to improve laboratory efficiency and testing throughput.

F. Hoffmann-La Roche Ltd

F. Hoffmann-La Roche Ltd is a leading player in the United States immunoassay market through its Diagnostics division, which offers a comprehensive portfolio of immunoassay solutions on the cobas platform. The company provides assays for oncology, infectious diseases, cardiology, women's health, endocrinology, and autoimmune disorders, serving hospitals, reference laboratories, and integrated healthcare networks.

- Key Products: cobas pro integrated solutions, cobas pure integrated solutions.

- Recent Developments: In March 2026, Roche announced that the U.S. FDA granted 510(k) clearance for its latest analytical units, the cobas c 703 and cobas ISE neo. These additions to the modular cobas pro integrated solutions enhance laboratory automation and help address staff shortages, space constraints, and rising testing volumes.

- Strategic Focus: Centered on expanding its cobas immunodiagnostic platform portfolio, enhancing laboratory automation, and advancing biomarker-driven diagnostics.

Market Concentration Analysis

The United States immunoassay market exhibits moderate to high market concentration, with a few multinational diagnostics companies accounting for a significant share of industry revenue. Major players benefit from extensive product portfolios, strong distribution networks, and large installed instrument bases. High regulatory requirements, substantial R&D investments, and the need for clinical validation create significant barriers to entry for new participants. At the same time, niche and emerging companies compete by introducing specialized assays, point-of-care solutions, and advanced biomarker technologies. Continuous innovation, strategic partnerships, and assay menu expansion remain key competitive differentiators in the market.

Investment & Growth Opportunities

Highest Growth Segments

Software and services (~8.9% CAGR), rapid test (~8.5% CAGR), reagents and kits (~7.6% CAGR through high-sensitivity and specialty reagent premium), oncology liquid biopsy immunoassay (~12-15% CAGR from smaller base), single-molecule immunoassay (~20-25% CAGR from smaller base through Alzheimer's blood test), and multiplex immunoassay panel (~10-12% CAGR through autoimmune and oncology panel) represent US immunoassay highest-growth investment vectors through 2034.

Investment Themes

- Blood-based Alzheimer's immunoassay: Blood-based Alzheimer's immunoassays represent an attractive investment theme due to the growing prevalence of Alzheimer's disease and the increasing demand for early, accessible diagnosis. These tests offer a less invasive and more cost-effective alternative to PET imaging and cerebrospinal fluid analysis, enabling broader population screening. Advancements in biomarker detection technologies are improving clinical utility and supporting adoption across healthcare settings. As disease-modifying therapies expand, demand for accurate Alzheimer's diagnostic testing is expected to grow significantly.

- AI-enhanced immunoassay LIS integration for clinical decision support: AI-enhanced immunoassay LIS integration for clinical decision support is an emerging investment theme as laboratories increasingly seek intelligent workflows and data-driven diagnostics. Integrating AI with Laboratory Information Systems (LIS) enables automated result validation, anomaly detection, and real-time clinical insights, improving diagnostic accuracy and operational efficiency. Growing testing volumes and workforce shortages are accelerating demand for smart laboratory solutions. This creates opportunities for investments in healthcare AI, laboratory automation, and connected diagnostic ecosystems.

Future Market Outlook (2026-2034)

The United States immunoassay market is projected to grow from USD 8.32 Billion in 2025 to USD 16.08 Billion by 2034, delivering a 7.37% CAGR over the forecast period, driven by chronic disease biomarker demand, POC decentralization, novel platform (single-molecule immunoassay, multiplex) premium pricing, and an AI-enhanced analyzer service model. The market's anchor value of USD 11.87 Billion in 2030 represents the US immunoassay market at a premium technology inflection.

Three structural forces define the US immunoassay market through 2034: rising chronic disease and cancer testing demand, rapid shift toward automated and high-throughput laboratory platforms, and growing adoption of point-of-care and decentralized diagnostics. Together, these forces are expanding test volumes, increasing recurring demand for reagents and kits, and encouraging innovation in sensitive, multiplexed, and AI-enabled immunoassay technologies.

