United States Palm Oil Market Size, Share, Trends and Forecast by Application and Region, 2026-2034

United States Palm Oil Market Size, Share, Trends & Forecast (2026-2034)

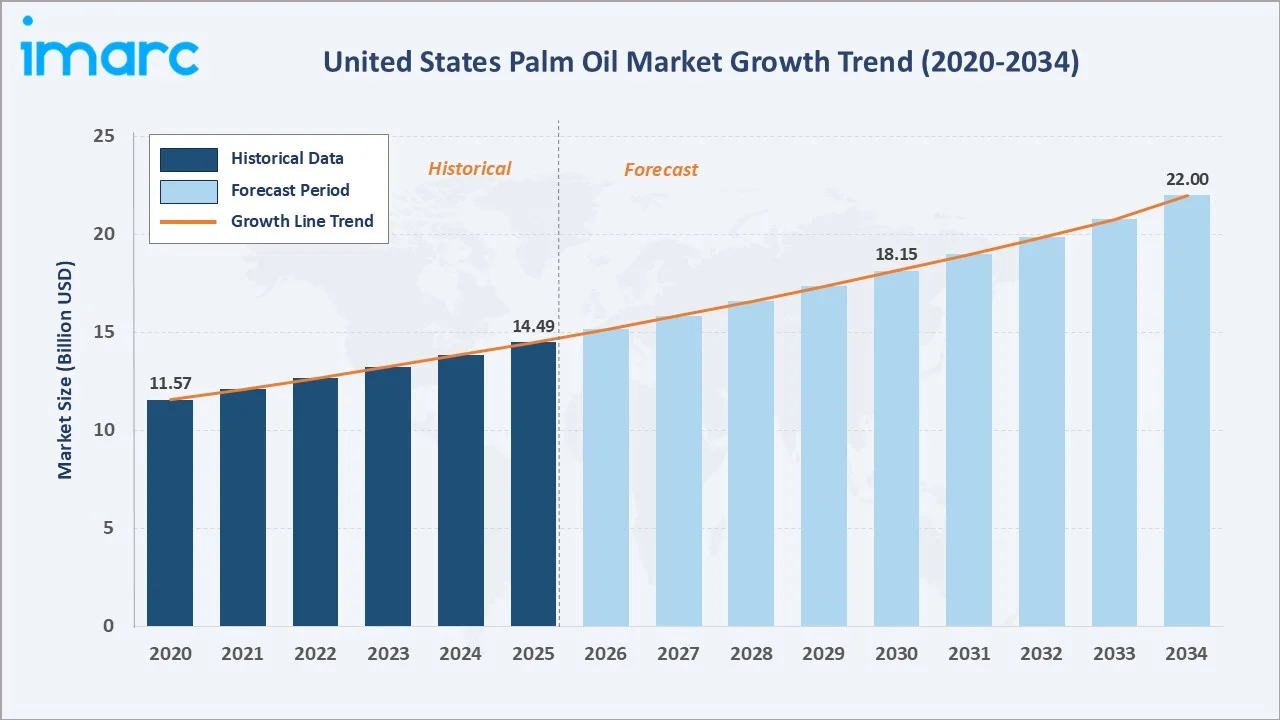

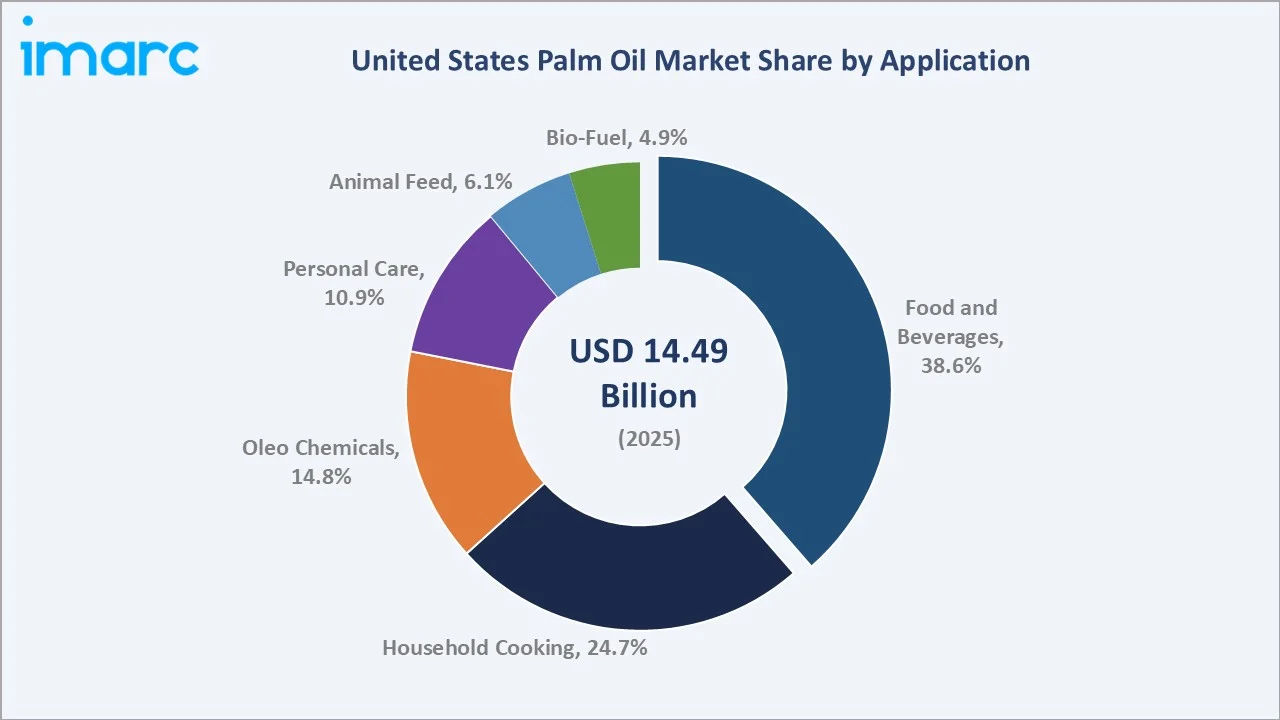

The United States palm oil market was valued at USD 14.49 Billion in 2025 and is projected to reach USD 22.00 Billion by 2034, exhibiting a CAGR of 4.61% during 2026-2034. Rising processed food consumption, cost competitiveness against alternative oils, broadening oleo chemical applications, and expanding bio-fuel mandates are the primary drivers shaping the market growth.

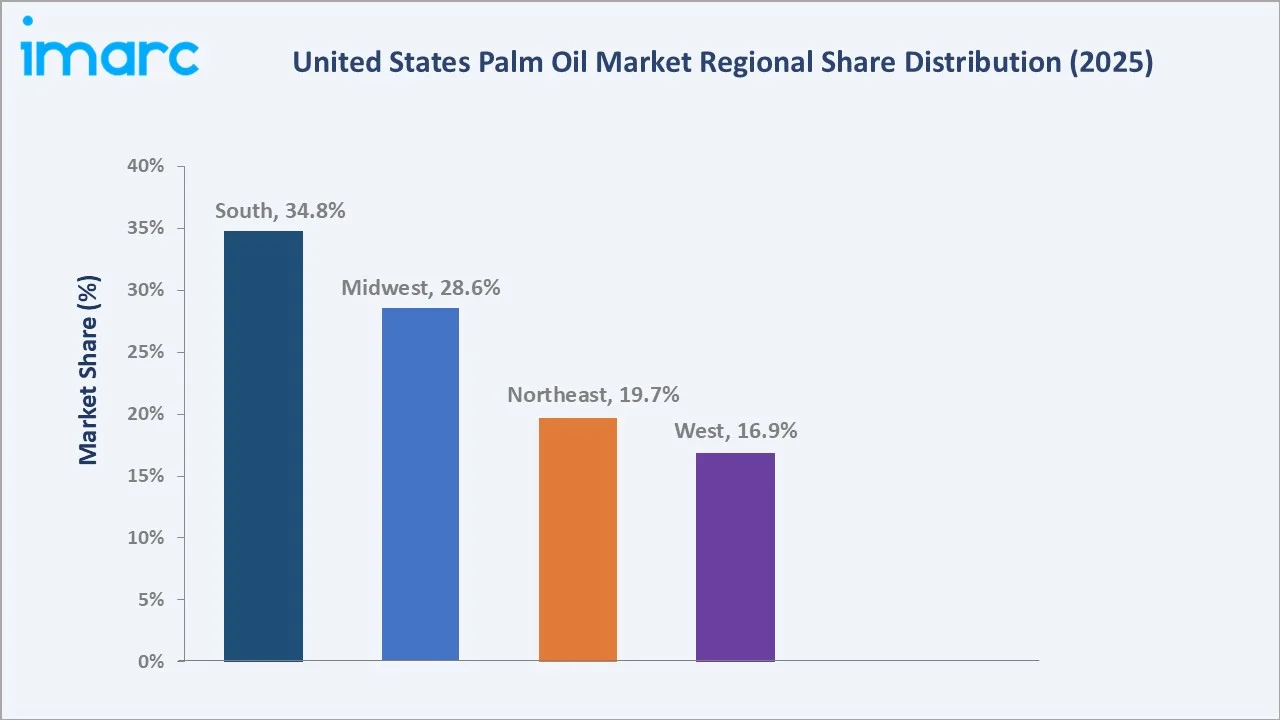

Food and beverages lead the application segment at 38.6% and South commands 34.8% regional share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 14.49 Billion |

|

Forecast Market Size (2034) |

USD 22.00 Billion |

|

CAGR (2026-2034) |

4.61% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

South (34.8%, 2025) |

|

Second Largest Region |

Midwest (28.6%, 2025) |

|

Leading Application |

Food and Beverages (38.6%, 2025) |

The United States palm oil market expanded from USD 11.57 Billion in 2020 to USD 14.49 Billion in 2025, driven by rising demand in packaged food manufacturing, growth in oleo chemical derivatives, and increasing bio-fuel blending requirements. Anchored at USD 18.15 Billion in 2030, the forecast to USD 22.00 Billion by 2034 is supported by expanding certified sustainable palm oil adoption, deeper integration into personal care formulations, and growing animal feed applications.

To get more information on this market, Request Sample

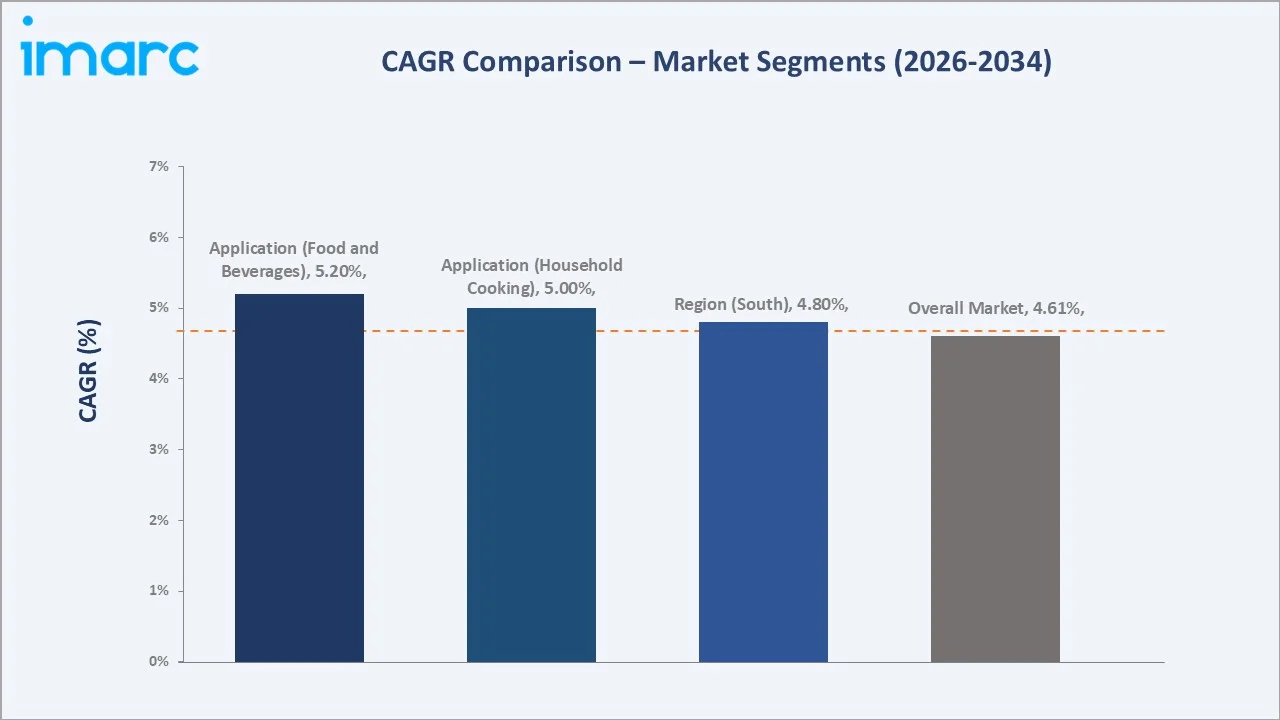

CAGR trajectories across application and regional sub-segments show oleo chemicals and household cooking expanding in line with or above the overall 4.61% market CAGR, driven by cost-competitiveness, wide formulation utility, and steady import volumes supporting domestic supply chains.

Executive Summary

The United States palm oil market is on a steady growth trajectory from USD 11.57 Billion in 2020 to USD 22.00 Billion by 2034. The segment has evolved from a basic commodity import to a strategically sourced ingredient across food manufacturing, personal care, oleo chemical production, animal feed, and bio-fuel sectors. Competitive pricing relative to alternatives, broad functionality, and a maturing certified sustainable supply chain are encouraging manufacturers to retain palm oil as a core ingredient across multiple categories.

Food and beverages dominate the application segment at 38.6% in 2025, supported by palm oil's wide use in bakery fats, frying oils, margarines, confectionery coatings, and packaged food formulations. South commands 34.8% regional share, anchored by extensive food processing infrastructure, Gulf Coast import infrastructure, and a large base of oleo chemical and biodiesel producers.

Key Market Insights

|

Insight |

Data |

|

Leading Application |

Food and Beverages – 38.6% share (2025) |

|

Second Largest Application |

Household Cooking – 24.7% share (2025) |

|

Leading Region |

South – 34.8% share (2025) |

|

Second Largest Region |

Midwest – 28.6% share (2025) |

|

Top Companies |

Cargill, Incorporated, Bunge, Wilmar International Ltd, ADM, Golden Agri-Resources Ltd., and Musim Mas Group |

Key Analytical Observations Supporting the Above Data:

- Food and beverages leadership at 38.6% is supported by palm oil's versatility in bakery applications, confectionery, frying oils, and processed snack formulations. Its semi-solid texture, oxidative stability, and cost efficiency make it a preferred alternative to trans-fat-containing partially hydrogenated oils in modern food manufacturing.

- Household cooking share at 24.7% reflects the continued use of palm-blended cooking oils across grocery retail channels, particularly in Southern and Midwestern markets where price sensitivity drives consumer purchasing decisions.

- South at 34.8% leads regional share, anchored by an extensive food manufacturing and distribution corridor, proximity to Gulf Coast import infrastructure, and a concentrated base of oleo chemical and biodiesel production facilities across Texas, Louisiana, and Georgia.

- Midwest at 28.6% is the second largest region, underpinned by large-scale agricultural and chemical processing, growing biodiesel mandates, and proximity to major corn-soy processing complexes that integrate palm derivatives into mixed feed and fuel blends.

United States Palm Oil Market Overview

Palm oil is a versatile edible vegetable oil derived from the fruit of the oil palm tree (Elaeis guineensis), predominantly sourced from Malaysia and Indonesia. In the United States, it is refined into several grades like refined, bleached, and deodorized (RBD) palm oil, palm olein, palm stearin, and palm kernel oil, each serving distinct food, industrial, and energy applications.

The United States market ecosystem integrates upstream importers and commodity traders, domestic refiners and fractionators, food and oleo chemical manufacturers, personal care and pharmaceutical processors, bio-fuel producers, and a broad distribution network reaching retail, food service, and industrial end-users. Regulatory oversight from the USDA, FDA, and EPA shapes import standards, labelling requirements, and bio-fuel blend mandates, while RSPO certification increasingly defines sustainable sourcing expectations.

Market Dynamics

To evaluate market opportunities, Request Sample

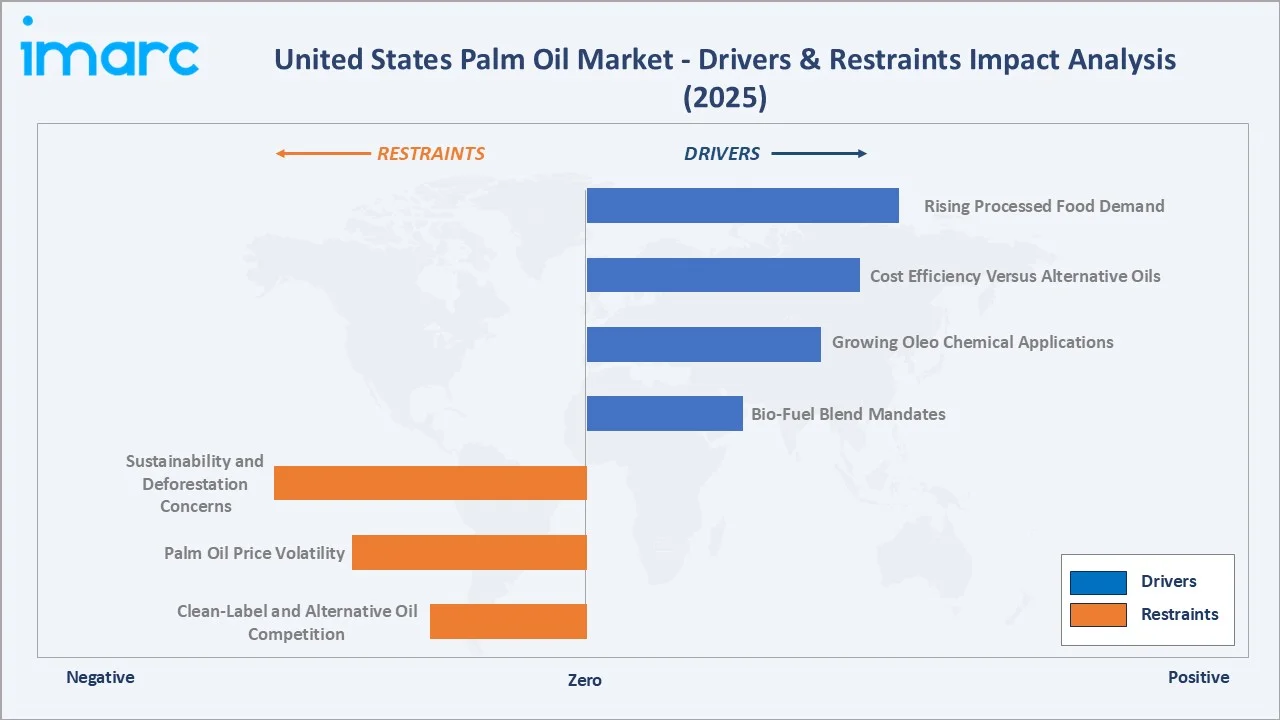

Market Drivers

- Rising Processed Food Demand: Expanding consumption of packaged, convenience, and fast food products in the United States is sustaining strong demand for palm oil as a preferred frying fat, baking shortening, and emulsifier. As per IMARC Group, the United States convenience food market size was valued at USD 16.4 Billion in 2025. Palm oil’s thermal stability, extended shelf life, and cost efficiency compared with butter and other tropical oils make it the preferred ingredient for large-scale food processors.

- Cost Efficiency Versus Alternative Oils: Palm oil consistently trades at a price discount to soybean, sunflower, and canola oils on a per-unit functional basis, making it an economically rational choice for food manufacturers, oleo chemical producers, and bio-fuel blenders operating under tight margin constraints.

- Growing Oleo Chemical Applications: Expanding use of palm-derived fatty acids, glycerol, and methyl esters in surfactants, lubricants, bio-plastics, and specialty chemicals is broadening demand beyond food applications. Oleo chemical producers in the United States are increasingly substituting petrochemical inputs with bio-based palm derivatives to meet corporate sustainability targets.

- Bio-Fuel Blend Mandates: State-level renewable fuel standards support growing demand for palm-based biodiesel and renewable diesel. The United States EPA has increasingly recognized palm-derived biodiesel pathways under the RFS, broadening the feedstock's qualification for bio-fuel production incentives and strengthening long-term demand.

Market Restraints

- Sustainability and Deforestation Concerns: Growing awareness of palm oil's link to tropical deforestation, biodiversity loss, and peatland destruction in Southeast Asia continues to generate consumer and regulatory pressure. Major United States retailers and food brands are under sustained pressure to achieve RSPO-certified sourcing targets, raising procurement complexity and cost.

- Palm Oil Price Volatility: Global crude palm oil prices are subject to significant fluctuations driven by weather conditions in Indonesia and Malaysia, competing bio-fuel demand, and currency movements. These supply-side dynamics translate into procurement cost uncertainty for United States food manufacturers and industrial processors, complicating budgeting and contract pricing.

- Clean-Label and Alternative Oil Competition: Growing consumer preference for clean-label, minimally processed, and locally sourced ingredients is driving some food manufacturers to explore alternative oils such as high-oleic sunflower, avocado, and coconut oil, creating substitution pressure in premium food product formulations.

Market Opportunities

- Certified Sustainable Palm Oil Adoption: Growing corporate sustainability commitments from major food and consumer goods companies are creating a premium-priced demand tier for RSPO-certified palm oil, rewarding suppliers with traceable, deforestation-free supply chains.

- Oleo Chemical Expansion: Rising demand for bio-based alternatives to petrochemicals in surfactants, lubricants, and specialty chemicals is opening significant growth avenues for palm-derived oleo chemical producers, particularly those with integrated supply chains.

- Personal Care and Pharmaceutical Growth: Expanding market for plant-derived cosmetics, personal care formulations, and nutraceuticals is generating new demand for palm kernel oil derivatives, offering diversification opportunity beyond commodity food-grade applications.

Market Challenges

- Supply Chain Traceability and Transparency: Establishing mill-to-field traceability across complex global palm oil supply chains remains a significant operational and cost challenge for United States importers and manufacturers seeking to meet evolving sustainability disclosure requirements.

- Regulatory and Labelling Compliance: Evolving FDA and retailer labelling mandates, combined with increasing attention to palm oil in ingredient declarations, are requiring manufacturers to invest in reformulation, supply chain auditing, and consumer communication programs.

Emerging Market Trends

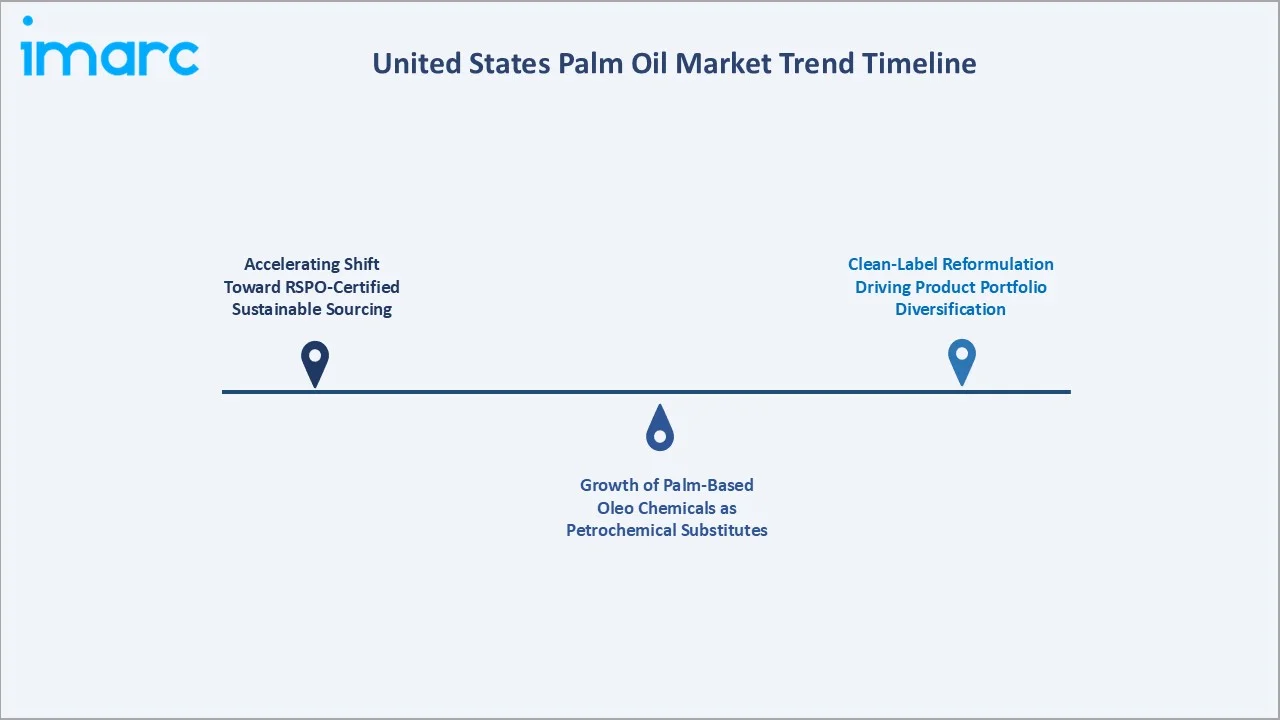

1. Accelerating Shift Toward RSPO-Certified Sustainable Sourcing

Major United States food manufacturers, retailers, and personal care companies are accelerating adoption of RSPO certified supply. This trend is encouraging greater procurement of certified palm oil volumes and strengthening sustainability standards across the palm oil value chain. Growing preference for sustainably sourced ingredients is also influencing supplier selection and long-term purchasing strategies across downstream industries.

2. Growth of Palm-Based Oleo Chemicals as Petrochemical Substitutes

United States manufacturers are increasingly substituting petroleum-derived inputs with palm-based oleo chemicals in surfactants, lubricants, coatings, and bio-plastics. The transition is accelerating as corporate net-zero commitments drive bio-based raw material mandates and as the cost competitiveness of palm-derived fatty acids versus petrochemicals improves. Oleo chemical producers are investing in expanded capacity and new downstream derivative capabilities to capture this structural demand shift.

3. Clean-Label Reformulation Driving Product Portfolio Diversification

Growing consumer and retailer pressure for clean-label, minimally processed formulations is pushing palm oil users in food manufacturing to invest in sustainably certified variants and to explore functional replacements such as high-oleic sunflower and shea in specific product categories. This trend is creating a two-track market where commodity-grade palm oil volumes remain stable in industrial applications while premium certified grades command higher prices in branded consumer food and personal care products.

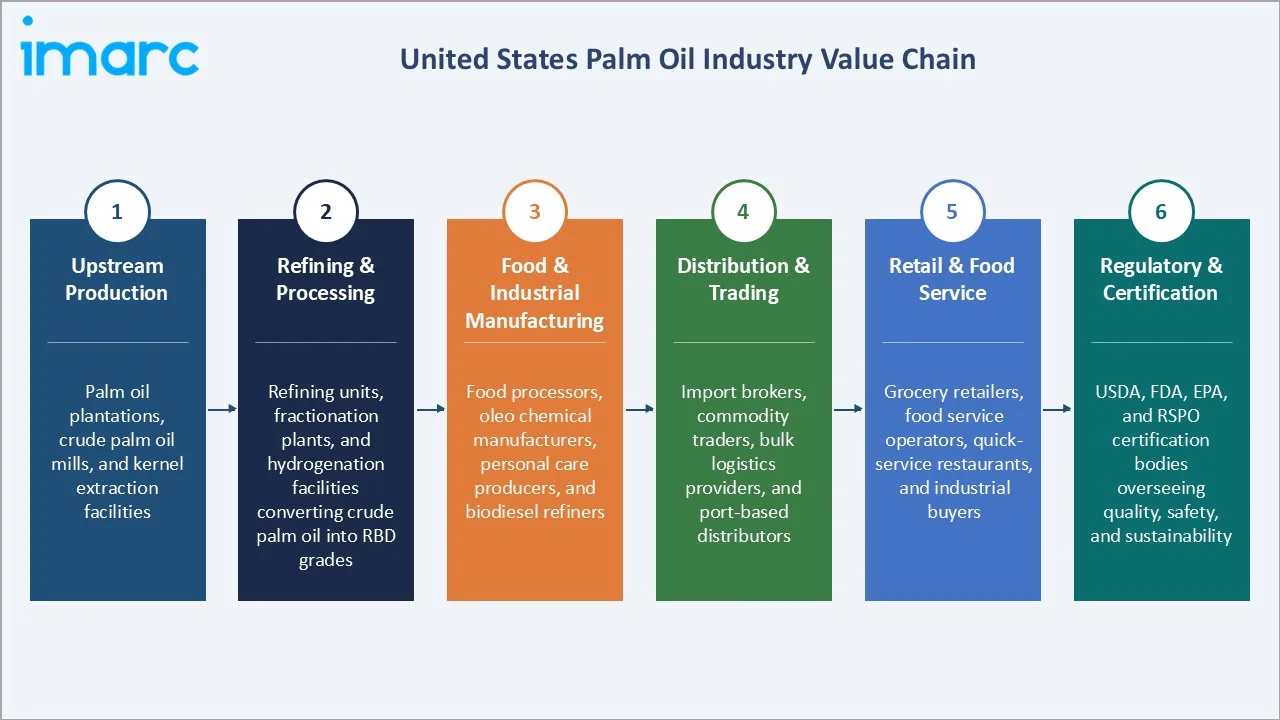

Industry Value Chain Analysis

The United States palm oil market value chain spans six stages from upstream tropical production through domestic refining, manufacturing, distribution, retail, and regulatory compliance. Refining, food manufacturing, and oleo chemical conversion capture the highest value-add within the domestic market, while importers and commodity traders play a critical intermediary role between offshore producing regions and the United States industrial and consumer base.

|

Stage |

Key Players / Examples |

|

Upstream Production |

Palm oil plantations, crude palm oil mills, and kernel extraction facilities supplying raw material to refiners |

|

Refining & Processing |

Refining units, fractionation plants, and hydrogenation facilities converting crude palm oil into refined, bleached, and deodorized (RBD) grades |

|

Food & Industrial Manufacturing |

Food processors, oleo chemical manufacturers, personal care producers, and biodiesel refiners converting RBD palm oil into end-use products |

|

Distribution & Trading |

Import brokers, commodity traders, bulk logistics providers, and port-based distributors managing supply flow to end-users |

|

Retail & Food Service |

Grocery retailers, food service operators, quick-service restaurant chains, and industrial buyers consuming refined palm oil |

|

Regulatory & Certification |

USDA, FDA, EPA, and RSPO certification bodies overseeing quality, safety, and sustainability compliance |

Integrated operators with direct import relationships, on-shore refining capacity, and diversified downstream customer bases are positioned to capture greater value than commodity-only brokers reliant on spot market procurement. RSPO certification and supply chain transparency capabilities are increasingly becoming competitive differentiators at each stage of the chain.

Technology Landscape in the United States Palm Oil Industry

Advanced Refining and Fractionation Technology

Modern palm oil refining facilities in the United States utilize continuous physical refining, dry fractionation, and enzymatic interesterification processes to produce high-purity RBD palm oil, palm olein, and palm stearin grades tailored to specific food and industrial applications. These technologies enable tighter quality control, lower process losses, and improved yield efficiency compared to older chemical refining approaches.

Blockchain and Digital Traceability Platforms

Leading United States importers and food manufacturers are deploying blockchain-based traceability platforms to map palm oil supply chains from plantation to processing facility. These tools provide real-time mill-level data, geospatial mapping of sourcing areas, and deforestation risk scores, enabling companies to meet retailer and investor disclosure requirements and to demonstrate commitment to no-deforestation, no-peat, and no-exploitation (NDPE) sourcing policies.

AI and Data Analytics in Supply Chain Management

AI and machine learning (ML) tools are being applied to optimize palm oil procurement, blending, and inventory management. Predictive analytics models are helping buyers anticipate price movements, manage currency and freight risk, and optimize contract timing, while quality monitoring systems using spectroscopic and near-infrared sensing are enabling faster in-line quality verification at refining and processing facilities.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Application |

Food and Beverages |

38.6% |

2025 |

|

Region |

South |

34.8% |

2025 |

By Application

Food and beverages command a 38.6% majority share in 2025, driven by palm oil's essential role as a frying fat, baking shortening, confectionery fat, and emulsifier across packaged food, snack, bakery, and quick-service restaurant supply chains. Its high oxidative stability, functional versatility, and cost efficiency versus alternative vegetable fats make it the dominant ingredient in large-scale United States food manufacturing.

To access detailed market analysis, Request Sample

Household cooking accounts for 24.7% in 2025, reflecting sustained consumer use of palm-blended cooking oil products across retail channels in the South and Midwest markets.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

South |

34.8% |

Large food processing base, strong household cooking oil demand, extensive food manufacturing clusters, and proximity to Gulf Coast import terminals |

|

Midwest |

28.6% |

High soybean and oleo chemical industrial activity, robust food manufacturing presence, large agricultural processing corridors, and growing biodiesel adoption |

|

Northeast |

19.7% |

Dense urban consumer base, strong personal care and pharmaceutical demand, established distribution networks, and high packaged food consumption |

|

West |

16.9% |

Growing food service industry, rising demand for sustainable certified palm oil, expanding health and wellness product categories, and port-driven import activity |

South at 34.8% in 2025 leads the regional landscape, anchored by Texas, Louisiana, Georgia, and Florida. Extensive food processing infrastructure, Gulf Coast import terminal access, and a concentrated base of oleo chemical and biodiesel production facilities support sustained regional leadership across both food-grade and industrial palm oil applications.

Midwest at 28.6% is the second-largest region. Large-scale agricultural and oleo chemical processing, growing biodiesel mandates in Midwest states, and proximity to major corn and soy processing complexes that integrate palm derivatives into mixed feed and fuel blends support strong regional demand.

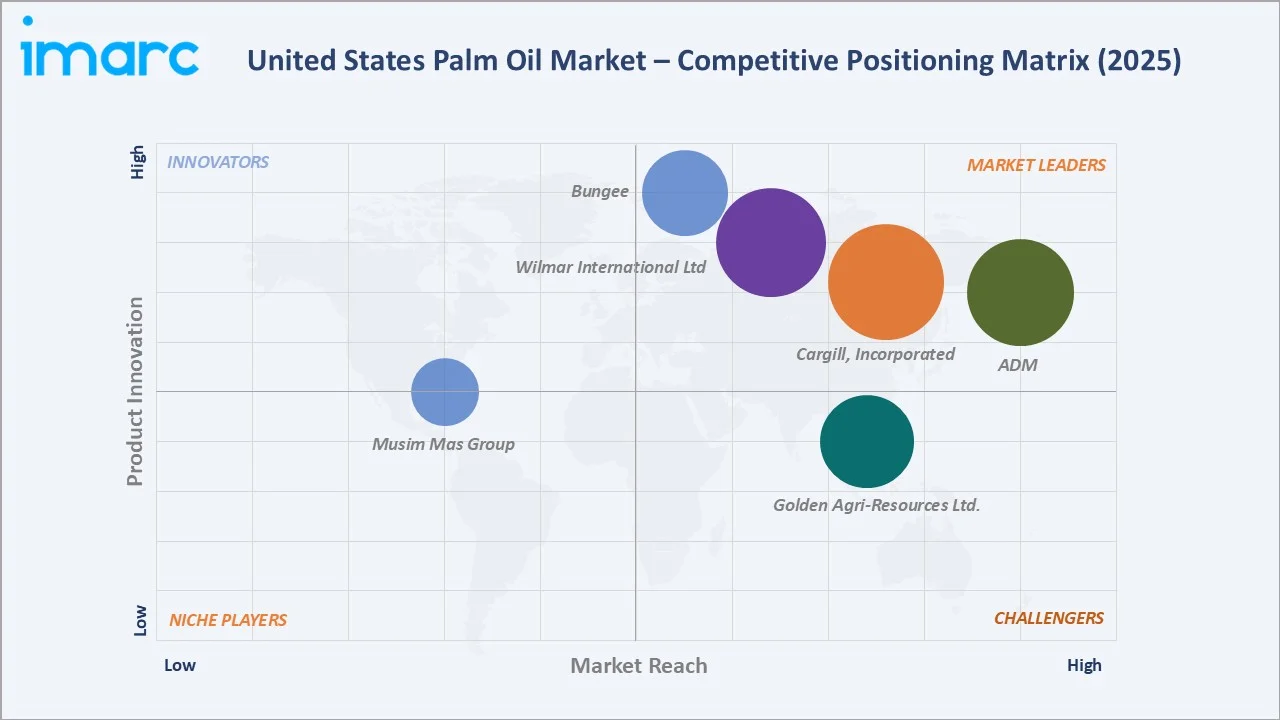

Competitive Landscape

The United States palm oil market is moderately concentrated, with a small number of integrated global commodity firms commanding significant import, refining, and distribution scale. Brand strength, supply chain depth, certification credentials, and downstream customer relationships form the key competitive moats in an environment where sustainability commitments increasingly differentiate leading players from emerging challengers.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Cargill, Incorporated |

Cargill |

Leader |

Integrated supply chain management with RSPO-certified-only palm oil supply from refineries |

|

Bunge |

Bunge Loders Croklaan |

Leader |

Specialty fats and oils innovation with sustainability-led sourcing and B2B food ingredient focus |

|

Wilmar International Ltd |

Wilmar |

Leader |

Vertically integrated palm oil supply chain with broad food, industrial, and oleochemical applications |

|

ADM |

Edible & Specialty Oil |

Leader |

Procurement, processing, and merchandising of palm oil and oilseed products through an integrated edible oils and specialty fats supply chain |

|

Golden Agri-Resources Ltd. |

Victory Tropical Oil USA |

Challenger |

Integrated plantation-to-refinery palm oil operations with certified sustainable supply to United States customers |

|

Musim Mas Group |

ICOF |

Emerging |

Integrated palm oil and oleo chemical supply with United States market access |

Key players include Cargill, Incorporated, Bunge, Wilmar International Ltd, ADM, Golden Agri-Resources Ltd., and Musim Mas Group, among others.

Key Company Profiles

Cargill, Incorporated

Cargill, Incorporated is one of the largest privately held corporations in the United States, headquartered in Minnesota. The company is a major global supplier of agricultural commodities, food ingredients, and risk management services, with an extensive palm oil procurement, refining, and distribution network serving food manufacturers, oleo chemical producers, and personal care companies across the United States.

- Product Portfolio: Refined palm oil, palm olein, palm stearin, and palm kernel oil supplied under RSPO-certified sustainable sourcing programs, serving food processing, oleo chemical, personal care, and bio-fuel applications in the United States.

- Recent Developments: The firm has continued to strengthen its sustainable sourcing initiatives, enhance supply chain traceability, and expand partnerships across the food, personal care, and industrial sectors to support evolving customer requirements and regulatory expectations.

- Strategic Focus: Deepening sustainable palm oil supply chain integration, expanding certified and traceable supply offerings, and growing value-added specialty fats and oleo-chemical product lines for food and industrial customers across the United States.

Bunge

Bunge is a global agribusiness and food company with operations spanning oilseed processing, grain trading, food ingredient manufacturing, and edible oils refining. The company maintains an extensive global sourcing, processing, and distribution network that supports supply chains across the food, feed, and industrial sectors.

- Product Portfolio: Specialty palm-based fats and oils for bakery, confectionery, infant nutrition, dairy alternatives, and food service applications, supplied to food manufacturers under the Bunge Loders Croklaan brand with RSPO-certified sustainable sourcing options.

- Recent Developments: Bunge has been advancing its sustainable palm oil sourcing and specialty fats product portfolio, expanding its certified supply capabilities, and investing in innovation to meet growing food manufacturer demand for functional and sustainably sourced palm-based ingredients.

- Strategic Focus: Driving specialty fat and functional oil innovation for food manufacturers, growing its sustainably certified palm-based product portfolio, and expanding customer service capabilities across bakery, confectionery, infant nutrition, and dairy alternative applications.

ADM

ADM is an American multinational food processing and agricultural commodities trading corporation headquartered in Chicago, Illinois. The company processes, merchandises, and distributes a broad range of agricultural commodities, including palm oil and palm kernel oil, serving food manufacturers, oleo chemical producers, animal feed customers, and bio-fuel producers across the United States.

- Product Portfolio: Refined palm oil, palm kernel oil, and specialty fats for bakery, confectionery, food service, and industrial applications, alongside edible oils, oilseed proteins, and bio-fuel feedstocks for customers across North America.

- Recent Developments: ADM has been investing in sustainable sourcing capabilities, expanding its edible and specialty oils product range, and growing its integrated oilseed processing and palm oil distribution business to meet evolving food manufacturer and industrial customer requirements across the United States.

- Strategic Focus: Procurement, processing, and merchandising of palm oil and oilseed products through an integrated edible oils and specialty fats supply chain, with growing emphasis on sustainable sourcing, supply chain transparency, and value-added ingredient solutions.

Market Concentration Analysis

The United States palm oil market is moderately concentrated, with the top four operators – Cargill, Incorporated, Bunge, Wilmar International Ltd, and ADM – collectively accounting for a significant majority of palm oil import, refining, and distribution activity across food, industrial, and personal care applications.

Barriers to entry include high capital requirements for refining infrastructure, established long-term supplier and customer relationships, RSPO certification and compliance costs, and the scale advantages available to integrated global commodity players. These factors favor well-capitalized incumbents with diversified palm oil supply chains and established United States distribution networks.

Consolidation trends are visible as mid-sized specialty fat companies partner with or are acquired by larger commodity trading groups seeking to expand downstream value-added capabilities. Strategic investment in traceability technology, sustainability certification, and oleo chemical derivative expansion is further differentiating leading players and raising entry barriers for smaller operators.

Investment & Growth Opportunities

Fastest-Growing Segments

Oleo chemicals are expanding the fastest among application segments, driven by growing demand for bio-based alternatives to petrochemicals in surfactants, lubricants, and specialty chemical applications. Personal care is the next-fastest growing application, supported by expanding demand for plant-derived cosmetic and personal care formulations across premium and mass-market categories.

Emerging Markets

Midwest is growing rapidly, supported by biodiesel mandate expansion, agricultural processing integration, and the growing oleo chemical cluster developing around established corn and soy processing infrastructure. West at 16.9% represents significant untapped potential, as health-oriented consumers, expanding food service networks, and port-driven import infrastructure create favorable conditions for sustainable certified palm oil demand growth.

Venture & Investment Trends

Investment is flowing into RSPO certification infrastructure, blockchain-enabled traceability platforms, and bio-fuel refinery capacity capable of processing palm-based feedstocks for renewable diesel and sustainable aviation fuel. Capital is also being directed toward oleo chemical expansion facilities and specialty fat processing capabilities serving high-growth personal care and pharmaceutical ingredient markets.

Future Market Outlook (2026-2034)

The United States palm oil market is forecast to expand from USD 14.49 Billion in 2025 to USD 22.00 Billion by 2034 at a CAGR of 4.61%, adding roughly USD 7.51 Billion in incremental market value over the forecast period.

Four forces will shape the market through 2034: a maturing sustainable sourcing and certification framework; the rise of bio-fuel and oleo chemical demand beyond food applications; deeper integration with health and wellness and personal care product supply chains; and structural supply chain restructuring toward traceable, deforestation-free sourcing.

By 2034, palm oil demand in the United States is expected to be characterized by a more segmented market structure, with commodity-grade palm oil volumes concentrated in industrial, bio-fuel, and animal feed applications, and premium certified sustainable palm oil commanding a growing share of food manufacturing and personal care procurement. Regulatory frameworks, corporate ESG commitments, and consumer labelling awareness are expected to further accelerate the transition toward verified sustainable supply chains.

Research Methodology

Primary Research

Primary research included structured interviews with import managers, refinery executives, food ingredient buyers, oleo chemical producers, personal care formulators, bio-fuel procurement leads, and sustainability officers, validating market sizing, application mix evolution, regional demand patterns, and competitive positioning within the United States palm oil value chain.

Secondary Research

Secondary sources included USDA Foreign Agricultural Service palm oil import data, RSPO annual reports, FDA ingredient labelling guidance, industry association publications from the American Palm Oil Council and National Oilseed Processors Association, and annual reports and sustainability disclosures from leading market participants.

Forecasting Models

Market forecasts used top-down and bottom-up models combining palm oil import volumes, application-level demand growth rates, pricing dynamics, bio-fuel mandate trajectories, and macroeconomic variables. Scenario analysis addressed sustainable sourcing adoption pace, commodity price cycles, regulatory changes, and substitution risk from alternative vegetable oils.

United States Palm Oil Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Applications Covered | Household Cooking, Food and Beverages, Oleo Chemicals, Personal Care, Animal Feed, Bio-Fuel |

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered |

Cargill, Incorporated, Bunge, Wilmar International Ltd, ADM, Golden Agri-Resources Ltd., Musim Mas Group, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the United States palm oil market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the United States palm oil market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the United States palm oil industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the United States Palm Oil Market Report

The United States palm oil market was valued at USD 14.49 Billion in 2025, fueled by strong demand from the food processing industry, widespread use in personal care and industrial applications, and its cost-effective functional properties.

The market is projected to grow at a CAGR of 4.61% from 2026-2034, reaching 22.00 Billion, driven by expanding food processing demand, bio-fuel mandates, and growing oleo chemical applications.

Market drivers in the United States palm oil market are mainly driven by its growing usage in processed foods, bakery, and confectionery owing to its long shelf life and stability. Increasing demand for renewable biofuels, heightened preference for trans-fat-free options, and affordability of palm oil in comparison to other vegetable oils are further driving its adoption in food, industrial, and energy applications.

South dominates with 34.8% share in 2025, supported by a large food manufacturing base, proximity to Gulf Coast import terminals, and strong household cooking oil demand.

Leading players include Cargill, Incorporated, Bunge, Wilmar International Ltd, ADM, Golden Agri-Resources Ltd., and Musim Mas Group, among others.

Key drivers include rising processed food consumption, cost competitiveness versus alternative oils, expanding oleo chemical applications, and growing bio-fuel blend mandates.

Key restraints include sustainability and deforestation concerns, palm oil price volatility linked to global commodity markets, and growing consumer preference for clean-label alternatives.

Global crude palm oil prices are subject to significant fluctuations driven by supply conditions from Malaysia and Indonesia, directly affecting cost structures for United States food manufacturers and industrial processors.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade