United States Timber Construction Market Size, Share, Trends and Forecast by End Use, Timber Type, and Region, 2026-2034

United States Timber Construction Market Summary:

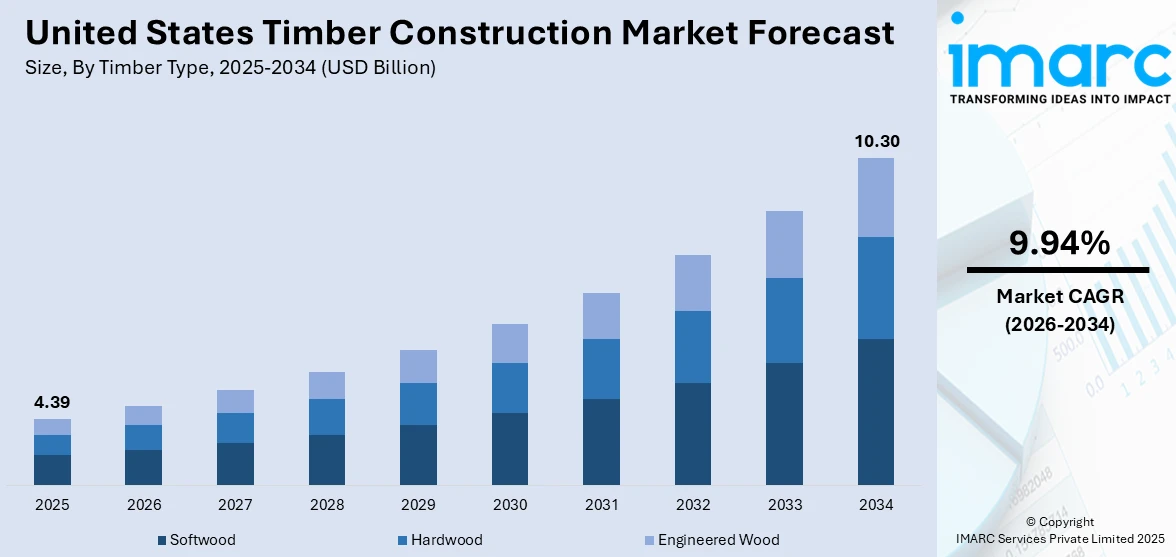

The United States timber construction market size was valued at USD 4.39 Billion in 2025 and is projected to reach USD 10.30 Billion by 2034, growing at a compound annual growth rate of 9.94% from 2026-2034.

As sustainable building methods spread throughout the residential and commercial sectors, the US timber construction business is expanding rapidly. Adoption is being accelerated by changing building rules to allow for larger mass timber structures, rising environmental consciousness about embodied carbon reduction, and increased domestic production capability for engineered wood goods. The market share of timber building in the United States is being strengthened by developments in cross-laminated timber technology and encouraging federal incentives.

Key Takeaways and Insights:

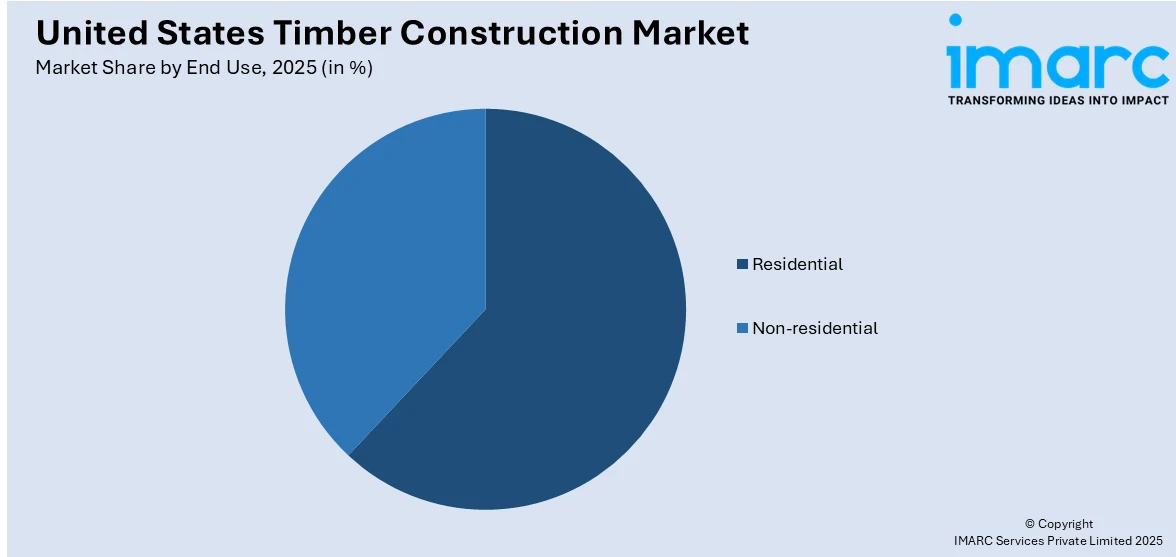

- By End Use: Residential dominates the market with a share of 62.4% in 2025, due to the ongoing demand for single-family and multifamily timber-framed construction in suburban and metropolitan regions brought on by the ongoing national housing shortage.

- By Timber Type: Softwood leads the market with a share of 48.9% in 2025, motivated by its extensive availability, affordability, and well-established status as the main structural frame material used in home building across the nation.

- By Region: West is the largest region with 41.3% share in 2025, encouraged by the high density of mass timber projects throughout the Pacific Northwest, modern construction rules, and the concentration of timber producing infrastructure in Oregon and Washington.

- Key players: In order to meet growing demand across residential and commercial construction segments nationwide, key players propel the US timber construction market by increasing capacity for manufacturing engineered wood, developing cross-laminated timber technologies, fortifying supply chain integration, and making investments in sustainable forestry practices.

To get more information on this market Request Sample

The United States timber construction market is advancing as builders, developers, and policymakers increasingly recognize timber as a viable and sustainable alternative to conventional steel and concrete construction systems. The growing adoption of mass timber technologies, particularly cross-laminated timber and glue-laminated timber, is enabling the construction of larger and taller wood-based structures that meet modern performance and safety standards. This momentum is further reinforced by evolving building codes that now permit mass timber structures in mid-rise and high-rise construction, significantly broadening the material's applicability across a wider range of building types. For instance, according to WoodWorks, approximately 2,598 multifamily, commercial, or institutional mass timber projects were either built or in progress across the United States as of December 2025. Federal investment programs, green building certification systems, and corporate sustainability mandates are collectively supporting timber’s deeper integration into mainstream construction practices. Rising consumer preference for eco-friendly and energy-efficient housing, combined with expanding domestic engineered wood manufacturing infrastructure, is positioning the market for robust long-term expansion.

United States Timber Construction Market Trends:

Rising Adoption of Mass Timber in Mid-Rise and High-Rise Construction

Mass wood is becoming more popular in mid-rise and high-rise construction projects in the US as architects and developers recognize its structural potential and sustainability benefits. Taller timber constructions are now allowed by progressive building rules, greatly increasing the material's use in institutional and commercial settings. Wider adoption is being fueled by demonstrated fire resistance, quicker building schedules, and less trash production on-site. Mass timber's reputation as a common building material for intricate urban constructions is being further strengthened by increased familiarity among engineers, contractors, and code inspectors.

Growing Integration of Biophilic Design Principles in Timber Buildings

In the United States, timber building is become more influenced by biophilic design ideas that prioritize natural materials and occupant well-being. Updated construction requirements have expanded potential for exposed timber surfaces in taller structures, allowing architects to showcase wood interiors that enhance aesthetic appeal while complying with safety regulations. By lowering finishing costs and attracting renters and occupants who value cozy, natural interior spaces, this regulation change promotes the expansion of the timber building industry in the United States. Timber's aesthetic warmth is being used by developers in the commercial, retail, and residential sectors to draw both ecologically concerned and health-sensitive tenants.

Advancements in Engineered Wood Product Innovation

The performance envelope of timber in structural applications is being expanded by the quick evolution of engineered wood technologies. Long-standing issues with fire safety, moisture resistance, and durability are being addressed by advancements in glue-laminated, cross-laminated, and next-generation treated wood products. Because of these developments, engineered wood is becoming more competitive with conventional building materials for major commercial and infrastructural projects. The development of stronger, lighter, and more resilient wood products that satisfy strict structural and environmental performance criteria across a variety of building types is being accelerated by ongoing research supported by federal funding.

Market Outlook 2026-2034:

The market for timber construction in the United States is expected to grow steadily over the course of the forecast period due to a combination of advantageous legislative changes, environmental demands, and technical breakthroughs in engineered wood systems. Expanding domestic production capacity for glue-laminated and cross-laminated timber, together with growing federal and state support for low-carbon construction, are anticipated to increase the use of timber in residential, commercial, and institutional building segments. The market generated a revenue of USD 4.39 Billion in 2025 and is projected to reach a revenue of USD 10.30 Billion by 2034, growing at a compound annual growth rate of 9.94% from 2026-2034. Higher income streams are anticipated as a result of growing consumer desire for sustainable housing, ongoing changes to building laws to allow for larger timber buildings, and growing corporate acceptance of green building standards. A more competitive, developed, and robust timber building environment is expected to be fostered nationwide by improved supply chain integration, worker development programs, and increased investor confidence in mass timber construction.

United States Timber Construction Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

End Use |

Residential |

62.4% |

|

Timber Type |

Softwood |

48.9% |

|

Region |

West |

41.3% |

End Use Insights:

Access the comprehensive market breakdown Request Sample

- Residential

- Non-residential

Residential dominates the market with a share of 62.4% of the total United States timber construction market in 2025.

The residential segment’s dominance is anchored in the deep-rooted preference for wood-framed construction in American homebuilding, where timber remains the primary structural material for single-family homes, townhouses, and low-rise multifamily developments. Light-frame wood construction offers builders significant advantages in terms of cost efficiency, design flexibility, and construction speed compared to steel and concrete alternatives. The sustained national housing shortage continues to fuel demand, with the Congressional Budget Office projecting housing starts to average 1.68 Million Units annually from 2025 to 2029, creating substantial ongoing consumption of structural lumber and engineered wood products.

Rising consumer awareness around energy efficiency and environmental sustainability is further strengthening timber’s position in the residential sector. Wood-framed structures inherently provide superior thermal insulation properties, reducing heating and cooling costs for homeowners while supporting compliance with increasingly stringent energy codes. The expansion of mass timber applications into mid-rise residential buildings, enabled by updated International Building Code provisions, is opening new construction possibilities in urban markets. For instance, in February 2025, Timberlab broke ground on a 190,000-square-foot cross-laminated timber manufacturing facility in Millersburg, Oregon, expanding domestic supply capacity for residential and commercial timber construction.

Timber Type Insights:

- Softwood

- Hardwood

- Engineered Wood

Softwood leads with a share of 48.9% of the total United States timber construction market in 2025.

Softwood's dominant position in the market is a reflection of its essential function as the foundation of structural building in the US. Framing timber applications are dominated by species like Douglas fir, southern yellow pine, and spruce-pine-fir because of their cost-effectiveness, workability, and superior strength-to-weight ratios. The bulk of softwood timber used domestically is used for home improvement projects and residential construction, particularly single-family homes. With continuously growing mill capacity, the U.S. South has become a vital manufacturing base, guaranteeing a steady and dependable supply for the building industry.

As manufacturers look to improve domestic supply chains and lessen dependency on imported timber, the softwood market also gains from increased industrial investment. Businesses have been setting up shop in the Southeast United States because of the region's rich wood resources, highly qualified workforce, and advanced infrastructure. The need for softwood is expanding beyond traditional framing due to its increasing use in the fabrication of glue-laminated and cross-laminated timber. Long-term supply availability is being strengthened by federal programs that encourage sustainable timber harvesting and active forest management, setting up the softwood market for future expansion in both traditional and engineered wood building applications.

Regional Insights:

- Northeast

- Midwest

- South

- West

West exhibits a clear dominance with 41.3% share of the total United States timber construction market in 2025.

The vast forest resources, concentrated infrastructure for timber manufacture, and forward-thinking legislative framework that actively promotes wood-based building systems are the main reasons responsible for the lead of the Western area in timber construction. The Pacific Northwest is the main source of structural lumber and engineered wood products since Oregon and Washington together produce the most of the nation's timber. Significant mass wood project activity has been observed in a number of western states in the commercial, institutional, and multifamily construction sectors, indicating strong and expanding demand across the area.

The Western region also benefits from a concentration of mass timber manufacturing capabilities and research institutions that support innovation and workforce development. The Pacific Northwest serves as the primary hub for cross-laminated timber and glue-laminated timber production in the United States, with multiple facilities expanding capacity to meet rising demand. Ongoing investments in new and upgraded manufacturing operations are strengthening the region's production capabilities and reinforcing its central role in the national timber construction supply chain. Supportive state-level policies, strong academic partnerships, and a skilled workforce further enhance the West's competitive positioning within the broader market.

Market Dynamics:

Growth Drivers:

Why is the United States timber construction market growing?

Supportive Building Codes and Government Policy Initiatives

Evolving building codes and proactive government policies are creating a highly favorable regulatory environment for timber construction in the United States. Recent editions of the International Building Code have been widely adopted across the country, permitting taller mass timber structures and significantly expanding the material's applicability in commercial, institutional, and high-rise residential projects. These code changes have removed critical regulatory barriers that previously limited timber to low-rise construction, enabling developers to consider wood-based systems for a much broader range of building types. At the federal level, sustained investment through grant programs and procurement mandates prioritizing low embodied carbon materials is reinforcing timber's competitiveness, funding research and pilot projects that demonstrate the structural and environmental benefits of engineered wood in public and commercial buildings.

Growing Demand for Sustainable and Low-Carbon Construction Materials

Increasing environmental awareness and corporate sustainability commitments are driving a significant shift toward timber as a preferred construction material in the United States. Timber structures demonstrate substantially lower embodied carbon compared to steel and concrete alternatives, positioning wood-based systems as a practical pathway for achieving climate-related construction targets. Green building certification systems are further incentivizing the use of renewable resources, encouraging developers to integrate timber into projects seeking environmental credentials. Corporate adoption of mass timber is accelerating as major companies incorporate sustainability into their facilities strategies, commissioning large-scale timber office complexes, data centers, and mixed-use developments that showcase the material's performance capabilities while advancing organizational carbon reduction goals.

Expanding Domestic Manufacturing Capacity for Engineered Wood Products

The expansion of domestic cross-laminated timber and glue-laminated timber manufacturing capacity is strengthening the supply chain foundation necessary to support the market's growth trajectory. Historically, the limited availability of domestically produced engineered wood panels created reliance on imports, increasing costs and lead times. However, significant investments in new and expanded manufacturing facilities are rapidly addressing this constraint and positioning the United States to meet rising construction demand with domestically sourced engineered wood products. Companies across the Pacific Northwest and southeastern regions are establishing and upgrading production operations, supported by federal grant programs that catalyze private-sector investment in engineered wood infrastructure across key timber-producing areas.

Market Restraints:

What challenges the United States timber construction market is facing?

Lumber Price Volatility and Rising Material Costs

Softwood lumber prices have experienced significant volatility in recent years, driven by supply chain disruptions, fluctuating demand cycles, and escalating trade tensions. Rising tariffs on softwood lumber imports from Canada are increasing material costs, while mill curtailments across North America are further tightening supply availability. These cost pressures are elevating construction input expenses and creating uncertainty for developers and builders, ultimately constraining project feasibility and dampening broader market expansion.

Shortage Of Skilled Labor in Timber Construction

The timber construction industry faces a growing skilled labor deficit as the existing workforce ages and insufficient training infrastructure limits new entrant recruitment. The limited availability of accredited vocational programs offering specialized training in sustainable forestry or mass timber installation techniques is restricting the pipeline of qualified workers entering the field. This widening skills gap increases project costs, extends construction timelines, and constrains the industry's ability to scale operations in line with rising demand.

Competition From Established Steel and Concrete Construction Systems

Steel and concrete construction systems maintain deeply entrenched positions in the United States building industry, supported by established supply chains, widespread engineering familiarity, and extensive contractor training infrastructure. Many structural engineers and developers remain more comfortable specifying conventional materials due to decades of precedent and standardized design practices. This institutional inertia, combined with the relatively nascent nature of mass timber expertise among construction professionals, creates competitive barriers that slow timber's penetration into mainstream commercial and institutional construction segments.

Competitive Landscape:

The United States timber construction market features a moderately fragmented competitive landscape characterized by the presence of large integrated forest products companies, specialized engineered wood manufacturers, and regional sawmill operators. Market participants are focusing on expanding manufacturing capacity, advancing product innovation, and strengthening vertical integration to secure competitive advantages. Strategic acquisitions, partnerships with construction firms, and investments in cross-laminated timber and glue-laminated timber production technologies are shaping competitive dynamics. Companies are also pursuing sustainability certifications and digital fabrication capabilities to differentiate their offerings and capture growing demand from developers committed to green building standards.

United States Timber Construction Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Billion USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

End Uses Covered |

Residential, Non-residential |

|

Timber Types Covered |

Softwood, Hardwood, Engineered Wood |

|

Regions Covered |

Northeast, Midwest, South, West |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the United States Timber Construction Market Report

The United States timber construction market size was valued at USD 4.39 Billion in 2025.

The market is expected to grow at a compound annual growth rate of 9.94% from 2026-2034 to reach USD 10.30 Billion by 2034.

Residential, holding the largest revenue share of 62.4%, remains pivotal for the United States timber construction market, driven by sustained housing demand, cost-effective wood-framed building practices, and growing consumer preference for energy-efficient and sustainable homes.

Key factors driving the United States timber construction market include supportive building code reforms, growing demand for low-carbon construction materials, expanding domestic manufacturing capacity for engineered wood products, federal sustainability incentives, and rising adoption of mass timber technologies.

Major challenges include lumber price volatility driven by rising Canadian import tariffs, skilled labor shortages in timber construction trades, competition from established steel and concrete systems, supply chain disruptions, and limited mass timber engineering expertise among construction professionals.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)