United States Robotic Process Automation Market Size, Share, Trends and Forecast by Component, Operation, Deployment Model, Organization Size, End User, and Region, 2026-2034

United States Robotic Process Automation Market Size, Share, Trends & Forecast (2026-2034)

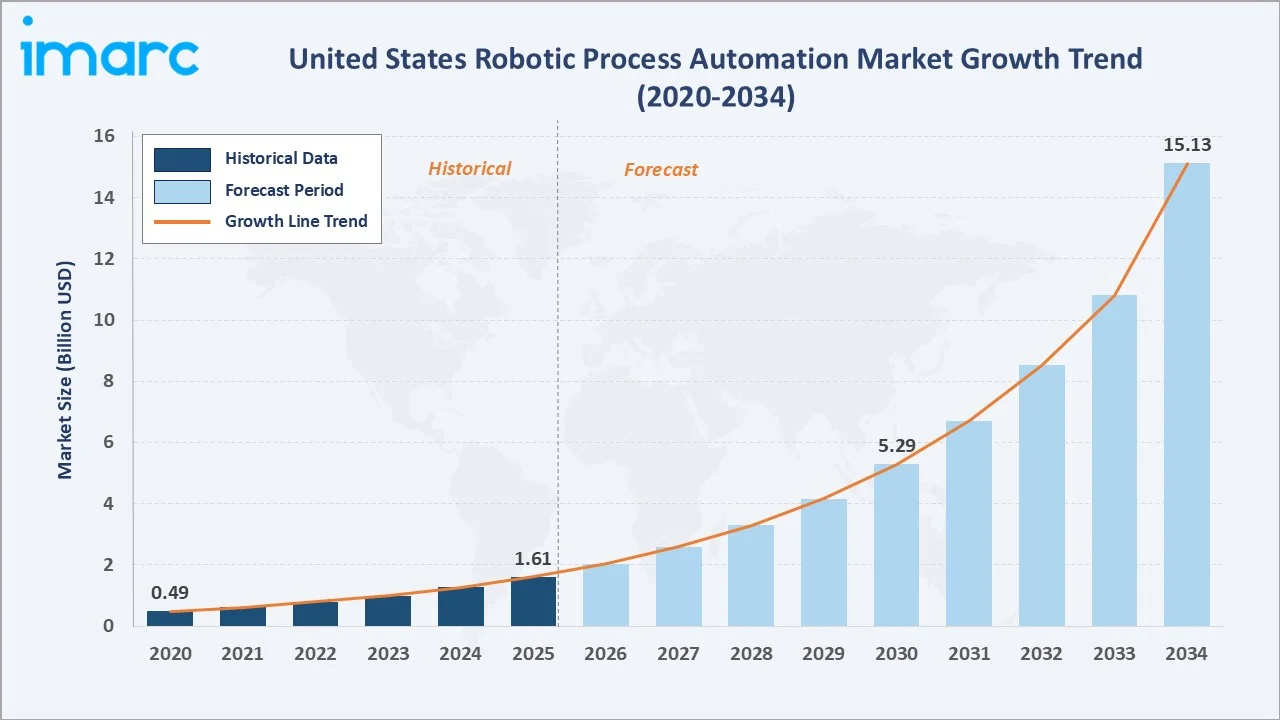

The United States robotic process automation market reached USD 1.61 Billion in 2025 and is projected to reach USD 15.13 Billion by 2034, growing at a CAGR of 26.88% during 2026-2034. The market is driven by the imperative to reduce operational costs, the integration of artificial intelligence with automation platforms, and accelerating digital transformation across industries.

