United States Track and Trace Solutions Market Size, Share, Trends and Forecast by Product, Technology, Application, End Use Industry, and Region, 2026-2034

United States Track and Trace Solutions Market Size, Share, Trends & Forecast (2026-2034)

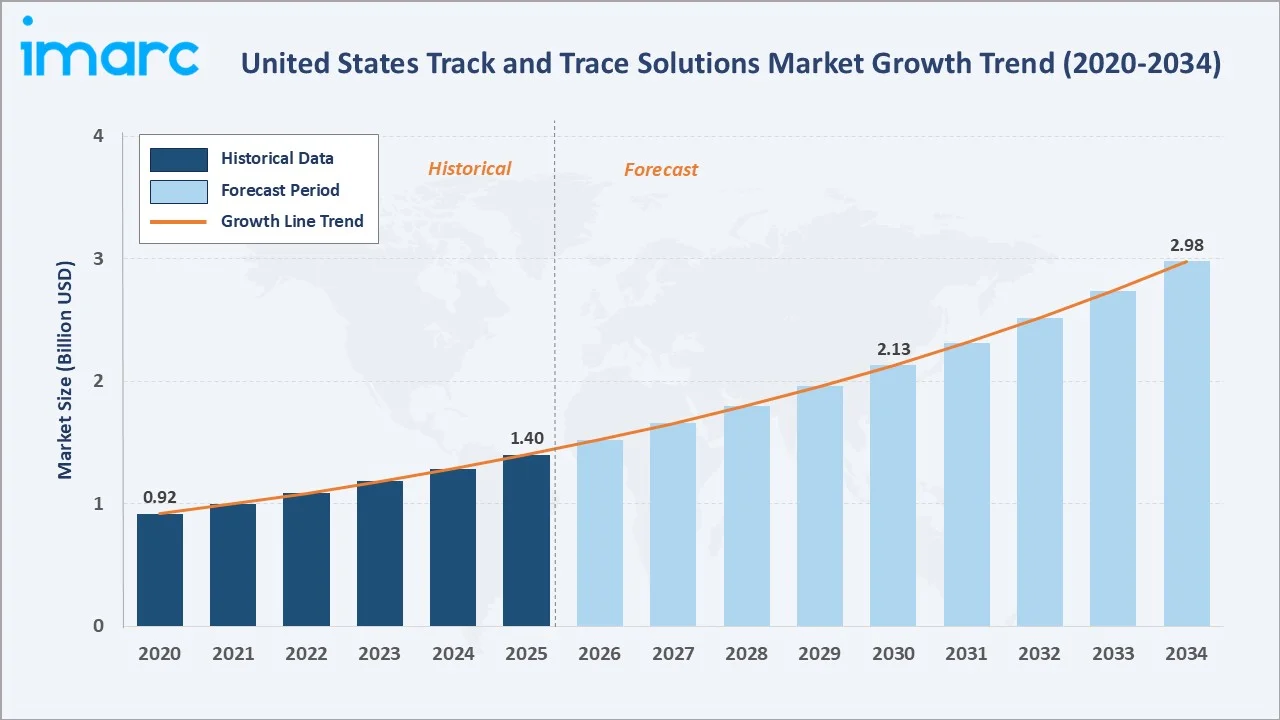

The United States track and trace solutions market reached USD 1.40 Billion in 2025 and is projected to reach USD 2.98 Billion by 2034, growing at a CAGR of 8.76% during 2026-2034. Regulatory mandates, pharmaceutical serialization requirements, and rising supply chain visibility needs are primary growth drivers.

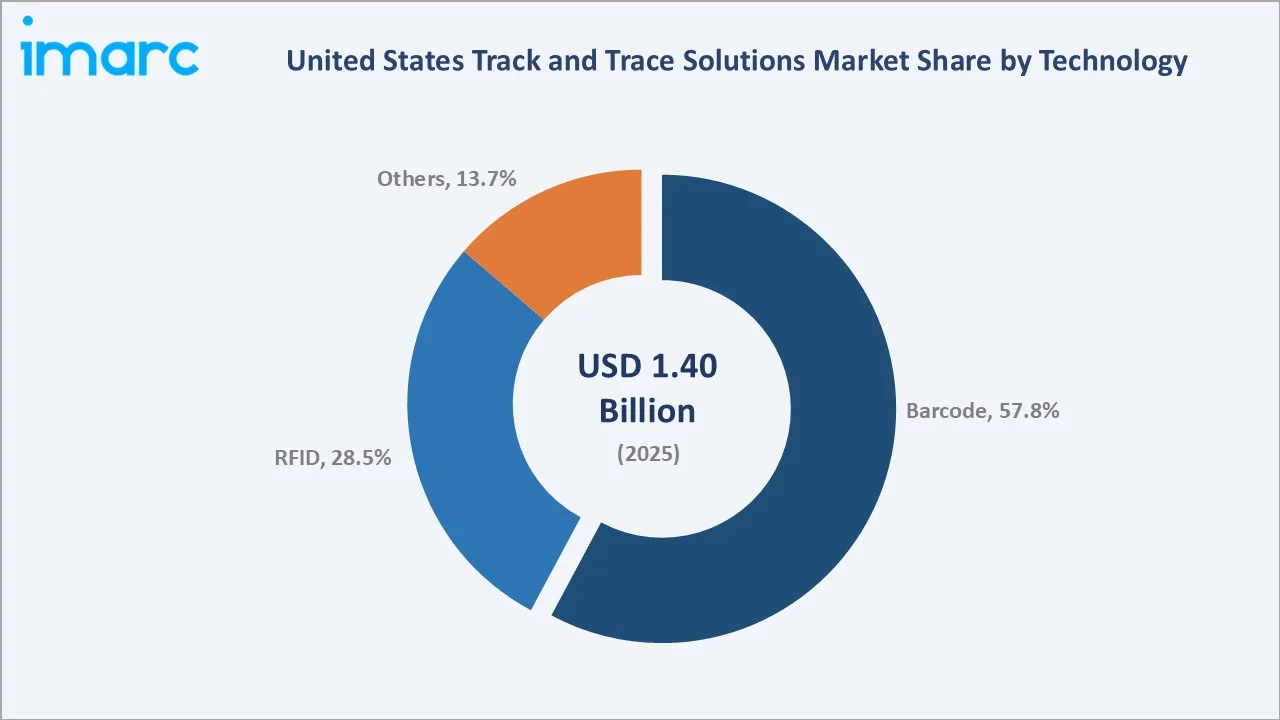

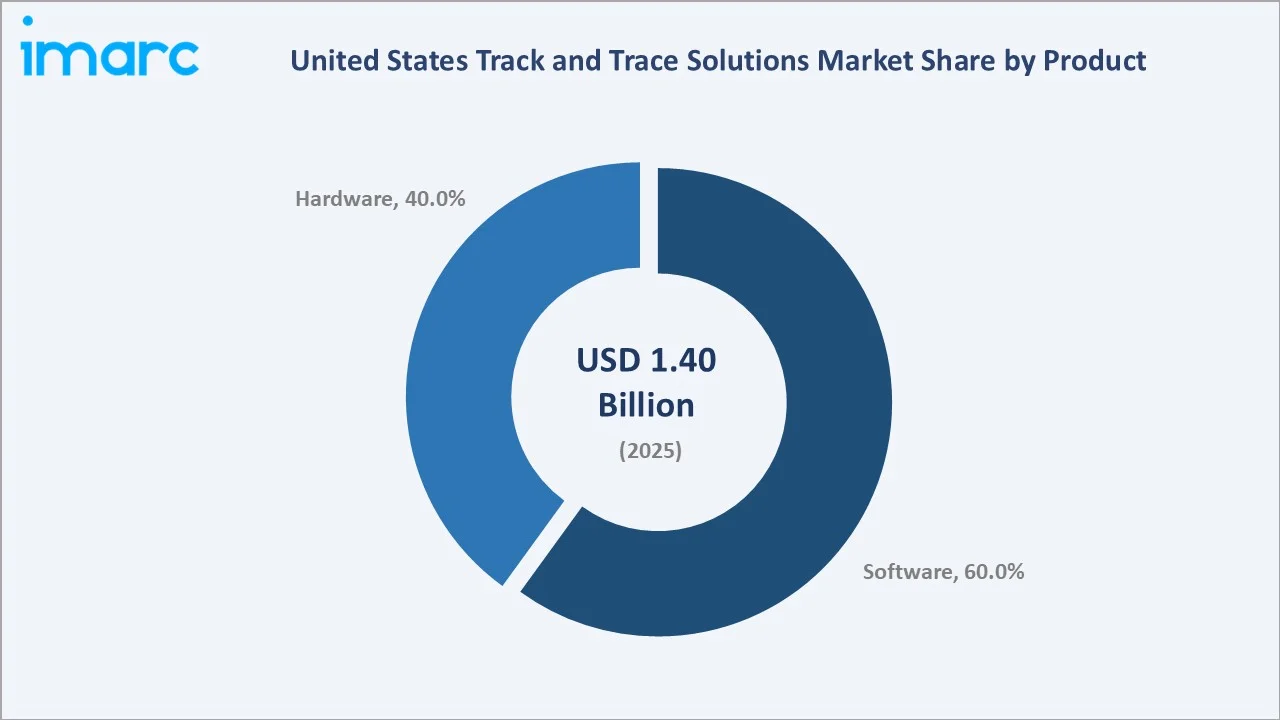

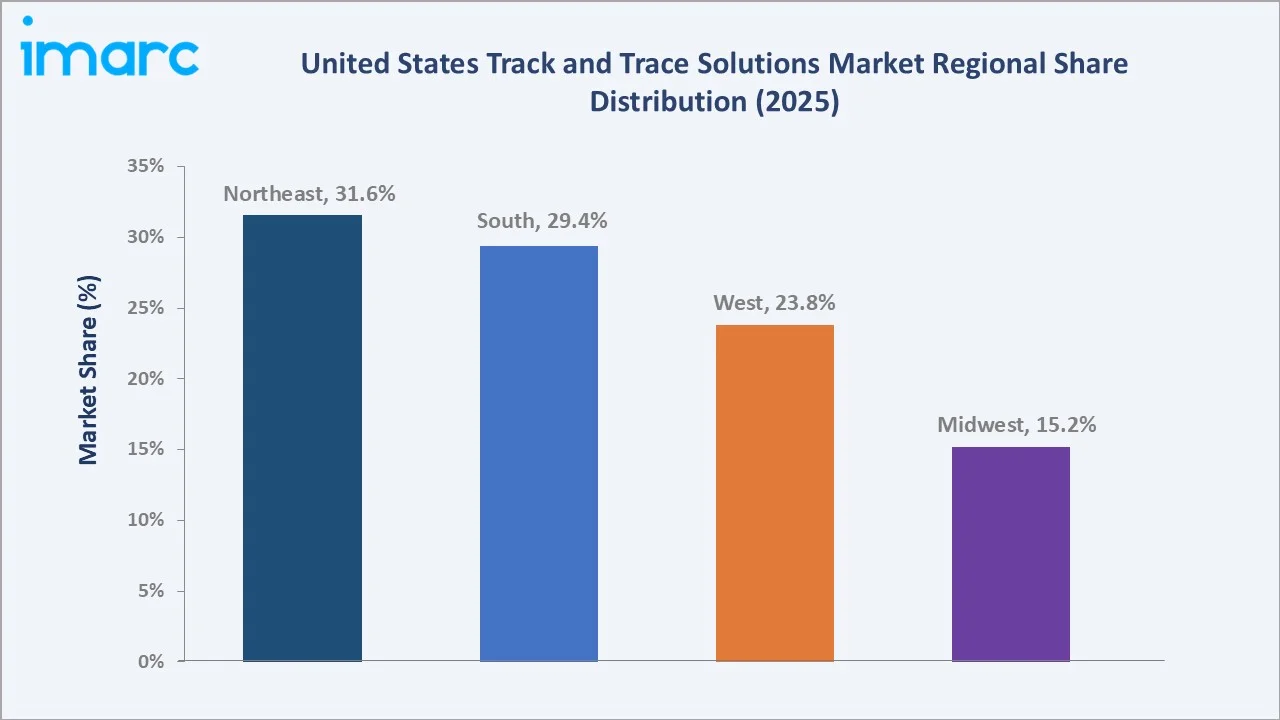

Barcode dominates technology at 57.83%, software leads product at 60.0%, and the Northeast commands 31.6% of the national market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.40 Billion |

|

Forecast Market Size (2034) |

USD 2.98 Billion |

|

CAGR (2026-2034) |

8.76% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Technology |

Barcode (57.83%, 2025) |

|

Dominant Product |

Software (60.0%, 2025) |

|

Leading Region |

Northeast (31.6%, 2025) |

To get more information on this market, Request Sample

The market grew from USD 0.92 Billion in 2020 to USD 1.40 Billion in 2025, anchored at USD 2.13 Billion in 2030 and forecast to reach USD 2.98 Billion by 2034. DSCSA enforcement timelines, FDA drug traceability mandates, and growing e-commerce logistics complexity sustained consistent demand growth throughout 2020-2025.

Executive Summary

The United States track and trace solutions market reached USD 1.40 Billion in 2025, driven by strict federal serialization mandates, expanding pharmaceutical and food safety regulations, and growing enterprise adoption of supply chain visibility platforms. The market is projected to reach USD 2.98 Billion by 2034.

Barcode technology at 57.83% dominates due to its widespread deployment across pharmaceutical, food & beverage, and logistics sectors. Software at 60.0% leads product demand as enterprises prioritise cloud-based serialization and aggregation management. The Northeast at 31.6% commands the largest regional share through its high concentration of pharmaceutical manufacturers and healthcare distributors.

Key Market Insights

|

Insight |

Data |

|

Dominant Technology |

Barcode – 57.83% share (2025) |

|

Dominant Product |

Software – 60.0% market share (2025) |

|

Leading Region |

Northeast – 31.6% market share (2025) |

|

Market Opportunity |

AI-powered traceability; IoT integration; blockchain-based serialization; cloud SaaS platforms |

Key Analytical Observations Supporting the Above Data:

- Barcode at 57.83%: Barcode remains the dominant technology due to its low deployment cost, universal compatibility with GS1 standards, and deep integration across pharmaceutical, retail, and food & beverage supply chains. DSCSA mandates require barcode-based serialization for all prescription drug packages, reinforcing segment dominance.

- Software at 60.0%: Software leads product demand as enterprise buyers shift from hardware-centric deployments to cloud-native serialization and aggregation platforms. SaaS-based track and trace solutions offer scalability, regulatory update flexibility, and real-time supply chain dashboards attractive to pharmaceutical and food companies.

- Northeast at 31.6%: The Northeast leads through its dense concentration of pharmaceutical manufacturers, major healthcare distributors, and biotech firms in states like New Jersey, New York, and Pennsylvania, generating the highest per-capita demand for DSCSA-compliant track and trace infrastructure.

United States Track and Trace Solutions Market Overview

The US track and trace solutions market encompasses hardware, software, and services enabling end-to-end product identification, serialization, aggregation, and supply chain monitoring. The ecosystem integrates barcode and RFID hardware manufacturers, serialization software vendors, system integrators, and regulatory compliance specialists.

Macroeconomic drivers include the Drug Supply Chain Security Act (DSCSA), FDA UDI regulations for medical devices, FSMA food traceability rules, and growing corporate investment in supply chain resilience. IoT connectivity, cloud platforms, and AI-based analytics are transforming traditional track and trace deployments.

Market Dynamics

To evaluate market opportunities, Request Sample

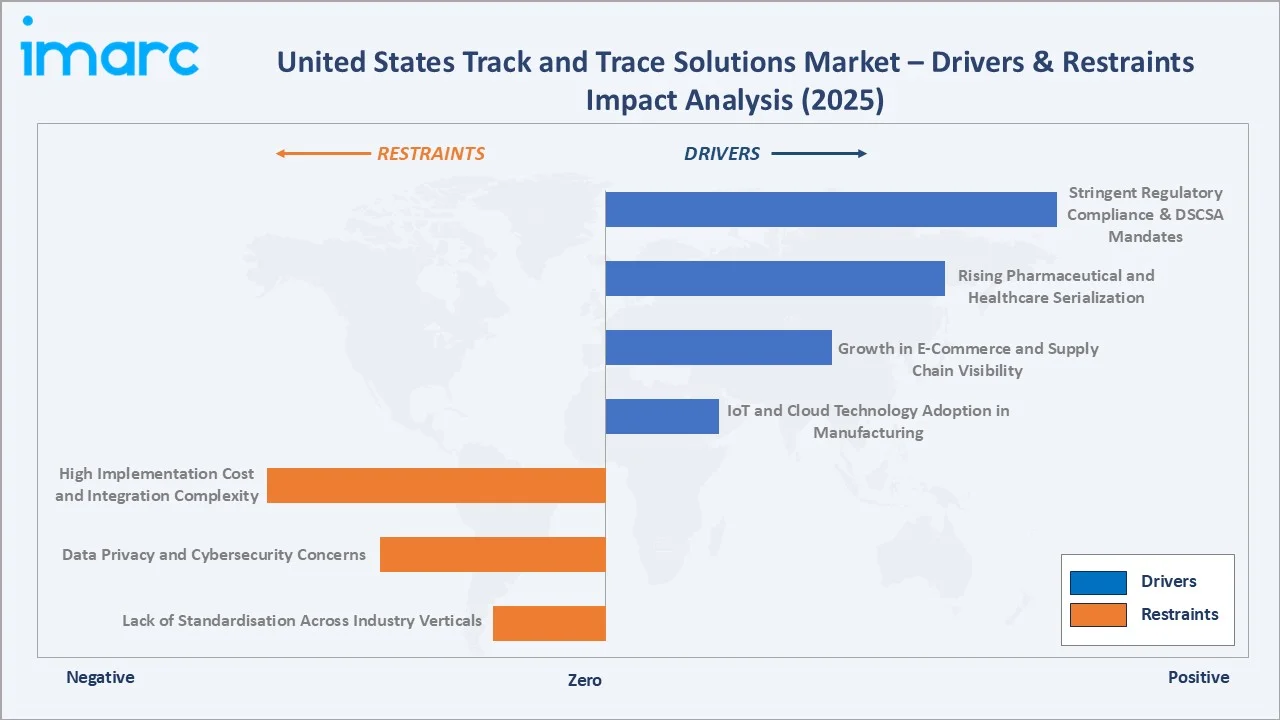

Market Drivers

- Stringent Regulatory Compliance & DSCSA Mandates: The Drug Supply Chain Security Act mandates serialization of all prescription drug packages by 2025, requiring pharmaceutical manufacturers and distributors to implement comprehensive track and trace systems. FDA enforcement creates non-negotiable procurement demand, driving sustained investment in both hardware and software track and trace infrastructure.

- Rising Pharmaceutical & Healthcare Serialization Demand: Growing pharmaceutical production volumes, complex multi-tier distribution networks, and counterfeit drug prevention requirements are accelerating serialization adoption. The US pharmaceutical market's scale ensures sustained hardware and software procurement as manufacturers upgrade legacy track and trace systems to meet DSCSA and FDA UDI compliance.

- Growth in E-Commerce & Supply Chain Visibility Needs: Rapid e-commerce expansion, last-mile logistics complexity, and consumer demand for real-time parcel tracking are driving enterprise investment in track and trace platforms. Retailers, logistics providers, and manufacturers are deploying IoT-connected serialization systems to achieve end-to-end supply chain visibility.

- IoT & Cloud Technology Adoption in Manufacturing: Increasing deployment of IoT sensors, cloud-based ERP integrations, and Industry 4.0 platforms in US manufacturing facilities is embedding track and trace capabilities into production workflows. Cloud-native SaaS serialization platforms reduce deployment cost and accelerate time-to-compliance for mid-market manufacturers.

Market Restraints

- High Implementation Cost & Integration Complexity: Full-scale track and trace deployments require substantial capital investment in hardware, software licences, system integration, and employee training. Legacy ERP and manufacturing execution system compatibility challenges increase implementation timelines and total cost, creating adoption barriers for small and mid-sized manufacturers.

- Data Privacy & Cybersecurity Concerns: Track and trace platforms aggregate sensitive product, supply chain, and transaction data across multiple enterprise systems, creating significant cybersecurity exposure. Data breach risks, proprietary supply chain information leakage, and compliance with state-level privacy regulations create operational caution among risk-averse enterprises.

- Lack of Standardisation Across Industry Verticals: Divergent serialization standards, data formats, and compliance requirements across pharmaceutical, food & beverage, medical device, and retail sectors increase solution complexity. Multi-industry manufacturers face duplication of effort and system proliferation when deploying track and trace across different end-use verticals.

Market Opportunities

- AI-Powered Traceability & Predictive Analytics: AI and machine learning integration with track and trace platforms enables predictive supply chain disruption detection, automated compliance reporting, and intelligent product recall management. Enterprise adoption of AI-driven traceability tools represents a high-value growth opportunity for solution vendors targeting regulated industries.

- Blockchain-Based Supply Chain Serialization: Distributed ledger technology offers tamper-proof product authentication and immutable serialization records across multi-party supply chains. Blockchain integration with existing track and trace platforms is emerging as a differentiating capability in pharmaceutical and food safety applications, creating new market segments.

Market Challenges

- Skilled Workforce Shortage for Implementation & Operations: Track and trace system deployment requires specialised expertise in serialization software, RFID integration, GS1 standards compliance, and regulatory frameworks. The shortage of certified implementation professionals and trained operations staff creates project delays and cost overruns, limiting deployment velocity.

- Rapid Technology Obsolescence & Version Management: Frequent software updates, evolving regulatory requirements, and hardware technology transitions create ongoing version management complexity. Enterprises face continuous investment cycles to maintain compliance and exploit new capabilities, creating total cost of ownership concerns that slow adoption decisions.

Emerging Market Trends

1. AI and Machine Learning Integration in Serialization Platforms

AI and ML capabilities are being embedded in track and trace software to automate compliance verification, detect counterfeit patterns, and optimise aggregation logic. Enterprise adopters report 30-40% reductions in compliance reporting time through AI-driven automation of DSCSA data exchange and FDA UDI submission workflows.

2. Cloud-Native SaaS Track and Trace Replacing On-Premises Deployments

Cloud-native serialization platforms are displacing legacy on-premises deployments as pharmaceutical and food companies prioritise regulatory update agility. SaaS platforms offer automatic compliance updates, multi-site scalability, and integration with ERP systems through pre-built APIs, reducing total implementation cost and regulatory risk.

3. RFID Adoption Accelerating in Pharmaceutical Distribution

RFID technology is gaining momentum in pharmaceutical distribution as costs decline and DSCSA's unit-level tracking requirements increase. Item-level RFID enables real-time inventory visibility, automated dispensing verification, and hospital-level product authentication, creating a high-growth RFID application segment within the broader track and trace market.

4. IoT-Connected Smart Packaging Enabling Real-Time Traceability

IoT-enabled smart packaging embedding NFC chips, temperature sensors, and GPS trackers is emerging as the next generation of track and trace infrastructure. Real-time condition monitoring during transport, automated cold chain compliance alerts, and consumer-facing product authentication are expanding the total addressable track and trace market.

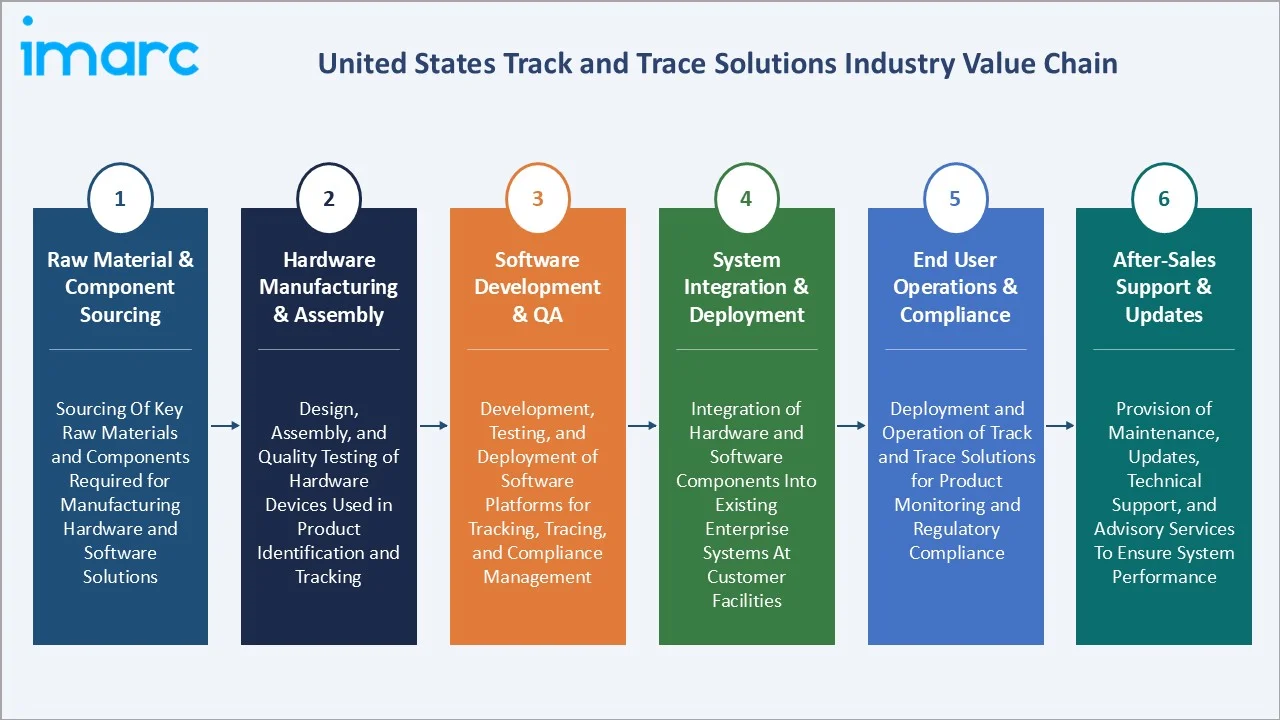

Industry Value Chain Analysis

The US track and trace solutions value chain integrates raw material sourcing, hardware manufacturing, software development, system integration, end-user deployment, and ongoing support. The ecosystem is progressively shifting toward integrated software-as-a-service models as enterprises prioritise compliance agility over hardware ownership.

|

Stage |

Key Participants |

|

Raw Material & Component Sourcing |

Sourcing of key raw materials and components required for manufacturing hardware and software solutions |

|

Hardware Manufacturing & Assembly |

Design, assembly, and quality testing of hardware devices used in product identification and tracking |

|

Software Development & QA |

Development, testing, and deployment of software platforms for tracking, tracing, and compliance management |

|

System Integration & Deployment |

Integration of hardware and software components into existing enterprise systems at customer facilities |

|

End User Operations & Compliance |

Deployment and operation of track and trace solutions to support product monitoring and regulatory compliance |

|

After-Sales Support & Updates |

Provision of maintenance, updates, technical support, and advisory services to ensure system performance |

The software development and system integration stages represent the highest value-add tiers of the US track and trace value chain. Vendor consolidation is accelerating as pharmaceutical-grade serialization platform providers acquire hardware and integration capabilities to offer end-to-end solutions.

Technology Landscape in the United States Track and Trace Solutions Industry

Barcode Technology

Barcode technology remains the foundational track and trace technology, underpinned by GS1-128 and 2D DataMatrix standards mandated by DSCSA and FDA UDI regulations. High-resolution printing, vision-based verification, and omnidirectional scanning capabilities make barcode the cost-effective standard for pharmaceutical and food packaging serialization.

RFID Technology

RFID technology enables non-line-of-sight, high-throughput item-level identification essential for pharmaceutical distribution and hospital-level tracking. Item-level UHF RFID adoption is accelerating as hardware costs decline and DSCSA unit-level tracking requirements create compliance-driven demand across pharmaceutical distribution networks.

IoT & Cloud Integration Technology

IoT sensor integration and cloud-based data management platforms are transforming track and trace from point-in-time serialization to continuous real-time supply chain monitoring. Cloud-native platforms enable multi-site aggregation management, automated regulatory reporting, and API-based integration with trading partner systems for end-to-end serialization data exchange.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Technology |

Barcode |

57.83% |

2025 |

|

Product |

Software |

60.0% |

2025 |

|

Application |

Serialization Solutions |

66.0% |

2025 |

|

End Use Industry |

Pharmaceutical |

26.85% |

2025 |

|

Region |

Northeast |

31.6% |

2025 |

By Technology

Barcode leads at 57.83% in 2025, capturing the highest volume of pharmaceutical, food & beverage, and retail serialization deployments driven by DSCSA and FDA UDI compliance mandates.

To access detailed market analysis, Request Sample

RFID at 28.47% is the fastest-growing technology segment, benefiting from declining hardware costs and expanding DSCSA unit-level tracking mandates in pharmaceutical distribution. Others at 13.70% include vision systems, NFC, and IoT-based traceability platforms gaining traction in specialised applications.

By Product

Software leads at 60.0% through enterprise adoption of cloud-native serialization, aggregation, and compliance management platforms driven by DSCSA and FDA UDI regulatory requirements across pharmaceutical and medical device manufacturers.

Hardware at 40.0% encompasses barcode printers, RFID readers, inspection systems, and labelling solutions. Growing pharmaceutical production volumes and RFID adoption are sustaining hardware demand as manufacturers upgrade legacy equipment to meet current compliance specifications.

Regional Market Insights

|

Region |

Share (2025) |

Key Drivers & Characteristics |

|

Northeast |

31.6% |

High demand driven by regulatory compliance requirements, industrial activity, and established supply chain infrastructure |

|

South |

29.4% |

Growing manufacturing base, expanding logistics networks, and increasing technology adoption driving market growth |

|

West |

23.8% |

Technology-driven adoption, strong innovation ecosystem, and regulatory compliance investments supporting market expansion |

|

Midwest |

15.2% |

Emerging manufacturing and distribution sector growth with increasing focus on supply chain visibility and compliance |

The Northeast leads at 31.6% through its high concentration of pharmaceutical manufacturers, specialty chemical producers, and major wholesale drug distributors in New Jersey, New York, and Pennsylvania, all subject to stringent DSCSA serialization compliance requirements generating sustained track and trace procurement.

The South at 29.4% benefits from growing pharmaceutical and food & beverage manufacturing in Texas, North Carolina, and Florida. RFID adoption in pharmaceutical distribution centres and FSMA-driven food traceability investments is accelerating the South region market growth through the forecast period.

The West at 23.8% is anchored by California's large biotech and medical device cluster, subject to FDA UDI regulations and California-specific drug serialization requirements. The Midwest at 15.2% is emerging as a growth market driven by FSMA food traceability mandates affecting its large food & beverage manufacturing base.

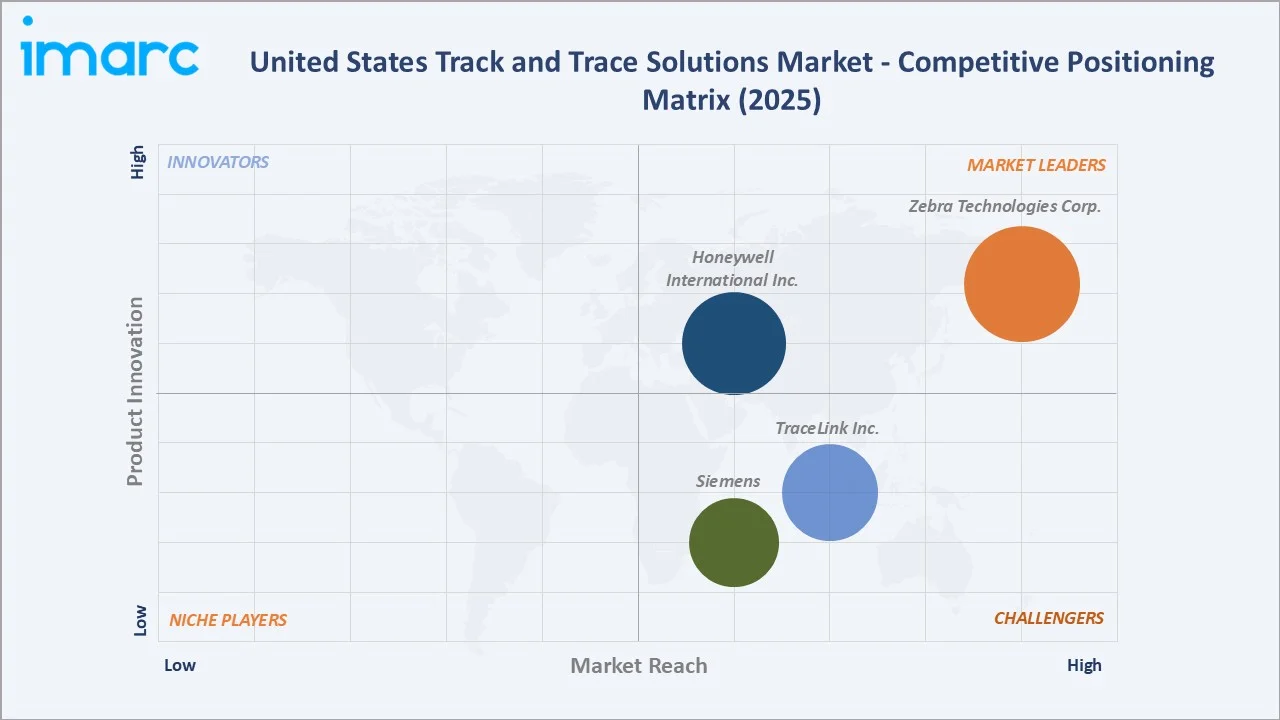

Competitive Landscape

The US track and trace solutions market competitive landscape is moderately concentrated, with global integrated technology providers, specialised serialization software vendors, and hardware-focused suppliers competing across pharmaceutical, food & beverage, and logistics verticals. Regulatory compliance expertise is the primary competitive differentiator.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

Zebra Technologies Corp. |

ZT600 Series Printers, DS Series Scanners, FX9600 RFID Reader |

Market Leader |

Broadest AIDC hardware portfolio; deep pharma and retail penetration |

|

Honeywell International Inc. |

Honeywell Track and Trace |

Market Leader |

Integrated hardware-software ecosystem; strong distribution network |

|

Siemens |

SIMATIC RF300 |

Strong Challenger |

Manufacturing execution system integration; pharmaceutical expertise |

|

TraceLink Inc. |

TraceLink Serialization, OPUS Platform |

Strong Challenger |

DSCSA-specialist SaaS platform; the largest pharma network reach |

Key players include Zebra Technologies Corp., Honeywell International Inc., Siemens, TraceLink Inc., and others.

Key Company Profiles

Zebra Technologies Corp.

Zebra Technologies is a US-based manufacturer of automatic identification and data capture (AIDC) solutions, headquartered in Lincolnshire, Illinois, with a dominant presence across pharmaceutical, retail, and logistics track and trace applications.

- Key Products: ZT600 Series Printers, DS Series Scanners, FX9600 RFID Reader

- Strategic Focus: Expanding integrated hardware-software AIDC portfolio for pharmaceutical and healthcare track and trace, leveraging the Elo acquisition to add self-service touchscreen capabilities across retail and healthcare end markets.

TraceLink Inc.

TraceLink is a US-based cloud-native supply chain serialization and traceability platform company, headquartered in Wilmington, Massachusetts, specialising in pharmaceutical-grade DSCSA compliance and multi-enterprise supply chain orchestration for regulated industries.

- Key Products: TraceLink Serialization, OPUS Platform

- Strategic Focus: Expanding OPUS platform adoption as the digital backbone for regulated pharmaceutical and life sciences value chains, emphasising multi-enterprise network effects, automated DSCSA data exchange, and AI-powered traceability analytics capabilities.

Market Concentration Analysis

The US track and trace solutions market is moderately concentrated at the enterprise serialization platform level, with the top 5 players collectively accounting for an estimated 55–65% of pharmaceutical and regulated industry track and trace revenue.

Market concentration is expected to increase moderately as SaaS platform network effects favour established multi-enterprise serialization networks. DSCSA enforcement creates winner-take-most dynamics in pharmaceutical serialization software, while hardware markets remain more fragmented through regional distribution channels.

Investment & Growth Opportunities

Highest Growth Segments

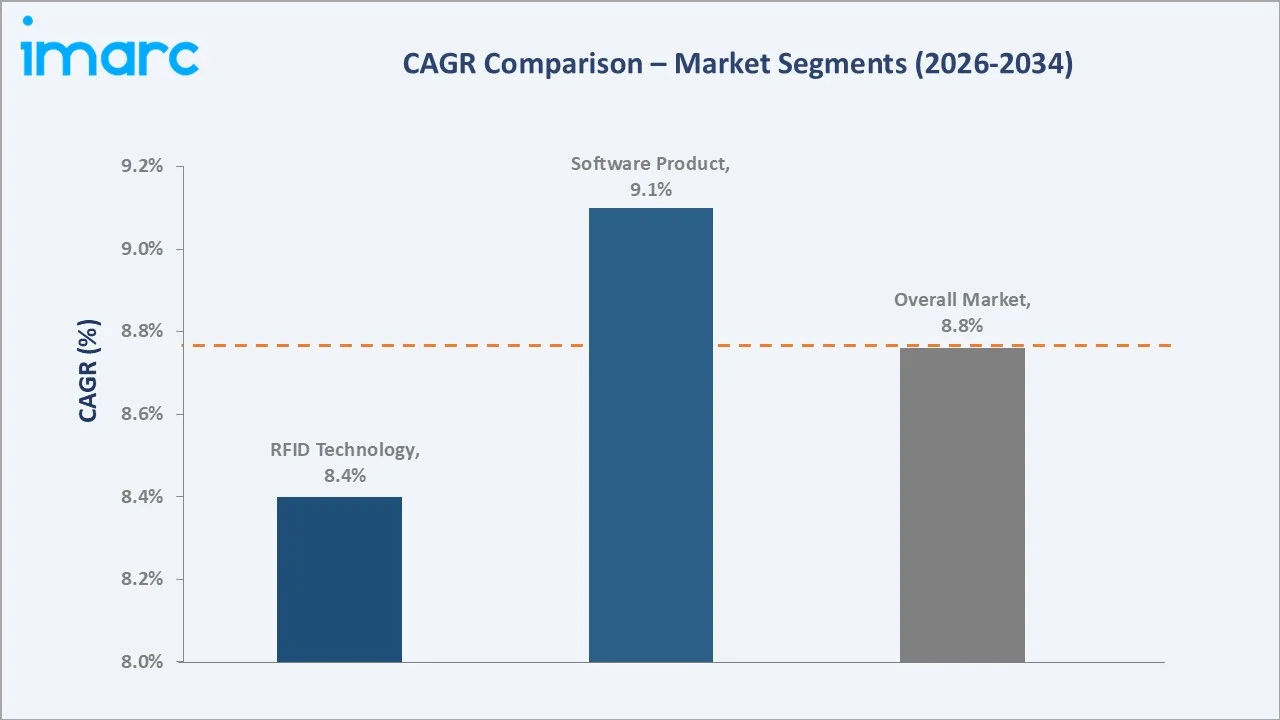

RFID technology (~10.5% CAGR), software products (~9.8% CAGR), AI-powered traceability platforms (~18%+ CAGR from emerging base), IoT smart packaging traceability (~15% CAGR), cloud-native SaaS serialization (~12% CAGR), and blockchain supply chain authentication (~20%+ CAGR from near-zero commercial base) represent the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

DSCSA unit-level pharmaceutical serialization represents the most policy-supported capital deployment opportunity in the US track and trace market. DSCSA 2025 enforcement, combined with FDA UDI medical device mandates and FSMA food traceability rules, creates a multi-regulatory demand floor that ensures sustained investment through the programmatic horizon.

Investment Themes

- AI-native serialization platforms for automated DSCSA compliance: AI-driven platforms automating DSCSA data exchange, compliance verification, and supply chain exception management create durable competitive advantages over rules-based serialization software, commanding 15-25% premium pricing in pharmaceutical procurement evaluations.

- RFID-as-a-Service for pharmaceutical distribution: RFID technology deployment through managed service models eliminates capital expenditure barriers for mid-size pharmaceutical distributors, creating a recurring revenue opportunity for hardware vendors and systems integrators targeting the USD 28.47% RFID market segment.

Future Market Outlook (2026-2034)

The US track and trace solutions market is projected to grow from USD 1.40 Billion in 2025 to USD 2.98 Billion by 2034, delivering an 8.76% CAGR. The market's growth is underpinned by DSCSA enforcement, FDA UDI expansion, FSMA food traceability rules, and enterprise investment in supply chain visibility and resilience.

Software will strengthen its dominance through cloud-native SaaS serialization platform adoption. RFID will grow its share as pharmaceutical unit-level tracking requirements expand. The Northeast will retain regional leadership while the South accelerates through food & beverage FSMA compliance investments and expanding pharmaceutical manufacturing.

Three structural forces define US track and trace market growth through 2034: the non-discretionary regulatory compliance mandate creating baseline demand across pharmaceutical and food industries; supply chain resilience investment accelerating enterprise track and trace adoption beyond compliance use cases; and AI and IoT integration expanding the total addressable market through new traceability applications.

Research Methodology

Primary Research

Primary research comprised structured interviews with 45+ industry stakeholders including pharmaceutical serialization managers, supply chain technology executives, FDA regulatory compliance specialists, RFID integration engineers, and enterprise software procurement directors conducted in 2025.

Secondary Research

Secondary research encompassed company annual reports, FDA DSCSA guidance documents, GS1 US standards publications, IMARC Group primary market data, industry association reports, and government regulatory publications. Over 55 secondary sources were reviewed across pharmaceutical, food safety, and technology domains.

Forecasting Models

Market revenue forecasts developed using a segmented bottom-up model: (i) pharmaceutical serialization compliance demand by DSCSA tier; (ii) non-pharmaceutical end-use adoption rates by vertical; (iii) average software and hardware spend per deployment; (iv) technology migration factors for barcode-to-RFID transition; (v) regional deployment weighting by manufacturing concentration.

United States Track and Trace Solutions Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Products Covered |

|

| Technologies Covered | Barcode, RFID, Others |

| Applications Covered |

|

| End Use Industries Covered | Pharmaceutical, Medical Device, Food and Beverages, Cosmetics, Others |

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered | Zebra Technologies Corp., Honeywell International Inc., Siemens, TraceLink Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the United States Track and Trace Solutions Market Report

The US track and trace solutions market reached USD 1.40 Billion in 2025, driven by DSCSA pharmaceutical serialization mandates, FDA UDI regulations, barcode technology dominance at 57.83%, and software product leadership at 60.0% across pharmaceutical, food & beverage, and medical device end-use industries.

The market grows at 8.76% CAGR during 2026-2034, reaching USD 2.98 Billion by 2034. Growth reflects DSCSA enforcement continuity, expanding RFID adoption, cloud-native SaaS platform proliferation, and AI integration creating new traceability applications beyond traditional compliance-driven deployments.

Barcode leads at 57.83%, capturing the highest volume of pharmaceutical and food & beverage serialization deployments mandated by DSCSA, FDA UDI, and FSMA regulations. Its low cost, GS1 standard compatibility, and universal deployment across US supply chains reinforce market dominance.

Software leads at 60.0% through cloud-native SaaS serialization and aggregation platform adoption driven by DSCSA compliance requirements, ERP integration demand, and enterprise preference for regulatory-update-agile solutions over hardware-centric deployments in pharmaceutical and food verticals.

The Northeast leads at 31.6% through its dense concentration of pharmaceutical manufacturers and major healthcare distributors in New Jersey, New York, and Pennsylvania, all subject to stringent DSCSA and FDA UDI compliance requirements generating the highest per-site track and trace procurement volumes.

Leading companies include Zebra Technologies Corp., Honeywell International Inc., Siemens, TraceLink Inc., and others.

The market is projected to reach approximately USD 2.13 Billion by 2030, supported by DSCSA unit-level tracking full enforcement, RFID pharmaceutical distribution expansion, AI-powered serialization platform adoption, and FSMA food traceability regulation driving food & beverage sector investments across all US regions.

Three priority opportunities: AI-native pharmaceutical serialization platforms capturing DSCSA compliance automation premium pricing; RFID-as-a-Service managed models for pharmaceutical distribution serving the 28.47% RFID market segment; and IoT smart packaging traceability creating new market applications beyond regulatory compliance use cases.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)