United States Telehealth Market Size, Share, Trends and Forecast by Component, Communication Technology, Hosting Type, Application, End User, and Region, 2026-2034

United States Telehealth Market Summary:

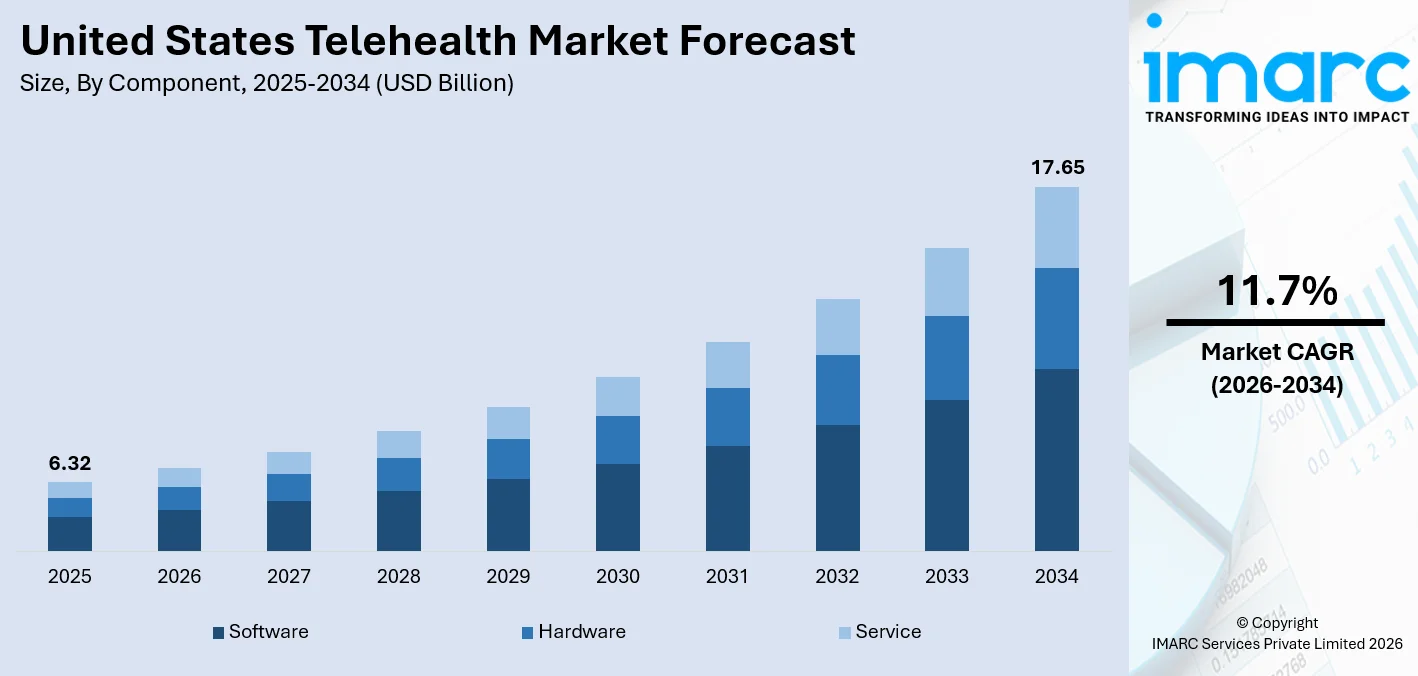

The United States telehealth market size was valued at USD 6.32 Billion in 2025 and is projected to reach USD 17.65 Billion by 2034, growing at a compound annual growth rate of 11.7% from 2026-2034.

The United States telehealth market is growing at a rapid pace, with digital healthcare services increasingly becoming accepted by patients as well as service providers. The increasing trend of adopting virtual consultations, the rise of demand for remote patient monitoring, and the implementation of favorable reimbursement policies are causing tremendous changes in the United States healthcare market. All these factors, along with the increased awareness of the benefits of telehealth services, are contributing to the growth of the United States telehealth market share.

Key Takeaways and Insights:

- By Component: Software dominates the market with a share of 45.3% in 2025, reflecting its foundational role in enabling virtual care delivery, digital platform integration, and seamless management of patient data across all healthcare settings.

- By Communication Technology: Video conferencing leads the market with a share of 52.4% in 2025, driven by its ability to facilitate real-time, face-to-face patient-provider interactions that closely replicate in-person clinical consultations across diverse specialties.

- By Hosting Type: Cloud-Based and web-based represents the largest segment with a market share of 68.5% in 2025, representing the most widely adopted infrastructure model due to scalability, flexible accessibility, and cost-effective data management.

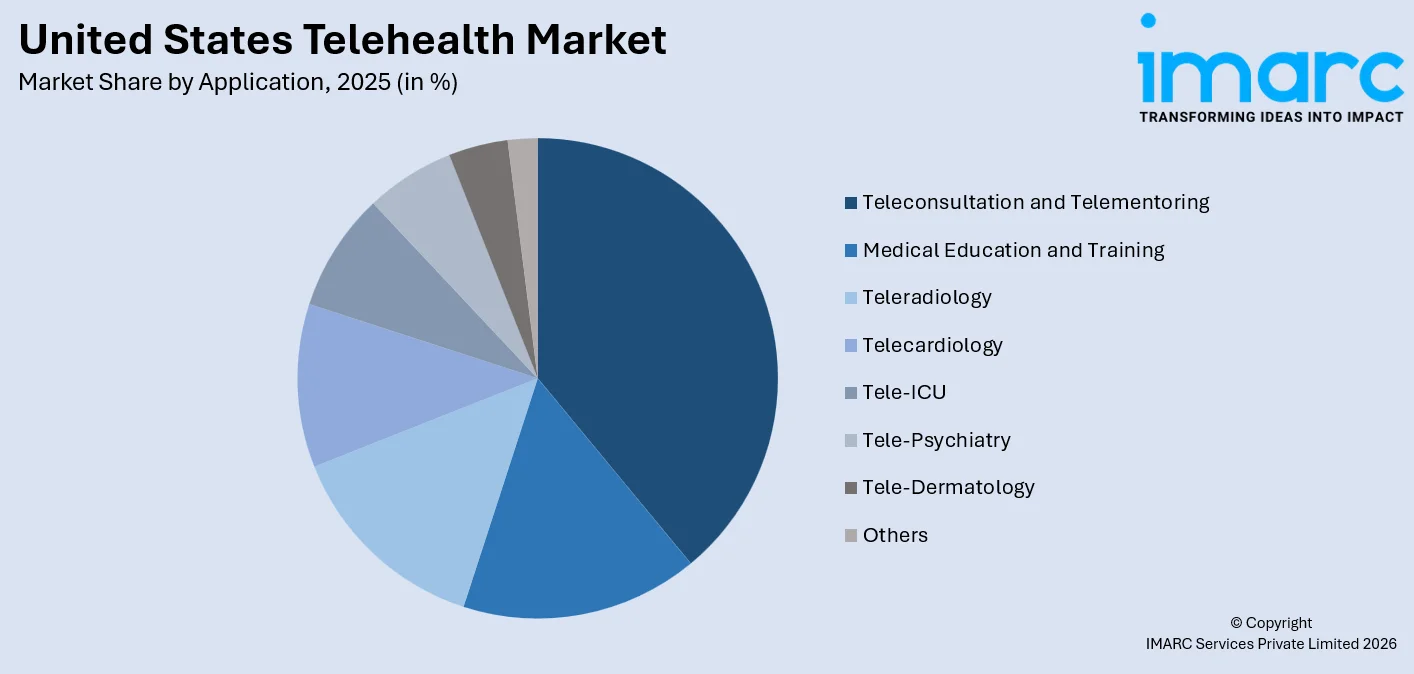

- By Application: Teleconsultation and telementoring dominates the market with a share of 38.2% in 2025, forming the core of telehealth service delivery and enabling patients to access specialist guidance and real-time clinical consultations remotely.

- By End User: Providers leads the market with a share of 48.6% in 2025, underscoring their central role in deploying virtual care platforms and integrating telehealth into standard healthcare delivery workflows.

- By Region: South dominates the market with a share of 31.5% in 2025, supported by its geographically dispersed population, significant rural communities with limited traditional healthcare access, and high prevalence of chronic conditions.

- Key Players: The United States telehealth market is highly competitive, with a diverse mix of established healthcare technology firms and specialized virtual care platforms continuously innovating to expand their service offerings and improve patient outcomes across all care settings.

To get more information on this market Request Sample

The United States telehealth market is witnessing robust growth, driven by an evolving healthcare landscape that increasingly prioritizes accessibility, efficiency, and patient-centered care. Advancements in digital infrastructure and mobile health technologies have extended telehealth services to both urban and rural communities. In 2026, Congress passed legislation extending Medicare telehealth coverage through the end of 2027, ensuring continued reimbursement for virtual care services delivered to seniors and other beneficiaries, a key policy boost supporting long‑term adoption in the U.S. The shift toward value-based care models has prompted widespread adoption of virtual consultations, remote patient monitoring, and digital health platforms among providers, payers, and patients. Policy changes enabling broader reimbursement for telehealth services have reinforced long-term adoption. The growing burden of chronic diseases, an aging population requiring continuous care management, and heightened consumer expectations for convenient healthcare access continue to accelerate demand. These converging factors are reshaping healthcare delivery across the nation, driving sustained expansion throughout the United States telehealth market.

United States Telehealth Market Trends:

Rising Adoption of AI-Powered Virtual Care Solutions

Artificial intelligence is increasingly embedded in telehealth platforms, transforming how virtual care is delivered and managed across the United States. In 2026, U.S. healthcare technology company OpenEvidence released a new AI‑integrated clinical decision‑support platform that now powers privacy‑centric telemedicine calls, secure messaging, and real‑time AI assistance within virtual care workflows, marking a significant expansion of AI into everyday telehealth practice. AI-driven tools are enhancing clinical decision-making, streamlining administrative workflows, and enabling more accurate remote diagnostics. Machine learning algorithms are being applied for automated triaging, symptom assessment, and predictive health monitoring, allowing providers to deliver more responsive and personalized care. These capabilities are accelerating wider adoption of AI-powered telehealth solutions across diverse medical specialties throughout the country.

Expansion of Remote Patient Monitoring and Wearable Technology

The integration of wearable health devices with telehealth platforms is redefining continuous care management for patients with chronic conditions. In March 2026, Microsoft unveiled Copilot Health, a new AI‑powered health tool that can connect data from over 50 types of wearable devices, including Apple, Fitbit, and Oura, with clinical insights and patient records, enabling users and clinicians to combine remote monitoring with virtual care interactions. Advanced monitoring tools can track vital signs, glucose levels, and cardiac activity in real time, enabling early detection of health deterioration. This shift is particularly impactful for managing long-term conditions such as diabetes, hypertension, and cardiovascular disorders. By supporting proactive clinical interventions and reducing avoidable hospitalizations, remote patient monitoring is becoming an essential component of virtual care delivery across the United States.

Growing Focus on Behavioral and Mental Health Telehealth

Mental and behavioral health services represent one of the most rapidly expanding segments within the United States telehealth market growth landscape. Virtual platforms are making psychiatric consultations, therapy sessions, and medication management more accessible, particularly in underserved and rural communities. In February 2026, telepsychiatry provider Talkiatry raised $210 million in a Series D funding round to scale its AI‑powered virtual psychiatry platform, highlighting continued investor confidence in tele‑mental health solutions across the U.S. Growing awareness of mental health challenges, reduced stigma surrounding treatment-seeking, and the convenience of remote care are driving strong and sustained demand for tele-psychiatry and virtual behavioral health services. This trend is reshaping how mental healthcare is delivered nationwide.

Market Outlook 2026-2034:

The United States market for telehealth services is expected to register steady and sustained growth during the forecast period. The United States telehealth market will benefit from continued investment in digital health infrastructure, changes in the reimbursement model, and growing adoption of telehealth services across various clinical specialties. The demand for telehealth services in managing chronic diseases, behavioral health services, and AI-based care delivery will be key revenue generators for the United States telehealth market. Technology will play a key role in shaping the future of the United States telehealth market. The market generated a revenue of USD 6.32 Billion in 2025 and is projected to reach a revenue of USD 17.65 Billion by 2034, growing at a compound annual growth rate of 11.7% from 2026-2034.

United States Telehealth Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Component |

Software |

45.3% |

|

Communication Technology |

Video Conferencing |

52.4% |

|

Hosting Type |

Cloud-Based and Web-Based |

68.5% |

|

Application |

Teleconsultation and Telementoring |

38.2% |

|

End User |

Providers |

48.6% |

|

Region |

South |

31.5% |

Component Insights:

- Software

- Hardware

- Service

The software dominates with a market share of 45.3% of the total United States telehealth market in 2025.

The software platforms are at the center of telehealth service delivery in the United States, ensuring that virtual consultations are conducted seamlessly, patient information is handled effectively, and schedules are kept efficiently. The platforms ensure that secure and compliant virtual environments are created to enable effective interactions between patients and healthcare services within all settings. The need for more connected platforms that enable clinical connectivity, automation, and artificial intelligence is ensuring that telehealth software remains at the center as a foundation for virtual healthcare services in the United States.

The growing complexity associated with delivering healthcare services is leading to more investments in advanced software solutions that can facilitate virtual care models involving various specialties. Telehealth software has advanced significantly to include a wide range of functionalities, such as real-time diagnostics support, patient monitoring integration, predictive analysis, and billing automation. As healthcare services aim to achieve greater efficiency and better patient outcomes through digital transformation, software is seen as the most critical facilitator of telehealth services, thereby reiterating its position as the leading telehealth component segment in the country.

Communication Technology Insights:

- Video Conferencing

- mHealth Solutions

- Others

The video conferencing leads with a share of 52.4% of the total United States telehealth market in 2025.

Video conferencing is the most commonly used communication modality in the United States telehealth market, allowing patients and providers to communicate in real-time, as well as have face-to-face interactions that mimic in-person care delivery. The ability of video conferencing to transmit visual and non-verbal communication cues, facilitate multiple-party clinical consultations, and integrate with digital health technologies has made it the most preferred communication modality for the delivery of care services, thereby establishing its position as the leading communication modality in the United States telehealth market.

The continued evolution of video conferencing infrastructure is enhancing the quality, reliability, and accessibility of virtual consultations for both providers and patients. Improvements in platform security, bandwidth optimization, and multi-device compatibility are making high-quality video-based care increasingly feasible across urban and rural settings alike. Integration with electronic health records, digital prescribing tools, and remote monitoring capabilities is further expanding the clinical utility of video conferencing, reinforcing its centrality to virtual care delivery across diverse medical specialties throughout the country.

Hosting Type Insights:

- Cloud-Based and Web-Based

- On-Premises

The cloud-based and web-based dominates with a market share of 68.5% of the total United States telehealth market in 2025.

Cloud-based and web-based hosting solutions have become the dominant infrastructure model in the United States telehealth market, offering scalability, cost efficiency, and remote accessibility that traditional on-premises systems cannot match. These platforms enable secure data storage, real-time updates, and multi-device access for both providers and patients. Their compatibility with electronic health records and ability to support high-volume care delivery across diverse healthcare organizations have driven widespread adoption throughout the country's rapidly expanding virtual care ecosystem.

The flexibility of cloud-based and web-based platforms is particularly valuable for healthcare organizations managing large and geographically dispersed patient populations. These solutions support seamless interoperability across care networks, enabling coordinated and continuous patient management without the constraints of physical infrastructure. As telehealth programs scale and diversify, cloud-based environments provide the technological agility required to incorporate AI-driven tools, remote monitoring integrations, and advanced analytics, positioning this hosting model as the preferred foundation for sustainable and future-ready telehealth operations across the United States.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Teleconsultation and Telementoring

- Medical Education and Training

- Teleradiology

- Telecardiology

- Tele-ICU

- Tele-Psychiatry

- Tele-Dermatology

- Others

The teleconsultation and telementoring leads with a share of 38.2% of the total United States telehealth market in 2025.

Teleconsultation and telementoring represent the foundational use cases of telehealth in the United States, enabling patients to access real-time clinical consultations and expert guidance across diverse medical specialties. These services reduce geographic barriers to care, particularly for patients in rural and underserved communities, and offer a convenient alternative to in-person visits for routine, chronic, and follow-up care. Their broad applicability across all healthcare disciplines has established them as the most widely utilized application within the telehealth landscape.

The growing adoption of teleconsultation reflects a broader shift in patient expectations toward accessible, convenient, and technology-enabled healthcare delivery. Virtual consultation platforms now support a wide spectrum of clinical needs, ranging from primary care and specialist referrals to complex case reviews and clinical mentoring for healthcare professionals. As providers continue to integrate these tools into standard care pathways, teleconsultation and telementoring are becoming indispensable components of comprehensive healthcare delivery, driving sustained demand within the application segment throughout the forecast period.

End User Insights:

- Providers

- Patients

- Payers

- Others

The providers dominates with a market share of 48.6% of the total United States telehealth market in 2025.

Healthcare providers are the primary adopters of telehealth platforms in the United States, leveraging virtual care tools to expand patient reach, reduce operational burden, and improve clinical outcomes. Hospitals, clinics, and specialty practices are integrating telehealth into standard care delivery to manage growing patient demand and enhance service accessibility. In October 2025, telehealth provider HealthTap partnered with Eli Lilly’s digital health platform LillyDirect to offer virtual diabetes management services, enabling HealthTap’s clinicians to provide medication oversight and preventive care through Lilly’s consumer‑facing digital channel and deepening provider adoption of telehealth tools in chronic care. The widespread use of remote consultations, patient monitoring, and digital care coordination has reinforced providers' central role in driving telehealth adoption across the national healthcare system.

The increasing emphasis on value-based care models is further motivating providers to invest in telehealth capabilities that support proactive patient management and reduce avoidable hospitalizations. Virtual care platforms enable providers to extend their services beyond traditional facility boundaries, reaching patients in remote and underserved areas. As reimbursement frameworks continue to evolve in favor of virtual care delivery, providers are expanding their telehealth portfolios to include chronic disease management, behavioral health services, and remote monitoring, cementing their dominant position within the end-user segment.

Regional Insights:

- Northeast

- Midwest

- South

- West

South exhibits a clear dominance with a 31.5% share of the total United States telehealth market in 2025.

The South holds the largest regional share in the United States telehealth market, driven by its large, geographically dispersed population and significant rural communities with historically limited access to traditional healthcare infrastructure. The high prevalence of chronic conditions such as diabetes, hypertension, and cardiovascular disease in the region generates strong demand for continuous remote care management. Ongoing investments in broadband connectivity and strong provider adoption of virtual care platforms are further reinforcing the South's leadership position within the national telehealth landscape.

State-level telehealth-friendly policies and an expanding network of digitally enabled healthcare facilities are accelerating virtual care adoption across the Southern United States. The region's diverse and growing population base, combined with persistent physician shortages in rural areas, has made telehealth an essential tool for bridging care gaps and ensuring equitable access to quality healthcare services. These structural and demographic factors collectively sustain the South's position as the largest and most dynamic regional contributor to the overall United States telehealth market throughout the forecast period.

Market Dynamics:

Growth Drivers:

Why is the United States Telehealth Market Growing?

Expanding Government Support and Reimbursement Policies

The United States government has taken significant steps to institutionalize telehealth as a sustainable component of the national healthcare system. Federal agencies have progressively broadened reimbursement frameworks, allowing providers across a wider range of settings to bill for telehealth services rendered to Medicare and Medicaid beneficiaries. In January 2026, the U.S. Department of Health and Human Services (HHS) and the Drug Enforcement Administration (DEA) jointly announced an extension of telemedicine prescribing flexibilities that allow clinicians to prescribe controlled medications via telehealth without a prior in‑person visit through the end of 2026, helping maintain continuity of care for patients with substance use disorders and other conditions. State-level telehealth parity laws further complement federal policy by requiring insurers to reimburse virtual visits at rates comparable to in-person consultations. These combined regulatory and financial support mechanisms reduce barriers to adoption and enable healthcare organizations to scale their telehealth capabilities effectively.

Rising Burden of Chronic Diseases and an Aging Population

The United States is experiencing a significant rise in chronic disease prevalence, with millions of individuals managing conditions such as diabetes, hypertension, cardiovascular disorders, and obesity. In 2023, about 76.4 % of U.S. adults, representing more than 194 million people, reported having at least one chronic condition, and over 51 % had multiple conditions, underscoring the widespread and growing health burden across the population. These conditions require continuous monitoring, frequent consultations, and ongoing care coordination that telehealth is uniquely positioned to address. The country's aging population is also growing rapidly, creating heightened demand for remote care services that reduce the physical burden of frequent in-person visits. This dual demographic pressure is generating sustained demand for remote healthcare services, strengthening the market's long-term growth trajectory.

Accelerating Technological Advancements in Digital Health

Continuous advancements in digital technology are expanding the capabilities and reach of telehealth solutions throughout the United States. Innovations in artificial intelligence, cloud computing, mobile applications, and wearable health devices are enabling more sophisticated, personalized, and efficient virtual care experiences. In March 2026, Amazon launched its “Health AI” agent across its website and app to provide 24/7 AI‑powered health guidance, including personalized insights, appointment scheduling, medication management, and direct integration with Amazon One Medical virtual care services, expanding how digital tools support everyday telehealth interactions. AI-powered diagnostic tools and predictive analytics are enhancing clinical decision-making by supporting early identification of health risks. Cloud-based platforms are enabling seamless integration with electronic health records, improving care coordination across healthcare networks and making virtual care an increasingly viable and integral component of the national healthcare ecosystem.

Market Restraints:

What Challenges the United States Telehealth Market is Facing?

Regulatory Uncertainty and Policy Instability

Telehealth reimbursement policies in the United States have been subject to frequent revisions and temporary extensions, creating operational uncertainty for providers dependent on Medicare and Medicaid billing structures. Recurring policy cliffs interrupt long-term planning, infrastructure investment, and workforce development decisions for healthcare organizations. This regulatory instability discourages smaller providers from fully committing to telehealth integration and undermines predictable market growth. Consistent, permanent legislative frameworks are essential to ensure continuity and confidence in virtual care services across the nation.

Data Privacy and Cybersecurity Vulnerabilities

Telehealth platforms manage vast volumes of sensitive patient health information, making them attractive and high-value targets for cybersecurity threats. Ensuring full compliance with federal and state privacy regulations while maintaining robust data security standards is a complex and resource-intensive undertaking for healthcare organizations. Ongoing challenges in protecting patient data from breaches, ransomware attacks, and unauthorized access undermine patient trust and expose providers to significant legal, financial, and reputational risks. These security imperatives add operational complexity that can hinder broader telehealth deployment and adoption.

Digital Divide and Technology Access Barriers

Despite widespread telehealth adoption, significant gaps in digital access persist across rural, elderly, and lower-income populations throughout the United States. Limited availability of reliable broadband internet connectivity, low digital literacy levels, and restricted access to compatible devices prevent many individuals from equitably benefiting from virtual care services. This unequal access creates persistent disparities in healthcare outcomes and constrains the market's potential for universal adoption. Bridging the digital divide requires coordinated investment in broadband infrastructure, device affordability programs, and targeted digital literacy initiatives.

Competitive Landscape:

The United States telehealth market is highly competitive, with a diverse ecosystem of established healthcare technology companies, dedicated virtual care platforms, and emerging digital health innovators continuously competing for market share. Differentiation is increasingly driven by expanded service portfolios, AI-enhanced care delivery capabilities, and seamless integration with existing clinical workflows and electronic health records. Strategic alliances between technology firms and healthcare systems have become central to accelerating telehealth deployment and broadening patient access across all care settings. The market is characterized by growing consolidation, as organizations seek to offer comprehensive solutions spanning primary care, behavioral health, chronic disease management, and specialty consultations. Reimbursement-aligned business models and value-based care frameworks are reshaping competitive dynamics, favoring providers that demonstrate measurable clinical and financial outcomes.

Recent Developments:

- In March 2026, TABLET, led by experienced pharmacy operators, has launched a nationwide telehealth platform combining traditional clinical care with digital services. The platform offers advanced therapies and personalized coaching, positioning TABLET as a hybrid model bridging virtual efficiency and trusted in-person care.

United States Telehealth Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Components Covered | Software, Hardware, Service |

| Communication Technologies Covered | Video Conferencing, mHealth Solutions, Others |

| Hosting Types Covered | Cloud-Based and Web-Based, On-Premises |

| Applications Covered | Teleconsultation and Telementoring, Medical Education and Training, Teleradiology, Telecardiology, Tele-ICU, Tele-Psychiatry, Tele-Dermatology, Others |

| End Users Covered | Providers, Patients, Payers, Others |

| Regions Covered | Northeast, Midwest, South, West |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the United States Telehealth Market Report Report

The United States telehealth market size was valued at USD 6.32 Billion in 2025.

The United States telehealth market is expected to grow at a compound annual growth rate of 11.7% from 2026-2034 to reach USD 17.65 Billion by 2034.

Software dominates the U.S. telehealth market with a 45.3% share, underpinning virtual consultations, patient data management, and scheduling through secure, AI-integrated, and clinically connected platforms across all healthcare settings.

Key factors driving the United States telehealth market include expanding government reimbursement policies, rising chronic disease prevalence, an aging population requiring continuous care management, advancements in AI and digital health technologies, growing consumer demand for convenient healthcare access, and increasing provider adoption of virtual care platforms.

Major challenges include regulatory uncertainty around telehealth reimbursement policies, data privacy and cybersecurity concerns, an unequal digital divide affecting rural and elderly populations, and the need for sustained investment in broadband infrastructure to support broader and more equitable virtual care adoption.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)