United States Power Tool Market Size, Share, Trends and Forecast by Mode of Operation, Tool Type, Application, and Region, 2026-2034

United States Power Tool Market Summary:

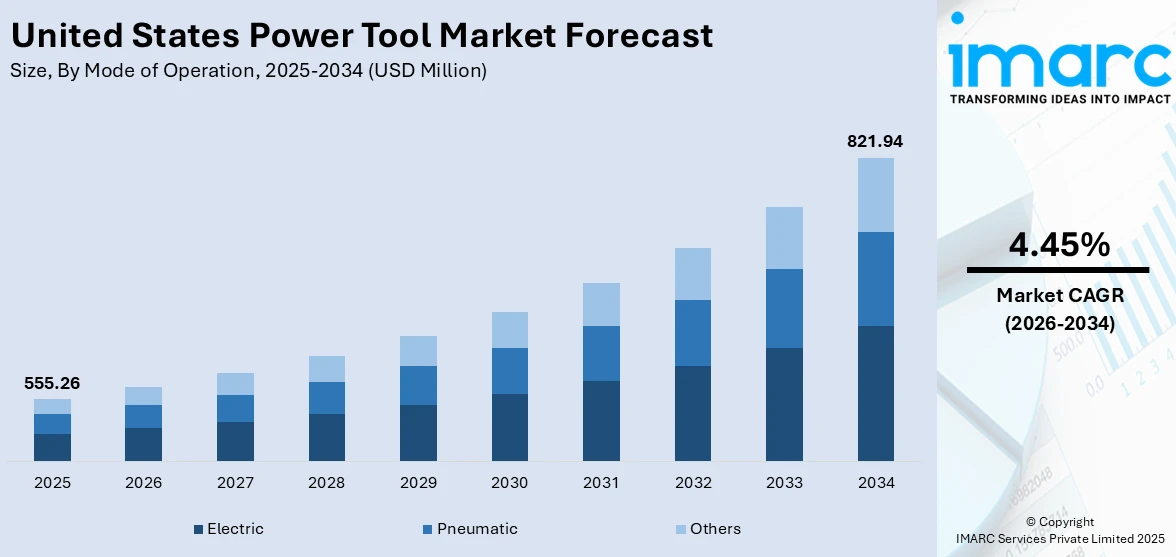

The United States power tool market size was valued at USD 555.26 Million in 2025 and is projected to reach USD 821.94 Million by 2034, growing at a compound annual growth rate of 4.45% from 2026-2034.

The United States power tool market is expanding as industrial modernization, infrastructure development, and evolving consumer preferences create sustained demand for advanced tooling solutions. Rising construction activity, growing interest in do-it-yourself home improvement projects, and rapid advancements in cordless battery technologies are reinforcing adoption across professional and residential segments. Expanding manufacturing operations, increased investments in energy and automotive sectors, and an emphasis on ergonomic and safety-enhanced tool designs are further supporting United States power tool market share.

Key Takeaways and Insights:

- By Mode of Operation: Electric dominates the market with a share of 71.9% in 2025, owing to widespread adoption of cordless lithium-ion battery-powered tools that deliver superior portability, consistent performance, and enhanced energy efficiency across professional and consumer applications.

- By Tool Type: Drilling and fastening tools lead the market with a share of 38.5% in 2025, driven by their indispensable role in construction, manufacturing, automotive assembly, and residential maintenance activities requiring precision fastening and hole-making capabilities.

