United States SCADA Market Size, Share, Trends and Forecast by Component, Architecture, End User, and Region, 2026-2034

United States SCADA Market Size, Share, Trends & Forecast (2026-2034)

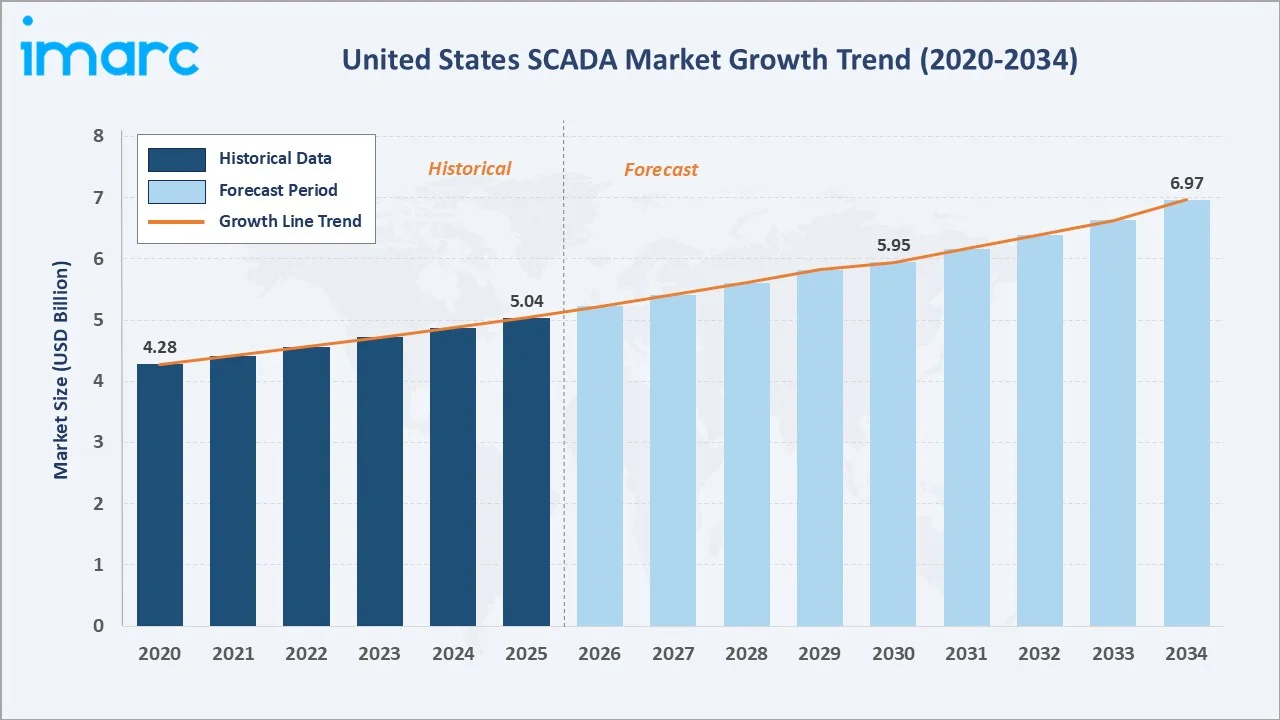

The United States SCADA market size increased from USD 5.04 Billion in 2025 to USD 5.21 Billion in 2026 and is projected to reach USD 6.97 Billion by 2034, exhibiting a CAGR of 3.35% during 2026-2034. Growing industrial automation, smart grid modernization, rising IIoT adoption, and cybersecurity mandates are primary forces driving growth.

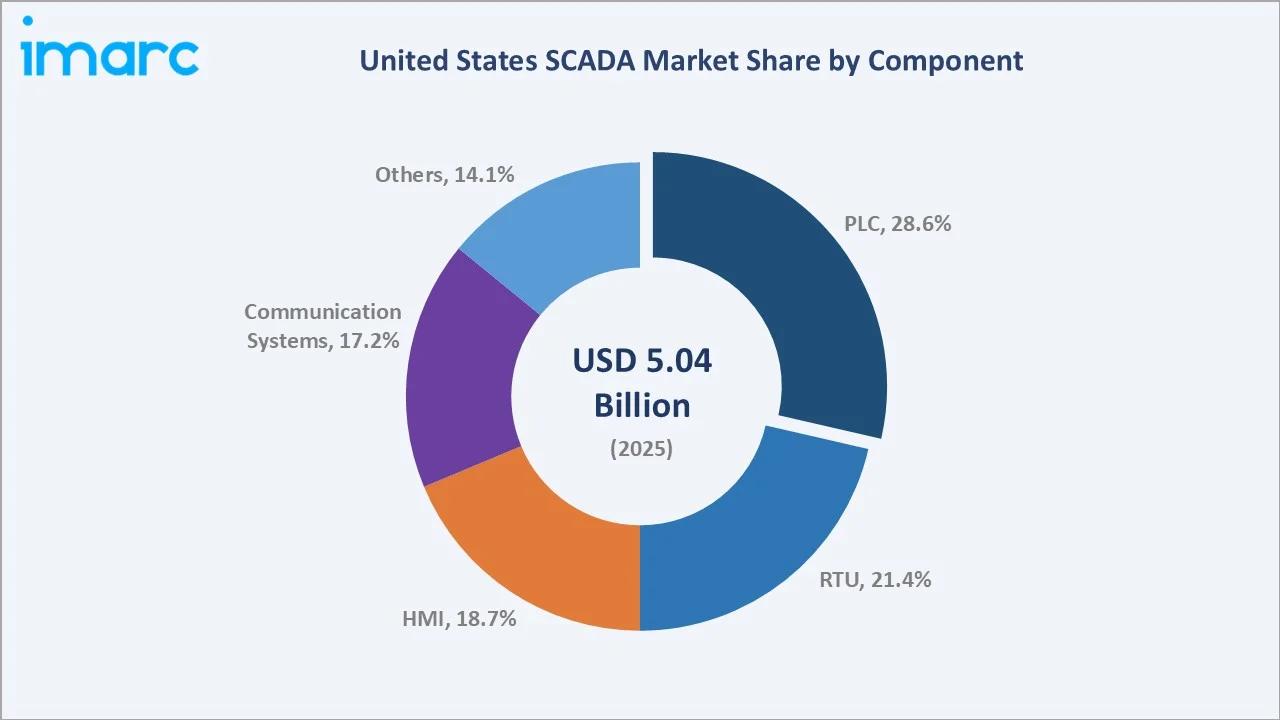

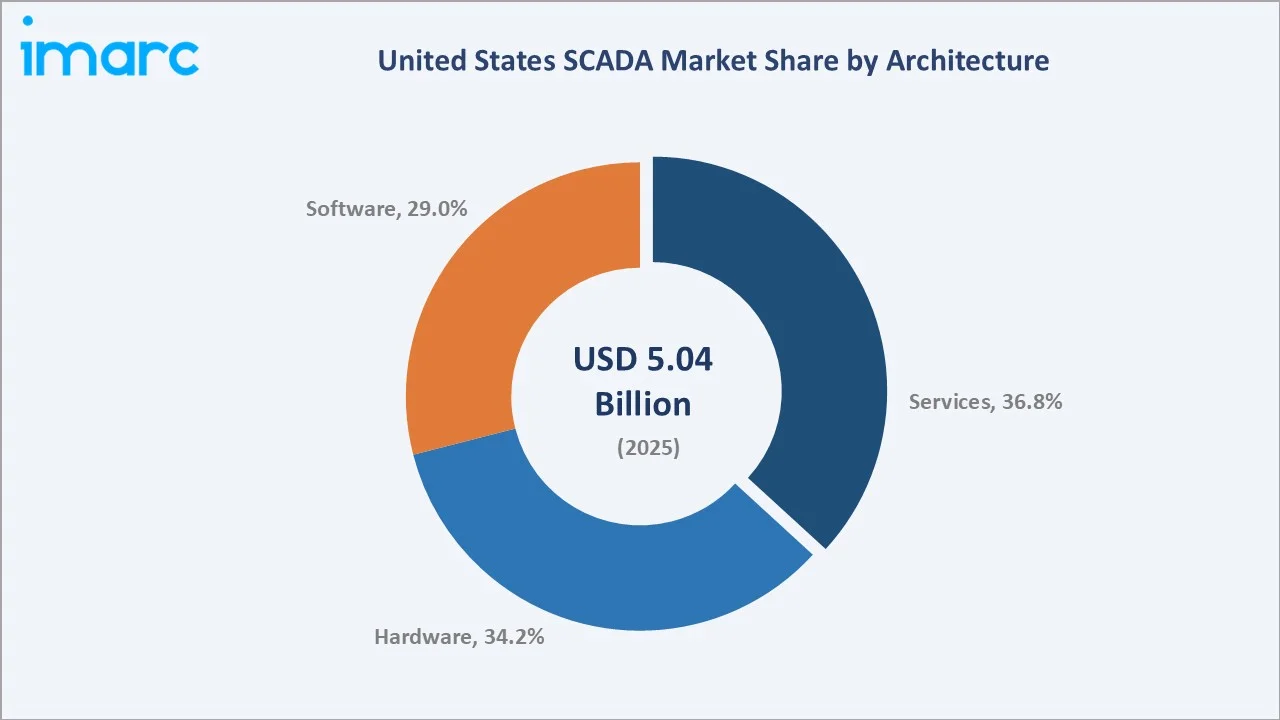

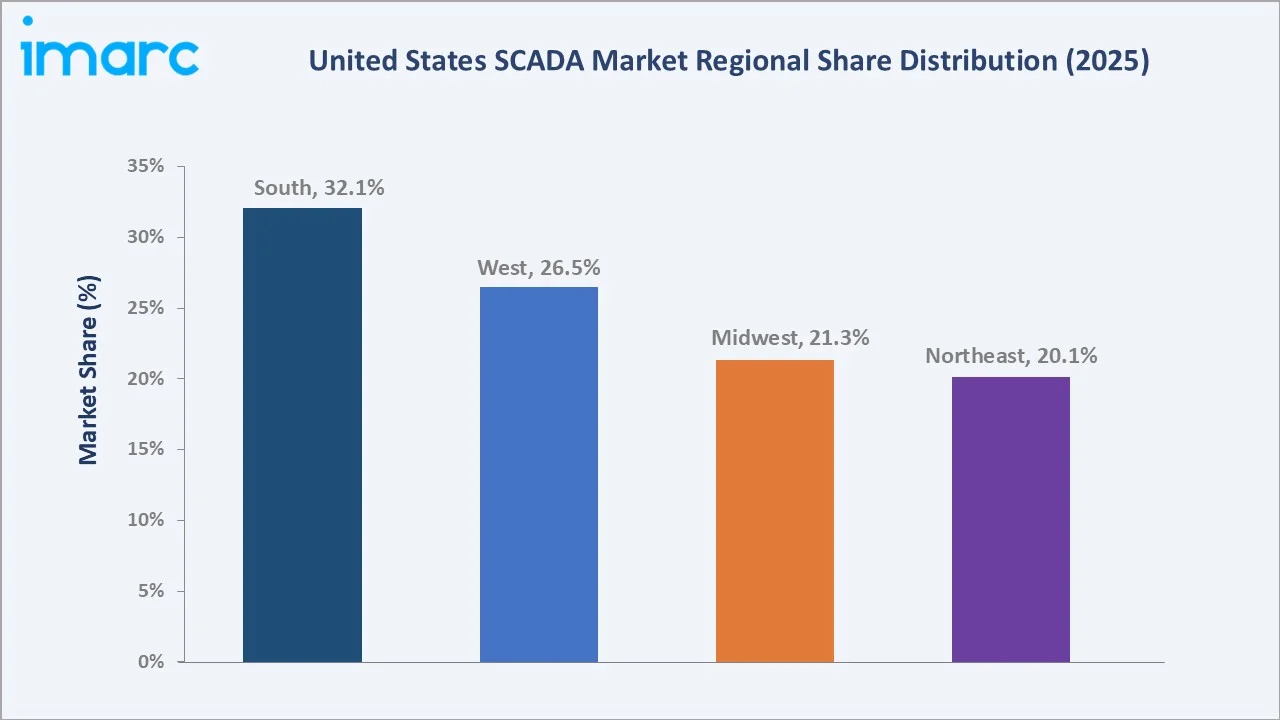

Programmable Logic Controller (PLC) dominates at 28.6% in 2025, while Services leads architecture at 36.8%. The South commands 32.1% regional share.

Market Snapshot

|

Metric |

Value |

|

Base Year Market Size (2025) |

USD 5.04 Billion |

| Market Size (2026) | USD 5.21 Billion |

|

Forecast Market Size (2034) |

USD 6.97 Billion |

|

CAGR (2026-2034) |

3.35% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Leading Component |

Programmable Logic Controller (PLC) – 28.6% (2025) |

|

Leading Architecture |

Services – 36.8% (2025) |

|

Largest Region |

South – 32.1% (2025) |

The United States SCADA market growth trajectory from 2020 through 2034, with historical expansion to USD 5.04 Billion in 2025 to USD 5.21 Billion in 2026 and forecast to USD 6.97 Billion by 2034, reflects sustained infrastructure-driven demand, energy transition investment, and IIoT integration across US industries.

To get more information on this market, Request Sample

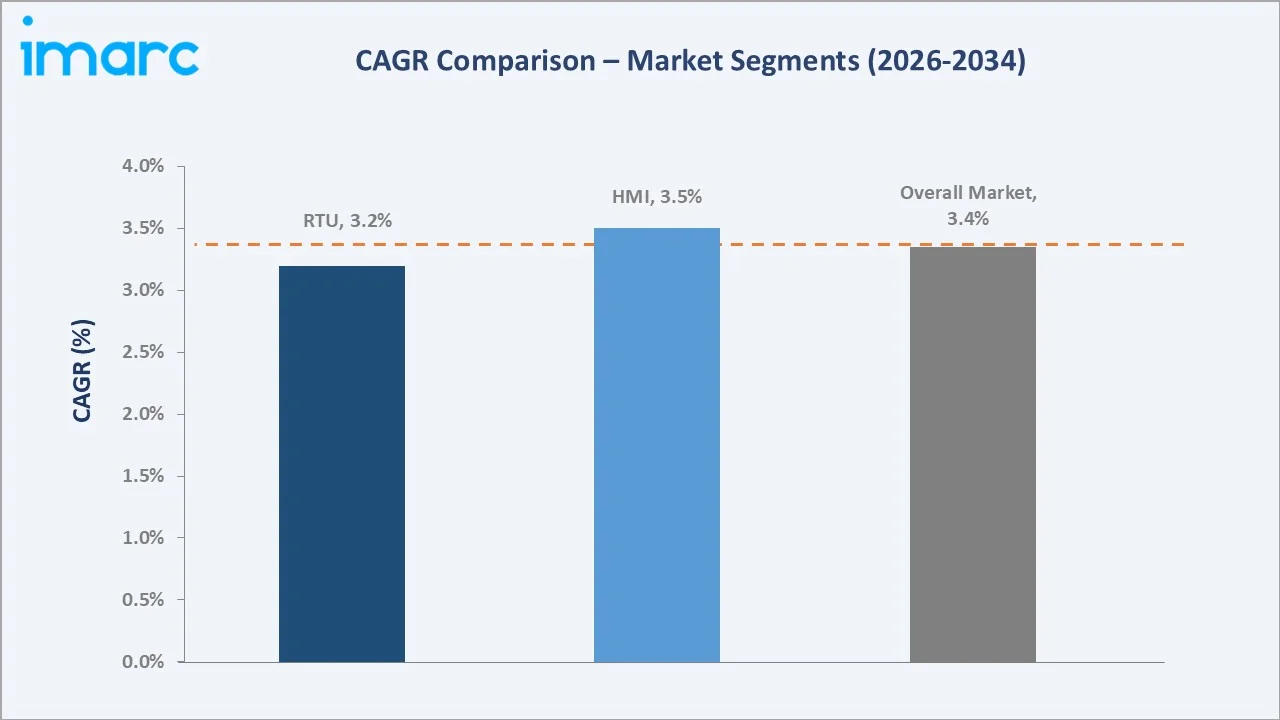

The CAGR trajectories across key component, architecture, and regional sub-segments, with Services at ~4.2% CAGR and Communication Systems at ~4.1% CAGR, represent the fastest-growing categories within the US SCADA industry through 2034.

Executive Summary

The United States SCADA market is on a sustained growth trajectory from USD 5.04 Billion in 2025 to USD 5.21 Billion in 2026 and is projected to reach USD 6.97 Billion by 2034. SCADA systems are deployed across energy, utilities, manufacturing, and water management for real-time monitoring and industrial control.

Programmable Logic Controllers (PLC) dominate at 28.6% in 2025, owing to their foundational role in discrete and process manufacturing automation across US industries. Remote Terminal Units (RTU) follow at 21.4%, deployed extensively in remote infrastructure monitoring.

Services architecture leads at 36.8% in 2025, reflecting growing demand for managed SCADA services, cloud migration support, and cybersecurity consulting. Hardware accounts for 34.2%, driven by new industrial deployments, while software at 29.0% grows fastest with cloud adoption.

The South dominates regionally at 32.1% in 2025, driven by oil and gas infrastructure concentration in Texas and Louisiana. The West follows at 26.5%, led by smart grid investments and California renewable energy integration programs.

Key Market Insights

|

Insight |

Data |

|

Leading Component |

Programmable Logic Controller (PLC) – 28.6% share (2025) |

|

Second Component |

Remote Terminal Units (RTU) – 21.4% share (2025) |

|

Leading Architecture |

Services – 36.8% share (2025) |

|

Leading Region |

South – 32.1% share (2025) |

|

Some Top Companies |

ABB, Emerson Electric Co., GE Vernova, Honeywell International Inc., Mitsubishi Electric Iconics Digital Solutions, Inc., Siemens, Yokogawa Electric Corporation |

Key Analytical Observations:

- PLC at 28.6% dominates because programmable logic controllers remain the foundational automation layer across US manufacturing, energy, and water treatment facilities, offering real-time control, scalability, and integration with HMI and SCADA software platforms.

- Services at 36.8% reflects the maturing US SCADA market where enterprises increasingly outsource integration, maintenance, cybersecurity monitoring, and cloud migration to specialized providers to reduce total cost of ownership.

- The South's 32.1% dominance reflects the concentration of oil and gas infrastructure in Texas and Louisiana, including offshore platforms, refineries, pipelines, and LNG export terminals requiring extensive SCADA monitoring networks.

- The West at 26.5% benefits from California smart grid investments, renewable energy integration, data center expansion, and the region's leadership in deploying advanced industrial IoT-enabled SCADA platforms.

United States SCADA Market Overview

SCADA (Supervisory Control and Data Acquisition) is a control architecture integrating computers, graphical user interfaces, and networked data communications for high-level supervisory management and real-time data acquisition from geographically distributed industrial assets across the United States.

The US SCADA ecosystem integrates hardware manufacturers (PLC, RTU, HMI), software developers, systems integrators, cybersecurity solution providers, communication infrastructure operators, and diverse end-use industries spanning energy, utilities, manufacturing, chemicals, pharmaceuticals, and transportation.

Market Dynamics

To evaluate market opportunities, Request Sample

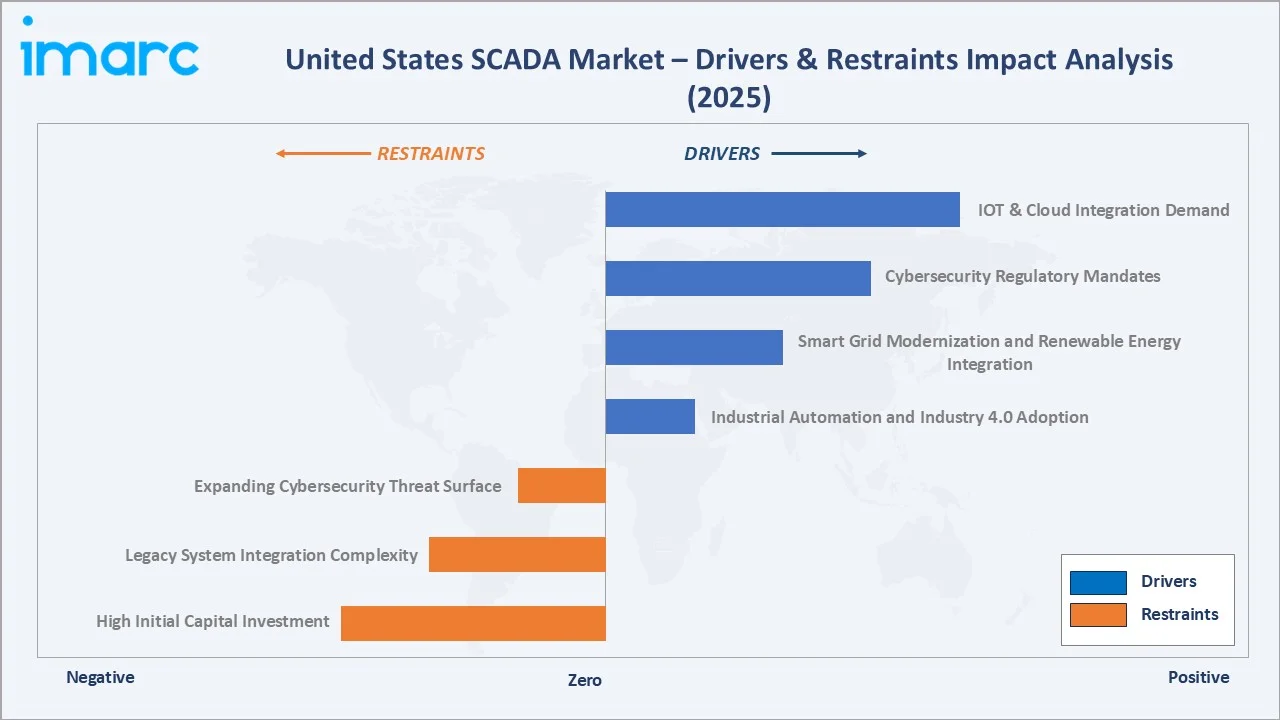

Market Drivers

- Industrial Automation and Industry 4.0 Adoption: US manufacturers are accelerating SCADA deployments as part of Industry 4.0 transformation. The US Department of Energy reported a 20% increase in operational efficiency from SCADA implementation, driving broader sector-wide adoption of advanced monitoring platforms.

- Smart Grid Modernization and Renewable Energy Integration: The US energy sector transition toward renewable sources requires advanced SCADA for real-time monitoring of decentralized generation. US electricity consumption reached a record 4.07 Trillion kWh in 2022, necessitating sophisticated grid management infrastructure.

- Cybersecurity Regulatory Mandates: Stringent TSA, NERC-CIP, and CISA regulations compel critical infrastructure operators to upgrade SCADA with advanced cybersecurity capabilities. Projected global cybercrime costs of USD 10.5 Trillion annually by 2025 underscore urgency for investment.

Market Restraints

- High Initial Capital Investment: Advanced SCADA deployment requires significant investment in hardware, software, and specialized integration personnel, deterring smaller enterprises and municipalities with constrained budgets from upgrading legacy industrial control systems.

- Legacy System Integration Complexity: Many US industrial facilities operate decades-old control systems difficult to integrate with modern SCADA platforms, requiring costly custom middleware development and extended project timelines that delay technology adoption benefits.

Market Opportunities

- Cloud-Based SCADA Expansion: Growing adoption of cloud-native SCADA platforms enables scalable, remote-access industrial monitoring without heavy on-premises hardware investment, creating significant opportunities for software vendors and managed service providers across US markets. In March 2022, Emerson Electric enhanced its Zedi Cloud SCADA platform by migrating it to Microsoft Azure, strengthening its ability to support scalable, secure, and sustainable industrial operations. This transition improves system performance, data protection, and threat intelligence, allowing organizations to expand their SCADA infrastructure more efficiently while reducing operational risks and costs.

- IIoT and Edge Computing Integration: The convergence of Industrial IoT sensors, edge computing, and AI analytics with SCADA creates new opportunities for predictive maintenance, autonomous process optimization, and reduced latency in critical real-time control applications.

Market Challenges

- Cybersecurity Threat Proliferation: As SCADA systems become increasingly connected to enterprise IT networks, attack surface expansion creates persistent vulnerabilities. Industrial control system cyberattacks have increased significantly, requiring continuous security investment and workforce upskilling.

- Skilled OT/IT Workforce Shortage: The shortage of professionals combining industrial operations technology with IT cybersecurity expertise creates staffing challenges for SCADA deployment, maintenance, and monitoring across US critical infrastructure operators.

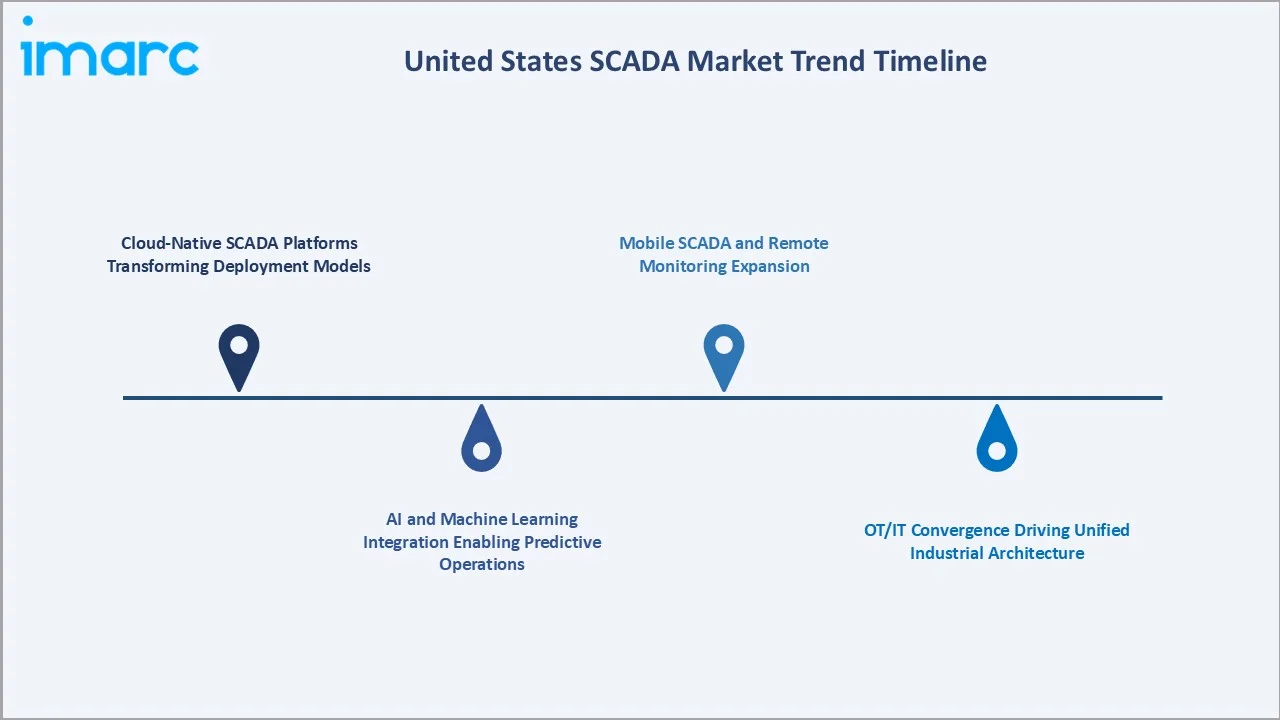

Emerging Market Trends

1. Cloud-Native SCADA Platforms Transforming Deployment Models

Cloud-based SCADA eliminates traditional server infrastructure costs and enables remote scalable access. Leading vendors offer cloud-native SCADA-as-a-Service, reducing deployment barriers for mid-sized US industrial operators seeking modernization without heavy capital expenditure commitments.

2. AI and Machine Learning Integration Enabling Predictive Operations

Integration of AI and machine learning into SCADA platforms enables predictive maintenance, anomaly detection, and autonomous process optimization. US utilities and manufacturers deploy AI-enhanced SCADA to reduce unplanned downtime, delivering measurable ROI that drives further technology investment.

3. OT/IT Convergence Driving Unified Industrial Architecture

The convergence of operational technology and information technology networks reshapes US SCADA architecture. Unified OT/IT platforms enable enterprise-wide visibility and analytics while requiring enhanced cybersecurity frameworks to protect expanded industrial network perimeters from evolving threats.

4. Mobile SCADA and Remote Monitoring Expansion

Mobile SCADA platforms enabling real-time monitoring via smartphones and tablets are transforming US workforce operations in oil and gas, utilities, and manufacturing. Remote monitoring capabilities accelerated by the pandemic remain permanent operational requirements across industrial sectors.

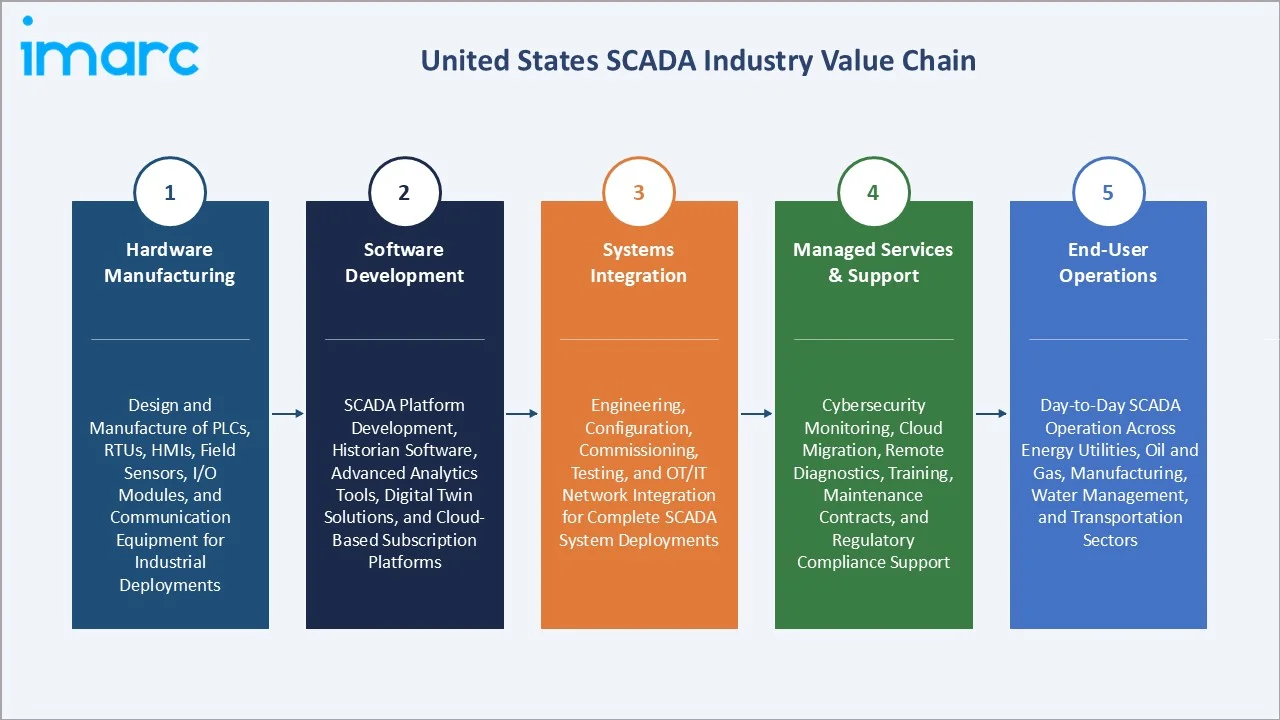

Industry Value Chain Analysis

The US SCADA value chain spans five stages from hardware manufacturing through end-user operations. Systems integration and managed cybersecurity services capture the highest value-add margins, while hardware manufacturing and software licensing provide the foundational product and platform layers.

|

Stage |

Key Activities / Examples |

|

Hardware Manufacturing |

Design and manufacture of PLCs, RTUs, HMIs, field sensors, I/O modules, and communication equipment for industrial automation deployments |

|

Software Development |

SCADA platform development, historian software, advanced analytics tools, digital twin solutions, and cloud-based subscription platforms |

|

Systems Integration |

Engineering, configuration, commissioning, testing, and OT/IT network integration for complete SCADA system deployments |

|

Managed Services & Support |

Cybersecurity monitoring, cloud migration, remote diagnostics, training, maintenance contracts, and regulatory compliance support |

|

End-User Operations |

Day-to-day SCADA operation and optimization across energy utilities, oil and gas, manufacturing, water management, and transportation |

The US SCADA value chain is characterized by increasing vertical integration at the systems integration stage, where leading vendors combine hardware, software, and services into bundled solutions. Managed services are the fastest-growing stage, capturing recurring revenue from operators outsourcing cybersecurity and cloud migration.

Software and services collectively account for approximately 66% of total US SCADA market value in 2025, reflecting the shift from hardware-centric deployment models toward subscription-based, cloud-delivered SCADA platforms that offer lower upfront costs and continuous capability upgrades.

Technology Landscape in the US SCADA Industry

Communication Protocols: From Legacy Standards to Open Architecture

The US SCADA industry is transitioning from proprietary protocols (DNP3, Modbus RTU) to open industrial standards including IEC 61850, OPC-UA, and MQTT. This migration enables seamless multivendor integration and cloud connectivity, accelerating digital transformation in US energy and manufacturing operations.

Cybersecurity Architecture: Defense-in-Depth for Industrial Networks

Modern US SCADA deployments implement defense-in-depth cybersecurity architectures incorporating industrial firewalls, unidirectional security gateways, anomaly detection systems, and encrypted communications. NIST CSF and ISA/IEC 62443 standards guide cybersecurity implementations across US critical infrastructure SCADA networks.

Edge Computing and Distributed Intelligence

Edge computing integration with SCADA enables local data processing at remote field sites, reducing latency for critical control decisions and bandwidth requirements for centralized cloud systems. US oil and gas operators lead edge SCADA adoption for offshore and remote pipeline monitoring applications.

Artificial Intelligence and Digital Twin Integration

AI-powered SCADA platforms use machine learning algorithms to analyze historical process data, detect anomalies, and predict equipment failure up to 30 days in advance. Digital twin technology creates virtual replicas of physical industrial assets that interact with live SCADA data streams, enabling scenario simulation, operator training, and virtual commissioning of new control strategies without operational disruption.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Component |

Programmable Logic Controller (PLC) |

28.6% |

2025 |

|

Architecture |

Services |

36.8% |

2025 |

|

End User |

Oil and Gas |

🔒 |

2025 |

|

Region |

South |

32.1% |

2025 |

By Component

Programmable logic controllers (PLC) command a 28.6% majority share in 2025 owing to their fundamental role as real-time industrial process controllers. PLCs provide millisecond-level scan cycle control, fault tolerance, and broad compatibility with field sensors and actuators across US manufacturing, utilities, and energy automation deployments.

To access detailed market analysis, Request Sample

RTUs at 21.4% serve critical roles in geographically remote monitoring applications including pipeline SCADA, electrical substations, and water distribution networks where localized control with minimal communication latency is essential for reliable operations.

By Architecture

Services architecture dominates at 36.8% in 2025, reflecting the growing trend of US enterprises outsourcing SCADA integration, maintenance, cybersecurity monitoring, and cloud migration to specialized providers. Managed SCADA services enable asset owners to focus on core operations while ensuring system reliability and regulatory compliance.

Hardware at 34.2% reflects ongoing US industrial facility upgrades and new plant construction requiring PLC, RTU, HMI, and communication equipment. Major capital investment in semiconductor fabs (CHIPS Act), LNG terminals, and renewable energy infrastructure drives hardware procurement demand.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

South |

32.1% |

Oil & gas (Texas/Louisiana), LNG export terminals, petrochemical SCADA infrastructure |

|

West |

26.5% |

Smart grid (California), renewable energy integration, data center and tech sector automation |

|

Midwest |

21.3% |

Industrial manufacturing automation, grain processing, utility modernization programs |

|

Northeast |

20.1% |

Water utility upgrades, transportation SCADA, pharmaceutical manufacturing automation |

The South's 32.1% market dominance in 2025 is driven by the most concentrated oil and gas infrastructure in the United States. Texas and Louisiana together host thousands of SCADA-intensive assets including refineries, LNG export terminals, offshore platforms, and pipeline networks totaling over 2.7 million miles.

The West at 26.5% benefits from California's aggressive grid modernization programs and renewable energy mandate requiring 100% clean electricity by 2045, demanding advanced SCADA for distributed energy resource management. Data center expansion in Oregon, Nevada, and Washington further amplifies regional demand.

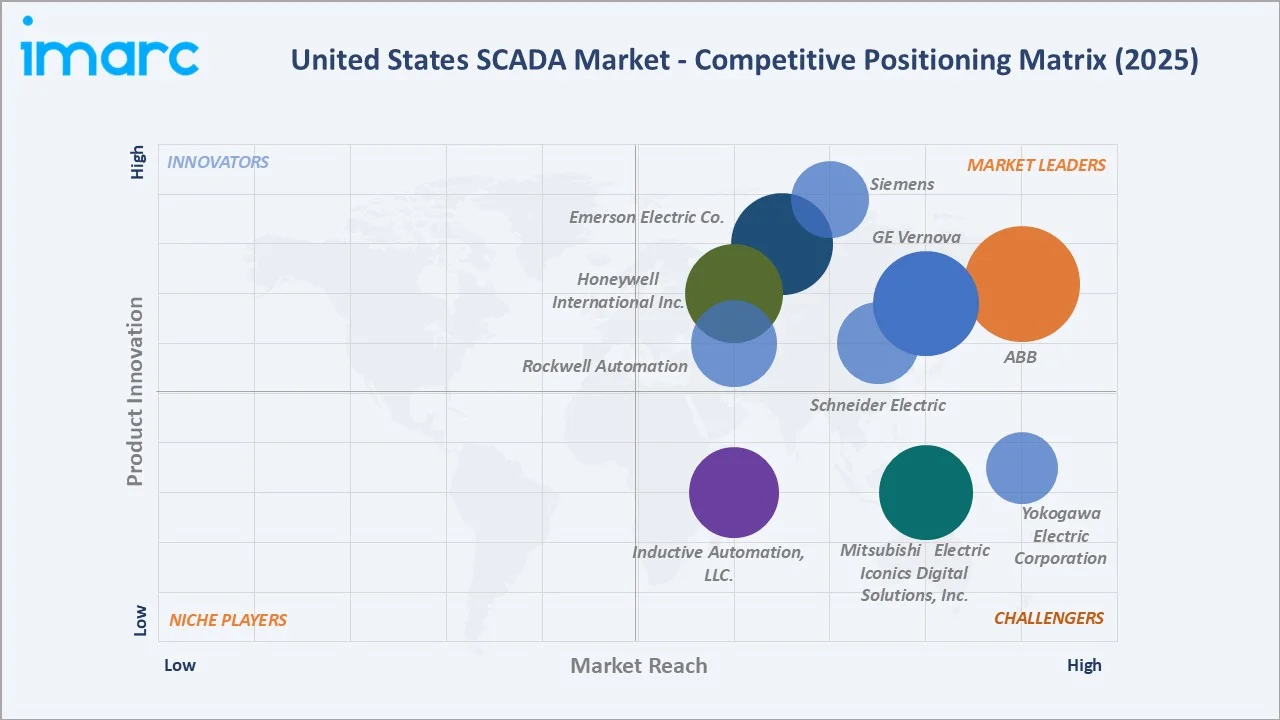

Competitive Landscape

The US SCADA market is moderately concentrated, with global automation leaders holding strong positions across major end-use verticals. Siemens, Schneider Electric, Honeywell, Rockwell Automation, and ABB collectively dominate the industrial automation and SCADA market, competing on technological breadth, cybersecurity capabilities, and sector-specific solutions.

|

Company Name |

Key Products |

Market Position |

Strategic Focus |

|

ABB |

Ability SCADAvantage, ABB Ability Symphony Plus SCADA, ABB Ability Symphony Plus for water and wastewater |

Leader |

Energy/utilities; digital twin; cloud SCADA |

|

Emerson Electric Co. |

DeltaV SaaS SCADA |

Leader |

Power & process industries; IIoT; managed services |

|

GE Vernova |

Proficy iFIX, Proficy Cimplicity |

Leader |

Grid SCADA; renewables; digital power management |

|

Honeywell International Inc. |

Experion SCADA, Experion Elevate, Experion HS, Experion PKS |

Leader |

Oil & gas; OT cybersecurity; cloud OT platform |

|

Mitsubishi Electric Iconics Digital Solutions, Inc. |

GENESIS Version 11, GENESIS64 |

Challenger |

Smart buildings; analytics; Azure integration |

|

Inductive Automation, LLC. |

Ignition SCADA Platform |

Challenger |

Cross-industry; open architecture; US manufacturing |

|

Rockwell Automation |

FactoryTalk View |

Leader |

Discrete manufacturing; OT/IT convergence; PLC SCADA |

|

Schneider Electric |

SCADAPack RTU, EcoStruxure Geo SCADA Expert, EcoStruxure RTU Operations Expert |

Leader |

Energy management; smart grid; cloud-native SCADA |

|

Siemens |

WinCC Unified PC, SIMATIC WinCC V8 |

Leader |

Process industries; IIoT; digital enterprise SCADA |

|

Yokogawa Electric Corporation |

FAST/TOOLS |

Challenger |

Oil & gas; refining; remote monitoring services |

Key players include ABB, Emerson Electric Co., GE Vernova, Honeywell International Inc., Mitsubishi Electric Iconics Digital Solutions, Inc., Inductive Automation, LLC., Rockwell Automation, Schneider Electric, Siemens, Yokogawa Electric Corporation, and others.

Key Company Profiles

Siemens

Siemens is a global technology leader with one of the broadest SCADA portfolios in the US market. Its SIMATIC WinCC and PCS 7 platforms serve process industries, utilities, and infrastructure operators, with its Insights Hub platform extending analytics capabilities to enterprise environments.

- Product Portfolio: WinCC SCADA, SIMATIC PCS 7

- Recent Developments: In March 2026, Siemens reaffirmed its commitment to strengthening industrial cybersecurity by validating TXOne Networks’ Stellar solution for compatibility with its SIMATIC WinCC Open Architecture (WinCC OA) platform. This validation ensures that trusted, high-performance security solutions can be seamlessly integrated into Siemens’ SCADA ecosystem. By approving Stellar, Siemens continues to expand its ecosystem of cybersecurity tools specifically suited for operational technology (OT) environments.

- Strategic Focus: Siemens leverages its global R&D scale and vertical domain expertise to compete as a full-stack industrial automation and SCADA provider in the US, with targeted investment in OT cybersecurity, digital twins, and cloud-native SCADA that address converging IT/OT infrastructure requirements.

Honeywell International Inc.

Honeywell is a major SCADA provider for US oil and gas, petrochemical, and industrial sectors. Its Experion PKS and Forge platforms combine traditional DCS/SCADA functionality with cloud-based OT monitoring, cybersecurity, and industrial AI analytics serving asset-intensive US industries.

- Product Portfolio: Experion PKS, Honeywell Forge, Connected Plant SCADA, Safety Manager

- Recent Developments: In July 2023, Honeywell announced its agreement to acquire SCADAfence as part of its strategy to strengthen its cybersecurity software portfolio, particularly in operational technology (OT) environments. Following the acquisition, SCADAfence’s solutions became part of Honeywell’s Forge Cybersecurity+ platform, enabling more comprehensive features such as improved visibility of assets, stronger threat monitoring, and better compliance management.

- Strategic Focus: Honeywell focuses on integrated OT cybersecurity and cloud SCADA convergence, leveraging its SCADAfence acquisition to provide end-to-end industrial security alongside its automation platform, targeting critical infrastructure operators with regulatory cybersecurity compliance requirements.

Rockwell Automation

Rockwell Automation is the leading US-headquartered SCADA and industrial automation provider with dominant market share in US discrete manufacturing. Its FactoryTalk View and PlantPAx platforms are deeply embedded in automotive, food and beverage, life sciences, and consumer goods manufacturing operations.

- Product Portfolio: FactoryTalk View, PlantPAx DCS/SCADA, Allen-Bradley PLCs, Plex MES platform

- Recent Developments: Rockwell strengthened its OT/IT convergence capabilities through the Plex Systems acquisition in September 2021, combining SCADA with cloud-based MES to provide connected manufacturing intelligence for US industrial customers.

- Strategic Focus: Rockwell focuses on OT/IT convergence in US manufacturing, combining its dominant Allen-Bradley PLC hardware base with FactoryTalk SCADA software and Plex cloud MES to create unified industrial intelligence competing against European automation majors in domestic manufacturing.

Market Concentration Analysis

The US SCADA market is moderately concentrated nationally, with the top five players collectively holding an estimated 50-60% of total market revenue. No single company holds more than 15-18% of US SCADA market revenue, reflecting significant competition across vertical market segments and geographies.

Vertical segment concentration is more advanced than national figures suggest. Rockwell Automation holds disproportionate share in US discrete manufacturing SCADA; Honeywell and Emerson dominate process industry DCS/SCADA; Schneider Electric and ABB lead power and energy utility SCADA applications across the country.

Investment & Growth Opportunities

Fastest-Growing Segments

Communication Systems and Services architectures at approximately 4.1% and 4.2% CAGR respectively through 2034 represent the highest-growth opportunity areas. Cloud SCADA services, OT cybersecurity monitoring subscriptions, and AI-powered analytics platforms are driving above-market growth, attracting significant venture and strategic investment.

Emerging Application Verticals

Grid-scale battery energy storage systems require specialized SCADA for charge/discharge cycle optimization, representing a rapidly emerging US market as utility-scale storage deployments accelerate under Inflation Reduction Act incentives. Agricultural SCADA for precision irrigation and monitoring is a nascent but growing application driven by water scarcity concerns.

Venture & Investment Trends

Private equity interest in consolidating fragmented US industrial software markets, including SCADA, is growing significantly. US cybersecurity investment firms targeting OT security convergence with SCADA represent a key trend, with notable acquisitions including Honeywell-SCADAfence. Federal funding creates large SCADA procurement opportunities across infrastructure sectors.

Future Market Outlook (2026-2034)

The US SCADA market is forecast to expand from USD 5.04 Billion in 2025 to an estimated USD 5.21 Billion in 2026 and reach USD 6.97 Billion by 2034 at a CAGR of 3.35%, adding USD 1.93 Billion in incremental annual market value. Sustained growth reflects infrastructure modernization, energy transition, and cybersecurity investment as structural demand drivers.

Three forces will shape the SCADA landscape through 2034. First, AI-autonomous SCADA enabling self-optimizing industrial processes will emerge by 2028-2030, transforming SCADA from a monitoring tool to an active production optimization platform. Second, quantum-resistant cryptography adoption will reshape SCADA cybersecurity architecture requirements. Third, digital twin integration will become standard in greenfield US industrial facility design.

Research Methodology

Primary Research

Primary research encompassed structured interviews with US SCADA industry stakeholders including senior SCADA architects, OT security managers, utility SCADA engineers, industrial automation procurement specialists, and trade association representatives at ISA, AWWA, and IEEE Power & Energy Society.

Secondary Research

Key secondary sources include US DOE energy infrastructure reports, NERC CIP compliance data, CISA industrial control system advisories, IEA energy investment reports, US Census Bureau manufacturing statistics, ISA-99 industrial cybersecurity standards, and trade media including Control Engineering and Power Magazine.

Forecasting Models

Market size estimations and growth projections were derived using top-down and bottom-up forecasting models incorporating GDP growth rates, US industrial production indices, energy transition investment forecasts, and historical SCADA market evolution patterns. Scenario analysis was performed to account for macroeconomic and policy uncertainty.

United States SCADA Market Report Coverage

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Programmable Logic Controller (PLC), Remote Terminal Units (RTU), Human Machine Interface (HMI), Communication Systems, Others |

| Architectures Covered | Hardware, Software, Services |

| End Users Covered | Oil and Gas, Power, Water and Wastewater, Manufacturing, Chemicals and Petrochemicals, Pharmaceutical, Others |

| Region Covered | Northeast, Midwest, South, West |

| Companies Covered | ABB, Emerson Electric Co., GE Vernova, Honeywell International Inc., Mitsubishi Electric Iconics Digital Solutions, Inc., Inductive Automation, LLC., Rockwell Automation, Schneider Electric, Siemens, Yokogawa Electric Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the United States SCADA Market Report

The United States SCADA market size is estimated at USD 5.21 Billion in 2026, reflecting consistent demand growth from industrial automation, energy sector modernization, and IIoT adoption across US industries.

The US SCADA market is projected to grow at a CAGR of 3.35% during 2026-2034, reaching USD 6.97 Billion by 2034, driven by smart grid investment, industrial automation, and cybersecurity regulatory requirements.

Programmable Logic Controllers (PLC) dominate the component segment with a 28.6% share in 2025. PLCs are foundational automation controllers providing real-time industrial process control across manufacturing, energy, and utility applications.

Services architecture leads with 36.8% share in 2025, reflecting growing enterprise outsourcing of SCADA integration, maintenance, cybersecurity, and cloud migration. Hardware follows at 34.2%, and Software accounts for 29.0% of the market.

The South leads with 32.1% share in 2025, driven by the concentration of oil and gas infrastructure in Texas and Louisiana including refineries, LNG export terminals, offshore platforms, and extensive pipeline networks requiring SCADA monitoring.

Key drivers include accelerating industrial automation and Industry 4.0 adoption, US smart grid modernization and renewable energy integration, stringent cybersecurity regulations (NERC-CIP, CISA), IIoT proliferation, and federal infrastructure investment under the Bipartisan Infrastructure Law and CHIPS Act.

Key players include ABB, Emerson Electric Co., GE Vernova, Honeywell International Inc., Mitsubishi Electric Iconics Digital Solutions, Inc., Inductive Automation, LLC., Rockwell Automation, Schneider Electric, Siemens, Yokogawa Electric Corporation, and others.

Key challenges include proliferating cybersecurity threats to connected OT networks, high initial capital investment requirements, complexity of integrating modern SCADA with legacy industrial control systems, and persistent shortage of professionals with combined OT and IT cybersecurity expertise.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade