United States Oligonucleotide Synthesis Market Size, Share, Trends and Forecast by Product, Application, End Use, and Region, 2026-2034

United States Oligonucleotide Synthesis Market Size and Share:

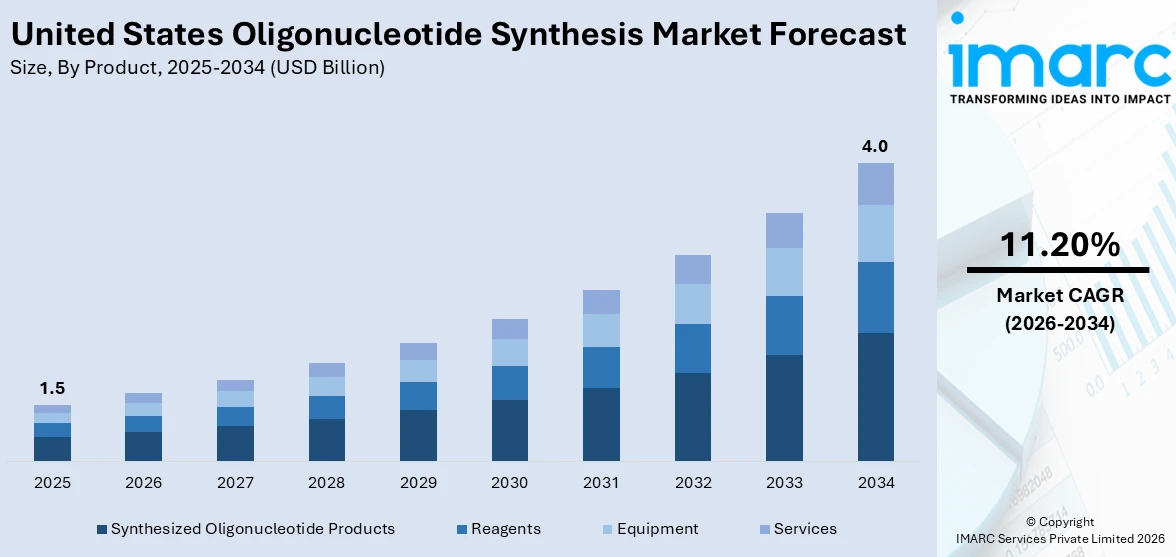

The United States oligonucleotide synthesis market size was valued at USD 1.5 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 4.0 Billion by 2034, exhibiting a CAGR of 11.20% from 2026-2034. The rising demand for personalized medicine, advancements in genomics and biotechnology, increasing research on genetic disorders, and the widespread adoption of oligonucleotides in drug development are propelling the growth of the market across the United States. In addition to this, the expanding applications in diagnostics and therapeutics, alongside government funding for genetic research, further fuel the market growth.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 1.5 Billion |

| Market Forecast in 2034 | USD 4.0 Billion |

| Market Growth Rate (2026-2034) | 11.20% |

The increasing demand for personalized medicine primarily drives the market growth across the United States as oligonucleotides play a vital role in developing targeted therapies for various diseases, including cancer, genetic disorders, and infectious diseases. Advances in genomics have further promoted the market by enabling high-throughput synthesis and improved accuracy of oligonucleotide production. The rising prevalence of genetic disorders and the growing emphasis on precision medicine have intensified research activities, boosting the adoption of oligonucleotides in drug discovery and development. According to industry reports, there are an estimated 10,000 types of single-gene diseases (also called monogenic diseases), which are diseases caused by mutations in a single gene. The World Health Organization estimates that 10 out of every 1000 people are affected. This means between 70 million and 80 million people worldwide live with one of these diseases. Pharmaceutical and biotech companies are leveraging oligonucleotide-based approaches, such as antisense oligonucleotides, siRNA, and aptamers, to create novel therapeutics, contributing to market expansion.

To get more information on this market Request Sample

Increased government funding and initiatives to advance genetic research also play a pivotal role. For instance, in September 2024, the National Institutes of Health (NIH) awarded $5.4 million in first-year funding to establish a new program that supports the integration of genomics into learning health systems. The new Genomics-enabled Learning Health System (gLHS) Network aims to identify and advance approaches for integrating genomic information into existing learning health systems. Support for large-scale projects like the Human Genome Project has spurred innovation in oligonucleotide synthesis technologies. Additionally, the widespread application of oligonucleotides in diagnostics, including PCR, qPCR, and next-generation sequencing, drives the demand, particularly in clinical and research settings.