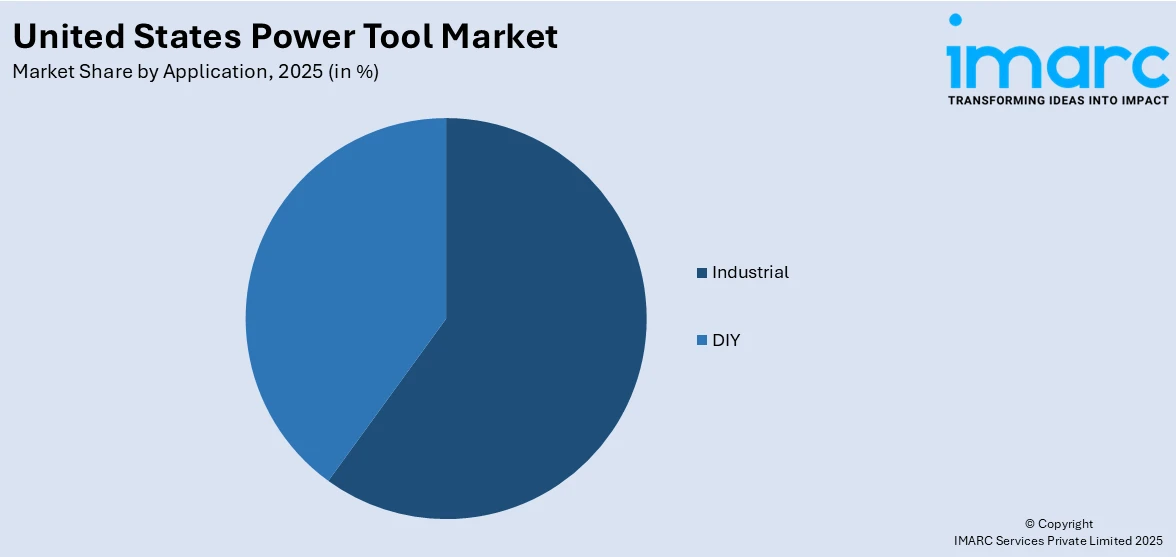

- By Application: Industrial leads the market with a share of 44.7% in 2025, reflecting strong demand from construction, automotive, energy, and manufacturing sectors that require high-performance, durable power tools for heavy-duty operational tasks.

- By Region: South represents the leading region with 35.8% share in 2025, driven by robust construction activity, large-scale infrastructure projects, expanding manufacturing operations, and a growing population base fueling residential and commercial development.

- Key Players: Key players drive the United States power tool market by investing heavily in research and development, expanding cordless tool platforms, introducing safety-enhanced designs, and strengthening distribution networks to capture professional and consumer segments.

To get more information on this market Request Sample

The United States power tool market is gaining momentum as technological innovation, infrastructure investment, and evolving end-user requirements converge to create a favorable growth environment. The transition from corded to cordless electric tools, powered by advanced lithium-ion and table battery cell technologies, is reshaping how professionals and homeowners approach construction, maintenance, and fabrication tasks. Federal investment programs, expanding residential renovation activity, and an increasingly technology-savvy consumer base are contributing to a more dynamic and competitive market landscape that supports sustained tool adoption. Growing emphasis on workplace safety, ergonomic design, and smart connectivity features is further accelerating product development cycles across the industry. Manufacturers are expanding multi-voltage battery platforms and broadening product portfolios to address diverse professional and consumer needs, reinforcing long-term demand across drilling, cutting, fastening, and demolition tool categories throughout the country.

United States Power Tool Market Trends:

Accelerating shift toward cordless tool platforms

The United States power tool market is experiencing a pronounced transition toward cordless platforms as battery innovations deliver performance that rivals or exceeds traditional corded models. Advanced brushless motors, high-capacity lithium-ion cells, and intelligent power management systems are enabling cordless tools to handle increasingly demanding heavy-duty applications, including demolition and concrete work. Manufacturers are expanding cordless lineups across drilling, cutting, grinding, and demolition categories, enabling greater jobsite mobility and supporting United States power tool market growth.

Integration of smart and connected tool technologies

Power tool manufacturers are embedding digital capabilities into their products, including Bluetooth connectivity, smartphone-based tracking, and diagnostic applications that enable real-time tool management. For instance, in 2025, Milwaukee Tool expanded its One-Key compatible cordless lineup, allowing professionals to wirelessly track, manage, and secure their tools across multiple jobsites. These smart features are improving inventory control, reducing tool loss, and enhancing operational efficiency for contractors and fleet managers.

Growing emphasis on safety and ergonomic design

Safety-focused innovations are becoming a defining trend as manufacturers integrate advanced injury-prevention features and ergonomic enhancements into power tool designs. For instance, in September 2025, the PERFORM AND PROTECT anti-rotation mechanism, which DEWALT launched with its ATOMIC 20V MAX 4-inch angle grinder series, reduces reactive torque by detecting pinch and bind-up situations. Enhanced vibration dampening, compact form factors, and improved grip designs are encouraging wider adoption among both professional tradespeople and occasional users.

Market Outlook 2026-2034:

The United States power tool market is positioned for sustained expansion, supported by continued infrastructure development, rising construction activity, and advancing tool technologies. Federal investments through the Infrastructure Investment and Jobs Act are channeling billions into highway, bridge, and transit projects, directly increasing demand for drilling, cutting, and demolition tools. The ongoing expansion of cordless battery platforms, featuring next-generation tabless lithium-ion cell technologies, is enabling manufacturers to deliver tools with longer runtimes and higher power output. Growing residential renovation spending, combined with professional market modernization, is expected to maintain positive demand trajectories across both consumer and industrial power tool categories throughout the forecast period. The market generated a revenue of USD 555.26 Million in 2025 and is projected to reach a revenue of USD 821.94 Million by 2034, growing at a compound annual growth rate of 4.45% from 2026-2034.

United States Power Tool Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Mode of Operation |

Electric |

71.9% |

|

Tool Type |

Drilling and Fastening Tools |

38.5% |

|

Application |

Industrial |

44.7% |

|

Region |

South |

35.8% |

Mode of Operation Insights:

- Electric

- Pneumatic

- Others

Electric dominates with a 71.9% share of the total United States power tool market in 2025.

The industry-wide shift from pneumatic and fuel-powered tools to battery-operated and corded electric alternatives, which provide greater convenience, lower maintenance costs, and reliable performance across a range of applications, is reflected in the electric segment's dominant position. Professional contractors and industrial users increasingly prefer electric power tools for their lower operating costs, elimination of compressor dependencies, and compatibility with expanding cordless ecosystems. The shift is further supported by enhanced brushless motor technologies that deliver higher efficiency and extended tool lifespan.

Electric power tools are gaining additional traction as manufacturers develop multi-voltage battery platforms that allow users to power an extensive range of tools from a single battery system, simplifying equipment management and reducing total ownership costs. The availability of high-capacity lithium-ion batteries with rapid charging capabilities is eliminating traditional performance gaps between corded and cordless models. Enhanced brushless motor technologies are further improving energy efficiency and extending tool lifespan, making electric platforms increasingly attractive for professionals seeking reliable, low-maintenance solutions across demanding jobsite applications.

Tool Type Insights:

- Drilling and Fastening Tools

- Material Removal Tools

- Sawing and Cutting Tools

- Demolition Tools

- Others

Drilling and fastening tools lead with a share of 38.5% of the total United States power tool market in 2025.

Drilling and fastening tools maintain their market leadership owing to their fundamental role across virtually every end-use sector, from residential construction and furniture assembly to automotive manufacturing and aerospace engineering. These tools encompass drills, impact drivers, impact wrenches, and screwdrivers that are essential for creating holes, driving fasteners, and assembling components with precision. The versatility of drilling and fastening tools across wood, metal, masonry, and composite materials ensures consistent demand from both professional tradespeople and do-it-yourself consumers.

Technological advancements in brushless motors, electronic torque control, and compact ergonomic designs are driving continuous innovation within the drilling and fastening tools category. Manufacturers are developing impact drivers with hydraulic drive systems that deliver reduced noise levels alongside increased driving power, addressing growing workplace noise regulations and user comfort demands. The expansion of cordless battery platforms has made high-performance drilling and fastening tools more accessible for field applications where mobility is critical.