Research Methodology

Primary Research

Primary research comprised interviews and discussions with diagnostic laboratories, hospitals, clinicians, procurement managers, and industry experts. It helped assess immunoassay adoption trends, testing demand, pricing dynamics, platform preferences, and competitive positioning. Inputs from manufacturers and distributors further supported understanding of supply chains, reagent usage, and technology shifts in the US market.

Secondary Research

Secondary research encompassed the review of company annual reports, investor presentations, regulatory filings, product brochures, industry journals, scientific publications, government databases, and healthcare statistics. It also included analysis of FDA approvals, laboratory testing trends, reimbursement policies, and diagnostic market developments. Information from industry associations, public health agencies, and company press releases was used to validate market size, technology trends, competitive landscape, and growth opportunities in the United States immunoassay market.

Forecasting Models

US immunoassay market revenue forecasts were developed using a clinical test volume model: US laboratory test volume multiplied by immunoassay-category-specific average CPT reimbursement and private payer rate premium. Technology share: enzyme immunoassay declining from 46.8% toward 43% by 2034, as rapid test grows toward 32%; software and services growing fastest from 15.7% toward 20% through the AI-service model.

United States Immunoassay Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Technologies Covered | Radioimmunoassay, Enzyme Immunoassay, Rapid Test, and Others |

| Products Covered | Reagents and Kits, Analyzers/Instruments, Software and Services |

| Applications Covered | Therapeutic Drug Monitoring, Oncology, Cardiology, Endocrinology, Infectious Disease Testing, Autoimmune Diseases, and Others |

| End Uses Covered | Hospitals, Blood Banks, Clinical Laboratories, Pharmaceutical and Biotech Companies, Academic Research Centers, and Others |

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered | Abbott, F. Hoffmann-La Roche Ltd, Siemens Healthineers AG, Danaher Corporation, BIOMÉRIEUX, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the United States immunoassay market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the United States immunoassay market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the United States immunoassay industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the United States Immunoassay Market Report

The United States immunoassay market reached USD 8.32 Billion in 2025, driven by the rising burden of chronic and infectious diseases, increasing demand for early diagnosis, and growing use of biomarker-based testing. Expanding adoption of automated, high-throughput analyzers in hospitals and reference laboratories is improving testing efficiency. The shift toward point-of-care diagnostics, oncology testing, therapeutic drug monitoring, and personalized medicine is further supporting market growth.

The US immunoassay market grows at 7.37% CAGR during 2026-2034, reaching USD 16.08 Billion by 2034. The CAGR reflects chronic disease biomarker demand, blood-based Alzheimer's immunoassay FDA clearance, multiplex immunoassay panel premium, POC CLIA-waived decentralization, and AI-enhanced analyzer service.

Enzyme immunoassay leads at 46.8% through ELISA and chemiluminescent immunoassay, dominating the US hospital central laboratory.

Reagents and kits lead at 52.7% through recurring consumable revenue from Abbott ARCHITECT reagents, Roche reagents, and Siemens reagents, creating the predictable recurring immunoassay revenue through US laboratories' long-term reagent supply agreement.

The Northeast leads at 30.7% through the highest US hospital and academic medical center density and a high insured population.

Leading companies include Abbott, F. Hoffmann-La Roche Ltd, Siemens Healthineers AG, Danaher Corporation, and BIOMÉRIEUX, among others.

The US immunoassay market is projected to reach approximately USD 11.87 Billion by 2030, with FDA clearance of blood-based Alzheimer's immunoassay creating a new neurological biomarker immunoassay market, CLIA-waived home immunoassay expanding beyond COVID into STI and metabolic home testing, and an AI-enhanced analyzer premium tier.

Three priority investment opportunities: Blood-based Alzheimer's immunoassay, AI-enhanced immunoassay LIS integration, and multiplex autoimmune immunoassay panel.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)