United States Mattress Market Size, Share, Trends and Forecast by Product, Distribution Channel, Size, Application, and Region, 2026-2034

United States Mattress Market Size, Share, Trends & Forecast (2026-2034)

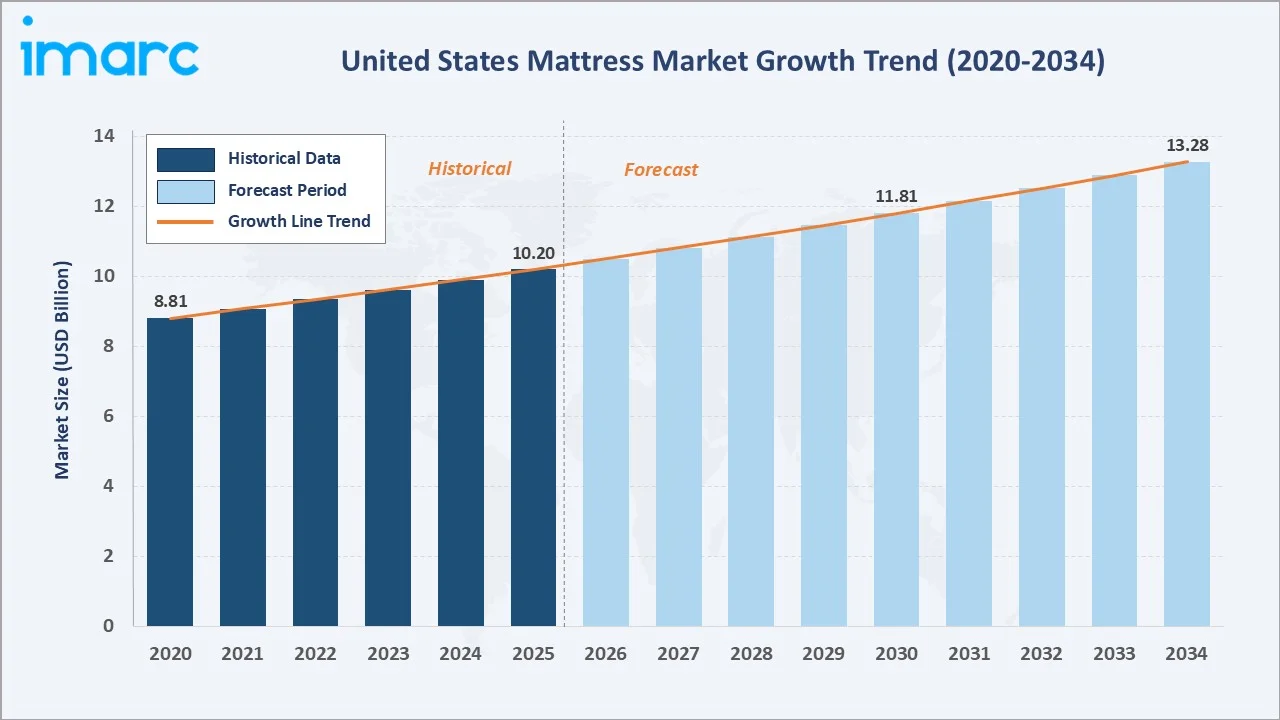

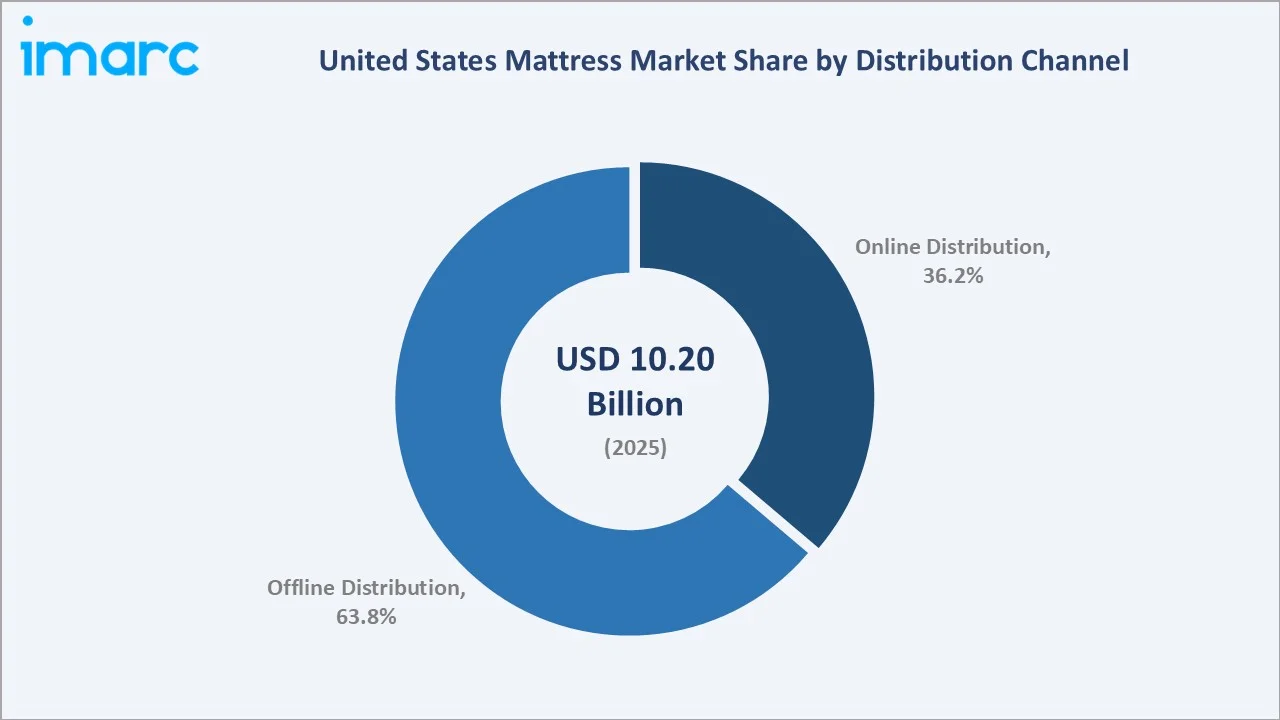

The United States mattress market size reached USD 10.20 Billion in 2025 and is projected to reach USD 13.28 Billion by 2034, exhibiting a CAGR of 2.98% during 2026-2034. Housing recovery, rising consumer health awareness, and e-commerce disruption are the primary growth drivers.

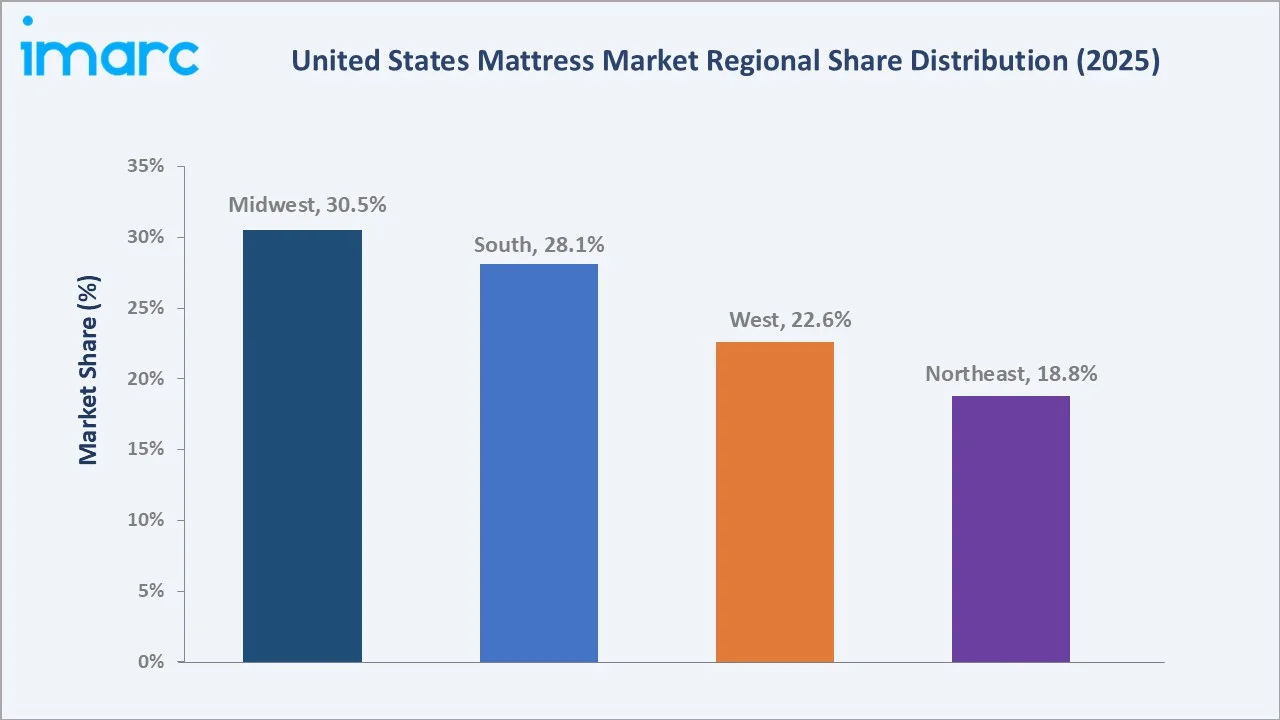

Innerspring mattresses lead product share at 38.7%, while offline distribution commands 63.8% in 2025. The Midwest holds the largest regional share at 30.5%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 10.20 Billion |

|

Forecast Market Size (2034) |

USD 13.28 Billion |

|

CAGR (2026-2034) |

2.98% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Midwest (30.5% share, 2025) |

|

Second Region |

South (28.1% share, 2025) |

|

Leading Product Type |

Innerspring Mattresses (38.7%, 2025) |

|

Leading Distribution |

Offline Distribution (63.8%, 2025) |

The US mattress market growth trajectory from 2020 through 2034, expanding to USD 10.20 Billion in 2025, reflects housing market recovery and rising consumer wellness investment. The forecast to USD 13.28 Billion captures continued DTC disruption, smart mattress adoption, and demographic-driven regional demand expansion.

To get more information on this market, Request Sample

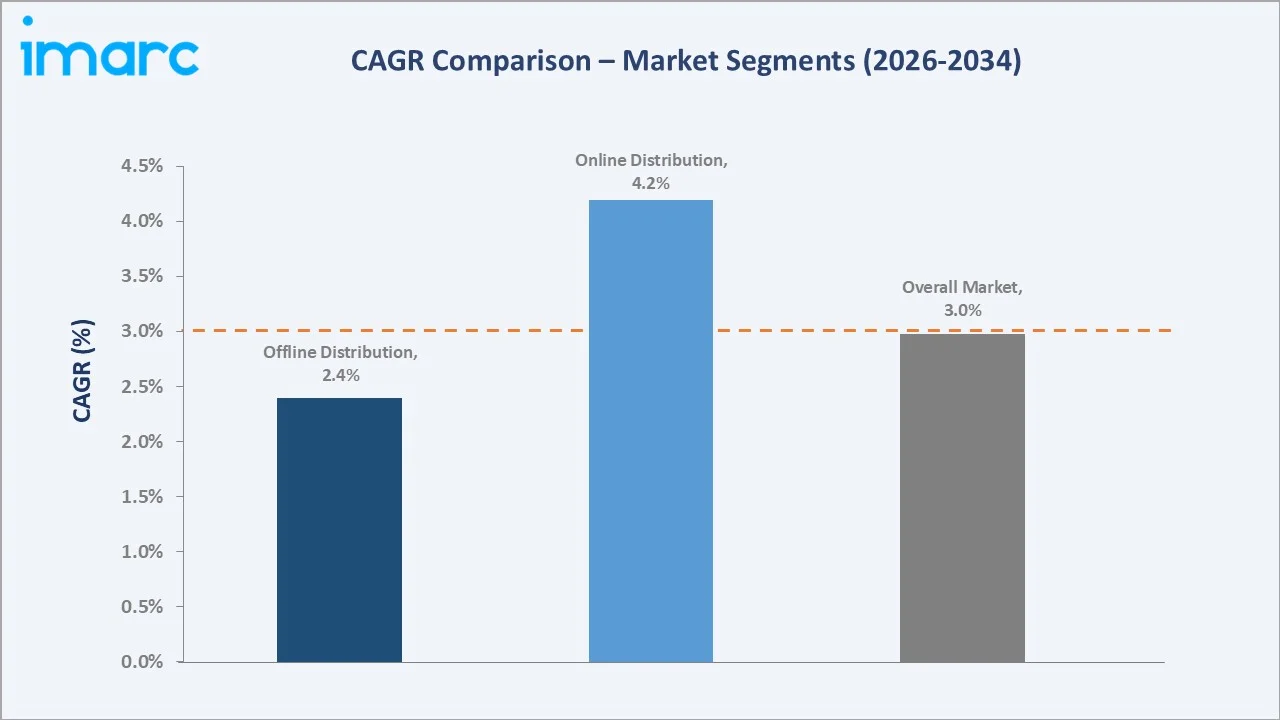

The CAGR trajectories across key product and distribution sub-segments, with online distribution at ~4.20% CAGR and memory foam mattresses at ~3.85% CAGR, represent the fastest-growing categories within the US mattress industry analysis through 2034.

Executive Summary

The US mattress market is on a sustained growth path from USD 10.20 Billion in 2025 to USD 13.28 Billion by 2034. Mattresses represent a non-discretionary household item with recurring replacement demand driven by a 7–10-year average lifecycle and housing formation rates.

Innerspring mattresses dominate product type at 38.7% in 2025, with widespread availability across retail channels and favorable price-to-comfort ratios. Memory foam mattresses (34.2%) represent the fastest-growing product segment driven by sleep health awareness and brand investment in science-based marketing.

Offline distribution leads at 63.8% in 2025, sustained by specialty retailers delivering tactile trial experiences essential for high-consideration purchases. Online distribution at 36.2% is the fastest-growing channel, accelerated by DTC innovation, 100-night trials, and compressed mattress-in-a-box logistics.

The Midwest commands 30.5% regional share, driven by the highest US homeownership rates and dense suburban housing development. The South (28.1%) benefits from the fastest US population growth and new home construction activity in Sun Belt markets.

Key Market Insights

|

Insight |

Data |

|

Leading Product |

Innerspring Mattresses – 38.7% share (2025) |

|

Second Product |

Memory Foam Mattresses – 34.2% share (2025) |

|

Primary Channel |

Offline Distribution – 63.8% share (2025) |

|

Online Channel |

Online Distribution – 36.2% share (2025) |

|

Top Companies |

Serta Simmons Bedding, Sleep Number Corporation, Purple Innovation, LLC, Whitestone Home Furnishings, LLC, Kingsdown Mattress |

Key Analytical Observations Expanding on the Above Data:

- Innerspring mattresses at 38.7% in 2025 dominate owing to cost-competitiveness and broad retail availability. They remain the default specification for mid-range and value-oriented consumers in mass-market channels, hospitality procurement, and replacement purchases.

- Memory foam mattresses at 34.2% lead premium growth, supported by consumer preference for pressure relief and motion isolation, and significant brand investments in sleep science marketing by Tempur-Pedic and Casper.

- Offline distribution at 63.8% persists due to the high-consideration nature of mattress purchases. Specialty retailers such as Mattress Firm maintain advantages through extensive floor displays, sales expertise, and white-glove delivery services.

- Online distribution at 36.2% is growing fastest at ~4.2% CAGR, driven by DTC brands offering 100-night trial policies, risk-free returns, and competitive pricing that bypasses traditional retail markups.

- The Midwest's 30.5% dominance reflects homeownership rates above 70% in states including Iowa, Minnesota, and Michigan, creating the densest concentration of recurring replacement demand alongside suburban development expansion.

United States Mattress Market Overview

A mattress is a resilient padded product consisting of inner components such as springs, foam, latex, or hybrid combinations, encased in upholstered fabric with quilted surfaces. Products are defined by construction type, comfort layers, support systems, and finish quality targeting diverse consumer needs.

.webp)

The US ecosystem integrates raw material suppliers, mattress manufacturers, surface treatment processors, specialty and mass-market retail networks, DTC e-commerce brands, white-glove logistics providers, and end-use sectors spanning residential households, hospitality, healthcare, and institutional buyers.

Market Dynamics

To evaluate market opportunities, Request Sample

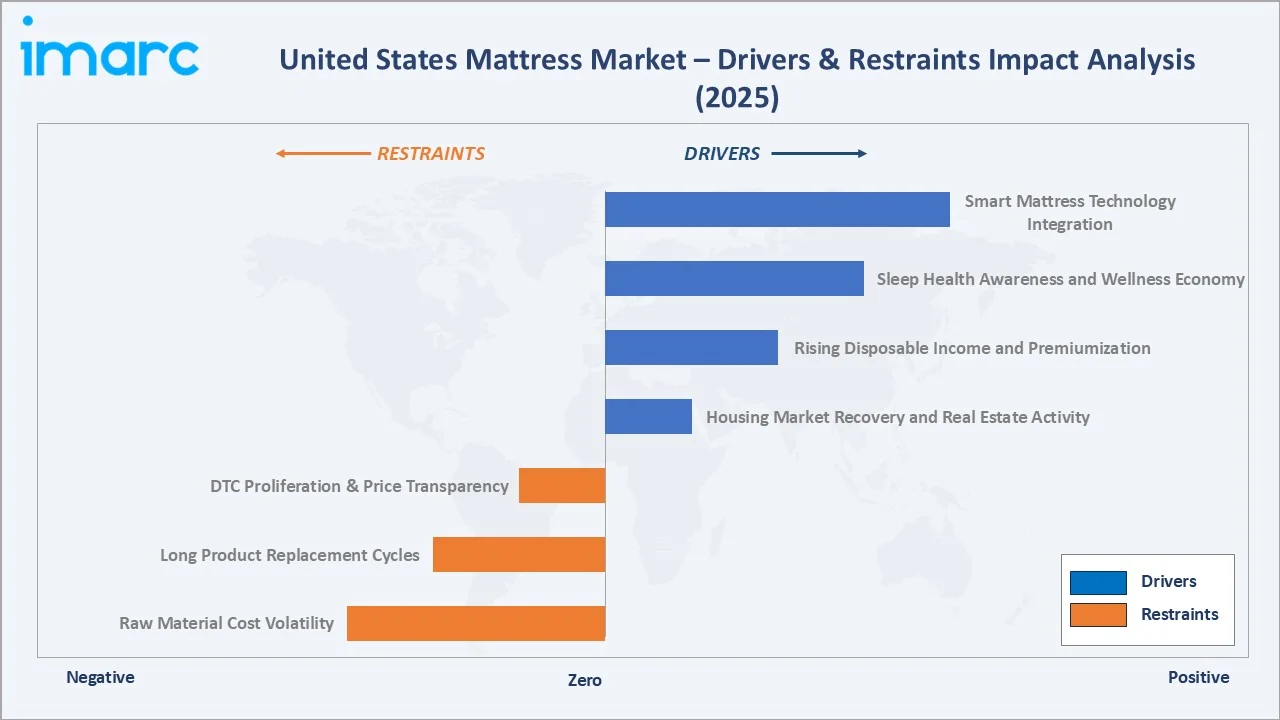

Market Drivers

- Housing Market Recovery and Real Estate Activity: The US housing market has experienced sustained recovery with over 1.4 million new housing starts annually. Each new housing unit generates near-certain mattress procurement, directly translating to first-time buyer and replacement demand across all price tiers.

- Rising Disposable Income and Premiumization: Improving household income levels are supporting a shift toward higher-value mattress products, with consumers increasingly opting for enhanced comfort, durability, and advanced material technologies. This trend is driving steady growth in average selling prices, as buyers prioritize quality and long-term value over basic offerings.

- Sleep Health Awareness and Wellness Economy: Increasing awareness of the importance of sleep quality, supported by the broader wellness movement, is influencing consumer purchasing decisions. As individuals place greater emphasis on health and well-being, there is a corresponding rise in demand for products that enhance sleep quality, leading to higher investment in mattress upgrades.

Market Restraints

- Raw Material Cost Volatility: Fluctuations in key input materials create cost uncertainty for manufacturers, impacting overall production economics and pricing strategies. Dependence on commodity-linked inputs exposes the industry to external supply and pricing cycles. This volatility can lead to margin pressure, particularly when cost increases cannot be fully passed on to consumers. As a result, companies must focus on supply chain optimization and material innovation to mitigate risk and maintain profitability.

- Long Product Replacement Cycles: With an average mattress lifespan of 7–10 years, replacement demand is inherently limited, creating a constrained expansion ceiling tied more to household formation rates than consumption frequency.

Market Opportunities

- Smart Mattress Technology Integration: The integration of advanced technologies such as IoT-enabled sensors, sleep tracking, and climate control systems is creating a high-value premium segment within the mattress market. These innovations are redefining product differentiation by enhancing user experience and personalization. This trend supports significant price premiums compared to traditional offerings, reflecting strong consumer willingness to pay for technology-driven comfort and insights. Additionally, the emergence of connected ecosystems and data-driven services is opening recurring revenue opportunities, further strengthening long-term value creation for manufacturers.

- Hospitality and Commercial Procurement: US hotel inventory of approximately 5.3 million rooms requires systematic mattress replacement every 5–7 years, generating institutional procurement volumes averaging USD 200–400 per unit across mid-scale to upscale properties.

Market Challenges

- DTC Brand Proliferation and Price Transparency: The rapid expansion of direct-to-consumer mattress brands has intensified market competition, increasing pricing transparency and reducing the ability of players to maintain premium price positioning. This heightened competition has led to downward pressure on average selling prices, as consumers can easily compare offerings across multiple platforms. At the same time, rising customer acquisition costs and marketing spend are compressing margins, forcing companies to optimize unit economics and differentiate through branding, product innovation, and customer experience.

- Mattress Disposal and Environmental Regulations: Approximately 50,000 mattresses are discarded daily in the US. State-level extended producer responsibility legislation in California, Connecticut, and Rhode Island imposes recycling fee obligations on manufacturers and retailers.

