U.S. LED Lighting Market Size, Share, Trends and Forecast by Application, and Region, 2026-2034

U.S. LED Lighting Market Size, Share, Trends & Forecast (2026-2034)

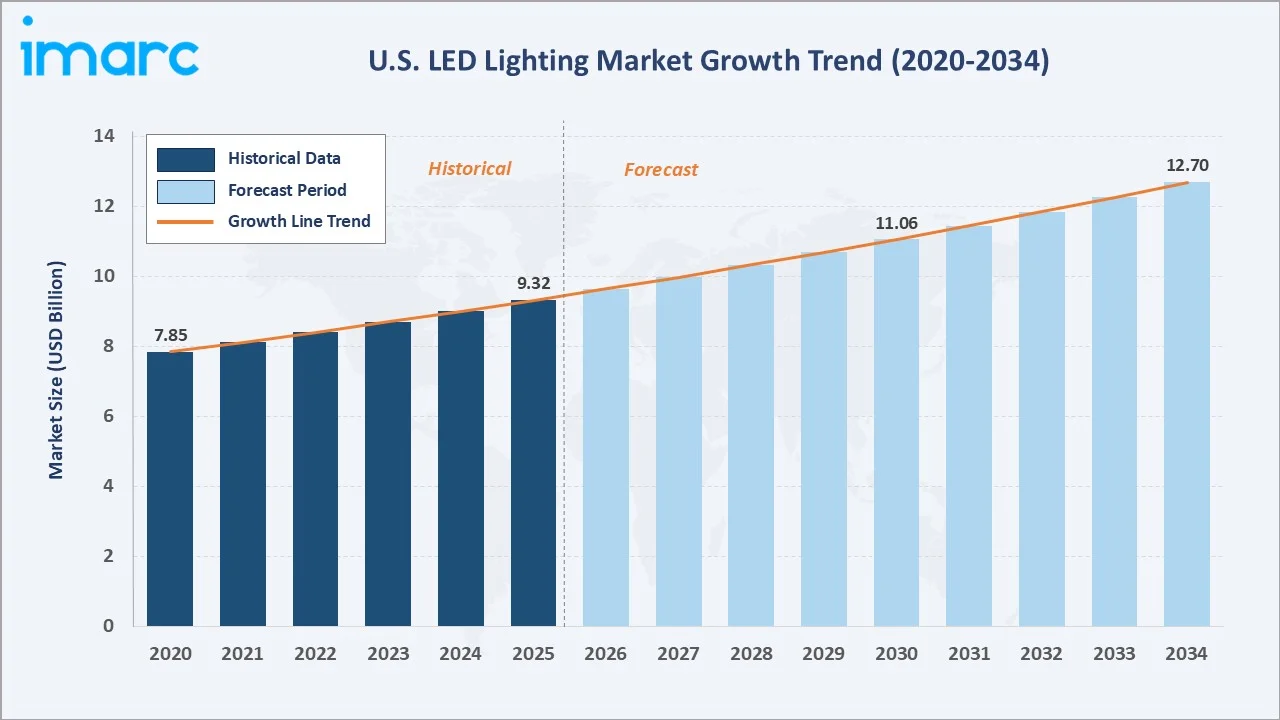

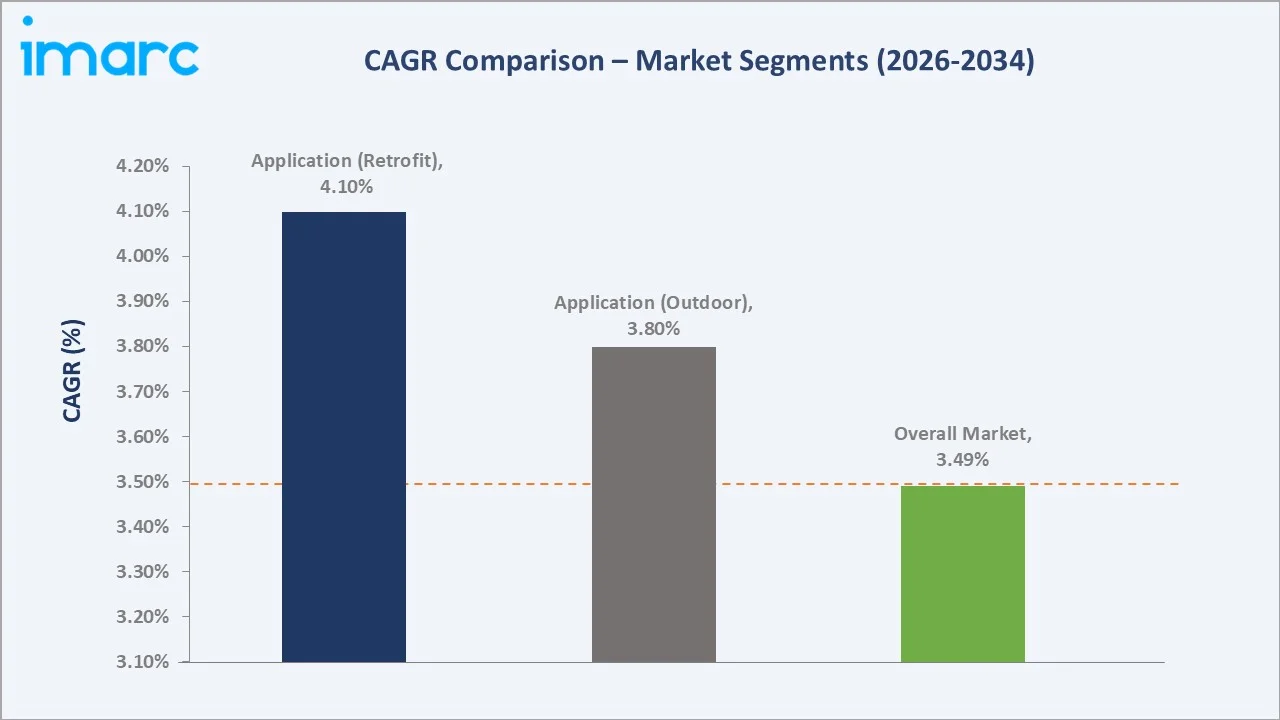

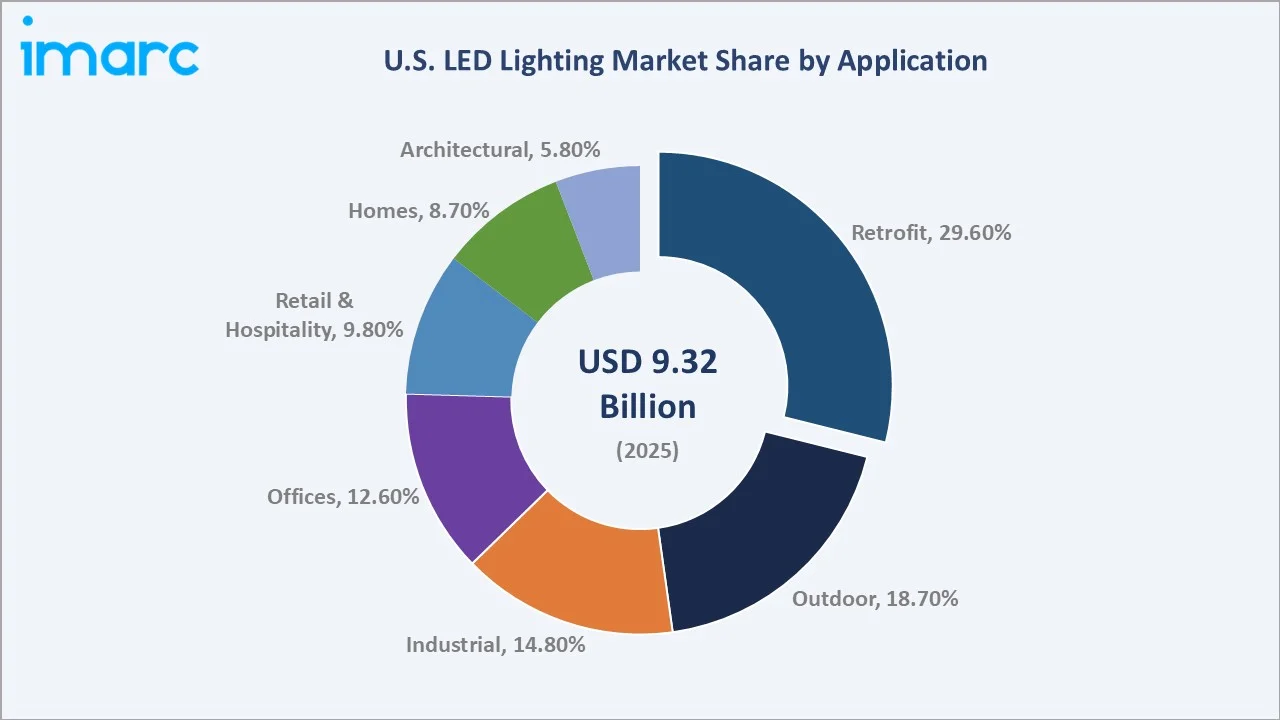

The U.S. LED lighting market size was valued at USD 9.32 Billion in 2025 and is projected to reach USD 12.70 Billion by 2034, growing at a CAGR of 3.49% during 2026-2034. Strong energy efficiency mandates, advancing smart lighting technology, and deep penetration across commercial, industrial, and residential sectors underpin consistent market expansion.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 9.32 Billion |

|

Forecast Market Size (2034) |

USD 12.70 Billion |

|

CAGR (2026-2034) |

3.49% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

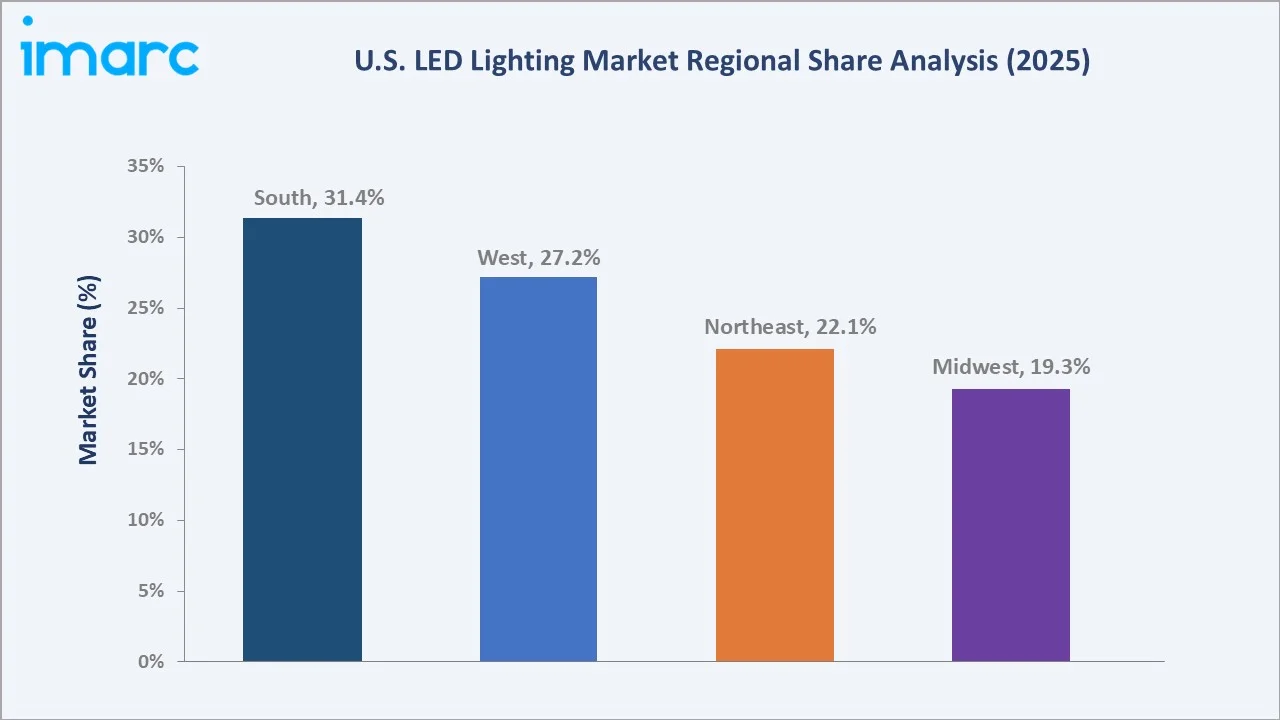

South (31.4% share, 2025) |

|

Largest Application Segment |

Retrofit (29.6% share, 2025) |

To get more information on this market, Request Sample

The South dominates, holding a 31.4% regional share in 2025, while retrofit leads application demand at 29.6%. The market benefits from government energy-efficiency mandates, the accelerating shift toward smart connected lighting, and declining LED product costs that enhance affordability across all end-use sectors.

Executive Summary

The U.S. LED lighting market is on a sustained growth trajectory, supported by energy-efficiency regulations, expanding smart building initiatives, and the ongoing phase-out of legacy incandescent and fluorescent lighting. The market reached USD 9.32 Billion in 2025 and is forecast to surpass USD 12.70 Billion by 2034, representing a healthy CAGR of 3.49% over the forecast period.

The South leads regionally with a 31.4% share in 2025, driven by robust construction activity, large commercial and industrial facility footprints, and strong utility rebate programs. The West accounts for 27.2%, benefiting from California's Title 24 building codes that mandate LED adoption. Retrofit installations command the largest application share at 29.6%, as commercial building owners aggressively upgrade legacy systems to meet decarbonization targets.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Application) |

Retrofit – 29.6% share (2025) |

|

Second Largest Application |

Outdoor – 18.7% share (2025) |

|

Leading Region |

South – 31.4% share (2025) |

|

Fastest Growing Region |

West (smart building codes + solar-LED integration) |

|

Top Companies |

Signify Holding, Acuity Inc., Eaton, ams-OSRAM AG, and Hubbell |

Key Analytical Observations Supporting the Above Data:

- Retrofit applications account for 29.6% of the U.S. LED lighting market in 2025, driven by upgrading from legacy lighting systems to LED fixtures with occupancy controls and networked management, which can reduce energy consumption by 50–80% and comply with local benchmarking ordinances.

- Outdoor lighting (18.7%) is expanding rapidly, supported by municipal streetlight LED conversion programs. According to the U.S. Department of Energy (DOE), the U.S. currently has more than 46 million outdoor LED street and area lights installed, creating demand for replacements and smart-control upgrades.

- The South holds 31.4% of the U.S. market in 2025, led by Texas, Florida, and Georgia, all of which maintain aggressive commercial construction pipelines and utility-funded LED rebate programs worth over USD 400 million annually.

- Industrial applications (14.8%) are benefiting from the re-shoring of manufacturing capacity into the U.S. Midwest and South, creating greenfield facility lighting demand for high-bay LED systems.

- The smart LED segment is the highest-growth investment vector, with IoT-integrated luminaires growing at an estimated 8.5% CAGR through 2034, driven by energy management mandates and occupancy-based lighting automation.

- Human-centric lighting (HCL) systems that adjust color temperature across the circadian cycle are gaining commercial traction in offices and healthcare facilities, representing a premium USD 480 million niche by 2030.

U.S. LED Lighting Market Overview

LED (Light Emitting Diode) lighting refers to solid-state lighting technology that converts electrical energy into visible light with substantially greater efficiency than incandescent or fluorescent alternatives. The U.S. market ecosystem encompasses LED chip manufacturers, driver and component suppliers, luminaire manufacturers, controls and software developers, distribution networks, and installation service providers.

Macroeconomic drivers, including federal energy-efficiency standards, mandatory phase-outs of inefficient lamps under the DOE's 45-lumen-per-watt rule, substantial utility rebate programs, and corporate sustainability commitments, are creating structurally persistent demand. The U.S. LED lighting market growth is further supported by the post-pandemic acceleration in smart building retrofits and the buildout of data centers, warehouses, and manufacturing facilities requiring high-efficiency, long-life lighting solutions.

Market Dynamics

To evaluate market opportunities, Request Sample

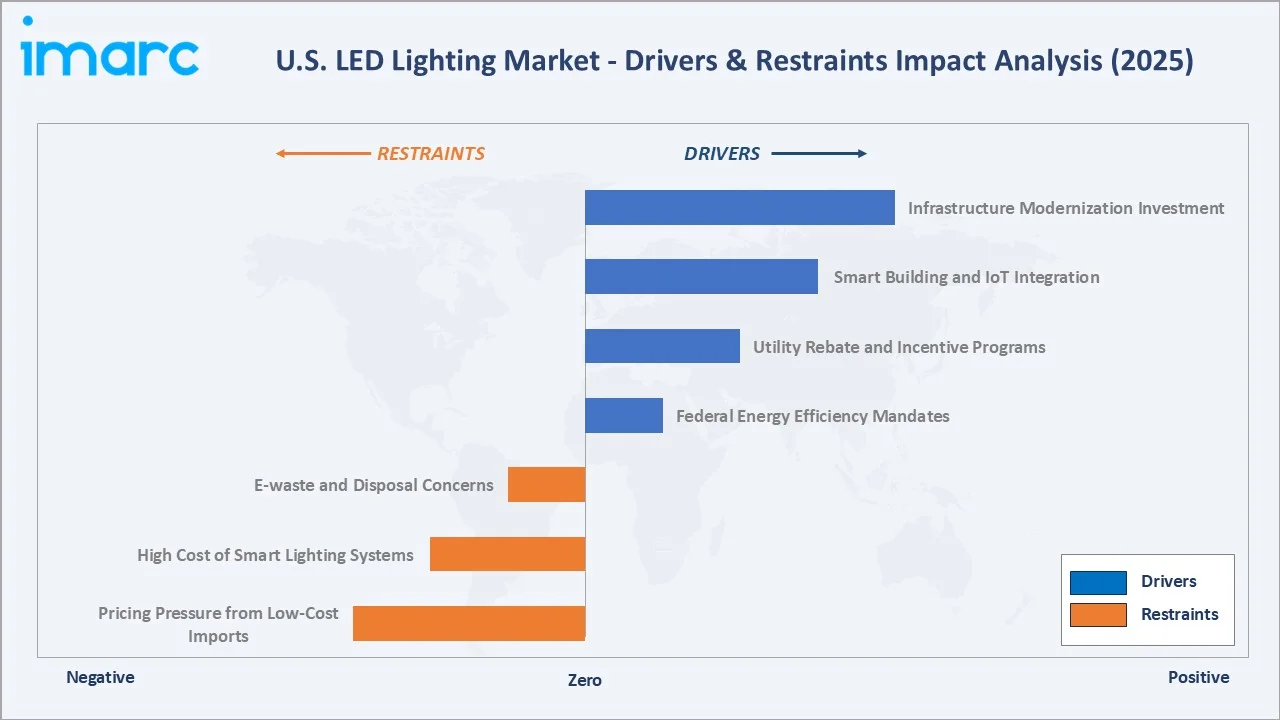

Market Drivers

- Federal Energy Efficiency Mandates: The U.S. Department of Energy, on April 26, 2024, issued the final rule that raises the minimum efficiency standard for the most common lightbulbs from 45 lumens per watt to over 120 lumens per watt, supporting the ongoing transition toward more efficient and longer-lasting LED lighting widely adopted by industry and consumers.

- Utility Rebate and Incentive Programs: Utility companies nationwide disbursed over USD 1.2 billion in LED lighting rebates in 2024, reducing payback periods for commercial retrofits to under 18 months and driving adoption across office, retail, and industrial segments.

- Smart Building and IoT Integration: The proliferation of smart building platforms, BACnet, DALI-2, and Zigbee-enabled systems require LED luminaires with integrated sensing and wireless control, elevating per-unit values and driving market revenue growth beyond simple volume expansion.

- Infrastructure Modernization Investment: The Bipartisan Infrastructure Law (BIL) allocated USD 1.2 trillion in federal funding toward transportation, energy, and climate infrastructure projects, supporting highway, bridge, and transit facility LED conversions.

Market Restraints

- Pricing Pressure from Low-Cost Imports: Commoditization of standard LED bulbs, largely manufactured in China, has compressed margins for domestic manufacturers and distributors, limiting revenue growth in the replacement lamp segment.

- High Cost of Smart Lighting Systems: Advanced networked LED systems with sensors, gateways, and software subscriptions can cost 3–5x more than basic LED fixtures, limiting adoption by small commercial and residential users with constrained capital budgets.

- E-waste and Disposal Concerns: LED products contain lead solder and rare earths in phosphors. Absence of universal recycling mandates creates reputational risk and potential future regulatory cost burdens for manufacturers.

Market Opportunities

- Human-Centric and Horticultural Lighting: Circadian-rhythm-aligned office lighting and full-spectrum LED grow lights for indoor farming represent nascent segments collectively valued at USD 11.3 billion by 2034 in the U.S., growing at an 8.90% CAGR during 2026-2034.

- Li-Fi and Visible Light Communication: Next-generation LED systems transmitting data via modulated visible light represent a transformational technology for secure enterprise environments, with early pilots in healthcare and government facilities in 2025.

- Solar-LED Hybrid Systems: Off-grid solar-powered LED street and pathway lighting is gaining traction in southern and western states with high solar irradiance, reducing municipal infrastructure costs while meeting sustainability targets.

Market Challenges

- Supply Chain Vulnerabilities: The majority of LED driver ICs and chip-on-board modules are sourced from Asia. Geopolitical tensions and logistics disruptions periodically create supply constraints, particularly for specialty high-power modules used in industrial and outdoor applications.

- Interoperability Fragmentation: Divergent smart lighting protocols (Zigbee, Z-Wave, Matter, BACnet, DALI) create integration complexity, slowing smart system adoption in retrofit markets where legacy infrastructure coexists with new controls.

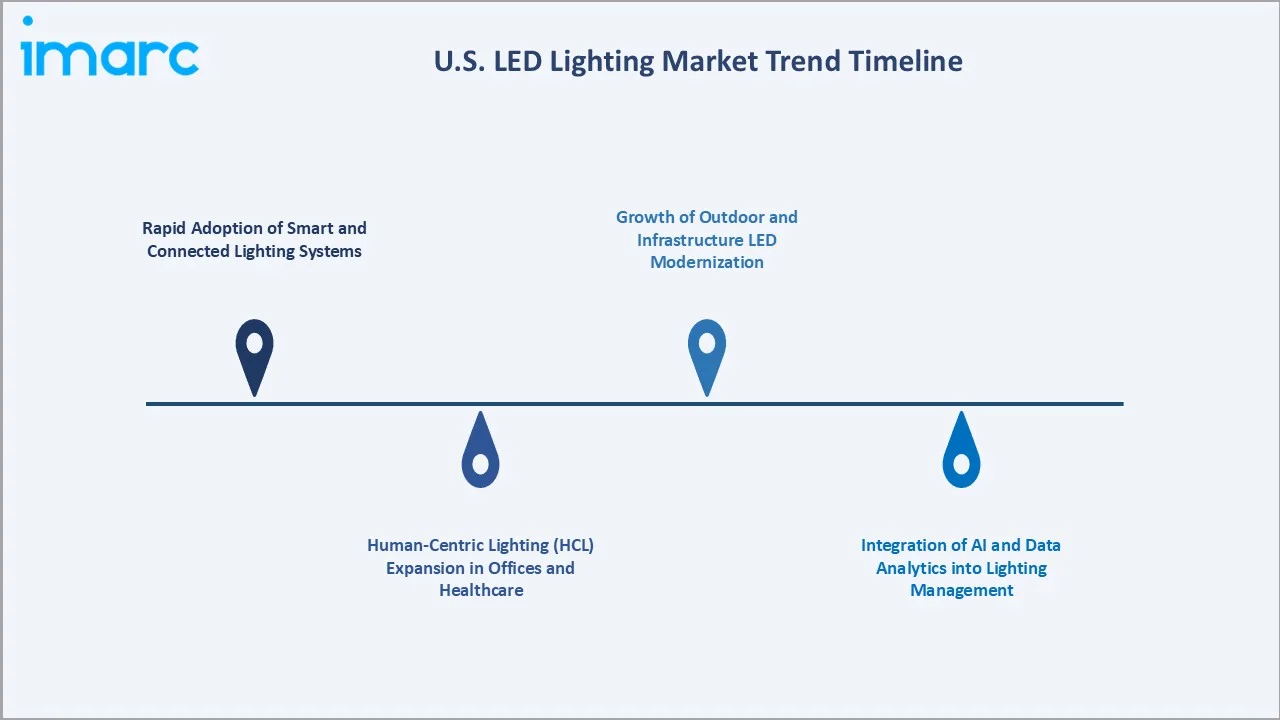

Emerging Market Trends

1. Rapid Adoption of Smart and Connected Lighting Systems

In 2024, estimates indicated that smart lighting can reduce energy use in commercial buildings by an additional 50-70% beyond the baseline LED efficiency gain. The U.S. LED lighting market trends show that major building owners such as REITs and corporate campuses now require DALI-2 or wireless mesh-enabled fixtures in standard procurement specifications.

2. Human-Centric Lighting (HCL) Expansion in Offices and Healthcare

Research published in 2025 confirmed that LED task lighting significantly improves sleep quality and reduces daytime dysfunction compared to fluorescent lighting in windowless office environments. Several U.S. hospital networks completed HCL retrofit pilots in 2024, and the American Institute of Architects (AIA) incorporated HCL guidance into its 2025 healthcare facility design standards, accelerating adoption across new hospital construction.

3. Integration of AI and Data Analytics into Lighting Management

In January 2025, Signify unveiled AI-assisted scene generation within the Philips Hue ecosystem, while enterprise platforms integrated predictive maintenance algorithms that flag luminaire degradation before lumen depreciation becomes visible. AI-powered lighting controls are transforming energy management in commercial buildings by using machine learning and predictive analytics to optimize usage, reduce energy consumption by 8%–30%, lower costs, and enhance overall lighting efficiency.

4. Growth of Outdoor and Infrastructure LED Modernization

Smart streetlight systems, incorporating gunshot detection, environmental sensors, and traffic monitoring cameras, are being piloted in cities including Los Angeles, Chicago, and Atlanta, commanding 2–3x revenue premiums versus standard LED street luminaires. Utility-scale solar-LED hybrid systems are also being deployed for pathway and perimeter lighting in logistics parks across the South and West.

