United States Smart Grid Security Market Size, Share, Trends and Forecast by Component, Subsystem, Deployment Type, Security Type, and Region, 2026-2034

United States Smart Grid Security Market Size, Share, Trends & Forecast (2026-2034)

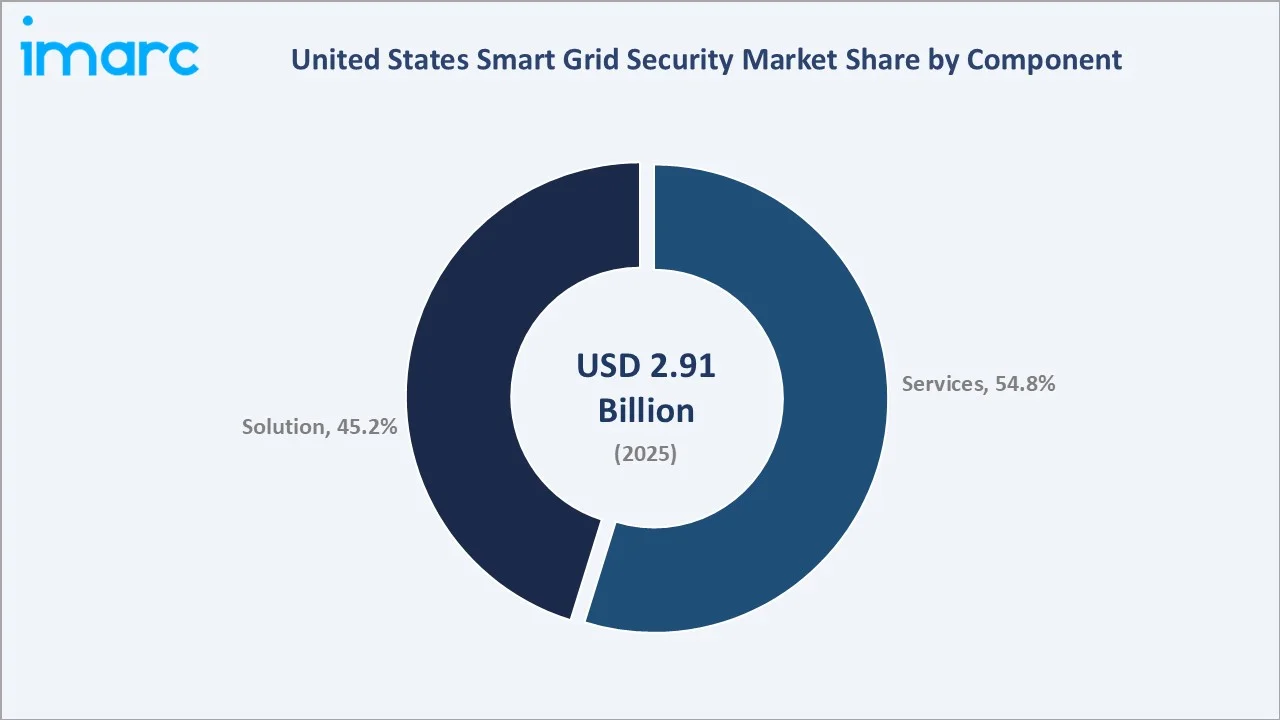

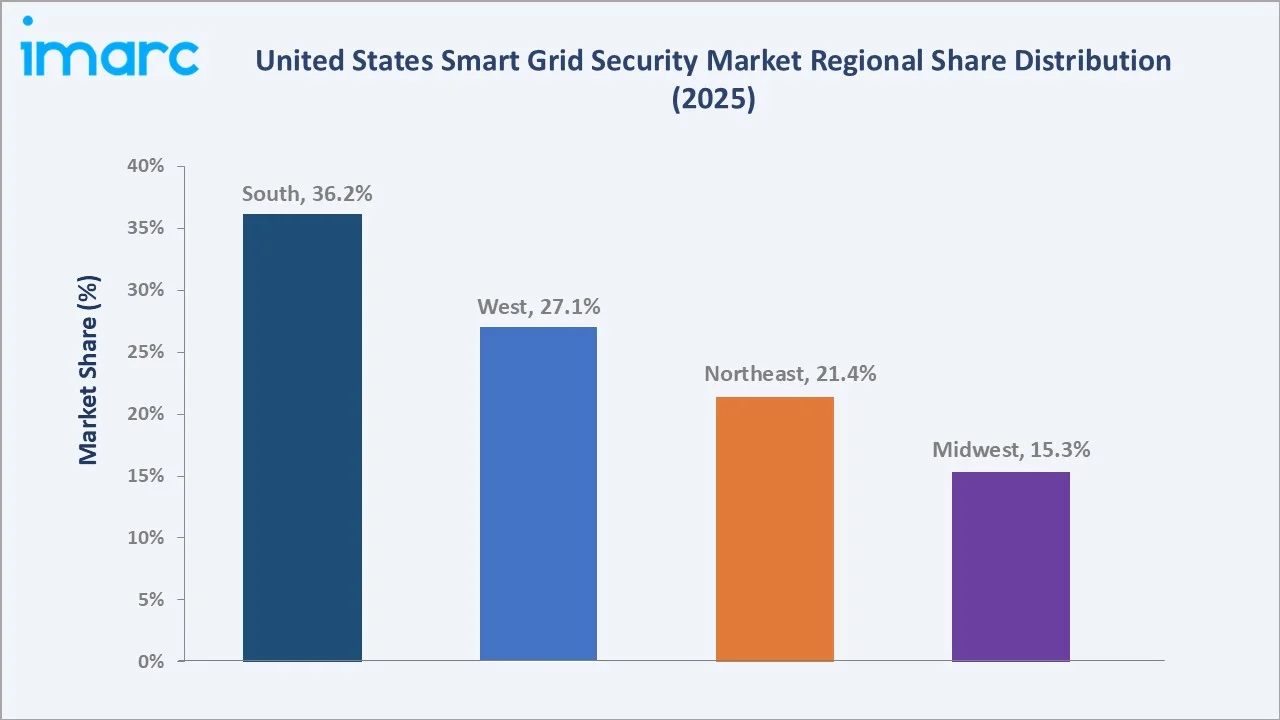

The United States smart grid security market reached USD 2.91 Billion in 2025 and is projected to reach USD 5.57 Billion by 2034, growing at a CAGR of 7.49% during 2026-2034. The market is driven by rising cyber threats targeting power utilities, increasing smart meter and IoT grid deployments, and the growing need to protect critical energy infrastructure. Reuters reported that cyberattacks on U.S. utilities rose by nearly 70% in 2024, increasing from 689 incidents in the previous year to 1,162 incidents. This sharp rise is driving the market by pushing utilities to invest in advanced cybersecurity, threat detection, grid monitoring, and resilience solutions to protect critical power infrastructure. Services lead component at 54.8%. On-premise leads deployment type at 58.3%. The South region leads at 36.2%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2.91 Billion |

|

Forecast Market Size (2034) |

USD 5.57 Billion |

|

CAGR (2026-2034) |

7.49% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Component |

Services (54.8%, 2025) |

|

Dominant Deployment Type |

On-premise (58.3%, 2025) |

|

Leading Region |

South (36.2%, 2025) |

The US smart grid security market grew from USD 2.03 Billion in 2020 to USD 2.91 Billion in 2025, reflecting steady adoption of cybersecurity solutions across utilities. It is projected to reach USD 4.18 Billion by 2030 and USD 5.57 Billion by 2034. Growth is supported by rising cyberattacks on power infrastructure, expanding smart grid deployments, and increasing regulatory focus on grid resilience.

.webp)

To get more information on this market, Request Sample

Cloud-based deployment grows fastest at ~8.8% CAGR through cloud SIEM-as-a-Service, security analytics SaaS for grid OT monitoring, and hybrid cloud-OT integration. Services grow at ~7.8% CAGR through managed security service provider (MSSP), grid SOC and OT incident response service.

