United States Solid Oxide Fuel Cell Market Size, Share, Trends and Forecast by Application, End User, and Region, 2026-2034

United States Solid Oxide Fuel Cell Market Size, Share, Trends & Forecast (2026-2034)

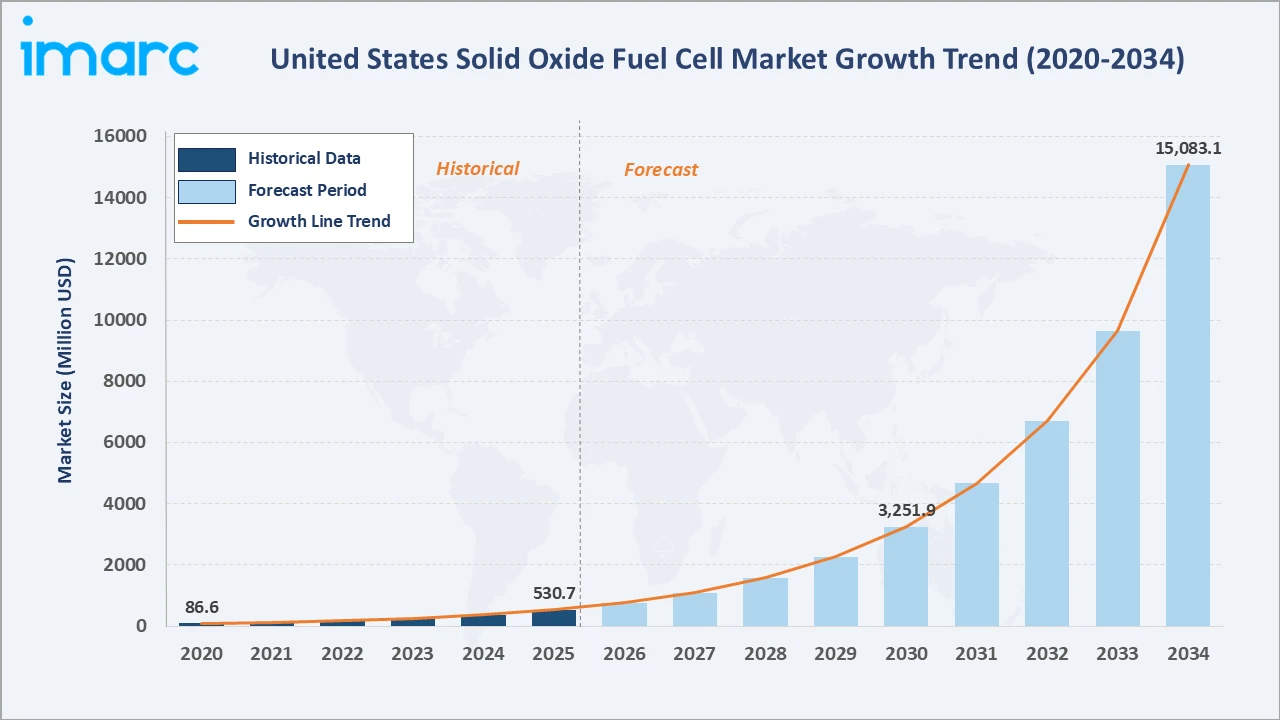

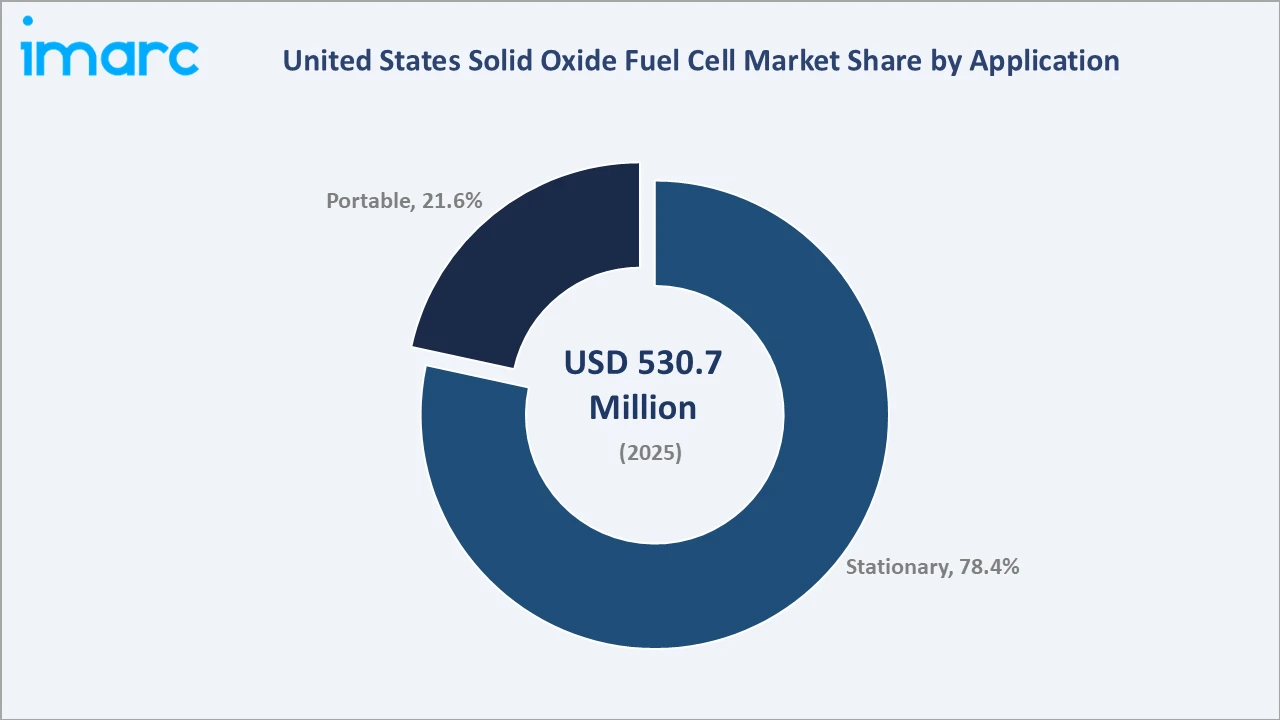

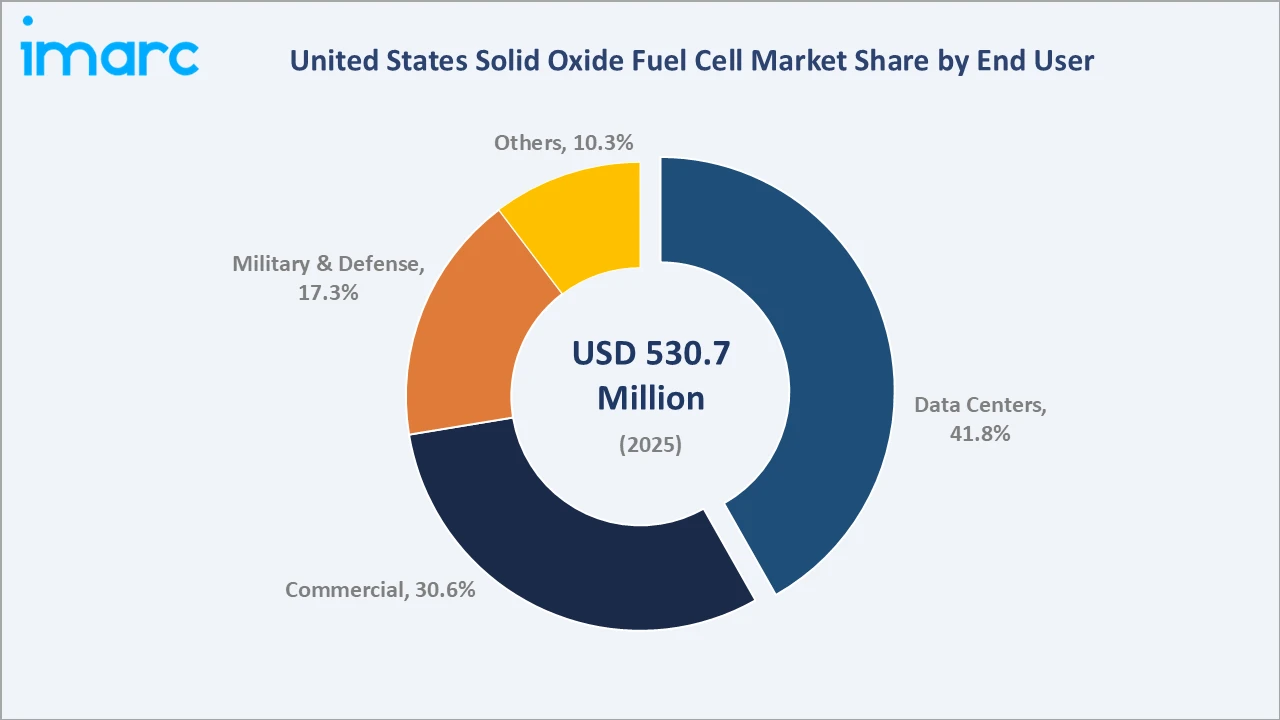

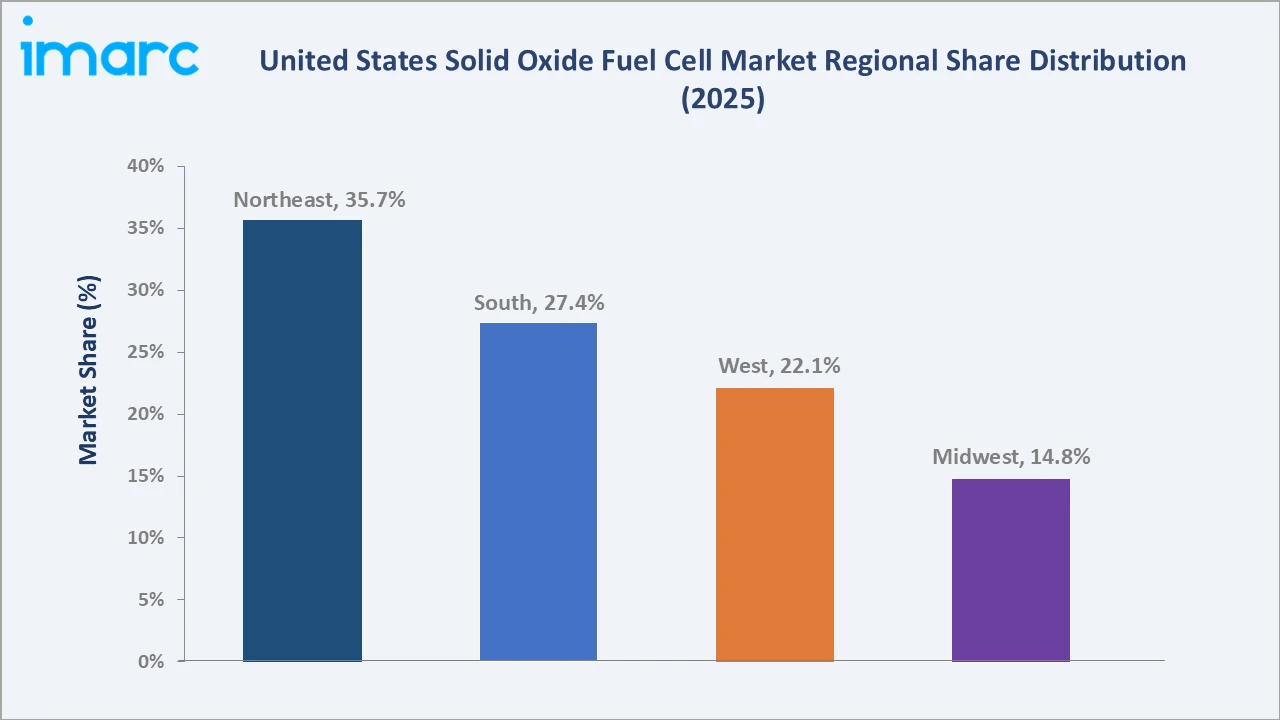

The United States solid oxide fuel cell market reached USD 530.7 Million in 2025 and is projected to reach USD 15,083.1 Million by 2034, growing at an exceptional CAGR of 43.70% during 2026-2034. The market is driven by rising demand for high-efficiency, low-emission power generation, growing deployment of distributed energy systems, and increasing investments in hydrogen infrastructure and clean energy technologies. The US has developed a large renewable energy base, with land-based wind, offshore wind, and utility-scale solar capacity sufficient to supply nearly 79 million homes, while utility-scale storage can support around 19 million additional homes during peak demand hours. This expanding clean energy ecosystem, backed by more than USD 743 Billion in capital investment across all 50 states, is driving demand for reliable, efficient, and low-emission power solutions. Stationary leads application at 78.4%. Data centers lead the end user at 41.8%. Northeast leads regionally at 35.7%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 530.7 Million |

|

Forecast Market Size (2034) |

USD 15,083.1 Million |

|

CAGR (2026-2034) |

43.70% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Application |

Stationary (78.4%, 2025) |

|

Dominant End User |

Data Centers (41.8%, 2025) |

|

Leading Region |

Northeast (35.7%, 2025) |

The United States solid oxide fuel cell (SOFC) market is witnessing rapid expansion, growing from USD 86.6 Million in 2020 to USD 530.7 Million in 2025. This growth reflects increasing adoption of high-efficiency, low-emission fuel cell systems across distributed power, data centers, and industrial applications. The market is expected to accelerate sharply to USD 3,251.9 Million by 2030, supported by clean energy incentives, hydrogen infrastructure development, and decarbonization goals. By 2034, it is forecast to reach USD 15,083.1 Million, indicating strong commercialization potential and wider deployment across stationary power and backup energy systems.

To get more information on this market, Request Sample

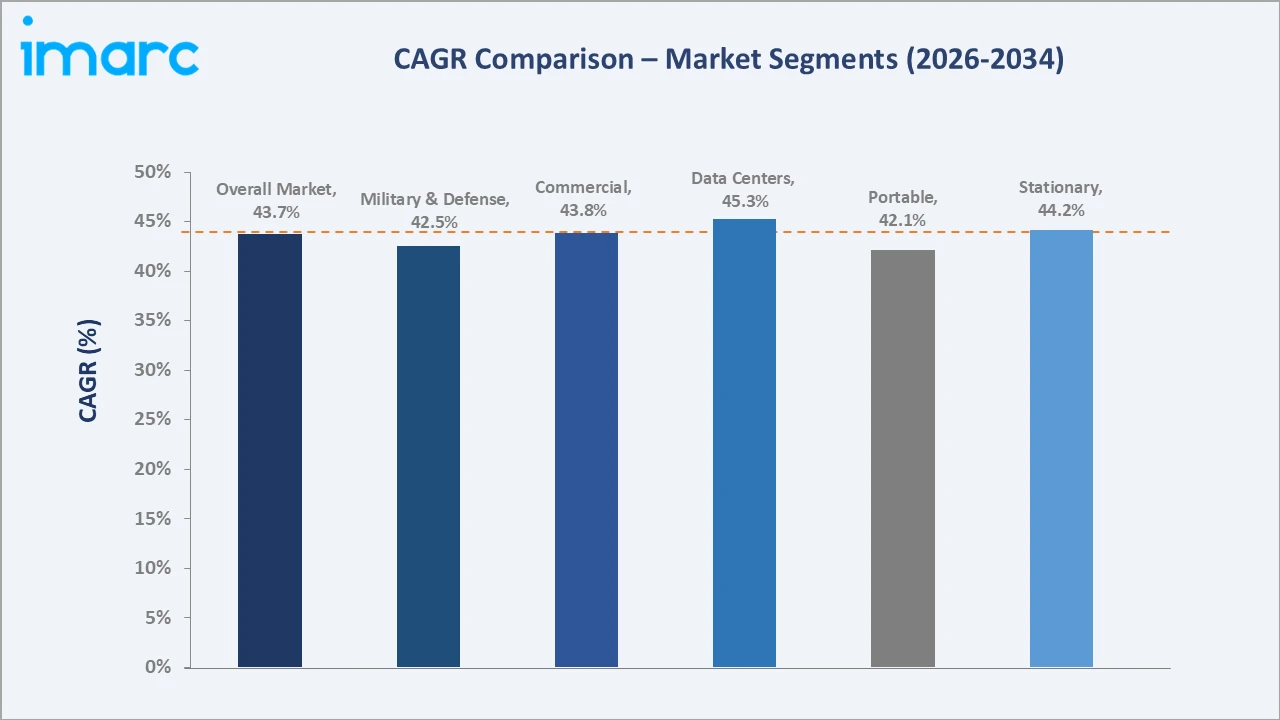

Stationary grows fastest at ~44.2% CAGR through AI hyperscale data center SOFC baseload and commercial CHP net-zero. Data centers grow at ~45.3% CAGR through AI GPU clusters with 24/7 zero-carbon power.

Executive Summary

The United States solid oxide fuel cell market is entering a high-growth phase, supported by rising demand for clean, efficient, and resilient power generation. Strong renewable energy additions, grid modernization needs, and expanding utility-scale storage capacity are creating opportunities for SOFC deployment in distributed and backup power applications. Growing investments in hydrogen infrastructure and decarbonization technologies are further strengthening the market outlook. SOFC systems are gaining preference due to their high efficiency, fuel flexibility, and ability to provide reliable power with lower emissions. Increasing adoption across data centers, industrial facilities, commercial buildings, and microgrids is expected to accelerate market expansion. By 2034, the market is positioned to become a key part of the US clean energy and distributed power ecosystem. Stationary at 78.4% leads through data center and commercial CHP. Data centers at 41.8% lead through Bloom Energy, Google, Microsoft, AT&T, and SOFC. Northeast leads regionally at 35.7%.

Key Market Insights

|

Insight |

Data |

|

Dominant Application |

Stationary - 78.4% share (2025) |

|

Dominant End User |

Data Centers - 41.8% market share (2025) |

|

Leading Region |

Northeast - 35.7% share (2025) |

|

Market Opportunity |

AI hyperscale data center zero-carbon SOFC baseload; commercial CHP net-zero building 2030; Bloom Energy Server 5th gen; utility-scale SOFC grid peaker |

Key Analytical Observations Supporting The Above Data:

- Stationary at 78.4%: The stationary segment dominates due to its widespread adoption for continuous on-site power generation, combined heat and power (CHP), backup power, and microgrid applications. Its high electrical efficiency, fuel flexibility, and ability to deliver reliable, low-emission electricity make it the preferred choice for commercial, industrial, utility, and data center installations.

- Data Centers at 41.8%: Data centers dominate due to their increasing need for uninterrupted, high-efficiency, and low-carbon power to support rapidly growing digital infrastructure. SOFC systems provide reliable baseload and backup electricity with high efficiency and low emissions, making them well suited for hyperscale and enterprise data center operations.

- Northeast at 35.7%: The Northeast dominates due to strong demand for resilient, low-emission distributed power across data centers, commercial buildings, healthcare facilities, and industrial sites. Supportive clean energy policies, grid reliability concerns, and high electricity costs further encourage SOFC adoption in the region.

United States Solid Oxide Fuel Cell Market Overview

The United States solid oxide fuel cell market encompasses stationary, portable, and transport-based SOFC systems used for clean and efficient power generation. It includes applications across data centers, commercial buildings, industrial facilities, utilities, microgrids, and backup power systems. The market covers fuel-flexible systems operating on natural gas, hydrogen, biogas, and other low-carbon fuels. It also includes components such as fuel cell stacks, balance-of-plant systems, power conditioning units, and related service infrastructure. Growing demand for resilient distributed energy, low-emission electricity, and hydrogen-ready technologies is expanding the market scope. The market further supports decarbonization efforts by enabling high-efficiency power generation with reduced environmental impact. Macroeconomic factors include rising US electricity demand, growing clean energy investments, and increasing capital spending on data centers, industrial facilities, and grid modernization.

Market Dynamics

To evaluate market opportunities, Request Sample

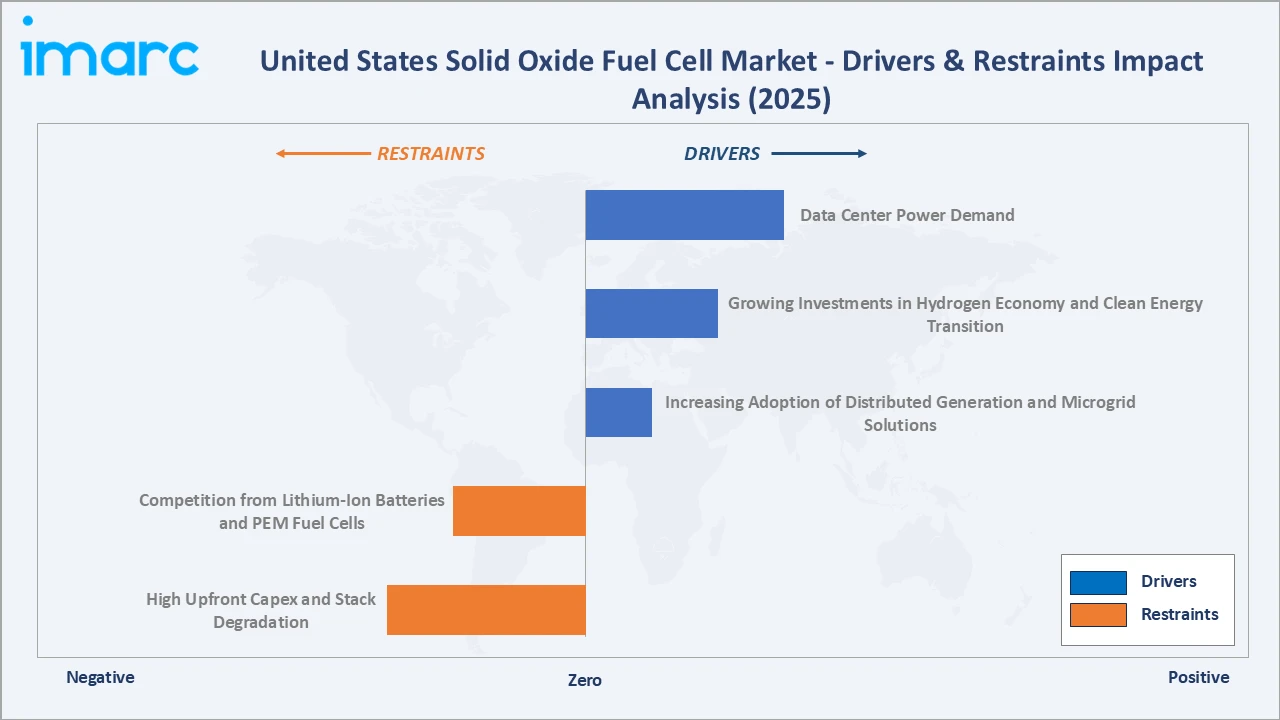

Market Drivers

- Data Center Power Demand: AI data centers in the US consumed around 312.6 terawatt-hours of electricity in 2025, equivalent to the annual power use of nearly 29 million average households. This massive electricity requirement highlights the scale of AI-driven digital infrastructure and its growing pressure on the power grid. SOFC systems offer reliable on-site power generation, reducing dependence on stressed grids and improving energy resilience. Their high efficiency and lower emissions make them suitable for data centers aiming to meet sustainability and decarbonization targets. Rising electricity consumption from digital infrastructure is therefore encouraging wider SOFC adoption for baseload, backup, and distributed power applications.

- Growing Investments in Hydrogen Economy and Clean Energy Transition: Growing investments in the hydrogen economy and clean energy transition are creating stronger demand for hydrogen-ready and low-emission power technologies. SOFC systems can operate on hydrogen, natural gas, biogas, and other fuels, making them suitable for the gradual shift toward cleaner energy sources. The US Department of Energy’s Hydrogen Shot initiative aims to reduce the cost of clean hydrogen to USD 1 per kilogram by 2031 through technology innovation, scale-up, and cost reduction efforts. As industries and utilities pursue decarbonization, SOFCs are gaining traction for efficient distributed generation, backup power, and combined heat and power applications.

- Increasing Adoption of Distributed Generation and Microgrid Solutions: Increasing adoption of distributed generation and microgrid solutions is driving the market as businesses seek reliable, on-site power with reduced dependence on centralized grids. SOFC systems are well suited for microgrids due to their high efficiency, fuel flexibility, and ability to provide continuous baseload electricity. Rising grid congestion, outage risks, and resilience needs are encouraging commercial, industrial, and utility users to deploy localized power systems. This is expanding SOFC use across data centers, campuses, hospitals, military facilities, and remote infrastructure.

Market Restraints

- High Upfront Capex and Stack Degradation: High upfront CAPEX and stack degradation increase the total cost of ownership and slow large-scale commercial adoption. SOFC systems require advanced ceramic materials, precision manufacturing, and complex balance-of-plant components, making installation costs relatively high. Stack degradation caused by high operating temperatures can reduce long-term performance and increase replacement or maintenance needs. These factors make buyers cautious, especially when comparing SOFCs with batteries, gas generators, and other fuel cell technologies.

- Competition from Lithium-Ion Batteries and PEM Fuel Cells: Competition from lithium-ion batteries and PEM fuel cells offers end users more mature, faster-deployable, and widely commercialized alternatives. Lithium-ion batteries are preferred for short-duration energy storage and fast-response backup power, while PEM fuel cells offer lower-temperature operation and quicker start-up. These technologies often have stronger supply chains, broader vendor availability, and greater customer familiarity. As a result, SOFC adoption can be delayed in applications where cost, response time, and proven deployment history are key purchasing factors.

Market Opportunities

- Integration with Green Hydrogen Production and Storage Ecosystems: Integration with green hydrogen production and storage ecosystems enables cleaner and more flexible power generation. SOFC systems can operate on hydrogen, making them well suited for future hydrogen hubs, renewable-powered electrolysis projects, and long-duration energy storage networks. The US industrial clean hydrogen demand is projected at 3.8–14.9 Mt/year by 2050, potentially cutting 28–133 MtCO₂e. Producing this green hydrogen could require up to 682 TWh of low-carbon electricity, equal to nearly 90% of current renewable generation. As green hydrogen availability improves, SOFCs can support low-carbon baseload power, backup power, and microgrid applications.

- Increasing Demand for Resilient Power in Remote and Off-Grid Locations: Increasing demand for resilient power in remote and off-grid locations supports dependable electricity supply where grid access is weak or unavailable. SOFC systems can provide continuous, high-efficiency power for remote industrial sites, telecom towers, military bases, and rural facilities. Their fuel flexibility allows operation on natural gas, hydrogen, biogas, or other available fuels. This makes SOFCs attractive for critical operations requiring low-emission, long-duration, and stable power without heavy reliance on diesel generators.

Market Challenges

- Achieving Long-Term Durability Under High Operating Temperatures: Achieving long-term durability under high operating temperatures is challenging as SOFC stacks typically operate in demanding thermal conditions. Prolonged exposure to high temperatures can cause material stress, thermal cycling damage, electrode degradation, and seal failures. These issues may reduce system efficiency, shorten stack life, and increase maintenance or replacement costs. As a result, manufacturers must improve materials, stack design, and thermal management to ensure reliable long-duration performance.

- Meeting Stringent Performance and Safety Standards: Meeting stringent performance and safety standards is challenging as systems must prove reliability, efficiency, emissions performance, and safe operation under high-temperature conditions. Compliance requires extensive testing, certification, and validation, which can increase development costs and delay commercialization. SOFC systems also need to meet grid interconnection, fuel handling, thermal safety, and building-code requirements. These complex approvals can slow deployment, especially for large-scale commercial, industrial, and data center applications.

Emerging Market Trends

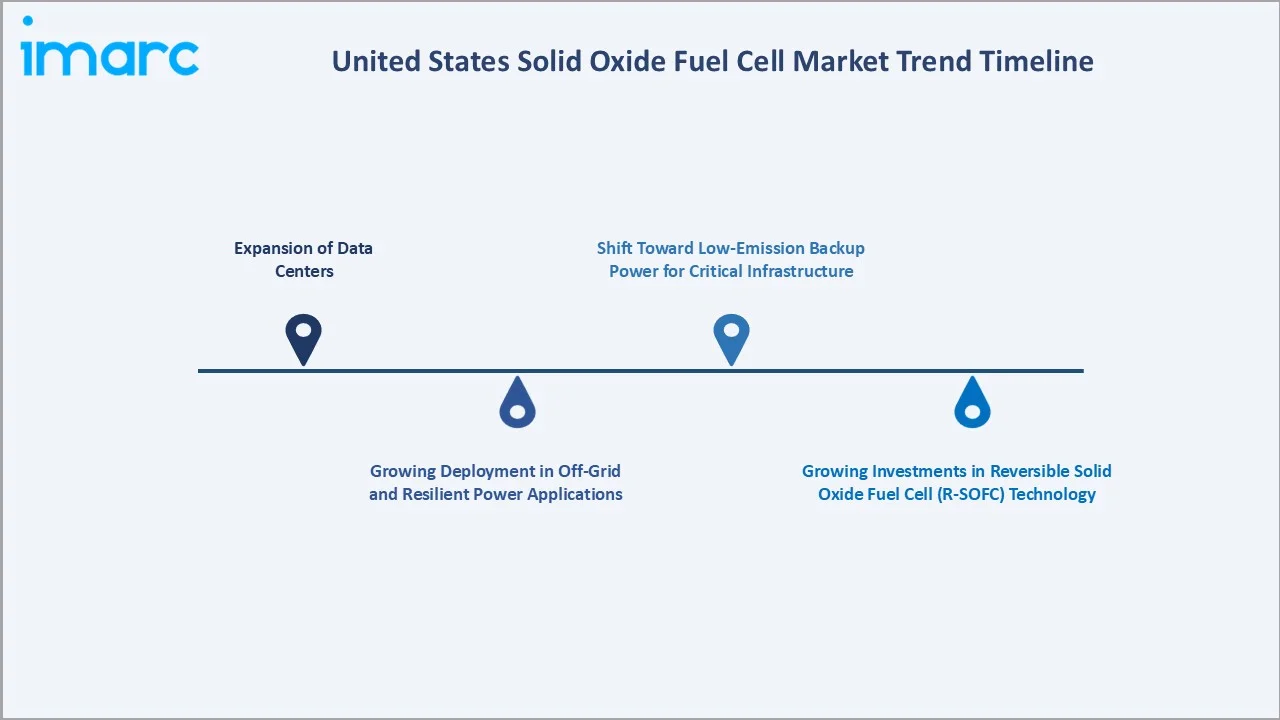

1. Expansion of Data Centers

The United States hosts more than 4,500 active data centers as of June 2026, with Virginia leading with over 665 facilities. Texas follows with 413 data centers, ahead of California, Illinois, and Ohio. In addition, more than 700 new data centers are under construction across 38 states. Expansion of data centers is emerging as AI, cloud computing, and digital services rapidly increase electricity demand. Data center operators are seeking reliable, on-site, and low-emission power sources to reduce grid dependence and avoid downtime. SOFC systems support this need by providing continuous baseload and backup power with high efficiency. Their ability to integrate with natural gas, biogas, or hydrogen also aligns with data centers’ long-term sustainability goals.

2. Growing Deployment in Off-Grid and Resilient Power Applications

Growing deployment in off-grid and resilient power applications is emerging as users seek reliable electricity beyond centralized grid systems. SOFCs are increasingly being considered for remote industrial sites, military bases, telecom infrastructure, hospitals, and disaster-resilient facilities. Their ability to provide continuous, fuel-flexible, and low-emission power makes them attractive alternatives to diesel generators. This trend is further supported by rising concerns over grid outages, extreme weather events, and the need for dependable backup power.

3. Growing Investments in Reversible Solid Oxide Fuel Cell (R-SOFC) Technology

Growing investments in reversible solid oxide fuel cell (R-SOFC) technology are emerging as these systems can support both power generation and hydrogen production. R-SOFCs enable electricity-to-hydrogen and hydrogen-to-electricity conversion, making them valuable for renewable energy storage and grid balancing. In September 2024, the US DOE’s Office of Fossil Energy and Carbon Management announced up to USD 4 Million in federal funding to improve the availability and affordability of clean hydrogen for power generation, industrial decarbonization, and transportation. The funding will support R&D projects focused on expanding solid oxide fuel cell technology, particularly reversible solid oxide fuel cell (R-SOFC) systems. This trend is expanding SOFC applications across green hydrogen, microgrids, CHP, and long-duration energy storage.

4. Shift Toward Low-Emission Backup Power for Critical Infrastructure

Shift toward low-emission backup power for critical infrastructure is emerging as facilities seek cleaner alternatives to diesel generators. SOFC systems can provide reliable backup and continuous power for data centers, hospitals, telecom networks, military sites, and emergency services. Their high efficiency and lower emissions support resilience without compromising sustainability targets. This trend is gaining momentum as grid outages, extreme weather risks, and decarbonization goals increase demand for dependable clean backup power.

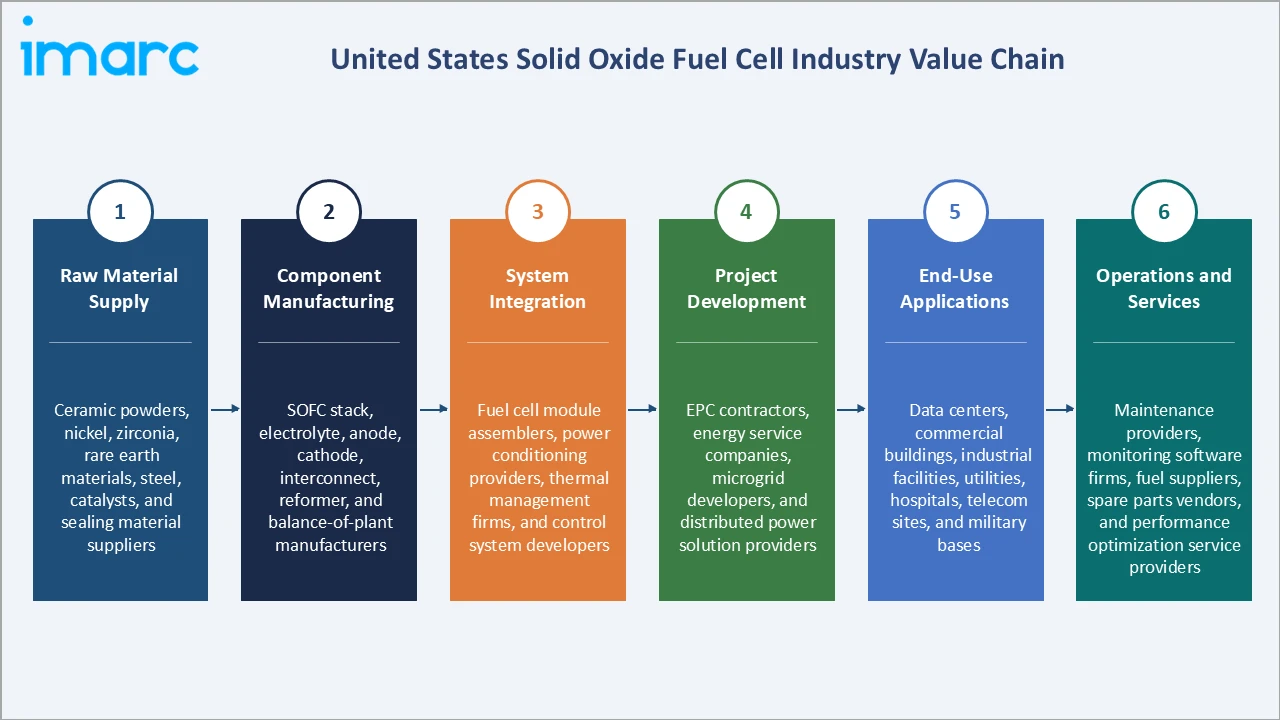

Industry Value Chain Analysis

The United States solid oxide fuel cell value chain integrates raw material supply, component manufacturing, system integration, project development, end-use applications, and operations and services.

|

Stage |

Key Participants |

|

Raw Material Supply |

Ceramic powders, nickel, zirconia, rare earth materials, steel, catalysts, and sealing material suppliers |

|

Component Manufacturing |

SOFC stack, electrolyte, anode, cathode, interconnect, reformer, and balance-of-plant manufacturers |

|

System Integration |

Fuel cell module assemblers, power conditioning providers, thermal management firms, and control system developers |

|

Project Development |

EPC contractors, energy service companies, microgrid developers, and distributed power solution providers |

|

End-Use Applications |

Data centers, commercial buildings, industrial facilities, utilities, hospitals, telecom sites, and military bases |

|

Operations and Services |

Maintenance providers, monitoring software firms, fuel suppliers, spare parts vendors, and performance optimization service providers |

System integration represents the most value-added stage in the United States solid oxide fuel cell value chain. This stage involves the design and integration of high-performance fuel cell stacks, power electronics, thermal management systems, and control software, which largely determine system efficiency, durability, and reliability. It requires significant R&D, advanced manufacturing capabilities, and engineering expertise, enabling manufacturers to differentiate their products and capture the highest margins within the value chain.

Technology Landscape in the United States Solid Oxide Fuel Cell Industry

SOFC Stack Technology

SOFC stack technology is improving system efficiency, durability, and power density. Advancements in ceramic electrolytes, electrode materials, and interconnect designs are extending stack lifespan while reducing performance degradation. In April 2026, Ceres introduced Ceres Endura, a solid oxide stack platform designed to support growing demand for resilient, efficient, on-site power in data centers and other energy-intensive sectors. The platform enables partners to serve both power and hydrogen markets through a shared production base. These innovations are expanding the use of SOFCs across data centers, microgrids, industrial facilities, and distributed power systems.

Fuel Flexibility and Hydrogen Technology

Fuel flexibility and hydrogen technology enable systems to operate on natural gas, biogas, syngas, and hydrogen. This flexibility supports near-term deployment using existing fuels while preparing systems for a low-carbon hydrogen future. Advances in hydrogen-ready stacks, fuel reforming, and reversible SOFC technologies are expanding use cases in power generation, storage, and industrial decarbonization. As hydrogen infrastructure develops, SOFCs are becoming increasingly relevant for clean, resilient, and distributed energy applications.

Planar Solid Oxide Fuel Cell (Planar SOFC) Technology

Compared with tubular designs, planar SOFCs offer lower electrical resistance and easier stack integration, making them suitable for commercial, industrial, and data center applications. Ongoing advancements in ceramic materials, interconnects, and sealing technologies are improving durability and reducing production costs. These developments are accelerating the commercialization of high-performance SOFC systems for distributed and clean energy generation.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Application |

Stationary |

78.4% |

2025 |

|

End User |

Data Centers |

41.8% |

2025 |

|

Region |

Northeast |

35.7% |

2025 |

By Application

Stationary leads at 78.4% (2025) due to their strong use in continuous on-site power generation, backup power, and combined heat and power applications. They are widely adopted across data centers, commercial buildings, industrial facilities, hospitals, and microgrids where reliable electricity is critical. Their high efficiency, fuel flexibility, and low-emission performance make them suitable for long-duration power supply. Rising demand for resilient distributed energy and grid-independent power further strengthens the dominance of the stationary segment.

To access detailed market analysis, Request Sample

Portable at 21.6% reflects military manpack SOFC, portable field generator, and vehicle auxiliary power unit APU SOFC. Portable grows at ~42.1% CAGR through the DoD portable SOFC and remote power applications.

By End User

Data centers lead at 41.8% (2025) due to rising demand for uninterrupted, high-efficiency, and low-emission on-site power. Rapid growth in AI, cloud computing, and hyperscale facilities is increasing electricity needs and grid pressure. SOFC systems support data centers by providing reliable baseload and backup power with lower emissions.

Commercial at 30.6% reflects strong adoption of SOFC systems in commercial buildings, office complexes, hotels, healthcare facilities, and educational campuses seeking reliable, efficient, and low-emission on-site power. Military and defense at 17.3% driven by the need for resilient, silent, and fuel-flexible power systems for military bases, command centers, and mission-critical infrastructure with enhanced energy security. Others at 10.3% include telecom towers, wastewater treatment plants, transportation infrastructure, research facilities, and remote off-grid installations using SOFCs for dependable distributed power generation.

Regional Market Insights

|

Region |

Share (2025) |

Key US SOFC Market Drivers & Characteristics |

|

Northeast |

35.7% |

Reflecting strong demand from data centers, healthcare facilities, universities, and commercial buildings. High electricity prices, ambitious decarbonization goals, and investments in distributed energy systems continue to support the regional growth. |

|

West |

27.4% |

Reflecting widespread adoption driven by clean energy policies, hydrogen initiatives, and advanced technology ecosystems. |

|

South |

22.1% |

Reflecting increasing deployment across industrial facilities, manufacturing plants, and rapidly expanding data centers. |

|

Midwest |

14.8% |

Reflecting steady demand from industrial CHP applications, utilities, and critical infrastructure. |

Northeast's 35.7% dominance is supported by a high concentration of data centers, healthcare facilities, universities, and commercial buildings that require reliable, low-emission distributed power solutions. West's 27.4% follows with strong adoption driven by clean energy policies, hydrogen initiatives, and investments in microgrids and renewable energy integration.

South's 22.1% is experiencing rapid growth due to expanding manufacturing activity, hyperscale data center development, and abundant natural gas infrastructure supporting distributed generation. Midwest's 14.8% maintains steady demand from industrial facilities and combined heat and power (CHP) applications, benefiting from its strong manufacturing base and increasing focus on energy resilience.

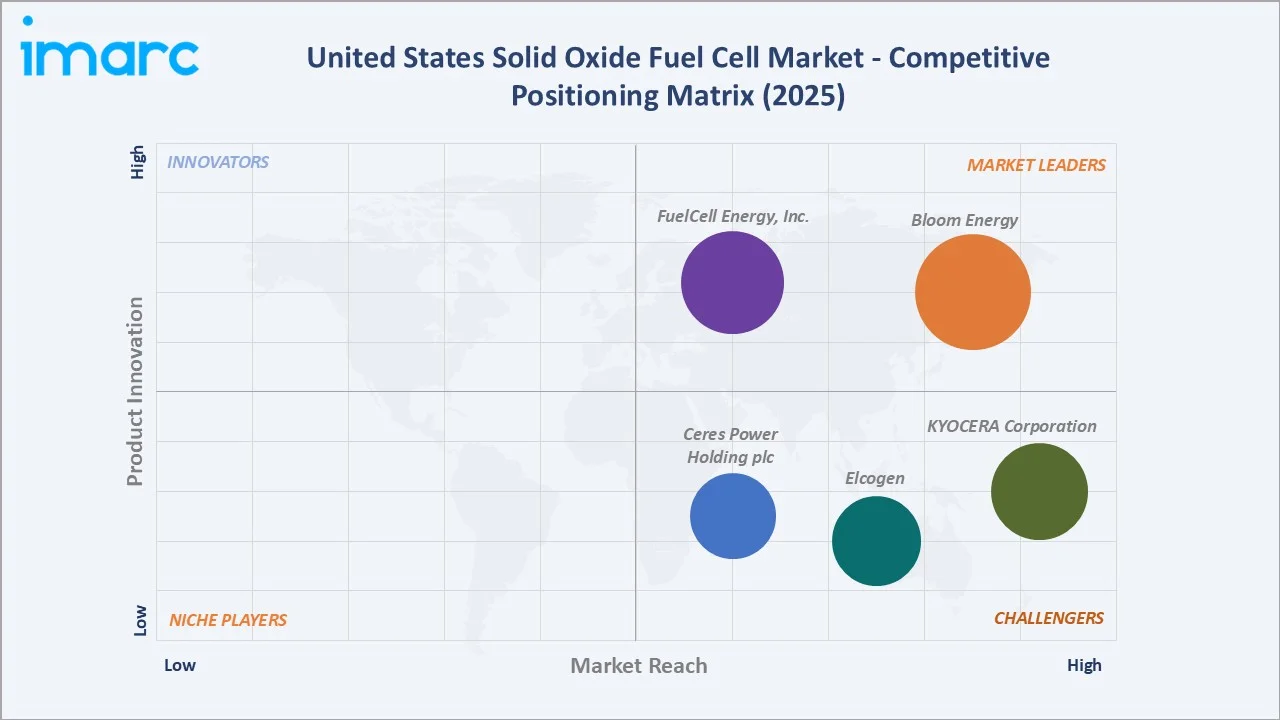

Competitive Landscape

The United States solid oxide fuel cell market is moderately competitive, with companies focusing on stack efficiency, fuel flexibility, durability, and system scalability. Key players are investing in hydrogen-ready and reversible SOFC technologies to expand applications across data centers, microgrids, CHP, and industrial power.

|

Company |

Key Products |

Market Position |

Core Strength |

|

Bloom Energy |

Bloom Energy Server |

Market Leader |

Bloom Energy is a dominant player in the United States Solid Oxide Fuel Cell (SOFC) industry, supplying highly efficient, combustion-free distributed power generation to commercial and industrial sectors. Their Energy Servers convert natural gas, biogas, or hydrogen into electricity on-site, bypassing the central grid to ensure reliability and reduce emissions. |

|

FuelCell Energy, Inc. |

FuelCell Energy’s Solid Oxide Electrolyzer Cell (SOEC) |

Market Leader |

FuelCell Energy, Inc. plays a critical, two-fold role in the United States solid oxide market: high-efficiency power generation and zero-carbon hydrogen production. |

|

Ceres Power Holding plc |

Ceres Endura |

Strong Challenger |

Ceres Power Holdings plc drives US Solid Oxide Fuel Cell (SOFC) and electrolysis markets through an asset-light, technology-licensing model. Rather than manufacturing directly, Ceres licenses its proprietary Ceres Endura steel-supported cell technology to strategic partners who build and commercialize the hardware. |

|

KYOCERA Corporation |

SOFC (Solid Oxide Fuel Cell) Stack |

Strong Challenger |

KYOCERA Corporation’s role in the US solid oxide fuel cell (SOFC) market centers on component supply and strategic clean-energy manufacturing. While their complete residential and commercial SOFC cogeneration systems are primarily commercialized in Japan, they are key players in the US clean energy sector through the mass production of the foundational SOFC cell stacks. |

|

Elcogen |

elcoCell, elcoStack, elcoModule |

Strong Challenger |

Elcogen operates as a core component manufacturer, supplying Solid Oxide Fuel Cell (SOFC) and electrolyser components to third-party system integrators globally, rather than selling finished systems directly. While historically centered in Europe, their technology is indirectly utilized in the US through international partnerships and integrations. |

Partnerships, licensing agreements, and government-backed R&D programs are shaping technology commercialization. Firms are also targeting lower system costs, faster installation, and improved lifecycle performance. Competition is expected to intensify as demand rises for resilient, low-emission on-site power solutions.

Key Company Profiles

Bloom Energy

Bloom Energy is one of the leading companies in the United States solid oxide fuel cell (SOFC) market, specializing in high-efficiency, solid oxide fuel cell-based distributed power generation systems. The company's Bloom Energy Server platform provides reliable, on-site electricity for data centers, commercial buildings, healthcare facilities, manufacturers, utilities, and other critical infrastructure. Bloom Energy is also expanding its portfolio with hydrogen-ready SOFC systems, electrolyzers for clean hydrogen production, and carbon capture-enabled technologies.

- Key Products: Bloom Energy Server.

- Recent Developments: In August 2024, Bloom Energy offered its Bloom Energy Server power solution with around 60% electrical efficiency when operating on 100% hydrogen. This efficiency milestone was achieved by Bloom engineers at the company’s R&D facility in Fremont, California.

- Strategic Focus: Focuses on expanding high-efficiency SOFC deployments for data centers, utilities, commercial buildings, and industrial facilities requiring resilient on-site power. The company is investing in hydrogen-ready fuel cell systems, electrolyzers, and carbon capture technologies to support the clean energy transition.

Ceres Power Holding plc

Ceres Power Holding plc is a leading developer of solid oxide fuel cell (SOFC) and solid oxide electrolyzer cell (SOEC) technologies. Rather than manufacturing complete fuel cell systems, the company licenses its technology to global partners for commercial production across power generation, hydrogen production, and industrial applications. Ceres' fuel-flexible technology can operate on natural gas, hydrogen, and other low-carbon fuels, making it well suited for distributed energy and data center applications.

- Key Products: Ceres Endura.

- Recent Developments: In April 2026, Ceres launched Ceres Endura, its flagship solid oxide stack platform designed to meet rising demand for resilient, efficient, on-site power in data centers and other energy-intensive applications. The platform enables partners to serve both power and hydrogen markets from a single production base. Its fuel flexibility supports natural gas use today while allowing future operation on hydrogen and other low-carbon fuels.

- Strategic Focus: Expanding the commercialization of its SOFC and SOEC technologies through a licensing-led business model and partnerships with global manufacturers. The company is prioritizing hydrogen-ready and reversible solid oxide technologies for distributed power generation, data centers, industrial decarbonization, and green hydrogen production.

Market Concentration Analysis

The United States solid oxide fuel cell market exhibits moderate market concentration, with a limited number of technology leaders holding significant expertise in SOFC stack development and system integration. Companies such as Bloom Energy, FuelCell Energy, Inc., Ceres Power Holding plc, KYOCERA Corporation, and Elcogen are prominent innovators, while several other fuel cell companies and technology developers contribute through partnerships and niche applications. Competition is driven by continuous investments in hydrogen-ready systems, stack durability, fuel flexibility, and efficiency improvements. Strategic collaborations, licensing agreements, and government-supported R&D initiatives are accelerating commercialization and market expansion. As demand grows across data centers, industrial facilities, and distributed energy systems, new entrants and technology partnerships are expected to gradually increase competitive intensity.

Investment & Growth Opportunities

Highest Growth Segments

Data centers AI SOFC (~45.3% CAGR), stationary commercial CHP IRA (~44.2% CAGR), military DoD SOFC (~42.5% CAGR), green hydrogen SOFC (~50% CAGR from small base), West California SGIP SOFC (~45% CAGR), and Northeast commercial Bloom expansion (~43% CAGR) represent the US SOFC highest-growth investment vectors through 2034.

Investment Themes

- AI Hyperscale Data Center SOFC Zero-Carbon Baseload: Growing investments in AI and hyperscale data centers are creating opportunities for SOFC systems to deliver high-efficiency, low-emission baseload power, reducing grid dependence while supporting continuous 24/7 operations.

- Military DoD SOFC FOB and Portable Resilient Power: Defense investments in resilient energy solutions are driving adoption of SOFC systems for forward operating bases (FOBs) and portable power applications, providing quiet, fuel-flexible, and reliable electricity for mission-critical operations in remote environments.

Future Market Outlook (2026-2034)

The United States solid oxide fuel cell market is projected to grow from USD 530.7 Million in 2025 to USD 15,083.1 Million by 2034, delivering a 43.70% CAGR over the forecast period through AI data center zero-carbon SOFC baseload explosion, green hydrogen H2-ready SOFC transition, military DoD forward operating base resilient power, and commercial net-zero building CHP. The market's anchor value of USD 3,251.9 Million in 2030 represents US SOFC at hyperscale data center mainstream and IRA hydrogen inflection.

Three structural forces define US SOFC growth through 2034: rising AI/data center power demand, accelerating clean hydrogen investment, and growing need for resilient distributed energy. Data centers are increasing demand for reliable, low-emission baseload power, while hydrogen initiatives are expanding the role of fuel-flexible and hydrogen-ready SOFC systems. At the same time, grid congestion, outage risks, and decarbonization goals are driving adoption across microgrids, industrial facilities, military bases, and commercial sites.

Research Methodology

Primary Research

Primary research comprised interviews with SOFC manufacturers, fuel cell technology providers, component suppliers, EPC contractors, utility companies, data center operators, hydrogen ecosystem participants, and industry experts across the United States. These discussions validated market size, technology adoption trends, end-user demand, pricing dynamics, competitive developments, and future investment outlook. Insights from key stakeholders were used to verify secondary research findings and refine market forecasts.

Secondary Research

Secondary research encompassed the analysis of company annual reports, investor presentations, press releases, government publications, US Department of Energy (DOE) reports, industry associations, scientific journals, and regulatory documents. It also included the review of market databases, technology white papers, hydrogen economy initiatives, and data center infrastructure developments to assess market trends, competitive positioning, and future growth opportunities.

Forecasting Models

Forecasting models were developed using a combination of historical market trends, adoption rate analysis, and demand-side assessment across key end-use industries. The analysis incorporated macroeconomic indicators, government clean energy policies, hydrogen infrastructure expansion, data center investments, and technology commercialization trends. Market projections were validated through primary industry interviews and triangulated with secondary research to ensure robust and reliable forecasts through 2034.

United States Solid Oxide Fuel Cell Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Applications Covered | Portable, Stationary |

| End Users Covered | Commercial, Data Centers, Military and Defense, Others |

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered | Bloom Energy, FuelCell Energy, Inc., Ceres Power Holding plc, KYOCERA Corporation, Elcogen, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the United States solid oxide fuel cell market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the United States solid oxide fuel cell market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the United States solid oxide fuel cell industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the United States Solid Oxide Fuel Cell Market Report

The United States solid oxide fuel cell market reached USD 530.7 Million in 2025, driven by rising demand for reliable, low-emission, and high-efficiency on-site power across data centers, commercial buildings, industrial facilities, and microgrids. Growing investments in hydrogen infrastructure, clean energy transition, and distributed generation are further accelerating SOFC adoption. Grid reliability concerns and the need for resilient backup power are also strengthening market growth.

The United States solid oxide fuel cell market grows at 43.70% CAGR during 2026-2034, reaching USD 15,083.1 Million by 2034. The CAGR reflects AI data center power explosion, green hydrogen H2 transition, military DoD SOFC, and Bloom Energy cost reduction learning curve, creating exponential volume-price growth.

Stationary leads at 78.4% due to strong demand for continuous, high-efficiency on-site power in data centers, commercial buildings, industrial facilities, and hospitals. Its ability to provide reliable, low-emission baseload and backup power supports its dominant market position.

Data centers lead at 41.8% due to their need for uninterrupted, high-efficiency, and low-emission power. Rising AI, cloud computing, and hyperscale infrastructure demand is increasing SOFC adoption for reliable baseload and backup electricity.

Northeast lead at 35.7% due to high demand from data centers, healthcare facilities, universities, and commercial buildings. High electricity costs, clean energy targets, and grid reliability needs further support for SOFC adoption in the region.

Leading companies include Bloom Energy, FuelCell Energy, Inc., Ceres Power Holding plc, KYOCERA Corporation, and Elcogen, among others.

The market is projected to reach approximately USD 3,251.9 Million by 2030, driven by increasing deployment across data centers, industrial facilities, and distributed energy systems. Continued investments in hydrogen technologies, grid resilience, and clean energy infrastructure are expected to support sustained market expansion.

Three priority investment opportunities are expected to shape the United States solid oxide fuel cell market through 2034. AI hyperscale data center power systems present significant potential as operators seek reliable, low-emission baseload electricity. Military and defense applications are driving investments in resilient SOFC solutions for forward operating bases and mission-critical infrastructure. Additionally, green hydrogen production and reversible SOFC technologies offer long-term growth opportunities by supporting energy storage, industrial decarbonization, and hydrogen-based power systems.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)