U.S. Liquid Biopsy Market Size, Share, Trends and Forecast by Product and Service, Circulating Biomarker, Cancer Type, End User, and Region, 2026-2034

U.S. Liquid Biopsy Market Size, Share, Trends & Forecast (2026-2034)

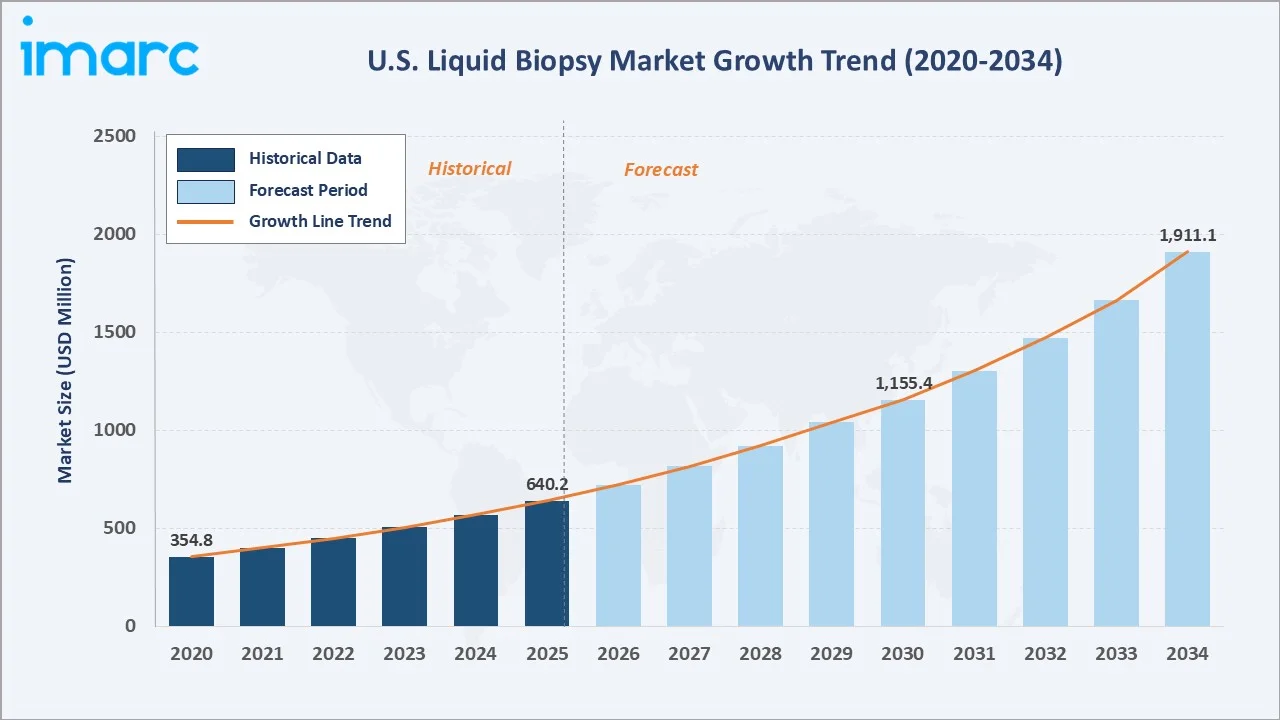

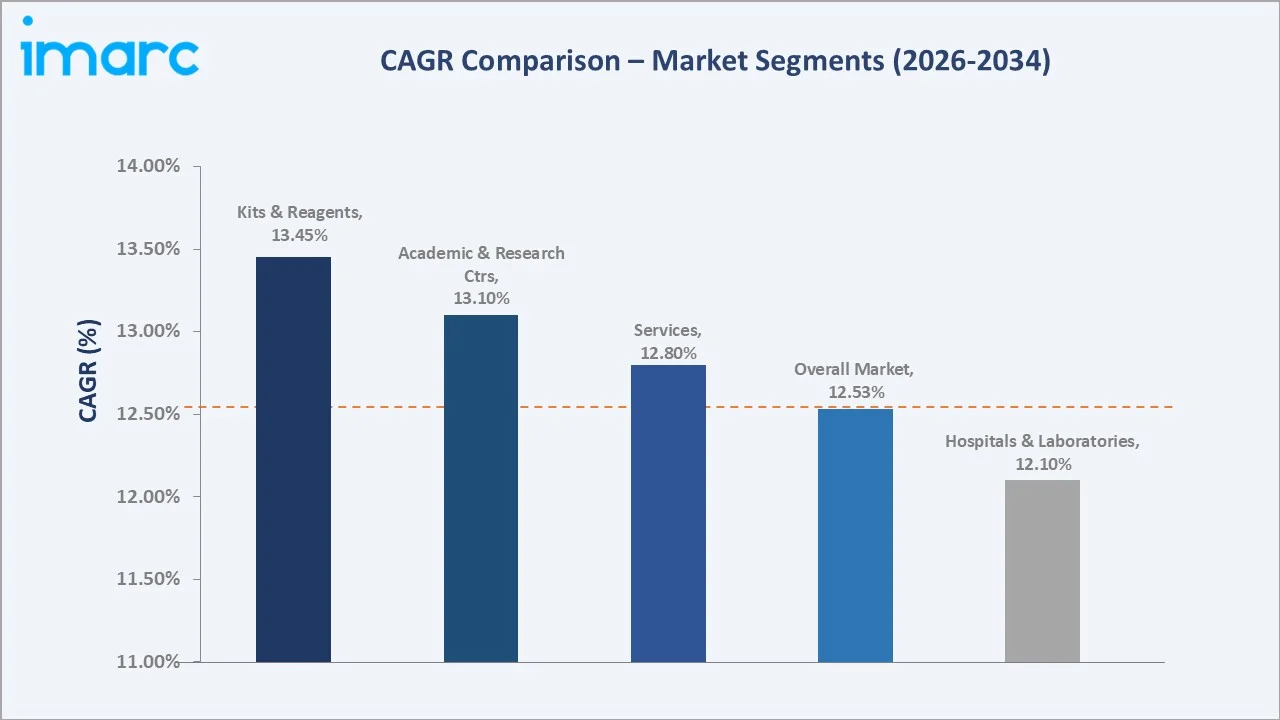

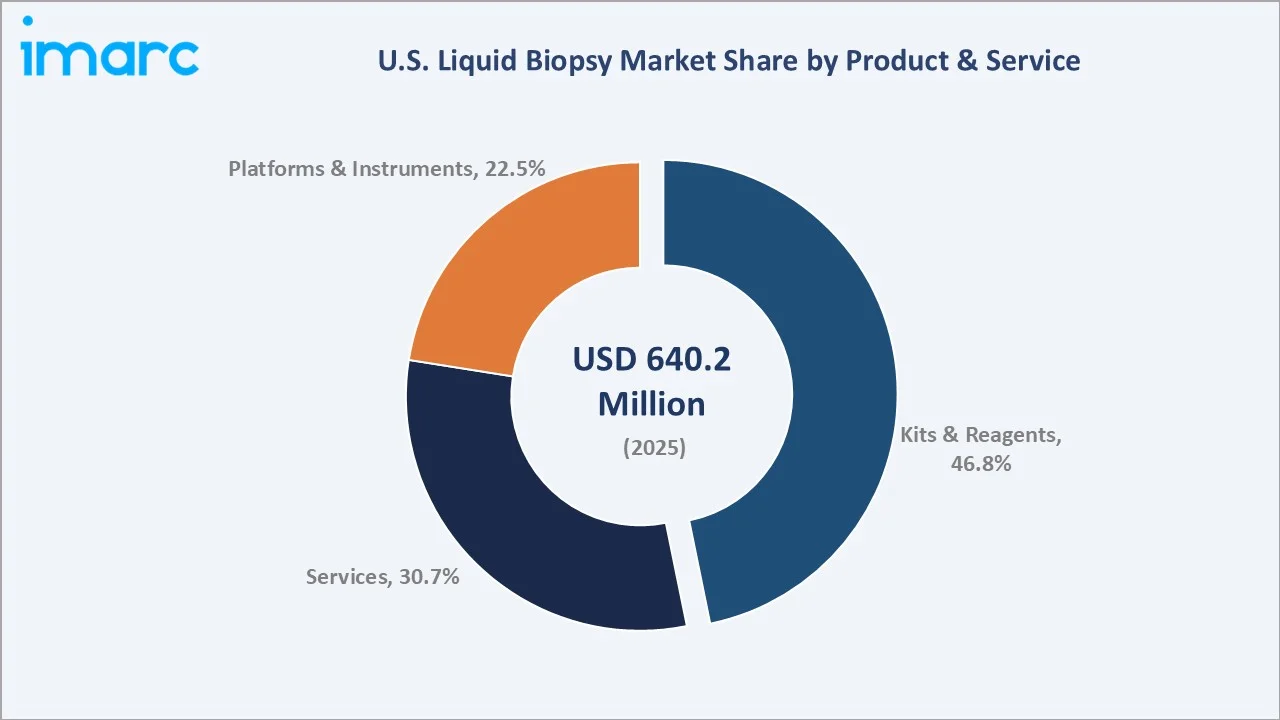

The U.S. liquid biopsy market reached USD 640.2 Million in 2025 and is projected to reach USD 1,911.1 Million by 2034, growing at a CAGR of 12.53% during 2026-2034. Rapid advances in next-generation sequencing (NGS), expanding clinical adoption of circulating tumor DNA (ctDNA) assays, and increasing reimbursement coverage are driving exceptional growth.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 640.2 Million |

|

Forecast Market Size (2034) |

USD 1,911.1 Million |

|

CAGR (2026-2034) |

12.53% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

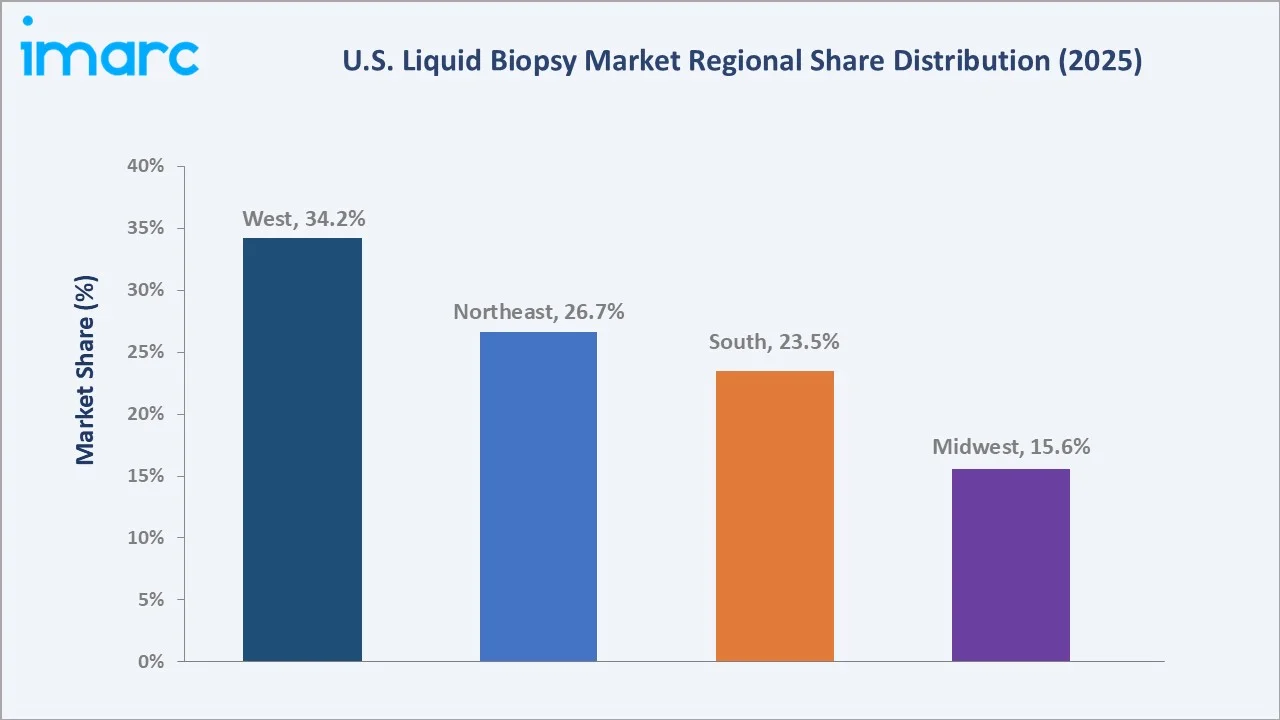

Largest Region |

West (34.2% share, 2025) |

|

Fastest Growing Region |

West |

The West dominates with a 34.2% share in 2025, driven by proximity to leading biotech innovators and research institutions. Kits and reagents lead the product and service category at 46.8%, reflecting the recurring revenue model of consumable-driven testing workflows.

To get more information on this market, Request Sample

With applications expanding from advanced non-small cell lung cancer (NSCLC) profiling into colorectal, breast, prostate, and multi-cancer screening, the U.S. liquid biopsy market is entering a phase of accelerated clinical integration, supported by an expanding roster of FDA-approved companion diagnostic tests and growing CMS reimbursement coverage.

Executive Summary

The U.S. liquid biopsy market is undergoing transformative growth, driven by the convergence of precision oncology, NGS cost reduction, and expanded FDA approval pathways. The market reached USD 640.2 Million in 2025 and is forecast to exceed USD 1,911.1 Million by 2034, reflecting a robust CAGR of 12.53%, among the highest in the broader in vitro diagnostics (IVD) sector.

The West leads with a 34.2% share, home to Guardant Health (Palo Alto), GRAIL (Menlo Park), and Illumina (San Diego). The Northeast commands 26.7%, anchored by major academic medical centers including Memorial Sloan Kettering, Dana-Farber, and Johns Hopkins, which drive clinical protocol adoption and payer coverage decisions.

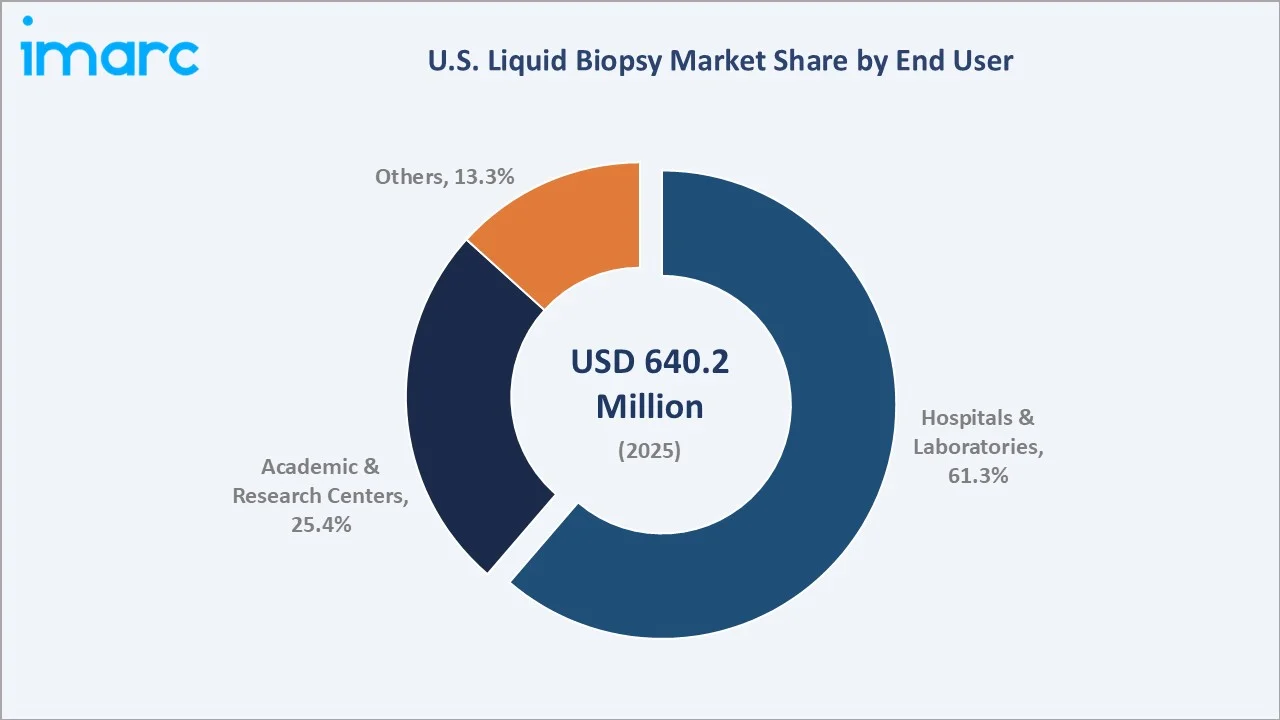

Hospitals and laboratories dominate end-user demand at 61.3% as centralized laboratory processing of liquid biopsy panels remains the standard workflow. Kits and reagents capture 46.8% of product and service revenue, driven by the consumable-intensive nature of NGS-based ctDNA workflows. GRAIL's Galleri multi-cancer early detection test, launched commercially in 2021, represents the most significant category expansion event of the decade, potentially driving billions in new market value as population screening applications mature.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (End User) |

Hospitals and Laboratories – 61.3% (2025) |

|

Largest Segment (Product & Service) |

Kits and Reagents – 46.8% (2025) |

|

Largest Region |

West – 34.2% (2025) |

|

Fastest Growing Region |

West (biotech hub concentration + genomics investment) |

|

Top Companies |

Guardant Health, Inc., F. Hoffmann-La Roche Ltd, GRAIL, Inc., Illumina, Inc., and Biodesix |

Key Analytical Observations Supporting the Above Data:

- Hospitals and laboratories account for 61.3% of the U.S. liquid biopsy market in 2025, reflecting the centralized lab processing model where high-complexity NGS panels are run in CLIA-certified reference laboratories serving oncology networks.

- Kits and reagents lead the product and service category at 46.8% in 2025, underpinned by the recurring consumable revenue model of sequencing-based ctDNA assays, which require fresh reagent inputs for every patient sample processed.

- The West holds 34.2% of the U.S. market in 2025, led by California's concentration of liquid biopsy innovators, venture-funded genomics companies, and the University of California health system's 15+ academic medical centers.

- The multi-cancer early detection (MCED) segment is the fastest-growing application, with GRAIL's Galleri targeting 50+ cancer types from a single blood draw, a potential USD 30+ billion total addressable market if population-scale screening is adopted.

- CMS's Local Coverage Determination (LCD) for ctDNA-based MRD testing in colorectal and other solid tumors, finalized in 2024, is accelerating adoption by removing the last major reimbursement barrier for hospital-based testing programs.

U.S. Liquid Biopsy Market Overview

Liquid biopsy is a non-invasive diagnostic approach that analyses cancer-derived biomarkers, including circulating tumor DNA (ctDNA), circulating tumor cells (CTCs), cell-free RNA (cfRNA), and exosomes, from blood and other bodily fluids. It provides real-time genomic information without the need for tissue biopsy, enabling dynamic molecular monitoring across the full oncology care continuum from early detection through treatment and recurrence surveillance.

3.webp)

The U.S. liquid biopsy ecosystem is uniquely positioned globally, benefiting from the highest concentration of FDA-approved companion diagnostics, a mature reimbursement infrastructure, and world-class academic medical centers that serve as early adopters and protocol setters. Macroeconomic factors, including the National Cancer Plan (2023), the Cancer Moonshot initiative extension, and NGS cost parity with traditional molecular diagnostics, are primary structural growth drivers underpinning the 12.53% CAGR forecast.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

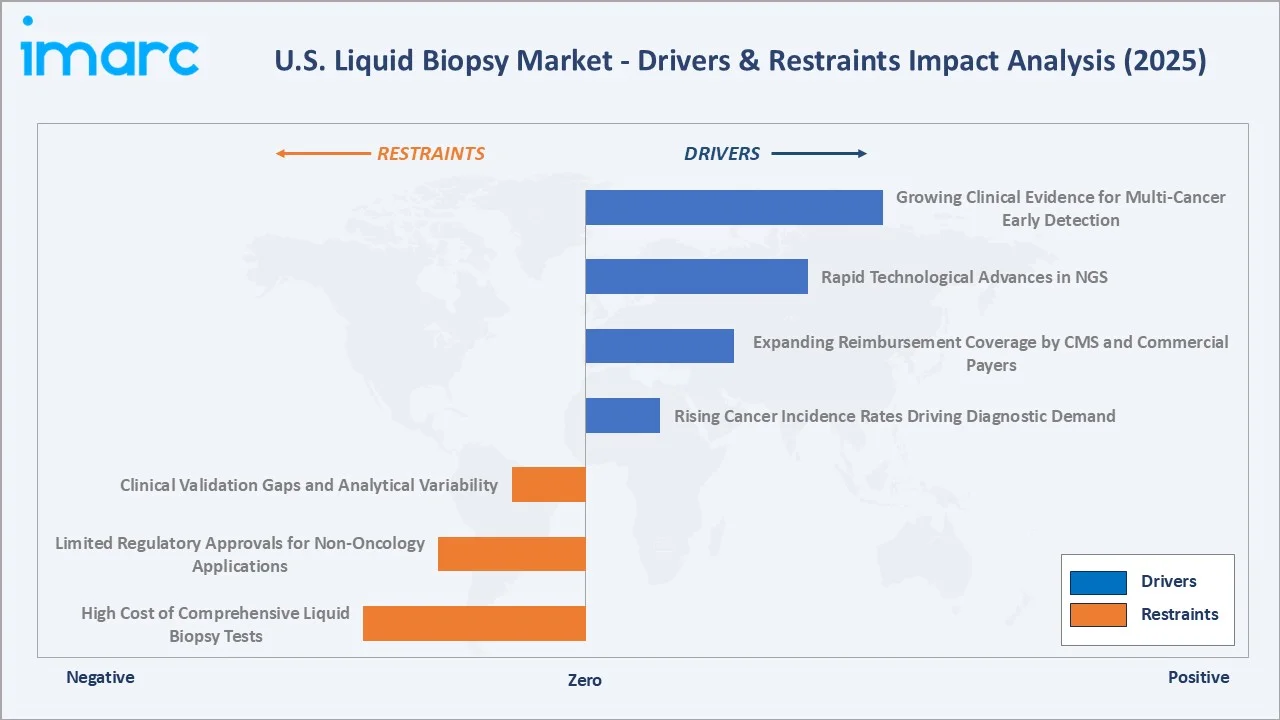

- Rising Cancer Incidence Rates Driving Diagnostic Demand: The American Cancer Society projects 2.1 million new cancer diagnoses and 626,000 cancer deaths in the U.S. in 2026. Liquid biopsy directly addresses the unmet need for earlier, more accurate, and less invasive cancer detection, particularly for NSCLC, colorectal, and breast cancers.

- Expanding Reimbursement Coverage by CMS and Commercial Payers: Guardant Health announced that its Shield blood test for colorectal cancer screening received Advanced Diagnostic Laboratory Test (ADLT) status from CMS. The test will be reimbursed at USD 1,495 during an initial nine-month period starting April 2025.

- Rapid Technological Advances in NGS: As next-generation sequencing costs decline, Illumina is driving greater affordability and accessibility of NGS through ongoing innovation, with the average cost per genome dropping by approximately 96% since 2013.

- Growing Clinical Evidence for Multi-Cancer Early Detection: The Galleri multi-cancer early detection test has been validated in The Lancet and Annals of Oncology, demonstrating strong clinical credibility. It shows high performance with 99.6% specificity, a low false-positive rate of 0.4%, and a positive predictive value of 61.6%, along with 93.4% accuracy in identifying the cancer’s origin.

Market Restraints

- High Cost of Comprehensive Liquid Biopsy Tests: Comprehensive genomic profiling (CGP) liquid biopsy panels range from USD 3,000 to USD 7,500 per test, creating affordability barriers for uninsured and underinsured patients.

- Limited Regulatory Approvals for Non-Oncology Applications: The majority of FDA-approved liquid biopsy tests are limited to cancer therapy selection in specific tumor types, with limited coverage of recurrence surveillance, MRD monitoring, and non-cancer applications.

- Clinical Validation Gaps and Analytical Variability: CAP proficiency testing surveys indicate a significant coefficient of variation in ctDNA quantification across platforms, creating clinical uncertainty that slows protocol adoption by oncologists seeking consistent, actionable results.

Market Opportunities

- Companion Diagnostic Co-Development with Pharma: The FDA approved KRAS G12C CDx for sotorasib (AMG-510) and EGFR exon 20 CDx for mobocertinib using ctDNA-based testing. With 400+ oncology drugs in Phase 3 trials requiring companion diagnostics, the CDx co-development pipeline represents a USD 400+ million revenue opportunity through 2034.

- Minimal Residual Disease Monitoring Expansion: ctDNA-based MRD monitoring in curative-intent colorectal, breast, and lung cancer is the fastest-growing application, with the DYNAMIC and CIRCULATE-Japan trials demonstrating MRD-guided chemotherapy de-escalation.

- AI and Bioinformatics-Enhanced Interpretation: Machine learning models integrating ctDNA patterns with clinical metadata are demonstrating superior cancer signal-to-noise discrimination compared to conventional bioinformatics pipelines. In April 2026, Tempus launched an automated active follow-up service that continuously tracks patient data and updates care recommendations in line with evolving clinical guidelines.

Market Challenges

- Tumor Heterogeneity and False Negative Rates: Stage I-II solid tumors shed minimal ctDNA into the bloodstream, with detection rates of 30-55% for early-stage disease depending on tumor type and burden. False negative liquid biopsy results in early-stage patients risk clinical under-treatment, requiring parallel tissue biopsy confirmation.

- Complex Regulatory Pathway for LDT-to-IVD Transition: The FDA's Laboratory Developed Test (LDT) final rule requires liquid biopsy laboratories previously operating under CLIA LDT exemptions to pursue formal FDA clearance or approval. This regulatory transition creates a compliance burden for smaller clinical laboratories.

Emerging Market Trends

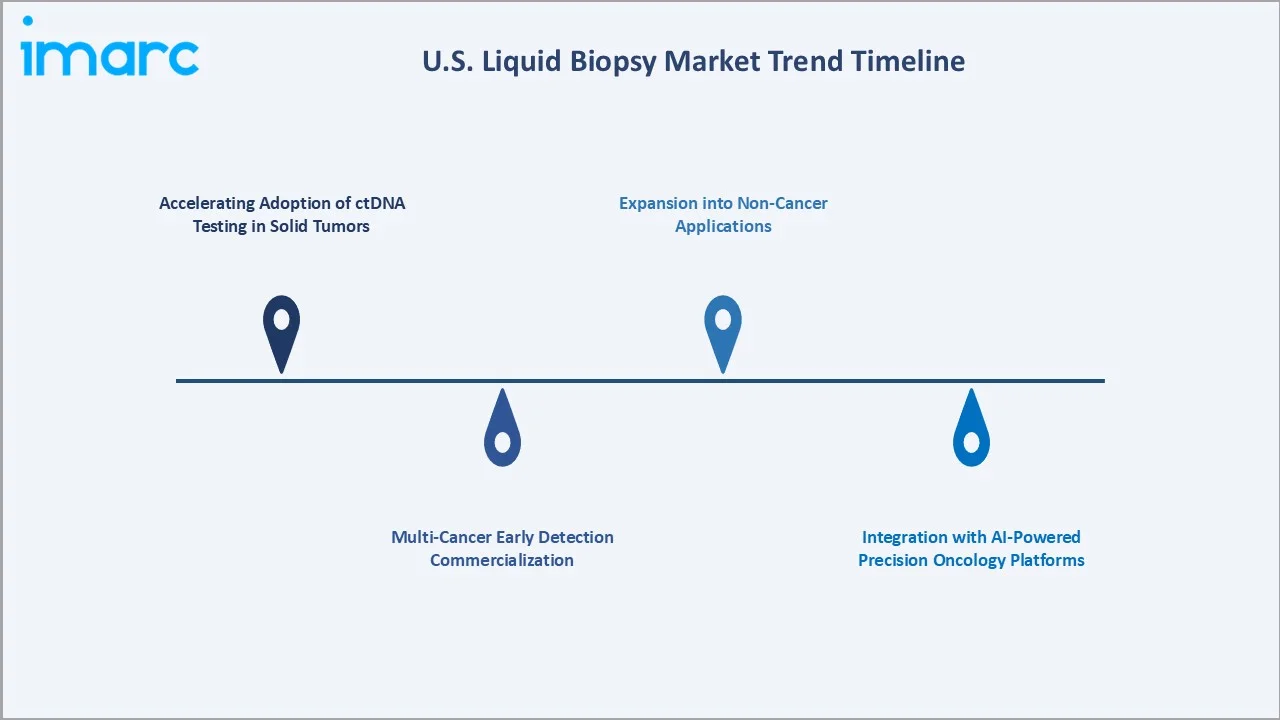

1. Accelerating Adoption of ctDNA Testing in Solid Tumors

ctDNA-based comprehensive genomic profiling became the standard of care for advanced NSCLC and colorectal cancer therapy selection by 2024, with National Comprehensive Cancer Network (NCCN) guidelines recommending ctDNA testing when tissue is unavailable or insufficient. Galleri test from GRAIL for multi-cancer early detection (MCED) reported that over 370,000 Galleri tests had been ordered since its launch in 2021.

2. Multi-Cancer Early Detection Commercialization

GRAIL and NHS England completed enrollment of 140,000 participants in the NHS-Galleri trial, the largest-ever study of a multi-cancer early detection (MCED) test involving healthy individuals aged 50–77. The randomized trial evaluates the clinical utility of the Galleri blood test alongside standard screening to determine its effectiveness in detecting cancer earlier at a population level.

3. Integration with AI-Powered Precision Oncology Platforms

Liquid biopsy data is increasingly being integrated with AI-driven oncology platforms that combine ctDNA results with electronic health records, imaging data, and treatment history to generate personalized therapy recommendations. Tempus AI's TIME Trial platform demonstrate that integrated liquid + tissue + clinical data models improve therapy match rates by approximately 23% compared to single-modality genomic testing.

4. Expansion into Non-Cancer Applications

Cell-free DNA analysis is expanding beyond oncology into organ transplant rejection surveillance (CareDx's AlloSure), prenatal anomaly detection (Natera's Panorama), and infectious disease monitoring. While oncology represents the majority of current U.S. liquid biopsy revenue, non-oncology applications are also expected to reach high revenue over the forecast period.

Industry Value Chain Analysis

The U.S. liquid biopsy value chain spans specimen collection through clinical reporting, with each stage characterized by high specialization, regulatory complexity, and strong vertical integration tendencies among leading diagnostic companies seeking to control the full testing workflow from blood draw to physician report.

|

Stage |

Key Players / Examples |

|

Sample Collection |

Whole blood draws, urine, CSF, saliva, and pleural fluid collection; cfDNA/ctDNA stabilization tubes and preservatives. |

|

Pre-Analytical Processing |

Plasma/serum separation, nucleic acid (cfDNA, cfRNA, exosomal RNA) extraction, and quality normalization |

|

Assay Development |

ctDNA, ctRNA, CTC, exosome, and methylation assay design; multi-cancer early detection (MCED) panels |

|

Analysis & Testing |

Next-generation sequencing (NGS), digital PCR, qPCR |

|

Clinical Reporting |

CLIA-certified test execution, CAP accreditation, structured clinical reports, oncologist dashboards, and EHR integration |

|

End Users & Payers |

Oncologists, pathologists, academic researchers; CMS, commercial insurers, hospital networks |

Technology Landscape in the U.S. Liquid Biopsy Industry

Next-Generation Sequencing (NGS) Platforms

Illumina's NovaSeq X and NextSeq 550 Dx platforms provide the sequencing infrastructure underpinning Foundation Medicine's FoundationOne Liquid CDx, Guardant360 CDx, and GRAIL's Galleri. Error suppression technologies, including Unique Molecular Identifiers (UMIs) and duplex sequencing (TwinStrand Biosciences), achieve variant allele frequency detection at 0.001%, enabling sub-clone detection critical for MRD monitoring.

Digital PCR and Methylation-Based Detection

Digital droplet PCR (ddPCR, Bio-Rad QX600) provides highly sensitive, targeted ctDNA quantification for known variants, widely used in clinical trials and MRD monitoring. Methylation-based detection, employed by GRAIL's Galleri identifies cancer-of-origin-specific methylation patterns in cfDNA, enabling multi-cancer detection without prior mutation profiling.

Circulating Tumor Cell (CTC) Technology

While ctDNA dominates, CTC-based platforms (CELLSEARCH, Menarini Silicon Biosystems) retain clinical utility in metastatic breast, prostate, and colorectal cancer prognosis. CTC enumeration is FDA-cleared for prognostic use in these indications, and CTC-derived whole genome sequencing is an emerging research tool for characterizing intra-tumoral heterogeneity unavailable in cell-free DNA analysis.

Exosome and Extracellular Vesicle Profiling

Exosome-based liquid biopsy is an emerging frontier, with companies including Exosome Diagnostics and Exai Bio developing exosomal RNA and protein cargo profiling for cancer detection. Exosome analysis provides unique tumor biology insights complementary to ctDNA, with potential applications in glioblastoma (crossing the blood-brain barrier) and pancreatic cancer, where ctDNA shedding is low.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product and Service | Kits and Reagents | 46.8% | 2025 |

| Circulating Biomarker | 🔒 | 🔒 | 2025 |

| Cancer Type | 🔒 | 🔒 | 2025 |

| End User | Hospitals and Laboratories | 61.3% | 2025 |

| Region | West | 34.2% | 2025 |

By End User

Hospitals and laboratories dominate end-user demand with a 61.3% share in 2025. This leadership reflects the centralized laboratory processing model of NGS-based liquid biopsy, where CLIA-certified high-complexity reference laboratories perform comprehensive genomic profiling on behalf of hospital oncology departments.

To access detailed market analysis, Request Sample

Academic and research centers hold a 25.4% share, playing a disproportionately influential role as clinical evidence generators. Institutions, including MD Anderson Cancer Center, Memorial Sloan Kettering, Dana-Farber Cancer Institute, and Stanford Cancer Institute, serve as protocol-setting early adopters whose liquid biopsy utilization patterns establish national standards of care.

By Product and Service

Kits and reagents lead the product and service category with a 46.8% share in 2025, reflecting the consumable-intensive nature of NGS workflows where each patient sample requires a fresh reagent kit for cfDNA extraction, library preparation, and sequencing.

Services capture a 30.7% share, encompassing laboratory testing services, bioinformatics interpretation, and physician reporting offered by commercial reference laboratories operating under certified send-out testing models. Platforms and instruments account for 22.5%, representing sequencers, digital PCR instruments, and automated liquid handling systems - a capital equipment category with strong follow-on consumable attachment rates.

Regional Market Insights

The West's market leadership (34.2%, 2025) is driven by California's unique concentration of liquid biopsy innovators. Guardant Health (South San Francisco), GRAIL (Menlo Park), Illumina (San Diego), and Roche Sequencing Solutions (Pleasanton) are located in the western region, creating a self-reinforcing innovation cluster.

|

Region |

Share (2025) |

Key Growth Drivers |

|

West |

34.2% |

Biotech hub density, leading research hospitals, and early technology adoption |

|

Northeast |

26.7% |

Academic medical centers, dense oncology networks, and payer coverage expansion |

|

South |

23.5% |

Growing cancer incidence, hospital system expansion, and Medicaid broadening |

|

Midwest |

15.6% |

University hospital adoption, large integrated health systems |

The Northeast (26.7%) represents the second-largest and most clinically mature region. Foundation Medicine (Cambridge, MA), NeoGenomics (Fort Myers with Northeast operations), and Tempus AI (Chicago's influence extends to Northeast academic accounts) all have significant Northeast market presence.

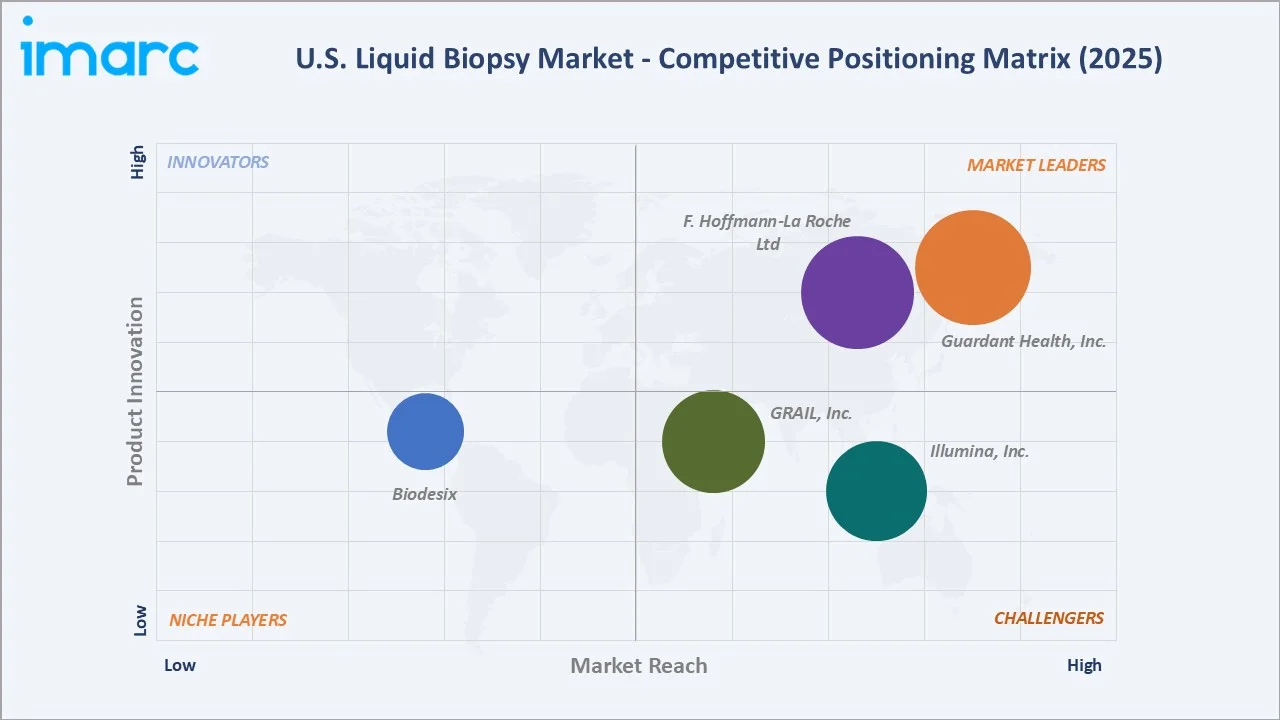

Competitive Landscape

The U.S. liquid biopsy market exhibits moderate-to-high concentration among FDA-approved companion diagnostics, with Guardant Health, Inc. and F. Hoffmann-La Roche Ltd collectively commanding approximately 55-60% of CDx-indicated liquid biopsy test volume in 2025.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

Guardant Health, Inc. |

Guardant360 Liquid, Guardant360 CDx |

Market Leader |

First FDA-approved CDx; comprehensive genomic profiling |

|

F. Hoffmann-La Roche Ltd |

FoundationOne Liquid CDx |

Market Leader |

Significant CDx label; global Roche distribution |

|

GRAIL, Inc. |

Galleri |

Strong Challenger |

Multi-cancer early detection |

|

Illumina, Inc. |

TruSight Oncology 500 ctDNA v2 (RUO) |

Strong Challenger |

NGS platform dominance; end-to-end sequencing ecosystem |

|

Biodesix |

GeneStrat NGS, GeneStrat ddPCR, VeriStrat, Nodify XL2, Nodify CDT |

Niche Player |

Lung cancer specialty; rapid turnaround diagnostic service |

However, the broader market, including LDT-based testing, MRD monitoring, and multi-cancer early detection, is significantly fragmented, with 80+ CLIA-certified laboratories offering some form of ctDNA testing.

Key Company Profiles

Guardant Health, Inc.

Guardant Health is a Palo Alto, California-based precision oncology company and the inventor of the Guardant360 liquid biopsy platform. The company pioneered the clinical adoption of comprehensive ctDNA profiling in advanced solid tumors, and its Guardant360 CDx received the first FDA approval for pan-solid tumor comprehensive genomic profiling from plasma.

- Product Portfolio: Guardant360 Liquid, Guardant360 CDx

- Recent Developments: In March 2026, Guardant Health, Inc. announced it will present 28 scientific abstracts at AACR 2026, highlighting advancements in tumor typing, therapy selection, and the expanded utility of both multi‑omic tissue and liquid biopsy testing.

- Strategic Focus: Population-scale cancer screening; MRD monitoring expansion; therapy companion diagnostic pipeline with pharma partners.

F. Hoffmann-La Roche Ltd

F. Hoffmann-La Roche Ltd, headquartered in Basel, Switzerland. FoundationOne Liquid CDx was developed by Foundation Medicine, Inc. (a Roche subsidiary). The broadest FDA-approved liquid biopsy companion diagnostic, analyzing more than 300 cancer-related genes.

- Product Portfolio: FoundationOne Liquid CDx (comprehensive genomic profiling).

- Recent Developments: In November 2024, the U.S. FDA approved FoundationOne Liquid CDx as a companion diagnostic for non‑small cell lung cancer (NSCLC). This liquid biopsy uses next‑generation sequencing of circulating tumor DNA to analyze over 300 cancer‑related genes.

- Strategic Focus: CDx co-development with pharmaceutical companies; Roche diagnostic ecosystem integration; oncology data analytics platform expansion.

Market Concentration Analysis

The U.S. liquid biopsy market exhibits a dual concentration structure. At the FDA-approved CDx level, the market is highly concentrated; Guardant Health, Inc. and F. Hoffmann-La Roche Ltd collectively account for approximately 55-60% of companion diagnostic testing volume, with Illumina, Inc.’s platform underlying a significant proportion of third-party testing.

Below the CDx tier, the market is highly fragmented, with over 80 CLIA-certified laboratories offering LDT-based liquid biopsy panels, particularly for research use and off-label clinical applications. The FDA's LDT final rule (2024) is expected to consolidate this segment by requiring formal FDA clearance or approval, which will favor well-capitalized companies with dedicated regulatory teams over smaller specialty laboratories.

Consolidation activity is accelerating. Roche's 2018 acquisition of Foundation Medicine for a total transaction value of USD 2.4 billion signals the strategic value of liquid biopsy assets. Between 2020 and 2025, significant M&A and investment transactions exceeding USD 100 million reshaped the competitive map, including Exact Sciences' acquisitions and NeoGenomics' platform expansion investments.

Investment & Growth Opportunities

Fastest Growing Segments

Multi-cancer early detection (estimated CAGR 28%), ctDNA-based MRD monitoring (22% CAGR), and AI-integrated liquid biopsy analytics platforms (18% CAGR) represent the three highest-growth investment vectors through 2034. Together, these emerging applications address a total addressable market of approximately USD 1.4 billion within the broader liquid biopsy space by 2030.

Emerging Market Expansion

Community oncology practices - representing approximately 80% of U.S. cancer care but historically underserved by liquid biopsy adoption - are an emerging market opportunity. Simplified, point-of-care ctDNA testing platforms designed for lower-complexity laboratory settings could expand testing access to the approximately 1,200 community oncology practice sites across the country, adding an incremental USD 350+ million revenue opportunity by 2034.

Venture and Institutional Investment Trends

- Key investment themes include MCED test clinical validation funding, AI-driven bioinformatics platforms, ctDNA-based therapy response monitoring, and cfRNA/methylation detection technology development.

- Pharma co-investment in liquid biopsy CDx development is accelerating, with 12+ pharmaceutical companies entering CDx co-development agreements with liquid biopsy companies in 2023-2024.

- Federal funding through NCI's Cancer Moonshot initiative allocated USD 125 million for liquid biopsy research in 2023-2025, supporting MCED trial infrastructure and MRD monitoring validation studies.

Future Market Outlook (2026-2034)

The U.S. liquid biopsy market is positioned for sustained, high-growth expansion through 2034. From a base of USD 640.2 Million in 2025, the market is projected to reach USD 1,911.1 Million by 2034, representing total incremental value creation of approximately USD 1.27 Billion over the forecast decade at a CAGR of 12.53%.

The structural catalysts defining the market's trajectory include CMS coverage expansion - if Galleri or equivalent MCED tests receive CMS population screening coverage, annual testing volumes could exceed 10 million by 2030, fundamentally transforming the market's scale. Second, the NGS cost parity trend will continue, with whole-genome cfDNA sequencing costs projected to fall below USD 50 by 2030, enabling broader clinical utility at lower reimbursement thresholds.

Long-term, liquid biopsy's trajectory is tied to the broader precision medicine paradigm - as comprehensive multi-omic patient profiling becomes standard in clinical oncology, liquid biopsy will serve as the preferred real-time molecular monitoring tool due to its non-invasive, repeatable, and tumor-heterogeneity-capturing characteristics unavailable from single-site tissue biopsy.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and surveys with over 120 industry participants in 2024–2025, including liquid biopsy test developers, clinical laboratory directors, oncologists, hospital procurement officers, insurance medical directors, and healthcare policy specialists across all four U.S. census regions.

Secondary Research

Secondary research encompassed a systematic review of company SEC filings and earnings reports, FDA 510(k) and PMA approval databases, CMS LCD and NCD coverage decisions, NIH ClinicalTrials.gov registry data, peer-reviewed publications (NEJM, Lancet Oncology, JCO, Nature Medicine), trade publications (GenomeWeb, Dark Daily, Precision Oncology News), and analyst databases (IQVIA, Citeline).

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting methodologies, incorporating oncology test volume data, NGS cost trajectory models, reimbursement coverage expansion rates, and historical market growth from comparable diagnostic categories. A base-case CAGR of 12.53% reflects consensus analyst projections validated against reported company revenue growth rates and FDA approval pipeline analysis.

U.S. Liquid Biopsy Market Report Scope

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Product and Services Covered | Kits and Reagents, Platforms and Instruments, Services |

| Circulating Biomarkers Covered | Circulating Tumor Cells, Extracellular Vesicles, Circulating Tumor DNA, Others |

| Cancer Types Covered | Lung Cancer, Breast Cancer, Colorectal Cancer, Prostate Cancer, Liver Cancer, Others |

| End Users Covered | Hospitals and Laboratories, Academic and Research Centers, Others |

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered | Guardant Health, Inc., F. Hoffmann-La Roche Ltd, GRAIL, Inc., Illumina, Inc., Biodesix, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the U.S. liquid biopsy market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the U.S. liquid biopsy market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the U.S. liquid biopsy industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the U.S. Liquid Biopsy Market Report

The U.S. liquid biopsy market reached USD 640.2 Million in 2025 and is forecast to reach USD 1,911.1 Million by 2034.

The market is projected to grow at a CAGR of 12.53% during the forecast period 2026-2034, one of the highest in the in vitro diagnostics sector.

The West leads with a 34.2% share in 2025, driven by California's concentration of liquid biopsy innovators and world-class oncology centers.

Hospitals and laboratories dominate with a 61.3% market share in 2025, reflecting centralised NGS-based ctDNA panel processing in CLIA-certified reference laboratories.

Kits and reagents lead with a 46.8% share in 2025, driven by the recurring consumable revenue model of sequencing-based ctDNA workflows.

Key players include Guardant Health, Inc., F. Hoffmann-La Roche Ltd, GRAIL, Inc., Illumina, Inc., and Biodesix.

Guardant360 CDx (Guardant Health, Inc.) and FoundationOne Liquid CDx (F. Hoffmann-La Roche Ltd) are the two leading FDA-approved liquid biopsy companion diagnostics.

GRAIL's Galleri targets 50+ cancers from a single blood draw. CMS coverage could drive annual testing volumes exceeding 10 million by 2030, representing a transformative market expansion.

Key challenges include high test costs, limited early-stage sensitivity, complex LDT regulatory transition requirements, and clinical evidence gaps for non-oncology applications.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)