.webp)

Executive Summary

The United States smart grid security market is expanding steadily, supported by rising cyberattacks on utilities and the growing digitalization of power infrastructure. The market is projected to grow from USD 2.91 Billion in 2025 to USD 5.57 Billion by 2034. Increasing smart meter, IoT, and grid automation deployments are strengthening demand for advanced cybersecurity solutions. Regulatory focus on critical infrastructure protection and grid resilience is further driving market adoption. Services at 54.8% leads through MSSP grid SOC and OT security consulting. On-premise at 58.3% reflects the data sovereignty requirement. The South region leads at 36.2%.

Key Market Insights

|

Insight |

Data |

|

Dominant Component |

Services - 54.8% share (2025) |

|

Dominant Deployment Type |

On-premise - 58.3% market share (2025) |

|

Leading Region |

South - 36.2% share (2025) |

|

Market Opportunity |

Zero Trust OT grid architecture; AI-powered anomaly detection for SCADA/DCS; smart meter endpoint security; EV charging grid security; quantum-resistant encryption for grid communication |

Key Analytical Observations Supporting the Above Data:

- Services at 54.8%: The services segment dominates as utilities require continuous consulting, monitoring, integration, maintenance, and incident response support. Growing cyber threats and complex grid systems are increasing reliance on managed security and professional services.

- On-premise at 58.3%: The on-premise segment dominates as utilities prefer direct control over critical grid data, systems, and security infrastructure. High compliance requirements, legacy grid assets, and concerns over cloud-based exposure further support on-premise deployment.

- South Region at 36.2%: The South region dominates due to its large utility base, expanding power demand, and growing smart grid modernization projects. Rising cyber-risk exposure across energy infrastructure and strong investment in grid resilience further support regional leadership.

