United States Obesity Drugs Market Size, Share, Trends and Forecast by Type, Age, Gender, Distribution Channel, and Region, 2026-2034

United States Obesity Drugs Market Size and Share:

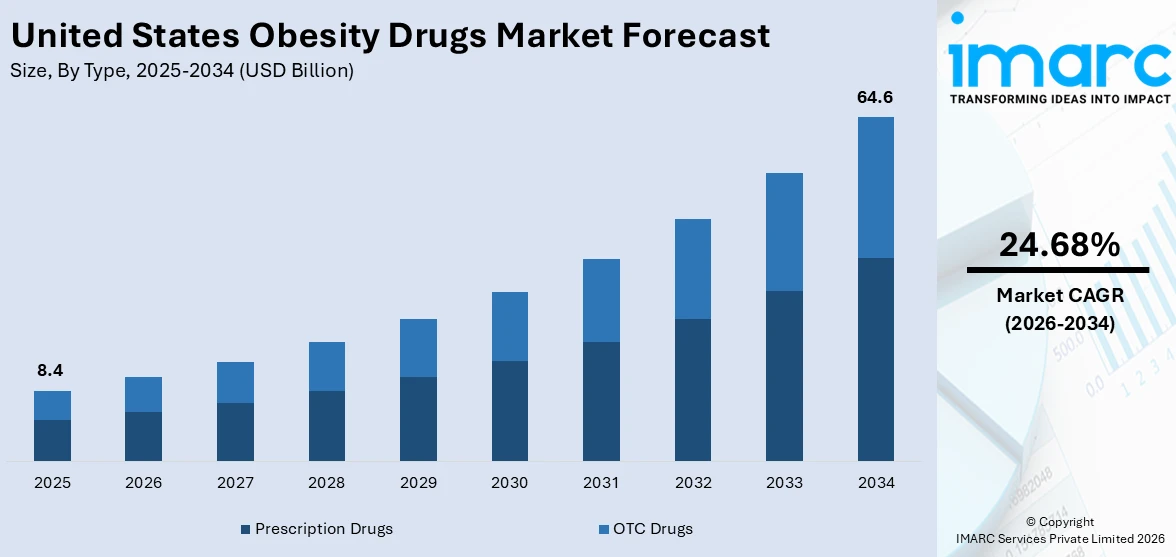

The United States obesity drugs market size was valued at USD 8.4 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 64.6 Billion by 2034, exhibiting a CAGR of 24.68% from 2026-2034. The rising incidence of obesity is significantly driving the market, as more individuals seek medical interventions to manage their condition. In addition, increasing efforts by both governmental agencies and non-profit organizations to generate awareness about the health risks associated with obesity are playing a crucial role in expanding the market. These initiatives aim to educate the public about healthy lifestyle choices, further catalyzing the demand for effective obesity treatments and thus contributing to the United States obesity drugs market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 8.4 Billion |

| Market Forecast in 2034 | USD 64.6 Billion |

| Market Growth Rate 2026-2034 | 24.68% |

At present, the market is experiencing growth on account of the increasing number of individuals affected by obesity, which is driving the demand for effective medical treatments. Many people struggle to lose weight solely by means of diet and physical activity. Consequently, healthcare providers are recommending pharmaceutical support, including obesity drugs. As awareness is rising about the serious health risks linked to obesity, such as type 2 diabetes, cardiovascular diseases, and certain cancers, individuals are turning to drug-based solutions for weight management. Insurers and healthcare systems are recognizing obesity as a chronic condition, expanding coverage for prescription treatments. Public health campaigns and wellness programs, which are encouraging individuals to take control of their weight, are fueling the United States obesity drugs market growth.

To get more information on this market Request Sample

Apart from this, pharmaceutical companies are wagering on research and development (R&D) activities, leading to more advanced and safer drugs with better results and fewer side effects. These innovations are making obesity drugs more appealing to both doctors and patients. The growing trend of preventive healthcare is enabling people to manage their weight proactively, and obesity drugs offer a convenient option. Social acceptance of medical weight loss is further motivating people to explore pharmaceutical interventions without stigma. Moreover, the expansion of retail outlets is improving drug affordability and access among a broader population. According to the IMARC Group, the United States retail market size is anticipated to show a growth rate (CAGR) of 2.28% during 2025-2033.

United States Obesity Drugs Market Trends:

Increasing prevalence of obesity

The rising incidence of obesity in the country is positively influencing the market. As per the Centers for Disease Control and Prevention (CDC), the prevalence of obesity was 40.3% among American adults between August 2021-August 2023. The growing implications of obesity in public health and the healthcare economy, putting a strain on resources due to related conditions, such as heart diseases, type 2 diabetes, and certain types of cancer, are driving the demand for obesity drugs. Moreover, the increasing incidence of obesity is creating the need for medical interventions geared towards weight management. Furthermore, the rising prescription of weight loss medications, coupled with lifestyle modification strategies that aim to reduce appetite, increase the feeling of fullness, and inhibit the absorption of fat, is bolstering the market growth.

Rising user awareness and education

The increasing public and professional awareness about health issues is offering a favorable United States obesity drugs market outlook. The growing efforts by governmental agencies, non-profit organizations, and healthcare institutions to educate the public about the health implications of obesity are encouraging the usage of obesity drugs. These education campaigns often focus on the risks of developing secondary conditions like cardiovascular diseases (CVDs), diabetes, and hypertension, which are closely tied to obesity. For instance, in 2022, 702,880 individuals in the United States died from various types of heart diseases, as per the Centers for Disease Control and Prevention (CDC). Moreover, every 33 seconds, a person passed away due to a cardiovascular disease in the United States. The rising awareness about the health implications of obesity, which helps in early diagnosis, is propelling the market growth. A well-informed population is more likely to engage with healthcare providers for weight management solutions, including obesity drugs. Moreover, the growing inclination of medical practitioners to prescribe these medications due to an improved understanding of their efficacy and a broad body of research supporting their use is positively influencing the market.

United States Obesity Drugs Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the United States obesity drugs market, along with forecast at the country and regional levels from 2026-2034. The market has been categorized based on type, age, gender, and distribution channel.

Analysis by Type:

- Prescription Drugs

- OTC Drugs

Prescription drugs hold a significant share in the market since they are usually recommended for individuals with a high body mass index and obesity-related health conditions. Prescription drugs offer stronger formulations and require medical supervision, which ensures proper dosage and monitoring of side effects. Healthcare providers often include these drugs as part of a structured weight loss program. According to the United States obesity drugs forecast, the segment will be benefiting from ongoing research, producing newer, safer, and more effective treatments.

OTC drugs are easily accessible and do not require a doctor's prescription, making them popular among individuals seeking self-managed weight loss solutions. OTC drugs often include appetite suppressants and fat blockers and are usually used for mild weight management. This segment is attracting people who are looking for convenient and affordable options. Individuals often use OTC products as a first step before exploring stronger treatments under medical guidance.

Analysis by Age:

- Children

- Adult

- Old

The children segment holds a significant share of the market, as childhood obesity is becoming a growing concern. Pediatric obesity leads to early health problems like diabetes and hypertension, creating the need for medical intervention. While drug use in children is limited and closely monitored, healthcare providers increasingly consider medications when lifestyle changes alone do not work. Regulatory authorities ensure safety and dosage guidelines for this age group.

The adult segment often faces obesity due to sedentary lifestyles, stress, poor diet, and other health factors. This group commonly seeks weight management solutions through both prescription and OTC drugs. Healthcare professionals frequently recommend medications for adults with high body mass index (BMI) and obesity-linked conditions. Adults are more likely to commit to long-term drug treatments and combine them with exercise and diet plans.

The old section is experiencing challenges like reduced metabolism, limited mobility, and pre-existing health conditions, which make weight management harder. Physicians often prescribe obesity drugs to help manage related issues like high blood pressure and diabetes. However, drug choices are made carefully to avoid side effects or interactions. As the elderly population is increasing and medical support is improving, older adults are seeking controlled pharmaceutical solutions to manage their weight safely.

Analysis by Gender:

- Male

- Female

The male segment is seeking medical help to manage weight. Many males face obesity due to high-calorie diets, lack of exercise, and job-related stress. Healthcare providers often recommend prescription drugs to men who are at risk of heart disease or diabetes. Men are generally more responsive to fast and visible results, which drives interest in effective medications. As awareness is increasing about obesity’s long-term health risks, men are turning to pharmaceutical solutions alongside lifestyle changes for better health outcomes.

Female holds a significant share of the market due to higher awareness and a stronger focus on personal health and appearance. Women often seek weight management options after pregnancy, during hormonal changes, and due to metabolic issues. Many females are proactive in consulting doctors and following medical plans that include obesity drugs. Emotional and social factors are also influencing their decision to use weight-loss medications.

Analysis by Distribution Channel:

Access the comprehensive market breakdown Request Sample

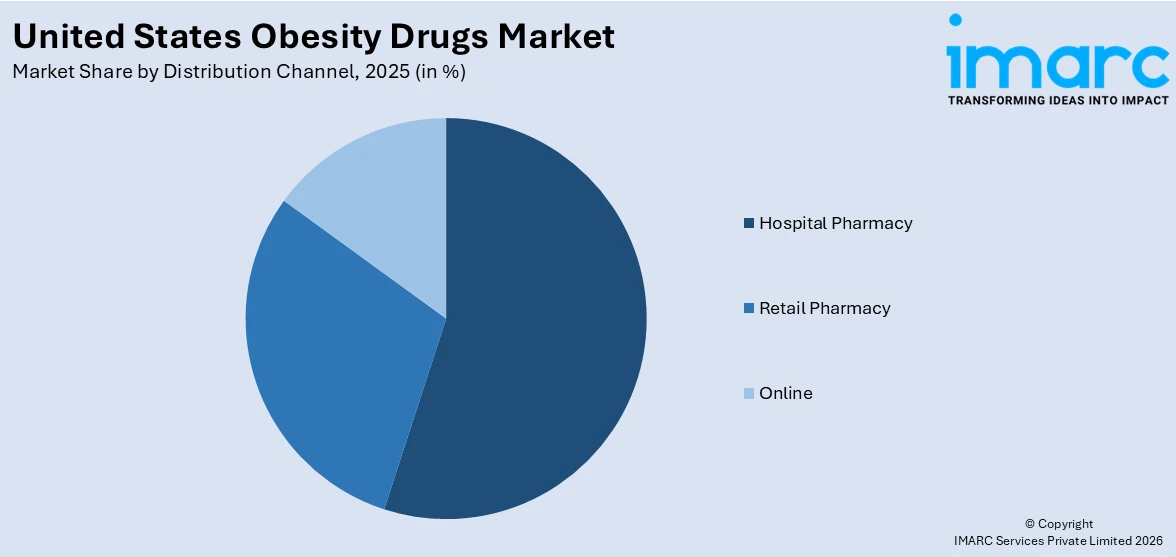

- Hospital Pharmacy

- Retail Pharmacy

- Online

Hospital pharmacy is gaining popularity as patients with severe obesity-related conditions often receive prescriptions during hospital visits or after undergoing medical checkups. Hospitals provide access to specialized medications and ensure professional supervision, which increases patient confidence. Physicians prefer hospital pharmacies for safe and reliable drug dispensing. This channel supports patients who need close monitoring and long-term treatment plans.

Retail pharmacy offers easy access to both prescription and OTC obesity drugs. Many individuals prefer retail pharmacies due to convenience, personal assistance, and trust in local pharmacists. Retail outlets also help spread awareness by providing information about weight loss medications. Frequent promotions and wide availability are attracting a large user base. As more people are seeking quick and accessible solutions for weight management, the role of retail pharmacies in distributing obesity drugs continues to expand.

The online segment holds a significant share of the market due to its convenience, privacy, and doorstep delivery. Online pharmacies offer a wide variety of products, customer reviews, and discounts, which appeal to tech-savvy users. The rise in digital health platforms and telemedicine is also supporting online prescriptions and purchases. As digital habits are strengthening and internet access is becoming more widespread, the demand for obesity drugs through online channels continues to rise.

Regional Analysis:

- Northeast

- Midwest

- South

- West

The Northeast region is noted for rising health awareness and access to advanced healthcare facilities. People in this area often seek medical guidance for weight management and prefer regulated treatment plans. Urban centers like New York and Boston are supporting the availability of prescription and OTC drugs. The presence of top hospitals and clinics is also contributing to the adoption of obesity medications.

The Midwest region is experiencing growth due to higher obesity rates and lifestyle-related health issues. Many residents are facing challenges like limited physical activity and unhealthy eating habits, creating the need for pharmaceutical intervention. Healthcare providers recommend both prescription and OTC drugs to help manage weight. The availability of retail and hospital pharmacies is supporting wide access to medications.

The South holds a significant market share, largely driven by high obesity prevalence and related chronic diseases. People in this region often face health challenges due to dietary patterns and sedentary lifestyles. As awareness is increasing, individuals are turning to medication to manage weight. Retail pharmacies and hospitals play a key role in distribution, while online platforms grow in popularity. Healthcare programs and community initiatives are further supporting the use of obesity drugs in the area.

The Western region shows rising interest in the obesity drugs market, supported by a health-conscious population and strong digital infrastructure. States like California and Washington are leading in wellness trends and supporting the use of medications alongside fitness and dietary programs. Online and retail pharmacies offer broad access to both prescription and OTC drugs. People in urban areas are adopting obesity drugs as part of preventive health routines.

Competitive Landscape:

Key players are working to develop enhanced formulations to meet the high demand. They are investing heavily in R&D activities to create innovative and effective medications with fewer side effects. These companies are conducting clinical trials to prove the safety and efficacy of their products, which helps gain approval from regulatory authorities. They also focus on generating awareness among healthcare professionals and patients through marketing and educational initiatives. Key players are forming partnerships with healthcare providers and insurance companies to improve drug accessibility and coverage. They monitor patient needs and preferences to provide tailored solutions that support long-term weight management. By continuously improving item offerings and expanding their reach, these companies are shaping the market landscape. For instance, in June 2024, Flagship Pioneering and ProFound Therapeutics formed a collaboration with Pfizer, a worldwide leader in biopharmaceuticals headquartered in New York, to conduct essential research aimed at discovering potential next-generation therapies for obesity. Through this partnership, ProFound intended to explore how its groundbreaking technology could meet unfulfilled obesity requirements.

The report provides a comprehensive analysis of the competitive landscape in the United States obesity drugs market with detailed profiles of all major companies.

Latest News and Developments:

- April 2025: Novo Nordisk submitted a request for US authorization of a 25-mg oral version of its well-known GLP-1 medication, semaglutide, aimed at weight loss for individuals who were overweight or obese. This signified the first possible endorsement of a GLP-1 tablet for weight reduction.

- March 2025: Eli Lilly, the American pharmaceutical firm, revealed intentions to introduce its highly successful drugs for diabetes and obesity management in Mexico, India, and Brazil. The implementation is anticipated to take place in the latter half of 2025 as production capacity gradually increases.

United States Obesity Drugs Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Prescription Drugs, OTC Drugs |

| Ages Covered | Children, Adult, Old |

| Genders Covered | Male, Female |

| Distribution Channels Covered | Hospital Pharmacy, Retail Pharmacy, Online |

| Regions Covered | Northeast, Midwest, South, West |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the United States obesity drugs market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the United States obesity drugs market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the United States obesity drugs industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the United States Obesity Drugs Market Report

The United States obesity drugs market was valued at USD 8.4 Billion in 2025.

The United States obesity drugs market is projected to exhibit a CAGR of 24.68% during 2026-2034, reaching a value of USD 64.6 Billion by 2034.

Advancements in pharmaceutical research are leading to the development of safer and more effective obesity drugs with fewer side effects, which is encouraging wider usage. Besides this, public awareness about the serious health risks associated with obesity, such as type 2 diabetes, cardiovascular diseases, and certain cancers, is motivating people to seek treatment. Additionally, healthcare providers and insurers are recognizing obesity as a chronic condition that requires long-term management, improving drug accessibility.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)