United States Pharmaceutical Contract Packaging Market Size, Share, Trends and Forecast by Industry, Type, Packaging, and Region, 2026-2034

United States Pharmaceutical Contract Packaging Market Size, Share, Trends & Forecast (2026-2034)

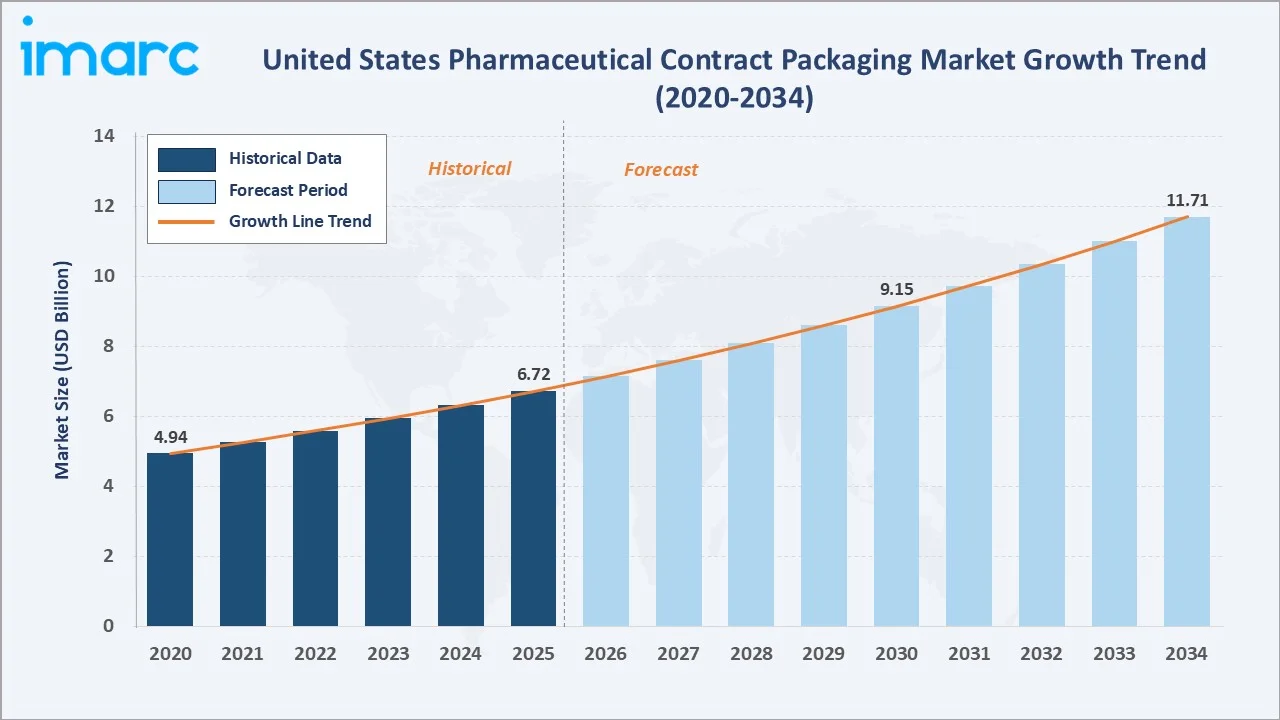

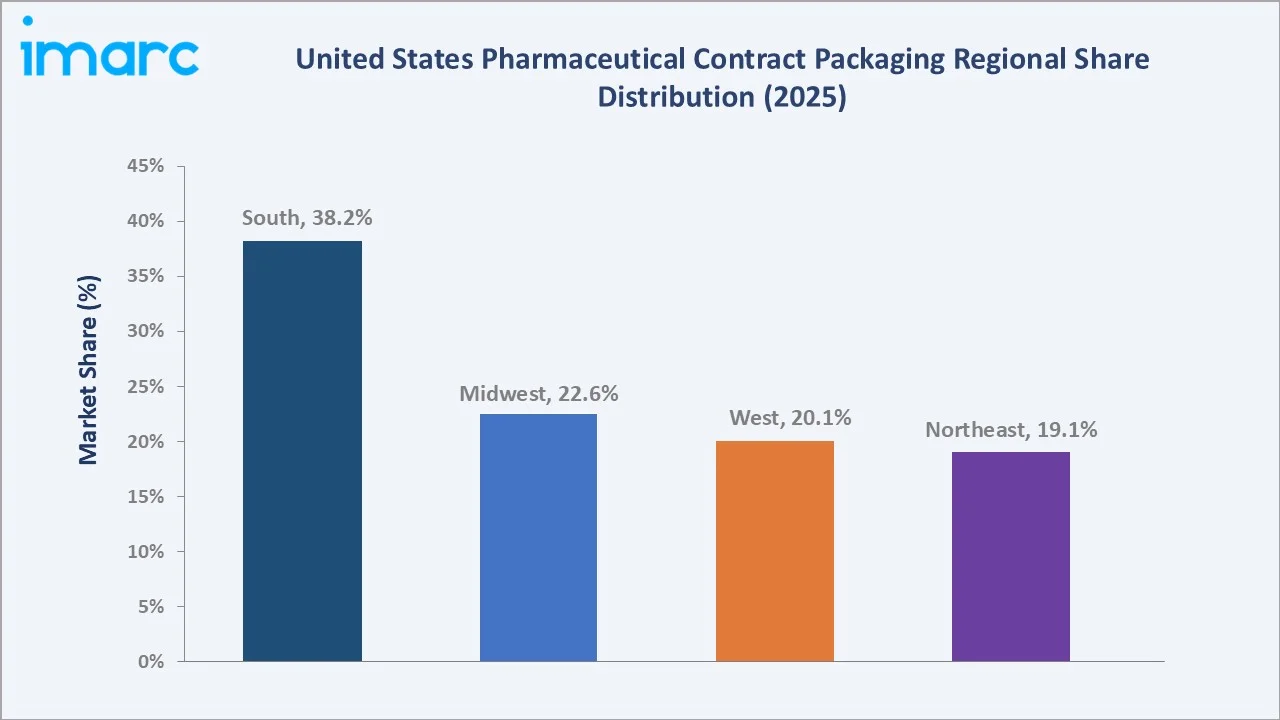

The United States pharmaceutical contract packaging market size was valued at USD 6.72 Billion in 2025 and is projected to reach USD 11.71 Billion by 2034, exhibiting a CAGR of 6.36% during the forecast period 2026-2034. Sustained pharmaceutical outsourcing, the GLP-1 and biologics surge, and full DSCSA serialization enforcement are driving the United States pharmaceutical contract packaging market growth. Small molecule packaging leads at 58.6% share in 2025, while sterile packaging accounts for 62.7% of total revenue. The South region dominates with 38.2% of national demand in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 6.72 Billion |

|

Forecast Market Size (2034) |

USD 11.71 Billion |

|

CAGR (2026-2034) |

6.36% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

South (38.2% share, 2025) |

|

Leading Industry Segment |

Small Molecule (58.6%, 2025) |

|

Leading Type Segment |

Sterile Packaging (62.7%, 2025) |

The United States pharmaceutical contract packaging market growth trajectory from 2020 through 2034 contrasts a steady historical expansion against a sustained forecast curve, supported by the structural rise of biologics, the GLP-1 prefilled-syringe boom, and full DSCSA serialization enforcement that took effect in November 2024.

To get more information on this market, Request Sample

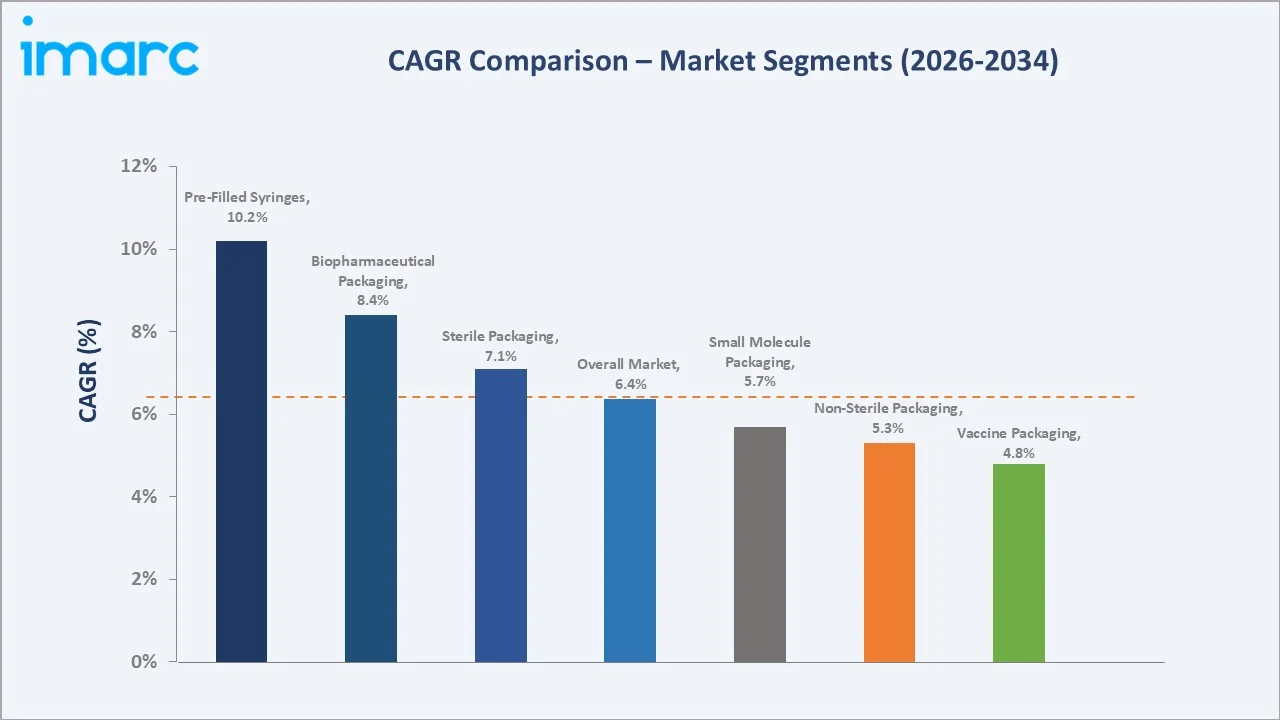

Segment-level CAGR comparisons highlight prefilled syringes and biopharmaceutical packaging as the fastest-growing sub-segments within the broader United States pharma contract packaging market forecast through 2034, while traditional non-sterile and vaccine packaging grow at a more measured pace.

Executive Summary

The United States pharmaceutical contract packaging market is undergoing a meaningful structural transformation. It is shaped by accelerating outsourcing, expanding biologics pipelines, and tightening serialization mandates under the Drug Supply Chain Security Act. Valued at USD 6.72 Billion in 2025, the market is projected to reach USD 11.71 Billion by 2034 at a CAGR of 6.36%, expanding from USD 4.94 Billion recorded in 2020.

Small molecule packaging commands 58.6% of market revenue in 2025, supported by a deep oral solid-dose pipeline, generics exclusivity expirations, and over-the-counter packaging volume. Biopharmaceutical packaging follows at 28.4%, propelled by the GLP-1 wave, monoclonal antibodies, and biosimilar approvals. Vaccine packaging contributes 13.0%, anchored by adult immunization programmes and influenza, RSV, and Covid booster cycles. Sterile packaging dominates by type at 62.7%, supported by the rise of injectable biologics and prefilled-syringe configurations.

The South leads with a 38.2% revenue share in 2025, anchored by North Carolina's Research Triangle, Florida's CDMO clusters, and Puerto Rico's pharmaceutical manufacturing footprint. The United States pharmaceutical contract packaging market outlook remains strongly positive as biologics expansion, GLP-1 demand, cell and gene therapy commercialization, and DSCSA-driven serialization upgrades converge across the country.

Key Market Insights

|

Insight |

Data |

|

Largest Industry Segment |

Small Molecule – 58.6% share (2025) |

|

Second Industry Segment |

Biopharmaceutical – 28.4% share (2025) |

|

Largest Type Segment |

Sterile Packaging – 62.7% share (2025) |

|

Fastest-Growing Sub-Segment |

Prefilled Syringes – ~10.2% CAGR (2026-2034) |

|

Leading Region |

South – 38.2% revenue share (2025) |

|

Top Companies |

PCI Pharma Services, Catalent Inc., Sharp Services LLC, Almac Group, Smurfit WestRock. |

|

Forecast Market Size (2034) |

USD 11.71 Billion |

Key Analytical Observations Supporting the Above Data:

- Small molecule's 58.6% dominance in 2025 reflects the depth of the United States generics pipeline, oral solid dose volumes, and OTC packaging demand. The FDA approved over 35,000 generic drugs in 2025, sustaining steady contract-packaging throughput across blister, bottle, and pouch formats.

- Biopharmaceutical's 28.4% share is propelled by GLP-1 medications, monoclonal antibodies, and biosimilar launches. United States prescription volumes for GLP-1 weight-management drugs surged through 2023-2024, lifting demand for prefilled syringes, auto-injectors, and cold-chain secondary packaging.

- Vaccine packaging's 13.0% position is supported by the adult-immunization programme, RSV vaccine launches across 2023-2024, expanded annual influenza coverage, and continued Covid-19 booster activity routed through United States pharmacy and clinic distribution channels.

- Sterile packaging's 62.7% lead reflects the structural shift toward injectable biologics, vials, prefilled syringes, and cartridges. Sterile fill-finish capacity in the United States remained tight through 2024, with several CDMOs announcing multi-billion-dollar capacity expansions for syringes and ready-to-use vials.

- Non-sterile packaging's 37.3% share captures bottles, blisters, sachets, and unit-dose formats for oral solid and liquid drugs. Volume remains underpinned by branded oral therapies, generics, and OTC products distributed through United States retail pharmacy chains.

- South's 38.2% regional dominance is underpinned by North Carolina's Research Triangle CDMO base, Florida's Tampa-Orlando life-sciences corridor, and Puerto Rico's deep pharmaceutical manufacturing legacy that hosts multiple top-20 pharma packaging operations.

United States Pharmaceutical Contract Packaging Market Overview

Pharmaceutical contract packaging refers to outsourced primary and secondary packaging services for finished drug products. Primary packaging includes vials, prefilled syringes, blisters, bottles, ampoules, and sachets that come into direct contact with the drug. Secondary packaging covers cartons, labelling, serialization printing, leaflet insertion, and case-pack formats that prepare the product for distribution to wholesalers, pharmacies, and hospitals.

The industry sits at the intersection of pharmaceutical manufacturing, regulated supply chains, and digital track-and-trace infrastructure. Macroeconomic and policy drivers include FDA cGMP enforcement, the Drug Supply Chain Security Act (DSCSA) which reached full enforcement in November 2024, and the Inflation Reduction Act provisions on Medicare drug pricing. The United States pharmaceutical contract packaging industry analysis must also factor in pharma sponsors' growing preference to outsource packaging in order to free internal capacity for high-value drug substance and drug product manufacturing.

Market Dynamics

To evaluate market opportunities, Request Sample

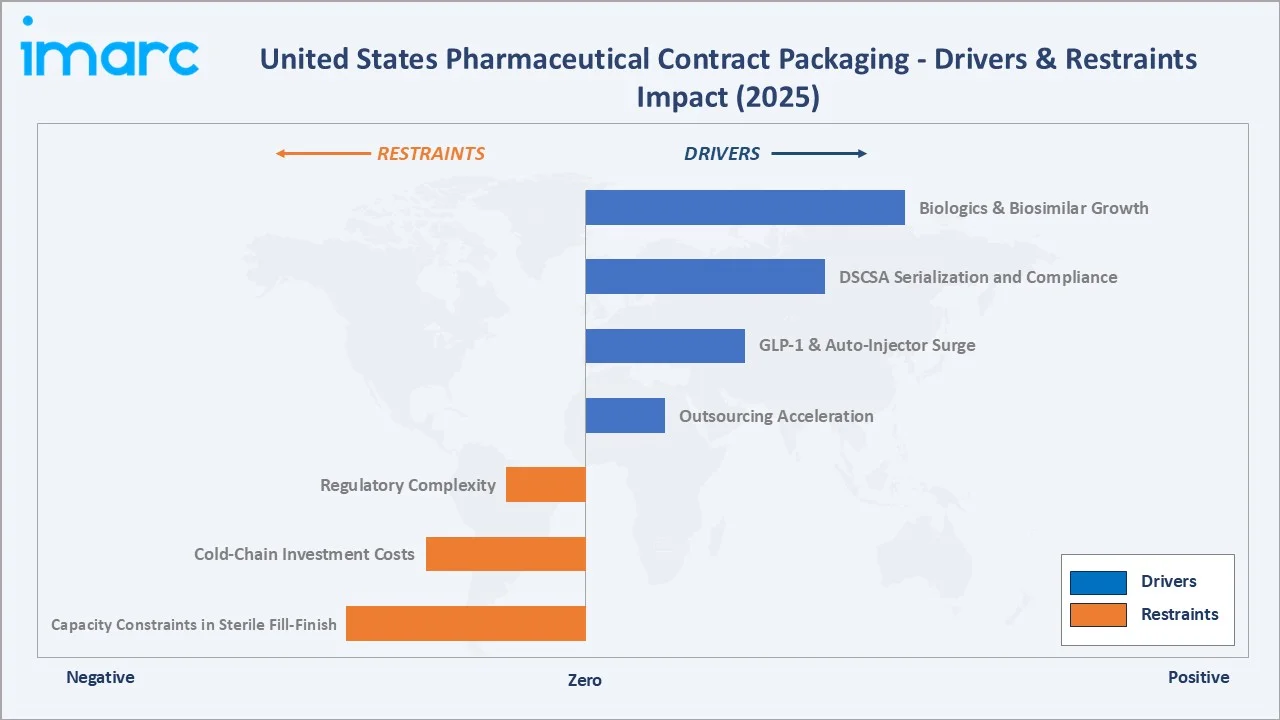

Market Drivers

- Biologics and Biosimilar Growth: Biologics now account for the majority of United States pharmaceutical revenue. The FDA approved a record number of biosimilars between 2022 and 2024, expanding the volume of injectable products that require sterile vial, syringe, and auto-injector packaging from contract partners.

- DSCSA Serialization and Compliance: The Drug Supply Chain Security Act reached full enforcement in November 2024, requiring interoperable electronic tracing of prescription drugs at the package level. Contract packagers continue to invest heavily in serialization printing, aggregation, and EPCIS-compliant data exchange systems through 2025-2026.

- GLP-1 and Auto-Injector Surge: United States prescription volumes for GLP-1 medications grew sharply through 2023-2024, driving exceptional demand for prefilled syringes, pen injectors, and high-precision secondary packaging. Several CDMOs announced multi-hundred-million-dollar capacity expansions for syringe filling and packaging in 2024.

- Outsourcing Acceleration: Top-20 pharma sponsors are outsourcing packaging at record rates to free internal capacity for higher-value drug substance manufacturing. Industry surveys conducted in 2024 indicated that more than 70% of United States pharma firms intended to maintain or increase their contract packaging spend through 2026.

Market Restraints

- Capacity Constraints in Sterile Fill-Finish: United States sterile fill-finish and syringe-packaging capacity has remained tight since 2022. Lead times for new injectable packaging slots stretched well into 2025-2026 at several major CDMOs, prompting urgent capacity-expansion announcements from PCI, Catalent, and others.

- Cold-Chain Investment Costs: Biologics, vaccines, and cell and gene therapies require validated cold-chain and ultra-cold-chain packaging infrastructure. Capital expenditure for qualified -20°C and -70°C storage and transit packaging remains a significant barrier for mid-size contract packagers.

- Regulatory Complexity: Concurrent compliance with FDA cGMP, DSCSA, USP <790> and <797> standards, and state-level pedigree requirements demands continuous investment in QA systems, technician training, and audit-ready documentation across multiple United States sites.

Market Opportunities

- Cell and Gene Therapy Packaging: The FDA approved several new cell and gene therapies between 2023 and 2024. Patient-specific packaging, ultra-cold-chain logistics, and chain-of-identity tracking represent a high-margin, fast-growing niche for specialized contract packagers across the United States.

- Sustainable and Recyclable Packaging: Top-20 pharma sponsors have set 2030 sustainability targets covering recyclable cartons, mono-material blisters, and reduced single-use plastics. Contract packagers that can offer validated sustainable formats are well-positioned to capture incremental wallet share through 2034.

Market Challenges

- Industry Consolidation: Catalent's planned acquisition by Novo Holdings, announced in February 2024 and closed in late 2024, illustrates ongoing consolidation. Mid-size United States packagers face heightened competitive pressure from scale players that bundle drug product manufacturing, packaging, and clinical-supply services.

- Skilled Labour and Validation Talent: Hiring qualified pharmaceutical packaging technicians, validation engineers, and DSCSA-trained QA staff remains a structural challenge across all four United States census regions, slowing the ramp-up of newly commissioned packaging lines through 2025-2026.

Emerging Market Trends

1. DSCSA Full Enforcement and Serialization Maturity

DSCSA reached full enforcement in November 2024, requiring electronic, interoperable, package-level traceability across the United States prescription drug supply chain. Contract packagers continue to invest in serialization printers, aggregation cameras, EPCIS data exchange, and exception-management workflows through 2025-2026.

2. Prefilled Syringe and Auto-Injector Boom

GLP-1 medications, biosimilars, and self-administered biologics are accelerating demand for prefilled syringes, dual-chamber syringes, and auto-injectors. The prefilled-syringe sub-segment is projected to grow at approximately 10.2% CAGR through 2034, faster than any other United States pharma packaging category.

3. Cold-Chain and Ultra-Cold-Chain Expansion

Validated cold-chain and ultra-cold-chain packaging infrastructure has scaled rapidly since 2021. PCM-based shippers, qualified VIP boxes, and -70°C dry-ice solutions are now standard for biologics, mRNA vaccines, and cell and gene therapy products distributed across the United States.

4. Sustainable Pharmaceutical Packaging

Mono-material blisters, paper-based cartons with reduced ink coverage, and recyclable PET vials are gaining traction as top-20 pharma sponsors progress toward 2030 sustainability targets. Several contract packagers introduced validated mono-material blister capabilities during 2024.

5. Automation, Robotics, and Digital Quality

Vision-based inspection systems, robotic case packing, and AI-led quality analytics are spreading across high-volume United States packaging lines. Investments in Industry 4.0 quality and serialization data platforms accelerated through 2024-2025, supported by capital-expansion programmes at PCI and Sharp.

Industry Value Chain Analysis

The United States pharmaceutical contract packaging value chain spans six integrated stages from active pharmaceutical ingredient supply through end-user delivery. Each stage has distinct margin, capital, and regulatory profiles that shape the broader United States pharma contract packaging market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

API & Drug Substance |

API CDMOs, fermentation, biomanufacturing for small molecules and biologics |

|

Drug Product Mfg |

Formulation, sterile fill-finish, oral solid dose manufacturing by integrated CDMOs |

|

Primary Packaging |

Vials, prefilled syringes, blisters, bottles, ampoules, cartridges, sachets |

|

Secondary Packaging |

Cartons, labels, serialization, aggregation, leaflet insertion, e-pedigree printing |

|

Distribution & Cold Chain |

Wholesalers, 3PLs, validated cold-chain logistics |

|

End Users |

Hospitals, retail pharmacies, specialty pharmacies, clinics, home-care patients |

Integrated CDMOs that bundle drug product manufacturing with primary and secondary packaging capture the highest strategic value, particularly for sterile injectables. Specialized contract packagers continue to differentiate on serialization expertise, cold-chain validation, and rapid changeover capability across small-batch and clinical-supply requirements.

Technology Landscape in the United States Pharma Contract Packaging Industry

Serialization, Aggregation, and EPCIS

Following DSCSA full enforcement in November 2024, serialization printing, machine-vision aggregation cameras, and EPCIS-compliant data exchange platforms became baseline capabilities. Leading United States packagers have integrated TraceLink, rfxcel, and Antares Vision platforms to support fully electronic interoperable traceability.

Sterile Packaging and Isolator Technology

Restricted Access Barrier Systems (RABS) and isolator-based aseptic packaging lines now dominate new sterile fill-finish investments across the United States. These technologies reduce contamination risk, improve operator safety, and support batch flexibility across vial, syringe, and cartridge formats for biologic and vaccine products.

Cold-Chain Packaging and Smart Sensors

Phase-change-material (PCM) shippers, vacuum-insulated panels (VIPs), and IoT-enabled temperature loggers have scaled rapidly since 2021. Real-time excursion alerts, NIST-traceable calibration, and integrated track-and-trace data flows are now standard for biologics, mRNA vaccines, and cell and gene therapy products.

Automation, Robotics, and AI Quality

Robotic case packing, computer-vision label inspection, and AI-led deviation analytics are spreading across high-volume United States packaging lines. Industry 4.0 investments improve right-first-time rates, reduce changeover times, and enhance audit-ready documentation - all critical levers for FDA cGMP compliance and sustained customer wins.

Market Segmentation Analysis

IMARC Group provides an analysis of the key trends in each segment of the United States pharmaceutical contract packaging market, along with forecasts at the national and regional level from 2026 to 2034. The market has been categorized based on industry and type.

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Industry | Small Molecule | 58.6% | 2025 |

| Type | Sterile | 62.7% | 2025 |

| Packaging | Plastic Bottles | 🔒 | 2025 |

| Region | South | 38.2% | 2025 |

By Industry

Small molecule packaging leads the United States market with a 58.6% share in 2025. This segment is anchored by oral solid dose tablets, capsules, and topical formulations packaged into bottles, blisters, sachets, and unit-dose formats. Demand is supported by a deep generics pipeline, OTC consumer health products, and Medicare Part D volume across major United States retail pharmacy chains. The FDA approved over 35,000 generic drugs in 2025, sustaining steady contract-packaging throughput.

To access detailed market analysis, Request Sample

Biopharmaceutical packaging holds 28.4% of market revenue and is the fastest-growing industry segment, projected to advance at roughly 8.4% CAGR through 2034. Demand is propelled by GLP-1 medications, monoclonal antibodies, biosimilar launches, and self-administered injectables that require prefilled syringes, auto-injectors, and validated cold-chain secondary packaging. Vaccine packaging contributes 13.0%, anchored by adult immunization programmes, RSV vaccines launched across 2023-2024, expanded annual influenza coverage, and continued Covid-19 booster activity routed through United States pharmacy and clinic distribution channels.

By Type

Sterile packaging is the dominant type at 62.7% of market revenue in 2025. This share reflects the structural shift toward injectable biologics, vials, prefilled syringes, cartridges, and ampoules that require aseptic fill-finish and validated sterile barriers. Sterile fill-finish capacity in the United States remained tight through 2024, with PCI Pharma Services, Catalent, and other CDMOs announcing multi-hundred-million-dollar capacity expansions for syringe filling and ready-to-use vial packaging.

Non-sterile packaging accounts for 37.3% of United States contract packaging revenue in 2025. The category covers bottles, blisters, sachets, pouches, sticks, and unit-dose formats for oral solid and oral liquid drugs, plus topicals such as creams, ointments, and gels. Volume remains underpinned by branded oral therapies, generics, and OTC consumer health products distributed through major United States retail pharmacy chains. While slower-growing than sterile, non-sterile packaging continues to deliver high-throughput, cost-efficient capacity that supports the country's deep oral solid dose pipeline.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

South |

38.2% |

NC Research Triangle CDMOs, FL life-sciences corridor, Puerto Rico pharma cluster, low-cost talent base |

|

Midwest |

22.6% |

Indianapolis biopharma hub (Lilly), generic and OTC capacity in IL, OH, MI |

|

West |

20.1% |

California biotech cluster, Bay Area cell & gene therapy, Pacific Northwest fill-finish |

|

Northeast |

19.1% |

NJ-PA pharma corridor, Boston-Cambridge biotech hub, top-20 pharma headquarters proximity |

The South leads with a 38.2% revenue share in 2025. North Carolina's Research Triangle hosts a deep concentration of CDMO and contract packaging operations spanning Catalent, Thermo Fisher, and Grand River. Florida's Tampa-Orlando corridor and Puerto Rico's pharmaceutical manufacturing legacy further reinforce regional scale. The South benefits from a favourable labour cost base, cGMP-trained talent pipelines, and proximity to major shipping ports that serve both domestic and Latin American distribution networks.

The Midwest holds 22.6% of national revenue, anchored by Indianapolis as a major biopharmaceutical hub headlined by Eli Lilly's manufacturing footprint and the GLP-1 production buildout. Illinois, Ohio, and Michigan host significant generic and OTC packaging capacity, while Wisconsin and Minnesota contribute specialty packaging operations. The region benefits from central United States logistics access and a deep base of skilled packaging technicians.

The West contributes 20.1%, led by California's biotech cluster spanning the Bay Area, San Diego, and Los Angeles. The region over-indexes on cell and gene therapy packaging, advanced biologics, and clinical-supply services for emerging biotech sponsors. Washington and Oregon add fill-finish and specialty packaging capacity. The Northeast accounts for 19.1%, driven by the New Jersey-Pennsylvania pharmaceutical corridor and the Boston-Cambridge biotech hub. The region houses headquarters for several top-20 pharma sponsors, supporting deep, long-term outsourcing relationships with regional contract packaging providers across small molecule, biologic, and clinical-trial supply formats.

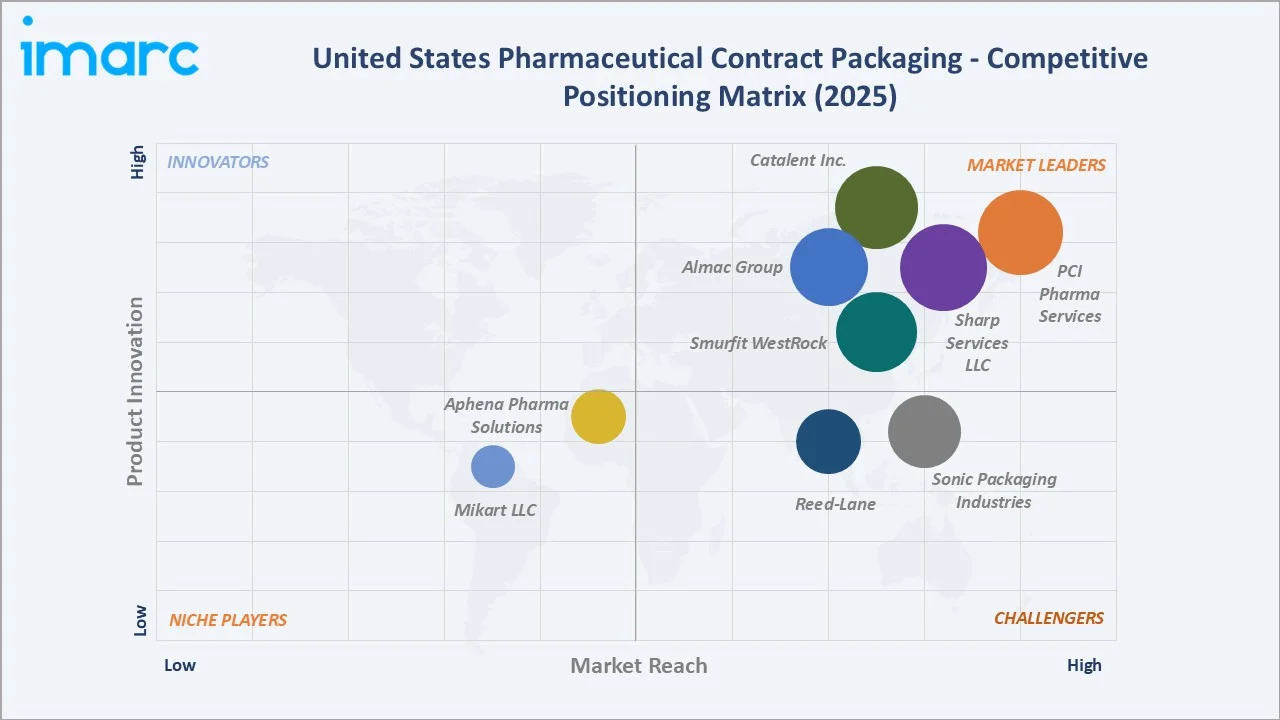

Competitive Landscape

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

|

PCI Pharma Services |

PCI Pharma Services |

Leader |

Largest United States clinical & commercial packager, sterile syringe expansion |

|

Catalent Inc. (a Novo Holdings company) |

Catalent Inc |

Leader |

Integrated CDMO, biologics fill-finish, cell & gene capabilities |

|

Sharp Services LLC |

Sharp Services |

Leader |

Clinical-supply leadership, serialization expertise, secondary packaging |

|

Almac Group |

Almac Pharma Services |

Leader |

Clinical-trial supply, cold-chain logistics, multi-region operations |

|

Smurfit WestRock |

Smurfit WestRock |

Leader |

Folding cartons, secondary packaging scale, sustainability focus |

|

Sonic Packaging Industries |

Sonic Packaging |

Challenger |

Mid-market CDMO, blister and bottle packaging, OTC and Rx coverage |

|

Reed-Lane |

Reed-Lane |

Challenger |

Bottling, blistering, and serialization services for branded Rx |

|

Aphena Pharma Solutions |

Aphena Pharma Solutions |

Emerging |

Contract manufacturing and packaging, OTC and Rx blister specialization |

|

Mikart LLC |

Mikart |

Emerging |

Atlanta-based CDMO, oral solid dose packaging, mid-market segment |

The competitive landscape in the United States pharmaceutical contract packaging market is moderately concentrated. Tier-1 integrated CDMOs such as PCI, Catalent, Sharp, and Almac compete on scale, sterile fill-finish capacity, serialization expertise, and biologics capabilities. Mid-market players differentiate through agility, clinical-supply specialization, and rapid changeover capabilities. Strategic M&A remains highly active - Novo Holdings completed its acquisition of Catalent in late 2024, while PCI continued multi-year capacity-expansion announcements for sterile syringe filling and ready-to-use vials.

Key Company Profiles

PCI Pharma Services

PCI Pharma Services is one of the largest pharmaceutical contract packaging and clinical-trial supply providers in the United States, headquartered in Philadelphia, Pennsylvania. The company operates more than 30 sites across the United States and internationally, serving both clinical and commercial-stage sponsors.

- Product & Platform Portfolio: PCI's portfolio spans clinical-trial packaging and labelling, commercial primary and secondary packaging, sterile fill-finish, lyophilization, prefilled-syringe assembly, serialization, and cold-chain logistics. Acquisitions of Bellwyck and Lyophilization Services have meaningfully extended PCI's biologic capabilities.

- Recent Developments: In 2024, PCI Pharma Services announced more than $365 million in investments across its U.S. and European facilities, expanding capacity for sterile fill-finish operations, including prefilled syringes and lyophilization, alongside high-potency and specialized packaging capabilities to meet rising demand for complex biologics.

- Strategic Focus: PCI's strategy centres on scaling sterile injectable packaging capacity, expanding lyophilization and high-potency capabilities, deepening clinical-supply leadership, and integrating digital serialization and quality systems across all United States sites through 2034.

Catalent Inc. (A Novo Holdings Company)

Catalent Inc. is a U.S.-based global contract development and manufacturing organization (CDMO), headquartered in Somerset, New Jersey. The company provides end-to-end development, manufacturing, and delivery solutions for pharmaceuticals, biologics, cell and gene therapies, and consumer health products. Catalent operates an extensive global network of facilities across North America, Europe, and Asia, supporting leading pharmaceutical companies as well as emerging biotech firms.

- Product & Platform Portfolio: Catalent’s portfolio spans drug substance and drug product development, with strong capabilities in biologics manufacturing, sterile fill-finish, oral solid dose technologies, and advanced delivery systems. The company is a key player in biologics and injectable manufacturing, with specialized expertise in high-demand areas such as cell and gene therapy, viral vector production, and mRNA-based platforms. Its proprietary technologies include softgel encapsulation, Zydis orally disintegrating tablets, and advanced formulation solutions aimed at improving bioavailability and patient compliance.

- Recent Developments: In December 2024, Catalent was acquired by Novo Holdings in a multi-billion-dollar transaction, taking the CDMO private and strengthening its exposure to biologics manufacturing and fill-finish capacity. The deal was closely aligned with supporting supply-chain needs for Novo Nordisk’s GLP-1 portfolio and broader industry demand for injectable therapies.

- Strategic Focus: Catalent focuses on expanding its leadership in biologics and advanced therapeutics manufacturing, particularly in high-growth segments such as GLP-1 therapies, cell and gene therapy, and sterile injectables. The company continues to invest in expanding fill-finish capacity, enhancing biologics production capabilities, and optimizing end-to-end CDMO services. Under Novo Holdings’ ownership, Catalent is expected to play a critical role in strengthening global biomanufacturing infrastructure and enabling scalable, high-quality production for next-generation therapies.

Sharp Services LLC

Sharp Services LLC is a leading United States pharmaceutical contract packaging provider, headquartered in Allentown, Pennsylvania. Sharp operates a multi-site footprint across the United States and Europe, serving both clinical and commercial sponsors with packaging, serialization, and clinical-supply solutions.

- Product & Platform Portfolio: Sharp's portfolio spans commercial blister and bottle packaging, serialization and aggregation, clinical-trial supply through Sharp Clinical, cold-chain handling, secondary packaging, leaflet insertion, and complex labelling for Rx, OTC, and biologic products.

- Recent Developments: In 2026, Sharp Services expanded its injectable packaging capabilities through a €20 million+ investment in its European facilities, adding assembly, labeling, and cold-chain storage capacity, alongside new syringe packaging lines and automation technologies to improve efficiency and support growing demand for injectable formats.

- Strategic Focus: Sharp's strategic focus centres on commercial and clinical-supply leadership, deepening serialization and aggregation expertise, expanding cold-chain and biologic capabilities, and supporting top-20 pharma sponsors with end-to-end DSCSA-ready packaging services through 2034.

Market Concentration Analysis

The United States pharmaceutical contract packaging market exhibits moderate concentration. The top five players - PCI Pharma Services, Catalent Inc., Sharp Services LLC, Almac Group, Smurfit WestRock - collectively account for an estimated 35-42% of United States contract packaging revenue in 2025. The remaining share is distributed across mid-market specialists such as Sonic Pharma, Reed-Lane, Aphena, and Mikart, alongside a long tail of regional packagers and in-house pharma operations across the country.

The market is undergoing steady consolidation. Tier-1 integrated CDMOs continue to gain share through capacity expansion, M&A, and bundled drug-product-plus-packaging service offerings. Novo Holdings' acquisition of Catalent in late 2024, alongside PCI's ongoing capacity-build programme, illustrates how capital is concentrating in scale players able to serve sterile-injectable and biologic demand. Mid-market specialists continue to compete by serving niche, agile, and clinical-supply use cases through 2034.

Investment & Growth Opportunities

Fastest-Growing Sub-Segments

Prefilled syringes and auto-injectors represent the highest-growth sub-segment at approximately 10.2% CAGR through 2034. Biopharmaceutical packaging follows at roughly 8.4% CAGR, supported by GLP-1 medications, biosimilars, and self-administered biologics. Sterile vial packaging and ultra-cold-chain solutions for cell and gene therapies round out the highest-margin growth opportunities.

Emerging Sub-Markets

Cell and gene therapy packaging, patient-specific clinical-supply kits, sustainable mono-material blisters, and digital serialization-as-a-service represent above-trend growth pockets through 2034. The FDA's continued approval cadence for cell and gene therapies during 2024-2025 supports expansion of specialized ultra-cold-chain and chain-of-identity packaging capabilities.

Strategic Investment Trends

Strategic M&A continues to reshape the competitive landscape. Novo Holdings completed the acquisition of Catalent in December 2024, while PCI continued multi-year capacity-expansion announcements through 2024-2025. Private equity, sovereign wealth funds, and pharma corporate venture arms are actively financing United States sterile fill-finish, syringe-filling, and cold-chain packaging buildouts through 2034.

Future Market Outlook (2026-2034)

The United States pharmaceutical contract packaging market forecast projects steady value expansion from USD 6.72 Billion in 2025 to USD 11.71 Billion by 2034 at a CAGR of 6.36%. The South is expected to retain regional leadership, while the West gains share on the back of cell and gene therapy packaging. Sterile, biopharmaceutical, and prefilled-syringe sub-segments are forecast to outpace overall market growth through 2034.

Three structural shifts will shape the United States pharmaceutical contract packaging market through 2034. First, biologics, GLP-1 medications, and self-administered injectables will sustain elevated demand for prefilled syringes and auto-injectors. Second, DSCSA-compliant serialization and electronic interoperability will become baseline expectations, raising the bar for mid-market packagers. Third, cell and gene therapies, sustainable packaging mandates, and Industry 4.0 quality systems will continue redefining the competitive set across all four United States census regions.

Research Methodology

Primary Research

Primary research included structured interviews conducted in 2024-2025 with United States pharmaceutical contract packaging stakeholders, including CDMO commercial leaders, packaging operations directors at top-20 pharma sponsors, serialization solution providers, sterile fill-finish managers, and clinical-supply procurement professionals. These interviews validated revenue sizing, segmentation estimates, and capacity-utilization benchmarks.

Secondary Research

Secondary sources included FDA approvals data, DSCSA compliance publications, USP <790> and <797> standards documentation, IQVIA prescription audit data, the Pharmaceutical Research and Manufacturers of America (PhRMA) industry reports, company annual reports and investor presentations, and trade publications such as Pharmaceutical Technology, Contract Pharma, and Pharmaceutical Engineering.

Forecasting Models

Market size estimates and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating pharmaceutical R&D spend, FDA approvals trajectories, biologics pipeline depth, outsourcing-rate trends, and historical category-evolution patterns. Scenario analysis was performed across base, optimistic, and conservative cases.

United States Pharmaceutical Contract Packaging Market Report Coverage

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Industries Covered | Small Molecule, Biopharmaceutical, Vaccine |

| Types Covered | Sterile, Non-Sterile |

| Packagings Covered | Plastic Bottles, Caps and Closures, Blister Packs, Prefilled Syringes, Parenteral Vials and Ampoules, Others |

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered | PCI Pharma Services, Catalent Inc. (a Novo Holdings company), Sharp Services LLC, Almac Group, Smurfit WestRock, Sonic Packaging Industries, Reed-Lane, Aphena Pharma Solutions, Mikart LLC, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the United States Pharmaceutical Contract Packaging Market Report

The United States pharmaceutical contract packaging market was valued at USD 6.72 Billion in 2025, supported by biologics expansion, the GLP-1 surge, DSCSA serialization investment, and sustained outsourcing by top-20 pharmaceutical sponsors across the country.

The market is projected to reach USD 11.71 Billion by 2034, growing at a CAGR of 6.36% during 2026-2034, supported by sterile injectable demand, prefilled-syringe expansion, cell and gene therapy commercialization, and sustained outsourcing trends nationwide.

Small molecule packaging leads with a 58.6% share in 2025, anchored by oral solid dose tablets, capsules, and OTC products. The FDA approved over 800 generic drug applications in 2024, sustaining steady contract packaging throughput across blister and bottle formats.

Sterile packaging dominates at 62.7% in 2025, reflecting the structural shift to injectable biologics, prefilled syringes, vials, and cartridges. Sterile fill-finish capacity remained tight through 2024, with major CDMOs announcing significant United States capacity expansions.

Prefilled syringes are the fastest-growing sub-segment, advancing at an estimated 10.2% CAGR through 2034. Demand is driven by GLP-1 medications, biosimilars, and self-administered biologics that require precision injectable packaging across the United States.

The South leads with a 38.2% share in 2025. North Carolina's Research Triangle, Florida's life-sciences corridor, and Puerto Rico's pharmaceutical manufacturing legacy anchor the region's CDMO base, supported by a low-cost talent pool and strong logistics access.

Key drivers include biologics and biosimilar growth, the GLP-1 medication surge, DSCSA serialization compliance, accelerating outsourcing by top-20 pharma sponsors, expanded vaccine programmes, and rising demand for sterile injectable packaging across the United States.

Major players include PCI Pharma Services, Catalent Inc., Sharp Services LLC, Almac Group, Smurfit WestRock, Sonic Packaging Industries, Reed-Lane, Aphena Pharma Solutions, Mikart LLC.

Key restraints include sterile fill-finish capacity constraints, cold-chain investment costs, regulatory complexity across FDA, DSCSA, and USP standards, ongoing industry consolidation, and skilled-labour shortages affecting newly commissioned packaging lines.

DSCSA reached full enforcement in November 2024, requiring electronic, interoperable, package-level traceability. Contract packagers continue investing in serialization printing, aggregation cameras, and EPCIS data exchange platforms to support compliant United States drug distribution.

The GLP-1 wave is driving exceptional demand for prefilled syringes, pen injectors, and high-precision secondary packaging. Several CDMOs announced multi-hundred-million-dollar capacity expansions for syringe filling and packaging in 2024 to address the volume surge.

Investment opportunities include sterile syringe-filling capacity, cell and gene therapy packaging, ultra-cold-chain logistics, DSCSA serialization platforms, sustainable mono-material blisters, and AI-led quality and automation systems across the United States contract packaging market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)