Application Insights:

Access the comprehensive market breakdown Request Sample

- DIY

- Industrial

- Automotive

- Construction

- Energy

- Manufacturing

- Others

Industrial represents the largest segment with a 44.7% share of the total United States power tool market in 2025.

The industrial application segment leads the market driven by the extensive use of power tools across construction, automotive manufacturing, energy infrastructure, and general industrial production activities. Professional contractors, fabricators, and assembly line operators rely on heavy-duty drilling, cutting, grinding, and demolition tools to maintain operational efficiency and meet project timelines. The robust construction pipeline in the United States, supported by federal infrastructure investment and private sector development, sustains strong demand for industrial-grade power tools.

The automotive and manufacturing sub-segments within industrial applications are contributing significantly to power tool demand as facilities expand production capacities and adopt modern assembly technologies. Electric vehicle manufacturing, in particular, is creating new requirements for specialized cordless power tools designed for precision assembly and maintenance operations. The energy sector also drives tool consumption through ongoing pipeline construction, solar farm installation, and wind turbine maintenance activities.

Regional Insights:

- Northeast

- Midwest

- South

- West

The South exhibits a clear dominance in the market with a 35.8% share of the total United States power tool market in 2025.

The market leadership position enjoyed by the Southern region is strengthened by the rapid population growth rate, construction activities, and the large number of manufacturing and industrial operations present in Texas, Florida, Georgia, and the Carolinas. Many construction projects undertaken in the region’s residential sectors, coupled with the modernization of the infrastructure sector, guarantee constant demand for various range of power tools. The region is also served well by the dealer networks and financial programs of various manufacturers, allowing ease of access to tools for consumers.

Additional important industrial undertakings in the South include development in advanced manufacturing facilities, energy infrastructure, and automotive production plant operations. These developments continue to validate the South’s position as the leading market force. States such as Texas, Florida, and Georgia continue to be at the top in massive commercial and residential project investment undertakings, backed by public infrastructure investment dollars. The business environment, as well as an improving market for labor, is likely to sustain the South as the principal market demand driver for power tools.

Market Dynamics:

Growth Drivers:

Why is the United States Power Tool Market Growing?

Expanding construction and infrastructure investment

The United States power tool market is benefiting from a sustained wave of construction and infrastructure spending that generates consistent demand for industrial-grade tooling. Federal programs, particularly the Infrastructure Investment and Jobs Act, are directing substantial funding toward highway rehabilitation, bridge replacement, and transit modernization projects nationwide. State and local governments are complementing these federal investments with their own capital improvement programs, further expanding the pipeline of construction projects that require power tools. As aging infrastructure systems require modernization and replacement, the demand for reliable, high-performance power tools continues to intensify across both public and private construction sectors. The convergence of residential development, commercial real estate expansion, and public works investment ensures a diversified demand base that insulates the market from volatility in any single construction segment.

Rising do-it-yourself home improvement activity

The growing culture of do-it-yourself home improvement across the United States is creating robust consumer demand for power tools, particularly in the drilling, cutting, and material removal categories. Homeowners are increasingly undertaking renovation, maintenance, and personalization projects driven by high housing costs that encourage stay-and-improve decisions, expanded access to online tutorials, and the availability of user-friendly cordless tools. The aging housing stock, with more than 80 percent of homes in the United States exceeding 20 years in age, necessitates regular maintenance and upgrade work that drives tool purchases. Retailers and manufacturers are responding to this trend by expanding entry-level and mid-range cordless tool offerings, providing bundled kits, and developing compact, lightweight models specifically designed for residential users, further broadening the consumer base for power tools.

Advancements in battery and cordless tool technologies

Rapid improvements in lithium-ion battery technology are transforming the power tool landscape by enabling cordless models to deliver performance equivalent to or exceeding traditional corded and pneumatic alternatives. Innovations such as electrode designs, high-capacity battery cells, and fast-charging systems are extending runtimes, increasing power output, and reducing tool weight simultaneously. These technological advancements are accelerating the industry-wide transition toward cordless platforms that offer superior mobility and convenience without compromising professional-grade performance. For instance, in 2024, Milwaukee Tool introduced its FORGE battery technology featuring lithium-ion cells that deliver significantly improved power-to-weight ratios and thermal management for demanding jobsite applications. Major manufacturers are investing heavily in research and development to bring next-generation battery systems to market, creating a competitive innovation environment that benefits end users with continuously improving tool performance and value across both professional and consumer segments.

Market Restraints:

What Challenges the United States Power Tool Market is Facing?

Elevated raw material and manufacturing costs

Rising costs of key raw materials, including lithium, cobalt, copper, and rare earth elements essential for battery and motor production, are placing upward pressure on power tool prices. Supply chain disruptions and geopolitical tensions continue to introduce volatility into material procurement processes, making it challenging for manufacturers to maintain stable pricing structures. Trade tariffs on imported components and finished goods from key manufacturing hubs further compound these cost pressures, potentially reducing affordability for price-sensitive consumer and professional segments.

Skilled labor shortages in end-use industries

The construction and manufacturing sectors across the United States are experiencing persistent skilled labor shortages that constrain project execution and, by extension, limit potential power tool demand growth. Workforce challenges are particularly acute in specialized trades such as electrical work, plumbing, and heavy equipment operation, where experienced professionals are retiring faster than new workers are entering the field. These shortages can delay project timelines and reduce overall tool utilization rates.

Intensifying competitive pressure from low-cost imports

The United States power tool market faces growing competitive pressure from low-cost imported tools, primarily from Asian manufacturing hubs that offer comparable basic functionality at significantly lower price points. This competition can erode market share for domestic and premium brands, particularly in the consumer and entry-level professional segments where price sensitivity is highest. Manufacturers must continuously invest in product differentiation through innovation, quality assurance, and brand development to maintain competitive positioning.

Competitive Landscape:

The United States power tool market is highly competitive, with both established global manufacturers and new entrants constantly looking to innovate and grab more market share. Established industry leaders are resorting to various strategies to maintain their competitive advantage by investing heavily in research and development activities. Strategic acquisitions and agreements with retail stores and expanding product offerings to various tool segments are some of the key competitive strategies adopted by different power tool manufacturers. Manufacturers are trying to differentiate their products by focusing on safety features, smart tool technology, ergonomically designed products, and green product initiatives like recycled materials. The level of competitiveness increases among power tool manufacturers due to the shift from corded to cordless power tools, which allows manufacturers to provide better battery life to tool users.

Recent Developments:

- In September 2025, DEWALT, a Stanley Black & Decker brand, introduced its first-ever cordless 4-inch angle grinder series under the ATOMIC 20V MAX lineup, including angle grinders, die grinders, and right angle die grinders designed for confined workspace applications. The tools deliver more power than select HP-rated pneumatic grinders without requiring hoses or complex pneumatic setups.

United States Power Tool Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Modes of Operation Covered |

Electric, Pneumatic, Others |

|

Tool Types Covered |

Drilling and Fastening Tools, Material Removal Tools, Sawing and Cutting Tools, Demolition Tools, Others |

|

Applications Covered |

|

|

Regions Covered |

Northeast, Midwest, South, West |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the United States Power Tool Market Report

The United States power tool market size was valued at USD 555.26 Million in 2025.

The United States power tool market is expected to grow at a compound annual growth rate of 4.45% from 2026-2034 to reach USD 821.94 Million by 2034.

Electric dominated the market with a share of 71.9%, driven by the widespread adoption of cordless lithium-ion battery platforms offering superior portability, lower maintenance costs, and consistent performance across professional and consumer applications.

Key factors driving the United States power tool market include expanding construction and infrastructure investment, rising do-it-yourself home improvement activity, rapid advancements in cordless battery technologies, and growing industrial demand from automotive and energy sectors.

Major challenges include elevated raw material and manufacturing costs, skilled labor shortages in construction and manufacturing sectors, intensifying competition from low-cost imports, supply chain disruptions, and trade tariff uncertainties affecting component pricing and availability.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)