United States Weight Management Market Size, Share, Trends and Forecast by Diet, Equipment, Service, and Region, 2026-2034

United States Weight Management Market Size, Share, Trends & Forecast (2026-2034)

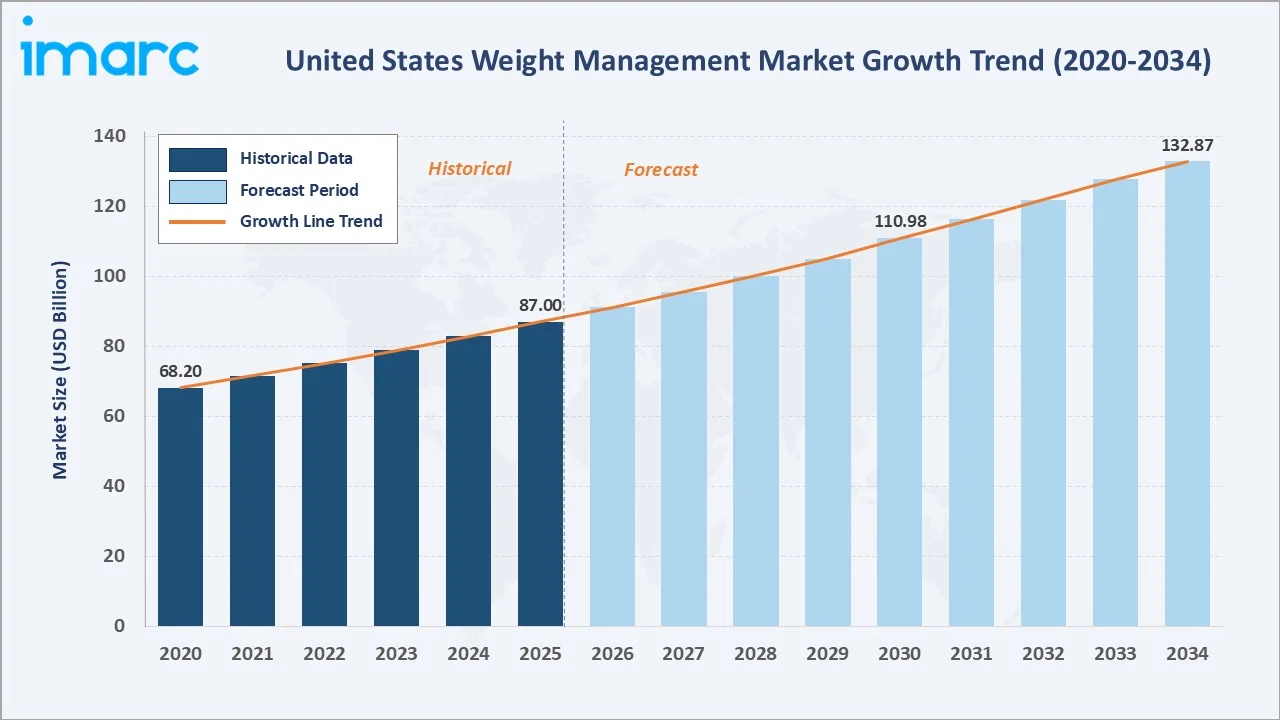

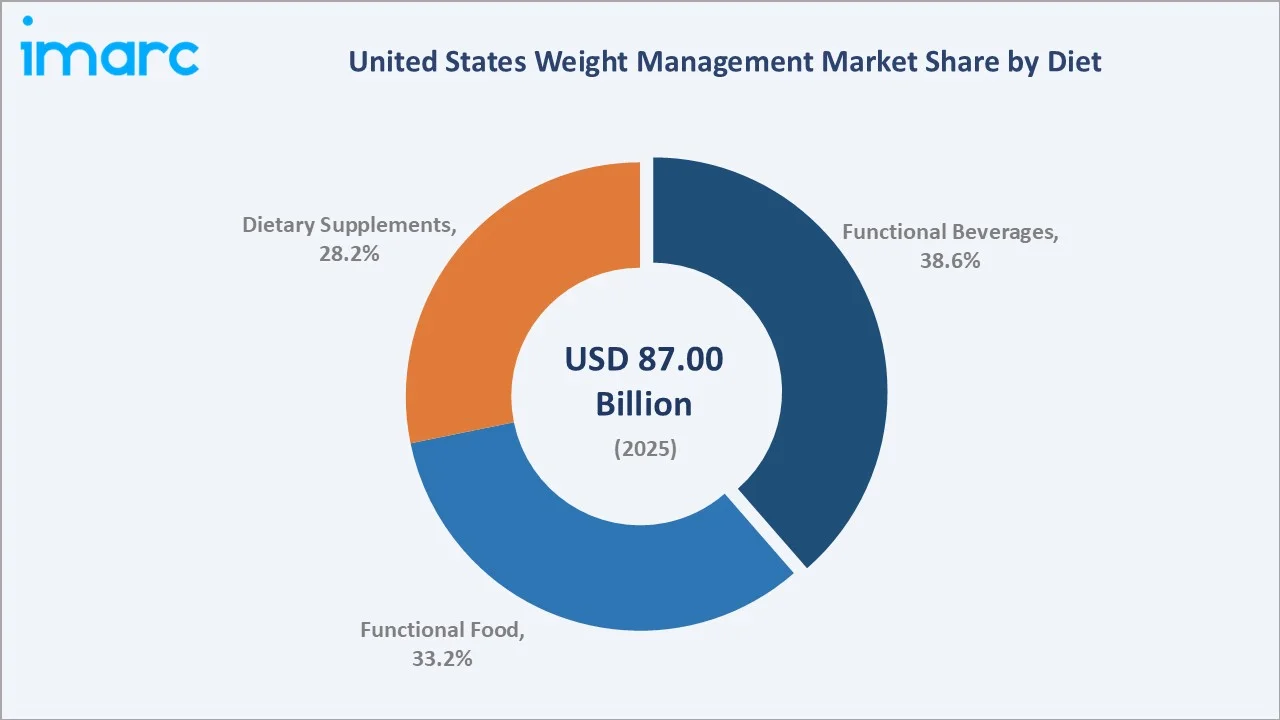

The United States weight management market size reached USD 87.00 Billion in 2025 and is projected to reach USD 132.87 Billion by 2034, exhibiting a CAGR of 4.99% during 2026-2034. Rising obesity prevalence, GLP-1 pharmaceutical interventions, and digital health expansion drive the market.

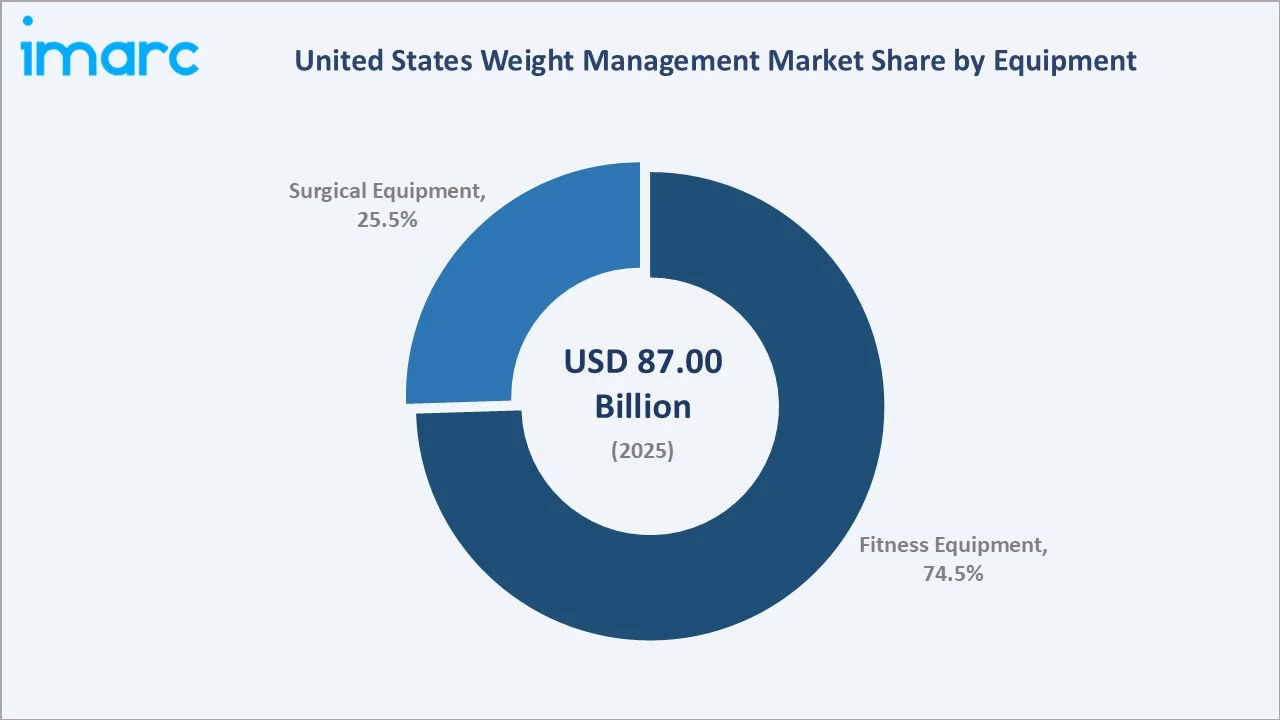

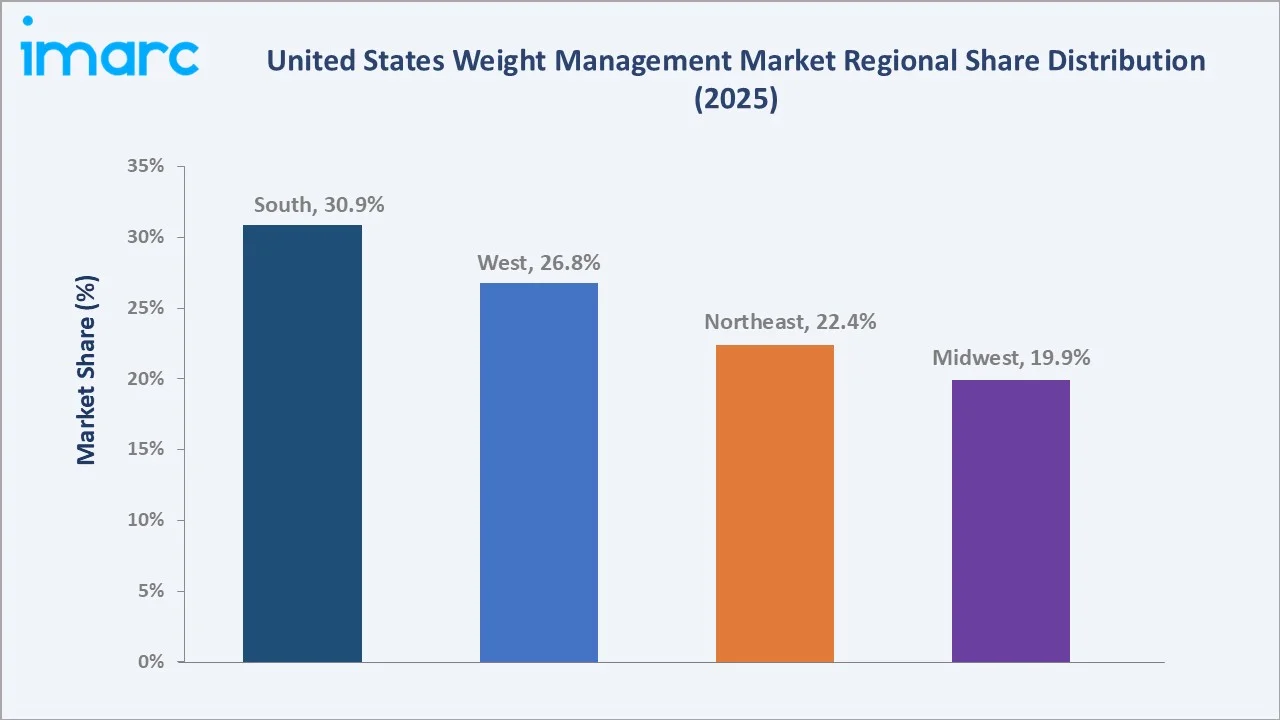

Fitness equipment dominates the equipment segment at 74.5% in 2025. Functional beverages lead the diet segment at 38.6%. The South commands a leading 30.9% regional share in 2025, anchored by high obesity prevalence across Texas, Florida, and Georgia metropolitan centers.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 87.00 Billion |

|

Forecast Market Size (2034) |

USD 132.87 Billion |

|

CAGR (2026-2034) |

4.99% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

South (30.9% share, 2025) |

|

Second Largest Region |

West (26.8% share, 2025) |

|

Leading Equipment Segment |

Fitness Equipment (74.5%, 2025) |

|

Leading Diet Segment |

Functional Beverages (38.6%, 2025) |

The growth trajectory from 2020 to 2034 reflects consistent non-discretionary demand. Historical expansion from USD 68.20 Billion (2020) to USD 87.00 Billion (2025) captures pandemic-driven fitness adoption. The forecast to USD 132.87 Billion captures accelerating pharmaceutical, digital, and clinical weight management investment.

To get more information on this market, Request Sample

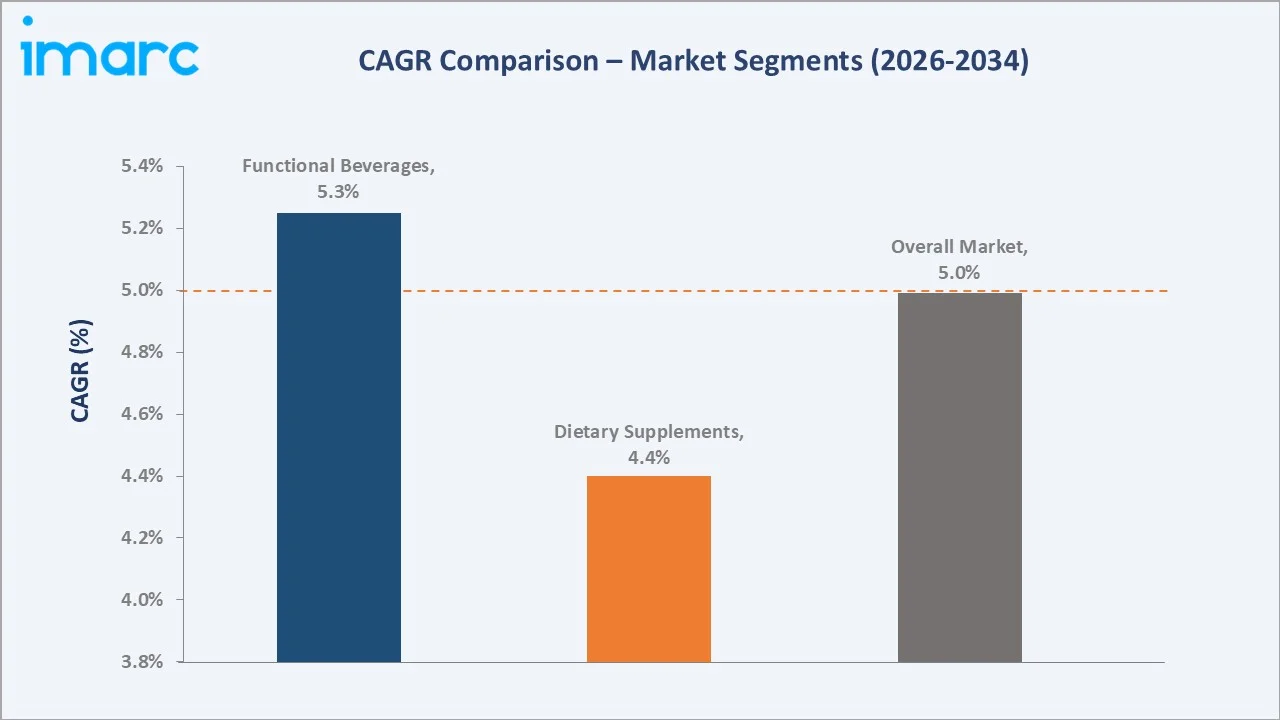

CAGR trajectories across equipment, diet, and regional sub-segments reveal surgical equipment at ~6.10% and functional beverages at ~5.25% as the fastest-growing categories within the US weight management industry through 2034, both outpacing the overall market CAGR of 4.99%.

Executive Summary

The United States weight management market is on a sustained growth path from USD 87.00 Billion in 2025 to USD 132.87 Billion by 2034. This market encompasses fitness equipment, dietary interventions, clinical surgical procedures, digital coaching, and pharmaceutical solutions targeting obesity and wellness.

Fitness equipment dominates the equipment segment at 74.5% in 2025, prpelled by connected fitness adoption and home gym investment. Surgical equipment at 25.5% serves growing bariatric procedure volumes. Functional beverages lead diet at 38.6%, followed by functional food at 33.2% and dietary supplements at 28.2%.

The South leads regionally with 30.9% share due to high obesity prevalence. The West (26.8%) benefits from health-conscious demographics. The Northeast (22.4%) and Midwest (19.9%) represent mature, steady-growth markets with strong employer wellness and health club infrastructure.

Key Market Insights

|

Insight |

Data |

|

Leading Equipment Segment |

Fitness Equipment – 74.5% share (2025) |

|

Fastest-Growing Equipment |

Surgical Equipment – ~6.1% CAGR (2034) |

|

Leading Diet Segment |

Functional Beverages – 38.6% share (2025) |

|

Second Diet Segment |

Functional Food – 33.2% share (2025) |

|

Third Diet Segment |

Dietary Supplements – 28.2% share (2025) |

|

Leading Region |

South – 30.9% revenue share (2025) |

|

Second Leading Region |

West – 26.8% revenue share (2025) |

|

Top Companies |

WW International, Inc., Medtronic, Abbott, Johnson & Johnson, The Simply Good Foods Company, Nutrisystem, LLC. |

Key Analytical Observations Supporting the Above Data:

- Fitness equipment at 74.5% dominates because connected fitness devices, cardiovascular machines, and AI-powered strength training systems have seen sustained investment. Employer wellness reimbursements and post-pandemic home gym culture ensure long-term category leadership through 2034.

- Functional beverages at 38.6% lead the diet segment due to convenience, portability, and strong retail distribution. Protein-enriched shakes, low-calorie meal replacements, and metabolism-supporting drinks span all demographic groups seeking on-the-go weight management support.

- Surgical equipment at 25.5% serves patients where lifestyle and pharmaceutical interventions prove insufficient. Next-generation laparoscopic and robotic bariatric surgical systems command high per-procedure revenue, driving ~6.1% CAGR as the fastest equipment growth segment through 2034.

- The South's 30.9% market leadership reflects the highest adult obesity rates in the US. CDC data identifies southeastern states, Mississippi, West Virginia, Alabama, and Arkansas, with over 40% adult obesity, generating concentrated demand for all weight management categories.

United States Weight Management Market Overview

The US weight management market integrates dietary solutions (functional foods, beverages, supplements), fitness and surgical equipment, digital health platforms, health club services, telehealth consultations, and pharmaceutical interventions. The market addresses obesity management, body composition improvement, chronic disease prevention, and aesthetic wellness goals.

The ecosystem spans raw material and ingredient suppliers, product manufacturers, distributors, retail and e-commerce channels, service providers (health clubs, surgical clinics, telehealth), insurance payers, and regulatory bodies (FDA, FTC, CDC). GLP-1 pharmaceutical companies form a powerful disruptive force reshaping demand across traditional diet and surgical segments.

Market Dynamics

To evaluate market opportunities, Request Sample

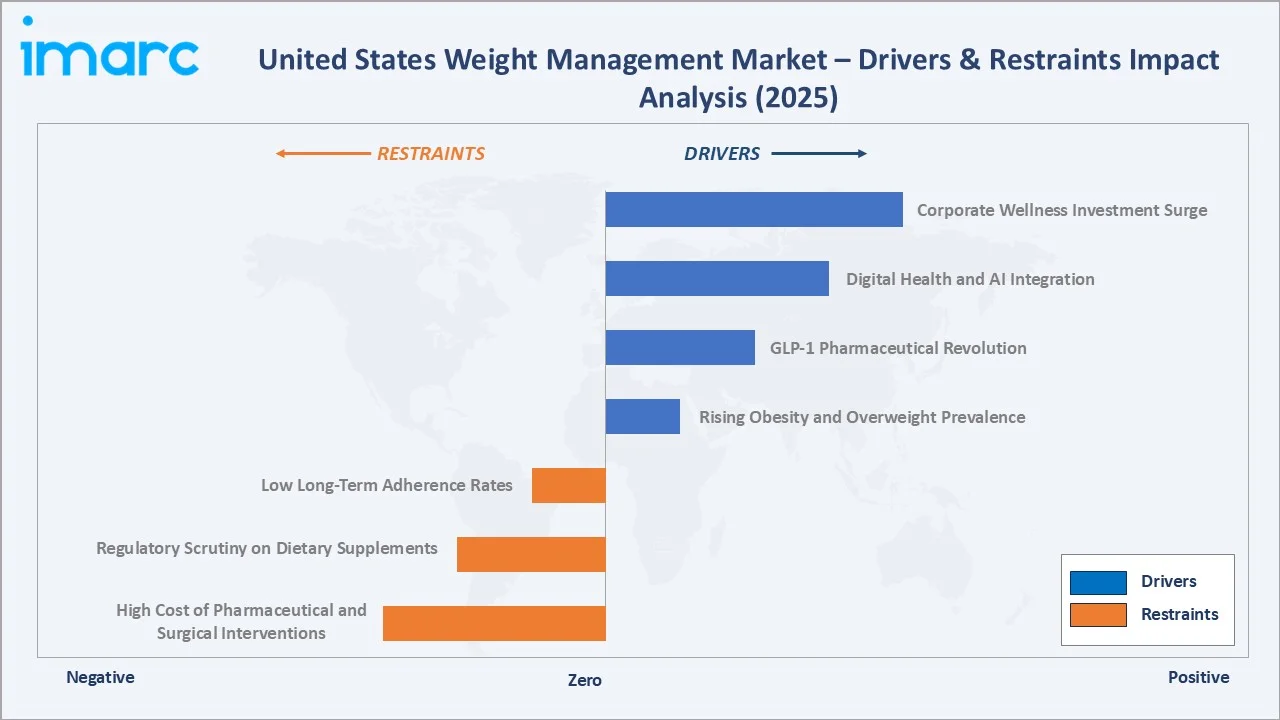

Market Drivers

- Rising Obesity and Overweight Prevalence: CDC data shows over 42% of US adults are classified as obese and 73.6% are overweight or obese, creating structural, non-discretionary demand for weight management solutions across pharmaceutical, fitness, dietary, and clinical channels nationwide.

- GLP-1 Pharmaceutical Revolution: Approved drugs including Wegovy, Ozempic, and Mounjaro demonstrate 10–20% body weight reduction in clinical trials, driving insurance coverage expansion, physician prescriptions, and adjacent demand for complementary nutrition and monitoring products across the ecosystem.

- Digital Health and AI Integration: Wearable devices, mobile nutrition apps, telehealth coaching, and AI-powered personalization platforms dramatically expand consumer engagement and program adherence, creating new subscription revenue streams and extending market reach beyond traditional gym and clinical channels.

- Corporate Wellness Investment Surge: Over 85% of large US employers now offer wellness benefits, creating substantial B2B demand for structured weight management solutions spanning fitness, nutrition, and digital health platforms, with employer-funded GLP-1 coverage expanding significantly since 2023.

Market Restraints

- High Cost of Pharmaceutical and Surgical Interventions: Advanced medical treatments, including drug therapies and surgical procedures, often involve substantial costs, which can limit accessibility for a broad patient population. Limited or inconsistent reimbursement coverage further restricts adoption, particularly among cost-sensitive groups, thereby constraining overall market expansion. This cost barrier also creates disparities in treatment access across different socioeconomic groups and regions. As a result, stakeholders are increasingly exploring more affordable, scalable alternatives and value-based care models to improve accessibility and drive wider adoption.

- Regulatory Scrutiny on Dietary Supplements: FDA and FTC enforcement actions against unsubstantiated weight loss claims restrict marketing language, product launches, and distribution of non-compliant thermogenic and fat-burning supplement formulations in the increasingly competitive diet category.

- Low Long-Term Adherence Rates: Clinical studies indicate 80–90% of dieters regain lost weight within 2–5 years. High program dropout rates reduce customer lifetime value for commercial weight loss programs and undermine evidence needed for expanded medical reimbursement approvals.

Market Opportunities

- GLP-1 Companion Nutrition and Services: With 24 million projected GLP-1 users in the US by 2035, demand for protein supplementation, muscle-preservation nutrition, micronutrient monitoring, and behavioral coaching represents a high-value emerging opportunity for established nutrition companies.

- Precision Nutrition and Biomarker-Based Solutions: Continuous glucose monitoring, metabolomics, and genetic testing are enabling truly personalized dietary recommendations. Companies offering data-driven, individualized weight management protocols command premium pricing and higher subscription retention.

Market Challenges

- Market Fragmentation and Intense Competition: The weight management supplement market is highly fragmented, with numerous brands competing for consumer attention. This fragmentation intensifies price competition, raises customer acquisition costs, and makes it challenging for companies to stand out. As a result, sustained differentiation increasingly depends on investments in clinical validation, strong brand positioning, and product innovation.

- GLP-1 Disruption of Traditional Segments: Pharmaceutical interventions are displacing demand for traditional meal replacement programs and some commercial diet plans. Companies must adapt their value propositions to complement rather than compete with prescription weight loss medications.

Emerging Market Trends

1. GLP-1 Medication Integration Reshaping Commercial Weight Management

Pharmaceutical and digital weight management companies are integrating GLP-1 prescription management into their service platforms. Noom's January 2025 GLP-1 Companion App update with AI-powered meal planning reflects industry-wide convergence toward medication management combined with behavioral coaching.

2. AI-Powered Personalization Elevating Program Efficacy

Artificial intelligence is enabling hyper-personalized nutrition plans, real-time adaptive coaching, and predictive relapse prevention. AI platforms simultaneously analyzing sleep, activity, nutrition, and biomarker data deliver measurably superior outcomes, driving premium subscription pricing and employer contract wins.

3. Connected Fitness Technology Sustaining Home Gym Investment

Smart gym equipment with embedded biometric tracking, live instructor streaming, and performance analytics extends the home fitness category beyond pandemic demand. Subscription-based content models generate recurring revenue streams that stabilize equipment manufacturers against hardware commodity cycle pressures.

4. Employer and Payer-Funded Weight Management Expansion

Growing insurance coverage for GLP-1 medications and bariatric procedures, combined with employer wellness investment, is institutionalizing weight management as a mainstream healthcare benefit, reducing consumer cost barriers and accelerating sustainable market growth across all product segments.

Industry Value Chain Analysis

The US weight management value chain spans six stages from raw material supply through consumer engagement. Product R&D, manufacturing, and integrated digital service delivery capture the highest value-added margins. Regulatory compliance and insurance reimbursement frameworks significantly influence value capture at each stage.

|

Stage |

Key Players / Examples |

|

Raw Material & Ingredient Supply |

Botanical extract suppliers, protein concentrate producers, equipment component manufacturers, chemical raw material distributors |

|

Product R&D & Manufacturing |

Nutrition product formulators, fitness equipment OEMs, pharmaceutical manufacturers, contract manufacturing organizations (CMOs) |

|

Packaging & Quality Testing |

Contract packaging providers, cGMP-certified testing laboratories, FDA regulatory consultants, quality assurance specialists |

|

Distribution & Retail / E-commerce |

Health and wellness specialty retailers, national pharmacy chains, mass merchandisers, direct-to-consumer e-commerce platforms |

|

Service Delivery (Clubs, Clinics) |

Fitness club operators, bariatric surgical centers, hospital-based weight management programs, telehealth service providers |

|

Consumer Engagement & Outcomes |

Digital health app developers, behavioral coaching platforms, wearable device integrators, corporate wellness program administrators |

Integrated companies with proprietary digital platforms and pharmaceutical partnerships achieve superior margins. Companies combining GLP-1 medication management, nutrition coaching, and fitness tracking in unified subscription offerings demonstrate the highest customer lifetime values and lowest churn rates across the market.

Technology Landscape in the US Weight Management Industry

Connected Fitness and Wearable Technology

Smart fitness equipment with biometric sensors, AI coaching algorithms, and cloud connectivity forms the core technology frontier. Heart rate monitoring, calorie tracking, and real-time instructor feedback through connected platforms are standard features driving the fitness equipment growth trajectory through 2034.

GLP-1 Drug Delivery and Monitoring Technology

Pharmaceutical advances include oral GLP-1 formulations, improved auto-injector devices, and combination therapies. Digital prescription platforms, remote monitoring, and AI-based adherence management tools are reducing clinical friction and expanding pharmaceutical weight management access across diverse patient populations.

Nutrigenomics and Precision Nutrition Platforms

DNA-based dietary recommendation platforms, continuous glucose monitors, and microbiome analysis services enable evidence-based personalized nutrition at scale. Multi-omic data platforms optimize dietary interventions, positioning precision nutrition as a premium high-growth segment within the broader weight management market.

AI and Behavioral Change Technology

Conversational AI coaches, computer vision food logging, and predictive behavioral analytics platforms transform user engagement. Machine learning algorithms identifying dropout risk in advance enable proactive interventions that measurably improve long-term adherence and clinical outcomes across all program types.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Diet | Functional Beverages | 38.6% | 2025 |

| Equipment | Fitness | 74.5% | 2025 |

| Service | Online Weight Loss Services | 🔒 | 2025 |

| Region | South | 30.9% | 2025 |

By Equipment

Fitness equipment commands a 74.5% majority share in 2025, driven by broad consumer investment in cardiovascular machines, strength training systems, and connected fitness devices. Post-pandemic home exercise normalization, employer wellness benefits, and smart gym equipment adoption sustain fitness segment dominance across all US consumer demographics.

To access detailed market analysis, Request Sample

Surgical equipment at 25.5% in 2025 serves clinical bariatric intervention needs. Growing at the fastest equipment CAGR of ~6.1% through 2034, surgical systems serve patients where lifestyle and pharmaceutical interventions are insufficient. High per-procedure revenue and consistent institutional demand underpin strong forecast growth.

By Diet

Functional beverages lead the diet segment at 38.6% in 2025, driven by consumer demand for convenient, portable nutrition solutions supporting weight management goals. Protein shakes, meal replacement beverages, appetite-suppressing functional waters, and metabolism-boosting drinks span retail, e-commerce, and DTC channels with strong recurring purchase behavior.

Functional food at 33.2% encompasses fortified meal replacements, high protein packaged foods, low-calorie structured diet programs, and medical nutrition products. Dietary supplements at 28.2% include thermogenic fat burners, appetite suppressants, fiber supplements, and protein powders, growing steadily as consumers seek pharmaceutical-adjacent solutions.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

South |

30.9% |

Highest US obesity rates; TX, FL, GA metro expansion; large population base; fitness infrastructure growth |

|

West |

26.8% |

Health-conscious CA demographics; premium wellness spending; tech-enabled digital health adoption; DTC brands |

|

Northeast |

22.4% |

High income levels; dense urban gym market; corporate wellness programs; telehealth penetration; clinical focus |

|

Midwest |

19.9% |

Rising obesity awareness; growing fitness club network; employer wellness program adoption; supplement retail growth |

The South's 30.9% market leadership reflects the structural reality of the highest adult obesity prevalence in the US. CDC data identifies southeastern states with over 40% adult obesity rates, generating concentrated demand for clinical, pharmaceutical, and dietary weight management interventions across both urban and rural settings.

The West, with 26.8% in 2025, benefits from California's health-conscious consumer culture, premium wellness spending capacity, and technology-driven digital health adoption. Silicon Valley investment in weight management technology startups and strong DTC e-commerce infrastructure give the West disproportionate innovation and market premium leadership.

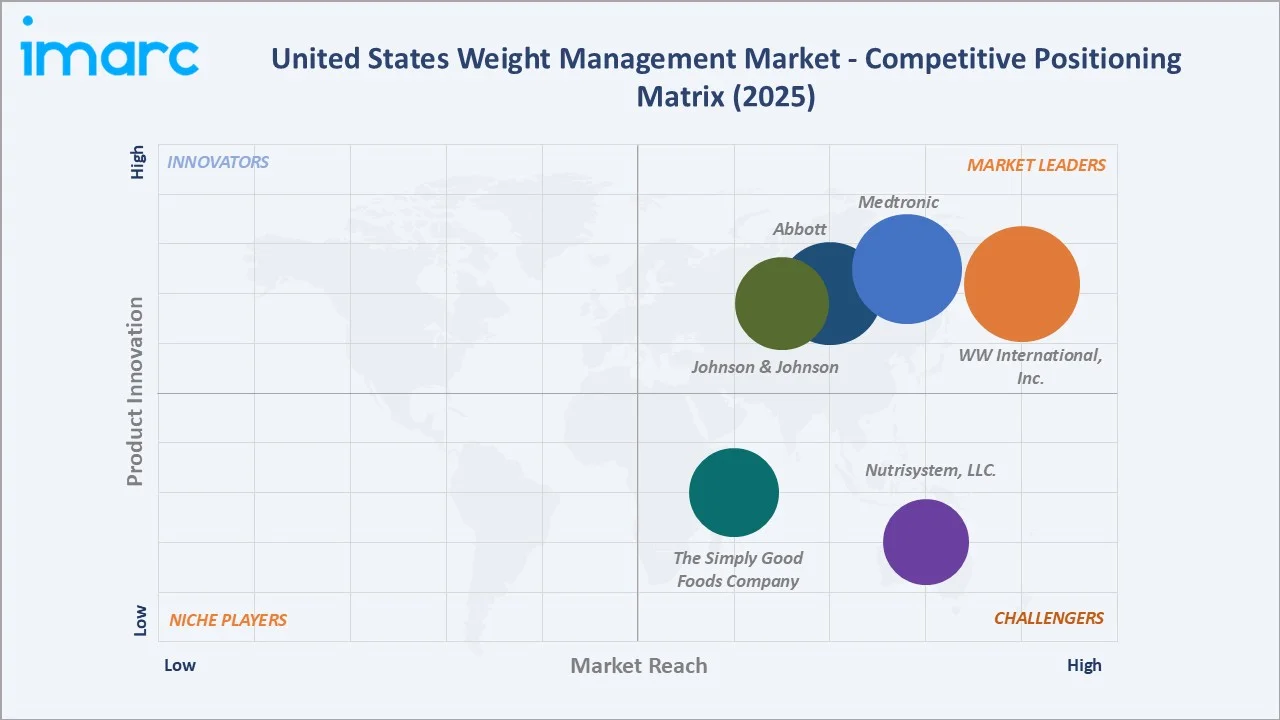

Competitive Landscape

The US weight management market is moderately fragmented across product, equipment, and service segments. Pharmaceutical entrants have introduced disruptive competition, while established commercial programs, fitness equipment makers, and nutrition companies are repositioning to complement or integrate with GLP-1 pharmaceutical offerings.

|

Company Name |

Key Products |

Market Position |

Strategic Focus |

|

WW International , Inc. |

WW App, GLP-1 companion, Points |

Leader |

Digital transformation; GLP-1 integration; clinical expansion |

|

Medtronic |

Surgical obesity devices, robotic bariatric platforms |

Leader |

Minimally invasive bariatric surgery; hospital system integration |

|

Abbott |

Ensure |

Leader |

Clinical nutrition; medical devices; continuous glucose monitoring |

|

Johnson & Johnson |

Ethicon products (staplers, energy devices) |

Leader |

Surgical platform; hospital procurement; procedure volume growth |

|

The Simply Good Foods Company |

Quest protein bars, OWYN |

Challenger |

Low-carb nutrition; e-commerce growth; protein demand capture |

|

Nutrisystem, LLC. |

Mealplans, telehealth coaching |

Challenger |

Subscription meal delivery; telehealth integration; digital coaching |

Key players include WW International, Inc., Medtronic, Abbott, Johnson & Johnson, The Simply Good Foods Company, Nutrisystem, LLC., and others.

Key Company Profiles

WW International Inc.

WW International Inc. is the United States' most recognized commercial weight management program operator, headquartered in New York. The company has evolved from a points-based diet program into an integrated digital health platform combining nutrition coaching, behavioral change tools, and GLP-1 companion program management.

- Product Portfolio: WW App, Points dietary program, GLP-1 Companion app with AI meal planning, clinical weight management services, WW-branded food products and cookbooks.

- Recent Developments: In December 2025, WW International introduced a fully integrated digital platform designed for the evolving GLP-1 weight management landscape, combining medical treatment with personalized lifestyle support. The platform brings together access to GLP-1 prescriptions, tailored nutrition plans, behavioral coaching, and community engagement within a unified app-based experience.

- Strategic Focus: WW's strategy pivots from subscription diet coaching toward comprehensive clinical weight management, integrating pharmaceutical access, behavioral science, and nutrition services. Investment in telehealth and GLP-1 companion programming aims to retain relevance among consumers pursuing pharmaceutical-assisted weight loss.

Medtronic

Medtronic is a global medical device company with deep expertise in minimally invasive surgical technologies relevant to bariatric and obesity management. With primary US operations in Minneapolis, Medtronic's surgical instruments and robotic-assisted platforms serve bariatric surgery centers and hospital systems nationwide.

- Product Portfolio: Hugo robotic-assisted surgery platform, surgical stapling systems, endoscopic tools, and laparoscopic instruments supporting sleeve gastrectomy, gastric bypass, and adjustable gastric band procedures.

- Recent Developments: In June 2023, Medtronic entered a collaboration with Allurion Technologies to expand access to AI-enabled weight management solutions across key international markets. Under the agreement, Medtronic leveraged its established distribution network to offer Allurion’s non-invasive gastric balloon system and its AI-powered digital care platform to healthcare providers in the Central and Eastern Europe, Middle East, and Africa region.

- Strategic Focus: Medtronic's obesity strategy leverages its leadership in minimally invasive surgical technologies to capture growing bariatric procedure volumes, targeting patients for whom pharmaceutical GLP-1 interventions are contraindicated or have proven clinically insufficient.

The Simply Good Foods Company

The Simply Good Foods Company, headquartered in Denver, Colorado, operates the Quest Nutrition and Atkins brands. The company targets health-conscious and weight management-focused consumers through high-protein, low-carbohydrate nutritional products sold across mass retail, specialty health stores, and e-commerce channels.

- Product Portfolio: OWYN, Quest protein bars, Quest protein chips, Quest cookies and snacks, Atkins meal replacement shakes, Atkins snack bars, and Atkins frozen meal products across multiple retail channels.

- Recent Developments: In June 2024, The Simply Good Foods Company completed its acquisition of Only What You Need (OWYN), a plant-based ready-to-drink protein shake brand, as part of its strategy to expand within the nutritious snacking category. The addition of OWYN strengthens the company’s portfolio by introducing a complementary brand and increasing its presence in the fast-growing ready-to-drink protein segment, while also enabling access to a broader and more diverse consumer base.

- Strategic Focus: Simply Good Foods focuses on growing high-velocity retail distribution, expanding Quest into beverages and hot food formats, and leveraging elevated protein demand from the GLP-1 era to position its brands as preferred nutritional companions for pharmaceutical weight loss users.

Market Concentration Analysis

The US weight management market exhibits moderate fragmentation at the overall category level and significant concentration within individual segments. Commercial diet programs, fitness equipment manufacturers, and GLP-1 pharmaceutical companies each display oligopolistic structures despite overall market diversity across product and service categories.

Consolidation through M&A is active: PE-backed fitness club operators are acquiring regional chains, nutrition companies are acquiring digital coaching platforms, and pharmaceutical companies are building integrated weight management service ecosystems around their GLP-1 drug franchises, creating new competitive advantages through 2034.

Investment & Growth Opportunities

Fastest-Growing Segments

Surgical equipment at ~6.1% CAGR through 2034 leads equipment growth, driven by complex obesity cases requiring clinical intervention and next-generation minimally invasive bariatric device innovation. Functional beverages at ~5.25% CAGR benefit from mass-market distribution, convenience positioning, and strong e-commerce channel acceleration.

Emerging Opportunities

GLP-1 companion nutrition and monitoring services represent the most significant emerging opportunity. With 24 million projected GLP-1 users by 2035, demand for protein supplementation, micronutrient monitoring, and behavioral coaching creates a high-value adjacent market for companies with clinical nutrition expertise and digital engagement capabilities.

Employer and insurer channel expansion offers substantial volume opportunity. Over 160 million Americans receive health insurance through employers, and weight management coverage is expanding as payers recognize ROI from obesity intervention. Companies with proven clinical outcomes and employer contracting capabilities will benefit most.

Venture & Investment Trends

VC and PE investment in digital weight management technology exceeded USD 2 Billion in 2023–2024. Precision nutrition platforms, AI behavioral coaching tools, and GLP-1 companion app companies attracted the largest funding rounds. Strategic M&A by pharmaceutical companies building integrated obesity management ecosystems is the dominant value creation theme.

Future Market Outlook (2026-2034)

The US weight management market is forecast to expand from USD 87.00 Billion in 2025 to USD 132.87 Billion by 2034 at a CAGR of 4.99%, adding USD 45.87 Billion in incremental annual value over the forecast period, driven by GLP-1 pharmaceutical expansion, digital health scaling, and broadening clinical coverage.

Three technology forces will shape the industry through 2034. First, next-generation oral GLP-1 medications will dramatically expand pharmaceutical accessibility, widening the addressable population. Second, continuous biomarker monitoring with AI-driven coaching will enable truly personalized intervention at scale for millions of consumers.

Third, employer and payer-funded integrated wellness programs combining pharmaceutical access, nutrition support, and behavioral coaching will institutionalize weight management as a mainstream healthcare benefit, reducing consumer cost barriers and accelerating sustainable market growth across all product and service segments.

Research Methodology

Primary Research

Primary research encompassed over 50 structured interviews with US weight management industry stakeholders, including commercial program operators, bariatric surgery directors, fitness equipment manufacturers, registered dietitians, insurance reimbursement specialists, and digital health platform executives, validating market sizing and segment shares.

Secondary Research

Key secondary sources include CDC National Health and Nutrition Examination Survey (NHANES), FDA medical device and drug approval databases, CMS healthcare expenditure data, IRI retail measurement services, IBISWorld industry reports, NIH obesity statistics, and trade publications including Nutritional Outlook, IDEA Health & Fitness, and Digital Health Today.

Forecasting Models

Market size estimations used bottom-up and top-down forecasting models incorporating US GDP growth rates, obesity prevalence trends, health insurance coverage data, pharmaceutical market penetration projections, and historical segment growth patterns. Scenario analysis (base, optimistic, conservative cases) accounts for GLP-1 adoption rate uncertainty.

United States Weight Management Market Report Coverage

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Diets Covered | Functional Beverages, Functional Food, Dietary Supplements |

| Equipments Covered | Fitness, Surgical |

| Services Covered | Health Clubs, Consultation Services, Online Weight Loss Services |

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered | WW International, Inc., Medtronic, Abbott, Johnson & Johnson, The Simply Good Foods Company, Nutrisystem, LLC., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the United States Weight Management Market Report

The United States weight management market size reached USD 87.00 Billion in 2025, driven by rising obesity prevalence, digital health expansion, and growing demand for GLP-1 pharmaceutical interventions.

The United States weight management market is projected to reach USD 132.87 Billion by 2034, representing an incremental addition of USD 45.87 Billion over the 2026-2034 forecast period.

The United States weight management market will exhibit a compound annual growth rate (CAGR) of 4.99% during the forecast period 2026-2034.

Fitness equipment leads the equipment segment with a 74.5% share in 2025, driven by connected fitness device adoption, home gym investment, and employer wellness program integration.

Surgical equipment accounts for 25.5% of the equipment segment in 2025, growing at the fastest equipment CAGR of approximately 6.1% through 2034 due to rising bariatric procedure volumes.

Functional beverages lead the diet segment with a 38.6% share in 2025, followed by functional food at 33.2% and dietary supplements at 28.2%, reflecting consumer preference for convenient nutritional solutions.

The South region leads with a 30.9% revenue share in 2025, driven by the highest adult obesity prevalence rates in the country and expanding fitness and healthcare infrastructure across Texas, Florida, and Georgia.

Key players include WW International, Inc., Medtronic, Abbott, Johnson & Johnson, The Simply Good Foods Company, Nutrisystem, LLC., and others.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)