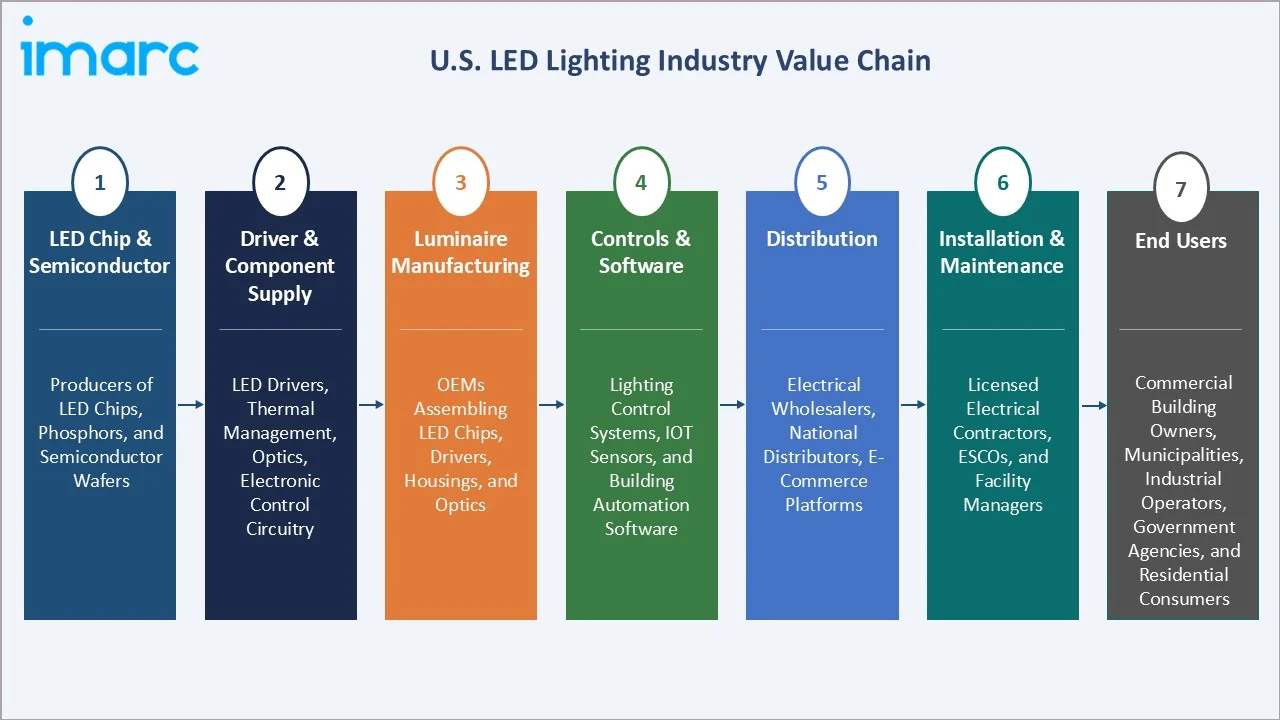

Industry Value Chain Analysis

The U.S. LED lighting value chain spans raw material extraction through end-consumer installation, with each stage populated by specialized operators whose performance directly influences product quality, efficiency, and total cost of ownership.

|

Stage |

Key Players / Examples |

|

LED Chip & Semiconductor |

Producers of LED chips, phosphors, and semiconductor wafers |

|

Driver & Component Supply |

Suppliers of LED drivers, thermal management components, optics, and electronic control circuitry |

|

Luminaire Manufacturing |

OEMs and contract manufacturers that assemble LED chips, drivers, housings, and optics into finished commercial, industrial, and residential luminaire products |

|

Controls & Software |

Developers of lighting control systems, IoT-enabled sensors, dimming technology, and building automation software |

|

Distribution |

Electrical wholesalers, national distributors, home improvement retailers, and e-commerce platforms that source and supply LED products to contractors, specifiers, and end users |

|

Installation & Maintenance |

Licensed electrical contractors, energy service companies (ESCOs), and facility management firms |

|

End Users |

Commercial building owners, municipalities, industrial operators, government agencies, and residential consumers |

Technology Landscape in the U.S. LED Lighting Industry

Advanced Chip-Scale Package (CSP) and Mid-Power LED Technology

Chip-Scale Package LEDs, where the LED die is packaged directly without a carrier, are enabling luminaire designers to achieve unprecedented lumen density in compact form factors. Mid-power LED arrays achieving 200+ lumens per watt at the component level are now commercially available, enabling slim panel and troffer designs that meet stringent DLC Premium efficacy thresholds.

Matter Protocol and Interoperable Smart Lighting

The Matter smart home standard (ratified 2022, major updates 2024) is resolving long-standing interoperability fragmentation by enabling LED luminaires, switches, and sensors from different manufacturers to communicate seamlessly over a unified IP-based protocol. Signify, Acuity Brands, and Lutron have all committed to Matter support in their 2025 product roadmaps, reducing integration friction for smart lighting deployment and expanding the addressable retrofit market.

Recycling and Circular Economy Technology

Advanced LED product recycling programs are emerging in the U.S. in response to growing e-waste concerns. LED luminaires contain recyclable aluminum heat sinks, copper windings, and glass diffusers, with LED drivers containing recoverable circuit board metals. Several major manufacturers piloted manufacturer take-back programs in California and New York in 2024–2025, aligning with proposed EPA extended producer responsibility frameworks for lighting products.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

| Application | Retrofit | 29.6% | 2025 |

| Region | South | 31.4% | 2025 |

By Application

Retrofit dominates the application segment with a 29.6% share in 2025 (equivalent to approximately USD 2.76 Billion). Its dominance reflects the large installed base of legacy fluorescent and HID lighting in commercial buildings, combined with mandatory building energy benchmarking programs in over 30 U.S. cities that incentivize energy-use reduction investments.

To access detailed market analysis, Request Sample

Outdoor LED applications represent 18.7% of the market, growing as municipal LED streetlight conversion programs near completion and smart city infrastructure spending accelerates. Industrial applications hold 14.8%, boosted by the re-shoring of U.S. manufacturing capacity. Office applications account for 12.6%, and retail and hospitality for 9.8%.

Regional Market Insights

The South's market leadership (31.4%, 2025) reflects robust commercial construction activity, large industrial facility footprints in Texas and the Gulf Coast, and utility rebate programs that accelerate LED adoption. Texas alone accounts for over 12% of total U.S. LED lighting demand, driven by a booming commercial real estate market and data center expansion.

|

Region |

Share (2025) |

Key Growth Drivers |

|

South |

31.4% |

Commercial construction, industrial facilities, utility rebates |

|

West |

27.2% |

CA Title 24, smart city initiatives, solar-LED systems |

|

Northeast |

22.1% |

Dense commercial buildings, NYSERDA, Mass Save programs |

|

Midwest |

19.3% |

Industrial re-shoring, agricultural LED, warehouse expansion |

The West is the highest-growth region, with California's Title 24 building energy standards mandating that all installed lighting meet minimum efficacy standards of 65 to 100 lumens per watt, typically achieved through advanced LED technology to maximize output while minimizing energy consumption. Smart city deployments in Los Angeles, San Francisco, and Seattle are also creating premium connected LED infrastructure demand.

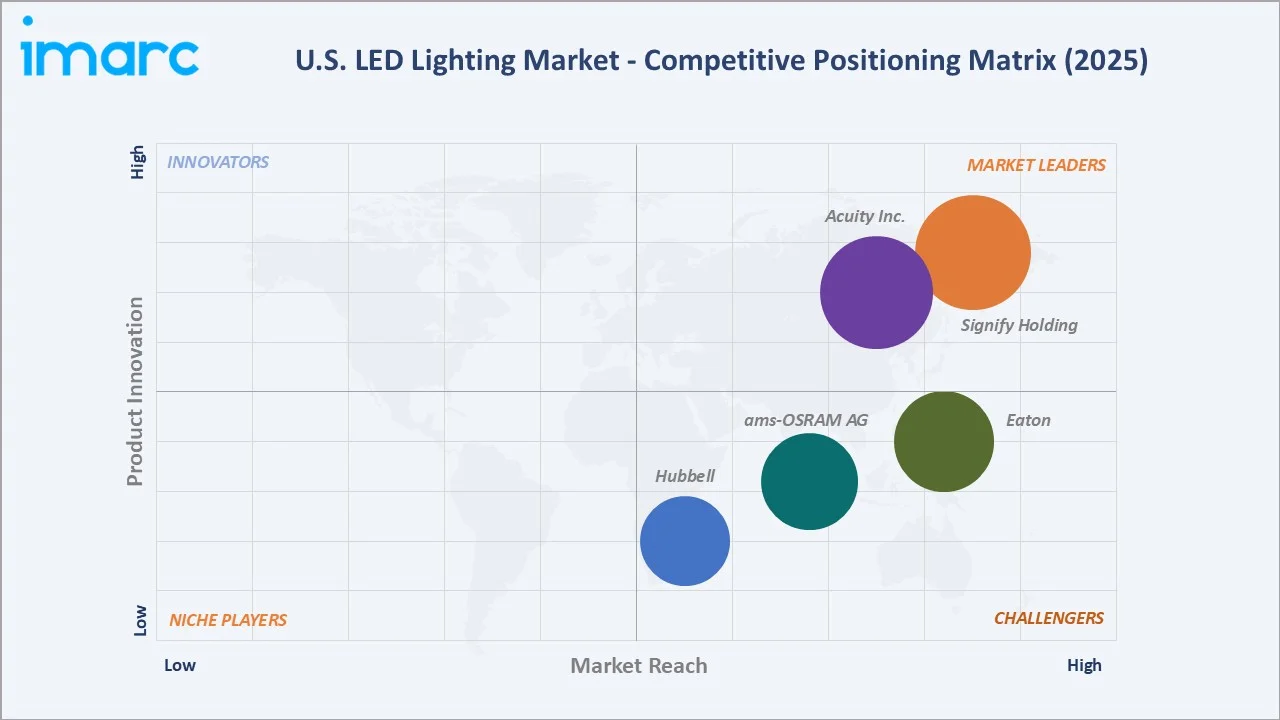

Competitive Landscape

The U.S. LED lighting market exhibits a moderately fragmented structure. The top five manufacturers, Signify Holding, Acuity Inc., Eaton, ams-OSRAM AG, and Hubbell, collectively hold approximately 25–30% of total U.S. market revenue in 2025.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

Signify Holding |

Philips |

Market Leader |

Global smart lighting leader; IoT integration; premium consumer and professional portfolios |

|

Acuity Inc. |

Lithonia Lighting/ Juno, Mark Architectural Lighting, Holophane |

Market Leader |

North America leader; broad commercial, industrial, and outdoor portfolio with advanced controls |

|

Eaton |

Crouse-Hinds |

Strong Challenger |

Industrial, and hazardous-location LED expertise; integrated power management |

|

ams-OSRAM AG |

OSLON, OSCONIQ, SYNIOS, OSRAM OSTAR |

Strong Challenger |

Chip-to-system expertise; automotive and specialty LED technology; architectural lighting |

|

Hubbell |

Chalmit |

Challenger |

Commercial and industrial LED; strong electrical distribution network; controls integration |

A long tail of regional manufacturers, private-label brands, and Chinese import-dependent distributors accounts for the balance, particularly in the residential replacement lamp and low-cost commercial fixture segments.

Key Company Profiles

Signify Holding

Signify Holding, headquartered in Eindhoven (Netherlands) with major North American operations in Burlington, MA, is the world's largest lighting company and holds the leading position in the U.S. LED market through its Philips Hue consumer platform and Interact IoT-enabled professional systems.

- Product Portfolio: Philips Hue (residential smart lighting), Interact Office and Retail (IoT platforms), and Philips professional luminaires for commercial and outdoor applications.

- Recent Developments: In February 2026, Signify won a U.S. patent trial in 2026, with a jury confirming infringement of six LED technology patents and awarding full damages, reinforcing the strength of its intellectual property portfolio.

- Strategic Focus: AI-driven lighting personalization; sustainability via Climate Pledge alignment; solar-LED integration for outdoor markets.

Acuity Inc.

Acuity Inc., headquartered in Atlanta, Georgia, is North America's largest commercial LED lighting manufacturer, operating brands including Lithonia Lighting, Holophane, Peerless, and nLight controls across indoor, outdoor, and industrial segments.

- Product Portfolio: Lithonia (commercial), Holophane (industrial), Mark Architectural Lighting

- Recent Developments: In August 2025, Acuity secured nine LED-based luminaires in the 2025 IES Progress Report. The selected solutions, including LED high bays, downlights, pathway, and healthcare luminaires, underscore advancements in energy-efficient, application-specific LED lighting technologies.

- Strategic Focus: Intelligent spaces platform convergence; Atrius IoT data analytics; DALI-2 and Matter protocol leadership.

Eaton

Eaton's Electrical Americas segment operates the Crouse-Hinds (hazardous-location) brand, serving stadiums, petrochemical, and industrial facility segments in the United States.

- Product Portfolio: Crouse-Hinds hazardous-location luminaires

- Recent Development: In 2026, Eaton Corporation reported strong full-year 2025 performance with total revenue reaching approximately $27.4 billion, reflecting around 10% year-over-year growth driven by robust demand across its electrical businesses, including LED lighting-related solutions within the Electrical Americas segment.

- Strategic Focus: Electrification mega-trend alignment; EV charging canopy LED integration; grid-resilient emergency lighting systems.

Market Concentration Analysis

The U.S. LED lighting market exhibits moderate concentration at the luminaire manufacturing level, with the top five global suppliers holding approximately 25–30% of total U.S. revenue in 2025. A substantial long tail of 1,000+ regional manufacturers, importers, and private-label distributors ensures significant fragmentation, particularly in residential replacement lamps and budget-tier commercial fixtures where Chinese import competition is intense.

Consolidation activity is accelerating, driven by smart lighting R&D capital requirements and the need for broad channel coverage. Between 2020 and 2025, notable transactions included ADLT's acquisition of Cree Lighting and Eaton's integration of Cooper Lighting Solutions. Private equity interest remains high in mid-tier controls and software companies that enable differentiation in the commoditized fixture market.

Investment & Growth Opportunities

Fastest Growing Segments

Smart connected LED systems (estimated 8.5% CAGR through 2034), human-centric lighting for offices and healthcare (12% CAGR), and horticultural LED for indoor agriculture (15% CAGR) represent the three highest-growth investment vectors. Together, these segments address a total addressable market of approximately USD 4.2 billion by 2030.

Infrastructure and Municipal Opportunities

Approximately 42 million streetlights in the U.S. remain unconverted to LED as of 2025, representing a concentrated near-term procurement opportunity estimated at USD 8–12 billion over 2026–2034 when smart-controls integration costs are included. Federal IIJA transportation lighting allocations provide funding certainty for municipal conversion programs, making this a low-risk capital deployment target for lighting manufacturers and installation contractors.

Venture and Institutional Investment Trends

- Key investment themes include AI-powered lighting management SaaS platforms, Li-Fi-enabled LED luminaires for enterprise connectivity, and solid-state lighting for vertical farming and controlled-environment agriculture.

- ESCO structured finance deals, where LED upgrades are financed through guaranteed energy savings, are expanding to Tier-2 and Tier-3 commercial markets, reducing first-cost barriers and accelerating penetration.

Future Market Outlook (2026-2034)

The U.S. LED lighting market is positioned for sustained, broad-based growth through 2034. From a base of USD 9.32 Billion in 2025, the market is projected to reach USD 12.70 Billion by 2034, representing total incremental value creation of USD 3.38 Billion over the forecast decade.

Regulatory evolution, particularly the DOE's continued tightening of efficacy standards, city-level carbon-emissions penalties (NYC Local Law 97, Boston BERDO 2.0), and state net-zero building codes, will drive continuous product reformulation and replacement cycles. Manufacturers achieving DLC Premium and ENERGY STAR certification for smart, high-efficacy systems by 2026 are positioned to capture a disproportionate share of institutional procurement budgets.

Long-term, the market's trajectory is tied to three structural macro-themes: building decarbonization (creating mandatory retrofit cycles), smart infrastructure investment (elevating per-luminaire revenue), and indoor agriculture expansion (opening a new high-growth application). LED lighting sits at the intersection of all three, ensuring resilient demand growth well beyond the forecast period.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and surveys with over 120 industry participants in 2024–2025, including LED lighting manufacturers, electrical distributors, energy services companies, facility managers, and procurement officers across the South, West, Northeast, and Midwest regions.

Secondary Research

Secondary research encompassed a systematic review of company annual reports, DOE Solid-State Lighting program publications, DesignLights Consortium (DLC) qualification data, ENERGY STAR program statistics, utility rebate databases, trade publications (LEDs Magazine, Architectural SSL), and publicly available financial data. Over 200 secondary sources were reviewed and triangulated.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting approaches, incorporating DOE lamp shipment data, construction starts, utility rebate disbursement trends, and historical market evolution. A base-case CAGR of 3.49% reflects consensus analyst estimates validated against reported manufacturer revenue growth rates.

U.S. LED Lighting Market Report Scope

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Applications Covered | Retrofit, Retail and Hospitality, Outdoor, Offices, Architectural, Homes, Industrial |

| Regions Covered | Northeast, Midwest, South, West |

| Comapnies Covered | Signify Holding, Acuity Inc., Eaton, ams-OSRAM AG, Hubbell, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the U.S. LED lighting market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the U.S. LED lighting market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the U.S. LED lighting industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the U.S. LED Lighting Market Report

The U.S. LED lighting market reached USD 9.32 Billion in 2025 and is projected to reach USD 12.70 Billion by 2034.

The market is expected to grow at a CAGR of 3.49% during the forecast period from 2026 to 2034, supported by energy efficiency mandates, smart lighting adoption, and infrastructure investment.

The South leads the market with a 31.4% share in 2025, driven by strong commercial construction activity, large industrial facility footprints, and utility-funded LED rebate programs in Texas, Florida, and Georgia.

The retrofit segment holds the largest application share at 29.6% in 2025 (approx. USD 2.76 Billion), driven by commercial building owners upgrading legacy fluorescent and HID systems.

Key players include Signify Holding, Acuity Inc., Eaton, ams-OSRAM AG, and Hubbell.

Key drivers include federal energy efficiency mandates (DOE 45-lumen/watt rule), utility rebate programs disbursing over USD 1.2 billion annually, smart building and IoT integration requirements, and the Infrastructure Investment and Jobs Act funding for transportation lighting upgrades.

Smart connected LED systems are growing at an estimated 8.5% CAGR through 2034, elevated by IoT platform integration, DALI-2 and Matter protocol standardization, and AI-driven energy management platforms that deliver 15–20% additional energy savings beyond conventional LED installations.

High-growth opportunities include AI-powered lighting management SaaS platforms, human-centric and horticultural LED systems, municipal streetlight smart-conversion programs (42 million unconverted fixtures), and ESCO-structured commercial retrofit financing targeting Tier-2 and Tier-3 markets.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)