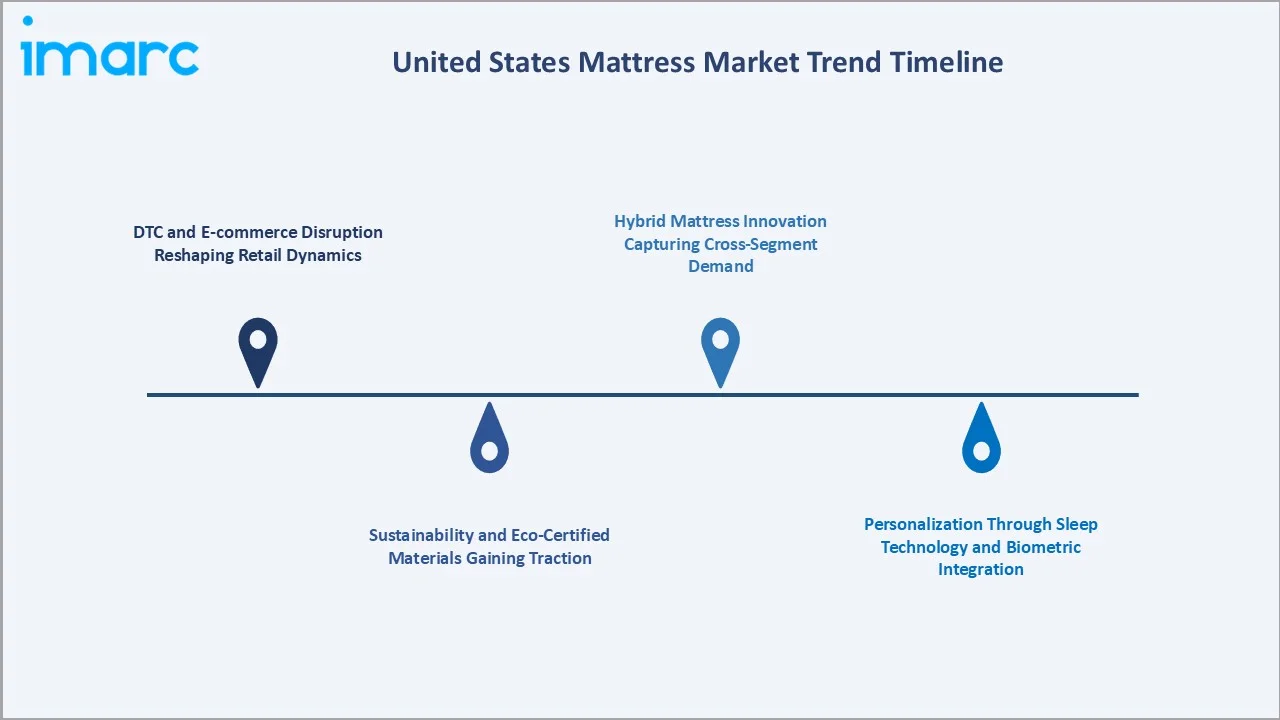

Emerging Market Trends

1. DTC and E-commerce Disruption Reshaping Retail Dynamics

DTC mattress brands now capture 36.2% of distribution, up from under 5% in 2015. Casper, Purple, and Saatva pioneered compressed mattress-in-a-box shipping and 100-night trials, fundamentally transforming consumer discovery, evaluation, and purchase behavior in the category.

2. Sustainability and Eco-Certified Materials Gaining Traction

Consumer demand for GOTS-certified organic cotton, GOLS-certified natural latex, and CertiPUR-US foam is accelerating. Brands incorporating verified sustainable materials command 15–25% price premiums, driving material reformulation investments among leading manufacturers through 2034.

3. Hybrid Mattress Innovation Capturing Cross-Segment Demand

Hybrid mattresses combining pocketed coil support with memory foam or latex comfort layers represent the fastest-growing product sub-type. Hybrids deliver innerspring responsiveness alongside foam pressure-relief benefits, enabling premium pricing above standalone product category.

4. Personalization Through Sleep Technology and Biometric Integration

AI-powered sleep tracking, biometric sensor integration, and dual-zone firmness adjustment are transforming mattresses into dynamic health platforms. Sleep Number's SleepIQ technology demonstrates 70% user engagement, validating recurring data service monetization models for leading manufacturers.

Industry Value Chain Analysis

The US mattress value chain spans six stages from raw material procurement through end-use delivery. Manufacturing and comfort layer integration capture the highest value-add margins, while DTC distribution and white-glove logistics create significant working capital requirements.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

Polyurethane foam, steel coils, latex, fabric, FR materials, and border rods |

|

Mattress Manufacturing |

Foam pouring, coil fabrication, component cutting, layer assembly, and quilting |

|

Surface & Finishing |

Ticking cover application, FR treatment, border rod fitting, and label attachment |

|

Distribution & Stocking |

Specialty retail, mass retail, furniture stores, online platforms, and white-glove delivery services |

|

Procurement & Installation |

Residential delivery, hospitality procurement, healthcare sourcing, and institutional supply |

|

End Use |

Residential households, hotels, hospitals, dormitories, military housing, and short-term rentals |

Integrated manufacturers with captive foam pouring and proprietary fabric quilting achieve 15–25% cost advantages over those relying solely on external procurement. Vertical integration from materials through retail represents the primary strategic differentiator among leading US mattress companies.

Technology Landscape in the US Mattress Industry

Foam Technology: Memory Foam, Latex, and Advanced Polyurethane

Viscoelastic memory foam remains the core premium comfort material. Gel-infused variants address heat-retention concerns via phase-change materials. Copper-infused foam targets antimicrobial positioning. Talalay and Dunlop latex processing produce natural comfort layers prized for durability and eco-certification credentials.

Coil System Innovation: Pocketed Springs and Micro-Coils

Advanced pocketed coil systems using individually fabric-wrapped springs provide superior motion isolation versus open Bonnell designs. Micro-coil layers of 1,000+ miniature coils are integrated as transitional layers in ultra-premium hybrid mattresses, with coil gauges varying 12.5–18 for distinct firmness profiles.

Smart Mattress Technology: IoT and Biometric Integration

Embedded pressure sensors, temperature regulation, and heart rate variability tracking transition mattresses into connected health devices. Sleep Number's platform integrates with Apple Health, Amazon Alexa, and Google Home, supporting broader smart home ecosystem positioning.

Sustainable Manufacturing: Recycled Materials and Green Chemistry

Bio-based foam formulations using soy polyols replace 20–40% of petroleum-derived polyols. Post-consumer steel recycling achieves 80–90% recycled content in coil manufacturing. Water-based adhesives reduce VOC emissions and enable CertiPUR-US foam certifications for environmentally conscious brands.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Innerspring Mattresses |

38.7% |

2025 |

|

Distribution Channel |

Offline Distribution |

63.8% |

2025 |

|

Size |

Queen Size |

🔒 |

2025 |

|

Application |

Domestic |

🔒 |

2025 |

|

Region |

Midwest |

30.5% |

2025 |

By Product Type

Innerspring mattresses command a 38.7% majority share in 2025 owing to cost-competitiveness and broad structural performance across mass-market, hospitality, and replacement purchase applications. Steel coil systems provide familiar bounce, breathability, and edge support consumers associate with traditional sleep comfort.

.webp)

To access detailed market analysis, Request Sample

Memory foam mattresses at 34.2% represent the premium growth driver, valued for motion isolation and pressure relief. Latex mattresses (14.6%) serve eco-conscious consumers at premium price points. Others (12.5%) include smart beds, air-adjustable systems, and specialty foam configurations.

By Distribution Channel

Offline distribution dominates at 63.8% in 2025, anchored by specialty retailers offering immersive in-store try-before-you-buy experiences critical for high-consideration purchases.

Online distribution at 36.2% in 2025 is the fastest-growing channel at ~4.2% CAGR through 2034. DTC brands leverage 100-night trials and compressed-box shipping to reduce consumer hesitancy. Amazon Prime's same-day delivery of compressed foam mattresses further accelerates e-commerce channel penetration.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Midwest |

30.5% |

Dense housing stock, growing suburban development, cost-conscious buyers |

|

South |

28.1% |

Population growth, new home construction boom, warm-climate demand |

|

West |

22.6% |

Premium product preference, tech-savvy DTC adoption, high real estate activity |

|

Northeast |

18.8% |

Urban renewal, high income households, brand-loyal premium buyers |

The Midwest's 30.5% market dominance in 2025 reflects the highest US homeownership rates above 70% in states including Iowa, Minnesota, and Michigan, creating dense concentrations of recurring replacement demand. Suburban development expansion in Columbus, Indianapolis, and Kansas City supports new unit mattress procurement.

The South at 28.1% benefits from the fastest-growing US population base, with Texas, Florida, and North Carolina posting consistent gains of 1.5–2.5% annually. Sun Belt new home construction generates first-time procurement demand alongside growing hospitality sector activity.

The West at 22.6% demonstrates the highest per-capita mattress expenditure, driven by California and Washington premium consumers with above-average incomes and preference for eco-certified and smart sleep technology products.

Competitive Landscape

The US mattress market is moderately consolidated at the top. Mid-tier and DTC brands occupy the remaining market with rapidly shifting share dynamics.

|

Company Name |

Key Products |

Position |

Strategic Focus |

|

Serta Simmons Bedding |

Serta, Beautyrest, Tuft & Needle, Beauty Sleep |

Leader |

Mass-market scale; extensive US retail footprint; hospitality procurement strength |

|

Sleep Number Corporation |

ComfortMode, ComfortNext, Climate |

Leader |

Adjustable smart beds; owned retail stores; biometric health data services |

|

Purple Innovation, LLC |

Purple, Restore, Rejuvenate |

Challenger |

Hyper-elastic polymer grid; direct & wholesale dual channel; innovation positioning |

|

Whitestone Home Furnishings, LLC |

Saatva Classic, Saatva Rx, Saatva HD, Saatva Latex Hybrid |

Emerging |

Luxury DTC; white-glove delivery; eco-conscious premium segment |

|

Kingsdown Mattress |

Select Syrah Plush Euro Pillowtop Hybrid Mattress, Insignia Cool Start Firm Smooth Top Hybrid Mattress, Passions Kelbrooke Hybrid Ultra Plush Euro Pillowtop Mattress |

Emerging |

Luxury coil technology; Body Diagnostics retail tool; independent retail focus |

Key players include Serta Simmons Bedding, Sleep Number Corporation, Purple Innovation, LLC, Whitestone Home Furnishings, LLC, Kingsdown Mattress, and others.

.webp)

Key Company Profiles

Serta Simmons Bedding

Serta Simmons Bedding is one of the largest US mattress manufacturers, owning the Serta and Beautyrest brands. The company serves mid-market to premium segments through nationwide retail distribution, hospitality procurement, and wholesale channels across the United States.

- Product Portfolio: Serta, Beautyrest, Tuft & Needle, BeautySleep, and others.

- Recent Developments: In January 2026, Serta Simmons Bedding announced two new product launches for its Serta and Beautyrest brands. Serta introduced the all-new Serta Perfect Sleeper, offering a new Q4 Support System, while Beautyrest expanded the Beautyrest Black portfolio with the launch of the all-new Beautyrest Black Hybrid XCS models.

- Strategic Focus: Serta Simmons focuses on brand heritage leverage across consumer retail and commercial hospitality channels, investing in comfort technology differentiation to defend mid-market share against DTC brand encroachment.

Sleep Number Corporation

Sleep Number Corporation is a Minneapolis-based sleep wellness company manufacturing adjustable air-chamber smart beds integrated with biometric sleep tracking. Its 650+ owned US retail stores anchor its premium brand positioning and consumer data collection capabilities.

- Product Portfolio: ComfortMode, ComfortNext, Climate, and others.

- Recent Developments: In March 2026, Sleep Number Corporation refreshed its mattress portfolio with five innovative new beds designed to adapt to users’ changing comfort needs over time. These smart beds automatically adjust night after night, offering a more personalized and responsive sleep experience.

- Strategic Focus: Sleep Number differentiates on sleep health data and wellness positioning, operating exclusively through owned retail to maintain premium brand control and accumulate consumer sleep data enabling recurring subscription revenue.

Market Concentration Analysis

The US mattress market exhibits moderate-to-high concentration at the top tier, with Tempur Sealy and Serta Simmons commanding approximately 55–60% of total market revenue through multi-brand portfolios. DTC brands collectively represent approximately 15–18% of revenue while driving disproportionate growth momentum.

Consolidation is accelerating through vertical integration. The proposed Tempur Sealy acquisition of Mattress Firm represents the most significant structural shift, potentially creating a fully integrated manufacturer-to-retailer channel controlling over 2,300 US specialty locations.

Investment & Growth Opportunities

Fastest-Growing Segments

Online distribution at ~4.20% CAGR through 2034 is the highest-growth channel, driven by DTC brand innovation and consumer preference for digital convenience. Memory foam mattresses at ~3.85% CAGR represent the broadest-based product growth opportunity through 2034.

Emerging Markets

The hospitality and institutional procurement sector represent a significant under-penetrated growth opportunity. With 5.3 million US hotel rooms requiring systematic replacement cycles and growing short-term rental platforms driving residential-grade mattress demand, commercial procurement volumes are expanding at 3–4% annually.

Venture & Investment Trends

Private equity interest in consolidating the fragmented mid-tier mattress manufacturing segment is growing. Sleep technology integration, sustainability certification infrastructure, and logistics innovation for white-glove delivery at scale are primary venture capital themes through 2030 in the US sleep industry.

Future Market Outlook (2026-2034)

The US mattress market is forecast to expand from USD 10.20 Billion in 2025 to USD 13.28 Billion by 2034 at a CAGR of 2.98%, adding USD 3.08 Billion in incremental annual market value. This sustained growth reflects the housing-linked, non-discretionary replacement demand characteristics.

Three forces will most significantly shape the industry through 2034. Smart sleep technology integration will expand the addressable premium segment, with IoT-enabled adjustable beds growing at 2–3x the overall market rate. Sustainability mandates from state-level mattress recycling programs will reshape material sourcing and end-of-life logistics across all manufacturers.

Online distribution will approach parity with offline channels by 2030, driven by improving last-mile white-glove delivery infrastructure and extended trial policies that reduce purchase risk. DTC brands investing in proprietary logistics capabilities will structurally improve unit economics and conversion rates over this period.

Research Methodology

Primary Research

Primary research encompassed over 45 structured interviews with US mattress industry stakeholders, including senior commercial managers at leading manufacturers, specialty retail buyers, e-commerce category managers, interior designers, and hospitality procurement executives. Primary data validated market sizing, segment shares, and regional demand estimates.

Secondary Research

Key secondary sources include the International Sleep Products Association (ISPA) Bedding Barometer, US Census Bureau housing starts and homeownership data, National Retail Federation consumer spending reports, and industry publications including Furniture Today, Sleep Savvy, and corporate annual reports from leading manufacturers.

Forecasting Models

Market size estimations and growth projections were derived using top-down and bottom-up forecasting models incorporating housing starts, household formation rates, replacement cycle data, income growth indices, and e-commerce penetration trajectories. Scenario analysis was performed to account for macroeconomic uncertainty.

United States Mattress Market Report Scope

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Products Covered | Innerspring Mattresses, Memory Foam Mattresses, Latex Mattresses, Others |

| Distribution Channels Covered | Online Distribution, Offline Distribution |

| Sizes Covered | Twin or Single Size, Twin XL Size, Full or Double Size, Queen Size, King Size Mattress, Others |

| Applications Covered | Domestic, Commercial |

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered | Serta Simmons Bedding, Sleep Number Corporation, Purple Innovation, LLC, Whitestone Home Furnishings, LLC, Kingsdown Mattress, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the United States mattress market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the United States mattress market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the United States mattress industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the United States Mattress Market Report

The US mattress market reached USD 10.20 Billion in 2025, reflecting consistent demand from housing market recovery, rising disposable income, and growing consumer sleep health awareness across all age groups.

The market is projected to reach USD 13.28 Billion by 2034, growing at a CAGR of 2.98% during 2026-2034, driven by DTC disruption, smart mattress adoption, and sustained household formation demand.

Innerspring mattresses lead with 38.7% product share in 2025, valued for cost-competitiveness and broad retail availability across mass-market, hospitality, and replacement purchase applications.

Offline distribution leads at 63.8% in 2025, anchored by specialty mattress retailers providing immersive product trial experiences critical for high-consideration purchases averaging USD 800–1,500.

The Midwest commands 30.5% market share in 2025, driven by the highest US homeownership rates, dense suburban development, and strong specialty retail infrastructure across key Midwestern metropolitan areas.

Online distribution is the fastest-growing channel at ~4.20% CAGR through 2034, driven by DTC brand innovation, Amazon integration, and consumer preference for 100-night trial policies and white-glove delivery.

Leading companies include Serta Simmons Bedding, Sleep Number Corporation, Purple Innovation, LLC, Whitestone Home Furnishings, LLC, Kingsdown Mattress, and others.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)