United States Package Boiler Market Size, Share, Trends and Forecast by Type, Fuel Type, Design, End Use, and Region, 2026-2034

United States Package Boiler Market Summary:

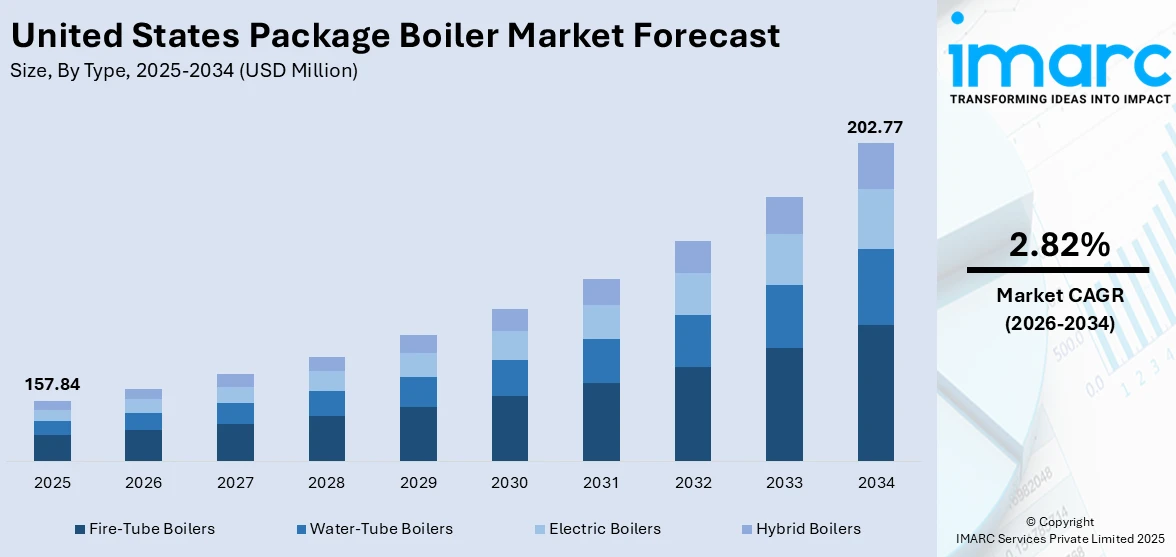

The United States package boiler market size was valued at USD 157.84 Million in 2025 and is projected to reach USD 202.77 Million by 2034, growing at a compound annual growth rate of 2.82% from 2026-2034.

The United States package boiler market is expanding steadily, as industries across the country prioritize efficient steam generation systems and low-emission heating solutions. Growing demand from the chemical, food processing, pharmaceutical, and energy sectors is driving adoption. Advancements in combustion technologies, the integration of smart automation controls, and regulatory emphasis on emission reduction are further strengthening the market share.

Key Takeaways and Insights:

- By Type: Fire-tube boilers dominate the market with a share of 42.7% in 2025, owing to their robust design, operational simplicity, and cost-effective maintenance suited for consistent low-to-medium pressure steam applications across the food processing, textile, and small-scale chemical production sectors.

- By Fuel Type: Gas leads the market with a share of 51.8% in 2025, driven by the widespread availability of natural gas infrastructure, competitive fuel pricing, and alignment with stringent federal emission standards that favor cleaner combustion alternatives over coal and oil.

- By Design: D-type exhibits a clear dominance in the market with 46.3% share in 2025, reflecting its compact configuration, reduced installation timelines, high-pressure handling capabilities, and suitability for heavy industrial applications, including power generation and large-scale manufacturing operations.

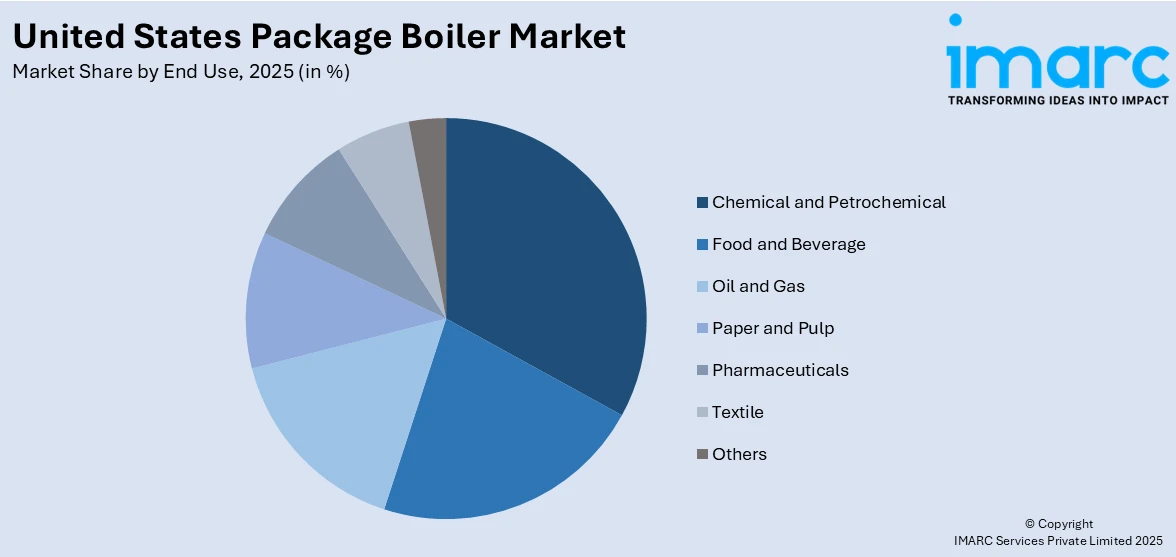

- By End Use: Chemical and petrochemical comprise the largest segment with a market share of 29.6% in 2025, driven by the sector’s intensive thermal energy requirements for processes, such as distillation, cracking, and catalytic reactions that demand reliable and efficient steam generation systems.

- By Region: South represents the largest region with 34.4% share in 2025, supported by the concentration of petrochemical facilities, refineries, and manufacturing plants along the Gulf Coast corridor, particularly in Texas and Louisiana, where industrial steam demand remains robust.

- Key Players: Key players in the United States package boiler market focus on expanding product portfolios, advancing low-emission combustion technologies, integrating digital monitoring solutions, and pursuing strategic acquisitions to strengthen market positioning, broaden service networks, and deliver energy-efficient boiler room solutions across industrial and commercial applications.

To get more information on this market Request Sample

The United States package boiler market is advancing, as industries modernize their steam generation infrastructure to meet evolving regulatory and operational requirements. A key factor shaping this progress is the growing emphasis on energy efficiency and emission compliance, which is accelerating the replacement of aging boiler systems with advanced, digitally integrated solutions. Policy support for industrial decarbonization, expanding natural gas infrastructure, and rising demand from the chemical, pharmaceutical, and food processing sectors are contributing to a more favorable environment for package boiler adoption across the country. In March 2024, the US Department of Energy (DOE) made a significant move to speed up industrial decarbonization and convert polluting heavy industries into clean production. The USD 6 Billion funding represented the biggest investment in industrial climate solutions to date and demonstrated the Biden Administration’s dedication to significantly lowering climate emissions while generating opportunities for American manufacturers and workers. In addition, the adoption of smart controls and Internet of Things (IoT)-enabled monitoring systems is enhancing operational reliability and predictive maintenance capabilities.

United States Package Boiler Market Trends:

Shift Towards Smart Boiler Technologies and Digital Integration

The United States package boiler market is witnessing rapid adoption of intelligent monitoring systems, IoT-connected sensors, and predictive maintenance platforms that enhance operational visibility and reduce unplanned downtime. As per the IMARC Group, the United States predictive maintenance market size reached USD 3.8 Billion in 2025 and is set to reach USD 20.5 Billion by 2034. These digital solutions are helping operators optimize fuel efficiency, extend equipment life, and ensure consistent compliance with federal emission standards, supporting the market growth.

Growing Adoption of Low-Emission and Electric Boiler Systems

Rising regulatory pressure to decarbonize industrial operations is driving interest in low-emission and fully electric boiler alternatives across the United States. In March 2024, AtmosZero, based in Colorado, completed a Series A funding round that would assist in speeding up the commercialization of its Boiler 2.0 technology. The unique Boiler 2.0 technology draws heat from the air and produces high-temperature steam with optimal efficiency and zero carbon emissions, enabling businesses to swiftly and affordably switch from their current natural gas and oil boilers.

Increasing Demand for Modular and Factory-Assembled Package Boilers

Industrial facilities across the United States are increasingly favoring modular, factory-assembled package boiler systems that minimize installation time and reduce on-site construction complexity. These systems offer faster commissioning, consistent manufacturing quality, and lower project risk compared to traditional field-erected boilers. Their compact footprint makes them well suited for facilities with space constraints. Additionally, modular package boilers provide greater scalability, allowing operators to add capacity incrementally as demand grows. Improved energy efficiency, ease of integration with existing plant systems, and reduced labor requirements are further driving adoption across diverse industrial applications nationwide.

Market Outlook 2026-2034:

The United States package boiler market is positioned for sustained expansion, supported by industrial modernization, regulatory emphasis on emission reduction, and growing demand from the energy-intensive manufacturing sector. The market generated a revenue of USD 157.84 Million in 2025 and is projected to reach a revenue of USD 202.77 Million by 2034, growing at a compound annual growth rate of 2.82% from 2026-2034. Increasing adoption of condensing boiler technologies, smart automation controls, and hybrid energy configurations is expected to drive higher operational efficiencies and lower lifecycle costs. The replacement of aging boiler infrastructure across chemical, food processing, and pharmaceutical facilities, combined with expanding natural gas availability and supportive industrial energy policies, will continue to foster a competitive and innovation-driven market landscape.

United States Package Boiler Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Type |

Fire-Tube Boilers |

42.7% |

|

Fuel Type |

Gas |

51.8% |

|

Design |

D-Type |

46.3% |

|

End Use |

Chemical and Petrochemical |

29.6% |

|

Region |

South |

34.4% |

Type Insights:

- Fire-Tube Boilers

- Water-Tube Boilers

- Electric Boilers

- Hybrid Boilers

Fire-tube boilers dominate with a market share of 42.7% of the total United States package boiler market in 2025.

Fire-tube boilers maintain their leadership position in the United States package boiler market due to their proven reliability, simplified maintenance requirements, and suitability for industries requiring consistent steam output at low-to-medium pressures. These systems are widely used in small-to-mid-scale chemical production facilities, food processing facilities, and textile manufacturing facilities where operational simplicity and modest footprints are important considerations. Their reduced initial investment costs make them even more alluring to industrial operators on a tight budget.

The compatibility of fire-tube boilers with low-emission burner technology and sophisticated combustion controls that assist facilities in meeting Environmental Protection Agency (EPA) criteria further supports their continued popularity. Improved fire-tube models with increased thermal efficiency, digital monitoring integration, and multi-fuel adaptability are being introduced by industry manufacturers. These developments increase operational visibility, compliance readiness, and equipment lifespan. Overall, fire-tube boilers are a reliable, future-ready option for establishments seeking both regulatory compliance and performance stability.

Fuel Type Insights:

- Oil

- Gas

- Coal

- Biomass

- Electric

Gas leads with a share of 51.8% of the total United States package boiler market in 2025.

Gas commands the largest share in the United States package boilers market, driven by the widespread availability of natural gas infrastructure, competitive pricing, and favorable combustion properties that align with EPA emission standards. The transition away from coal and oil towards cleaner-burning natural gas continues to accelerate across industrial operations seeking regulatory compliance and enhanced operational efficiency. According to the US Energy Information Administration, domestic dry natural gas production totaled 37.72 Trillion cubic feet in 2024, ensuring abundant and cost-effective fuel supply for gas-fired boiler operations.

The incorporation of sophisticated condensing technologies and programmable logic controllers that optimize thermal efficiency further solidifies the supremacy of gas-fueled package boilers. In order to optimize fuel consumption and lower greenhouse gas emissions, natural gas boilers are increasingly being combined with economizers and intelligent combustion management systems. Their accurate load-following capabilities and quick startup times support variable industrial steam demand. Furthermore, end users benefit from improved uptime and cheaper total cost of ownership, due to fewer maintenance requirements than solid-fuel systems.

Design Insights:

- D-Type

- A-Type

- O-Type

D-type comprises the largest segment with a 46.3% share of the total United States package boiler market in 2025.

D-type maintains market leadership, owing to its compact structural configuration, which significantly reduces installation time and associated costs while delivering high thermal efficiency. As D-type boilers are designed to withstand high-pressure and high-capacity operations, they are especially well-suited for heavy industrial uses, such as large-scale manufacturing, petrochemical processing, and power generation. Stable performance in energy-intensive operations is ensured by their capacity to handle quick changes in load.

D-type designs are becoming more popular because of their energy-efficient operation and adherence to strict emission regulations, which complement larger sustainability and regulatory goals across the United States. Manufacturers are constantly adding better heat recovery capabilities, digital controls, and integrated automation to D-type systems. Predictive maintenance and real-time performance improvement are made possible by these advancements. Higher uptime, increased fuel efficiency, and long-term operating cost savings are advantageous to end users.

End Use Insights:

Access the comprehensive market breakdown Request Sample

- Food and Beverage

- Chemical and Petrochemical

- Oil and Gas

- Paper and Pulp

- Pharmaceuticals

- Textile

- Others

Chemical and petrochemical exhibit a clear dominance with a 29.6% share of the total United States package boiler market in 2025.

Chemical and petrochemical drive the largest share of package boiler demand in the United States, reflecting the industry’s intensive thermal energy requirements for processes, including distillation, cracking, drying, and catalytic reactions. These operations necessitate reliable, high-capacity steam generation systems that maintain consistent pressure and temperature profiles. The concentration of chemical and petrochemical facilities along the Gulf Coast, particularly in Texas and Louisiana, further amplifies demand for package boilers in this end use category.

Beyond core process heating, package boilers play a critical role in supporting auxiliary operations, such as feedstock preheating, solvent recovery, and plant utilities, within chemical and petrochemical complexes. Ongoing capacity expansions, debottlenecking projects, and modernization of aging assets are driving replacement demand for high-efficiency boiler systems. Increasing emphasis on operational safety, emissions control, and energy optimization is encouraging facilities to adopt advanced package boilers with digital monitoring and redundancy features, ensuring uninterrupted operations and compliance across large, integrated chemical manufacturing sites.

Regional Insights:

- Northeast

- Midwest

- South

- West

South represents the leading segment with a 34.4% share of the total United States package boiler market in 2025.

South commands the largest share of the United States package boiler market, driven by the high concentration of petrochemical complexes, oil refineries, and manufacturing facilities along the Gulf Coast corridor. States, such as Texas and Louisiana, serve as major industrial hubs where steam-intensive processes across the chemical, energy, and food processing sectors sustain robust demand for package boiler systems. The region’s competitive advantage is further strengthened by abundant natural gas supply from the Permian and Haynesville basins, which provides cost-effective fuel for gas-fired boiler operations.

Furthermore, the South gains from continuous industrial growth, plant modernization initiatives, and robust capital investment inflows, which support the construction and improvement of new boilers. Efficient equipment deployment and maintenance services are supported by existing industrial infrastructure, favorable business legislation, and close access to ports. Because of the warm environment in the area, there are less seasonal operational disturbances, allowing steady industrial production all year long. All of these elements work together to support the South's dominance in the United States package boiler market.

Market Dynamics:

Growth Drivers:

Why is the United States Package Boiler Market Growing?

Expanding Industrial Activity and Manufacturing Investment

The United States is experiencing sustained growth in industrial activity, with significant investments flowing into chemical manufacturing, pharmaceutical production, food processing, and energy infrastructure. These sectors rely on package boilers as critical components for steam generation, process heating, and temperature regulation. The expansion of domestic manufacturing capacity, driven by reshoring initiatives and federal investment programs, is creating consistent demand for reliable, high-efficiency boiler systems across the country. For instance, in July 2025, AstraZeneca announced a landmark USD 50 Billion investment in the United States by 2030, aimed at expanding its manufacturing and research footprint with new facilities in Virginia, Maryland, California, Massachusetts, Texas, and Indiana. Such large-scale pharmaceutical and industrial expansions directly increase the need for clean steam generation and process heating infrastructure, positioning package boilers as essential equipment for emerging and expanding production facilities.

Stringent Environmental Regulations and Emission Compliance Requirements

Federal and state-level environmental regulations are compelling industrial operators to replace aging, high-emission boiler systems with modern, low-emission alternatives. State-specific emission limits require facilities to adopt boiler technologies that minimize particulate matter, sulfur dioxide, and nitrogen oxide emissions. This regulatory environment creates a continuous replacement cycle that benefits the package boiler market. Compliance-driven demand is accelerating the adoption of advanced combustion controls, condensing technologies, and ultra-low NOx burner systems that enhance thermal efficiency while meeting stringent emission thresholds. Simultaneously, early adoption of cleaner boiler technologies is being encouraged by grant programs and regulatory incentives. Industrial operators are increasingly integrating emissions monitoring and reporting systems to ensure ongoing compliance and operational transparency. This focus on regulation is also driving closer collaboration between boiler manufacturers and end users during system design and commissioning.

Abundant Natural Gas Supply and Cost-Competitive Fuel Access

The United States benefits from a robust natural gas infrastructure that provides industrial operators with reliable, cost-effective fuel for boiler operations. Record-level natural gas production, supported by prolific shale formations across Texas, Pennsylvania, and Louisiana, ensures stable supply conditions that favor the continued dominance of gas-fired package boilers. Low fuel costs enhance the economic viability of boiler investments, particularly for price-sensitive industrial end users seeking to optimize operational expenditures. The availability of affordable natural gas also supports the adoption of high-efficiency condensing boilers and hybrid configurations that maximize thermal output per unit of fuel consumed. Additionally, widespread pipeline connectivity and storage capacity reduce supply disruptions and price volatility for industrial consumers. This infrastructure advantage enables long-term fuel planning and supports consistent boiler performance across diverse industrial applications.

Market Restraints:

What Challenges the United States Package Boiler Market is Facing?

High Capital Costs and Extended Payback Periods

The upfront investment required for advanced package boiler systems, particularly those equipped with low-emission burners, digital controls, and condensing technologies, remains substantially higher than conventional alternatives. Industrial facilities, especially small and mid-sized operations, often face budget constraints that delay boiler modernization projects. Extended payback periods and complex return-on-investment calculations further discourage immediate adoption, slowing the pace of equipment upgrades across price-sensitive sectors.

Competition from Alternative Heating Technologies

The growing viability of electric heat pumps, solar thermal systems, and other decentralized heating alternatives is introducing competitive pressure on traditional package boiler systems. Industries pursuing aggressive decarbonization targets are increasingly evaluating non-combustion-based heating solutions that eliminate direct emissions entirely. While these technologies are still maturing for large-scale industrial applications, their improving performance and declining costs are gradually challenging the market position of conventional gas-fired and oil-fired package boilers.

Skilled labor shortages and maintenance challenges

The United States industrial sector faces a growing shortage of skilled technicians capable of installing, operating, and maintaining advanced boiler systems. Modern package boilers incorporate sophisticated controls, sensors, and automation platforms that require specialized expertise. Limited availability of trained personnel can increase installation costs, extend commissioning timelines, and elevate maintenance risks. For some operators, concerns over long-term serviceability and workforce readiness act as a restraint on adopting technologically advanced boiler solutions.

Competitive Landscape:

The United States package boiler market is characterized by the presence of established domestic and international manufacturers, competing on the basis of product efficiency, emission performance, service network strength, and technological innovation. Companies are investing in digital boiler management platforms, advanced combustion systems, and modular product configurations to differentiate their offerings. Strategic acquisitions and partnerships are reshaping the competitive landscape, as firms seek to expand market reach, enhance research capabilities, and deliver integrated boiler room solutions. The growing emphasis on sustainability and regulatory compliance is further driving competition towards low-emission, energy-efficient product development.

United States Package Boiler Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Types Covered |

Fire-Tube Boilers, Water-Tube Boilers, Electric Boilers, Hybrid Boilers |

|

Fuel Types Covered |

Oil, Gas, Coal, Biomass, Electric |

|

Designs Covered |

D-Type, A-Type, O-Type |

|

End Uses Covered |

Food and Beverage, Chemical and Petrochemical, Oil and Gas, Paper and Pulp, Pharmaceuticals, Textile, Others |

|

Regions Covered |

Northeast, Midwest, South, West |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the United States Package Boiler Market Report

The United States package boiler market size was valued at USD 157.84 Million in 2025.

The United States package boiler market is expected to grow at a compound annual growth rate of 2.82% from 2026-2034 to reach USD 202.77 Million by 2034.

Fire-tube boilers dominated the market with a share of 42.7%, driven by their robust design, operational simplicity, cost-effective maintenance, and widespread suitability for low-to-medium pressure steam applications across the food processing and chemical manufacturing sectors.

Key factors driving the United States package boiler market include expanding industrial manufacturing activity, stringent environmental regulations mandating low-emission boiler technologies, abundant natural gas supply, growing demand from chemical and pharmaceutical sectors, and adoption of smart digital boiler management platforms.

Major challenges include high capital costs for advanced boiler systems, complex and fragmented regulatory compliance requirements across jurisdictions, competition from alternative heating technologies, supply chain constraints for specialized components, and workforce shortages in boiler installation and maintenance services.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)