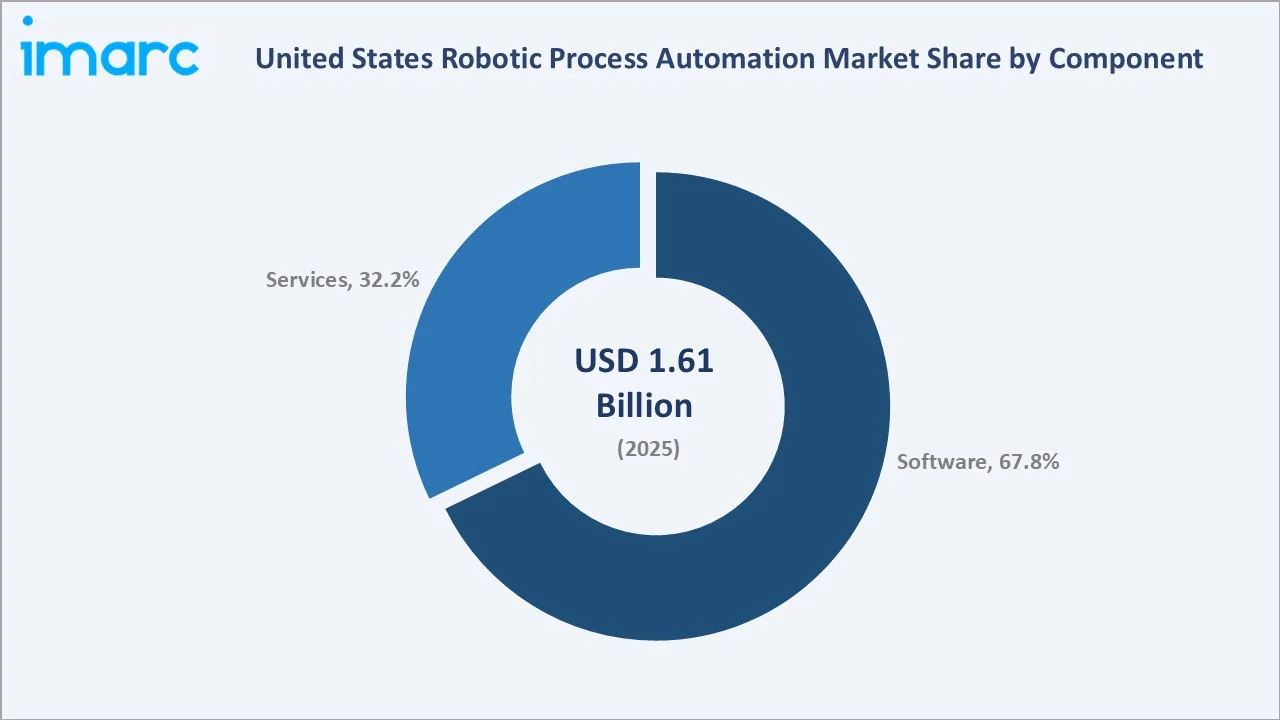

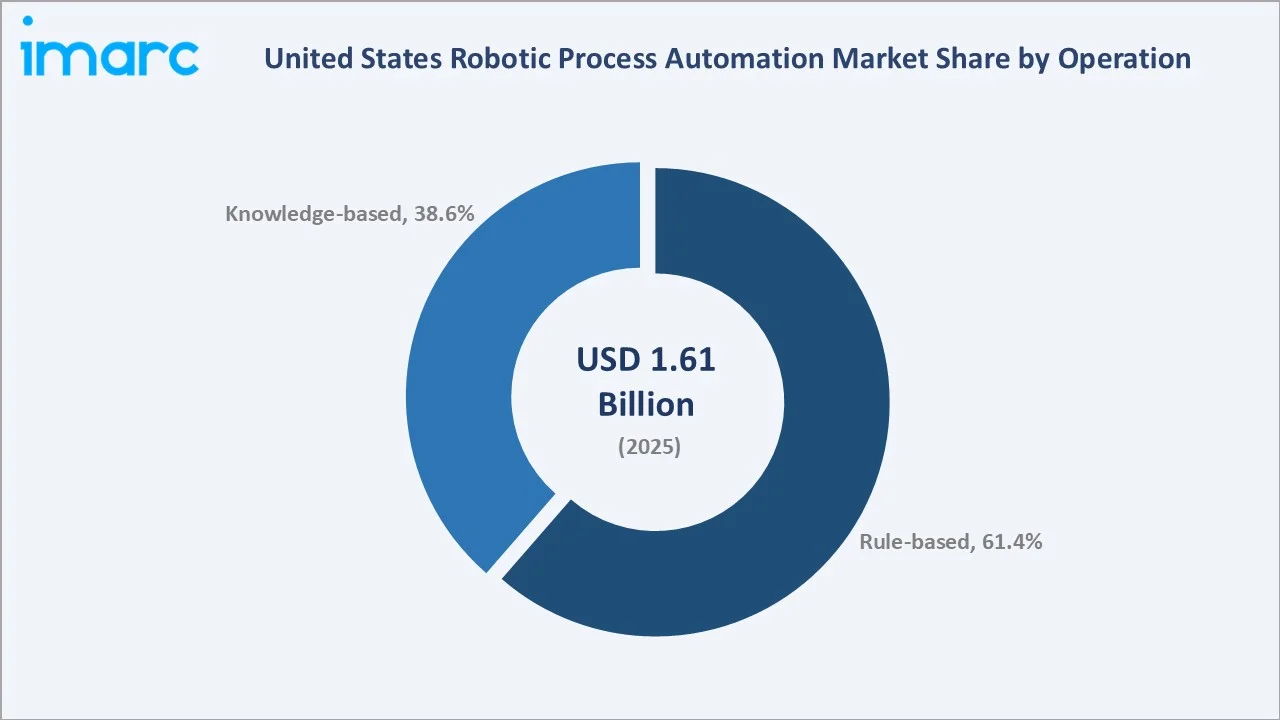

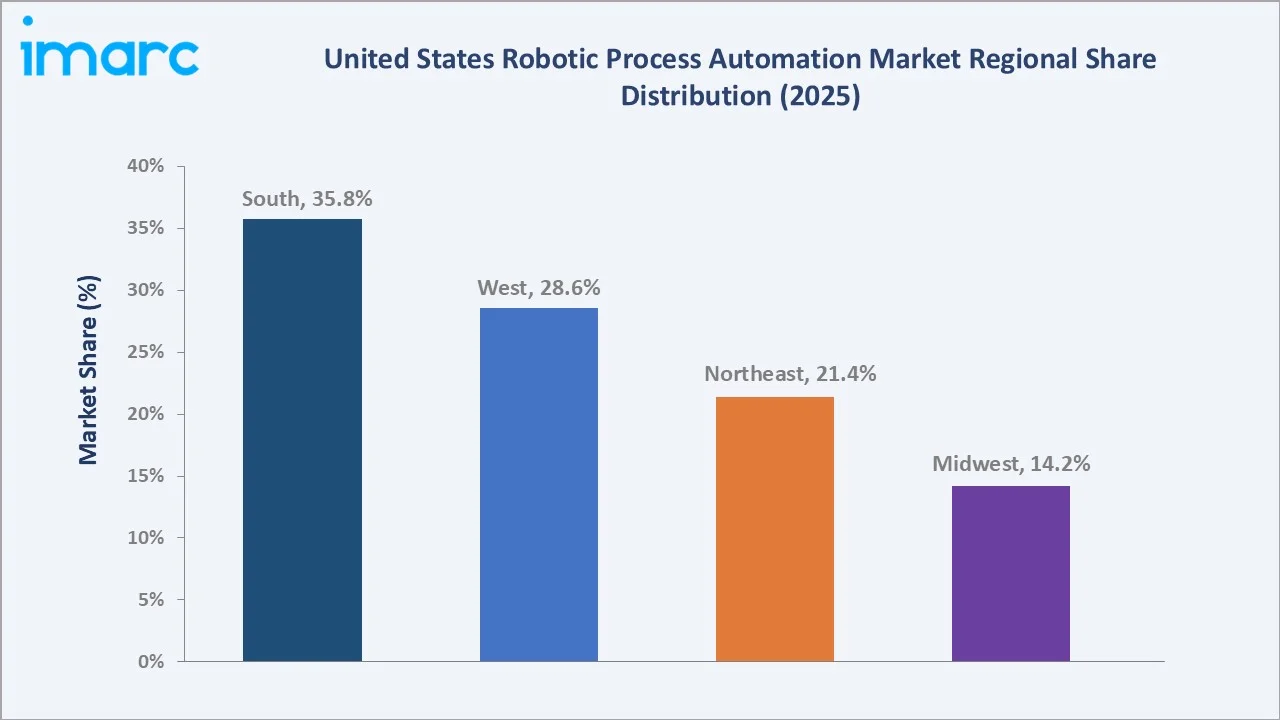

Software dominates the component segment at 67.8%, rule-based operations lead at 61.4%, and the South region commands the largest share at 35.8% of the total US RPA market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.61 Billion |

|

Forecast Market Size (2034) |

USD 15.13 Billion |

|

CAGR (2026-2034) |

26.88% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Component |

Software (67.8%, 2025) |

|

Dominant Operation |

Rule-based (61.4%, 2025) |

|

Leading Region |

South (35.8%, 2025) |

The market expanded from USD 0.49 Billion in 2020 to USD 1.61 Billion in 2025, anchored at USD 5.29 Billion in 2030 and forecast to reach USD 15.13 Billion by 2034. The rapid deployment of AI-integrated RPA across financial services, healthcare, and government sectors is the primary structural driver sustaining this compound growth trajectory through the forecast period.

To get more information on this market, Request Sample

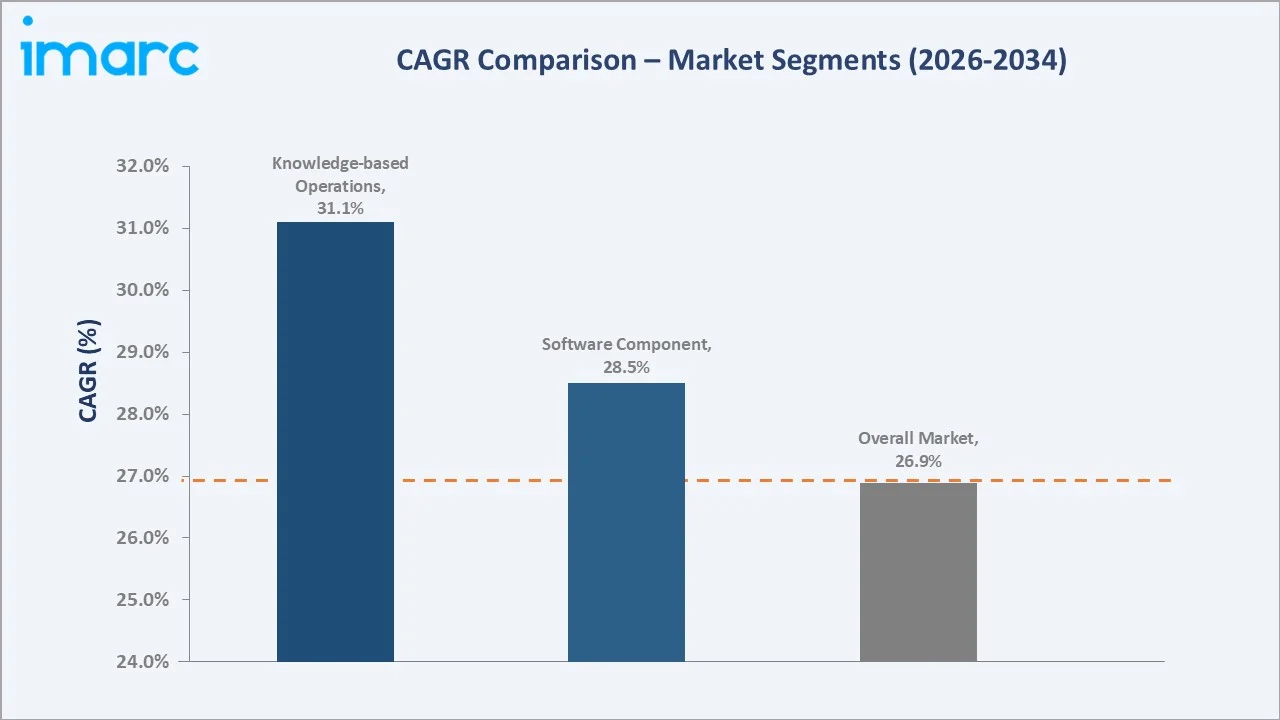

Software grows fastest at ~28.5% CAGR as enterprises invest in platform licenses and AI-augmented automation suites. Knowledge-based RPA grows at ~31.1% CAGR as AI-enabled bots handle unstructured data and complex decision-making workflows that extend well beyond traditional rule-based automation scope.

Executive Summary

The United States robotic process automation market reached USD 1.61 Billion in 2025, positioning the US as the single largest country-level RPA market globally. RPA enables software robots to mimic human interactions with digital systems, automating data entry, document processing, and transaction handling without requiring significant changes to existing IT infrastructure.

Software at 67.8% dominates through platform licensing revenues from enterprise RPA suites, cloud-hosted orchestration hubs, and AI-enabled automation tools. Rule-based operations at 61.4% lead through deterministic, structured process automation in BFSI, healthcare, and retail verticals. The South region, at 35.8%, commands the largest share through its high concentration of financial services, healthcare, and technology enterprises deploying automation at an enterprise scale.

Key Market Insights

|

Insight |

Data |

|

Dominant Component |

Software – 67.8% share (2025) |

|

Dominant Operation |

Rule-based – 61.4% market share (2025) |

|

Leading Region |

South – 35.8% market share (2025) |

|

Market Opportunity |

Agentic AI-RPA convergence; hyperautomation platforms; low-code citizen developer tools; BFSI and healthcare compliance automation |

Key Analytical Observations Supporting the Above Data:

- Software at 67.8%: The software segment dominates as enterprises invest in RPA platform licenses, cloud-hosted orchestration hubs, and AI-augmented automation suites. Vendors including UiPath Inc. and Automation Anywhere Inc. drive recurring subscription revenue models that continuously increase software's share relative to services as deployments scale.

- Rule-based at 61.4%: Rule-based operations dominate through high-volume, structured process automation in accounts payable, claims processing, and data entry workflows. The deterministic execution model provides the compliance auditability required by regulated industries, ensuring rule-based bots remain the primary deployment mode across enterprise deployments.

- South at 35.8%: The South region leads through Texas and Florida's large financial services, healthcare, and logistics enterprise bases deploying RPA at scale. Favorable business regulation and a large enterprise workforce in states including Texas, Florida, North Carolina, and Georgia create strong structural automation demand that exceeds other US regions.

United States Robotic Process Automation Market Overview

The United States robotic process automation market encompasses the design, deployment, and management of software robots that automate repetitive, rule-based digital tasks across enterprise business processes. These bots interact with digital systems and applications to execute tasks including data entry, document processing, transaction handling, and workflow orchestration without requiring significant changes to existing IT infrastructure.

The ecosystem integrates RPA software vendors, cloud and IT infrastructure providers, system integrators and consultants, enterprise automation platform hubs, tier-1 technology partners, regulatory and compliance bodies, and end-user organizations. Macroeconomic factors include the accelerating digital transformation imperative, rising labor costs, workforce efficiency demands, and the convergence of artificial intelligence and machine learning with automation platforms.

Market Dynamics

To evaluate market opportunities, Request Sample

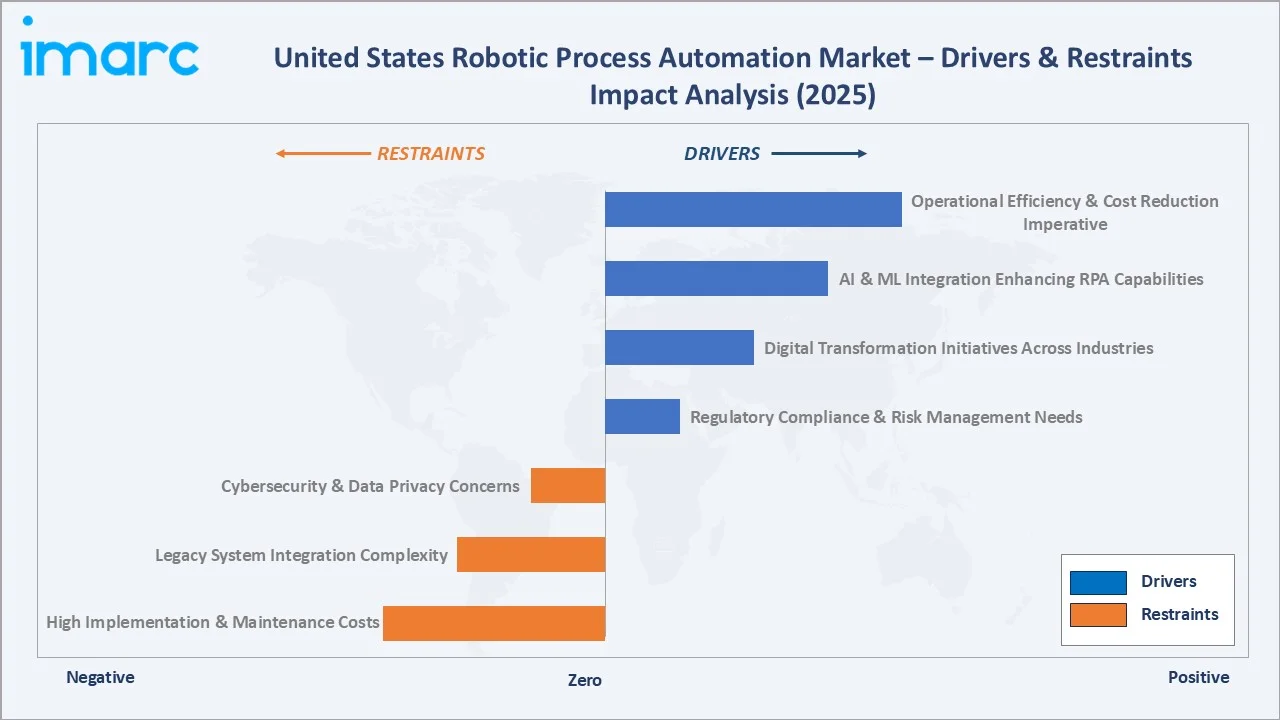

Market Drivers

- Operational Efficiency & Cost Reduction Imperative: Organizations across BFSI, healthcare, and retail are mandating digital transformation programs that place RPA at the center of operational efficiency strategies. Cost reduction targets of 30–50% in back-office operations are driving RPA deployment, enabling reallocation of human capital to higher-value strategic activities and reducing error rates in high-volume repetitive processes.

- AI & ML Integration Enhancing RPA Capabilities: The integration of AI and machine learning with RPA platforms, known as intelligent automation, significantly expands addressable use cases beyond rule-based tasks to complex decision-making workflows.

- Digital Transformation Initiatives Across Industries: The accelerating pace of digital transformation creates a structural tailwind for RPA adoption as organizations modernize legacy processes, migrate to cloud platforms, and automate workflows to remain competitive. Over 30 US federal agencies have adopted RPA to reduce lengthy wait times, increase throughput, and eliminate compliance difficulties, demonstrating the technology's enterprise-grade maturity across both private and public sectors.

- Regulatory Compliance & Risk Management Needs: Increasing regulatory complexity in healthcare, finance, and government sectors demands audit-ready, error-free process execution. RPA bots provide consistent, traceable automation that satisfies compliance requirements across HIPAA, SOX, and federal procurement frameworks, making them essential for regulated enterprise environments that require both speed and governance.

Market Restraints

- High Implementation & Maintenance Costs: Initial RPA deployment requires significant capital expenditure for platform licenses, infrastructure provisioning, integration services, and ongoing bot maintenance. For mid-market organizations, these upfront costs can delay return on investment realization and slow adoption relative to large enterprises that benefit from scale economics in automation program management.

- Legacy System Integration Complexity: Many US enterprises operate on heterogeneous legacy IT environments that are difficult to integrate with modern RPA tools. Unstructured data formats, outdated ERP systems, and lack of API connectivity create technical barriers requiring custom integration development, increasing deployment costs and extending implementation timelines beyond initial project estimates.

- Cybersecurity & Data Privacy Concerns: RPA bots with access to sensitive financial, healthcare, and personal data create cybersecurity and data privacy risks. Ensuring compliance with data governance frameworks while maintaining automation speed and scale presents ongoing operational challenges for enterprises deploying bots across regulated data environments.

Market Opportunities

- Agentic AI-RPA Convergence: The convergence of agentic AI with RPA platforms creates new opportunities for autonomous, multi-step workflow automation that dynamically adapts to exceptions without human intervention. In February 2026, UiPath Inc. launched agentic AI solutions for healthcare, enabling medical records summarization and claim denial prevention at enterprise scale.

- Low-Code Citizen Developer Expansion: Low-code and no-code RPA development environments are democratizing automation for citizen developers, expanding the total addressable market beyond enterprise IT departments to business unit leaders who can build and deploy bots without specialized coding expertise, significantly broadening the enterprise user base.

Market Challenges

- RPA Scaling & Governance Complexity: Enterprises often struggle to scale beyond initial bot deployments due to governance challenges, process standardization gaps, and organizational change management requirements. Establishing a robust center of excellence with defined bot lifecycle management practices is essential but resource-intensive for sustained program growth.

- Talent Shortage in Automation Expertise: The shortage of skilled RPA developers and intelligent automation specialist’s limits deployment velocity, particularly for knowledge-based and AI-augmented automation requiring advanced technical proficiency in both RPA platforms and machine learning methodologies.

Emerging Market Trends

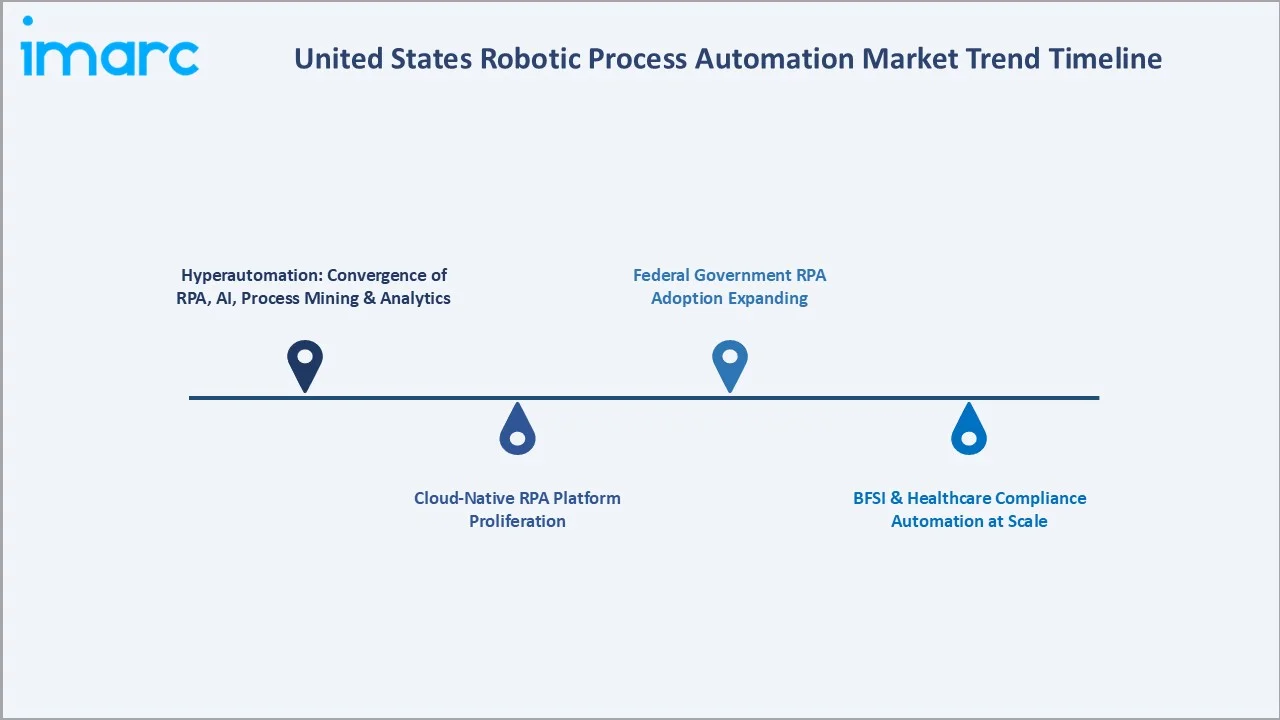

1. Hyperautomation: Convergence of RPA, AI, Process Mining & Analytics

Hyperautomation integrates RPA with AI, machine learning, process mining, and analytics to automate entire business workflows rather than isolated tasks. US enterprises are building hyperautomation centers of excellence that orchestrate end-to-end process transformation, replacing point automation solutions with enterprise-wide intelligent automation platforms that deliver measurably higher returns on automation investment.

2. Cloud-Native RPA Platform Proliferation

The shift to cloud-native RPA eliminates on-premises infrastructure requirements, enabling faster deployment, elastic scalability, and consumption-based pricing models. Automation Anywhere Inc.'s cloud-native architecture and Microsoft Corporation's Power Automate embedded in M365 are accelerating cloud RPA adoption across the US enterprise and mid-market segments by reducing the total cost and time to deployment.

3. BFSI & Healthcare Compliance Automation at Scale

Financial services and healthcare organizations are deploying RPA at scale to address regulatory reporting, claims adjudication, and audit trail requirements. NICE Ltd. secured a major contract with a leading global financial services firm to deploy robotic process automation across multiple back-office functions, validating the growing enterprise demand for compliance-grade automation in regulated sectors.

4. Federal Government RPA Adoption Expanding

Over 30 US federal agencies have adopted RPA to reduce lengthy wait times, increase throughput, and eliminate compliance difficulties. The US Air Force's adoption of RPA for repetitive task automation signals deepening government sector penetration that will expand through 2034 as agencies pursue efficiency mandates and workforce productivity improvement programs.

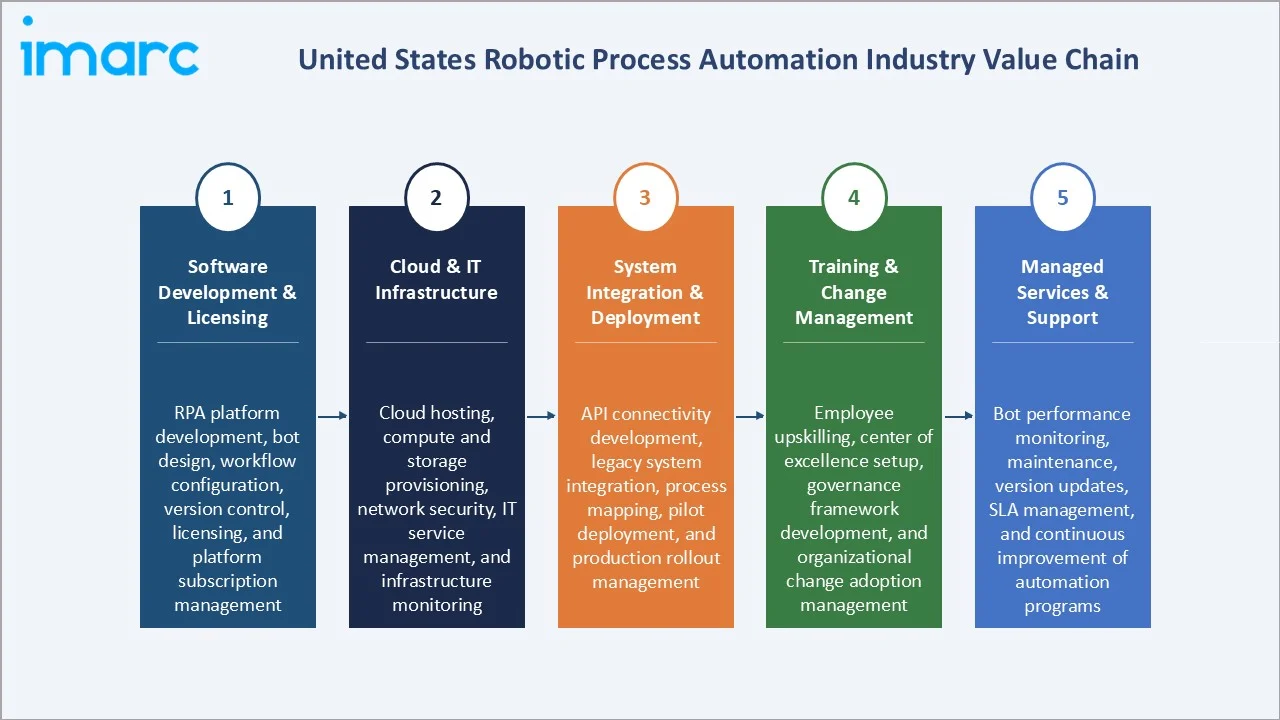

Industry Value Chain Analysis

The United States RPA value chain integrates software platform development, cloud and IT infrastructure provisioning, system integration and deployment services, training and change management, and managed services and support. The commercial architecture has progressively consolidated toward end-to-end platform partnerships as the dominant format, replacing the former separation between RPA tool vendor, integration services firm, and managed services provider.

|

Stage |

Key Participants & Activities |

|

Software Development & Licensing |

RPA platform development, bot design, workflow configuration, version control, licensing, and platform subscription management |

|

Cloud & IT Infrastructure |

Cloud hosting, compute and storage provisioning, network security, IT service management, and infrastructure monitoring |

|

System Integration & Deployment |

API connectivity development, legacy system integration, process mapping, pilot deployment, and production rollout management |

|

Training & Change Management |

Employee upskilling, center of excellence setup, governance framework development, and organizational change adoption management |

|

Managed Services & Support |

Bot performance monitoring, maintenance, version updates, SLA management, and continuous improvement of automation programs |

The software development and licensing tier captures the highest value-add, with leading vendors commanding recurring subscription premiums for AI-augmented platform capabilities. The system integration and deployment tier is experiencing the strongest services growth as enterprises require specialized expertise for complex, multi-system automation programs that span legacy and modern IT environments.

Technology Landscape in the United States Robotic Process Automation Industry

Rule-Based RPA Technology

Rule-based RPA technology automates structured, repetitive tasks through predefined if-then logic without requiring AI capabilities. It provides high-speed, error-free execution for high-volume transactional processes, including data entry, report generation, and invoice processing. Its non-invasive architecture, which allows bots to interact with existing systems through user interfaces without API integration, enables rapid deployment with minimal IT infrastructure change.

Intelligent Automation (AI-Augmented RPA) Technology

Intelligent automation integrates RPA with AI, natural language processing, and machine learning to handle unstructured data and complex decision-making processes. UiPath Inc.'s agentic automation platform was named one of TIME's Best Inventions of 2025 and recognized in G2's 2026 Best Software Awards in five categories, reflecting broad enterprise validation of AI-enhanced RPA capabilities that extend well beyond traditional rule-based automation scope.

Low-Code & No-Code RPA Platforms

Low-code and no-code platforms democratize bot development for citizen developers without programming expertise, expanding addressable automation use cases to non-technical business users. Microsoft Corporation's Power Automate, embedded within M365 subscriptions, represents the most widely deployed low-code automation platform in the US market, significantly broadening the population of automation practitioners beyond centralized IT departments.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Component |

Software |

67.8% |

2025 |

|

Operation |

Rule-based |

61.4% |

2025 |

|

Deployment Model |

🔒 |

🔒 |

2025 |

|

Organization Size |

🔒 |

🔒 |

2025 |

|

End User |

🔒 |

🔒 |

2025 |

|

Region |

South |

35.8% |

2025 |

By Component

The software segment leads at 67.8% in 2025, driven by platform licensing revenues from enterprise RPA suites, orchestration hubs, and AI-enabled automation tools. The segment captures recurring subscription value as vendors transition from perpetual licenses to SaaS models, continuously increasing software's revenue concentration over the forecast period as cloud-native deployments scale.

To access detailed market analysis, Request Sample

Services at 32.2% encompasses professional services for bot development, system integration, change management, and managed automation operations. As enterprises scale beyond pilot deployments to enterprise-wide automation programs, services demand intensifies, supporting sustained services segment growth. The services segment is expected to grow consistently through 2034 as the complexity of intelligent automation programs drives demand for specialist implementation and governance support.

By Operation

Rule-based operations dominate at 61.4% in 2025, capturing the structured, high-volume automation core of the US RPA market. Rule-based bots execute deterministic workflows with the accuracy and auditability required in regulated BFSI and healthcare environments, maintaining their leading position as the foundational automation layer upon which intelligent automation capabilities are built through 2034.

Knowledge-based operations at 38.6% represent the market's fastest-growing segment at approximately 31.1% CAGR, driven by AI-augmented RPA platforms that handle unstructured data, natural language inputs, and exception-based decision-making. The convergence of generative AI with RPA is accelerating knowledge-based adoption across customer service, financial analysis, and clinical documentation applications as AI models become embedded in enterprise automation workflows.

Regional Market Insights

|

Region |

Share (2025) |

Key RPA Market Drivers & Characteristics |

|

South |

35.8% |

Driven by large enterprise concentration in financial services, healthcare, and logistics sectors, supported by favorable business regulation and strong digital transformation investment |

|

West |

28.6% |

Driven by technology sector density and software-native enterprise culture, with organizations building internal automation capabilities alongside vendor-deployed platforms |

|

Northeast |

21.4% |

Driven by financial services, healthcare systems, and insurance sector automation demand, with emphasis on compliance-grade, audit-ready automation deployments |

|

Midwest |

14.2% |

Driven by manufacturing, logistics, and agricultural enterprise automation of supply chain, ERP, and back-office workflows, with growth accelerating as industries digitize |

The South, at 35.8%, leads through its combination of large financial services headquarters, major healthcare systems, and high-volume logistics and retail operations. The West, at 28.6%, reflects the California and Washington technology industry concentration where software-native enterprises build internal automation capabilities alongside vendor-deployed RPA solutions.

The Northeast, at 21.4%, captures compliance-driven automation demand from financial institutions deploying RPA for regulatory reporting, trade reconciliation, and customer onboarding. The Midwest, at 14.2%, is driven by manufacturing and logistics enterprises automating supply chain workflows, with growth accelerating as industrial enterprises pursue digitization programs aligned with broader US manufacturing modernization trends.

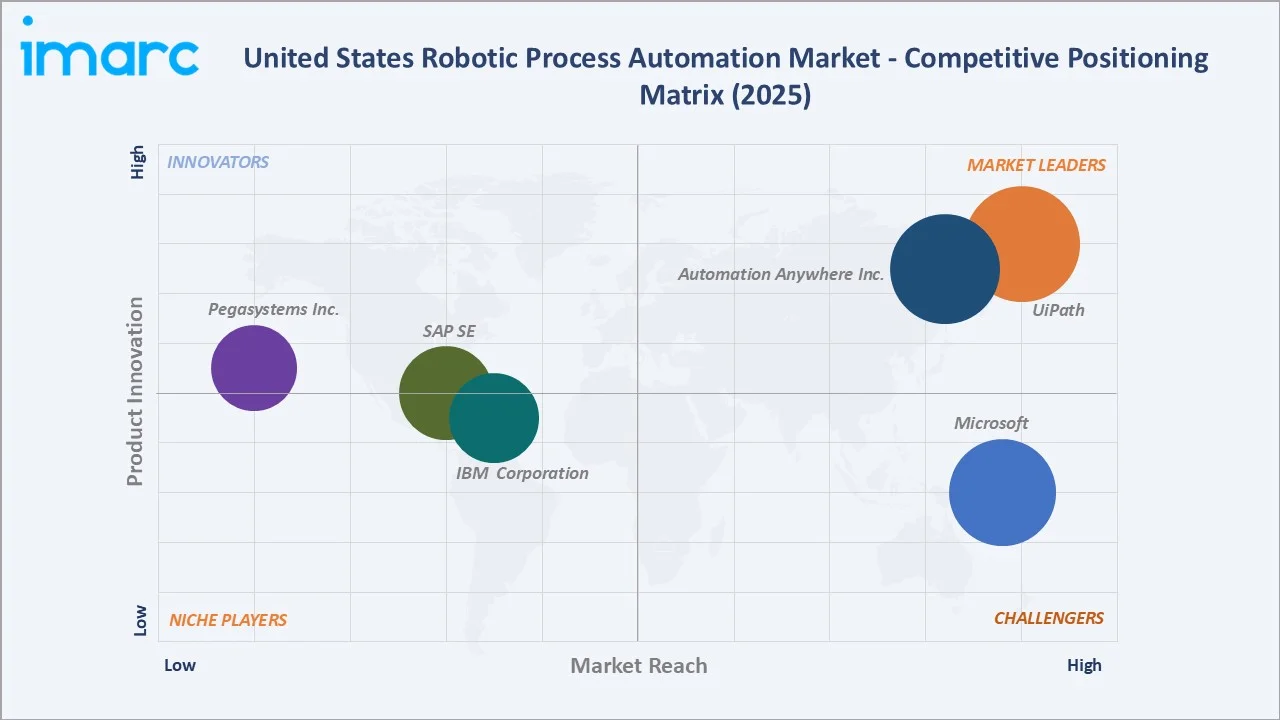

Competitive Landscape

The United States robotic process automation market competitive landscape is moderately concentrated with three distinct competitive tiers: pure-play enterprise RPA leaders with dedicated automation suites, enterprise software giants embedding RPA capabilities within broader platform ecosystems, and specialized compliance-focused automation platforms serving regulated industry verticals with governance-first architectures.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

UiPath |

UiPath Platform, Studio, Orchestrator, Document Understanding |

Market Leader |

UiPath specializes in enterprise-grade agentic automation, combining RPA, AI agents, and process orchestration to deliver end-to-end automation across complex business workflows. |

|

Automation Anywhere Inc. |

Automation 360, IQ Bot, Bot Store, CoE Manager |

Market Leader |

Automation Anywhere Inc. specializes in cloud-native intelligent automation, offering a fully SaaS-based platform that combines RPA, AI-powered document processing, and agentic process automation at enterprise scale. |

|

Microsoft |

Power Automate, Azure Logic Apps, Copilot Studio |

Strong Challenger |

Microsoft specializes in low-code and AI-powered automation, embedding RPA and workflow automation capabilities natively within its Microsoft 365 and Azure cloud ecosystem for enterprise and mid-market organizations. |

|

IBM Corporation |

IBM RPA |

Established Player |

IBM Corporation specializes in enterprise AI-driven automation, combining robotic process automation with intelligent agent orchestration to deliver governed, hybrid-cloud automation solutions. |

|

SAP SE |

SAP Build Process Automation |

Established Player |

SAP SE specializes in native ERP-integrated process automation, delivering low-code RPA and workflow automation capabilities built directly within the SAP Business Technology Platform. |

|

Pegasystems Inc. |

Pega Platform |

Established Player |

Pegasystems Inc. specializes in AI-powered enterprise process automation, combining RPA, business process management, and case management capabilities. |

Key players include UiPath, Automation Anywhere Inc., Microsoft, IBM Corporation, SAP SE, Pegasystems Inc., and others.

Key Company Profiles

UiPath

UiPath is a New York-based enterprise automation platform company and the world's largest pure-play RPA vendor by revenue. UiPath Inc. leads the US RPA market through its enterprise-grade automation suite, combining RPA, AI document processing, process mining, test automation, and agentic orchestration capabilities that address the full spectrum of enterprise automation requirements.

- Key Products: UiPath Platform, Studio, Orchestrator, Document Understanding

- Strategic Focus: Expanding agentic AI orchestration capabilities, integrating RPA with large language models for enterprise-wide intelligent automation, and deepening healthcare and financial services vertical automation solutions. UiPath Inc. reported a 107% dollar-based net retention rate, reflecting strong enterprise platform stickiness.

Automation Anywhere Inc.

Automation Anywhere Inc. is a San Jose, California-based cloud-native RPA and intelligent automation platform company. Automation Anywhere Inc. holds the second-largest enterprise RPA market share globally, competing directly with UiPath Inc. through its fully cloud-hosted multi-tenant SaaS architecture that requires no on-premises infrastructure investment from enterprise customers.

- Key Products: Automation 360, IQ Bot, Bot Store, CoE Manager

- Strategic Focus: Expanding AI-powered intelligent automation for SAP and Salesforce ecosystems, scaling cloud-native RPA deployment across enterprise and mid-market segments, and growing consumption-based pricing models that reduce upfront enterprise adoption friction.

Microsoft

Microsoft is a Redmond, Washington-based global technology company embedding RPA capabilities within its M365 and Azure cloud ecosystem through Power Automate. Microsoft Corporation's Power Automate represents the most broadly deployed automation capability in the US market through its deep integration within M365 subscription packages consumed by enterprises of all sizes.

- Key Products: Power Automate, Azure Logic Apps, Copilot Studio

- Recent Developments: In May 2020, Microsoft announced the acquisition of Softomotive, a leading provider of robotic process automation (RPA) solutions. The acquisition was aimed at strengthening the capabilities of Microsoft Power Automate by integrating advanced desktop automation features into its low-code automation ecosystem.

- Strategic Focus: Expanding low-code RPA and AI agent capabilities within the M365 ecosystem to capture the citizen developer market, while building enterprise-grade automation through strategic partnerships with pure-play RPA vendors to extend automation capabilities across the full enterprise automation value chain.

Market Concentration Analysis

The US RPA market is moderately concentrated at the enterprise platform level, with the top 4 players collectively accounting for approximately 55–65% of US enterprise RPA platform revenue. The mid-market segment is more fragmented, with Microsoft Corporation's Power Automate dominant among small and medium-sized enterprises embedded within existing M365 deployments at relatively low incremental cost.

Market concentration is declining over the forecast period as Microsoft Corporation's platform growth expands the citizen developer automation segment, IBM Corporation and SAP SE grow within their respective enterprise ecosystems, and emerging agentic AI automation vendors create new competitive segments at the premium platform tier, reducing the aggregate market share of the top three pure-play RPA vendors.

Investment & Growth Opportunities

Highest Growth Segments

Knowledge-based operations at approximately 31.1% CAGR, software component at approximately 28.5% CAGR, agentic AI-RPA platform development at approximately 35%+ CAGR from an emerging commercial base, federal government automation at approximately 25% CAGR, healthcare compliance automation at approximately 28% CAGR, and BFSI intelligent automation represent the highest-growth investment vectors through 2034 in the US market.

Emerging Investment Opportunities

Agentic AI-RPA platform development represents the US RPA market's highest-value emerging opportunity, as enterprises transition from task-level automation to autonomous workflow orchestration that handles multi-step, multi-system processes without human intervention at each decision point. Healthcare revenue cycle management automation presents a structural growth opportunity driven by claims adjudication, prior authorization, and clinical documentation automation requirements at enterprise scale.

Investment Themes

- Hyperautomation Platform Development: Platforms that combine RPA, AI agents, process mining, and analytics into unified orchestration environments capture the highest enterprise value and create the strongest platform stickiness. Vendors offering complete hyperautomation suites command premium license revenue versus point-solution RPA vendors and demonstrate significantly higher customer retention rates.

- Government Sector Automation Expansion: Federal and state government RPA deployment represents a large, long-cycle, and competitively protected market segment requiring compliance certification, security clearance integration, and audit-ready bot governance. Vendors with established federal sector credentials are well-positioned to capture this expanding and highly defensible segment through 2034.

Future Market Outlook (2026-2034)

The United States robotic process automation market is projected to grow from USD 1.61 Billion in 2025 to USD 15.13 Billion by 2034, delivering a 26.88% CAGR over the nine-year forecast period. The market's interim value of USD 5.29 Billion in 2030 reflects a US automation landscape at its most transformative commercial inflection, as agentic AI platforms begin displacing traditional rule-based bot architectures at the enterprise level and hyperautomation programs move from pilot to enterprise-wide deployment.

Three structural forces define US RPA market growth through 2034 with high confidence: the digital transformation imperative creating persistent structural automation demand across all enterprise verticals; the AI-RPA convergence that multiplies addressable use cases from structured task automation to unstructured workflow management; and the government sector adoption that expands the total addressable market with long-cycle, high-value automation contracts that are competitively defensible once initial deployment is established.

Research Methodology

Primary Research

Primary research comprised structured interviews with 45+ industry stakeholders conducted in 2025, including Chief Digital Officers, RPA center of excellence program leads, enterprise automation architects, federal agency IT directors, and cloud platform integration specialists. Interview insights were triangulated with market model outputs to validate segment sizing assumptions and growth rate forecasts.

Secondary Research

Secondary research encompassed company annual reports, Gartner Magic Quadrant for RPA 2025, Everest Group intelligent process automation assessments, G2 enterprise software rankings, US federal agency automation program disclosures, Forrester RPA market analysis reports, and vendor investor relations materials. More than 55 secondary sources were reviewed and synthesized in the final market model.

Forecasting Models

Market revenue forecasts were developed using an enterprise adoption-based bottom-up model incorporating: US enterprise automation budget allocation by vertical and organization size; RPA platform license revenue per enterprise by segment; services attachment rate per license deployment; and AI-augmentation premium adjustment for intelligent automation versus standard rule-based RPA pricing. Forecast outputs were validated against comparable market growth rates from analogous enterprise software categories.

United States Robotic Process Automation Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Software, Services |

| Operations Covered | Rule-based, Knowledge-based |

| Deployment Models Covered | On-premises, Cloud-based |

| Organization Sizes Covered | Large Enterprises, Small and Medium-sized Enterprises |

| End Users Covered | BFSI, Healthcare and Pharmaceuticals, Retail and Consumer Goods, IT and Telecommunication, Government and Defense, Transportation and Logistics, Energy and Utilities, Others |

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered | UiPath, Automation Anywhere Inc., Microsoft, IBM Corporation, SAP SE, Pegasystems Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the United States robotic process automation market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the United States robotic process automation market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the United States robotic process automation industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the United States Robotic Process Automation Market Report

The US RPA market reached USD 1.61 Billion in 2025, driven by software platforms at 67.8%, rule-based automation at 61.4%, the South region leading at 35.8%, and accelerating AI integration expanding enterprise automation scope across BFSI, healthcare, and government sectors.

The US RPA market grows at 26.88% CAGR during 2026-2034, reaching USD 15.13 Billion by 2034, reflecting the structural digital transformation imperative, AI-RPA convergence, low-code platform democratization, and government sector automation expansion.

Software leads at 67.8% through platform licensing revenues from enterprise RPA suites and AI-augmented automation tools. Recurring SaaS subscription models continuously increase software revenue concentration as enterprise deployments scale and AI capabilities are added to automation platforms.

Rule-based operations lead at 61.4% through structured, deterministic automation in BFSI, healthcare, and retail workflows. Knowledge-based operations grow fastest at approximately 31.1% CAGR as AI-augmented bots expand the addressable automation universe beyond structured tasks.

The South leads at 35.8% through Texas and Florida's large financial services, healthcare, and logistics enterprise concentration, followed by the West at 28.6% driven by the California technology sector and software-native enterprise culture.

Leading companies include UiPath, Automation Anywhere Inc., Microsoft, IBM Corporation, SAP SE, Pegasystems Inc., and others.

The US RPA market is projected to reach approximately USD 5.29 Billion by 2030, with agentic AI automation becoming mainstream, hyperautomation platforms displacing point-solution RPA tools, and government sector automation expanding significantly across federal and state agency deployments.

Three priority investment opportunities: agentic AI-RPA platform development for enterprise hyperautomation, healthcare revenue cycle and clinical documentation automation at scale, and federal government RPA deployment with compliance-certified bot governance frameworks.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)