United States Oligonucleotide Synthesis Market Trends:

Advancements in Genomics and Precision Medicine

The growing focus on precision medicine drives the demand for oligonucleotides in targeted therapies for cancer, genetic disorders, and infectious diseases. Rapid advancements in genomics and biotechnology enable high-throughput, accurate oligonucleotide synthesis, supporting their critical role in drug discovery, diagnostics, and research applications. For instance, in November 2024, Trace Neuroscience, Inc., a biopharmaceutical company working in the field of genomic medicine for people living with neurodegenerative diseases, announced its launch with a $101 million Series A financing led by Third Rock Ventures, with participation from Atlas Venture, GV, and RA Capital Management. The company is developing novel genomic therapies that restore UNC13A protein to re-establish healthy communication between nerves and muscle cells impacted by neurodegenerative disease.

Expanding Therapeutic and Diagnostic Applications

Oligonucleotides are increasingly used in therapies like antisense RNA, siRNA, and aptamers, as well as in diagnostics, such as PCR and next-generation sequencing. These applications address rising genetic and chronic diseases, thus propelling the market growth. For instance, in July 2024, a research article published in Nature Biotechnology highlights the details of a method for synthesizing single-stranded RNA that was developed by scientists at the Wyss Institute for Biologically Inspired Engineering at Harvard University and Harvard Medical School (HMS). The technology, which is being commercialized by EnPlusOne Biosciences, produces single-stranded RNA with efficiencies and purities that are comparable to traditional chemical synthesis using water and enzymes, and without using a template sequence. Such initiatives exemplify the steadily expanding usage of oligonucleotides in various therapies, thus driving the market toward growth further.

Government Support and Technological Innovations

Government initiatives, funding for genomics research, and regulatory approvals for oligonucleotide-based drugs boost market expansion. Increased investment by pharmaceutical and biotechnology companies in R&D for nucleic acid therapeutics also drives growth. The establishment of streamlined pathways for oligonucleotide drug approval by regulatory bodies like the FDA has encouraged innovation and accelerated the translation of oligonucleotide-based solutions from research to clinical use. For instance, in June 2024, the FDA published the final version of the guideline titled “Clinical Pharmacology Considerations for the Development of Oligonucleotide Therapeutics Guidance for Industry”. This document replaces the draft from 2022 and provides recommendations to assist the industry in the development of oligonucleotide therapeutics, but it also poses new challenges for developers and manufacturers.

United States Oligonucleotide Synthesis Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the United States oligonucleotide synthesis market, along with forecasts at the country and regional levels from 2026-2034. The market has been categorized based on product, application, and end use.

Analysis by Product:

- Synthesized Oligonucleotide Products

- Reagents

- Equipment

- Services

Synthesized oligonucleotide products are integral to numerous applications, including diagnostics, gene editing, and therapeutics, driving their dominance in the market. Customization options allow researchers and clinicians to obtain specific sequences for unique experimental or therapeutic needs. With the growing adoption of oligonucleotide-based drugs and advanced genetic tools, demand continues to rise. Their role as fundamental components in cutting-edge technologies like CRISPR and RNA-based therapies ensures their significant share in the market.

Reagents, such as primers, probes, and nucleotides, are indispensable for oligonucleotide synthesis and downstream applications like PCR, sequencing, and molecular diagnostics. Their essential role in enabling accurate synthesis and experimental success makes them a core market segment. As research in genomics and precision medicine expands, the demand for high-quality reagents grows. Additionally, the increasing use of diagnostic tools during outbreaks, like COVID-19, underscores their critical importance, ensuring sustained growth in their market share.

Advanced synthesis equipment, including automated oligonucleotide synthesizers, ensures precise, high-throughput production of oligonucleotides. They eliminate errors and streamline workflows in addition to allowing scalability against industry needs in a developing market. Innovations in the synthesis technology that improved efficiency and capability in producing complicated and longer oligonucleotides increase dependency on specialized equipment. Their critical contribution to oligonucleotide manufacturing and operation efficiency creates a substantial market share.

Oligonucleotide synthesis services provide customized demands of research and pharmaceuticals with regard to specifically tailored sequences, modifications, and scales. They serve all fields of academia, biotechnology, and pharmaceutical, where accuracy and know-how matter the most. The main driving force for outsourcing synthesis to specialized providers is that they produce high-end results but with less demand on internal resources. With the growing complexity of research and therapeutic applications, these services remain essential, ensuring their substantial share in the market.

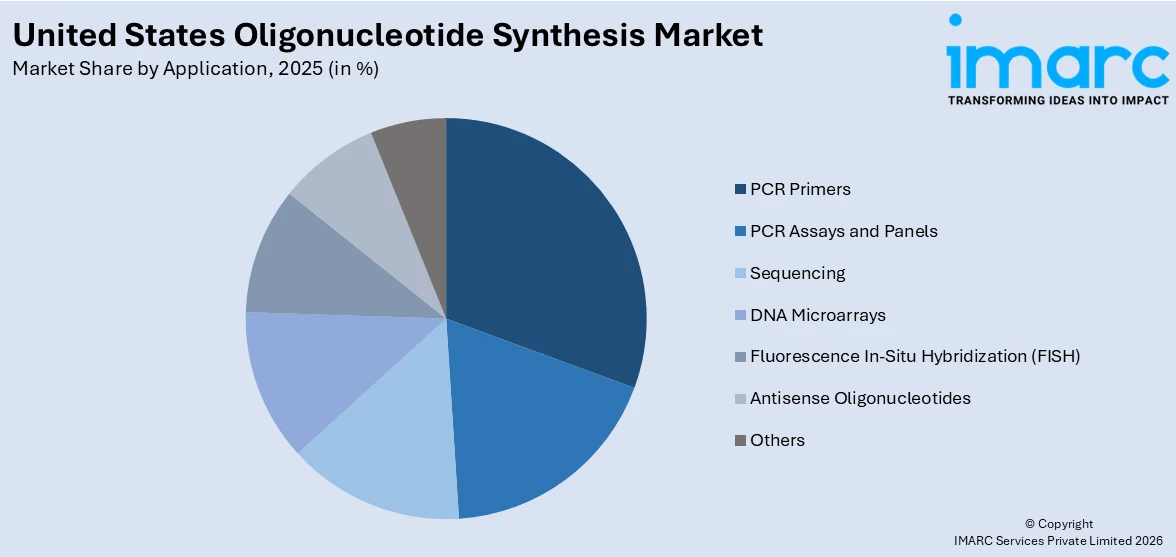

Analysis by Application:

Access the comprehensive market breakdown Request Sample

- PCR Primers

- PCR Assays and Panels

- Sequencing

- DNA Microarrays

- Fluorescence In-Situ Hybridization (FISH)

- Antisense Oligonucleotides

- Others

PCR primers are key to the amplification of a certain DNA or RNA sequence and have found importance in molecular diagnostics, research, and clinical applications. They are one of the highly demanded products, owing to the increased application of PCR in various fields, including disease diagnosis, genetic research, and forensic studies. Advances in personalized medicine and the use of PCR in pathogen detection such as during the COVID-19 pandemic emphasize the importance of PCR primers. Their versatility and necessity in multiple sectors ensure they hold a significant share of the market.

PCR assays and panels facilitate a broad analysis of multiple genetic markers in one single assay thus increasing the efficiency of diagnostics. There were marked increases in the utility for the diagnosis of infectious diseases and cancer biomarkers considering the multiplexing technologies being established. The need for rapid and accurate diagnostics in healthcare, coupled with their role in disease surveillance and treatment monitoring, drives their demand. Their growing importance in clinical and research settings ensures they maintain a large market share.

Sequencing technologies, enabled by synthesized oligonucleotides, serve at the heart of genomics study, precision medicine, and diagnostics. The adoption of next-generation sequencing (NGS) in determining genetic variations, and molecular mechanisms underlying disease, along with targeted therapy increases the growth plans for the market. Oligonucleotides aid the sequencing library preparation and secretion, leading to a steady demand. Indeed, as genomics expands into healthcare and biopharmaceuticals, sequencing remains a crucial pillar of the market, taking a significant share.

Analysis by End Use:

- Pharmaceutical and Biotechnology Companies

- Hospital and Diagnostic Laboratories

- Academic Research Institutes

The pharmaceutical and biotechnology industries are adopting oligonucleotide synthesis for advanced therapies, including antisense oligonucleotides, siRNAs, and gene-editing tools. The companies are leading personalized medicine and nucleic acid drug development innovations to consider unmet medical needs. Increased R&D investment and collaboration with synthesis providers accelerate product development. As the FDA approves more oligonucleotide-based therapies, there will undoubtedly be further applications in precision medicine, ensuring that these companies own much of the market.

Hospital and diagnostic laboratories utilize oligonucleotides for molecular diagnostics, including PCR-based pathogen detection, genetic screening, and biomarker analysis. The growing demand for rapid and accurate diagnostic solutions in clinical settings fuels their reliance on synthesized oligonucleotides. As precision medicine and point-of-care testing expand, the need for customized assays and probes rises. Laboratories’ pivotal role in disease diagnosis, monitoring, and outbreak management ensures their significant share in the market.

Academic research institutes are key drivers of demand for synthesized oligonucleotides due to their extensive use in genetic studies, functional genomics, and basic research. These include CRISPR gene editing, RNA interference, and sequencing applications. The effects of government funding and inter-institutional collaboration are making these institutions continuously source oligonucleotides high in quality and customized. Such new developments will contribute to therapeutic target and technology discovery, thereby cementing their stronghold in the market.

Regional Analysis:

- Northeast

- Midwest

- South

- West

The Northeast has also benefitted from the concentration of some of the world's most prestigious research institutions, biotech hubs, and pharmaceutical companies, which are making consistent progress in oligonucleotide synthesis through research in genomics, drug development, and diagnostics. Strong government funding in the healthcare biomedical sector and proximity to venture capital firms add to the market growth in this region.

The Midwestern hold on agri-biotechnology and precision medicine creates a surge for oligonucleotides in applications of genetic modification and research. Universities, biotechnologies, and healthcare providers are forming partnerships that will sponsor more development in genetic therapies and diagnostics.

The South sees market growth driven by its expanding healthcare sector, investments in genomic medicine, and increasing demand for oligonucleotide-based diagnostics and therapeutics. State-level funding and the presence of research parks and innovation hubs, particularly in Texas and North Carolina, contribute significantly to oligonucleotide synthesis activities.

The West leads in oligonucleotide synthesis due to its vibrant biotech ecosystem, particularly in California, with numerous startups, established firms, and academic research centers. High venture capital investment, a focus on cutting-edge therapies like CRISPR and RNA-based treatments, and advancements in technology platforms drive the region's market expansion.

Competitive Landscape:

The market in the United States is highly competitive, featuring key players like Thermo Fisher Scientific, Agilent Technologies, and Integrated DNA Technologies (IDT). These companies lead through advanced technologies, robust product portfolios, and strategic collaborations. Emerging biopharma companies also contribute with specialized oligonucleotide-based therapies. The market is characterized by increasing mergers, acquisitions, and investments to expand capabilities in high-throughput synthesis and precision medicine. Service providers are focusing on automation, cost efficiency, and customization to meet growing demand in drug development, diagnostics, and research. Innovation and scalability remain critical factors for maintaining competitive advantages in this rapidly evolving market. For instance, in late 2023, IDT announced the completion of its new Therapeutic Oligonucleotide Manufacturing facility in Iowa, which commemorated its entrance into the therapeutics space.

Latest News and Developments:

- In May 2024, Creyon Bio, Inc., a drug development company that engineers Oligonucleotide-Based Medicines (OBMs) with industry-leading efficiency creating novel, best-in-class gene-centric medicines to treat rare and common diseases, and Cajal Neuroscience, ("Cajal"), a biotechnology company integrating disease-focused genetics and human data with state-of-the-art experimental capabilities to discover novel targets and therapeutics for neurodegeneration, announced a partnership to develop novel OBMs for neurodegenerative diseases.

- In May 2024, Molecular Assemblies, Inc., a pioneer and leader in the field of enzymatic DNA synthesis, announced the launch of its Partnering Program to license Molecular Assemblies’ Fully Enzymatic SynthesisTM (FESTM) technology for onsite synthesis. FES technology accelerates the production of long, pure, and accurate DNA to power a new rapidly emerging generation of therapeutics and diagnostics. Molecular Assemblies also announced that the company has opened early access to order oligonucleotides up to 400mer in length, limited to the first 20 customers.

- In September 2024, Eurofins Genomics US announced the opening of a new world-class oligonucleotide manufacturing facility. The expansion significantly increases manufacturing capacity and capabilities, allowing Eurofins Genomics US to meet the ever-growing global demand for GMP-grade and research-use oligonucleotides.

United States Oligonucleotide Synthesis Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Synthesized Oligonucleotide Products, Reagents, Equipment, Services |

| Applications Covered | PCR Primers, PCR Assays and Panels, Sequencing, DNA Microarrays, Fluorescence In-Situ Hybridization (FISH), Antisense Oligonucleotides, Others |

| End Uses Covered | Pharmaceutical and Biotechnology Companies, Hospital and Diagnostic Laboratories, Academic Research Institutes |

| Regions Covered | Northeast, Midwest, South, West |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the United States oligonucleotide synthesis market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the United States oligonucleotide synthesis market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the United States oligonucleotide synthesis industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the United States Oligonucleotide Synthesis Market Report

Oligonucleotide synthesis is the chemical process of creating short DNA or RNA sequences (oligonucleotides) with specific nucleotide arrangements. This technique is crucial in molecular biology, diagnostics, and therapeutics, enabling applications like gene editing, PCR, and RNA-based drugs. It involves sequentially adding nucleotides using automated synthesizers.

The United States oligonucleotide synthesis market was valued at USD 1.5 Billion in 2025.

IMARC estimates the United States oligonucleotide synthesis market to exhibit a CAGR of 11.20% during 2026-2034.

The key factors driving the market are advancements in genomics, increasing demand for personalized medicine, expanding therapeutic and diagnostic applications, rising research on genetic disorders, and government funding. Technological innovations and outsourcing synthesis services further boost the growth of the market across the United States.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)