United States Smart Grid Security Market Overview

The US smart grid security market operates within the broader US critical infrastructure protection ecosystem as the most regulated and most-invested critical infrastructure security sector. The market's commercial uniqueness lies in its role in protecting critical national energy infrastructure from increasingly sophisticated cyber threats. Unlike traditional IT security markets, smart grid security requires specialized solutions that secure both operational technology (OT) and information technology (IT) environments. The market also benefits from recurring revenue through managed security services, compliance monitoring, threat intelligence, and continuous system upgrades. Growing grid digitalization further strengthens long-term demand for advanced cybersecurity solutions.

.webp)

The US smart grid security ecosystem integrates OT/IT cybersecurity vendors, utilities and grid operators, regulatory framework, national laboratory partners, and technology vendors. Macroeconomic factors include rising US electricity demand, increasing grid modernization spending, and growing investment in critical infrastructure protection.

Market Dynamics

.webp)

To evaluate market opportunities, Request Sample

Market Drivers

- Rising Cyberattacks on US Utilities: Reuters reported that cyberattacks against US utilities rose sharply in 2024, increasing by nearly 70% from 689 incidents in the previous year to 1,162 incidents. These rising cyberattacks on US utilities are a major driver, as power companies face increasing threats from ransomware, malware, and nation-state cyber activities. The growing frequency and sophistication of attacks are pushing utilities to strengthen cybersecurity across transmission, distribution, and smart meter networks. Utilities are investing in advanced threat detection, network monitoring, identity management, and incident response solutions to protect critical infrastructure. This heightened focus on grid resilience and operational continuity is accelerating demand for smart grid security technologies.

- Expanding Smart Grid and Smart Meter Deployments: Expanding smart grid and smart meter deployments, increasing the number of connected devices across utility networks. As grids become more digital and data-driven, cyberattack entry points also expand. Utilities are therefore investing in encryption, identity access management, endpoint protection, and real-time monitoring. This growing need to secure smart meters, sensors, substations, and communication networks is boosting demand for smart grid security solutions.

- Growing Grid Modernization: The US electric grid is a major engineering achievement, comprising more than 9,200 power-generating units with over 1 million megawatts of capacity, connected through more than 600,000 miles of transmission lines. Growing grid modernization is driving as utilities upgrade aging power infrastructure with digital sensors, automation, and connected control systems. These upgrades improve efficiency but also increase cyber exposure across grid operations. As a result, utilities are investing in OT security, network monitoring, access control, and threat detection. Rising modernization spending is therefore creating sustained demand for advanced smart grid security solutions.

Market Restraints

- Legacy OT System Integration Complexity: Legacy OT system integration complexity hampers the market because many utilities still operate aging substations, SCADA systems, and control devices not designed for modern cybersecurity tools. Integrating advanced security solutions with these legacy assets can be costly, technically difficult, and operationally risky. Utilities must avoid service disruptions while upgrading protection across critical grid infrastructure. This slows deployment timelines and increases implementation costs for smart grid security solutions.

- Budget Constraints at Smaller Municipal and Cooperative Utilities: Budget constraints at smaller municipal and cooperative utilities hamper market growth because these organizations often have limited capital for advanced cybersecurity upgrades. High costs for security platforms, skilled personnel, monitoring tools, and compliance programs can delay adoption. As a result, many smaller utilities prioritize basic grid operations over large-scale security modernization. This creates uneven cybersecurity readiness across the U.S. smart grid ecosystem.

Market Opportunities

- Zero Trust OT Architecture for Grid: Zero trust OT architecture for grid applies continuous verification and least-privilege access principles across operational technology environments. As cyber threats targeting substations, SCADA systems, and grid control networks become more sophisticated, utilities are increasingly adopting Zero Trust frameworks to reduce attack surfaces. These architectures improve visibility, access control, and threat containment across distributed grid assets. Growing regulatory focus on critical infrastructure protection is expected to accelerate investment in Zero Trust-based smart grid security solutions.

- AI-Powered OT Anomaly Detection: AI-powered OT anomaly detection enables real-time identification of unusual behavior across substations, SCADA systems, smart meters, and grid control networks. AI and machine learning algorithms can detect cyber threats, equipment malfunctions, and operational abnormalities that traditional rule-based systems may miss. This improves threat response times, grid reliability, and operational efficiency. As utilities generate increasing volumes of grid data, demand for AI-driven security analytics and predictive monitoring solutions is expected to grow significantly.

Market Challenges

- Data Privacy and Access Control Risks: Data privacy and access control risks challenge the market as smart meters, sensors, and grid systems collect large volumes of sensitive utility and customer data. Unauthorized access can expose consumption patterns, operational controls, and critical infrastructure information. Utilities must invest in encryption, identity management, and strict access controls, increasing cost and complexity. These risks can slow digital grid adoption, especially among smaller utilities with limited cybersecurity resources.

- Securing Large-Scale Smart Meter and IoT Networks: Securing large-scale smart meter and IoT networks is challenging because each connected device can become a potential cyberattack entry point. Utilities must protect millions of endpoints, communication channels, and data flows across distributed grid systems. Managing device authentication, firmware updates, encryption, and real-time monitoring increases operational complexity. This creates higher cybersecurity costs and implementation challenges for utilities.

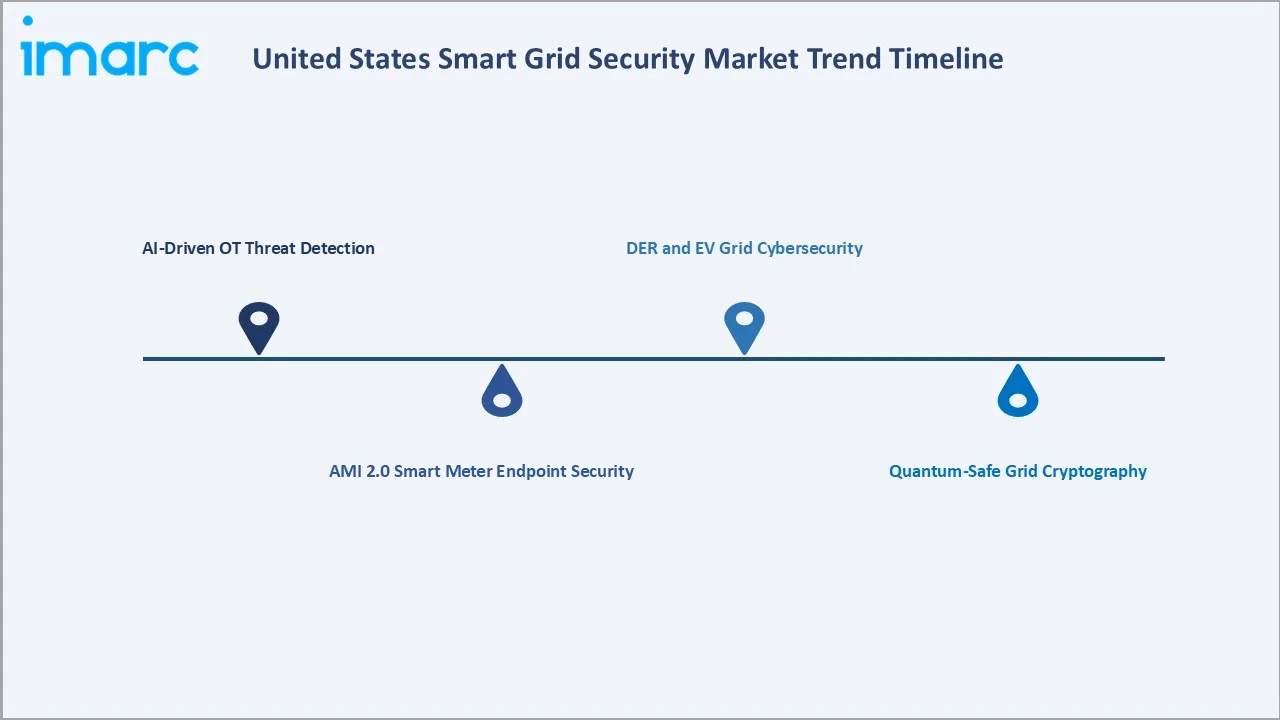

Emerging Market Trends

1. AI-Driven OT Threat Detection

AI-driven OT threat detection is emerging as utilities need faster identification of cyber risks across substations, SCADA systems, smart meters, and grid control networks. AI tools can analyze large volumes of operational data to detect abnormal behavior, malware activity, and unauthorized access in real time. This improves incident response, reduces downtime, and strengthens grid resilience. Growing grid digitalization and rising cyberattack sophistication are accelerating the adoption of AI-based OT security platforms.

2. AMI 2.0 Smart Meter Endpoint Security

AMI 2.0 smart meter endpoint security is emerging as utilities deploy more advanced, connected meters with two-way communication capabilities. Nearly 120 million smart meters have been installed across the US to serve up to 145 million customers. These meters increase grid visibility but also expand the cyberattack surface at the endpoint level. Utilities are adopting stronger device authentication, encryption, firmware protection, and real-time monitoring to secure meter networks. This trend is supporting demand for specialized endpoint security solutions across the US smart grid ecosystem.

3. DER and EV Grid Cybersecurity

DER and EV grid cybersecurity is emerging as distributed energy resources, rooftop solar, battery storage, and EV chargers become increasingly connected to the grid. These assets create new cyber entry points across distribution networks and demand-response systems. Utilities are adopting secure communication protocols, device authentication, real-time monitoring, and threat detection to protect grid stability. This trend is driving demand for specialized cybersecurity solutions for decentralized energy infrastructure.

4. Quantum-Safe Grid Cryptography

Quantum-safe grid cryptography is emerging as utilities prepare for future risks from quantum computing that could weaken traditional encryption methods. Smart grids rely on secure communications between substations, smart meters, DER assets, and control centers, making encryption resilience critical. Utilities and technology providers are exploring post-quantum cryptography to protect long-life grid infrastructure. This trend is creating opportunities for next-generation secure communication and identity-management solutions.

Industry Value Chain Analysis

The US smart grid security value chain integrates cybersecurity research & technology development, security product & platform development, system integration & regulatory compliance, utility deployment & infrastructure integration, security operations & incident response, and grid resilience, monitoring & recovery.

|

Stage |

Key Participants |

|

Cybersecurity Research & Technology Development |

Cybersecurity vendors, research institutions, government agencies, OT/IT security specialists, and threat intelligence providers |

|

Security Product & Platform Development |

Firewall vendors, endpoint security providers, identity and access management companies, encryption technology providers, and OT security software developers |

|

System Integration & Regulatory Compliance |

System integrators, cybersecurity consultants, compliance specialists, utility technology partners, and certification bodies |

|

Utility Deployment & Infrastructure Integration |

Electric utilities, transmission operators, distribution companies, smart meter providers, and grid automation vendors |

|

Security Operations & Incident Response |

Security Operations Centers (SOCs), managed security service providers, incident response teams, threat monitoring providers |

|

Grid Resilience, Monitoring & Recovery |

Utility operators, grid control centers, disaster recovery providers, infrastructure resilience teams, and government and regulatory agencies |

Security product & platform development is the most value-added stage in the United States smart grid security value chain. This stage creates proprietary cybersecurity solutions such as OT security platforms, threat detection systems, encryption technologies, and identity management tools that generate high software and subscription-based margins. Continuous innovation and recurring licensing revenues make it the most commercially attractive segment.

Technology Landscape in the United States Smart Grid Security Industry

OT-Native Threat Detection Platforms

OT-native threat detection platforms provide cybersecurity solutions specifically designed for operational technology environments such as SCADA systems, substations, and industrial control networks. These platforms continuously monitor grid operations to detect abnormal behavior, cyber intrusions, and equipment anomalies in real time. Unlike traditional IT security tools, they understand industrial protocols and operational processes, improving threat visibility and response. Growing utility investments in grid resilience and OT security are accelerating the adoption of these specialized platforms.

Grid Fault Detection and Localization Platforms

Grid fault detection and localization platforms enable utilities to identify the exact location and timing of faults across distribution networks. In June 2026, Electrical Grid Monitoring announced its patented Accurate Fault Location and Detection solution, designed to identify both the timing and location of distribution-grid faults within a single pole-span distance. The company states that this capability could cut U.S. customer outage durations from 3–5 hours to nearly one hour and reduce utility crew-time costs significantly. These platforms improve grid visibility, reduce outage duration, and support faster crew dispatch. By integrating sensors, analytics, and OT monitoring, they also help detect abnormal grid behavior and potential cyber-physical risks. This strengthens grid resilience and supports the move toward self-healing power networks.

Network Segmentation and Secure Communication Technologies

Network segmentation and secure communication technologies isolate critical grid assets, such as substations, SCADA systems, and control centers, from potential cyber threats. These technologies reduce lateral movement opportunities for attackers and limit the impact of security breaches. Secure communication protocols, encryption, and authenticated data exchanges help protect information flowing across smart meters, sensors, and grid networks. Their growing adoption is strengthening grid resilience, regulatory compliance, and protection of critical energy infrastructure.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Component |

Services |

54.8% |

2025 |

|

Subsystem |

Supervisory Control and Data Acquisition (SCADA)/ Industrial Control System (ICS) |

🔒 |

2025 |

|

Deployment Type |

On-premise |

58.3% |

2025 |

|

Security Type |

Network Security |

🔒 |

2025 |

|

Region |

South |

36.2% |

2025 |

By Component

Services lead at 54.8% (2025), as utilities require continuous support for cybersecurity consulting, system integration, monitoring, compliance, and incident response. Growing cyber threats and complex OT/IT grid environments increase reliance on managed and professional security services.

To access detailed market analysis, Request Sample

Solution at 45.2% encompasses OT security platforms, network security, SIEM, endpoint security, and vulnerability management.

By Deployment Type

On-premise leads at 58.3% (2025), because utilities prefer direct control over critical operational technology (OT) systems, grid data, and security infrastructure. On-premise deployments offer greater visibility, customization, and protection for mission-critical assets such as SCADA systems and substations.

.webp)

Cloud-based at 41.7% grows fastest at ~8.8% CAGR, by enabling utilities to scale cybersecurity monitoring, analytics, and threat intelligence more efficiently. It reduces upfront infrastructure costs and supports faster updates across distributed grid assets. Growing adoption of remote monitoring, AI-based security tools, and managed security services is further increasing cloud-based deployment demand.

Regional Market Insights

|

Region |

Share (2025) |

Key US Smart Grid Security Market Drivers & Characteristics |

|

South |

36.2% |

Supported by its large utility base, extensive transmission and distribution infrastructure, and ongoing grid modernization programs. |

|

West |

27.1% |

Driven by high adoption of renewable energy, distributed energy resources (DERs), smart meters, and advanced grid technologies. |

|

Northeast |

21.4% |

Reflecting a strong regulatory focus on critical infrastructure protection, advanced utility cybersecurity programs, and significant investments in grid resilience. |

|

Midwest |

15.3% |

Supported by ongoing utility modernization efforts, growing deployment of smart grid technologies, and increasing focus on protecting operational technology (OT) environments. |

The South leads the US smart grid security market with a 36.2% share, supported by its large utility base, extensive grid infrastructure, and modernization programs. The West follows with 27.1%, driven by renewable energy integration, DERs, smart meters, and digital grid adoption.

The Northeast holds 21.4%, supported by a strong regulatory focus and advanced cybersecurity programs. The Midwest accounts for 15.3%, driven by utility upgrades, smart grid deployment, and rising OT security needs.

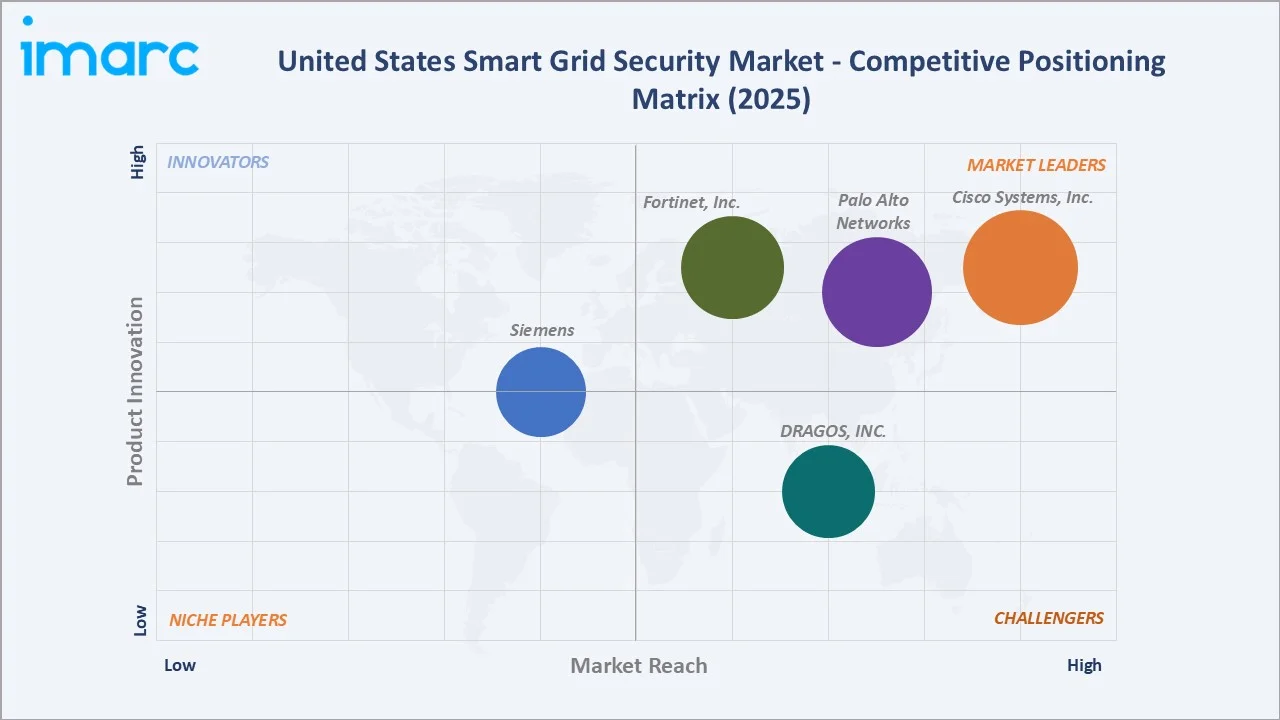

Competitive Landscape

The United States smart grid security market is moderately concentrated. Competition is focused on OT security, threat detection, network segmentation, identity management, and real-time grid monitoring solutions. Market participants are investing in AI-driven cybersecurity, Zero Trust architectures, and cloud-enabled security platforms to address evolving cyber threats. Strategic partnerships with utilities, acquisitions, and product innovation remain key competitive strategies. Growing grid modernization, renewable energy integration, and regulatory compliance requirements continue to drive technological differentiation and market expansion.

|

Company |

Key Solutions |

Market Position |

Core Strength |

|

Cisco Systems, Inc. |

Cisco Secure Malware Analytics (Threat Grid) |

Market Leader |

Cisco Systems, Inc. plays a foundational role in US smart grid security by providing secure, scalable, and intelligent communication architectures. |

|

Palo Alto Networks |

VM-Series, Palo Alto Networks Next-Generation Firewalls (NGFWs) |

Market Leader |

Palo Alto Networks plays a critical role in U.S. smart grid security by securing the convergence of IT and Operational Technology (OT) for electric utilities. |

|

Fortinet, Inc. |

Ruggedised Next-Generation Firewall, Ethernet Switching, Wireless LAN (WLAN), FortiGuard OT Security |

Market Leader |

Fortinet, Inc. plays a critical role in U.S. smart grid security by providing a comprehensive, AI-driven security framework that secures operational technology (OT) and IT infrastructure. |

|

DRAGOS, INC. |

The Dragos Platform |

Strong Challenger |

Dragos, Inc. is a leading provider of cybersecurity for Industrial Control Systems (ICS) and Operational Technology (OT), playing a critical role in securing the U.S. smart grid by providing specialized threat intelligence, asset visibility, and vulnerability management. |

|

Siemens |

SIPROTEC 5, SIPROTEC Compact, SICAM Substation Automation, SICAM RTUs, SICAM Power Quality |

Established Player |

Siemens is a major player in US smart grid security, providing comprehensive, "defense-in-depth" cybersecurity for utility substations, DERs, and control systems. |

The US smart grid security competitive landscape is evolving through zero trust OT adoption, AI-enhanced OT detection premium, and platform consolidation.

Key Company Profiles

Cisco Systems, Inc.

Cisco Systems, Inc. is a leading participant in the United States smart grid security market, providing a broad portfolio of networking, cybersecurity, and industrial security solutions for utility operators and critical infrastructure providers. The company offers secure networking, threat detection, identity and access management, network segmentation, and OT security technologies designed to protect smart grids, substations, and utility communication networks.

- Key Solutions: Cisco Secure Malware Analytics (Threat Grid).

- Recent Developments: In March 2026, Cisco introduced the Cisco AI Grid with NVIDIA reference design, combining Cisco’s Mobility Services Platform with NVIDIA RTX PRO Blackwell Series GPUs. The solution enables service providers to use existing networks to deliver managed edge AI services with carrier-grade reliability and data sovereignty.

- Strategic Focus: Strengthening cybersecurity across utility IT and operational technology (OT) environments through secure networking, Zero Trust architectures, and industrial cybersecurity solutions.

Palo Alto Networks

Palo Alto Networks, Inc. is a leading cybersecurity provider in the United States smart grid security market, offering advanced solutions to protect utility networks, operational technology (OT) environments, and critical energy infrastructure.

- Key Solutions: VM-Series, Palo Alto Networks Next-Generation Firewalls (NGFWs).

- Recent Developments: In March 2026, Palo Alto Networks launched Next-Generation Trust Security (NGTS), introducing a new approach to operational resilience. As the industry shifts toward a 47-day certificate renewal cycle, NGTS automates cryptographic trust management, reducing manual errors, preventing service disruptions, and improving operational efficiency.

- Strategic Focus: Protecting utility operational technology (OT) and IT environments through AI-driven cybersecurity, Zero Trust frameworks, and real-time threat intelligence.

Market Concentration Analysis

The United States smart grid security market is moderately concentrated, with a mix of global cybersecurity leaders, industrial automation companies, and specialized OT security providers competing for market share. Major players benefit from strong technology portfolios and established relationships with utilities. High barriers to entry, including regulatory compliance requirements, critical infrastructure expertise, and advanced cybersecurity capabilities, limit new competition. The market is increasingly driven by innovation in AI-powered threat detection, Zero Trust architectures, OT security platforms, and cloud-based monitoring solutions. Strategic partnerships, acquisitions, and utility-focused cybersecurity offerings remain key competitive differentiators.

Investment & Growth Opportunities

Highest Growth Segments

Cloud-based deployment (~8.8% CAGR), services (~7.8% CAGR), AI-powered OT detection (~12-15% CAGR from smaller sub-segment), Zero Trust OT architecture (~10-12% CAGR), DER and EV grid cybersecurity (~15-18% CAGR), and AMI 2.0 endpoint security (~10-12% CAGR through second-generation smart meter security) represent US smart grid security highest-growth investment vectors through 2034.

Investment Themes

- Zero Trust OT architecture for utility grid: This is an investment theme as utilities are moving toward continuous verification, least-privilege access, and network segmentation across SCADA, substations, and control systems. Rising cyberattacks and regulatory pressure are increasing demand for Zero Trust solutions that protect critical grid assets and limit breach impact.

- DER and EV grid cybersecurity for renewable integration and V2G security: This theme is gaining traction as solar, battery storage, EV chargers, and vehicle-to-grid systems create new digital entry points for cyber threats. Securing these distributed assets supports renewable integration, grid stability, and safe two-way power/data flows, creating opportunities for specialized cybersecurity platforms.

Future Market Outlook (2026-2034)

The United States smart grid security market is projected to grow from USD 2.91 Billion in 2025 to USD 5.57 Billion by 2034, delivering a 7.49% CAGR over the forecast period through regulatory expansion, grid modernization, nation-state OT threat escalation, and zero trust OT architecture adoption. The market's anchor value of USD 4.18 Billion in 2030 represents the US smart grid security market at an architectural transformation.

Three structural forces define US smart grid security growth through 2034. First, the rapid expansion of smart grids, smart meters, and connected utility infrastructure is increasing cybersecurity requirements across the power sector. Second, rising cyber threats targeting critical energy infrastructure are driving sustained investment in OT security, threat detection, and grid resilience solutions. Third, growing renewable energy integration, distributed energy resources (DERs), and electric vehicle networks are expanding the attack surface, creating demand for advanced security technologies to protect increasingly decentralized grids.

Research Methodology

Primary Research

Primary research comprised interviews with utility executives, grid operators, cybersecurity professionals, OT security specialists, technology vendors, and industry consultants. These discussions provided insights into cybersecurity investment priorities, smart grid deployment trends, threat landscapes, and regulatory requirements. Feedback from market participants was also used to validate market sizing, competitive dynamics, and future growth opportunities in the United States smart grid security market.

Secondary Research

Secondary research encompassed the review of utility reports, government publications, regulatory guidelines, cybersecurity frameworks, company filings, and industry databases. It also included analysis of smart grid deployment trends, cyberattack statistics, grid modernization programs, and technology developments. These sources helped validate market trends, competitive landscape, and growth opportunities in the United States smart grid security market.

Forecasting Models

US smart grid security market revenue forecasts were developed using a utility cybersecurity expenditure model: US electric utility cybersecurity spend per MW of generation capacity multiplied by US electric generation capacity and grid modernization investment CAGR correlation coefficient.

United States Smart Grid Security Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered |

|

| Subsystems Covered | Demand Response System, Supervisory Control and Data Acquisition (SCADA)/ Industrial Control System (ICS), Home Energy Management System, Advanced Metering Infrastructure, Others |

| Deployment Types Covered | Cloud-based, On-premise |

| Security Types Covered | Endpoint Security, Application Security, Database Security, Network Security, Others |

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered | Cisco Systems, Inc., Palo Alto Networks, Fortinet, Inc., DRAGOS, INC., Siemens, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the United States Smart Grid Security Market Report

The United States smart grid security market reached USD 2.91 Billion in 2025, driven by rising cyberattacks on utilities, expanding smart meter and IoT grid deployments, and growing grid modernization investments. Increasing integration of renewable energy, DERs, and EV charging infrastructure is expanding the grid attack surface. Strong regulatory focus on critical infrastructure protection is further accelerating demand for OT security, threat detection, and managed cybersecurity services.

The US smart grid security market grows at 7.49% CAGR during 2026-2034, reaching USD 5.57 Billion by 2034. The CAGR reflects regulatory expansion, nation-state OT threat escalation, and grid modernization.

Services lead at 54.8% as utilities need continuous cybersecurity consulting, system integration, compliance support, monitoring, and incident response. Growing OT/IT complexity and rising cyber threats increase dependence on managed and professional security services. Recurring maintenance, threat intelligence, and security upgrades further support service demand.

On-premise leads at 58.3% as utilities prefer direct control over critical grid assets, OT systems, and sensitive operational data. It supports stronger customization, compliance management, and protection of legacy SCADA and substation infrastructure. Cybersecurity concerns and strict reliability requirements further strengthen on-premise adoption.

The South leads at 36.2% due to its large utility base, extensive transmission and distribution infrastructure, and rising electricity demand. Ongoing grid modernization, smart meter deployment, and severe weather resilience programs are increasing cybersecurity investments. Strong growth in renewables, DERs, and EV infrastructure further supports regional demand for smart grid security solutions.

Leading companies include Cisco Systems, Inc., Palo Alto Networks, Fortinet, Inc., DRAGOS, INC., and Siemens, among others.

The market is projected to reach approximately USD 4.18 Billion by 2030, reflecting steady growth in utility cybersecurity spending. This expansion will be driven by smart grid modernization, rising cyber threats, and broader deployment of smart meters, DERs, and EV charging networks. Growing regulatory focus on grid resilience will further support demand for advanced security solutions.

Three priority investment opportunities: Zero trust OT architecture for utility SCADA, AI-enhanced OT SOC for MSSP grid managed detection and response, and DER and EV grid cybersecurity.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade